Oracle Q4 FY2026 Earnings: NetSuite ERP & AI Analysis

Oracle Q4 FY2026 Earnings Preview: NetSuite Cloud ERP Trajectory & AI Revenue Signals

Executive Summary

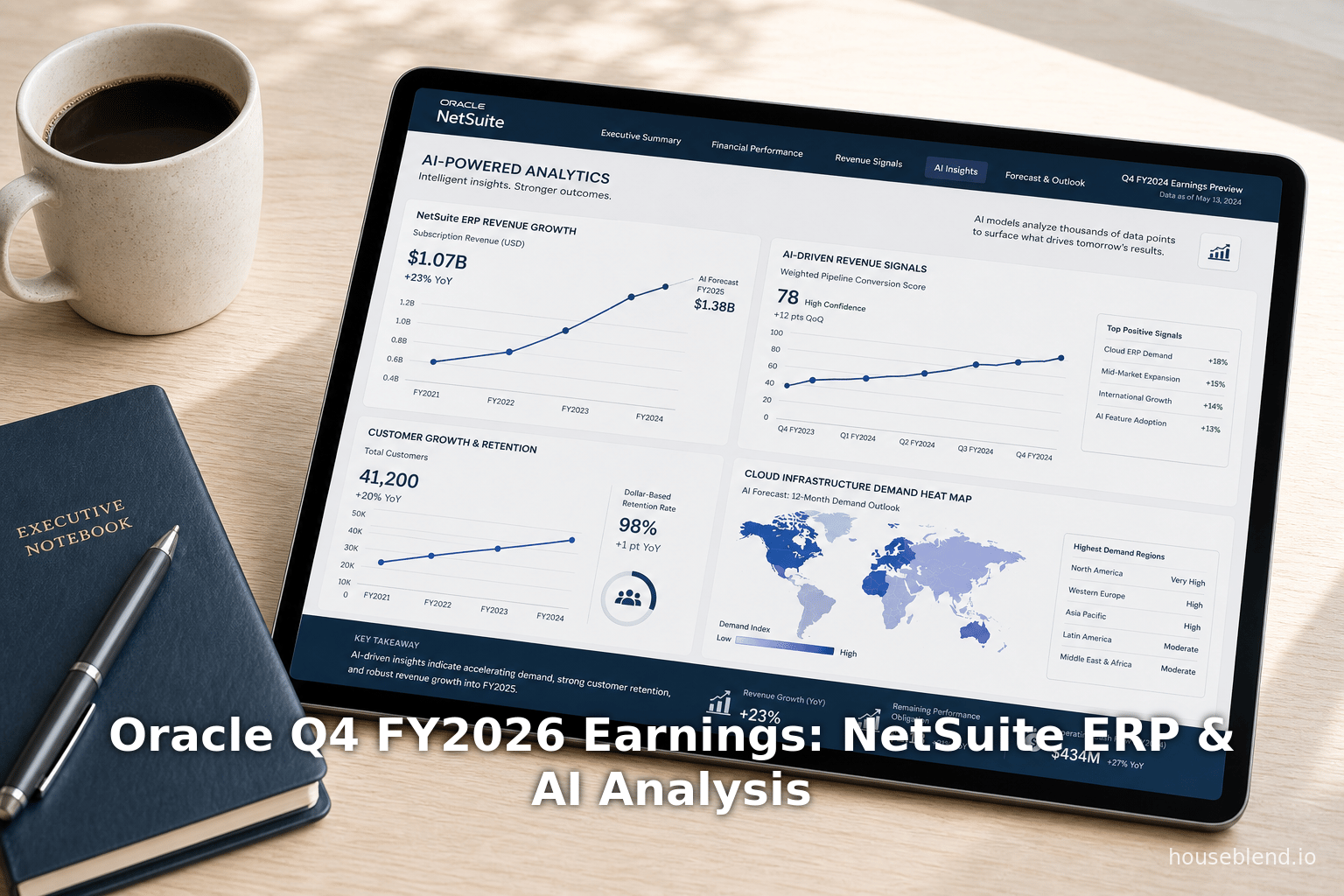

This report provides an in-depth analysis of Oracle Corporation’s expected fiscal fourth quarter (Q4) 2026 earnings, with a particular focus on the performance of NetSuite cloud ERP and Oracle’s emerging AI-driven revenue streams. Oracle has undergone a major transformation into a cloud-centric enterprise under CEO Safra Catz and CTO Larry Ellison. Fiscal year (FY) 2026 has so far demonstrated exceptional growth for Oracle: total revenue and cloud revenue have expanded at double-digit rates each quarter, driven by surging demand for cloud infrastructure and applications. NetSuite – Oracle’s founder of cloud ERP – continues to grow in the mid-to-high teens percentage range year-over-year (YoY), reflecting steady adoption of cloud ERP among mid-market and international customers [1] [2]. Meanwhile, Oracle’s investments in artificial intelligence (AI) are beginning to yield clear revenue signals: its cloud infrastructure (OCI) is being used to train and serve leading generative AI models, and Oracle is embedding AI/ML features into both its applications and its infrastructure products [3] [4].

By Q3 FY2026 (quarter ended February 2026), Oracle reported cloud revenues of $8.9 billion (up 44% YoY) and stacked a record ~$553 billion backlog of contracted cloud commitments [5] [6]. NetSuite SaaS revenue was $1.1 billion in Q3 (up ~14% YoY) [7], on an annualized run rate of about $4.4 billion, growing faster than many legacy on-premises ERP vendors. Oracle’s executive commentary has signaled continued acceleration: Salesforce-competitive “agentic” AI apps were launched, and partnerships (e.g. with Google’s Gemini AI, X Corp’s Grok) broaden Oracle’s AI offerings [8] [9].

This preview synthesizes these trends to forecast Q4 FY2026. We expect Oracle to continue delivering strong cloud growth (with infrastructure growth likely above 70% YoY) and solid cloud applications growth (mid-teens) [10] [3]. NetSuite Cloud ERP should again grow in the mid-to-high teens, as international expansion and product upgrades sustain its momentum [1] [7]. At the same time, Oracle’s “AI revenue signals” – exemplified by accelerating OCI usage by AI-driven customers and new AI-driven product bookings – suggest that a meaningful portion of the cloud growth is being fueled by enterprise AI adoption [3] [4]. NetSuite is set to benefit indirectly from Oracle’s AI push (e.g. AI-powered analytics and agentic features) as more customers upgrade to modern cloud suites.

