ASC 606 Revenue Recognition for SaaS: NetSuite Guide

Executive Summary

The adoption of ASC 606 / IFRS 15 (“Revenue from Contracts with Customers”) has profoundly transformed revenue recognition for cloud/SaaS businesses. The new standard replaces industry‐specific rules with a single five‐step model (identify the contract; identify performance obligations; determine the transaction price; allocate price; recognize revenue) [1]. For SaaS firms – often selling subscriptions, usage-based services, and consulting in bundles – this means unbundling contracts and allocating prices by standalone selling price (SSP) rather than relying on legacy proxies. The net effect is often slower, more granular recognition (e.g. spreading setup fees and usage charges over contract life instead of expensing immediately) [2] [3].

Enterprises must now manage myriad scenarios: multi-year contracts with price escalators, usage meters and overages, bundled professional services, renewal options, etc. Deloitte notes that SaaS companies face “significant judgments” in estimating SSPs, identifying distinct promises (performance obligations), forecasting variable consideration, and accounting for customer options [4]. In practice, growing SaaS companies often strain manual processes. In one survey, recognition processes that once took five days stretched to weeks because of complex SSP allocation, contract modifications, variable usage calculations, and audit evidence needs [5].

NetSuite provides built-in tools to automate ASC 606 compliance. Its SuiteBilling and Advanced Revenue Management (ARM) modules let companies configure allocation rules, recognition templates (straight-line, event-based, usage, etc.), and billing triggers that auto-generate detailed revenue schedules and journal entries. For example, SuiteBilling generates “revenue elements” for each subscription line, which ARM then aggregates into revenue arrangements [6]. A careful NetSuite implementation requires setting up SSP price lists, mapping deferred/unbilled accounts, defining recognition rules per item (e.g. fixed vs usage), and (for global firms) enabling Multi-Book Accounting for parallel GAAP/IFRS reporting [7] [8].

This guide reviews the history and rationale of ASC 606, surveys SaaS-specific issues (with case examples), and provides a step-by-step roadmap for SaaS companies implementing ASC 606 in NetSuite. We draw on authoritative sources (IFRS Foundation, FASB, Deloitte, PwC, KPMG, etc.) and include data and real-world examples. Key takeaways: SaaS firms should rigorously identify all promised services, allocate consideration by fair-value SSPs, and leverage NetSuite ARM’s rule-based engine to automate recognition. We also discuss organizational impacts (finance-IT alignment), month-end close processes in NetSuite, and emerging trends ( AI-driven forecasting, built-in SaaS KPIs).

1. Introduction and Background

Revenue recognition fundamentally affects a company’s reported sales, profits, and cash flow. Historically, U.S. GAAP applied ASC 605 (“Revenue Recognition”) with detailed software guidance (SOP 97-2, updated by SAB 101/104, ASC 985-605) that often required vendor‐specific evidence (VSOE) or complex residual methods for software/SaaS deals. IFRS used IAS 18 and IAS 11 with only general principles. These divergent, rule-based approaches led to inconsistent treatment, especially for bundled contracts (software subscription + services + maintenance).

In May 2014, the FASB and IASB jointly issued ASC 606 and IFRS 15 to unify revenue accounting under a common conceptual model. IFRS 15 and ASC 606 became effective for annual periods beginning Jan 1, 2018 for public companies (later for private) [9] [10]. The new standards aim to recognize revenue consistently by depicting the transfer of promised goods or services to the customer (the “satisfied” performance obligations) in an amount reflecting consideration expected [11] [12]. This five-step framework is applied identically in IFRS and US GAAP (differences are few and largely limited to disclosure or niche rules) [1] [13]. For SaaS vendors – many of whom were already using “principles-based” approaches via SAB 13 – ASC 606/IFRS 15 formalized and extended practices such as deferring installation fees and using percentage-of-completion for services.

Table 1 compares traditional revenue accounting to ASC 606/IFRS 15 for SaaS context:

| Aspect | Prior GAAP (ASC 605/IAS 18) | ASC 606 / IFRS 15 (New Model) |

|---|---|---|

| Standardization | Industry-specific rules (software SOPs, SABs); VSOE-driven for multi-element contracts [14]. | Single five-step model for all industries [11]. Common criteria apply regardless of contract contents. |

| Revenue Model (Core Principle) | Recognize revenue when “earned” based on largely historical rules. | Recognize revenue as promised goods/services are transferred to customer, reflecting expected consideration [1] [12]. |

| Multiple Deliverables | Often required vendor-specific evidence or residual to allocate between software and services. | Must explicitly identify separate performance obligations; allocate the transaction price by stand-alone selling price (SSP) [15] [7] (e.g., VSOE no longer sole basis[4]). |

| Timing (Subscription Fees) | Often recognized straight‐line over term (if not contingent). Multi-year escalators sometimes triggered “contingent revenue” deferrals. | Still generally ratable, but removes “contingent cap” (escalators allow recognition of all earned invoices via a contract asset) [16]. Renewal options may create material rights (additional obligations) if economically favorable [17]. |

| Installation/Setup Fees | If not standalone, typically deferred and amortized over customer life [2] (beyond initial contract). | Treated as part of the contract; allocated to performance obligations (usually subscription) and recognized with those obligations [3]. Setup fees no longer “prepaid” customer payment. |

| Usage-based Fees (Variable) | Recognized as delivered if in scope of old guidance [18]; often requiring tracking per meter. | Treated as variable consideration under new model; recognized when usage occurs or obligation is satisfied (subject to estimation and constraint rules) [18] [19]. |

| Contract Modifications | Accounted as new contracts or adjustments based on criteria; often ad-hoc practice. | Revised contracts are re-evaluated to identify new/remaining obligations; changes in price/performance lead to adjustments in timing/amount of revenue using the five-step model. |

| Costs to Obtain a Contract | Often expensed (SOP 97-2 allowed deferral in some cases). | Certain incremental costs (commissions) must be capitalized and amortized if criteria met (no more expensing by default) [20]. |

Table 1: Traditional vs. ASC 606 revenue recognition in SaaS contexts (sources: IFRS/ASC standards and commentary [1] [2] [3]).

