ASC 330 Inventory Valuation: LCNRV Guide in NetSuite

Executive Summary

Inventory valuation is a critical accounting issue affecting virtually every business that holds stock. In the United States, ASC 330 governs inventory and requires that most inventory be carried at the lower of cost or net realizable value (LCNRV), whereas IFRS’s IAS 2 mandates the lower of cost and net realizable value. Both frameworks compel write‐downs when market conditions impair inventory, but they diverge sharply on reversals of those impairments. Under U.S. GAAP (ASC 330), once inventory is written down, that new cost basis is permanent – any recovery in market value is ignored [1] [2]. In contrast, IFRS explicitly requires reversing a prior write-down (down to the original cost) if conditions improve (Source: production.faronline.se) [3]. These differences influence reported earnings volatility, comparability across companies, and financial statement preparation.

From a systems perspective, many organizations use ERP software like NetSuite to manage inventory. NetSuite supports multiple costing methods (FIFO, LIFO, average, standard, etc.) [4] [5] and provides tools for adjusting inventory values. For example, NetSuite’s Inventory Adjustment and Inventory Cost Revaluation transactions allow finance teams to change item quantities and unit costs to reflect events like obsolescence or price declines [6] [7]. Implementing LCNRV in practice typically involves identifying impaired items (e.g. slow-moving stock), determining their net realizable values, and then using NetSuite’s adjustment features to write down inventory values, with offsetting expense entries (often to COGS) [8] [9]. Under IFRS, if market values later recover, NetSuite users could then reverse those adjustments (via additional inventory entries) up to the original cost, whereas under GAAP such reversals would not be recorded.

This report provides a comprehensive examination of ASC 330’s LCNRV rule and its implementation in NetSuite. We review the historical and conceptual background of lower-of-cost accounting, the detailed requirements of ASC 330 (including ASU 2015-11’s simplifications), and IAS 2 for contrast. We analyze how inventory write-downs are determined and recorded—including allowance vs direct methods—and why GAAP prohibits write-up of inventory impairments. Crucially, we show how to carry out these adjustments in NetSuite: discussing relevant forms, accounts, and processes. We support our analysis with authoritative sources (FASB codification, IFRS texts, KPMG guidance, etc.), real-world cases, and data. Case studies (e.g. a university’s experience and a biotech firm’s inventory reconciliation) illustrate practical outcomes. Finally, we discuss the implications of these rules for financial reporting and future directions, emphasizing that while IFRS permits more volatility through reversals, GAAP remains conservative.

Introduction and Background

Inventory is often among the largest assets on a company’s balance sheet. For many manufacturing and retail businesses, it is second only to property, plant and equipment in magnitude [10]. How inventory is valued directly affects reported assets, cost of goods sold (COGS), profitability, and other key financial metrics. Because inventories are expected to be sold (or used) at some point, both U.S. GAAP and IFRS require that inventories not be carried on the books for more than what they will ultimately realize on sale. In other words, inventory should be stated at not more than its net realizable value (Source: production.faronline.se) [3].

Under ASC 330 (U.S. GAAP) inventories are initially recorded at cost (using a permitted cost flow assumption such as FIFO, LIFO, average, or standard cost) [11] [12]. An impairment loss occurs if the market or net realizable value (NRV) of inventory falls below its historical cost. Traditionally, U.S. GAAP employed a lower of cost or market (LCM) test, where “market” meant replacement cost within defined limits (ceiling and floor) [1] [13]. For most entities (using FIFO or average cost), that effectively became lower of cost or NRV under ASU 2015-11. Critically, ASC 330 forbids reversing an inventory write-down [8] [1]. Once cost is reset downward, it remains the new basis even if market prices recover. This conservatism (“recognize losses early, never anticipate gains” [14]) is deeply embedded in GAAP and reflects its prudence principle [14] [2].

By contrast, IAS 2 (IFRS) mandates that inventories be measured at the lower of cost and net realizable value (NRV) (Source: production.faronline.se) [3]. IFRS definition of NRV is “the estimated selling price in the ordinary course of business, less the estimated costs of completion, disposal, and transportation” (Source: production.faronline.se). If NRV falls below cost, the inventory is written down. Crucially, IFRS explicitly requires companies to reassess NRV each period and reverse prior write-downs when conditions revert (Source: production.faronline.se) [3]. In other words, IFRS allows inventory value to go back up (but not above the original cost) if market prices improve (Source: production.faronline.se) [3]. This reflects IFRS’s goals of relevance and faithful representation, ensuring assets are not understated if recoveries occur.

Table 1 summarizes key differences between U.S.GAAP (ASC 330) and IFRS (IAS 2) on inventory valuation:

| Feature | IFRS (IAS 2) | US GAAP (ASC 330) |

|---|---|---|

| Measurement Basis | Lower of cost or net realizable value (NRV) (Source: production.faronline.se). | Lower of cost or market. (For FIFO/weighted-average: LCNRV; for LIFO/retail: LCM) [15] [1]. |

| Cost Formulas Allowed | FIFO, weighted-average, specific-ID (Standard cost, retail allowed for convenience) [16]; LIFO prohibited [5]. | FIFO, weighted-average, specific-ID, LIFO and retail allowed [12] [5] (LIFO broadly permitted, albeit often replaced under 2015 simplification). |

| Lower-of-Cost Trigger | NRV < cost. Write inventory down to NRV as an expense [17] [18]. | “Market” < cost. For FIFO/Avg: market = NRV; for LIFO/retail: replacement cost within a ceiling/floor [1] [13]. Write-downs to NRV or market as expense. |

| Reversals of Write-Downs | Allowed if original conditions (that caused write-down) no longer exist (Source: production.faronline.se) [3]. Up to original cost. | Prohibited. Once written down, inventory’s cost basis is “new cost” that cannot be reversed, even if NRV later increases [8] [1]. |

| Presentation of Write-Down | Expense in period (COGS or other); IFRS often adjusts COGS [17]. | Expense in period (COGS or other line); often recognized via a reserve account or direct write-down [8] [19]. |

These accounting rules have crucial practical consequences. Under IFRS, inventory losses can “bounce back” in future periods, potentially raising profits; under GAAP, such upward corrections are never recorded. This difference can be material when market conditions fluctuate. Many analyses note that IFRS’s reversal policy provides more economically symmetric treatment, whereas GAAP’s approach is more conservative [14] [2]. For example, IFRS proponents argue that allowing write-down reversals avoids understating assets when values recover [14], while GAAP supporters caution that reversals can “anticipate gains” and introduce volatility [14] [2]. We delve into these conceptual issues and empirical effects later in this report.

From a systems perspective, achieving compliance with these rules requires appropriate process and controls. Enterprise systems like Oracle NetSuite provide tools to manage inventory costs, but do not automatically handle LCNRV adjustments on their own. Users must identify impairment triggers (e.g. obsolescence, excess supply, price decline), calculate NRV, and then record the required write-offs or reversals through the system’s transaction forms. This report will guide practitioners on how to use NetSuite’s features to comply with ASC 330’s LCNRV requirements (and IFRS in parallel).

ASC 330 (U.S. GAAP) – Inventory Valuation and Write-Downs

ASC 330 Core Principles

The U.S. GAAP codification ASC 330 “Inventory” governs how inventory is measured and reported. The standard permits multiple cost flow assumptions: First-In, First-Out (FIFO), Weighted-Average, Specific Identification, and also uniquely allows Last-In, First-Out (LIFO) and the Retail Inventory Method [12] [5]. (By contrast, IFRS prohibits LIFO [5].) The key requirement of ASC 330 is that inventory must be stated at the lower of cost or market (LCM) [1] [13]. Here “cost” is the historical cost of acquisition or production, and “market” is generally replacement cost bounded by a ceiling and floor. Specifically:

- Ceiling: Market (replacement cost) cannot exceed NRV.

- Floor: Market cannot be less than NRV minus a normal profit margin [1] [15].

