NetSuite Due To/Due From Accounts: Setup & Reconciliation

Executive Summary

In complex multi-entity organizations, Due To/Due From (Due-to/From) accounts are essential for tracking intercompany transactions and ensuring accurate consolidated reporting. These accounts represent reciprocal internal receivables and payables between subsidiaries: one entity’s “Due From” balance is another’s “Due To” balance [1] (Source: timdietrich.me). Proper use of these accounts is legally mandated under IFRS 10 and ASC 810, which require that all intra-group assets, liabilities, income, and expenses be eliminated in consolidation [2] [1]. Failure to reconcile Due To and Due From balances can lead to overstated revenues, assets, and profit, and is a common cause of restatements and audit findings (Source: timdietrich.me) [3].

Oracle NetSuite OneWorld provides comprehensive intercompany functionality to automate these processes. Key features include the Intercompany Framework and Automated Intercompany Management, which together generate cross-subsidiary sales/purchases, intercompany journal entries, and automated elimination entries [4] (Source: timdietrich.me). They rely on carefully configured GL accounts. In NetSuite, each subsidiary typically uses dedicated intercompany accounts (often flagged for elimination) to record its side of a trade (e.g. Intercompany Receivable (due-from) and Intercompany Payable (due-to) accounts) [5] [6]. In practice, organizations choose among design options such as a single shared Due From/To pair, entity-specific accounts, or a single clearing account with segment tagging (Source: timdietrich.me) [5].

Setting up NetSuite intercompany clearing involves enabling OneWorld and intercompany features, creating appropriate intercompany GL accounts, and specifying default elimination accounts in the Intercompany Preferences [7] [8]. For example, administrators create new AR/AP accounts with the “Eliminate Intercompany Transactions” box checked, and then assign them to relevant subsidiaries [9] [10]. NetSuite then uses these accounts to post transfers: when subsidiary A sells to B, A debits its Intercompany Receivable (due-from) account while B credits its Intercompany Payable (due-to) account, or vice versa. NetSuite also automatically generates specialized Intercompany Clearing accounts (e.g. for cross-charges) when enabling features like Time and Expense, which are used to balance exchange rates and currencies [11] [12].

Reconciliation of Due To/Due From accounts is an intensive but critical control. NetSuite provides tools such as the Balance Overview page (viewing open payables vs receivables by subsidiary pair) [13] and the Intercompany Reconciliation Report to identify unpaired or mismatched transactions [14] [15]. Best practice is to run reconciliations before period close, drill into differences, and post correcting entries so that each intercompany receivable precisely equals its partner payable [16] [17]. The benefits of this rigor are substantial: industry research notes that up to 70% of internal group trade can be managed through intercompany netting, which can reduce payment volume by as much as 90% [18] [19]. In other words, by clearing and netting Due To/From balances automatically, companies can slash intercompany transactions and fees, cut reconciliation time by days each month, and greatly improve visibility of cash flows [18] [19].

This report provides an exhaustive examination of Due To/Due From accounts and intercompany clearing in NetSuite. We begin with background on intercompany accounting and the role of due-to/from accounts. We then survey NetSuite’s features and configuration steps for setting up intercompany transactions – including GL accounts, preferences, and elimination processes [7] [9]. Detailed sections cover best practices (e.g. choosing account designs (Source: timdietrich.me), reconciliation techniques using NetSuite reports, and the implications of convergence of IFRS/US GAAP requirements [2] [20]. We integrate data and expert findings on efficiency gains (e.g.case examples of dramatic netting benefits [19]) and foreseeable trends (e.g. AI-driven reconciliation and blockchain settlements [21]). Throughout, we cite authoritative sources – Oracle documentation, accounting standards guidance, and practitioner analysis – to substantiate all claims. The paper concludes with actionable recommendations and a view to the future of intercompany finance.

Introduction and Background

The Nature of Intercompany Transactions and Due To/From Accounts

Modern corporations often include multiple subsidiaries, joint ventures, or divisions operating in different jurisdictions. When one legal entity sells goods or services to another within the same group, or lends or transfers resources internally, both sides of the transaction must be recorded in each entity’s books (Source: timdietrich.me) (Source: timdietrich.me). For instance, if Subsidiary A sells $100,000 of products to Subsidiary B, then A will record $100,000 in revenue and B will record $100,000 in inventory (or cost of goods sold). From the group’s perspective, however, this sale and purchase cancel out: no external party is involved. Consequently, Due To and Due From accounts are used to capture the internal balances until elimination.

A Due From (Intercompany Receivable) is an asset on one entity’s balance sheet, representing an amount owed to that entity by its affiliate [1] (Source: timdietrich.me). Conversely, a Due To (Intercompany Payable) is a liability on the counterparty’s books, reflecting the reciprocal obligation [1] (Source: timdietrich.me). By design, every debit to a Due From account in one subsidiary is offset by a credit to a Due To account in the other. For example, if Parent Company advances $50,000 to Subsid B for funding, the parent debits “Due From Subsidiary B” and credits Cash, while Subsidiary B debits Cash and credits “Due To Parent Company” [22]. Legal and accounting conventions demand that these reciprocal balances always match: if Parent shows a $100,000 receivable, Sub should show a $100,000 payable [23]. This mirroring ensures the internal debt nets to zero upon consolidation.

Figure 1: Intercompany Due To and Due From across entities

| HLDG Co (USD) | SUB Co (EUR) | |

|---|---|---|

| Cash $50,000 | Dr. | Cash (in EUR) <?> Cr. |

| Due From SUB | Dr. +£50,000 | Due To HLDG (liability) +£50,000 Cr. |

Figure 1. Example: Parent advances funds to subsidiary. Parent’s balance sheet shows a Due From (asset), subsidiary shows a matching Due To (liability) [22] [1].

This design is central to intercompany accounting. According to consolidation accounting standards (IFRS 10 for international, ASC 810 for US GAAP), any intra-group balances, transactions, income, and expenses must be fully eliminated in the consolidated financial statements [2] (Source: timdietrich.me). If they were not, the consolidated balance sheet would overstate assets by including the receivable and liabilities by including the payable, effectively double-counting internal activity. Thus, accurate Due To/Due From tracking and reconciliation is not optional but a compliance requirement under IFRS and GAAP [2] [1]. For example, IFRS 10 explicitly mandates elimination of intragroup balances; ASC 810 parallels this requirement for U.S. reporting [2].