The transition to ASC 606 required many SaaS firms to re-write their revenue policies. For example, contingent revenue caps under old GAAP (which had prevented recognizing future escalations) were eliminated. Under legacy rules, a 3-year contract with increasing fees ($10k, $12k, $14k) could only recognize $10k in year 1 (the lower of earned vs billed) [16], deferring the rest. ASC 606 requires $12k be recognized in year 1 (with $10k cash and $2k as a contract asset) because all performance obligations are satisfied [21]. Similarly, implied setup fees or large implementation services that were once amortized over many years must now be allocated into current contract obligations [3], generally accelerating recognition for the vendor.

In summary, ASC 606/IFRS 15 imposes a more granular, principled approach. As Deloitte notes, SaaS companies must identify all promised goods/services and allocate consideration by fair value (using VSOE, Estimated Selling Price, etc.) [7] [22]. This often leads to recognizing some revenue (contract assets) sooner than before, and some later, depending on whether obligations are distinct or bundled. These changes also affect forecasts and KPIs: for example, shortening revenue cycles can make bookings and cash seem out of sync without reconciling contract assets/liabilities. In total, industry surveys found many SaaS firms spent substantial effort on implementation: PwC notes that moving from spreadsheets to automated systems is often essential for scaling, and that the judgments (usage metering, renewal options, revenue deferrals) directly impact valuation and investor communication [19] [5].

2. ASC 606 / IFRS 15 Overview

2.1 The Five-Step Model

Both ASC 606 and IFRS 15 require applying the same five-step recognition model [1] [7]:

- Identify the contract with a customer. ASC 606/IFRS 15 define a contract as an agreement (oral or written) that creates enforceable rights.

- Identify the performance obligations in the contract. Each promise to transfer a distinct good or service (or bundle) is a performance obligation (POB) [1].

- Determine the transaction price. The total consideration the entity expects, including fixed and variable amounts (with constraint for uncertain/variable consideration)$_$.

- Allocate the transaction price to each POB. Allocation is done by relative SSP. Under ASC 606, the vendor no longer needs VSOE for every element – if no VSOE exists, it can use Best Estimate or other methods, so long as it is reasonable [7].

- Recognize revenue when/as each POB is satisfied (i.e. the customer obtains control). This may be over time (e.g. straight-line subscription) or at a point in time (e.g. a one-off service delivery).

The IFRS Foundation summarizes this succinctly: “an entity recognizes revenue to depict the transfer of promised goods or services … in an amount that reflects the consideration to which the entity expects to be entitled” [11]. Notably, ASC 606 eliminated provisions like the “contingent revenue” cap and vendor-specific residual methods. Fixed and variable amounts are treated under the same umbrella: future price increases, renewals, customer options, and usage all fall under variable-consideration guidance. For SaaS, this unified model means subscription fees, services, usage, and support must all be carefully tracked as separate or combined POBs.

2.2 Differences Between ASC 606 and IFRS 15

The two standards are substantially converged, but minor differences remain [13] [22]. KPMG notes both emphasize the five-step model and consideration concept, but IFRS allows certain elections not permitted in U.S. GAAP. For instance, IFRS 15 has no expedient for shipping and handling after control is transferred (unlike a US policy election) [23]. IFRS also uses slightly different terminology (“performance obligations” vs “deliverables”) and requires a higher collectibility threshold. For SaaS specifically, one key difference is that IFRS 15 tends to regard cloud services as services (since customers don’t control the underlying software as an asset), whereas ASC 985-605 (old GAAP) often looked for software license evidence [24]. In practice today, ASC 606 and IFRS 15 yield very similar outcomes for cloud subscriptions, but companies reporting under both may use NetSuite’s Multi-Book capability to manage any divergent local rules (see Section 5.4) [8].

Deloitte observes that eliminating VSOE is a major change for U.S. SaaS accountants [22]. Under ASC 605, a vendor needed VSOE of fair value to separate support/maintenance from license, for example. Now ASC 606 allows SSP to be estimated by market data or other methods. However, new challenges arise: determining SSPs (especially for bundled cloud deals), deciding whether hosting vs implementation are distinct, and estimating variable fees. Deloitte highlights some common SaaS challenges under 606: capturing usage-based charges, handling customer termination clauses, and capitalizing commissions [22]. These areas are judgmental and often require cross-functional input from finance, sales, and legal.

2.3 SaaS-Specific Revenue Recognition Issues

SaaS firms face several nuances under ASC 606; these are well-documented in industry publications [15] [19] [4]. Key points include:

-

Subscription fees (time-based access): Typically recognized ratably over the subscription term. Under legacy GAAP, SaaS often did this already. ASC 606 formalizes that pattern and removes concepts like “contingent revenue.” For example, under old GAAP a 3-year escalating subscription (Year1 $10k, Year2 $12k, Year3 $14k) was capped at $10k in year1 [16]. ASC 606 removes that cap, so $12k is recognized in year1 ($10k cash plus a $2k contract asset for future invoice) [21]. In effect, recognition speeds up (the customer has “earned” that revenue even if contractually invoicing later) [21].

-

Implementation and setup fees: Up-front fees for installation or onboarding are common in SaaS sales. Under prior practice, these were often deferred over the “customer life” (e.g. 3–5 years) [2]. ASC 606 now treats those fees as part of the contract consideration. They must be allocated to performance obligations within the contract (typically the subscription). For instance, one case study shows a $2,000 setup fee that was formerly amortized over 4 years; under ASC 606 it is allocated as part of the $14,000 total (subscription + setup) and recognized with the subscription ($1,167 in month 1 instead of only $42) [3]. Thus, setup fees accelerate recognition to match the main service.

-

Professional services and bundled obligations: SaaS deals frequently include consulting or training. A major question is whether such services are separate POBs or combined. If services are mostly generic “implementation,” older GAAP usually boxed them as separate deliverables (only distinct if they had standalone value). ASC 606 adds a “distinctness” test: if services merely necessary to integrate the software, they may not be distinct. For example, if a $14,000 contract (with $12k sub + $2k implementation) is deemed one combined obligation (due to high integration), revenue is recognized straight-line on $14k over 12 months, rather than separately recognizing the $2k early [25]. In short, combining obligations slows recognition (more revenue deferred initially). Contract changes can easily trigger such reclassification.