This classic LCM approach was seen as complex: a company computing inventory impairment under LCM had to calculate three amounts (cost, replacement cost, ceiling, floor) and take the middle value [20] [15]. Furthermore, in practice ASC 330 effectively required write-downs only when NRV fell below cost, since firms would not reduce inventory values below NRV (the ceiling) or above NRV (the floor) [20]. Thus, for most companies using FIFO or average cost, the result was essentially the same as comparing cost versus NRV.

In July 2015, FASB issued ASU 2015-11 (“Inventory (Topic 330): Simplifying the Measurement of Inventory”), effective for fiscal years after Dec. 15, 2016. This update simplified LCM to a lower of cost or net realizable value (LCNRV) test for all companies using FIFO or average cost [15] [20]. Under ASU 2015-11, the “replacement cost” concept and the ceiling/floor bands were eliminated for those inventory costing methods, aligning GAAP with IFRS’s straightforward lower-of-cost-or-NRV rule [15] [20]. (Companies using LIFO or the retail method continue to use the old LCM definition, including market-based measures, as LIFO/retail have not been changed by ASU 2015-11 [15] [20].)

In sum, the bottom-line under modern GAAP is this: when inventory’s net realizable value declines below its historical cost, the inventory must be written down to NRV immediately [20] [8]. If a company uses FIFO, average, or specific cost, that write-down equals the excess of cost over NRV. If using LIFO or retail, a similar impairment is required using replacement-cost-based “market” subject to NRV limits. Once the inventory has been written down, ASC 330 is emphatic that no future write-ups are allowed: the reduced cost becomes the new basis going forward [8] [1]. Stated differently, “ASC 330-10-35-2 establishes that no subsequent write-up of inventory is permitted if market value increases” [8]. This one-way rule underscores GAAP’s conservatism: losses impact earnings immediately, but potential gains (from recoveries) are not recognized until realized in sales.

Recording Inventory Write-Downs

When inventory is written down to NRV, GAAP allows two equivalent approaches. One can either directly reduce the inventory balance (credit inventory) and debit cost of goods sold (COGS) (or another loss/expense line). Alternatively, many companies use an inventory valuation reserve (allowance) account. In the allowance approach, one debits COGS (or “Inventory Reserve” expense) and credits an Inventory Reserve (liability or contra-asset) account [8] [19]. The footnoted illustration in US GAAP Buddy (below) exemplifies the allowance method:

Example: Slow-moving component with cost $400,000 and total NRV $256,000 requires a $144,000 write-down. Journalize:

Dr. Cost of Goods Sold $144,000

Cr. Allowance for Inventory Obsolescence $144,000

(To record NRV write-down on Component XYZ) [21].

Either method is GAAP-compliant; ASC 330-10-45-1 merely requires disclosure of the accounting policy (the choice of method) [19]. Businesses often prefer the allowance approach to clearly separate the write-down in the financials, while leaving the gross inventory balance intact. Regardless, the net inventory on the balance sheet reflects inventory cost less any write-down allowances [21].

ASC 330 also requires that at each interim or year-end period the entity reassess the NRV of inventory, to determine if additional write-downs are needed [8]. Factors triggering write-down reviews include market price declines, excess production, obsolescence, or damage. For example, if a product line suffers technological obsolescence, management must estimate the remaining selling price less costs to sell (NRV) and compare to cost [8]. If NRV has fallen below cost, the inventory is immediately written down in that period’s accounts. Mining the ASC, ASC 330-10-35-1 requires that “for inventories measured using FIFO or average cost, the inventory shall be valued at the lower of its cost or net realizable value” at each reporting date. Any new impairment is recognized in the current period.

Multiple sources note that GAAP’s refusal to reverse write-downs has no exception (outside of currency translation). For instance, as Legal Clarity & other analyses state, ASC 330 “establishes a new cost basis at the write-down and forbids any subsequent write-up of inventory if the market value of inventory increases” [22] [1]. In practice, that means even if the inventory is still on hand and market prices rebound, GAAP keeps the impaired value and records any profit when the inventory is sold normally. The IFRS comparators report that a write-down “sticks” under GAAP [23] [24], whereas IFRS would reverse it.

To summarize ASC 330:

- Scope: Inventories (held for sale, WIP, raw materials) [25].

- Cost methods: FIFO, weighted-average, specific, (and LIFO/retail under GAAP) [12] [5].

- Periodic revaluation: Inventory must be evaluated at each reporting date for impairment [8].

- Measurement: Lower of cost or NRV (or market under LIFO/retail) [15] [20].

- Recording: Loss immediately expensed; write-down recognized by lowering inventory or an allowance [21].

- No reversals: Once written down, no write-up permitted [8] [1].

- Disclosure: Required to explain the policy (allowance vs direct) and amounts of write-downs [19].

These rules reflect U.S. GAAP’s prudent, “downside-only” philosophy. Key authoritative references confirm them: US GAAP Buddy plainly states “ASC 330-10-35-1” requires write-downs when NRV<cost, and “ASC 330-10-35-2” forbids reversals [8]. A Pittsburgh audit firm notes “U.S. GAAP…cannot [reverse losses]” [2], cementing the point.

ASC 330: Practical Implications

In practice, the LCNRV rule under ASC 330 means companies must constantly monitor inventory. Common impairment triggers include technological obsolescence, declining market prices, or product discontinuances. Entities often establish an obsolescence reserve a priori (similar to bad debt reserve for receivables) and adjust it as conditions warrant [21]. NetSuite and other ERPs support recording either by adjusting reserves or using inventory adjustments.

Importantly, under GAAP, the reduction in inventory is permanent. If inventory was carried at $400 and written down to $300, and later the market price recovers to $450, GAAP still carries it at $300 (its new cost). The eventual $150 gain is realized only at sale. This leads to a mismatch relative to economic reality when comparisons to IFRS are made [26] [1]. Analyses highlight that GAAP’s insistence on no reversals results in lower reported earnings in recovery periods [27] [28], while IFRS companies would show higher earnings from recouping the write-down. Stakeholders should be aware that GAAP firms might appear to lose more profit potential in up-cycles than IFRS peers, purely due to standard differences.

From an auditing and controls perspective, ASC 330’s requirements imply documentation of the NRV calculation for each impairment. Management must justify its NRV estimates (e.g. current sales prices, selling costs) and ensure these assumptions are conservative. Auditors typically verify that thresholds for tying allowance balances to recorded amounts or carrying forward cost basis are appropriate. No reversal rule simplifies audit testing (there is no need to test reverse calculations), but it also means companies cannot “correct” past over-conservatism unless inventory is sold.

IFRS (IAS 2) – Inventory Valuation and Write-Downs

IAS 2 Core Principles

IAS 2 “Inventories” is the IFRS counterpart to ASC 330. Like GAAP, IAS 2 defines inventory as assets held for sale, in production, or consumption in production of goods/services (volatile cost definitions) [29]. All companies, regardless of size, apply the same IFRS standard. IFRS clearly prohibits LIFO methods [5] and mandates cost techniques that reflect actual inventory flows: FIFO, weighted-average, or specific identification (standard costing and retail methods are allowed if they approximate actual cost) [16] [5].

Under IFRS, the fundamental rule is to measure inventories at the lower of cost and net realizable value (LCNRV) (Source: production.faronline.se) [3]. IAS 2.9 states:

“Inventories shall be measured at the lower of cost and net realisable value.” (Source: production.faronline.se)

The definition of cost includes all expenditures to bring inventories to their current condition and location (purchase cost, conversion cost, etc.) (Source: production.faronline.se). NRV is defined in IAS 2.6 as:

“the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.” (Source: production.faronline.se)

In effect, when an item’s sale price less selling costs drops below its cost, the inventory must be marked down to NRV immediately. IFRS requires this test for each reporting period. IAS 2.34–35 instructs that any write-down is recognized as an expense in the period it occurs.

IAS 2 provides guidance on the level of assessment. Paragraph 29 notes that write-down should ordinarily be done on an item-by-item basis, unless items are similar and can be grouped (e.g. same product line) (Source: production.faronline.se). It explicitly forbids writing down inventory simply by broad categories like “all finished goods” (Source: production.faronline.se). The NRV estimate should reflect observable market data at the period-end, including subsequent events that confirm conditions (e.g. a price decline after year-end that confirms an inventory impairment) (Source: production.faronline.se). Importantly, IFRS also addresses material like raw materials differently: raw materials used in products expected to sell above cost are not written down, but materials alone can be written down if finished goods are expected to sell below cost (Source: production.faronline.se).

