Houseblend Article

ASC 326 CECL Accounting for Trade Receivables in NetSuite

Inside this article

Executive Summary

ASC 326 (the Current Expected Credit Losses, or CECL, standard) fundamentally changed U.S. GAAP by requiring forward-looking, lifetime expected credit-loss allowances for most financial assets at amortized cost, including trade receivables and contract assets [1] [2]. Under CECL companies must estimate credit losses over an asset’s entire life using historical loss experience, current conditions, and reasonable forward forecasts [1] [3]. This replaces the old “incurred loss” model, under which bad-debt provisions were recognized only when losses became probable. As a result, companies now recognize allowances on Day 1 of a receivable (or contract) and adjust them each period, yielding generally higher and more volatile allowances and earlier hit to earnings [4] [5].

In practice, CECL adoption led to substantial one-time reserve builds for many companies. For example, a Federal Reserve analysis found that U.S. banks’ total credit‐loss allowances jumped by ≈37% at January 1, 2020 (when large banks first adopted CECL) compared to the old incurred-loss model [6] [5]. The onset of COVID-19 then caused even sharper provisioning: CECL adopters’ allowances grew ~76% in the first half of 2020 (versus 32% for banks still on the incurred model) [6] [5]. Similarly, in the corporate world Jones Lang LaSalle (a large services firm) recorded a one-time $3.6 million increase in its trade receivable allowance (to $71.7M) and established a $1.7 million allowance on contract assets at adoption [7]. These examples illustrate CECL’s front-loading of credit losses: it “does not change the total amount of credit losses that will be ultimately recorded,” but it “shifts when [those losses] hit earnings (earlier under CECL)” [8].

CECL’s broader scope means almost all companies with trade receivables must now implement it. Under ASC 326, all credit exposures measured at amortized cost (e.g. trade accounts and notes receivable, contract assets from ASC 606 revenue, lease receivables, off-balance commitments, etc.) require allowance estimation [9] [3]. Companies must also carefully distinguish between credit losses and revenue concessions (discounts or price concessions): only genuine uncollectibility goes into CECL allowances, whereas concessions reduce revenue [10] [11]. In the NetSuite context, this means implementing new processes and data models on top of the existing “bad‐debt allowances” framework. For example, NetSuite supports an “Allowance for Doubtful Accounts” contra‐asset (netting with gross AR) [12], which under CECL must be determined by a formal expected‐loss calculation rather than by periodic ad-hoc estimates.

This report provides an in-depth analysis of ASC 326 (CECL) for the common case of trade receivables under U.S. GAAP. We begin with background on credit-loss accounting and the shift from the incurred‐loss model to CECL [13] [14]. We then detail CECL’s scope and core requirements, including examples of how allowances jumped on adoption [6] [5]. Next we examine estimation methods and data: companies must pool receivables by risk profile and apply suitable methods (historical loss‐rate, roll‐rate, discounted cash flows, PD×LGD, aging matrices, etc.) to forecast lifetime losses [15] [16]. We also discuss interaction with ASC 606 revenue rules (credit loss vs revenue concessions) [10]. A detailed comparison with IFRS 9’s model highlights differences (IFRS 9 uses staged 12-month vs lifetime rules and prescriptive guards, whereas CECL is a single‐stage lifetime model with more flexibility) [17] [18].

Throughout, we use empirical data and examples (including banks and nonbanks) to quantify CECL’s effects. We incorporate case studies such as the Federal Reserve’s bank analysis [5] and corporate examples [7] [19]. We also address implementation challenges, including how NetSuite users can adapt their systems: e.g. leveraging NetSuite’s multi-book accounting and chart-mapping to handle multiple accounting frameworks [20] [21], and updating workflows for AR aging and provision calculations.Finally, we discuss broader implications for financial reporting and credit management, and possible future developments in credit-loss accounting. All assertions are backed by authoritative sources, ensuring an evidence-based, comprehensive analysis.

Introduction and Background

The Pre-CECL Era: Incurred-Loss Model

Before ASC 326, U.S. GAAP used an “incurred loss” model for credit impairment. Financial assets (like loans and receivables) were carried at amortized cost, and a loss provision was recognized only after a loss event became probable (e.g. delinquency or default) [13] [14]. In practice this meant lifetime losses often hit financial statements “too little, too late.” As the Federal Reserve documented, during the 2007–2009 financial crisis banks had low allowances entering the downturn, then sharply stepped up provisions as defaults materialized, compressing earnings and capital at exactly the worst time [22] [14]. For trade receivables in other industries, many companies adopted a similar approach of writing off receivables or accruing bad debts only after receipt was overdue or subjective impairment was evident. Independent reviews of that era criticized the lack of forward-looking provisioning [13] [14].

In response to these shortcomings, both U.S. and international standard- setters pursued reforms. The IASB issued IFRS 9 (Financial Instruments) in 2014 (effective 2018 for banks), which replaced IAS 39’s incurred-loss model with a three-stage expected-loss model keyed to credit deterioration [23] [17]. In parallel, the FASB began a project that culminated in ASU 2016-13 (ASC 326), “Financial Instruments – Credit Losses,” approved in June 2016 [24] [14]. ASC 326 introduced the Current Expected Credit Losses (CECL) framework, mandating that entities estimate credit losses over the entire remaining contractual life of each financial asset at amortized cost [1] [25]. CECL thus requires forward-looking provisioning: at origination (or adoption) and each reporting date an allowance is recorded for all expected lifetime losses, based on “relevant information about past events, current conditions, and reasonable and supportable forecasts” [1] [3]. This was a dramatic change from the incurred-loss rules, intended to smooth the recognition of credit losses over time and align reserves more closely with evolving risk [1] [26].