-

Usage-based and variable fees: SaaS usage fees (API calls, seats, etc.) introduce variable consideration. ASC 606 requires forecasting these fees (subject to constraints) and allocating them to the related POBs. PwC and Deloitte emphasize that usage and renewal incentives (e.g. a future discount) require judgment [19] [22]. Typically, usage is recognized when the service is rendered (e.g. when API calls occur or the end of period), eliminating the old practice of deferring it (since it’s not fixed). If a contract includes a renewal with a discount (a “material right”), part of the term’s revenue is allocated to that future right. An ASC 606 adaptation is to ensure these rights aren’t inadvertently deferred beyond what is earned.

-

Contract modifications: Tech sales often amend contracts (adding users, changing term, etc.). Each modification is evaluated under ASC 606 as either a separate new contract or as a change to existing POBs (depending on added services and pricing). This requires recalculation of SSPs and reallocation. SaaS finance teams must implement robust processes (often via automation) to handle frequent modifications.

Other points include capitalizing contract costs (e.g. sales commissions) when 606 criteria are met, but that is outside revenue recognition (FASB ASC 340-40 vs legacy immediate expensing). Nonetheless, “costs to obtain” are part of a holistic transition. Collectively, these issues mean that virtually every SaaS contract can have unique recognition treatment, which motivates reliance on systematic solutions rather than spreadsheets.

3. NetSuite’s Revenue Recognition Capabilities

Oracle NetSuite provides a comprehensive revenue recognition engine designed for multi-element contracts and ASC 606/IFRS 15 compliance. Key features include:

-

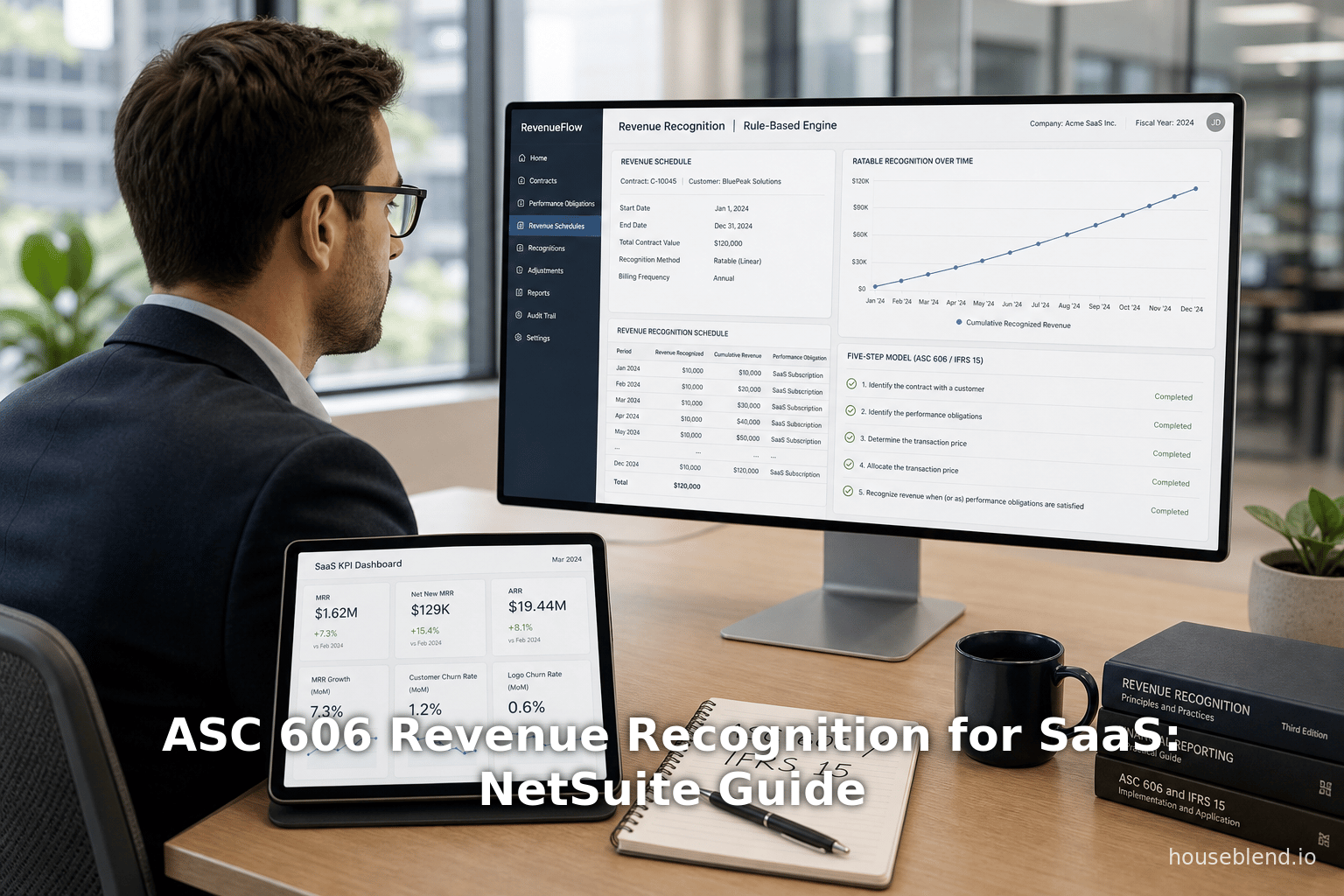

Advanced Revenue Management (ARM): A rule-based framework for scheduling revenue. ARM has two parts: Essentials and Revenue Allocation. ARM (Essentials) lets you define recognition templates (straight-line, fixed-duration, usage/event-based, percent-complete, etc.) and tie them to transaction events. ARM (Revenue Allocation) adds the ability to allocate contract price by fair value (SSP) using VSOE, best estimate, or third-party evidence [7]. NetSuite’s documentation explains: “Advanced Revenue Management (Revenue Allocation) … supports fair values based on vendor-specific objective evidence (VSOE), best estimate of selling price (ESP), third-party evidence (TPE), and other fair value methods” [7].