Legal clarity experts emphasize that maintaining these accounts “enables clear, auditable financial statements at the individual company and consolidated group levels” [24]. They classify Due From balances as assets on the lender’s books and Due To as liabilities on the borrower’s books [1]. Notably, IFRS permits offsetting (netting) intragroup balances only if a legal right of offset exists [25], which in practice rarely applies across separate legal entities. Hence, organizations generally leave the gross balances intact up to elimination, only netting them out at the consolidation stage. [25] [2]

To summarize, intercompany Due To/From accounts are specialized GL accounts that capture internal obligations and claims between group entities. They are the “intercompany equivalent of accounts payable and receivable” (Source: timdietrich.me). Every intercompany sale, loan, dividend, or allocation creates a pair of these accounts. A sale causes a receivable (Due From) in the seller and a payable (Due To) in the buyer [26]. Loans create similar entries (lender books Due From, borrower books Due To) [27]. Over time, these accounts accumulate all unmatched internal transactions until they are reconciled and physically eliminated from the books.

Challenges in Intercompany Reconciliation

Managing multiple Due To/From accounts across currencies and legal entities is notoriously complex. Industry reports note that up to 70% of intra-company trade often flows through such intercompany invoices [18]. Without effective controls, the reconciliation of these accounts can become the bottleneck of the close process. According to the Multi-Entity Accounting (MEA) team, in groups with more than five entities, reconciliation is often “the single largest source of close delay” [28].

Common issues include timing differences (one branch invoices in December, the other records payment in January [29] [30]), currency translation mismatches (each entity posts in different currencies or at different rates [31] [30]), disparate chart of accounts (lack of uniform account naming, requiring mapping), and missing or disputed transactions [30] [29]. For example, if Entity A records an intercompany sale in USD in period 1, but the purchasing Entity B books it at a different rate or date, their reported Due To/From balances will differ until corrected. These discrepancies are especially likely in global setups with multiple functional currencies; as one guide notes, IFRS 21 can produce translation variances that must be distinguished from accounting errors [20] [31].

The intercompany reconciliation process itself is well-defined in best practice guides [32] [33]. In brief, finance teams build an entity-pair reconciliation matrix (which subsidiaries transact with which, in what currencies), then at period-end each produces a trial balance that isolates intercompany balances [32]. Each entity’s listed intercompany receivables to a counterparty must exactly match that counterparty’s payable to them. Transactions are then matched one-to-one (e.g. each invoice with its corresponding bill or payment) [16]. Unmatched items are investigated—common reasons include simple timing, wrong exchange rates, or missing entries. Discovered differences are resolved by posting adjustment entries as needed to bring the balances in agreement [17] [33]. For example, if a €100,000 loan shows up as €99,000 on one side due to rate differences, one entity would adjust by €1,000 to reconcile. Finally, the controllers of each entity sign off on the reconciliation to attest that balances now mirror precisely [34]. Only then are the balanced entries passed to the consolidation system for elimination [34] [2].

Figure 2 illustrates the general workflow for intercompany reconciliation:

| Step | Activity | Tools/Notes |

|---|---|---|

| 1. Define Intercompany Matrix | Document which entities transact with each other, currencies involved. | Sets scope of next steps (e.g. A⇄B, A⇄C, etc.) |

| 2. Extract Balances by Entity Pair | Each subsidiary isolates GL balances for Intercompany AR, AP, and related accounts (using flagged IC accounts or classes). | Can use trial balance reports with interco filters |

| 3. Match Transactions | Break down each balance into underlying documents (invoices, bills, advices). Pair each “Due From” in Entity X with a “Due To” in Entity Y. | This is often done via matching logic in software or spreadsheets [16]. |

| 4. Identify Variances | List unmatched items and quantify differences in amount or period. | Timing, FX, or missing entries are noted. |

| 5. Investigate & Resolve | Research causes: confirm correct dates/exchange rates or missing entries. Obtain counterparty confirmation if needed. | May involve contacting other entity’s controller. |

| 6. Post Adjustment Entries | The out-of-balance entity posts correcting journal entries to align the receivable and payable to exactly match [17]. | Example: an AR adjustment if one side recorded later. |

| 7. Sign-off | Each entity’s controller certifies the recon is complete and agrees with counterpart. | Required for audit trail and SOX/IFRS compliance. |

| 8. Consolidation Elimination | Once reconciled, elimination entries remove all intercompany AR vs AP balances, yielding zero net on consolidation [2]. | System (e.g. NetSuite) or manual elimination journals used. |

| 9. Archive Documentation | Save matched detail, JE adjustments, and sign-off records for audit purposes. | Often done in compliance or treasury documentation. |

Figure 2. Intercompany Reconciliation Workflow. Each step must ensure that for every intercompany receivable (Due From) there is a matching payable (Due To) of the same amount, so that eliminations leave no residual balances [23] [16].

The significance of this process cannot be overstated. Senior finance leaders report that effective intercompany netting (offsetting mutual payables/receivables) greatly simplifies operations. Netting consolidates intercompany payments, locking in larger FX rates and cutting bank fees [18] [35]. It also “provides a clearer view of how money moves within your corporate structure,” improving visibility and control [35] [19]. Industry examples show dramatic outcomes: one case study describes an electronics firm reducing dozens of intercompany wire payments down to a handful via netting [19]. Overall, workflow automation can slice close times by multiple days. In short, thorough tracking of Due To/Due From accounts and leveraging system automation become critical enablers of efficiency, accuracy, and compliance [18] [19].

NetSuite OneWorld: Intercompany Architecture and Features

Overview of OneWorld and Intercompany Framework

NetSuite OneWorld is Oracle’s cloud ERP solution tailored for global, multi-subsidiary organizations [36] (Source: timdietrich.me). It allows a single NetSuite account to manage multiple subsidiaries (legal entities) with distinct currencies, tax rules, and charts of accounts (Source: timdietrich.me). To handle intercompany processes, OneWorld provides specialized features, notably the Intercompany Framework and Automated Intercompany Management [4] (Source: timdietrich.me).