Effective Dates and Adoption

FASB phased in CECL by entity type. SEC-registered public companies (excluding smaller reporting companies) had to apply ASC 326 for fiscal years beginning after December 15, 2019 (i.e. January 1, 2020 for calendar-year filers) [27] [28]. All other public business entities (non-SEC public companies) implemented it starting fiscal 2021, and most private/nonprofit entities by fiscal 2023 (ASU 2019-10 postponed their effective date to years after Dec 15, 2022 [27] [28]). Early adoption was permitted for years starting after Dec 15, 2018. (For example, by early 2019 FASB staff noted that some late-adopting banks were already preparing for a 2023 implementation.)

Under the modified retrospective transition allowed by ASC 326, companies did not restate past financials. Instead, at the adoption date they adjusted the opening allowance and retained earnings for the cumulative effect: in effect “as if” CECL had always been in place from origination of existing assets [7] [5]. For example, when Jones Lang LaSalle adopted CECL as of Jan 1, 2020, it increased its trade receivable allowance by $3.6 million (reducing retained earnings) to reflect lifetime losses on pre-existing receivables [7]. A smaller private company noted an increase of only ~$149k in its AR allowances upon transition [7]. In broad terms, CECL typically increased initial reserves relative to the old model (since lifetime losses were recognized up front) [7] [5]. Importantly, however, CECL “does not change the total amount of credit losses that will ultimately be recorded” – it simply shifts the timing of provisioning, so that losses hit earnings earlier rather than after defaults have occurred [8] [5].

Scope of ASC 326 (Trade Receivables, Contract Assets, etc.)

ASC 326 applies to “almost all financial assets measured at amortized cost” [9] [25]. In particular, trade receivables and contract assets (from ASC 606 revenue contracts) are explicitly in scope. FASB confirmed that receivables arising under revenue contracts must be presented at the net amount expected to be collected [29] [18]. In practice, this means that once a customer contract exists, both billed receivables and unbilled contract assets need CECL allowances. For example, ASC 606-10-45-3 directs that contract assets be evaluated for credit losses by reference to ASC 326, just like accounts receivable [29] [18]. Other in-scope items include loans receivable, lease receivables (net investments in leases), held-to-maturity debt securities, reinsurance recoverables, and certain off-balance-sheet exposures (e.g. loan commitments, standby letters of credit, and financial guarantees) [25] [3]. One sector study flatly observes “all entities with balances due (e.g. trade receivables) … are also subject to the new guidance” [30].

By contrast, ASC 326 explicitly excludes assets measured at fair value through earnings (e.g. trading instruments) and those held for sale, as well as available-for-sale debt securities (which remain governed by ASC 320) [9] [31]. Notably, unlike some earlier GAAP allowances (which might be done only at year-end or when triggers occur), CECL requires that every qualifying asset be assessed each period. Any receivable deemed at risk must have an allowance booked contemporaneously – even on day one if needed – rather than waiting for delinquency. In short, under CECL all trade receivables and related contract assets are “on the hook” for credit losses from inception, and management must establish processes to calculate those allowances [29] [3].

Conceptual Shift to Forward-Looking Estimates

Under the CECL model, allowances represent the portion of an asset’s amortized cost that is not expected to be collected [32] [3]. The standard mandates that companies “immediately recognize an allowance for expected losses over the entire life of the loan when the loan is originated” [26] [3]. Thus, from the moment a sale is made on credit, companies must estimate expected lifetime bad debts—taking into account not only historical write-offs, but also current customer conditions and economic forecasts [1] [3]. FASB emphasizes that this estimation is principles-based and broad: companies should use “information about past events and historical experience, current conditions, and reasonable and supportable forecasts” to arrive at a realistic loss estimate [1] [33]. Management judgment is required, but reasonable and supportable inputs must be documented in the financial statements.

This forward-looking stance aligns ASC 326 more closely with IFRS 9’s expected-loss model, but with some key differences (see later section). Importantly, FASB clarified that while forecasts are required, firms “need not forecast unrealistically far beyond a reasonable and supportable horizon” [10] [11]. In practice, companies often determine a forecast period (such as several quarters or a few years) for which they can support economic assumptions, then roll back to historical loss rates beyond that period. The chosen reversion method (e.g. gradually reverting to long-term loss averages) must be reasonable and consistently applied [34] [35].

Once calculated, the allowance is recorded as a contra-asset on the balance sheet (net of gross receivables) [12] [36]. For example, NetSuite’s documentation illustrates that if gross AR is $100,000 and the expected uncollectible portion is $5,000, the balance sheet shows $100,000 in receivables less a $5,000 Allowance for Doubtful Accounts, yielding $95,000 net realizable value [12]. CECL simply raises the bar for determining that $5,000 (and doing so every quarter), but the mechanics of using a contra account and periodically writing off actual defaults remain the same.