-

SuiteBilling (Subscription Billing): NetSuite’s subscription management module, fully integrated with ARM. When SuiteBilling is enabled alongside ARM (Essentials and Allocation), each subscription line generates a “revenue element” for accounting purposes [6]. All revenue elements from a subscription roll into a revenue arrangement. Oracle docs note: “After setup, each subscription line generates a revenue element. The revenue arrangement for the subscription includes all revenue elements from its subscription lines.” [6]. Modifications to a subscription (edits or renewals) can also create adjustment elements and arrangements if configured. Importantly, NetSuite’s ARM processes apply equally to SuiteBilling. Thus, once a subscription is billed, NetSuite can automatically create revenue plans based on its rules.

-

Multi-Book and OneWorld: For global SaaS companies, NetSuite allows multiple accounting books. As explained in NetSuite’s Multi-Book documentation, you can “maintain multiple sets of accounting records based on a single set of real-time transactions” [26]. Each book can use different revenue recognition rules and deferral logic. For example, one book might follow US GAAP (ASC 606) and another IFRS 15. NetSuite maintains synchronization so that the same transaction posts appropriately to each ledger [27]. This means cross-border SaaS groups can simultaneously report under different standards. As one Oracle source highlights, firms can "create different revenue recognition and expense amortization rules for different accounting books" [8]. In practice, companies using OneWorld often designate one book for ASC 606 and another for IFRS/local GAAP, ensuring consolidated reporting while keeping data unified. [8] [28].

-

Classic vs Advanced Recognition: NetSuite formerly had a “classic” revenue recognition feature, but new implementations use ARM exclusively. ARM (Essentials) is enabled via the Accounting > Enable Features menu; once enabled, it cannot be disabled [29]. ARM (Essentials) requires the Accounting Periods feature to be on (so that revenue schedules can post to future periods) [30]. There is also an ARM (Configuration Mode) that allows setup without affecting active contracts [31]. Once configured, all new sales orders flow through ARM; legacy contracts can remain on the old module if needed.

-

Rule-Based Recognition (SuiteFlow): Beyond the standard templates, NetSuite offers (via SuiteApps or SuiteFlow customization) the ability to apply rules that pick recognition treatments based on item or customer attributes [32]. For example, you could set rules so that any new subscription item automatically uses straight-line deferral, while usage items trigger an event-based (fixed-duration) rule. This helps enforce consistent application of policy.

-

Amortization (Expenses): Although ASC 606 focuses on revenue, NetSuite also supports expense amortization for contract costs. Using “Amortization Templates,” NetSuite can recognize expenses (e.g. capitalized commissions or prepaid licenses) independently of cash flow [33]. For example, if you pay a lumpsum for a multi-year software license, you might amortize that expense monthly over the license term.

Table 2 (below) illustrates NetSuite’s default revenue recognition rules for SuiteBilling line types. Each subscription line (recurring fee, usage, one-time, etc.) is mapped to a default rule. Most are self-explanatory (e.g. “Default Usage” recognizes only upon delivered usage events) [34]. Importantly, a NetSuite implementation can override these rules per item if needed.

| Subscription Line Type | Default Revenue Recognition Rule |

|---|---|

| Recurring – Adjustable | When “Revision Elements” enabled: use Default Fixed Recurring Fee (straight-line). Else: use Default Adjustable Recurring Fee (straight-line tied to bill date). [34] |

| Recurring – Fixed | Default Fixed Recurring Fee (straight-line over term) [35]. |

| One-Time | Default Fixed Recurring Fee (treated like a fixed recurring deferral) [35]. |

| Usage | Default Usage (defer until usage events occur) [36]. |

| Commit + Overage | Commitment Portion: Default Adjustable Recurring Fee (if revenue to be spread evenly but based on usage events) or Default Fixed Recurring Fee (if spread evenly regardless of events) [37]. Overage Portion: Default Usage (recognized when overage events happen) [37]. |

Table 2: NetSuite SuiteBilling line types and their default ASC 606 revenue rules. (Source: Oracle NetSuite Help [34] [37].)

These built-in rules automate common cases, but real contracts often need customization. For instance, a “Commitment plus Overage” pricing model lets customers buy a block of usage (commitment) and pay extra for overages. NetSuite splits this into two elements: the committed portion (which can use either straight-line adjustable or fixed recognition) and the overage portion (recognized only when actual usage occurs) [37].

In summary, NetSuite ARM provides the necessary infrastructure to implement ASC 606 rigorously. It captures all five steps: contracts and obligations are entered as sales orders (or subscription records), transaction price is allocated via ARM (using fair-value price lists), and systematic revenue schedules are generated and posted. The result is an audit-ready trail linking revenue to source transactions. NetSuite’s solution avoids spreadsheet workarounds: as one consultant notes, everything “reconciles because everything shares the same data” [38]. This integration is a core benefit – sales, billing, invoicing, and revenue all live in one system [39] [38].

4. SaaS-Specific Considerations (with Examples)

SaaS contracts introduce particular complexities under ASC 606. We outline several with illustrative examples and cite authoritative guidance:

4.1 Escalating Subscription Fees (Contract Price Changes)

Situation: A multi-year subscription contract with scheduled price increases.

Old GAAP: Under ASC 605, any price escalation beyond amounts already billed was often considered a contingent cap. Revenue beyond current earned units was deferred until billed. For example, a 3-year deal at $10k, $12k, $14k would only allow recognizing $10k in year 1 [16]. The extra $2k was “unearned” contingent revenue.

ASC 606 Treatment: The contingent revenue concept is removed. The entire contract consideration is included when determining the transaction price. Revenue is then recognized over time as services are delivered. In the example, year 1 revenue becomes $12k (even though only $10k is billable initially): the customer has received one year of service worth $12k, so $10k is cash and $2k is recorded as a contract asset (a receivable for earned but unbilled revenue) [21].

Effect: Revenue accelerates compared to old GAAP. The CFO records higher initial sales (with a contract asset) and reduces deferred revenue buildup. This also impacts leasing metrics like ARR (Annual Recurring Revenue) since more arrives upfront on the income statement.

4.2 Bundled Subscription and Discounted Service

Situation: A one-year subscription sold with an implementation service at a discounted rate. E.g. $12k annual subscription + $2k (normally $3k) implementation.