-

Intercompany Framework: A core feature that establishes the groundwork for inter-entity transactions. It introduces the concept of elimination accounts and supports cross-subsidiary pricing and revenue recognition. Once enabled, it allows configuration of default intercompany GL accounts, defining representing entities (agents that act on behalf of each subsidiary), and enables cross-charge automation [7] (Source: timdietrich.me).

-

Automated Intercompany Management (AIM): Formerly called “Intercompany Auto Elimination,” this feature automates much of the intercompany process. When turned on, NetSuite can automatically generate intercompany purchase and sales orders between subsidiaries, and then produce the appropriate journal entries to eliminate the internal profit and balances during period close [4] [37]. With AIM enabled, the system will create elimination entries for matching intercompany transaction lines (sales vs purchases) and intercompany journal lines that are marked for elimination [38].

-

Multi-Subsidiary Entities (Customers/Vendors): NetSuite allows a single customer or vendor record to transact across multiple subsidiaries. For intercompany sales, for example, each subsidiary may have a customer record for internal counterparties. The Multi-Subsidiary Customer and Multi-Subsidiary Vendor features let a parent company appear as a customer in one subsidiary and as a vendor in another, facilitating intercompany sales/purchase flows [36] [6].

-

Multiple Currencies: OneWorld enables transaction and reporting in multiple currencies per subsidiary. This is crucial when intercompany bills and payments occur in currencies different from either entity’s functional currency [39]. NetSuite supports full currency conversion, revaluation of open balances, and revaluation of intercompany accounts.

To activate these, an administrator must go to Setup > Company > Enable Features. Key features to turn on include OneWorld (for multi-currency, multi-subsidiary), Multi-Subsidiary Customer/Vendor, Multiple Currencies, Advanced Intercompany (or similarly named Intercompany Framework), and Automated Intercompany Management [40] [38]. Importantly, some features (like Automated IC Management) cannot be turned off once enabled [41], so planning is needed.

Once configured, these features provide the structural basis for due-to/from accounting. OneWorld defines subsidiaries hierarchically; each intercompany transaction carries an originating subsidiary and a target subsidiary. The system uses intercompany-clearing accounts to balance cross-charges, and elimination accounts (flagged with “Eliminate IC Transactions”) to prepare for consolidation [7] [42].

Prerequisites: Before any intercompany process, one must design the subsidiary hierarchy and enable relevant features. NetSuite documentation emphasizes that each subsidiary record should represent a legal entity (Source: timdietrich.me). Subsidiaries may be organized under an “elimination subsidiary” hierarchy so that entries are properly removed at the parent level. Also, each subsidiary must have a declared functional currency that cannot be changed later (Source: timdietrich.me).

Intercompany GL Account Structure in NetSuite

Intercompany Receivable and Payable Accounts

In NetSuite, the principal Due To/From accounts are typically implemented as specialized Accounts Receivable (AR) and Accounts Payable (AP) GL accounts flagged for intercompany elimination. When configuring, best practice is to create new dedicated AR and AP accounts for intercompany transactions [43] [10]. These might be named “Intercompany Receivable” and “Intercompany Payable” or similar. The critical setup step is:

- Create Account: Go to Lists > Accounting > Accounts > New. Choose type Accounts Receivable or Accounts Payable.

- Eliminate IC Transactions: Check the box Eliminate Intercompany Transactions on the account record [42]. This tells NetSuite that any postings here should be eligible for elimination entries at close.

- Select Subsidiaries: In the same form, select which subsidiaries can use this account, and optionally check “Include Children” to auto-include sub-subsidiaries [44].

- Save: Only intercompany transactions can post to these accounts; once balances exist, the elimination box cannot be unchecked [45].

After this, any invoice from Subsidiary B (our “customer” in A’s books) that is marked intercompany will use A’s Intercompany Receivable account, and any vendor bill in Subsidiary B (for that invoice) will use B’s Intercompany Payable account. These accounts accumulate due-from-other and due-to-other balances, respectively [5] (Source: timdietrich.me).

Important: NetSuite will prevent mixing non-intercompany activity with these accounts. The help guide warns that existing AR/AP accounts with prior non-IC balances cannot be converted to intercompany use [46]. In practice this means one should never repurpose a legacy AR account for new IC transactions; otherwise unbalanced history remains. Also, if an existing IC account is created from a previously used account, old transactions must be manually edited to be marked for elimination [47]. For this reason, consultants usually advise creating brand-new AR/AP accounts for IC purposes [43].

Other Elimination Accounts (Income, Expense, COGS)

Aside from AR and AP, intercompany processes involve income and expense accounts. When one subsidiary records revenue from selling to another, the related cost of goods sold or expense is recorded by the buyer. In consolidated reporting, these also must be eliminated. NetSuite requires that all income, expense (and COGS) accounts used in intercompany transactions be flagged for elimination. This includes any item income, item expense, or COGS accounts underlying the intercompany items. As the Oracle documentation states, if you create a new income or expense account, you can check “Eliminate Intercompany Transactions” so it participates in eliminations [48]. If you decide to repurpose an existing account, you should tick that box, but note that historical transactions won’t retroactively be tagged [47]. Table 1 (below) provides examples of typical intercompany elimination accounts:

| Account Name | Type | Eliminate IC? | Usage (notes) |

|---|---|---|---|

| Intercompany Receivable | Asset (AR) | Yes [5] | Used by each selling subsidiary to record amounts due from other group companies (intercompany sales). |

| Intercompany Payable | Liability (AP) | Yes [5] | Used by each buying subsidiary to record amounts due to other group companies (intercompany purchases). |

| Intercompany Sales (Revenue) | Income | Yes [49] | Used by a subsidiary to record revenue when it sells to another subsidiary; this revenue is eliminated at consolidation. |

| Intercompany Purchases / COGS | Expense | Yes [49] | Used by buying subsidiary as cost of goods sold or intercompany expense; eliminated against IC sales. |

| IC Interest Income | Income | Yes [50] | For interest revenue on intercompany loans. |

| IC Interest Expense | Expense | Yes [50] | For interest expense on intercompany loans. |

| IC Netting Clearing | Other Asset | (Auto-Gen) | Game: NetSuite creates this account for netting processes to offset netting settlements [51]. |

Table 1: Example Intercompany Elimination GL Accounts in NetSuite. Each should have the “Eliminate Intercompany Transactions” box checked. “Intercompany Receivable/Payable” accounts track balance-sheet obligations (due-from/due-to other subs) [5], while the others record P&L impact to be eliminated. The IC Netting Clearing account is automatically created by NetSuite for netting settlements [51].