Suffice to say, this is a major organizational shift. As one authoritative review notes, moving to CECL “will require major changes to the debt asset holder’s operations, processes and internal controls,” and even significant IT and data upgrades, to capture the needed historical and forecast data for loss modeling [37] [16].

Key Principles of the CECL Model

Lifetime Expected Loss

The cornerstone of ASC 326 is the lifetime loss requirement. Unlike the old model, CECL obligates companies to estimate losses over the full remaining contractual life of a financial asset. [1] [3] For example, if a $10,000 invoice is credited to a customer for one year and that customer is judged at 10% default risk, the lifetime expected loss might be $1,000 (to be recognized immediately), even if no delinquency has yet occurred. Practically, this means that as soon as a receivable exists (or at adoption for existing receivables), an appropriate allowance must be established for expected credit losses on that entire amount over time [1] [36].

FASB stresses that CECL will produce higher allowances at each reporting date compared to the incurred-loss model, because in CECL reserves are built up pre-emptively. The Federal Reserve’s analysis of banks confirms this expectation: because CECL allowances represent lifetime losses (versus the shorter “loss emergence period” under ILM), “CECL generally results in a higher level of allowances at each reporting period” [26] [6]. This front-loaded provisioning inevitably reduces current earnings and capital relative to the old model (although regulators in many jurisdictions provided transitional relief to soften the capital hit [38]).

Allowance Measurement: ASC 326-20 does not mandate a single calculation method. Instead, companies have discretion to use any reasonable approach that incorporates historical experience, current conditions, and forecasts [33] [16]. In practice, companies often divide receivables into segments (pools) of similar credit risk and then apply one of several estimation techniques. Common methods include:

- Roll-Rate (Migration) Method: Using historical transition rates between aging buckets or credit grades. For example, a company might observe that 5% of 60-90-day receivables defaulted historically, and apply that “roll rate” to current balances in that range [39].

- Loss-Rate (Loss-Rate or Proportion) Method: Applying a single loss rate (often historical average loss %) to the balance of a pool [40]. (E.g. if a company historically lost 2% of 30-60-day receivables, it may apply 2% to its current 30-60-day receivables balance.)

- Discounted Cash Flow (DCF) Method: Discounting estimated future shortfalls in cash flows (e.g. where individual receivables are significant), reflecting a time value of money [41] [35]. This is often only used for large or unusual receivables.

- Probability of Default (PD × LGD): Estimating the probability that a customer will default and the loss‐given‐default on each exposure, then multiplying by exposure to get an expected loss [42]. This approach is common in banking risk models.

- Aging-Matrix or Provision Matrix: Assigning fixed loss rates to buckets of receivables by age (e.g. 0–30 days, 31–60 days, etc.) – effectively a more structured roll-rate method [19] [43]. Companies often start with past write-offs by aging bucket and adjust rates for forecasts.

- Regression or Predictive Models: Some companies may use statistical models (e.g. regression against macroeconomic indicators) to forecast losses in each pool.

These methods (and hybrids or other techniques) are all permitted under CECL [44] [16]. The choice depends on data availability, accounting policies, and the nature of the receivables portfolio. Baker Tilly notes that many nonfinancial companies will continue using methods similar to those they used under the old model (such as loss-rate or vintage analysis), but applied over the lifetime of receivables [43]. Whatever method is used, the result is a single allowance balance that reduces the gross receivables to the “net amount expected to be collected” [32] [36].

Reasonable and Supportable Forecasts

ASC 326-20 explicitly requires incorporating forecast information into the loss estimate, but with a key caveat: companies must use forecasts to the extent that they are reasonable and supportable, but need not predict indefinitely into the future [10] [11]. In practice, this has led to a two-phase approach. First, an entity sets a forecast horizon (for example, 1–3 years) over which it collects reliable economic or industry outlooks (GDP, credit spreads, unemployment, etc.). The company adjusts loss rates within this horizon based on these forward assumptions. Beyond the forecast horizon, CECL permits a “reversion method”: reverting to long-term historical loss rates (or gradually converging to a steady state) since future forecasts are too uncertain [10] [34].

For instance, a company might know that delinquency rates are likely to rise over the next two years given current economic projections, and increase its loss rates accordingly. But if it cannot credibly forecast beyond, say, two years, it may assume loss rates beyond that simply follow the long-run average. The FASB guidance leaves this judgement to management, provided it is “reasonable and consistently applied” [34] [45]. Notably, CECL is more permissive than IFRS 9 in this regard: IFRS 9 generally expects entities to consider multiple scenarios and probability-weight them, whereas CECL practice often allows using the single “most likely” scenario or a simple reversion [45].

In all cases, the historical component of the model must be relevant. Companies typically base their baseline loss assumptions on their own write-off history under comparable economic conditions, then adjust for the current/future outlook [33] [16]. The forecasts themselves may be qualitative or quantitative, as long as they are documented. For example, a NetSuite user might incorporate customer credit ratings, economic forecasts, and segment-level models into a spreadsheet or BI tool, and then use that output to set the quarterly allowance that is recorded via a Journal Entry in NetSuite. Crucially, CECL requires companies to justify how current conditions or forecast changes differ from the past, and to disclose key assumptions [33] [46].