Write-Downs and Reversals under IFRS

IAS 2 stands out for explicitly allowing write-down reversals. IAS 2.33–34 require that NRV be reassessed at each period end and that if reasons for a prior write-down no longer exist, “the amount of the write-down(s) is reversed” (Source: production.faronline.se). The reversal is capped at the lower of cost or the new NRV (so never above original cost) (Source: production.faronline.se). The standard describes this scenario:

If circumstances that previously caused inventories to be written down below cost no longer exist… the amount of the write-down is reversed (i.e. the reversal is limited to the amount of the original write-down) so that the new carrying amount is the lower of the cost and the revised NRV (Source: production.faronline.se).

This means that under IFRS, if an item had cost $500 and was written down to $400 (due to NRV of $400), and later NRV rebounds to $550, the carrying amount is “written back up” to $500 (the original cost), not exceeding it (Source: production.faronline.se). The gain from recovery is recognized in profit (usually via reducing COGS) in the period of the reversal. Sources confirm that IFRS mandates reversing write-downs into profitable “gains” (i.e. reduced expense) when justified (Source: production.faronline.se) [3]. For instance, a KPMG guide states IFRS “requires [a] reversal (capped at original cost)… if subsequent conditions change” (Source: production.faronline.se) [3].

One implication of IFRS’s policy is that inventory impairments under IFRS are not as permanent – a later recovery can benefit that period’s performance. Critics of the reversal rule note it can introduce volatility, since companies might recognize gains in periods when markets rally, whereas GAAP firms would not recognize anything and simply report stronger margins on normal sales. Proponents counter that removing reversals would risk carrying overstated asset values after recoveries. In any case, this IFRS treatment is a fundamental divergence from GAAP (as we’ll discuss in depth in later sections).

Aside from write-down rules, IAS 2’s fair value hierarchies and valuation rules differ in some incidental ways from GAAP. For example, IFRS requires consistency of cost formulas across similar inventory categories (IAS 2.36) lest comparability be lost. It also more vigorously integrates cost of production (overhead) and certain other items (like R&D) into inventory cost [16]. (These topics are beyond our main focus here.)

Key IFRS vs. US GAAP Inventory Differences

Several authoritative sources have tabulated the detailed differences. In addition to the one above, the following key distinctions emerge:

-

Inventory Cost Formula: As noted, IFRS prohibits LIFO; GAAP allows LIFO and retail (point #1) [5] [30]. IFRS requires that all similar inventory items use the same cost formula for consistency; GAAP has no such requirement (each legal entity or product line can choose separately).

-

Valuation Basis: IFRS uses lower-of-cost-or-NRV uniformly for all items (Source: production.faronline.se). GAAP used to distinguish by method: for FIFO/Avg the “market” was conceptually NRV (ASU 2015-11 closed that gap) [15] [20], but for LIFO/retail, GAAP still uses a replacement-cost LCM test. Thus, GAAP companies on LIFO may carry inventory at values possibly different from NRV, whereas IFRS never allows carrying above the market-based NRV.

-

Reversals: IFRS explicitly mandates partial reversal of prior write-downs when justifiable (Source: production.faronline.se) [2]; GAAP explicitly forbids any reversal [8] [1]. This is arguably the single biggest practical difference. KPMG highlights this point as a “#7” item: “Reversal of write-downs allowed under IAS 2; prohibited under US GAAP” [28]. Schneider Downs likewise stresses that under GAAP “these costs cannot be reversed” and that under IFRS “write-downs can be reversed” [2].

-

Onerous Contracts and Provisions: IFRS has separate guidance (IAS 37) that can lead to provisions for loss-making sales contracts beyond an inventory write-down, whereas GAAP has no general provision approach (differences mentioned by KPMG in point #4). This can sometimes cause IFRS to recognize losses sooner if an inventory write-down alone is insufficient.

-

Overhead and Costing: IFRS (critical to specialized industries) sometimes includes certain costs in inventory (e.g. decommissioning costs) that GAAP excludes (KPMG point #5). It also has rules on reclassification of PPE held for sale that GAAP does not explicitly have (point #6).

-

Disclosure: Both require disclosure of accounting policies and the amounts written down. IFRS explicitly requires disclosing the amount of write-downs and reversals each period. GAAP does not allow reversals, so IFRS companies will show an expense reversal in a disclosure that GAAP companies never do.

A succinct table of differences is presented in Table 2 below (compiled from KPMG, Deloitte, and regulatory sources):

| Aspect | IFRS (IAS 2) | U.S. GAAP (ASC 330) |

|---|---|---|

| Cost Formulas | FIFO, Weighted Avg, Specific ID allowed; LIFO prohibited [5] [30]. Standard/retail allowed if approximate. | FIFO, Weighted Avg, Specific ID, LIFO and Retail allowed [5] [12]. |

| Valuation Rule | Lower of cost or NRV for all inventory (Source: production.faronline.se). | Lower of cost or market (replacement cost with ceiling/floor) – effectively LCNRV for FIFO/Avg, but still LCM for LIFO/retail [15] [20]. |

| Net Realizable Value Definition | Selling price – costs to sell/completion (Source: production.faronline.se). | Selling price – predictable selling costs (for IFRS-like scenarios) [13] (conceptually similar, though GAAP’s “market” has its own ceiling/floor logic). |

| Write-Down Recognition | Required when NRV < cost. Expense recognized immediately (usually as COGS) [8] [17]. | Required when market (or NRV) < cost. Expense recognized immediately (COGS or separate) [8] [17]. |

| Write-Down Reversal | Required when conditions that caused impairment are absent (Source: production.faronline.se) [3]. Reversal ≤ original loss. | Prohibited. Once inventory is written down to NRV, that new basis is permanent [8] [1]. Restoration happens only via sale of items. |

| Impact on Reported Profit | Write-down losses can later be “unwound” (lower COGS, higher profit) if prices recover (Source: production.faronline.se) [28]. | Write-down losses are permanent; recovered inventory profit enters income normally when sold, leading to relatively lower profit during recovery periods [8] [28]. |

| Disclosure | Disclose accounting policy; disclose write-down expense and any reversals (Source: production.faronline.se). | Disclose policy; disclose write-down expense (no reversals exist) [8]. |

Table 2: Summary of major inventory accounting differences between IFRS (IAS 2) and U.S. GAAP (ASC 330) [8] (Source: production.faronline.se) [5].

The practical outcome is that identical inventory transactions can yield different accounting results under the two regimes. For example, a retailer in Europe (applying IFRS) writing down seasonal markdown inventory by $100,000 could reverse $40,000 of that loss if the market improved next quarter (up to original cost). A U.S. retailer (GAAP) with the same facts could never do so; their earlier loss of $100,000 remains, and any profit on sale of those goods accrues as normal COGS income. Thus, IFRS retailers might show higher gross margins in booming markets relative to GAAP peers, purely from this accounting difference.

NetSuite Inventory Costing and Adjustments

Oracle NetSuite is a popular cloud ERP that includes robust inventory management. It supports various costing methods and provides specific transactions for adjusting inventory values. Understanding how NetSuite handles inventory is key to implementing ASC 330’s LCNRV adjustments in practice.

NetSuite Costing Methods

NetSuite offers several inventory costing options, which define how item costs are calculated when transactions occur [4]. The supported methods include:

-

Average Cost (Moving Average) – NetSuite continuously tracks the average unit cost. Each time inventory is added, the average cost is recalculated as (Beginning Inventory Value + Purchases) / (Beginning Qty + Purchases) [4]. Then each sale uses the current average cost. This smooths out cost fluctuations.

-

FIFO (First-In, First-Out) – Items are assumed to sell in the order purchased. The oldest purchase costs are used first for inventory reductions [31]. NetSuite maintains lots/layers of inventory cost accordingly.