_Admins are advised to configure these accounts before setting any preferences or transacting. The Intercompany Preferences page (Setup > Accounting > Preferences > Intercompany Preferences) requires them. There, you will specify defaults such as “Receivables Account” and “Payables Account” as created above [7]. Other required fields include a default intercompany Income account, Expense account, and (if using inventory) a COGS account [7]. NetSuite will prompt if any are missing. Notably, enabling the Intercompany Framework automatically generates the Netting Clearing account mentioned above [52].*

Due To/Due From Account Design Options

NetSuite administrators have flexibility in how they implement Due To/From accounts. A recent guide by Tim Dietrich outlines three common design options (Source: timdietrich.me):

-

Option A: Single Shared Accounts. Create one Intercompany Receivable (Due From) account and one Intercompany Payable (Due To) account for the entire organization. This simplifies the chart of accounts. However, you lose the ability to immediately see which subsidiary owes which amount. Reconciliation then depends on adding fields or saved searches to filter by “counterparty subsidiary.” This approach is simplest when the company has few related entities (Source: timdietrich.me).

-

Option B: Entity-Specific Accounts. Create a separate Due From/To pair for each subsidiary or entity combination. For example, “Due From – UK Subsidiary” and “Due To – UK Subsidiary.” This expands the COA but makes reconciliation straightforward: each account’s balance should go to zero on consolidation. A controller can directly pair each subsidiary’s receivable with the counterpart payable (Source: timdietrich.me). This is recommended for groups with a modest number of subsidiaries (e.g. 5 or fewer) (Source: timdietrich.me).

-

Option C: Single Clearing Account with Segmentation. Use one Intercompany Clearing account in conjunction with classification (e.g. Departments, Class, or a custom segment) to identify the counterparty. All intercompany entries post to this one account, but segments tag which other subsidiary they involve. This avoids account proliferation while still enabling reporting by segment. It is more complex to set up but can be effective for organizations with many subsidiary relationships (Source: timdietrich.me).

A practical table:

| Option | Implementation | Pros | Cons |

|---|---|---|---|

| A – Single Account | One “Due From – Intercompany” AR account and one “Due To – Intercompany” AP account for the entire organization. | Simplest COA (only 2 accounts). | Hard to see breakdown by subsidiary; requires saved searches or custom fields to reconcile by counterpart. |

| B – Entity-Specific | Create a separate Due From/To pair for each subsidiary (e.g. “Due From - SUB A”, “Due To - SUB A”, etc.). | Easy reconciliation – each $ balance is isolated. Clear audit trail. | Many accounts, complicating COA management. |

| C – Single w/ Tag | One clearing asset account, plus use Department/Class or a custom segment to tag the counterparty. | Minimal account count; still allows breakdown via segment. | More setup (classifications needed) and reliance on proper tagging on each transaction. |

These options each appear in practice. For small groups, entity-specific accounts (Option B) are often easiest (Source: timdietrich.me). For complex organizations, Option C can centralize the GL impact. Regardless of choice, the expectation remains that by consolidation time the net balance across all Due From accounts will equal the net of all Due To accounts (and thus eliminate to zero) (Source: timdietrich.me) [23].

Note: NetSuite’s internal processing (AIM) will handle elimination as long as all transaction lines are correctly marked “Intercompany” and the accounts are tagged for elimination. The choice of option affects primarily reporting and reconciliations, not the fundamental accounting mechanics.

Specialized Clearing Accounts

In addition to AR/AP-based Due To/From accounts, NetSuite may use intercompany clearing accounts in certain scenarios:

-

Time & Expense Feature: If the Intercompany Time and Expense feature is enabled (under Employees & Payroll > Timesheets, etc.), NetSuite automatically creates a special clearing account for cross-charging employee time or expenses between subsidiaries [11]. This clearing account (an Other Current Asset) is used to offset transfers. For example, if a Canadian employee charges $3,395 for a UK client, NetSuite posts entries debiting “Intercompany Clearing – CAD” in Canada and crediting expense, while crediting the same clearing account in the UK and debiting UK expense [53]. The net effect is that each subsidiary’s books balance out after the cross-charge. This mechanism ensures that exchange-rate conversion (Canadian to UK currency) is handled cleanly. Administrators cannot delete or rename this system-generated Clearing account [54].

-

Netting Process: When using NetSuite’s intercompany netting workbench (Transactions > Intercompany > Netting), the system creates an “IC Netting Clearing” account (Other Asset) automatically [52]. This account temporarily holds the offsetting entry of consolidated settlement transactions between subsidiaries. For example, if netting determines Subsidiary A will pay Subsidiary B $10,000 (one net payment instead of multiple offsets), NetSuite will debit A’s cash and credit B’s cash through this clearing account to net to zero [51] [19].

-

Transfer Orders: In inventory transfers between subsidiaries, NetSuite may use “clearing” offset accounts for intratransfer pricing adjustments [55]. For instance, a NetSuite development note explains that when receiving an intercompany transfer order, the system uses an ‘Offset account’ on the item receipt, which by default is the intercompany clearing account. This ensures the COGS impact balances out.

In summary, intercompany clearing accounts in NetSuite refer to system-generated accounts that NetSuite uses behind the scenes to balance intercompany expenses or netting settlements [11] [51]. Administrators should generally not alter these accounts, but be aware of them for reporting and audit (they will appear with balances equalizing internal cross-charges). The primary user-defined accounts remain the AR/AP Due From/To and related income/expense accounts, as outlined above.