Impact on Reporting (AR and Contract Assets)

The practical impact on the balance sheet and income statement is direct. Under CECL, the Allowance for Credit Losses (often labeled Allowance for Doubtful Accounts) is treated as a contra-asset reducing trade receivables [12] [36]. The corresponding expense (Provision for Credit Losses) hits the income statement in real time. Over time, as specific receivables are written off (with charge to the allowance), the net receivable balance should approximate the expected collectible amount. As noted earlier, a defining change is that companies will often carry a non-zero allowance on receivables that otherwise appear “current.” For instance, a NetSuite account aged 0–30 days might still have an allowance if historical default rates or forecasts warrant it.

Because contract assets (unbilled revenue under ASC 606) are effectively customer payments owed, quickly receivable, FASB requires them to be treated like receivables for CECL. Thus, a contract asset balance must also be net of an expected-credit-loss allowance. In practice, this means collecting information on unbilled work-in-process and forecasting a recoverable percentage (often paralleling the customer’s collectibility) [29] [18]. This interplay with ASC 606 is important: only bona fide credit risk affects CECL allowances, whereas any genuine price concession (discount or refund) would instead reduce the transaction price under ASC 606, not increase CECL reserves [10] [47].

Comparison with IFRS 9 (Global Perspective)

While this report focuses on U.S. GAAP, it is worth highlighting key contrasts with IFRS 9’s expected-loss model for a global perspective. Both frameworks move away from the incurred-loss regime, but they differ structurally. IFRS 9 uses a three-stage model: Stage 1 assets (no significant deterioration) hold a 12-month ECL; Stage 2 (significant increase in credit risk) and Stage 3 (credit-impaired) carry lifetime ECL [17]. CECL, by contrast, has no staging: all assets, regardless of credit status, require a lifetime‐loss allowance from the outset [17] [18]. In effect, CECL “front-loads” loss provisioning more aggressively.

Other differences include:

-

Loss Horizon: As noted, IFRS 9 only requires limited (12-month) ECL for high-quality assets, whereas CECL always uses lifetime. This tends to give CECL higher provisions for performing assets. (On the other hand, IFRS 9 lets Stage 1 companies defer some losses, potentially smoothing earnings when credit risk remains low.) [17].

-

Simplified Approach: IFRS 9 permits (optionally) a simplified approach for trade receivables: bypassing staging altogether and taking lifetime ECL by default [48]. Ironically, this aligns with CECL’s requirement. Many companies may find that adopting CECL means treating all receivables effectively under IFRS-9’s simplified approach.

-

Forecasting Approach: IFRS 9 emphasizes probability-weighted scenarios and requires fair-value discounting of cash flows when calculating ECL [35] [45]. CECL in practice often allows point-in-time or most-likely forecasts, and does not require present-value discounting (companies can use simple loss percentages or aging matrices without explicit discount factors) [35] [45].

-

Disclosures and Capital: IFRS 9 and ASC 326 carry different disclosure requirements (IFRS 7 vs ASC 326-20), but both seek transparency on how allowances are determined. Note that U.S. regulators eased CECL’s capital impact at adoption (e.g. allowing banks to phase in the reserve increase in Common Equity Tier 1 capital [38]), whereas IFRS 9 was implemented without such relief by many international regulators.

In summary, both models aim to incorporate forward-looking information, but CECL’s single-stage, lifetime approach is more aggressive than the staged IFRS 9 model. Companies reporting under both standards should be mindful of these structural differences and ensure their NetSuite multi-book or parallel-system reporting captures the required treatments in each framework [20] [21].

Estimation Methods and Data Gathering

Implementing CECL for trade receivables demands robust data analysis. Companies must gather historical loss data and current receivable balances at sufficient granularity. Typically, receivables are segmented into homogeneous pools (e.g. by customer type, geography, product line, or credit score) [49] [16]. Each pool should consist of assets with similar credit risk characteristics; assets with demonstrably different risk profiles are often evaluated on a standalone basis [49] [50].

Once pools are defined, firms apply estimation techniques suitable for the available data:

-

Loss-Rate / Aging-Matrix: Often, companies start with an aging schedule of receivables. Historical write-off rates by bucket can yield initial loss-rates. CECL then adjusts these rates for current conditions (e.g. tightening economy might increase long-past-due loss rates) and for forecasts. [19] [43]. For example, in a BDO illustrative case, existing allowances under an incurred model were based on fixed loss rates by age (e.g. 6% for 1–30 days, 28% for 31–60 days, etc.), summing to about $4.83M [19]. Under CECL, those rates were modestly increased (reflecting forward-looking factors) to produce a new allowance of $5.1875M [19] (Table 1). This example shows how even small changes in each bucket’s rate can materially grow the overall reserve, consistent with CECL’s lifetime focus.

-

Roll-Rate (Migration) Models: A more dynamic approach uses historical migration matrices. If data exist on how past receivables aged and defaulted (e.g. the percentage of 90-120-day balances that eventually went bad), one can project current balances through a “roll” to default. This inherently integrates aging with outcome probabilities [51].

-

Discounted Cash Flow: For significant accounts (or when detailed forecasts are available), companies may project expected cash flows (including recoveries and note terms) and discount them to present value. In principle this provides a precise lifetime loss estimate. However, it requires estimating timing of defaults, which can be difficult for ordinary trade receivables. It is more common for large loans than day-to-day AR [41].