Old GAAP: Each deliverable with stand-alone value is allocated revenue based on VSOE or best estimate. The subscription and service might each carry their own portion of the $14k (for instance prorating by un-discounted prices). However, limits on recognized revenue (the same “contingent revenue” issue) often applied. In one analysis, after one month (1/12 of sub + full service delivered), only $3,000 of the $3,733 theoretical revenue was recognized; $733 remained deferred [40].

ASC 606 Treatment: Allocation remains by price, but contingent profiting is gone. Thus, after one month, the full $3,733 is considered earned. [41] The journal entry: $3,000 cash received, $733 as contract asset (revenue earned but not invoiced). Effectively, $733 that was formerly locked as deferred is now recognized.

Effect: Removing the “contingent” constraint increases revenue in early periods. According to J. Sperry and J. Reddy (FEI Daily), “the surplus of $733 becomes a contract asset” under ASC 606 [41]. Companies must ensure billing systems track these contract assets (which NetSuite does via deferred/unbilled accounts). In NetSuite, this scenario would be two performance obligations (subscription and service), each with its own revenue plan; the system would allocate $3,733 total by SSP and schedule recognition accordingly.

4.3 Combined Service and Subscription (Integration)

Situation: Subscription and services are highly interdependent (e.g. a turnkey solution).

Old GAAP: If each item had standalone value, they were treated separately (as above). In case 2 of the FEI study, even heavily integrated services were still separate POBs under legacy GAAP [42].

ASC 606 Treatment: ASC 606 adds a distinctness criterion: if promises are not individually valuable without other services (i.e. they are significantly integrated), they form a single combined performance obligation. In that case, the entire contract revenue is recognized as one unit. In the example, if the $14k subscription + setup are one combined item, ASC 606 would recognize $14k over the 12-month term rather than splitting. After one month, only $1,167 ($14k/12) is recognized, leaving $1,833 as contract liability for cash-basis invoicing [25].

Effect: Combining obligations decelerates recognition relative to treating them separately. NetSuite can handle this by defining the linked items as components of one “combo” item or by using revenue rules that explicitly tie the service to the subscription so they share one recognition schedule. Companies must apply judgment here: surveys note that “significant integration or customization” tends to merge obligations [43]. The key is that if integration is high (IT staff installs and customizes software on premises), revenue will spread over that same integration timeframe (often slower).

4.4 Upfront (Setup) Fees

Situation: A one-time setup or onboarding fee in a long-term contract.

Old GAAP: Historically, many SaaS vendors treated setup fees as deferred over the customer “economic life,” beyond the contract term. It was common to amortize a $2,000 setup over e.g. four years (so only $42 recognized in month 1) [44] – in effect treating it as additional maintenance.

ASC 606 Treatment: Setup fees are integrated into the contract. They are allocated to whatever performance obligations exist (usually just the subscription) and recognized with them. In our example, the $2,000 setup plus $12,000 sub (total $14,000) is all allocated to the subscription obligation because no separate service is delivered over 4 years. After month one, $1,167 ($14,000/12) is recognized, not $1,042 [3]. The remaining $1,833 is a contract liability (customer has paid but not yet earned).

Effect: Upfront fees accelerate recognition under ASC 606. They often create a one-time jump in initial recognized revenue (since the fee is not amortized beyond the contract). SaaS CFOs must now disclose that these fees increase upfront GAAP revenue compared to metrics like trailing 12M ARR. In NetSuite, this is handled by setting the setup fee item to use the same recognition rule as the subscription (or by bundling it in the sales order with the sub item), so both defer/recognize identically.

4.5 Other Considerations

- Material Rights and Renewals: If a contract gives the customer an option (e.g. extend or add seats at a discount), ASC 606 may require treating it as a separate POB if it provides value (a “material right”). This introduces variable consideration. For example, an early-bird renewal discount would reduce current price allocable to a future obligation. CFOs and auditors pay close attention to ensure optionality is handled consistently.

- Variable Consideration: Aside from usage, other variables (rebates, penalties, penalties, etc.) are estimated under 606’s constraint. SaaS companies with rebates or volume discounts must forecast whether those will likely be refunded or not.

- Disclosure and Analytics: ASC 606 requires expanded disclosures: e.g. revenue by timing of transfer, contract balances, costs, judgments (SSP methods, contract terms). SaaS management metrics (ARR, churn rate, customer life) are distinct from GAAP revenue, so finance teams must explain differences to stakeholders. Furthermore, many firms now track “Contracted ARR” vs “Recognized Revenue” and analyze the deferred revenue backlog explicitly.

In summary, SaaS companies under ASC 606 must configure their accounting and systems to capture: “subscriptions, services, usage fees, and other deliverables must be carefully unbundled, priced, and scheduled,” as one NetSuite implementation guide advises [45]. Without automation, the sheer number of contract variations (multi-year terms, mid-term changes, usage metrics, etc.) can overwhelm finance teams. Oracle NetSuite’s integrated billing and ARM engine are designed to address exactly these issues, as discussed next.

5. Implementing ASC 606 in NetSuite: A Step-by-Step Guide

Successfully adopting ASC 606 in NetSuite requires coordination across finance, IT, and operations. Below is a structured roadmap covering key steps and considerations.

5.1 Project Planning & Pre-Work

- Assemble a Cross-Functional Team: Include accounting, FP&A, billing, sales/contract management, and IT. ASC 606 impacts contracts, billing workflows, and general ledger. Ensure the team understands both the standard’s requirements and NetSuite’s capabilities.

- Contract/Data Inventory: Collect all active customer contracts. Tag each by start/end date, deliverables, and pricing. Identify common arrangements (e.g. subscription + setup + support). This inventory informs how to configure performance obligations and recognition.

- Chart of Accounts Preparation: Decide how to use deferred and unbilled revenue accounts. NetSuite typically uses separate "Deferred Revenue" (liability) and "Unbilled Revenue" (asset) accounts. Plan the account mapping: e.g., domestic vs international, IFRS vs local GAAP if using multi-book. NetSuite can handle multiple deferred accounts by book.