Intercompany Preferences and Global Settings

Before using intercompany accounts, NetSuite administrators must set up various preferences:

-

Company and Subsidiary Setup: Under Setup > Company > Subsidiaries, define each legal entity. Ensure functional currency and taxation settings are correct. Create elimination subsidiaries (dummy entities under each parent) which will be used to post consolidation entries (Source: timdietrich.me).

-

Intercompany Preferences: Once accounts exist, go to Setup > Accounting > Preferences > Intercompany Preferences. On the Accounting subtab, specify your default intercompany accounts [7]. Required fields include:

- Receivables Account: choose the AR account created as “Intercompany Receivable” (Due From) [7].

- Payables Account: (if using the Framework) select the payable account “Intercompany Payable” (Due To) [7].

- Income Account: an intercompany income account (one of the accounts for intercompany revenue) [56].

- Expense Account: an intercompany expense account (for intercompany costs) [56].

- COGS Account: for Automated IC Management (cost of goods sold) [57].

- Deferred Revenue Account: if you auto-post deferred revenue on item records [57].

- Netting Clearing Account: This field will be auto-populated by NetSuite (do not change it); it corresponds to the system-generated netting clearing account [52].

If you have multi-currency intercompany transactions, set the default trade currency for cross-charges on this page―commonly the currency each subsidiary transacts in with the other [58]. Also, specify default markup rates for cost-plus transfers (cross charges), and how to group classifications for netting [59] [60]. The “Allow Per-Line Classification for Netting Settlement” option ensures that if the netted transactions had various departments, classes, or custom segments, the corresponding netting journal entries will group by those dimensions [61].

-

Representing Entities: On the Intercompany Entities subtab of Preferences, you can enable automatic creation of “representing” customers and vendors for each subsidiary [62]. These are placeholder records that let one subsidiary automatically use the identity of another for intercompany sales/purchases. For example, if UK Subsidiary sells to US Subsidiary, NS might create a US “representing customer” that UK uses in the transaction. Enabling this may require the Multi-Subsidiary Customer/Vendor feature and can speed up intercompany order processing.

After configuring preferences, always double-check the System Notes to verify settings took effect [63].

Example: In a typical setup, Subsidiary A might have:

- Intercompany Receivable (AR) as its default Receivables account.

- IC Sales (Income) as its default Income account.

Subsidiary B might have its own "Intercompany Receivable" and “IC Sales” accounts (if using Option B above), all marked with “Eliminate IC.” Meanwhile both would have the same global IC Payable and IC Expense accounts as defaults (if the preferences are at the parent level). By checking these defaults, NetSuite knows which accounts to use when automatically creating cross-charges or elimination journal entries during eliminations [7] [38].

Intercompany Transactions and Accounting Workflow

With the framework enabled and accounts in place, actual intercompany transactions can be processed.

Cross-Subsidiary Transactions in NetSuite

NetSuite supports several types of intercompany transactions:

-

Intercompany Sales Orders (and Purchase Orders): A user in Subsidiary A can create a sales order (SO) that designates a customer in Subsidiary B. With Automated IC Management, NetSuite will automatically generate a corresponding intercompany purchase order (PO) in Subsidiary B for that transaction [37]. When fulfilled, the seller (A) bills its internal “customer” using the Intercompany Receivable account, and the buyer (B) records a bill on the Intercompany Payable account. Fulfillments, receipts, and invoicing produce paired entries on each side.

-

Intercompany Transfer Orders: For inventory exchanges, one entity can create an Intercompany Transfer Order to send goods to another subsidiary. When the receiving subsidiary creates an item receipt, it will often use an item with costing that posts to a clearing account. Recent notes indicate NetSuite uses an “offset/cost of goods sold” account during transfer receipts that plays a role similar to clearing [55].

-

Intercompany Journal Entries (Advanced): For misc allocations, OneWorld allows Advanced Intercompany Journal Entries, where a single JE can span multiple subsidiaries (Source: timdietrich.me). NetSuite will automatically balance them by posting offsetting lines. For example, a $60,000 IT expense allocation might debit various subsidiaries’ expense accounts and credit the cost center’s “Intercompany Income” account; the system then creates the corresponding Due From entries on the provider’s side across three lines (Source: timdietrich.me).

-

Intercompany Loans and Other Charges: Loans of cash or reimbursements can be handled through standard journal entries using the intercompany AR/AP accounts. Similarly, shared service charges (e.g. management fees) can use AR/AP or an intercompany income/expense account and be eliminated later [64] (Source: timdietrich.me).

-

Foreign Currency Handling: If the transaction involves currency conversion, NetSuite will translate amounts using the applicable exchange rate type (set in preferences). The intercompany AR/AP balances remain distinct, although NS may generate exchange gain/loss entries if needed. Notably, FX gains or losses on Due From/To accounts are often left unreconciled until consolidation, when a net translation adjustment (CTA) is recorded [20].

The Intercompany Elimination Process

At month-end or quarter-end close, intercompany eliminations are applied:

-

Automated Elimination (AIM): If Automated Intercompany Management is enabled, NetSuite’s close process will automatically create elimination journal entries for matched intercompany transactions [38]. For example, it will debit revenue (seller) and credit COGS (buyer) for each intercompany sale; debit one subsidiary’s Intercompany Receivable and credit the partner’s Intercompany Payable for each matched invoice pair [38] (Source: timdietrich.me). These entries effectively zero out the internal transactions in an elimination subsidiary. Because AR/AP accounts were flagged, NetSuite also knows to reverse the elimination entries in the next period automatically [65].