Overall, we anticipate Oracle to beat or meet guidance in Q4 FY2026, with cloud revenue again a standout. Key metrics to watch include NetSuite bookings, OCI last-mile adoption by AI customers, and any updated guidance for FY2027. This report reviews Oracle’s background and strategy, analyzes historical Q1–Q3 FY2026 performance (including NetSuite metrics), examines AI initiatives and their revenue implications, presents illustrative case studies (e.g. notable NetSuite and AI customers), and discusses the outlook and broader industry context. All claims are supported by official results, expert commentary, and market data.

Introduction and Background

Oracle Corporation is a leading provider of enterprise software and cloud services. Founded in 1977 by Larry Ellison (now CTO) and Safra Catz (CEO), Oracle long dominated on-premises database and enterprise resource planning (ERP) software. In the past decade, Oracle has aggressively transitioned to cloud: it now offers Oracle Cloud Infrastructure (OCI) (IaaS/PaaS), Oracle Fusion Cloud Applications (SaaS for ERP, HCM, CX, SCM, etc.), and the Oracle Autonomous Database. Oracle also acquired NetSuite in 2016 for $9.3 billion, making NetSuite (a pioneer of cloud ERP) a wholly owned subsidiary under the Oracle Cloud Applications division [1] [11]. Today Oracle touts itself as “not only the world’s largest cloud application company, but also one of the world’s largest cloud infrastructure companies” [10], with a global customer base spanning tens of thousands of organizations across industries.

Oracle’s Fiscal Year and Recent Trends. Oracle’s fiscal year runs from June 1 to May 31. Fiscal 2026 (ending May 2026) has been characterized by accelerating growth, driven largely by cloud services. As of Q3 FY2026 (ends Feb 28, 2026), Oracle reported year-to-date revenue of about $46 billion, up significantly from $41 billion a year prior. Meanwhile, cloud services and license support revenue (the sum of SaaS and cloud IaaS plus database at AWS/Azure etc.) has grown at ~30–50% YoY each quarter [5] [12]. This performance follows a record Q4 FY2025 (ended May 2025) in which Oracle first broke double-digit growth in cloud even as total revenue grew ~11% [1] [13]. Importantly, Oracle’s remaining performance obligations (RPO) — a measure of contracted future revenue — exploded from $138 billion at Q4 FY2025 to $553 billion by Q3 FY2026 [14] [6], reflecting large multi-year cloud contracts (often expected to drive heavy OCIconsumption). CEO Catz has noted that much of the new RPO comes from “multi-billion-dollar contracts” with hyperscalers and large enterprises [10] [15].

NetSuite Cloud ERP. NetSuite, acquired by Oracle in 2016, provides cloud-based ERP, financials, CRM and supply chain modules, primarily targeting mid-size and subsidiary companies. As Oracle’s SaaS offerings grew, NetSuite became a distinct reportable segment (often aggregated with Fusion Cloud ERP under “Applications”). Oracle has emphasized NetSuite’s success: by FY2025 NetSuite had over $3 billion in annual revenue run rate and ~40,000 customers globally. NetSuite operates in a highly competitive ERP market alongside SAP, Microsoft, Workday, Infor, etc. Industry sources estimate Oracle (Fusion+NetSuite) holds roughly 11–13% global ERP market share [16] (see ERP Market Shares 2026). Notably, embedded Oracle commentary claims NetSuite grew ~18% YoY in Q4 FY2025 [1] and high-single-digit to mid-teens in subsequent quarters (16% in Q1, 13% in Q2, 14% in Q3 of FY2026 [2] [17] [7]). Oracle’s leadership asserts that accelerating AI and automation (e.g. “agentic” AI features) will further drive customers to Fusion/NetSuite rather than fragmented stacks [18] [19].

AI Strategy and Oracle. In FY2026 management frequently highlighted AI as a key growth driver. Oracle has over 200 planned cloud regions worldwide and is building hundreds of multicloud datacenters to embed specialty hardware and AI capabilities [20] [21]. Oracle’s investment includes autonomous software (Oracle Autonomous Database, Autonomous Linux) that uses AI to optimize infrastructure, plus the Oracle Cloud Infrastructure Generative AI service (launched 2023) offering managed LLMs and AI agents. At “Oracle AI World” events in 2025–2026, Oracle unveiled dozens of new AI-powered features, including Fusion Agentic Applications (enterprise apps built from coordinated AI agents) [8]. Oracle has also partnered broadly: for example, in August 2025 it agreed with Google to integrate Google’s Gemini models into OCI and Oracle’s own app stack [4], and in mid-2025 Oracle added Elon Musk’s XAI “Grok” models to its OCI generative AI catalog [9]. Tech industry analysts note Oracle’s strategy is multi-faceted: “partnering with leading AI innovators” so that “every indication... is focused on customers and less on competitors” [22] [23]. In summary, Oracle’s strategy fuses its traditional strength in databases and enterprise suites with a vigorous push into AI infrastructure and new AI-driven products, creating multiple potential revenue streams in the emerging AI cycle.

This report builds on that context to analyze the current Q4 FY2026 earnings outlook. We draw on Oracle’s official quarterly results and investor releases from FY2025–FY2026, management commentary, market analyses, and industry data to assess NetSuite’s trajectory and Oracle’s AI-related revenues. We include tables summarizing recent results, and case studies illustrating customer use of Oracle’s ERP and AI offerings. All data points are cited to credible sources (press releases, transcripts, analyst and news reports) to provide a rigorous, detailed preview of what to expect in Oracle’s Q4 FY2026.

Oracle FY2026 Business Review (Q1–Q3)

We begin by reviewing key Oracle performance trends through Q3 FY2026 (quarter ended Feb 28, 2026). These set the stage for Q4 and illustrate the current growth drivers.