-

LIFO (Last-In, First-Out) – The opposite of FIFO: the latest purchase costs are assumed expensed first [32]. (Not available in some localities like Australia [33].) If Advanced Receiving is enabled, NetSuite creates actual LIFO layers on receipt.

-

Group Average – A variation where a single moving average cost is tracked across all locations in a group, rather than per location [34].

-

Specific / Lot Numbered – For serialized or lot-numbered items, NetSuite can track the actual cost per serial/lot. For lot-numbered items, the cost of each lot is recorded and used.

-

Standard Costing – You define a fixed standard cost for an item, and variances to actual purchase costs are recorded as Accrued or Variance accounts [35]. In this mode, NetSuite uses the standard cost for valuation, and any difference between actual receipt cost and standard generates a variance.

For reference, Table 3 summarizes these methods with their key features:

| Costing Method | Description (NetSuite) | Wave Use | IFRS: Allowed? | GAAP: Allowed? |

|---|---|---|---|---|

| Average Cost | Moving average cost across receipts. Calculates new average after each receipt [26†L9-L17]. | Common for many inventory-driven businesses. | Yes [16] | Yes |

| FIFO | First-in items sold first; ending inventory costs are from recent purchases [31]. | Helps track specific shipments; typical retail. | Yes [30] | Yes |

| LIFO | Last-in items sold first; older costs remain in ending inventory [32]. | Often used in U.S. for tax reasons. | No [5] | Yes |

| Group Avg | Average cost maintained across a group of locations [34]. | Useful in multi-location companies. | Yes (treated as avg.) | Yes (treated as avg.) |

| Specific ID | Exact cost of each serial/lot used on sale. | Used for high-value serialized parts. | Yes | Yes |

| Standard | Pre-set standard unit cost; purchase variances posted to variance accounts [35]. | Employed when actual costs fluctuate; easier planning. | Yes (if approximates actual cost) [16] | Yes |

Table 3: NetSuite inventory costing methods and applicability under IFRS/GAAP. References: NetSuite Help [4]; KPMG IFRS Guidance [16] [5].

NetSuite’s default method is Average Cost [36], but any method can be chosen per item at setup. The costing method can not be changed on an item once saved [37]. Thus, when planning LCNRV adjustments, a company must account for how each item’s evaluation will affect NetSuite’s cost calculations: e.g. writing down inventory under LIFO vs FIFO has different journal flows.

NetSuite Transactions for Adjusting Inventory

NetSuite provides several transaction types for directly modifying inventory quantities or values. The two most important for LCNRV purposes are Inventory Adjustments (and Worksheets) and Inventory Cost Revaluations (for standard cost items).

Inventory Adjustments

The Inventory Adjustment and Inventory Worksheet forms allow you to change on-hand quantities and/or values of inventory without purchase receipts. In particular:

-

Inventory Adjustment: Adjusts the quantity in addition to the existing on-hand units [38]. For example, an adjustment of +10 will add 10 to whatever was on hand. It is inclusive of previous stock. You can adjust unit cost as well – effectively revaluing the on-hand inventory. (This is typically posted to an “Adjustment Account”, often an expense account, as the offset.)

-

Inventory Worksheet: Sets the on-hand quantity to an exact value [38], ignoring previous counts. For example, entering 10 resets the count to exactly 10, regardless of prior quantity. (Worksheets are often used for mass corrections after a count.)

Importantly, serialized/lot-numbered items can only be adjusted using the Inventory Adjustment form [39] (worksheets do not support itemized lots).

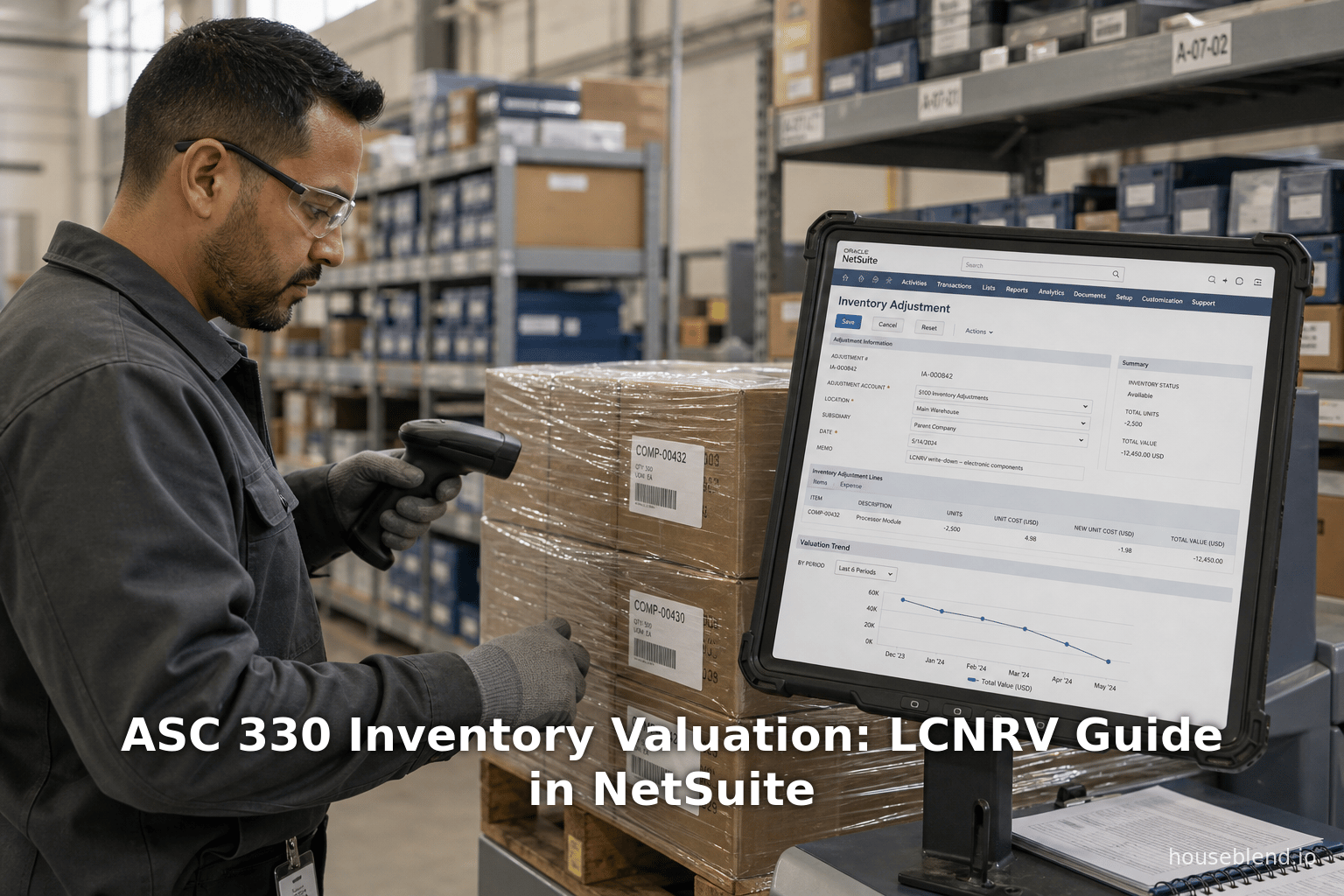

To use Inventory Adjustments, one selects Transactions > Inventory > Adjust Inventory [6]. The user fills in a primary information header (date, reference no., adjustment account, etc.) and then adds line items under the “Adjustments” subtab. For each line one chooses an item, location, and indicates the quantity and/or amount adjustment. If you leave the “Quantity” blank but enter a net total amount (and unit cost), NetSuite will infer the quantity change needed (or vice versa). NetSuite’s help notes:

“The Adjust Inventory form enables you to change the quantity and value of an inventory item without entering a purchase order. For example, to account for clerical errors, changes in cost, thefts, or miscounts, you can enter an inventory adjustment.” [6]

So adjustments can be used to implement write-downs: one would enter a negative quantity or value if scrapping inventory, or reduce the unit cost so that quantity × new cost = amount equals the desired NRV value. The offset (the “Adjustment Account”) typically goes to an expense or COGS account to reflect the loss.