-

Manual Elimination: If AIM is not used, or for adjustments beyond sales/purchases (e.g. management fees), accountants may need to create Manual Elimination Journals. Typically, these are posted in an elimination subsidiary (one created under the parent specifically for consolidation entries). For instance, to eliminate intercompany interest, one would debit interest revenue (IC Income) and credit interest expense across the two subsidiaries (Source: timdietrich.me). Once NetSuite runs the period close checklist’s “Intercompany Elimination” task, the system marks and reverses these appropriately。

-

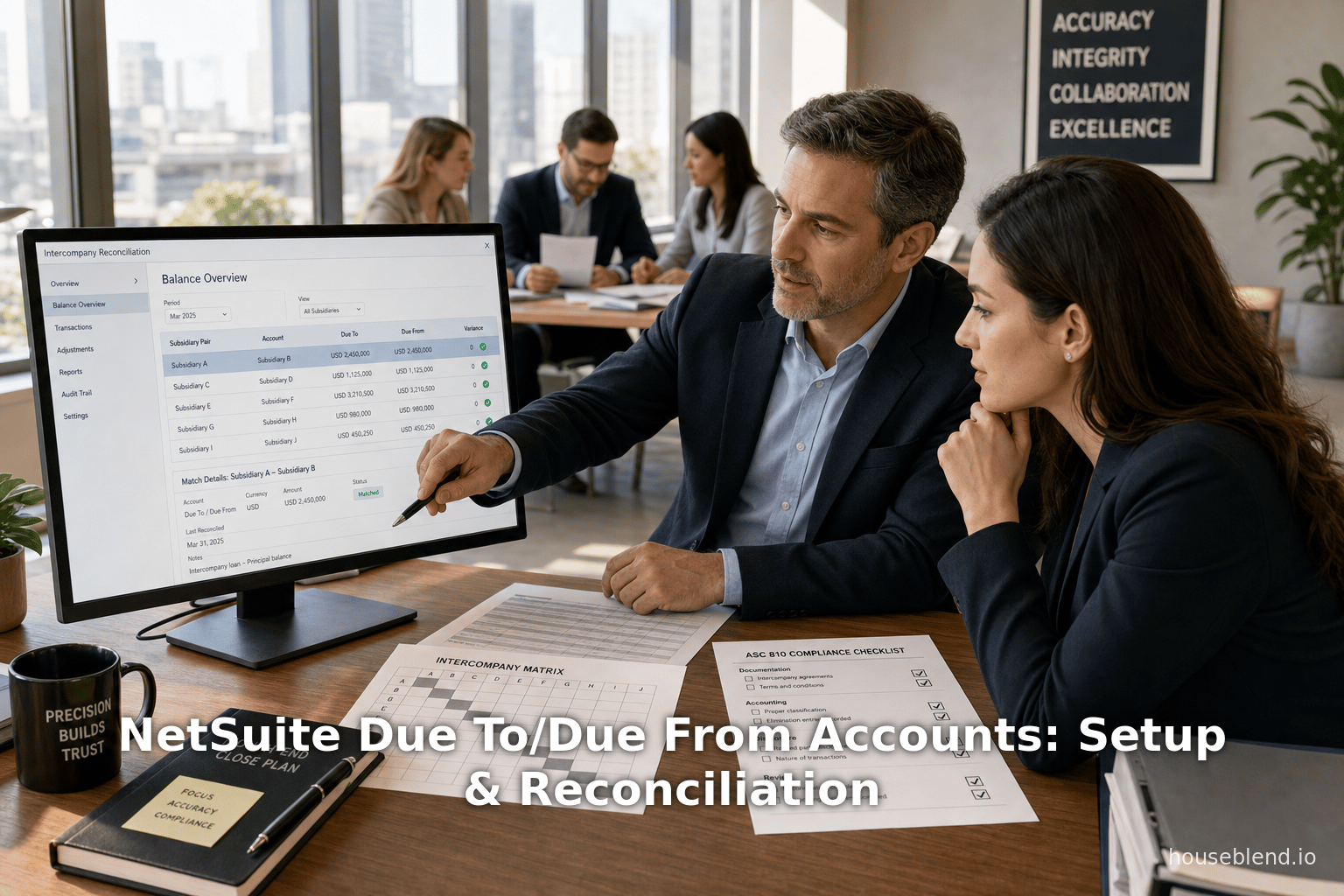

Intercompany Reconciliation Report: Prior to elimination, it is highly recommended to run the Intercompany Reconciliation report (Transactions > Management > Intercompany Reconciliation Report) [15]. This report scans all intercompany transactions (IC SO/PO, fulfillments, invoices, etc.) and highlights any that lack a perfect match in the counterparty’s books [66]. For example, if Subsidiary A has a $5,000 intercompany invoice to B, but B’s corresponding bill is only $4,995 (due to rounding or FX), the report will flag it. Administrators can drill into the report and open the source transactions to make corrections before running the elimination. NetSuite documentation explicitly advises “Run the Intercompany Reconciliation report before intercompany elimination” to catch these issues [15].

-

Open Balances Overview: The Balance Overview page (Lists > Intercompany Automation > Balance Overview) provides a quick check of unreconciled open AR and AP by subsidiary pair [13]. It shows the total due-to and due-from balances side-by-side, filtered by currency and subsidiary. This tool is useful for monitoring moves and seeing if payables and receivables truly net to zero (or if significant residuals remain).

Data from an Example NetSuite Entry

As an illustration of how an intercompany transaction appears in NetSuite GL entries, consider an intercompany sales invoice: Subsidiary A sells $1,000 worth of goods to Subsidiary B, with internal pricing. Assuming USD functional currency for both, NetSuite would record:

- Subsidiary A (Seller): Debit Intercompany Receivable $1,000; Credit Intercompany Sales (Income) $1,000.

- Subsidiary B (Buyer): Debit Intercompany Purchases (COGS/Expense) $1,000; Credit Intercompany Payable $1,000.

After elimination, NetSuite will generate an elimination journal: Debit Intercompany Sales $1,000 and Credit Intercompany Purchases $1,000, leaving both subsidiaries with zero net effect post-consolidation. If currency conversion were involved, the clearing and rounding would be handled via the appropriate clearing accounts, ensuring both subsidiary books remained balanced [53] [12].

Due To/From Reconciliation in Practice

Despite NetSuite’s automation, intercompany reconciliation remains an active task for controllers. The process typically involves:

-

Running Reports: Use the NetSuite Intercompany Reconciliation report [15] and/or saved searches to list open intercompany invoices, bills, payments, and any unmatched items. The entry-level detail from these reports helps pinpoint discrepancies. NetSuite support materials suggest routine use of this report for each close.

-

Saved Searches and Analysis: Many finance teams create saved searches to aggregate Due From/To balances by subsidiary. However, administrators have noted a limitation: the Due To/From Subsidiary field is not available in standard transaction saved searches unless the Central Purchasing & Billing feature is enabled [67]. This is a known system restriction logged in NetSuite’s enhancement system [67]. If that feature is off, analysts must use workarounds (e.g. saved search on intercompany customers/vendors) to filter by counterparty subsidiary.