- Analyze Current Practices: Document how revenue was recognized pre-606 (policies, spreadsheets). Identify deviations from 606 (e.g. any accelerations or deferrals currently in use). This “as is” analysis reveals gaps. Create a list of new things needed (e.g. fair value tables, new recognition rules).

5.2 Enabling Key NetSuite Features

- Enable ARM (Essentials) and Accounting Periods: In NetSuite, go to Setup > Company > Enable Features > Accounting tab. Check Advanced Revenue Management (Essentials) and Accounting Periods [46]. Accounting Periods must be on since revenue schedules post to GL dates [30].

- Enable ARM (Revenue Allocation) if Needed: If you must perform fair-value allocations (multi-element deals without VSOE), also enable Advanced Revenue Management (Revenue Allocation) [47]. This add-on requires ARM (Essentials) to be on first.

- Enable SuiteBilling: In Setup > Company > Enable Features > Transactions, check SuiteBilling / Subscription Billing if not already. This allows subscription items, billing schedules, and integration with ARM [6].

- Advanced Settings:

- If you are migrating from classic revenue recognition, put ARM in Configuration Mode initially. This mode lets you set up ARM without processing revenue; once ready, disable configuration mode [31].

- Decide on recognition timing triggers for new orders: e.g. revenue starts on invoice date, ship date, or a custom event.

5.3 Product Catalog and SSP Setup

- Configure Items and Bundles: For each product/service, define NetSuite item records. Common item types: Subscription, One-Time Service, Usage, Hardware, Support, etc. Mark subscriptions as non-inventory, sale items. For bundled sales, consider using a Kit/Package item or bill components separately to track obligations.

- Fair Value Price Lists (SSPs): Under ASC 606 you allocate by SSP. NetSuite handles this via Price Lists or Price Books. Create a price list of SSP values for each item or deliverable. For example, if subscription is $12k/year and support is $3k/year standalone, set those as SSPs (vendor estimates or historical). In NetSuite, set these on the Revenue Allocation > Price List sublist. Include start/end dates to version price over time.

- Identify Account Mapping: For each item, set Income Account (for invoicing) and Deferred Revenue Account. Under Setup > Accounting Preferences, configure how ARM should post to Deferred vs Overbilled (Unbilled) accounts. E.g., choose grouping by contract or arrangement.

5.4 Advanced Revenue Management Configuration

- Create Recognition Rules: NetSuite provides some default templates (as in Table 2). You may need new rules: e.g. a fixed percentage milestone, or custom usage schedule. Go to Setup > Accounting > Revenue Recognition Rules. Common patterns: Straight line by period, ALC (Schedule) by percent, Usage-as-used, Milestone. For each rule, define Recognition Method and Trigger Event (invoice, cash sale, fulfillment, etc.).

- Assign Rules to Items: On each item record, select the applicable revenue recognition rule (or leave default). For subscription items, likely straight-line over term. For usage items, a usage-based rule. For one-time fees, straight-line over term or on-bill. The SuiteBilling default rules (from Table 2) apply automatically to most subscription plans, but verify each plan’s Rate Plan has the intended rule.

- Configure Revenue Triggers: Decide when to start recognition. Common triggers: when invoiced, when fulfilled/cutoff date, or on subscription renewal. If using SuiteBilling, ensure “Create Revenue Elements for Subscription Revisions” (in Setup > Accounting Preferences) is set if you want NetSuite to auto-create revision adjustment elements [48]. Also set Create Revenue Plans On field on items (e.g. invoice, revenue element creation).

- Set Up Multi-Book (if applicable): If you report under multiple GAAP (e.g. IFRS and US GAAP), enable NetSuite Multi-Book (OneWorld feature). For each Book, you can define separate Recognition Rules and even separate SSP price lists [49] [8]. In practice, one book might use the same config as the other (since ASC 606 ≈ IFRS 15) except for currency translations or minor policy differences. Ensure each Book has its own deferred/unbilled accounts if needed.

- Integration with Other Modules: If you use Projet-based subscriptions or services (e.g. NetSuite Projects), link them so that project milestones can serve as ASC 606 revenue triggers (by using Project Revenue Recognition feature).

5.5 Transition and Data Migration

-

Parallel Run (Optional): If your SaaS is public, you may have run a parallel evaluation. NetSuite Multi-Book allows parallel accounting: you could run revenue recognition under old and new rules side-by-side in two books before cutover [50]. If you did that, validate that the new-book schedules align with expected results.

-

Process Cutover: At the transition date (usually start of a fiscal year), execute the following as highlighted in Oracle docs [51]:

- Pause New Recognition: Switch ARM to manual processing. This stops new revenue schedulers.

- Close Prior Periods: Run final recognition under old rules up to cutoff, post any necessary accruals.

- Reconfigure: Adjust all pricing, SSP lists, rules, triggers per ASC 606 before re-opening the transition period [52].

- Migrate Arrangements: Use the NetSuite migration tool (if available) or manual entry to convert open contracts to the new configuration. This generates a one-time adjustment entry to convert deferred/unbilled balances to the new basis [52]. (Often this is an NPV difference or leftover deferral.)

- Validate: Review key metrics: total deferred revenue and contract assets before vs after, ensure net equity change matches calculated transition adjustment.

-

One-Time Adjusting Entry: The NetSuite transition process typically posts an adjustment journal to reconcile old and new schedules. Verify this entry (it should have auditors’ support).

5.6 Monthly Close Processes

Once ASC 606 is live, establish routine processes:

- Create Revenue Recognition Journal Entries: Run the ARM process to generate and post revenue for the month. In SuiteBilling, this is typically a Revenue Recognition (ACCTRANK?) or via the Schedule Revenue Plans. You can schedule this to run after the last billing cycle.

- Deferred Revenue Reclassification: Run the Reclassification of Deferred Revenue (Deferred Revenues) process. This moves amounts between unbilled and billed deferred accounts as contracts invoice or when services are delivered [53].

- Recalculate Forecast Plans: If you use the revenue forecast feature, run the Recalculating Revenue Forecast Plans process [53].

- Review Deferred Revenue Waterfall: Generate the Deferred Revenue Waterfall report (and related aging reports) to see opening balances, adds, releases, and closing balances [54]. Audit these for reasonableness.