-

Probability Models (PD×LGD): Credit-risk models from banking (estimating borrower default probability and loss severity) can be adapted to customer portfolios. This requires statistical data on customer behavior, often unavailable to small businesses, but some mid-sized firms deploy simple credit scores or external rating equivalents.

-

Statistical / Machine-Learning Methods: Some companies use regression or econometric models linking receivable losses to macroeconomic indicators. By stress-testing different economic scenarios, they derive an expected percentage loss. Such models were not widely used prior to CECL except in large financial institutions, but they are permitted [43].

Regardless of the method, predictive reasonableness is key. Entities must ensure historical data are adjusted for changing conditions. For example, if a firm’s receivables mostly come from a new market and its historical losses reflect an older, different market, the old rates must be recalibrated materially. Baker Tilly emphasizes that allowances “should reflect any risk of loss, even if that risk is remote” and that assessments compare past vs current/future conditions [31]. The standard allows considerable latitude, but demands disclosure of how management arrived at its loss projections [46].

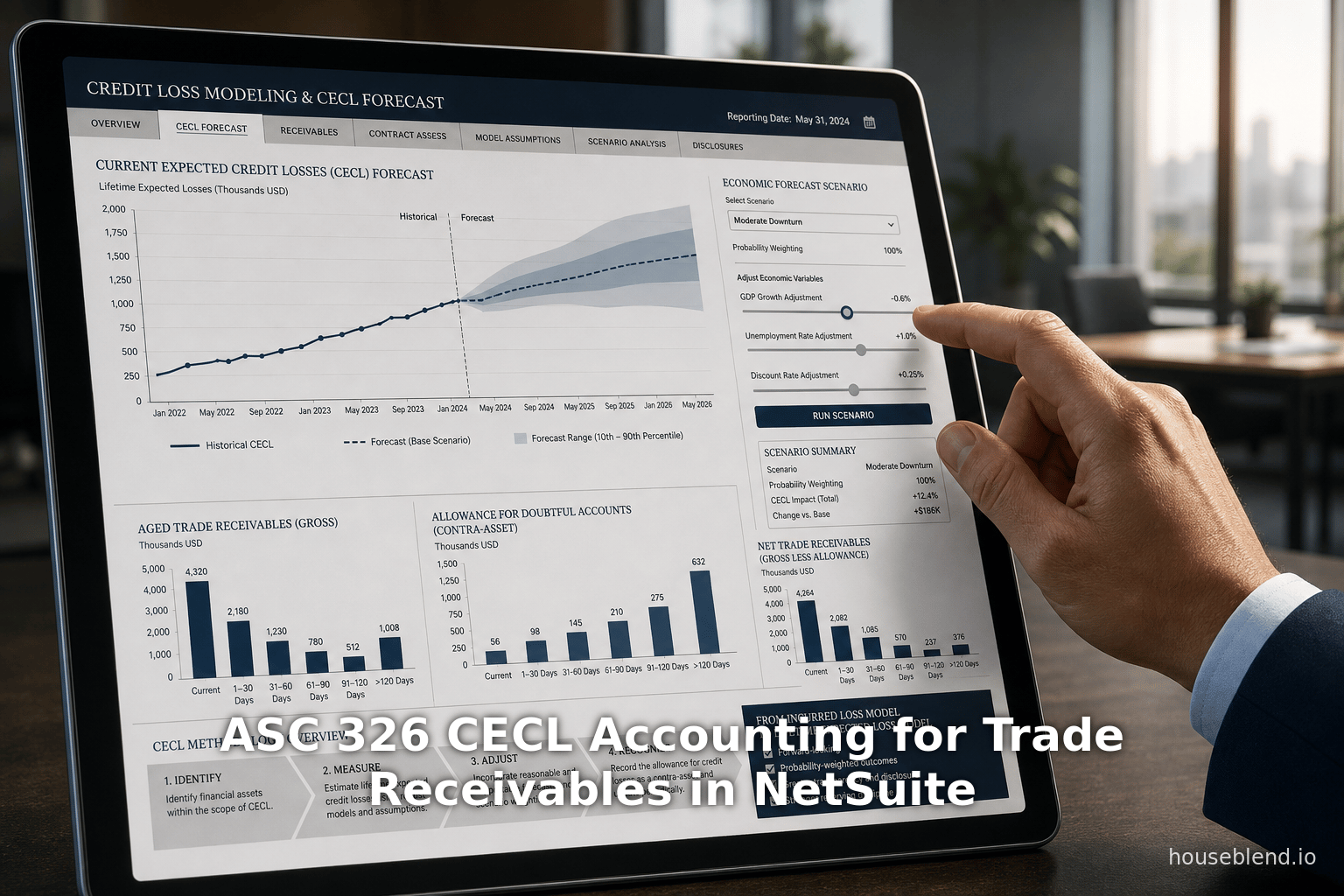

In practice, many NetSuite adopters will use external tools or spreadsheets to perform the CECL calculations. NetSuite itself does not automatically compute forward-looking allowances (beyond its built-in allowance account). Instead, finance teams might export AR data via saved searches, apply the chosen estimation model in Excel or BI software, then book the resulting allowance via adjusting journal entries. Key fields (like customer credit score, AR aging, and write-off history) should be captured in NetSuite to feed this analysis. As an example of data reporting, NetSuite’s Financial Reporting consultants note that it’s possible to run ECL reports by legal entity and IFRS stage (in IFRS modules), displaying allowances, provisions and exposures [52]; even if primarily IFRS-oriented, such reporting canvases illustrate how the data can be structured.