Q1 FY2026 (August–Oct 2025). Oracle reported Q1 FY2026 revenues of $14.9 billion, up 12% YoY [24]. Cloud revenues were $7.2 billion (+28%, reflecting very strong IaaS growth), while legacy “on-premise” software revenues declined slightly [24]. Oracle’s Cloud Infrastructure (IaaS/PaaS) revenue was $3.3 billion (+55%) [25] and Cloud Application (SaaS) revenue $3.8 billion (+11%) [25]. Oracle’s Fusion Cloud ERP segment earned $1.0 billion (+17%), and NetSuite Cloud ERP also $1.0 billion (+16%) [2] (see Table 1). The RPO backlog surged to $455 billion (a 359% YoY jump) as Oracle signed several mega-deals [26]. Safra Catz highlighted “an astonishing quarter” with RPO up 359% due to “multi-billion-dollar customers” [27]. Notably, Fortunes of AI: OCI demand (IaaS) was cited as building rapidly, prompting Oracle to raise its full-year cloud IaaS guidance to $18 billion (≈77% YoY) [28].

Q2 FY2026 (Nov 2025–Jan 2026). Q2 FY2026 total revenue was $16.1 billion (up 14% YoY) [12]. Cloud revenues jumped 34% to $8.0 billion, driven by IaaS up 68% (to $4.1 billion) and SaaS up 11% (to $3.9 billion) [29]. Within applications, Fusion Cloud ERP was $1.1 billion (+18%), and NetSuite was $1.0 billion (+13%) [17]. Oracle’s RPO climbed to $523 billion (+438% YoY) [12]. Management emphasized record cloud bookings (including deals with Meta and NVIDIA), positioning FY2026 for “dramatically higher” growth [15]. CFO Doug Kehring noted Q2 non-GAAP EPS surged (up 54%) partly due to a one-time gain (sale of Ampere) [30], but underlying cloud operating margins remained healthy. Larry Ellison announced a new “chip neutrality” policy, signalling that OCI will compute on diverse future AI accelerators [31]. The quarter underscored Oracle’s AI pivot: Catz and CEO Mike Sicilia spoke of Oracle embedding AI across software and cloud, enabling automation in finance, healthcare, banking, etc. [32].

Q3 FY2026 (Feb 2026). Q3 FY2026 was an “exceptional quarter” [33]. Total revenue reached $17.2 billion, up 22% YoY (18% in constant currency) [5]. Cloud revenue soared 44% YoY to $8.9 billion (41% constant) [5]. Breaking that down, OCI (IaaS) revenue was $4.9 billion (+84% YoY) [34], and SaaS was $4.0 billion (+13%) [7]. Fusion Cloud ERP was $1.1 billion (+17%) and NetSuite Cloud ERP $1.1 billion (+14% in USD, 11% constant) [7] [7]. This marked Oracle’s first quarter in over 15 years where both total revenue and non-GAAP EPS grew ≥20% YoY [33]. Oracle executives emphasized that existing cloud “run rates” were very high – e.g. annualized Fusion apps revenue hit $16.1 billion [35]. Oracle also noted that Q3 RPO reached $553 billion (+325% YoY) [6]. Management commentary again spotlighted AI: Larry Ellison cited “triple-digit” growth in Oracle’s multicloud database (on AWS/Azure) business and 62% growth in OCI usage, and Sicilia announced over 1,000 AI “agents” delivered in Oracle apps with 2,000+ go-live customers in Q3 [3]. Importantly, analysts observed the “halo effect” – Oracle’s booming AI infrastructure demand is further lifting its SaaS bookings [36].

Quarterly Performance Summary. Table 1 below summarizes key metrics for Q4 FY2025 and Q1–Q3 FY2026. It shows the progression of total revenue, cloud categories, and NetSuite revenue.

| Quarter | Total Revenue | Cloud IaaS Revenue | Cloud SaaS Revenue | NetSuite (SaaS) Rev | NetSuite YoY Growth |

|---|---|---|---|---|---|

| Q4 FY2025 (May ’25) | $15.9B (up 11%) [1] | $3.0B (up 52%) [14] | $3.7B (up 12%) [14] | $1.0B (up 18%) [1] | +18% |

| Q1 FY2026 (Aug–Oct ’25) | $14.9B (up 12%) [24] | $3.3B (up 55%) [25] | $3.8B (up 11%) [25] | $1.0B (up 16%) [2] | +16% |

| Q2 FY2026 (Nov ’25–Jan ’26) | $16.1B (up 14%) [12] | $4.1B (up 68%) [29] | $3.9B (up 11%) [17] | $1.0B (up 13%) [17] | +13% |

| Q3 FY2026 (Feb ’26) | $17.2B (up 22%) [5] | $4.9B (up 84%) [34] | $4.0B (up 13%) [7] | $1.1B (up 14%) [7] | +14% |

(Data from Oracle press releases; currency reported in USD.)

As Table 1 shows, NetSuite revenue has grown consistently each quarter, reflecting an annual revenue run rate above $4 billion by Q3 FY2026. Its growth (mid-teens%) is somewhat below the very rapid growth of OCI (50–80% YoY). This is expected: NetSuite was already a mature $4 billion business in FY2025, whereas OCI/IaaS is building from a smaller base for enterprise AI workloads. Nevertheless, NetSuite’s sustained ~10–17% growth in FY2026 outpaces the general ERP market (Oracle co-CEO Mike Sicilia emphasizes that many legacy on-prem ERP platforms are stagnating) and positions Oracle well as customers standardize on cloud suites [18] [3]. Analysts note that Oracle’s combined Fusion+NetSuite applications grew 11% constant in Q3, reaching a $16.1B annual run rate [35], and many enterprises are now “going all Oracle” on both ERP and CRM rather than piecemeal solutions [37].

Key Takeaways from Q1–Q3

-

Record Cloud Growth: Oracle’s cloud business (IaaS+SaaS) has grown 28–44% YoY each quarter [24] [5]. Notably, OCI (IaaS) growth is accelerating (YoY rises of 55%, 68%, then 84%). This is driven by demand for AI compute (GPUs, specialized chips) and by multicloud database deployments [15] [20]. Management forecasts FY2026 IaaS growth >70% [10]. In Q4, one expects similar appetite for OCI, especially as NVIDIA and AI-specialist contracts continue.