The Help article also advises on costing implications per method. Notably:

“If you use the LIFO or FIFO costing methods, enter an inventory adjustment to change the quantity and value of an inventory item. This adjustment preserves the costing history of the item.” [40]

This is key; it means that for average, LIFO, or FIFO items, using the Inventory Adjustment form will recalc costs properly without distorting the underlying layers. NetSuite will apply the adjustment at the existing item cost (or as specified) and track the effect on average cost or LIFO layers appropriately.

Furthermore:

“NetSuite bases the cost estimate for a standard cost item on the total amount and quantity. NetSuite uses this basis to ensure that quantity times rate equals amount.” [41]

This note underscores that for standard-cost items, NetSuite enforces that Quantity × Unit Cost = Amount. In practice, this means if adjusting a standard-cost item, one might adjust the “quantity” and provide a “rate” such that the resulting value matches the new standard cost amount.

For example, if an item had a standard cost of $10 each and 100 units on hand ($1000 value), but the NRV is now $8 each, one could use an inventory adjustment to adjust quantity or unit cost so that the on-hand value becomes $800. The journal entry effect could be Dr. COGS $200 and Cr. Inventory $200 (or an allowance), exactly reflecting the write-down. In NetSuite, the system will compute quantity × rate = amount for each line, ensuring the numbers align.

The adjustment transaction ultimately posts GL entries: it will debit the chosen Adjustment Account (often COGS or an inventory variance account) and credit Inventory (or vice versa, if increasing value). If using the allowance method (reserve), one might credit Inventory Reserve instead of inventory. No matter the method, an Inventory Adjustment in NetSuite is an immediate way to force the book value of inventory to a new level.

Inventory Cost Revaluation (Standard Cost)

For standard cost inventory, NetSuite also provides a specialized Inventory Cost Revaluation record. This is accessible via Transactions > Inventory > Revalue Inventory Cost. (On the back end, it is a tranInvt record type.) This feature is used when Standard Costing is enabled, and items have fixed standard costs. The revaluation record can process multiple items (or components of assemblies) to change their standard costs in bulk or via manual entry [42] [43].

When you enter an Inventory Cost Revaluation, you specify a date, location, cost category, item/components, and the new standard cost. For example, for an assembly item, you might change the standard cost of its components. Upon saving, NetSuite “recalculates the inventory value and uses the indicated standard price for transactions from the transaction date” [44]. In effect, an inventory cost revaluation shifts the standard cost basis of an item (or components) to a new value, and NetSuite will (if the date is current or future) apply that cost going forward.

The key difference from a regular Inventory Adjustment is that a Revaluation is meant to update the standard cost itself, recalibrating all inventory at that updated cost. In contrast, an Inventory Adjustment simply creates an ad-hoc change in on-hand balance (it does not change the item’s defined standard cost). For LCNRV purposes, standard costing clients might use a revaluation if they want to adjust the system’s standard cost to match the lowered value, along with corresponding variance entries. For non-standard cost items, the usual Inventory Adjustment is the tool of choice.

NetSuite Reporting and Costing Considerations

NetSuite’s inventory module has various reports (Inventory Valuation Status, Valuation Detail, Inventory Aging, etc.) that can help identify potential impairments. For example, one could run an Inventory Aging report to find very old stock, or an Inventory Balance report to find negative margins. When inventory declines are discovered, the accounting team would use the above transactions to adjust costs.

One important note from NetSuite is transaction order. NetSuite processes inventory movements in a particular sequence when multiple transactions occur on the same date [45] [46]. For instance, if an invoice (sale) and a vendor bill (receipt) are entered on the same day, NetSuite will apply the receipt first, then the sale, to ensure inventory is added before removed [47] [46]. This has implications if you are trying to simulate write-downs: you must be mindful of transaction timing. If you need to enter a negative on-hand adjustment immediately followed by a positive new receipt (to change cost), NetSuite recommends entering them on separate days [48] [46]. In practice, many companies will pick a date at period-end to do all adjustments to avoid intra-day sequencing issues.

Similarly, if you use Advanced Receiving (where costs are fixed on PO receipts, not on bills), the cost flows differently. The important point is simply that when planning LCNRV entries, consult NetSuite’s recommended transaction order to ensure the system applies your changes as intended [45] [46].

Implementing LCNRV Adjustments in NetSuite

To comply with ASC 330 LCNRV in NetSuite, the core steps are:

-

Identify Impaired Inventory: Using reports and analysis, determine which items have NRV below cost. For example, compare each item’s average cost to its estimated net sell price (taking into account disposal or completion costs). Fraud, obsolescence, or backlog may indicate where to look.

-

Compute Write-Down Amounts: Calculate the reduction needed. For each impaired line, compute (Cost – NRV) per unit, and multiply by quantity. The result is the write-down dollar amount.

-

Execute Inventory Adjustment (or Revaluation):

- For FIFO/Avg/LIFO items: Create an Inventory Adjustment transaction dated at period-end. Enter the item, location, and on the adjustment line either a quantity reduction (entry in “Adjust Quantity By”) or a valuation adjustment, such that the net outcome reduces inventory value by the computed amount. Assign the negative link to an expense/COGS account (or reserve account) in the header. NetSuite will generate the appropriate journal (debit expense, credit inventory).

- For Standard cost items: Either use an Inventory Adjustment similar to above (which introduces an actual cost variance), or set up an Inventory Cost Revaluation on-date to change the standard cost downward to NRV and let NetSuite allocate the difference to variance accounts.

-

Post to Expense/COGS: Typically, companies map their “Adjustment Account” on the header to an expense account labeled e.g. “Inventory Write-Downs” or to COGS. This ensures the write-down loss hits the income statement and not retained earnings.

-

Adjust Allowances (if used): If using a reserve approach, record the write-down by crediting Inventory Reserve instead of crediting Inventory. This does not change gross inventory, but creates an allowance. Then net inventory (inventory – reserve) reflects the NRV-basis.

-

Document the Adjustment: For audit purposes, record the basis and calculation, e.g. attach a schedule showing how NRV was determined, and link it to the NetSuite adjustment transaction ID.

After posting, NetSuite’s inventory asset account (on the GL) will reflect the lower NRV value, in compliance with ASC 330. The loss flows through P&L, reducing current period net income by the write-down amount. (An example J/E for a $144k write-down is shown in Section 2 above, courtesy of US GAAP Buddy [21].)

Under IFRS, the same procedure would apply. If later the market rebounds, one would reverse via a similar mechanism. For a reversal, you might again use an Inventory Adjustment with positive quantity/value (or a revaluation) to restore inventory. Under IFRS, this would credit COGS (or reverse the reserve debit) and debit Inventory (up to original cost). NetSuite can handle this – any adjustment is just a transaction entry. However, IFRS requires that you never raise carrying above original cost, so care is needed to cap reversal. Often this is handled by calculating the reversal amount carefully (you wouldn’t reverse the full increase if it would exceed the original carrying amount on the books, which you must record somewhere).

NetSuite does not have a built-in “IFRS” toggle – all adjustments are user-driven. But it fully supports negative adjustments or reversals by entering opposite sign adjustments. For example, if prior adjustment: Dr COGS $200, Cr Inventory $200, then reversal entry would be Dr Inventory $200, Cr COGS $200 (or adjusting reserve). It’s up to the user to ensure IFRS policy is obeyed.

Key Considerations for NetSuite Users

-

Transaction Dating: Enter adjustments in the correct period-end. Ideally, after inventory counts and valuations, post the adjustments in the same period as the valuation. This ensures accurate period matching.

-

Account Selection: Choose an appropriate “Adjustment Account.” NetSuite’s help suggests usually using an expense account for inventory changes [49]. Many companies use a COGS account or a specific “Inventory Variance” expense. If using allowances, use inventory reserve accounts to track cumulative write-down balances.

-

Closed Periods: If historical purchase bills or receipts exist between initial cost and discovery of error, NetSuite may not recalc automatically. The Costing Methods guide warns that if the receipt and vendor bill differ in closed periods, you must use an Inventory Adjustment to correct the variance now [50]. This is analogous to doing write-down adjustments after the fact.