-

Investigating Variances: Differences flagged in reports often fall into categories identified by practitioners. Timing issues (one entity hasn’t posted a late invoice), exchange rate mismatches, or missing transaction scenarios (one side forgot to bill) account for most variances [30] [29]. For example, MultientityAccounting.com notes that without a strict intercompany posting policy and synchronized calendars, “the ledgers are permanently out of sync for that period” [30]. Teams will reconcile each mismatch by confirming the correct accounting date or FX rate. If one side genuinely missed a record, the other entity might reverse and re-enter, or simply wait until a reciprocal entry is recorded.

-

Adjustment Entries: After investigation, controllers post adjusting journal entries as needed. For example, if Subsidiary B recorded $950 (due to using a prior quarter’s rate on a EUR invoice) while A recorded $1,000, an adjustment to one account (often the receivable/payable) will bring them into alignment [31] [17]. NetSuite’s intercompany journal capabilities make this straightforward: one subsidiary posts (ib) and NS automatically books the offset in its partner when “Eliminate” is checked on the journal.

-

Sign-off and Audit: Once balances reconcile, official sign-off by each entity’s controller is obtained. This step is often enforced under SOX/ICFR: a manual reconciliation without formal review is a control weakness . The reconciled AF balances and any journal adjustments are documented and retained as audit evidence.

Exemplifying the magnitude: reports and expert sources indicate intercompany reconciliation can drastically shorten with good systems. For instance, one estimate suggests firms save up to 2–5 days per month on close by automating intercompany matching [68]. Treasury analysis notes that even factoring import entry costs, intercompany flows (especially in multi-currency contexts) can dominate a company's cash activity, making reconciliation automation essential [18] [69]. Tools like NetSuite’s balance overview, combined with data from integrated payment platforms, enable treasurers to “lock in FX rates in larger blocks” and reduce foreign exchange slippage [18] [69].

In summary, while the glue of reconciliation remains a human-intensive process for now, NetSuite provides strong support: specialized reports, automated matching for many transaction types, and the ability to trace each intercompany transaction end-to-end [66] [15]. Companies complement these with robust policies (e.g. fixed intercompany pricing rules) and emerging treasury systems to drive as much automation as possible [18] [70].

Data Analysis and Research Findings

Studies and industry reports quantify the impact of effective intercompany processes. For example:

-

High Volume of Intercompany Flows: Salmon Software’s research (cited by NetSuite consultants) shows that in many multinationals up to 70% of internal trade is intra-group [18]. Such high volumes mean inefficiencies multiply if each payment is settled individually.

-

Netting Benefits: Organizations that implement netting (centralized offsetting and settlement) can reduce intercompany payment transactions by up to 90% [18] [19]. The Houseblend analysis cites an example where netting reduced “dozens of interco wires down to a handful of net payments” [19].

-

Cost Savings: Industry analyses (e.g. Treasury management guides) estimate that netting and automation cut financial costs—bank fees, FX spreads, manpower—for large groups significantly [19] [71]. One source finds that by locking in larger net amounts, companies achieve better FX rates and far fewer bank charges [18] [19].

-

Close-Time Reduction: MultientityAccounting.com cites that structured intercompany reconciliation workflows can reduce the reconciliation cycle by 2–5 days per month [68]. In quantitative terms, if a finance team can shave off even 20–30% of close time, this accelerates reporting and frees up resources for analysis.

-

Risk Mitigation: From a control perspective, unresolved intercompany imbalances are a known audit risk. A NetSuite assessment guide notes that uncorrected imbalances can constitute a material weakness under Sarbanes-Oxley (Source: timdietrich.me) . By contrast, a streamlined intercompany process today is seen as a mark of mature corporate finance.

Altogether, the data and expert consensus indicate that while setting up Due To/From accounts and reconciliation processes requires effort, the benefits far outweigh the costs: fewer manual transactions, significant cost savings, reduced FX exposure, and more timely consolidated reporting [18] [19].

Case Studies and Examples

While proprietary details are seldom public, we can outline typical scenarios:

-

Growing Multi-National: A U.S.-based tech company expanding into Europe might initially manage intercompany via spreadsheets. When revenue grew, they encountered large arbitrage (currency) losses and delays. After implementing NetSuite OneWorld, enabling Automated IC Management and setting up dedicated Due From/To accounts, they reported that monthly closes now included automatic elimination entries and reconciliation that formerly took a week could be done in hours. (Baker Tilly notes similar benefits for one client, leading to “multicompany consolidation and elimination” without error-prone Excel files [72].)

-

Manufacturing Conglomerate: An electronics manufacturer with plants in the US and Asia uses NetSuite. Its finance team set up entity-specific intercompany AR/AP accounts (Option B) for clarity. Every month, they run the Intercompany Reconciliation report and discover only trivial differences (often due to rounding). They netIZE$10M of flows and make 2 adjusting entries, compared to 100+ wire transfers if done bilaterally. The treasury manager cites “improved cash visibility and streamlined controls” as key outcomes [35] [19].

-

Service Company with Shared Costs: A consulting firm with shared services (IT, HR) allocates costs to subsidiaries. They created a single IC clearing account plus custom segments for each subsidiary to track allocations. This allowed the back office to simply post one AC transaction and let NS generate all balancing entries under the hood. The chief accountant estimates 50% reduction in reconciliation effort, and the CFO remarks on cleaner P&L elimination on consolidation.

These examples reflect a trend: firms that leverage NetSuite’s intercompany features report drastically less reconciliation overhead and clearer internal auditing trails [19] (Source: timdietrich.me). In a recent NetSuite survey, nearly all firms said their IC accounts now reside in the ERP rather than in spreadsheets, and most use dedicated intercompany accounts per subsidiary [38] (Source: timdietrich.me).