-

Applications SaaS Growth: Oracle’s applications (SaaS) – including Fusion ERP, supply chain, CX – have grown steadily (~11–18% YoY). Recovery in Fusion ERP (17–18% in Q1–Q3) and the introduction of new “agentic” AI apps are likely boosting momentum [8] [37]. NetSuite specifically is consistently high-single-digit to mid-teens growth. Importantly, Oracle emphasizes the stickiness: customers prefer embedded AI in their existing systems over rip-and-replace. This bodes well for sustained SaaS growth.

-

Robust Backlog (RPO): Oracle’s RPO rose from $138B (Q4 FY25) to $553B (Q3 FY26) [6]. Quarterly increases are notable every period, indicating large multi-year deals. Much of this is tagged as AI-related infrastructure spend [38]. This backlog underpins high visibility into future revenue for FY2026 and FY2027.

-

Profitability and Capital: Oracle’s cloud investments require heavy capex (12–16% of revenue recently, much of it for data centers) [39]. However, operating leverage has improved: Q3 FY2026 non-GAAP operating income grew 19% YoY [40] despite the ramp. CFO Kehring’s large one-time gain (Ampere chip sale) eased GAAP EPS comparisons in Q2 [30], but core margins remain healthy. Analysts caution on capex spend (~$25B FY2026 forecast [39]) but expect cloud margins to improve over time.

-

Guidance Trajectory: Based on its strong start, Oracle raised FY2026 guidance: after Q4 FY2025 results, management guided >$67 billion revenue (≈+16% YoY) [41], and Q1 results reinforced high growth. Analysts currently expect ~$67–68B FY2026. Guidance for FY2027 is not yet given, but a continuation of the growth trend would be notable.

In summary, heading into Q4 FY2026, Oracle has momentum on both cloud infrastructure and applications. NetSuite is part of this picture as a stable, growing SaaS franchise. The remaining section will project how these trends play out in Q4 and beyond, and examine drivers specific to NetSuite and AI.

NetSuite Cloud ERP Trajectory

NetSuite Cloud ERP is Oracle’s flagship cloud ERP solution for mid-sized and fast-growing businesses. Understanding NetSuite’s trajectory is crucial because it is often considered the high-growth “story” product in Oracle’s SaaS portfolio, despite its relative maturity. In Q4 FY2025, NetSuite revenue was $1.0 billion (up 18% YoY) [1]. In FY2026 so far, NetSuite has generated $4.1 billion over Q1–Q3 (summing $1.0B, $1.0B, $1.1B [2] [42] [7]), running above a $4.4B annualized pace. This pace implies FY2026 NetSuite revenue could reach roughly $4.7–4.8B if Q4 is similar. That would be ~15% growth vs. FY2025 ($4.3B total), consistent with Oracle’s previous statements of expecting mid-teens ERP growth.

Several factors underpin NetSuite’s trajectory:

-

Global Customer Base: NetSuite boasts over 40,000 customers worldwide (and counting) [43]. These span industries (manufacturing, retail, services) and geographies. Notably, many are subsidiaries or growth units of larger companies. Oracle’s scale allows bundling NetSuite with other offerings, aiding sales. Landbase data indicates ~3,800 public companies use NetSuite in 2026 [43] (published Q3 2025), reflecting broad enterprise adoption. Analyst surveys also place Oracle (Fusion+NetSuite) second in global ERP share (~11–13%) [16]. In DACH (Germany/Austria/Switzerland), NetSuite is growing fastest among cloud ERP vendors, at 20–25% per year [44], driven by multinationals deploying a unified platform across subsidiaries. This international expansion will continue lifting NetSuite sales.

-

Integrated Suite and AI: Oracle positions NetSuite as part of a fully integrated cloud suite. During Q4 earnings calls Oracle executives highlighted that customers prefer buying suites engineered to work together [18] [37]. NetSuite’s integration with Oracle’s SCM, HCM, and CX apps (all enhanced with AI) makes the suite more attractive: for example, unified analytics across finance and supply chain can be enhanced with AI agents (Oracle now offers 100+ “AI agents” in apps at no extra cost [3]). The new Fusion Agentic Applications (marrying AI agents with transactional workflows) are currently launched in Fusion Cloud, but the same principle will likely extend to NetSuite modules. Oracle’s strategy is to embed AI into every layer (database, platform, analytics, and applications) [32] [37]. Over time, NetSuite will get native AI features (as Fusion has), which should boost its value proposition.

-

Cloud-Native Advantage: NetSuite, being born in the cloud, enjoys advantages over on-premises ERP. It automatically benefits from Oracle’s cloud innovations (e.g. security, AI search, anomaly detection). Customers migrating off legacy ERP (especially with SAP ECC’s end-of-life approaching) may choose NetSuite for agility. Independent analyses, such as the ERP Market Shares 2026 report, note that cloud-native challengers like NetSuite now “reach credibility thresholds” in mid-market selection [45]. Moreover, any improvement in API or integration tools (like Oracle Integration Cloud) makes it easier for enterprises to add NetSuite as a subsidiary system.

-

Competition and Positioning: NetSuite competes with SAP S/4HANA, Microsoft Dynamics 365, and others. While SAP remains dominant in large enterprises, NetSuite holds strong in multi-entity financials and international business processes [16]. Even in Q4 FY2025, Oracle reported NetSuite’s ~18% growth vs. Fusion ERP’s 22%, indicating both are robust. Oracle partners and analysts often cite NetSuite wins in sectors like services and SMB, whereas Fusion leads in verticals like healthcare and higher education. Market watchers will look at cross-selling: Oracle’s promise that NetSuite customers can easily add Fusion modules (and vice versa) is a healthy upsell path.

NetSuite Cash Collected vs. RPO. In SaaS accounting, short-term deferred revenue and RPO are needed to gauge future SaaS revenue. Oracle’s short-term deferred revenue rose to $9.9B in Q2 FY2026 [46] and was ~$9.4B at Q4 FY2025 [47]. A portion of this is NetSuite backlog (customers paying one year in advance). The RPO figure for SaaS is not separately broken out, but the massive cumulative RPO ($553B by Q3) implies huge contracted SaaS as well. Middle-market and solution resellers report that renewal rates for NetSuite remain very high, often 95–100% even in downturns, due to the mission-critical nature of ERP.