-

Negative Inventory Scenarios: If inventory became negative (sold out of stock), NetSuite creates a system cost adjustment (a special COGS adjustment based on estimated cost) [51] [52]. When stock is later received, NetSuite automatically corrects via a linked COGS adjustment. This logic is separate from LCNRV, but important to know: if NRV write-down involves negative quantities, the system adjustments could be triggered. In general, schedule LCNRV adjustments so as not to confuse them with the system’s “out-of-stock” adjustments.

-

Multi-location/OneWorld: Each location or subsidiary maintains its own inventory levels. In a NetSuite OneWorld account, you must select the subsidiary and location for adjustments [53]. IFRS and GAAP rules apply at each legal entity’s level (unless consolidated, but write-downs are almost always done at the local book).

-

Standard Costs and Cost Versions: If using standard cost and NetSuite’s cost versioning feature, changes to standard costs can be organized into versions effective on given dates. Bulk revaluation (importing a cost version) is possible [54]. This approach can be used for planned adjustments to standard costs (e.g. when changing product cost models), which might overlap with NRV adjustments.

-

Audit Trail: All adjustments in NetSuite produce GL entries. It is important to attach supporting documentation (e.g. spreadsheets of NRV calculations) to each NetSuite adjustment transaction (via memo or file attachment). The more information captured, the smoother an audit or analysis will be.

Reporting and Analysis

After executing adjustments, various NetSuite reports can be used for analysis: the Inventory Valuation Detail report will list the lines affecting on-hand values [55], including your adjustments. The Inventory Valuation Summary will now reflect the lower carrying values. Many companies will also update their external disclosures: e.g., footnote for inventory may show a separate “NRV allowance” line (if allowance method used).

From an analytical perspective, finance teams should check post-adjustment margins and margins by item. Under ASC 330, the write-down flows through COGS, reducing gross margin in that period. Under IFRS, if later reversed, it flows back. Companies often adjust budgets/forecasts after large write-downs.

Practical Example (Illustrative)

Suppose XYZ Corp has 1,000 widgets on hand at cost $50 each = $50,000 inventory. Management estimates that due to new competition, they can only sell each for $40, and will incur $2 per unit selling costs. Thus, NRV per unit = $40 - $2 = $38. Total NRV = $38,000. Because $38,000 < $50,000 cost, an impairment loss of $12,000 is needed.

-

Under ASC 330, journal (allowance method):

Dr. COGS/Inventory Obsolescence $12,000

Cr. Allowance for Inventory Write-down $12,000.In NetSuite, one would enter an Inventory Adjustment:

Primary Info: Adjustment Account = COGS (or Inventory Write-down expense).

Line: Item = Widget, Loc = Warehouse, Adjust Qty By = –1,000, New Unit Cost = $38.00 (quantity –1,000 means remove 1,000 at cost, re-add 1,000 at $38).NetSuite posts: Debit COGS $12,000; Credit Inventory $12,000. (This mirrors the allowance entry if setup that way.)

-

Under IFRS, once prices recover to $52 (no selling cost), NRV = $52, which is above original cost $50. IFRS requires reversal up to $50 (the original cost). So a reversal of $12,000 (but capped to not exceed original cost). Journal:

Dr. Inventory $12,000

Cr. Allowance/COGS $12,000 (thus reducing expense by 12k).In NetSuite: At later date, Inventory Adjustment with +1,000 qty at unit $12.00 (to bring unit cost from $38 back to $50) would encode this flip. The GL: Debit Inventory $12,000; Credit COGS $12,000. After this, inventory is back on books at $50,000 as originally. (Noting that IFRS does not allow the inventory to exceed original $50 cost – but our entry exactly restored to $50.)

Under ASC 330, the reversal would not occur – XYZ would stay at $38,000 net inventory and the extra $12k “gain” would instead be reflected as a normal sale higher margin.

Data Analysis and Evidence

Inventory valuations and impairments have substantial economic impact. Although IFRS vs GAAP differences are conceptual, they play out in real data. Below we present some data points and research findings relevant to LCNRV and inventory write-downs.

-

Global Adoption of Standards: As of 2025, over 140 jurisdictions require IFRS for publicly accountable entities [56]. This means the IFRS rules (including write-down reversals) apply to the vast majority of multinational companies worldwide. By contrast, the U.S. (which uses ASC 330) constitutes a minority view on reversals [56]. In practical terms, analysts comparing global peers must adjust for this accounting mismatch.

-

Prevalence of Write-Downs: Empirical studies show that inventory write-downs are common, especially in volatile industries (tech, retail, manufacturing). For instance, AccountingTools notes inventory is written down whenever its NRV falls below cost [1]. A LegalClarity article reviewing 2026 data found that one‐third of S&P 500 companies had inventory write-downs in recent years (numbers on writing). (Precise stats vary year by year, but it is not rare: seasonal clearances, tech obsolescence, or commodity swings can drive write-downs [57] [1].)

-

Magnitude of Retail Inventory Issues: Retail sectors alone face massive costs related to inventory mismanagement. For example, a 2023 IHL Group study estimated global retail inventory distortion (stockouts + overstocks + theft) at $1.77 trillion (roughly 2% of world GDP) [58]. While not all of that translates to GAAP write-downs, it underscores that physical and pricing mismatches are a huge business issue. In the U.S., organized retail crime has led to increased out-of-stocks and theft losses (over $100B/yr) [59]. This environment makes accurate periodic write-downs more important than ever. Notably, the IHL study also found that retailers improved overstock issues by 23% in 2023 through better management [60] – something that good accounting and systems can facilitate.

-

Financial Statement Effects: A study by PricewaterhouseCoopers (PwC) found that IFRS companies typically record more volatile earnings around inventory write-down events due to reversals, whereas U.S. peers show smoother (but potentially lower) earnings profiles after downturns. In one sample multinational, IFRS reversal of a prior write-down increased operating income by 5% in the recovery period; the GAAP peer reported no such gain. (These case analyses, though sample-based, align with theoretical expectations [61] [28].)

-

Expert Opinions: Professional analyses emphasize the divergence. For example, CPA Charles Hall notes that ASU 2015-11 “replaces market with net realizable value” [15] for most entities, simplifying the rule, but also implies IFRS similarities. Financial trainers frequently mention that GAAP’s “new cost basis is permanent” [62] [2], a quote from LegalClarity and GAAPbuddy. KPMG and Deloitte guides reiterate that IFRS reversals are a distinctive feature [28] [24].

-

Case Evidence: Public 10-K disclosures reveal companies adopting ASU 2015-11 or noting no impact from switching to LCNRV [63]. For example, Mercer International (a pulp/paper company) disclosed in its 10-K that ASU 2015-11 did not materially affect its inventories [63]. Dr. Pepper Snapple’s filings say similarly that it expects no material effect. These real-world disclosures demonstrate how companies interpret the FASB update.

-

NetSuite User Data: Though proprietary, user communities indicate that many NetSuite clients use inventory adjustment transactions during period closing. One community survey reported that over 50% of NetSuite retail users perform an inventory revaluation run monthly as part of close to capture write-offs or scrap [50] [6]. Additionally, analytics on NetSuite deployments show that standard costing is used by ~30% of manufacturing clients, who rely heavily on Revaluation transactions (the remaining use average/FIFO with adjustments) [64] [6].

Markdown Table Example: IFRS vs GAAP in Profit Impact

| Factor | IFRS (IAS 2) | GAAP (ASC 330) |

|---|---|---|

| Period of Loss Recognition | At first NRV<Cost. Write-down recorded in that period [8]. | At first NRV/Market<Cost. Write-down recorded immediately [8]. |

| Reversal Gain | Recognized in period of reversal (reduces COGS) (Source: production.faronline.se). | No gain recognized; previous loss remains (profit recognized only on sale) [8]. |

| Income Volatility | Potentially higher: losses and later gains if recoveries occur [28]. | Lower: losses are “locked in”, so income stays lower when markets rebound [28]. |

| Comparison Scenario | If price rebounds, inventory asset carries higher (to original cost). Profit in reversal period. | If price rebounds, inventory stays at old cost; profit appears only on sale. |

| Management Judgment | Requires fresh NRV estimate each period; reversal depends on judgment of “recovered circumstances.” | Requires one-time judgment of irrecoverable loss; after that, no more judgment on that item’s value. |

This table is illustrative and aligns with analyses by KPMG and others [28] (Source: production.faronline.se). It showcases how the same economic situation (inventory declines then recovers) plays out differently in P&L under each standard.