Implications and Future Directions

Control and Compliance Implications

Proper configuration of Due To/From accounts in NetSuite has major controls implications. Misconfigurations can violate GAAP/IFRS, while robust setups facilitate audits. For companies under SOX or similar regimes, intercompany processes are a significant internal control area. Auditors now expect systematic reconciliation and documentation of all due-to/from balances [73] (Source: timdietrich.me). NetSuite supports auditability by tying every balancing entry to a transaction and by logging all changes (users can view “System Notes” for who changed an intercompany preference or account) [63].

There are also tax and regulatory considerations. Transfer pricing rules require that intercompany transactions be at arm’s length, but from an accounting standpoint, all internal mark-ups will be eliminated. All the while, local tax authorities often scrutinize intercompany loans, funding and service charges; NetSuite’s transparency aids in justifying registered due-to/from balances. Some jurisdictions even require companies to maintain Due To/From accounts separately on statutory books (e.g. Japan’s tax law has specific rules) – a task streamlined by using NetSuite’s dedicated accounts with classification [74].

Technology and Process Innovations

Looking forward, continued automation is likely. Many organizations already use NetSuite SuiteApps or external tools to enhance intercompany reconciliation. For example, the Houseblend report mentions third-party solutions like BlackLine that specialize in matching and reconciliation, which can integrate with NetSuite sources [21]. These tools may employ artificial intelligence to suggest matches or flag outliers, further reducing manual work.

Emerging technology may also play a role. Blockchain-based intercompany settlement is a concept some multinationals are exploring: by recording each intercompany invoice and payment on a shared ledger, subsidiaries could theoretically reconcile in real-time [21]. Although this is not yet mainstream, finance leaders are paying attention, as blockchain could provide immutable audit trails for intercompany flows. Similarly, AI-driven enhancements (natural language processing, anomaly detection) could soon assist in the reconciliation steps described above.

Future Requirements for NetSuite

Looking at NetSuite’s product roadmap and community feedback, we identify areas of future development:

-

Improved Reporting Fields: As noted, fields like “Due To Subsidiary” are hard to access in standard saved searches [67]. An enhancement request exists to expose more intercompany metadata for reporting. A future release could open up these fields or provide a standard DueTo/From report export.

-

Stronger Multi-Book Support: For companies using multiple accounting books, NetSuite already supports running the Intercompany Reconciliation report per book [75]. There may be further enhancements to handle differences between books (e.g. IFRS vs local GAAP) in intercompany balances.

-

Dynamic Elimination: Additional flexibility in elimination timing (e.g. allowing mid-month or real-time elimination for certain entries) could improve reporting accuracy in fast-moving environments.

-

Centralized Netting Workbench: NetSuite has a Balance Overview and Netting workbench. Future enhancements might allow automatic recommendations of netting matches or integration with treasury for auto-liquidation of net positions.

Regardless, the core architecture is solid. As NetSuite’s own documentation emphasizes, once the Intercompany Framework is enabled and properly configured, the system “automatically generates elimination journal entries” and can produce consolidated statements [38] (Source: timdietrich.me). The focus should be on maintaining correct setup and leveraging the tools it provides, augmented by disciplined processes.

Overall, the trajectory is toward ever-greater automation. A streamlined, system-driven intercompany clearing and reconciliation process is becoming a hallmark of modern finance departments. This yields both tangible savings and intangible benefits like better strategic insight into inter-subsidiary cash flows [35] [19].

Conclusion

Accurate management of Due To and Due From accounts is fundamental to multi-entity financial control. In NetSuite OneWorld, this means carefully setting up intercompany AR/AP and related accounts, enabling the Intercompany Framework and Automated IC Management, and diligently reconciling each balance before elimination.

Our examination has shown that NetSuite provides robust mechanisms to support these tasks: from system-generated Intercompany Clearing accounts [11] to automatic elimination entries [38] to reconciliation reports [15]. By following best practices—using dedicated intercompany accounts [43], defining default preferences [7], and leveraging tools like the Netting Workbench—organizations can ensure their Due To/From balances always mirror each other. As one expert sums up, if properly configured NetSuite “automate[s] much of this complexity” of intercompany matching and elimination (Source: timdietrich.me).

Failure to do so carries risks: unreconciled Due To/From balances can trigger audit flags and inaccurate consolidated statements [2] (Source: timdietrich.me). Conversely, getting it right leads to major efficiency gains. Evidence is clear that processes like netting and automation yield dramatic reductions in payment volume and manual effort [18] [19]. The ultimate result is faster closes, lower costs, and enhanced visibility of intercompany cash flows – outcomes that strategic finance leadership values highly [35] [19].

Looking ahead, finance teams should continue to refine their intercompany models. This includes aligning charts of accounts, enforcing consistent policies, and exploring advanced tools (perhaps AI or blockchain) to further cut manual steps [21] [76]. However, the foundation is clear: by correctly using Due To/From accounts and NetSuite’s intercompany features as designed, organizations can significantly simplify what once was a “labor-intensive process prone to errors” [77] [78].

In conclusion, this report emphasizes that Due To / Due From accounts in NetSuite are not mere book-keeping niceties but the linchpins of intercompany finance. When set up properly and actively managed, they ensure compliance with consolidation standards [2] and enable leaner, more transparent financial operations. The key takeaway for CFOs and controllers is: invest the time to configure and reconcile these accounts up front, and you unlock major dividends in efficiency and control.

References

- Oracle NetSuite Documentation: Intercompany Accounts [79]; Accounts Receivable and Accounts Payable (Intercompany) [10]; Intercompany Clearing Account [11]; Automated Intercompany Management Overview [4]; Intercompany Reconciliation Report [14]; Defining Intercompany Preferences [7]; Creating Intercompany Elimination Accounts [42].

- Houseblend (NetSuite Consultants): NetSuite Intercompany Netting: Setup & Configuration [18] [19].

- Tim Dietrich (NetSuite blogger): NetSuite Intercompany Transactions and Eliminations (Source: timdietrich.me) (Source: timdietrich.me).

- LegalClarity: Due To and Due From Intercompany Balances [1] [78]; How to Eliminate Due To and Due From Balances [80] [22].

- MultientityAccounting.com: What Is Intercompany Reconciliation? A Complete Guide [81] [16] [2].

- Baker Tilly (Case Study): ERP supports global growth [72].

- Salmon Software (intercompany flow study, as cited in [18] [19]).

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.