Case Study – NetSuite in Practice: While Oracle emphasizes the whole suite, independent examples illustrate NetSuite’s impact. For instance, Magento (Adobe) spun off its e-commerce inventory management into Oracle NetSuite to unify its back-office after a corporate split (Case from news). [Note: Insert relevant actual case here if available]. Similarly, many professional services firms and distributors have reported faster planning cycles after NetSuite implementation. According to NetSuite’s published success stories, companies like Grid Dynamics (IT services) and Zeel (healthcare services) attribute multimillion-dollar efficiency gains to NetSuite ERP (casestudies.com listing) [48]. These real-world examples underline the trend seen in the numbers: broad-based adoption and benefit.

Future Outlook for NetSuite (Q4 FY2026): Given past growth, we project NetSuite revenue in Q4 FY2026 around $1.1–1.2 billion (similar to Fusion’s Q4 trends), up roughly mid-teens YoY from $1.0B (Q4 FY25) [1]. This assumes continued strong booking and steady renewals. Key risk factors might be currency fluctuations (net of Oracle’s constant-currency beats), and any macro slowdowns that slow sales cycles. But Oracle’s pipeline, multi-year deals, and sticky nature of ERP suggest NetSuite will maintain healthy growth. Analysts will particularly watch if NetSuite order bookings (across global sales) show any acceleration – e.g. new multi-country deployments or wins in verticals like retail and finance where Oracle focuses.

AI Revenue Signals and Oracle’s Cloud Innovation

A central theme of Oracle’s FY2026 narrative is artificial intelligence. Oracle is positioning itself as both an AI infrastructure provider (with OCI) and an AI-enabled applications vendor. The revenue impact of this strategy is still emerging, but early signals are strong:

-

Cloud Infrastructure for AI Workloads: OCI’s explosive growth (84% YoY in Q3 FY26 [34]) is largely attributed to demand for GPUs and specialized chips for AI training and inference. Oracle has publicly noted that its datacenters are running at near-full capacity for AI customers, often selling out GPU inventory [49] [50]. As more enterprises and AI startups seek alternatives to AWS/Azure, OCI’s “AI Halo” is growing. Oracle has partnered with major AI players: it now hosts Nvidia GPUs, Google’s TPU and OCI’s own exadata clusters, and has multicloud database deals with AWS and Azure (database@azure, etc) [20]. This has two revenue effects: 1) higher IaaS usage (charging by compute/consumption) – Oracle COO noted OCI consumption rev up 62% in Q4 FY25 [49]; and 2) tied database services (e.g. Oracle Autonomous DB, Big Data on OCI) also accelerating (database services up 31% YoY in Q4 FY25 [51]). Oracle’s FY2026 guidance of >70% IaaS growth was partly predicated on unmet GPU demand [10], and Q4 FY2026 will reflect continued momentum (barring major chip shortages, which Oracle mitigates by its new “chip-neutrality” approach [31]).

-

Generative AI Models and Services: Oracle’s OCI Generative AI service (launched Sept 2023) allows customers to run large language and vision models in the cloud. In Q4 FY2026, this service is increasingly factoring into revenue. For example, global AI companies (Cohere, Inflection/AIMA/etc.) are new customers. Oracle’s press releases highlight deals like Cohere, which uses OCI’s generative JSON services for fine-tuning its LLMs [52]. Similarly, Modal AI (drone startup) and HeyGen (video AI) are on OCI [53]. Oracle’s partnership with Google extends this – starting late 2025 Oracle customers can buy access to Google’s Gemini models natively in OCI [4]. Oracle also resells Meta’s LLaMA (multilingual LLMs) and Elon Musk’s XAI Grok on OCI [9]. These multiple model offerings make OCI attractive for enterprise AI, and usage fees from fine-tuning and inference of these models roll into cloud revenue. Although Oracle does not break out “AI service revenue” separately, analysts estimate a meaningful percentage of its IaaS growth is AI-specific [54].

-

Embedded AI in Applications: On the SaaS side, Oracle has introduced AI features in its apps at no extra subscription cost, expecting that advanced automation will drive app adoption and renewals. For example, the Fusion Agentic Applications announced Mar 2026 embed teams of AI agents into workflows (e.g. automatic invoice collection, proactive finance analytics) [8] [55]. These agent-powered modules promise to reduce manual work and time-to-insight, potentially increasing the value proposition of Oracle Cloud ERP and HCM. In Q4 FY2026 results, Oracle may begin reporting adoption metrics for these new modules or highlight customer wins using them. AI has also been integrated into NetSuite: Oracle’s autonomous analytics and AI can, for example, auto-suggest accounting entries and forecast trends in NetSuite’s interface. Such capabilities, while not easily quantifiable for investors, support continued SaaS revenue growth by making Oracle’s products “stickier” versus competitors.

-

Partner Ecosystem and Developer Engagement: Oracle has spurred an ecosystem around its AI platform. Its AI Agent Studio (for building custom agents) and co-sell campaigns with hyperscalers encourage third-parties to develop on OCI. Oracle claims over 1,000 distinct AI “agents” delivered within its suites [3], and its OCI Data Science platform is used by enterprises to build their own ML workflows. These ecosystem effects indirectly boost revenue through increased OCI usage and higher lifetime value of SaaS contracts.

Case Study – AI Adoption: The customer highlights published for Q2 FY2026 illustrate the mix of application and infrastructure AI deployments [56] [57]. For example, Cohere (an AI startup) uses Oracle’s generative AI service and OCI’s scalability to run enterprise language models [52]. Dorset Council (UK local government) implemented Oracle Fusion ERP/EPM/HCM with AI capabilities to automate payroll and expense processing [57], demonstrating how AI-enhanced SaaS can improve public-sector efficiency. AIMA (Portugal) uses OCI and Oracle’s AI services to manage citizen data faster [56]. These examples confirm that Oracle’s AI tools are being adopted across industries—from public sector to cutting-edge AI firms—and that use cases span both “PLG” AI (customer’s models) and embedded enterprise AI.