Throughout, companies must also embed controls. Auditors and regulators expect CECL approaches to be vetted by risk teams. Firms often involve multiple departments – accounting, credit, treasury, and economics – in making assumptions [47] [37]. For instance, the RevenueHub analysis stresses that developing an expected-loss forecast “may require input and collaboration from multiple departments” (e.g. finance, SRM, sales) [47]. Systematically documenting models and regularly back-testing them (comparing past predictions to outcomes) are now essential parts of the AR process.

Interplay with Revenue Recognition (ASC 606)

Because CECL now touches trade receivables and contract assets, companies must carefully coordinate CECL with ASC 606 revenue rules. Under ASC 606, a contract is recognized only if collectibility is probable; once a contract exists, cash or receivable is recorded. CECL’s allowance is distinct from any revenue adjustment: CECL is about credit risk, ASC 606 is about price/risk allocation. In concrete terms, if a customer fails to pay part of an invoice, management must judge whether this shortfall arises from credit impairment or a contractual price concession. Only true credit losses (e.g. customer bankruptcy) justify using the CECL allowance; a negotiated discount or settlement would instead be accounted as a change in transaction price under ASC 606 [10] [47]. (FASB provides guidance that entities “need to distinguish credit losses from revenue concessions” in applying these standards [11].)

For practitioners, the practical implication is that gross revenue should not be artificially eroded by expected unearned discounts – only actual credit losses hit the bad-debt reserve. NetSuite users might, for example, continue using credit memos or write-off entries to handle concessions, while isolating true defaults in the allowance calculation. Adequate data collection (e.g. tracking disputes vs delinquencies) is needed so that genuine credit risk can be modeled separately from contractual pricing adjustments [47] [10].

Implementing CECL in NetSuite

For companies running Oracle NetSuite, embracing CECL may require both accounting and system changes. NetSuite does not have a one-click “CECL” module, so users must adapt existing functionality and processes. Key considerations include:

-

Accounts and Chart of Accounts Mapping: Create a dedicated contra-asset account (e.g. “Allowance for Credit Losses – GAAP”) to record the ASC 326 allowance. (NetSuite’s standard “Allowance for Doubtful Accounts” account can be repurposed or replaced.) If a business also reports under IFRS, it should use NetSuite’s Multi-Book Accounting (OneWorld) to maintain parallel ledgers: one for U.S. GAAP (with ASC 326 CECL treatment) and one for IFRS (with IFRS 9 treatment). NetSuite allows different GL mappings per book [21]. For example, a transaction (like writing off a receivable) could post to different allowance accounts in each book (“Allowance–GAAP” vs “Allowance–IFRS”) without duplicating entries. Such configuration ensures that CECL adjustments flow only into the GAAP book. If Multi-Book is not used (e.g. the company only reports GAAP), then a single set of accounts is fine.

-

Processes for Data Collection: NetSuite’s AR Aging reports and customer analytics should be leveraged. Set up saved searches or reports that segment receivables by customer, aging, credit rating, location, etc. These are the inputs for CECL models. If necessary, add custom fields (e.g. on Customer records) to track a customer’s internal credit score or “CECL pool” identifier. Many companies also build intercompany or consolidated AR pools (using the legal-entity hierarchy functionality [53]) so that CECL can be applied at the appropriate aggregation level.

-

Journal Entries and Workpapers: In practice, most NetSuite users will perform the CECL calculation outside (in spreadsheets or specialized software) and then post the allowance via a Journal Entry each period. This entry debits Bad Debt Expense (or a provision account) and credits the Allowance account. To support auditability, companies should save the calculation worksheets, forecasts, and assumptions that underlie these entries. NetSuite’s attaching of documents to transactions or its Excel add-in can help link the data. Balance Sheet and Income Statement impact (lower Accounts Receivable and higher expense) should be reviewed for reasonableness against collection experience.

-

Reporting and Disclosures: Firms should update their financial statements notes. NetSuite’s financial close process (with entity-specific reports) must now include commentary on CECL. While Oracle does provide some IFRS 9 reporting canvases (e.g. expected credit loss reports by entity under IFRS 9 [53]), those can also inspire CECL disclosures. For example, companies should report a roll-forward of the Allowance for Credit Losses each period (additions, write-offs, recoveries, foreign exchange effects, etc.). NetSuite’s Saved Searches and consolidated financial reports can generate the numeric data; formatting as required for SEC/XBRL disclosure is a separate step.

-

Internal Controls and Audit Trails: Operations must now ensure the CECL processes are controlled. This means segregation of duties between those estimating allowances and those recording them. NetSuite’s Audit Trail feature will record who made the journal entries. Additionally, companies may implement checklist-style controls (for example, verifying that forecast inputs were updated, or comparing predicted losses to actual charge-offs) at each close.