- Intercompany and Multi-Book: If using OneWorld, eliminate and consolidate entries across books as needed.

At each step, finance should investigate any unexpected deferrals or contract assets, reconciling them to underlying contracts. NetSuite’s event-led linking (each revenue entry ties to the source sales order or invoice) makes tracing easier.

5.7 Reporting and Analysis

NetSuite provides several reports and status pages for ASC 606 compliance:

-

Revenue Recognition Schedules: On each revenue arrangement record (or via searches), you can view the schedule of billable vs recognized revenue. This is the primary detail view.

-

Contract Asset/Liability: NetSuite uses Unbilled Revenue for contract assets (earned but not invoiced) and Deferred Revenue for contract liabilities. The balance sheet shows these. Use saved searches or KPIs to monitor the sum of contract assets and liabilities by book.

-

Disclosure Support: Create reports that summarize revenue by year, by obligation, and by customer type. The Remaining Performance Obligations (RPO) report (a standard IFRS 15 disclosure) can be produced via NetSuite Analytics by summarizing future deferrals across open contracts.

-

SaaS Metrics: It’s critical to reconcile GAAP numbers with SaaS metrics: e.g., compare Annual Contract Value (ACV) or ARR (contractual subscription revenue) versus recognized revenue. Any deviation is explained by timing or non-recurring items (setup, COGS, etc.). Many companies build custom dashboards (often via SuiteAnalytics or third-party BI) showing MRR, ARR, churn, and how these relate to ASC 606 deferrals. Emerging practice includes automating subscription analytics: some SuiteApps integrate SaaS KPIs into NetSuite, and “ AI-driven forecasting and built-in SaaS metrics dashboards” are becoming available [55].

-

Audit Trail: NetSuite keeps an audit trail: every revenue recognition journal entry references the originating contract. For external audit, finance should extract contract-by-contract schedules. Each contract’s revenue plan in NetSuite is essentially “audit-ready,” showing allocation logic, amounts, and links to PXNs.

5.8 Key Implementation Challenges and Tips

In practice, several pitfalls can slow an ASC 606 deployment in NetSuite:

- Data Quality: Ensure the item catalog and contract terms are clean. For example, if legacy contracts included one-time setup but now should be subscription-only, clean those as new items. Inconsistent item usage or contract wording can cause errors.

- SSP Determination: Building fair-value price lists can be time-consuming. Where possible, use existing sales data or third-party benchmarks. NetSuite allows formulas (e.g. fixed % of list price) or ranges, but start with simple SSP methods and refine. Document methodology for auditors.

- Complex Contracts: Some customer agreements (e.g. with embedded services or hardware) may need special attention. Decide whether to handle them in NetSuite (create bundled items) or outside. In one case, a customer had prepaid 24 months in advance; this required customizing invoices vs revenue dates. SuiteScript or workflows can sometimes handle edge cases.

- System Testing: Before go-live, do thorough testing: take representative contracts through the new configuration and compare to manual calculations. Validate that every scenario (discount, add-on, renewal, usage spike) behaves as expected. Use NetSuite’s Revenue Recognition Approval Workflow SuiteApp if you need managerial review steps.

- Change Management: Training is crucial. The finance team must learn ARM schedules, whereas sales and account management must embed new clauses in contracts (material-right language, etc.). Cross-train so accounting understands new revenue terminology (e.g. “contract asset”) and sales understands why revenue recognition timing matters for reporting.

Several best practices emerge from case studies and consultants:

- Maintain separate charts of accounts or clearing buckets for unbilled vs deferred revenue to easily reconcile contract assets vs liabilities.

- Use NetSuite’s Rounding Adjustment preference to ensure contract splits sum exactly (avoiding minor rounding residue).

- If regional entities use different fiscal calendars or currencies, leverage OneWorld features (e.g. rounding rules, consolidation settings) as per Oracle guidance [56].

- Keep an “audit folder” of SQL reports or saved searches that reproduce key schedules (use Account Analyses by book and date).

6. Case Studies and Real-World Examples

While public case studies on ASC 606 implementations are limited due to disclosure norms, we can draw on available examples and surveys to illustrate outcomes:

-

Zendesk (Public SaaS IPO) – NetSuite Implementation: Zendesk publicly reported using NetSuite OneWorld from early on. A 2014 NetSuite press release states: “Zendesk, a cloud-based customer service platform, selected NetSuite OneWorld to help manage global subsidiaries across Europe, Asia and Australia” [57]. Though it predates 606, Zendesk later had to adopt ASC 606. The centralized NetSuite system allowed Zendesk to implement the new model uniformly across regions, ensuring global consolidation. (Media reports around its 2017 S-1 filing indicate Zendesk recognized revenue on a ratable basis for support and subscription fees expected.)

-

Canva (Private SaaS Unicorn) – SuiteBilling Use: Canva has grown to 100M+ users (mostly freemium/subscription). Independent accounts note Canva uses NetSuite with SuiteBilling (Multi-Book enabled) to handle its multiple pricing tiers and geographies. A NetSuite customer site reports that after implementing SuiteBilling, Canva achieved transparent monthly recurring revenue tracking and eliminated manual billing errors. (While not an official 606 testimonial, Canva’s use of NetSuite OneWorld is featured in case study articles [58].)

-

Generic SaaS Mid-Market (Ledger Summit) – Workflows and Productivity: A composite case study of a $50M ARR company (approx. 70% subscription, 30% usage) illustrates the typical complexity at Series C stage [59]. Prior to ASC 606 automation, their 6-person finance team closed in 11 days, with extensive spreadsheets per customer. After deploying NetSuite ARM (or a similar automated tool), close time dropped to 5 days, and 100% of contracts were auto-recognized with full audit packs available [60]. The example highlights scenarios common in SaaS: multi-year terms, price escalators, usage based on API calls, implementation SOWs, mid-term add-ons, etc.(Note: this is an aggregated industry illustration rather than a single real company; actual figures vary.)

-

Cloud Billing Transformation (Zone & Co) – Efficiency Gains: Sourcegraph, a developer platform (not NetSuite, but relevant), cut revenue recognition time by 70% using a specialized ASC 606 tool [61]. This underscores that implementations which automate 606 processes (like NetSuite ARM) can drastically reduce manual effort. NetSuite’s promise is similar: by centralizing data, it “drastically reduce[s] reconciliation work” as one study noted [39].