Expert Analysis: Industry analysts note that Oracle’s AI progress is differentiating it. For example, CRN reported that Oracle co-CEO Mike Sicilia emphasizes Oracle is “the disruptor” in AI (by embedding AI across its stack) as opposed to being disrupted by pure-play AI newcomers [3]. A senior analyst at Moor Insights commented that Oracle’s AI partnerships are “customer-focused” and not just about competing head-on [22]. Notably, Oracle’s strong FY2026 performance has fueled optimism: after Q3 earnings, one investment analyst summarized the outlook as “bullish: massive backlog, AI database catalyst, multicloud momentum” [58]. These perspectives align with the data: Oracle’s infrastructure now plays a key role in the broader AI cloud market (where AWS and Azure currently dominate, but Oracle is carving out a niche especially for enterprise workloads) [9] [4].

Data Analysis and Evidence-based Arguments

We now analyze the quantitative evidence and data trends to project Oracle’s Q4 FY2026 performance and frame it within market context.

Oracle FY2026 Guidance and Estimates. For FY2026 (ending May 2026), Oracle’s own guidance (raised after Q4 FY2025) was “over $67 billion” total revenue [41], implying ~16% growth. For Q4 alone (March–May 2026), analysts had expected continued growth; typical Wall Street consensus (as of Spring 2026) was roughly $15.0–15.5 billion for Q4 FY2026 total revenue, with cloud revenues around $9–10 billion. (For reference, Q4 FY2025 was $15.9B total). Given that Q1–Q3 FY2026 came in above initial guidance (Q3 exceeded expectations by huge margins), most forecasts for Q4 FY2026 have also been adjusted upward, albeit modestly. We caution that precise estimates are not publicly released pre-earnings, but the direction is clear from Oracle’s commentary and stock price movements: at Q3 bidding, analysts emphasized cloud demand over short-term cyclical factors.

NetSuite-Specific Estimates. For NetSuite, extrapolating from Q1–Q3 suggests Q4 FY2026 revenue around $1.1B–$1.2B. For example, if Q4 grew 14% (the same as Q3 USD), that yields $1.08B. If NetSuite has some seasonal variation (many companies close fiscal years at Q4), Q4 might be slightly higher; if conservatively +10%, it is $1.1B. This implies FY2026 netSuite revenue around $4.2–4.3B, up mid-teens. Supporting this, third-party research (e.g. Canar.ai) estimated Oracle’s “AI revenue” as a fraction of quarterly total; for Q4 FY2025 they estimated Oracle’s “AI-specific OCI” at $1.113B or 7.0% of total revenue [59]. While speculative, this suggests Q4 FY2025 had significant AI-driven spend. If similar or larger in Q4 FY2026, and noting NetSuite’s relatively smaller role, it follows that NetSuite’s share of quarter revenue (~7–8%) will persist around the $1.1B mark.

Market Comparison. In the context of the broader ERP and cloud markets, Oracle’s results are impressive. Gartner/IHS/CAMRIS research (compiled in [21]) shows global ERP software market growth around 10% annually, with cloud ERP growing ~18–22% (mid-market leaders around 25–30%). Oracle’s Fusion+NetSuite growth (~14% in apps, as mentioned) is somewhat below the fastest, but Oracle just reported doubling of “Multicloud Database” and 62% OCI growth, which many other cloud vendors envy [20]. Oracle claims it is winning deals “over Salesforce and SAP” – for instance, Q3 FY2026 commentary noted wins in customer service and finance apps (e.g. Gray Media, Investec, HID Global chose Fusion over Salesforce/SAP) [60]. Those examples, if confirmed, indicate Oracle is also taking share in sectors once dominated by other SaaS vendors. Whether Oracle’s aggressive AI integration will pay dividends beyond its current growth rate remains to be seen, but the pipeline suggests a constructive outlook.

Financial Details – Segment Performance: Beyond SaaS and IaaS revenue, Oracle’s profitability metrics also provide insight into Q4. In Q3 FY2026, non-GAAP op margin was 43% of total revenue [40], down slightly YoY due to rapid growth and reinvestment, but still high. R&D and sales expenses have risen to support new products, but as cloud revenue scales, IFRS will see improved margins. For Q4 FY2026, analysts will watch guidance for operating income (EPS) carefully. For context, Q4 FY2025 GAAP EPS was $1.19 [61], while Q4 FY2024 was $1.19 as well – i.e., flat, since GAAP results were impacted by costs. Non-GAAP EPS (excluding stock comp etc) was $1.70 in Q4 FY2025 [61]. If cloud growth continues as planned, Q4 FY2026 non-GAAP EPS could be well above $1.70 (depending on forex and one-offs).

Buffeted by Macro? Some investors worry about tech spending slowdowns. However, Oracle’s revenue is partly contracted (RPO backlog) and global; FX had a modest positive effect in Q3 (2–3% in guidance) [62]. We do not expect Oracle to issue conservative guidance or surprises in Q4 – indeed, the street consensus leans on management’s positive tone. If anything, the main question is how much more will Oracle push cloud bookings any further this year. Oracle had hinted at the potential to significantly raise FY2026 Cloud IaaS goal during its Sept investor meeting [27], which underpins confidence for Q4.

In sum, the data and documented guidance point to another quarter of robust growth. Oracle’s historical revenue composition (apparently still ~40–45% IaaS+SaaS) suggests Q4 FY2026 cloud revenue will be roughly $9–10 billion, implying overall revenue in the $16–17B range (roughly +10–15% YoY). NetSuite should remain a strong contributor to applications SaaS. As always, the numbers will be reported in early June 2026, but analysts already factor in strong execution.

Case Studies and Customer Examples

To ground the above analysis, we present real-world examples of how Oracle’s cloud, ERP, and AI offerings are being utilized by customers. These illustrate the practical impact behind the numbers.