-

Integration with External Data: In some cases, companies may pull in external economic data (e.g. GDP forecasts or industry sales trends) to justify CECL assumptions. While NetSuite does not directly provide such data, SuiteScript or integration tools (like SuiteTalk) could be used to import key metrics from third-party APIs or spreadsheets into custom records. This is more typical for large companies; smaller firms might simply annotate their models with references (e.g. to published economic forecasts) without embedding them in NetSuite.

In short, CECL implementation in NetSuite is largely a process and policy change, supported by configuration (accounts, reports) rather than a new feature. NetSuite’s flexibility (saved searches, multi-book ledger, dashboard reports) can accommodate CECL if properly set up. As one NetSuite site notes in the context of IFRS 9, “NetSuite’s Multi-Book Accounting can facilitate running parallel ledgers (e.g. one for local GAAP, one for IFRS)” [20]. By analogy, a NetSuite OneWorld user could designate one book as “ASC 326 (GAAP)” and another as “IFRS 9” when needed, ensuring each framework’s rules are applied in the appropriate ledger [54] [21].

Case Studies and Examples

Banking Sector (Fed Analysis): The most comprehensive empirical analysis comes from the Federal Reserve, which compared U.S. banks that adopted CECL on Jan 1, 2020 against those that remained on the incurred-loss model (ILM). The findings were striking: under the relatively benign conditions of late-2019, the mere switch to CECL caused CECL adopters’ aggregate allowances to jump by 37% on January 1, 2020 [5]. In other words, if banks were comparing their reserves “under CECL” vs “what ILM would have produced,” CECL yielded 37% more reserves immediately at adoption. During the COVID downturn this gap widened: CECL-adopting banks increased loss provisions much more rapidly, as CECL rules forced them to incorporate the unfolding stress. By mid-2020, allowances at CECL banks had surged 76% compared to year-end 2019, whereas non-adopters’ allowances (still following ILM) rose only 32% [5]. Importantly, as the economic outlook improved, CECL banks began to release their excess provisions (allowances gradually declined), whereas non-adopters peaked later. By mid-2021 the allowance gap had re-converged to roughly the original 37% difference. The Fed concluded that CECL made provisioning more timely and responsive to forward conditions, though with greater volatility [5] [38]. Regulators also noted that CECL’s overall impact on regulatory capital was largely neutralized by transition relief (e.g. allowing reserves to be added back to Tier 1 capital) [38].

Commercial Example (JLL): A practical non-bank example is provided by Jones Lang LaSalle’s (JLL’s) SEC filings upon CECL adoption [7]. JLL reported that applying ASC 326 on Jan 1, 2020 required re-evaluating its reserves for receivables and contract assets. The one-time effect was a $3.6 million increase in the allowance on trade receivables (boosting it from $68.1M to $71.7M) and a $1.7 million allowance on contract assets. Taken together, these adjustments reduced JLL’s opening retained earnings by $14.9M [7]. This concrete case shows how, even for a service firm outside finance, CECL can meaningfully raise reserves on receivables that might previously have been unreserved. Another company (not named, but described as a smaller private firm) added about $149,000 to its AR allowance at transition [7], illustrating that the effect scales with portfolio size and risk profile.

Illustrative Roll-Forward (BDO/CPE Example): A hypothetical example from a professional accounting publication (adapted by BDO) illustrates how an aging-matrix approach yields higher reserves under CECL. In the pre-CECL scenario, the company had $40 million of trade receivables aged across buckets, with fixed loss rates (e.g. 6% on 0–30 days, 28% on 31–60 days, etc.) giving an existing allowance of $4.83M [19]. Under CECL, those loss rates were slightly adjusted upward (reflecting lifetime expectations) – for instance, raising the 0% on current receivables to 1.50% – and applied to the same amortized costs to compute a new allowance of $5.1875M [19]. Table 1 (below) summarizes this illustrative roll-forward:

Table 1. Example: Moving from an incurred-loss allowance to CECL (in $). Based on a hypothetical aging schedule. Source: BDO (2023) [19].

| Aging Category | Amortized Cost of Receivables | Existing Loss Rate (%) | Existing Allowance | Adjusted CECL Loss Rate (%) | Allowance under CECL |

|---|---|---|---|---|---|

| Current (0–30 days) | $19,000,000 | 0.00% | $0 | 1.50% | $285,000 |

| 1–30 days | $11,000,000 | 6.00% | $660,000 | 6.09% | $669,900 |

| 31–60 days | $6,000,000 | 28.00% | $1,680,000 | 28.42% | $1,705,200 |

| 61–90 days | $3,000,000 | 54.00% | $1,620,000 | 54.81% | $1,644,300 |

| Over 90 days | $1,000,000 | 87.00% | $870,000 | 88.31% | $883,100 |

| Total | – | – | $4,830,000 | – | $5,187,500 |

This example shows that small rate increases (e.g. from 6.00% to 6.09%) can noticeably raise the overall allowance (here by $357,500 or ~7.4%) [19]. In real practice, the adjustments might be larger if management’s forecasts turn negative.

Other Industries / Non-Financials: Although banks dominate the CECL discussion, a growing body of advice applies to manufacturers, retailers, and other non-banks. For instance, Baker Tilly (a CPA firm) notes that nonfinancial companies must also adopt CECL for any credit exposures. Its guidance reiterates that receivables (and related items like lease receivables or guarantees) must be measured at “net amount expected to be collected,” and that the model is principles-based [55] [31]. While no specific case data is given, such industry accounts emphasize that firms can and should use versions of their existing impairment techniques (loss-rate, vintage analysis, etc.) under the new standard [16].