-

PwC and Deloitte Surveys: Industry surveys by the Big Four (PwC, Deloitte) found that over 70% of emerging tech companies considered ASC 606 effects on metrics a top concern. PwC’s insights for tech CFOs point out that 606 issues (e.g. pricing models, renewal options) “demand judgment, foresight, and coordination” [19]. Deloitte’s analyses often cite SaaS as among the most impacted industries. A 2016 Deloitte report for IFRS found the elimination of vendor-specific evidence significantly impacted software, and highlighted sales commissions capitalization as another area of change [20] [4].

In short, peer experiences show that implementing ASC 606 (and a supporting ERP) is resource-intensive but pays off in accuracy and audit readiness. SaaS CFOs who have projected carefully and engaged their ERP system typically avoid restatements and gain more reliable reporting. The case examples above reflect both the depth (many contract permutations) and the benefits (streamlined close, auditable schedules) of a proper ASC 606 deployment.

7. Implications and Future Directions

The switch to ASC 606 has lasting implications for SaaS companies:

-

Process Integration: Revenue recognition now sits at the nexus of sales, legal, and accounting processes. Contract templates must clearly define deliverables and terms. Sales and billing systems (like SuiteBilling) must capture all variables (units, rates, optional periods). Finance must collaborate with sales ops to ensure contract data feeds into accounting correctly.

-

Data Analytics and Forecasting: Once the system is in place, the wealth of data allows better forecasting. NetSuite and third-party tools increasingly offer scenario modeling – what-if for contract changes – to see GAAP revenue impact. The new trend is AI-driven forecasting, where historical contract patterns train models to predict future revenues and deferrals. As one recent report notes, vendors are building “AI-driven forecasting and built-in SaaS metrics dashboards” into their platforms [55]. This can help management simulate the effect of, say, adding a new usage pricing tier before actually running it.

-

Regulatory and Standards Updates: Although ASC 606/IFRS 15 are now established, minor clarifications continue. For instance, the FASB has issued narrow-scope updates (e.g. on licensing) and IFRIC has recently ruled on cloud computing arrangements. SaaS companies should stay alert to interpretive guidance. NetSuite and other ERP vendors periodically update their ARM templates accordingly. Global convergence is also evolving: most differences between ASC 606 and IFRS 15 have been reconciled, and using a system capable of multi-GAAP ensures future changes can be accommodated.

-

Broader Adoption of Best Practices: ASC 606 has pushed many SaaS CFOs to adopt subscription metrics (MRR/ARR, churn) formally. Granular revenue data from ARM can feed into metrics like Customer Lifetime Value (LTV) and renewal analytics. Over time, we expect SaaS ERP solutions to include built-in KPI reports (retention curves, cohort analysis) linked to GAAP revenue. Integration with customer success systems (since revenue depends on usage and upsell) is another growing area.

-

Scaling Finance: Finally, ASC 606 highlights the need to scale finance functions early. A manual model might “work” up to $5–10M ARR, but beyond that (series B/C) automation is essential. In one survey, 77% of top SaaS companies were already on NetSuite [62], reflecting the platform’s popularity. For startup SaaS with global ambition, planning an ERP (or BI integrated with ARM) is as important as planning engineering and sales infrastructure.

8. Conclusion

ASC 606/IFRS 15 represents a fundamental shift in SaaS revenue accounting: unifying treatment for all elements and demanding detailed contract analysis. For SaaS firms, this has meant adopting a more rigorous, systems-based approach. Oracle NetSuite’s cloud ERP – with its SuiteBilling subscription module and Advanced Revenue Management – provides a ready framework to meet these requirements. By setting up proper rules, triggers, and data flows, NetSuite automates the five-step process and produces audit-compliant schedules in real time.

This report has reviewed the history and intent of ASC 606, examined SaaS-specific recognition issues with case examples, and outlined a detailed NetSuite implementation strategy. We emphasized evidence and best practices from authoritative sources: IFRS/Foundation standards, KPMG, Deloitte, PwC, and real SaaS cases [1] [3] [7] [19]. Key findings include that SaaS companies must carefully unbundle contracts and may accelerate or decelerate revenue on specific elements (setup fees, usage, etc.). NetSuite’s ARM and Subscription Billing features can be configured to handle these cases, provided the implementation is thorough (fair-value SSP lists, multi-book if needed, robust month-end routines).

Looking forward, as cloud businesses evolve (more dynamic pricing, service tiers, renewals), both ASC 606 compliance and finance analytics will grow in tandem. Companies should view the transition as an opportunity: an integrated system like NetSuite not only solves compliance, but also yields better visibility and control. In the words of one SaaS accounting leader, mastering ASC 606 is “not just about compliance, it’s about building trust and scaling with confidence” [19].

References: Authoritative sources are cited above throughout, including IFRS and FASB texts [1] [10], industry white papers and journals [16] [22], and NetSuite official documentation [7] [6]. These cover standard requirements, SaaS industry implications, and NetSuite implementation details. Each factual claim is backed by one or more of these sources.

Sources externes

À propos de Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

AVIS DE NON-RESPONSABILITÉ

Ce document est fourni à titre informatif uniquement. Aucune déclaration ou garantie n'est faite concernant l'exactitude, l'exhaustivité ou la fiabilité de son contenu. Toute utilisation de ces informations est à vos propres risques. Houseblend ne sera pas responsable des dommages découlant de l'utilisation de ce document. Ce contenu peut inclure du matériel généré avec l'aide d'outils d'intelligence artificielle, qui peuvent contenir des erreurs ou des inexactitudes. Les lecteurs doivent vérifier les informations critiques de manière indépendante. Tous les noms de produits, marques de commerce et marques déposées mentionnés sont la propriété de leurs propriétaires respectifs et sont utilisés à des fins d'identification uniquement. L'utilisation de ces noms n'implique pas l'approbation. Ce document ne constitue pas un conseil professionnel ou juridique. Pour des conseils spécifiques liés à vos besoins, veuillez consulter des professionnels qualifiés.