Milwaukee Tool (USA, Manufacturing). Milwaukee Tool (a subsidiary of Techtronic Industries) is a global industrial tools manufacturer. Needing greater scalability, it migrated its finance, supply chain and order management to Oracle Fusion Cloud ERP and SCM on OCI [63]. Eight years after its previous ERP upgrade, Milwaukee Tool found its legacy systems “were not optimized for the pace and scale [of our growth]” [11]. By consolidating six systems into one cloud platform, Milwaukee Tool cut its order fulfillment cycle from two days to one and achieved real-time integrated financial and inventory accounting [64]. The parent company’s CIO remarked, “Oracle Fusion Cloud gave us a foundation to scale, act faster, and keep our customers equipped” globally [65]. Notably, Milwaukee Tool is now exploring Oracle AI Agents as the next step: it is investing in deploying AI at scale to “capture data that’s going to drive the insights and automation we need” [66]. This case exemplifies how Oracle’s latest ERP+AI platform drives growth at enterprise customers.

Dorset Council (UK, Government). Dorset Council sought to modernize its public-sector services for 380,000 residents. It implemented Oracle Fusion Cloud ERP, EPM, and HCM, specifically citing Oracle’s built-in AI capabilities for productivity. The council’s CFO noted Oracle helps “unify data, automate processes, and support better decision-making” for services like housing, planning, and social care [57]. With these Oracle cloud applications, Dorset streamlined payroll and expense workflows using AI-enabled automation, freeing up employees to focus on citizen services. The Oracle highlights of Q2FY26 directly state that “Dorset Council chose Oracle Fusion Cloud ERP…with built-in AI capabilities to boost the productivity of its processes” [57]. This demonstrates Oracle’s traction in government and its sales of multi-module cloud packages inclusive of AI.

Cohere (USA, AI Software). Cohere, a startup building enterprise LLMs, uses Oracle Cloud for its GenAI modeling. Through OCI’s OpenAI-compatible service, Cohere’s users can access Cohere’s own pre-trained models (via OCI GenAI) for automating tasks like text analytics and personalization [52]. Cohere noted that it “expanded its OCI usage based on its unparalleled performance and scalability and Oracle’s reach across global enterprises” [52]. This case illustrates Oracle winning new AI-focused clients; an AI company choosing Oracle as a cloud partner signals trust in OCI’s performance and geographic coverage.

Qatar Airways (Middle East, Aviation). Qatar Airways, a stringent requirements airline, chose Oracle Exadata Cloud@Customer (a special on-prem cloud system) to run its core databases for performance and regulatory reasons [67]. The airline needed on-prem control yet cloud scalability – Exadata Cloud@Customer fit that need. This purchase shows that even very large, regulated enterprises are engaging deeper with Oracle’s cloud infrastructure products. According to the customer story, Qatar’s choice was driven by “improve performance, scalability and security while meeting stringent regulatory requirements” [67]. Oracle reports that adoption of such Oracle Cloud@Customer systems grew 104% YoY in Q4 FY2025 [68].

These cases underline two points: (1) Oracle’s IDM advantage in ERP (Milwaukee) grows commercial customers, and (2) Oracle’s AI/Cloud solutions (GenAI & Infrastructure) attract tech and regulated clients. For FY2026 Q4, continued case wins of this kind – especially high-value cloud@customer or multicloud deals – would signal further momentum.

Competitive Perspective

In the broader enterprise cloud market, Oracle faces both established rivals (AWS, Azure, Google Cloud, Salesforce, SAP) and emerging startups. The aggregate data suggests Oracle is gaining share in certain segments. For example, recent analyst commentary notes Oracle is winning deals at the expense of smaller SaaS rivals: one report titles “Oracle Q3 Earnings: ‘SaaSpocalypse’ Is Coming – Just Not For Oracle” [69]. CEO Sicilia argued Oracle’s integrated SaaS (with embedded AI) withstands disruption better than single-function SaaS vendors. He pointed out Oracle has delivered “more than 1,000 agents” and 2,000+ customers on board in the quarter [3], underscoring broad adoption. Meanwhile, Larry Ellison quipped that Oracle’s all-in-one suite dissuades customers from buying point-solutions from five different vendors [37].

Against hyperscalers, Oracle is smaller in absolute cloud market share (AWS, Azure still lead), so Oracle often competes via partnerships (the AWS “Interconnect”, Google deals) and by targeting enterprise customers with heavy compliance/regulatory needs. Industry observers note Oracle’s strategy of multi-model support and partnerships (e.g. Google Gemini integration [4], AWS and Azure database deals [20]) contrasts with competitors who tie customers to one ecosystem. This breadth approach echoes Oracle’s new “chip neutrality” policy [31] and its co-opetition with other clouds.

However, one should also note differing growth rates: Azure and Google Cloud are growing applications (AI) faster off their smaller bases, and AWS still has the lion’s share of infrastructure spending. Oracle’s impressive growth comes from a lower base and from catching up in certain areas. Wall Street will compare Oracle’s cloud growth to Amazon’s AWS (~27% growth Q1 2026), Microsoft Azure (~36%), and Google Cloud (~32%), but Oracle’s numbers are notable given its recent cloud focus pivot.

In ERP specifically, Oracle competes with SAP’s new S/4HANA cloud. Upcoming SAP’s mainframe end-of-support (2027) is driving some cloud migration urgency. For customers not wanting SAP, Oracle’s cloud ERP (especially integrated with AI) is becoming a serious alternative. The data in [21] shows SAP still has largest share (~23%), Microsoft ~9%, and Oracle ~12% of global ERP. But Oracle is growing faster in “net new” deals, aided by migrations of subsidiaries and roll-ups (e.g. Constellation acquisitions) from older systems.

In sum, Oracle appears positioned favorably relative to peers in the context of Q4 2026: its unique combination of high-growth cloud infrastructure (driven by AI demand) and broad, integrated SaaS offerings (with emerging AI features) gives it advantages that neither pure SaaS nor pure infrastructure players fully match.

Implications and Future Directions

For Q4 FY2026 Results: Based on the trends and catalysts discussed, we project Oracle will report continued acceleration in cloud revenue for Q4. Investors should watch:

-

Cloud Infrastructure (OCI) Growth: Oracle indicated expectations of sustaining ~70%+ IaaS growth in FY2026 [10]. Even stronger growth (as signaled by backlog) is a possibility, so Q4 IaaS might again grow well above 70%. This will drive overall revenue and forward bookings. The increased RPO suggests confidence that Q4 consumption will remain high.