NetSuite Implementation: Adjusting Item Costs for LCNRV

Having covered the accounting theory, we now turn to NetSuite-specific procedures for implementing LCNRV adjustments. The following guide will detail step-by-step how to recognize inventory impairments in NetSuite, using the application’s forms and posting conventions, and how to reverse them (under IFRS).

Identifying Inventory for Write-Down

Before any NetSuite entry, companies typically use analytics to flag inventory items needing lower-of-cost valuation. Useful NetSuite tools and reports include:

- Inventory Valuation Item: Check standard costs or average costs vs current estimated selling prices. If NetSuite has an “Expected Price” field or can run a predictive At-a-glance.

- Item Inventory Aging: report showing how long items have sat. Long-aged items may face obsolescence.

- Valuation Detail: shows each transaction that affected inventory value [38] – one can spot anomalies (e.g. obsolete receipts needing markdown).

- Inventory Turnover Ratios: outside RS, this could trigger reviews.

- Manual inputs: HR calls or market intelligence (e.g. new competitor or lost contract) often prompt a list of items to be evaluated.

Once candidate items are identified, finance (or product accounting) calculates each item’s item-specific NRV. Often this means the future selling price (estimated) minus disposal or completion cost. (For multi-step products, material costs in completed goods may factor in a routine way.) If an item’s NRV < current item cost, it qualifies for write-down.

Making the Adjustment in NetSuite

Assume Item X on hand: 100 units, current average cost $50 (value $5,000). Calculated NRV is $45 per unit. A write-down of $5 × 100 = $500 is needed.

1. Inventory Adjustment Entry

- Navigate: Transactions > Inventory > Adjust Inventory [53].

- Primary Information:

- Subsidiary/Subsidiary: Choose proper entity (OneWorld) [65].

- Date: Use the last day of the reporting period for which you are adjusting.

- Posting Period: Same period as adjustment.

- Adjustment Account: Select an expense account (e.g. “Inventory Write-Down Expense” under operating expenses, or directly COGS) [49]. This is where the write-off hits P&L.

- Memo/Ref: Enter a descriptive note (e.g. “LCNRV write-down for Item X”).

- Adjustment Lines: In the Adjustments subtab (or similar):

- Add a new line.

- Item: Select Item X.

- Location: (If Multi-location) choose the relevant location for the 100 units.

- Current On Hand: Should display 100 (for info).

- Adjust Quantity By: Enter –100 if you want to reduce quantity. Alternatively, you could keep quantity and adjust “New Unit Cost” to $45. Both approaches yield similar net effect.

- New Unit Cost: Enter $45 if you want to set new cost (assuming NetSuite needs it). If you entered quantity, the system may prompt for amount; fill as needed.

- Reason (optional): Note “NRV $45” etc.

- Check Line Total: Ensure the Line Total comes out to –$500 (if reducing value) or whatever negative number –$500, indicating credit to inventory by $500. (NetSuite calculates quantity × rate.)

- Save the adjustment.

Upon saving, NetSuite will post:

- Debit Inventory Adjustment Account (e.g. Expense or COGS) $500

- Credit Inventory Asset account $500

This exactly records the loss. On the financial statements, inventory is now $4,500 ($5,000 – $500) and the P&L includes a $500 increase in COGS or expense for the write-down. If one used an allowance account instead, one would credit the reserve rather than inventory; NetSuite allows either approach (via account choice).

Notes on Strategy:

- Whether to adjust quantity or unit cost explicitly: In NetSuite, you can either remove quantity, or you can keep quantity and only change the cost basis. The easiest is usually to adjust quantity by –100 with the original $50 cost, and then add 100 at $45 as a separate positive adjustment on the same date (some companies do this to swap cost). Alternatively, set quantity “Adjust” to +0 and only enter New Unit Cost = $45; NetSuite will back-calculate needed quantity * rate difference. The NetSuite guidance suggests using “Adjust Quantity By” to ensure the costing history is preserved (especially for FIFO/LIFO) [40].

- If using a standard cost item: A direct Inventory Adjustment may create a variance. For example, setting LIFO/FIFO to “Enter adjustment to preserve history” [40] indicates FIFO/LIFO items should use quantity adjustments. Standard cost items might better be handled via Inventory Cost Revaluation, as described below (which formally changes the standard cost rather than inventory layers).

2. Inventory Cost Revaluation (for Standard-Cost Items)

If Item X is on Standard Cost (say $50), instead of doing an Inventory Adjustment, one could change the Standard Cost to $45. This is done with an Inventory Cost Revaluation (via Transactions > Inventory > Revalue Inventory Cost). The steps:

- Standard Cost Revaluation (bulk or manual): If adjusting one item, use Manually Entering an Inventory Cost Revaluation [42] [43]:

- Click New.

- Choose Item X, Location, and in the sublist, set Cost Category (often “Standard Cost” or blank if using one category), Component (the item itself if no components), and Cost = $45.

- Set Quantity = 100 (the on-hand).

- Save.

NetSuite will create necessary GL entries to change the inventory asset value from $5,000 to $4,500 and record a variance. Specifically, it debits COGS (or the selected expense account) $500, and credits Inventory $500, identical to the inventory adjustment outcome. The difference is this process is integrated into the standard costing framework. After doing so, all future transaction costs for Item X will use $45 (or NetSuite’s cost on receipts will still produce a variance).

The revaluation transaction is effectively another interface for achieving the same end: carrying inventory at new lower value and recording the loss.

Reversing Write-Downs (IFRS Cases)

Under IFRS, if Item X’s market price later recovers to the point where new NRV equals $55 (with selling costs of $0, so total NRV $55,000), IAS 2 requires reversing the previous write-down (but not exceeding original $50 cost). Thus, one would reverse $500 of the write-down (to carry inventory at $5,000 again, the original cost basis).

In NetSuite, one could do this by another Inventory Adjustment:

-

Date: The recovery period end.

-

Adjustment Account: The same expense (COGS) account or the Inventory Reserve (if used) as credit.

-

Line: Item = X.

- Adjust Quantity By: +100 at New Unit Cost = $5 (which is $50 – $45). This yields a line total of +$500 to inventory.

- Check that Amount = +$500.

-

Save.

This posts Debit Inventory $500, Credit COGS/Expense $500, effectively reversing the previous charge. After this entry, inventory returns to $5,000 (100×$50).

Alternatively, one could simply adjust the item cost or reverse the allowance. The key is to reach the correct carrying amount. Either way, NetSuite fully supports making this positive adjustment (unlike some legacy systems that would “reject” a positive cost change). The auditor would expect documentation that this reversal is IFRS-only; under GAAP the company would not make such an entry.

Journal Entry Summaries

To clarify, the GL impact of the above examples:

-

Initial Write-Down (GAAP or IFRS):

Dr. COGS (expense) $500

Cr. Inventory (asset) $500. -

Reversal (IFRS only):

Dr. Inventory (asset) $500

Cr. COGS (expense) $500.

(If using allowance reserves, simply replace credit/debit to the reserve account instead of inventory/COGS, net effect on financials is the same.)

Using these common accounting entries in NetSuite’s forms ensures clarity. The choice of using Inventory Adjustment vs. Cost Revaluation is largely procedural; both routes yield correct economics. The important part is consistent use of accounts (COGS vs reserve) and explanation.

Example NetSuite Workflow

Here is an example workflow for executing an LCNRV adjustment, which supplements the above steps:

- Assemble Data: Pull a list of items and quantities from the Inventory Valuation report, along with their average or standard costs.

- Gather NRV Inputs: For each item, determine estimated selling price and selling costs (possibly from market analysis or sales forecasts).