In summary, both empirical studies and anecdotal cases show that CECL tends to increase reserve levels and move loss recognition earlier across the credit cycle [5] [7]. For NetSuite users, this means planning for higher periodic bad-debt expenses and larger allowance balances than under old GAAP, along with rigorous explanation of how those numbers were derived.

Implications and Future Directions

CECL’s adoption has broad implications for financial reporting, credit management, and system design. We highlight several key themes and look ahead:

-

Earnings and Capital Volatility: By front-loading losses, CECL can increase short-term volatility in profitability (especially in downturns) [5] [8]. Companies that sell on net terms may see credit-loss expense spike even during healthy revenue growth. Many stakeholders believe, however, that this volatility is more transparent and economic (good in bad times, then easing off) than the old approach. Regulators in the U.S. signaled their approval by providing capital transition relief for banks [38]; future guidance from FASB or regulatory bodies may similarly refine disclosures or allowances if needed. For NetSuite users, the implication is that the allowance and bad-debt expense accounts will become more dynamic drivers of reported results than before; planning and budgeting processes should account for this.

-

Risk Management Integration: CECL forces tighter integration between accounting and credit management. Sales and credit teams need to communicate their expectations about customer payment behavior, and IT systems (like NetSuite) must capture credit metrics. Governance of the CECL model becomes a board-level issue in many companies. Over time we expect to see credit scorecards, scenario analysis, and even machine-learning models become routine in closed-loop with accounting. NetSuite might in the future offer more built-in analytics or APIs to risk systems, reflecting this trend.

-

Comparability and Convergence: The coexistence of ASC 326 and IFRS 9 means that many multinational groups will continue mapping between models. Analysts may question differences in allowance balances that arise solely from methodological dissimilarities [56] [57]. Over time, there may be calls for greater convergence or at least clearer reconciliation requirements. So far, FASB has not signaled major moves to change CECL’s structure, but it has made minor technical updates (ASU 2019-04 clarifications, CECL implementation guides). On the international front, IFRS 9 remains the global standard outside the U.S., so companies frequently use NetSuite’s multi-book capability to run both models in parallel [20] [21] and must present duplicate credit-loss disclosures in their consolidated reports. This dual compliance will likely continue for the foreseeable future.

-

Data and Technology Evolution: CECL’s data demands have already spurred improvements in financial systems. Firms that were manually tracking receivable aging now often automate the collection of key metrics. Future directions may include integration of macroeconomic data feeds, more sophisticated BI tools, and perhaps AI-driven forecast models. For example, while today many NetSuite users export to Excel for CECL, we may see dedicated SuiteApps or third-party add-ons that provide more automated ECL modeling within the ERP. In the meantime, companies should continuously refine their models with new data; for instance, the experience of the COVID crisis has updated the way many calibrate “reasonable and supportable” forecasts.

-

Disclosure and Investor Communication: With CECL, public companies have added disclosure requirements: roll-forwards of the allowance, qualitative discussion of model changes, and explanation of significant assumptions [46]. Future SEC guidance may require standard formats for these disclosures (some guidance is already in ASC 326 and SEC staff Q&As). CFOs must ensure that NetSuite financial close cycles incorporate these disclosures. In IFRS cases, IFRS 7 and IFRS 9 disclosure amendments (effective 2026) will further expand disclosure around ECL methods, though those mostly target equity and financial instrument classification (not trade receivables specifically) [58].

-

NetSuite road map: While NetSuite itself has not publicly announced a built-in CECL module, Oracle’s broader financial software suite (Oracle Cloud ERP, Oracle FCCS, etc.) may add CECL support that could be mirrored in NetSuite over time. In the meantime, NetSuite organizations should leverage features like custom records, saved searches, and advanced intercompany to capture and reconcile credit-loss data. The Houseblend IFRS guide notes that careful NetSuite setup (enabling multi-book, configuring ledger mappings, etc.) can address complex instrument accounting [54] [21]. By analogy, CECL impacts can be managed with similar attention to system design.

In conclusion, ASC 326 CECL represents a major overhaul of credit-loss accounting for trade receivables under US GAAP. It requires technical changes (modeling and reserves) and strategic changes (closer credit monitoring). For NetSuite users, thorough planning and system configuration are essential. The advantages of earlier loss recognition (less “surprise” losses) must be balanced against the need for more robust data and controls. Over time, as CECL matures and possibly evolves, companies should closely monitor FASB and industry guidance. For now, CECL is the new normal: trade receivables will be tracked and reported at their net collectible value by default [55] [31], and NetSuite implementations must reflect this paradigm to ensure accurate, GAAP-compliant financial statements.

Conclusion: Under ASC 326, allowances for credit losses are now a planned, data-driven element of NetSuite financials, not just an afterthought. Effective implementation will give stakeholders more timely insight into credit risk, albeit with greater modeling complexity. By systematically building expected losses into their accounts receivable processes (leveraging NetSuite’s reporting and accounting features as described), companies can meet the spirit and letter of CECL, improving the reliability of their receivables valuation and overall financial reporting [1] [34].

External Sources (58)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.