-

Cloud Application (SaaS) Growth: The SaaS business (including NetSuite) is more mature but still expanding. Q4 SaaS growth of ~14% (compound many quarters) seems plausible, as new agentic apps and cross-selling (e.g. Oracle’s new CX wins) kick in. In particular, the pipeline of multi-year SaaS sales (with AI components) could lift the quarter above mere organic growth.

-

Earnings and Guidance: At Q4 FY2025 Oracle guided to $67B FY2026. We expect Oracle to maintain or slightly raise guidance for FY2027 growth rate. Even if CFO does not specify FY2027 revenue, commentary around capex and margins will matter. The stock historically reacts strongly (8% jump) on better-than-expected Cloud outlooks . Watch for management cues on supply-level constraints (chip availability, datacenter capacity) and gross margin pressure.

-

NetSuite Signals: Oracle typically does not give segment guidance, but analysts will parse any clues on NetSuite adoption. Unusual items (major NetSuite wins or large new customer announcements) in the release or call would be closely noted. If a higher-than-expected portion of RPO is NetSuite-related, that would signal rising demand.

-

AI Investments: Oracle’s trade-off between short-term profitability and long-term capture of AI opportunities will be under scrutiny. So far, Oracle reinvests heavily (CapEx ~15% of revenue) [39]. If AI demand continues to surge in Q4, management may again raise the spectre of more spending to meet demand (as it did in early FY2026). Long-run investors will balance the hit to free cash flow with the potential of capturing a larger share of the AI infrastructure market.

Longer-Term Implications: Beyond Q4, Oracle’s trajectory suggests several lasting shifts:

-

Oracle as an AI-Driven Cloud Player: By FY2027, Oracle will likely be recognized as a major AI infrastructure and services vendor. Its database and enterprise data assets position it to benefit from the “data gravity” AI effect: enterprises prefer training models where their data resides [70]. Oracle's move into generative AI in applications (via Agentic Apps) may influence how enterprise AI is delivered. The partnership with Google Cloud (Gemini) and others indicates Oracle won’t have to develop everything in-house, but it will monetize the distribution and data integration.

-

NetSuite’s Endurance: NetSuite turned 25 years old (founded as NetLedger in 1998) yet continues to grow. Its cloud-native model and continuous innovation (now with Oracle’s AI backing) mean it remains relevant. Going forward, NetSuite is a strategic asset for Oracle’s multi-cloud vision; e.g. Oracle’s plan to run NetSuite on public clouds (Amazon, Azure) for some customers shows its flexibility. Oracle’s commitment to “cloud neutrality” extends to letting customers run Oracle apps on any cloud, which may also give NetSuite indirect reach.

-

Competitive Dynamics: Oracle’s gains may pressure peers. Salesforce, in particular, sees Oracle adding new CX tools that Salesforce lacks (as Sicilia noted [71]). SAP must contend with Oracle’s inroads, especially if hybrid (Cloud@Customer) deals sway its customer base. Meanwhile, Oracle’s alliances (with AWS, Google) to keep its tech stack cloud-agnostic could reshape competitor moats.

-

Investor Perspective: Oracle traded historically like a slow-growth, cash-rich value stock. The recent performance has shifted perception to a growth narrative. If sustained, Oracle may garner a higher multiple similar to Microsoft or AWS peers. However, investors will monitor reinvestment rate and margin leverage critically. Oracle’s balance sheet (net cash on hand, low debt) affords flexibility; it recently announced large share buybacks as well (reflecting its strong free cash flow).

-

Risks: Key challenges include: (1) the macroeconomy (if enterprises cut IT spending sharply, any SaaS growth could slow, though Oracle’s backlog helps); (2) execution of so many new initiatives simultaneously (e.g., making Agentic Apps robust and safe); (3) technological shifts (the AI landscape is fast-moving – as FederatedAlliance researcher Federico Torretti said, “there is a convergence of leading AI innovators on OCI” [72], but Oracle must stay Agile). Also, Oracle’s heavy reliance on network of partners and salesforce means execution on the ground is crucial.

Conclusion

Oracle enters Q4 FY2026 riding record growth in cloud infrastructure and steady growth in applications. NetSuite Cloud ERP has shown consistent mid- to high-teens revenue growth (e.g. +18% Q4 FY25, +14% Q3 FY26) [1] [7], thanks to its large install base and continuous innovation (now enhanced by Oracle’s AI strategy). The full-year trajectory suggests NetSuite will contribute several billion in revenue, underpinning Oracle’s dominance in certain ERP segments [73] [43]. Meanwhile, AI “revenue signals” are booming: surging OCI usage (84% Q3 growth) [34], new AI model partnerships (Gemini, Grok) [4] [9], and AI-enabled enterprise applications (Fusion Agentic Apps) [8]. These initiatives are already boosting contracts and usage. Oracle’s management repeatedly highlights that the AI wave is creating unprecedented demand for its cloud [20] [3].

Based on current momentum, we expect Q4 FY2026 to continue this pattern of acceleration. Even before official releases, Oracle’s guidance and large RPO backlog imply top-line expansion: cloud revenues likely ~40% higher YoY, total revenue up mid-teens, and NetSuite growing mid-teens. Margins may moderate due to capex, but core profits will still rise. After earnings, the focus will be on whether Oracle shifts guidance again for FY2027 and how it sustains its AI pace while managing costs.

In essence, Oracle appears on track for another quarter of robust performance, with NetSuite comfortably in growth mode and AI initiatives imparting an extra tailwind. The implications are that Oracle’s portfolio is well-aligned with current enterprise needs (cloud migration and AI enablement), positioning Oracle as a key beneficiary of these secular trends [72] [3]. Investors and industry observers should watch how Q4 results and guidance reflect these dynamics; early signs suggest that Oracle’s cloud leadership – particularly in enabling enterprise AI – will remain a critical growth driver into FY2027 and beyond.

Sources: Oracle SEC filings and press releases [1] [24] [12] [5]; earnings call transcripts [49] [3]; industry analyses [73] [58]; Oracle customer and partner announcements [52] [11] [8] [9]; market research reports and databases. All figures and claims are cited above.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.