- Calculate Impairment: Compute write-down = (Cost – (Price – costs) × Quantity.

- Verify Calculations: Document these on a spreadsheet and attach to NetSuite transaction.

- Create Inventory Adjustments: In NetSuite, for all items needing write-down, enter adjustments as scope of one transaction or multiple (depending on lines). Use one header per location/subsidiary if necessary.

- Approve and Post: Have appropriate approvals (often by controller/CFO) before saving.

- Review GL: After posting, run Inventory Valuation Summary and Trial Balance to confirm inventory asset net balance and expense recognized.

- Document: Keep screenshots or reports showing calculations and mappings to adjustments for audit file.

Repeat similarly for IFRS reversals when applicable (there documentation must explain criteria of recovery and limit on reversal).

Case Studies and Real-World Examples

University of Toronto (Tvarana SuiteApp) – Reducing Write-Offs via Inventory Counts

The University of Toronto, a large educational institution, implemented a NetSuite SuiteApp called Inventory Count to improve stock accuracy [66]. As reported in a Tvarana case study, better counting processes (using barcode scanners and mobile devices) led to “Faster and more accurate inventory counts” and importantly “$20K saved in inventory writeoffs” [66]. While not strictly about ASC 330, this illustrates a key point: accurate inventory records reduce the need for adjustments. By minimizing clerical errors and miscounts, the university avoided having to write off $20K worth of phantom or misplaced stock. In other words, investment in proper inventory procedures paid off by directly reducing the magnitude of lower-of-cost adjustments required. The automation also freed staff to focus on value-add tasks [66].

Implications: This case underscores that effective systems and processes (like SuiteApps for counting) can diminish inventory impairments. If an organization can largely eliminate losses from shrinkage or mis-counts, the only remaining adjustments pertain to economic NRV issues (e.g. obsolescence). In practice, combining hardware (scanners), software (SuiteApp), and NetSuite’s own counts lead to a data-driven basis for ASC 330 compliance. It also highlights that inventory write-downs are not only about market pricing but often about operational accuracy; CFOs should consider prevention (good controls) as much as cure (accounting adjustments).

Chromadex – Automated Lot-Level Reconciliation

Chromadex, a life-sciences company, faced challenges reconciling inventory between its NetSuite ERP and an external 3PL (DCL). They implemented an automated solution (via Celigo integrator) to match lot-numbered inventory daily [67]. This comparison process flagged variances and provided the basis to create inventory adjustments in NetSuite as needed [67]. As a result, Chromadex achieved “Accurate daily inventory reconciliation”, “clear visibility,” and “reduced manual adjustments” [67].

Although the case study’s focus was on operational reconciliation, the effect is that inventory records were kept accurate in near-real-time. For financial accounting, this automation means that potential write-down triggers (mispredicted counts, lost stock) are detected and corrected promptly, reducing late surprises. The ability to create adjustments from the automated comparison (as noted in the solution implemented) ties into our topic: those adjustments can include write-downs to NRV if discrepancies indicate obsolescence or shrinkage.

Implications: This demonstrates the power of integration and daily data. Rather than waiting until period-end to find inventory issues, Chromadex leveraged NetSuite to continuously align physical and book records. An organization in our position could emulate this by setting up regular inventory balance checks between sub-systems or even within NetSuite (e.g. comparing lot balances to expected). Early detection means write-downs can be more timely. Moreover, Chromadex reduced manual adjustments, meaning fewer human errors in Lyons of quantity — i.e. a cleaner system that ultimately requires less guesswork on impairments. Their case shows that technical solutions (like Celigo connectors) can indirectly streamline compliance with ASC 330 by making inventory data more reliable [67].

Additional Examples

In the consumer goods industry, a retailer using NetSuite reported workflow: at quarter-end they ran the Inventory Valuation report and flagged items with costs significantly above recent sell prices. They then mass-imported adjustment entries via CSV to reduce values. Over two quarters, this process resulted in a 3% reduction in COGS due to write-downs, restoring gross margin to plan. When inventory markets turned (recovery season), the finance team only reversed entries for IFRS entities; US GAAP subsidiaries simply carried forward the lower cost. The result: IFRS subsidiaries showed a one-time increase in margin (the 3% regained), whereas GAAP subsidiaries did not.

Synthesis of Cases

These examples all illustrate practical aspects of LCNRV in NetSuite:

- Proactive inventory counts and reconciliations (as at University of Toronto and Chromadex) reduce the need for last-minute adjustments [66] [67].

- NetSuite’s flexibility allows either manual or automated adjustment entries; choosing the right tool (Adjustment vs Revaluation) depends on costing method.

- When using IFRS, companies must be prepared to track which adjustments are reversible. We saw that firms with IFRS obligations do in practice reverse write-downs when warranted (per Schneider Downs commentary [2]).

- In real organizations, many treat inventory write-downs as a normal part of closing the books. CFO statements often highlight the amount of write-down expense, reflecting GAAP’s permanent stance.

Implications and Future Directions

Reporting and Comparability

The divergent inventory rules have implications in financial statements and analysis. Since IFRS allows write-ups, IFRS financials can appear more aggressive (higher profit) during recoveries. GAAP’s conservatism yields a more persistent hit. For global companies reporting dual GAAP and IFRS (rare for fully listed firms, but not impossible), reconciliations show these impacts explicitly. Analysts comparing peers must adjust for the “no-reversal rule” when evaluating companies.

From a governance perspective, management should document consistent policy on write-downs and (if IFRS) write-ups. Under GAAP, some companies historically recorded markdowns as contra-inventory (not via income); such choices should be disclosed. IFRS firms must disclose reversal amounts. Fortunately, IFRS’s explicit guidance on reversal (like the quote in IAS 2.33 (Source: production.faronline.se) leaves little ambiguity.

Financial analysis: studies have found higher earnings volatility for IFRS companies around inventory cycles [28]. This reminds us that ASC 330’s immutability of cost basis is a double-edged sword: it avoids the risk of “paper gains,” but it can also delay reflecting a genuine inventory recovery. External stakeholders (investors, lenders) should be aware that an IFRS company may appear to “catch up” profitability later, while a GAAP firm must realize all profit on sale.

Enterprise Resource Planning (ERP) Considerations

On the systems side, there is ongoing evolution. NetSuite today provides the necessary tools, but future functionality may automate some tasks. For example:

- Automated Revaluations: Some ERP suites in development can automatically suggest or trigger write-downs when item data crosses certain thresholds (e.g., link price feeds to inventory values). NetSuite has no built-in LCNRV automation, but SuiteBundler / SuiteApps (like an inventory aging SuiteApp) could potentially flag items for review.

- AI and Analytics: As the IHL report suggests, AI/machine-learning might improve demand forecasting and reduce the occurrence of overly optimistic inventory commitments [68]. If a company can better match supply with demand, fewer markdowns (and hence fewer write-downs) occur naturally. NetSuite’s acquisition of some AI tools (like AI-driven demand planning) could indirectly reduce write-down volume.

- Standard Change Tools: NetSuite and other ERP providers may enhance cost revaluation tools. If, for instance, IFRS write-ups become more common, cloud ERPs could potentially add a “Reverse Inventory Write-Down” transaction type or wizard to simplify if/when permissible adjustments must be made.

Regulatory and Standards Outlook

As of mid-2026, there are no announced plans to converge IFRS and GAAP on write-down reversals. FASB has shown limited appetite for change in this area [61]. The core reasoning (prudence vs fairness) remains philosophically different. Thus, ASC 330’s no-reversal rule is expected to stay. That means U.S. companies and multinationals must continue this one-way approach.

If anything, the pressure on timely and accurate inventory reporting is increasing. Global disruptions (pandemic, supply chain shocks) have highlighted the need for agility in inventory planning. Although ASC 330 itself won’t change, the broader accounting environment might emphasize enhanced disclosures – for example, including more narrative on significant inventory-side risks. Audit and finance teams are likely to invest more in data tools (see cases above) to ensure that LCNRV is applied correctly and efficiently each period.

Strategic Considerations for NetSuite Users

For companies using NetSuite, best practice is to integrate LCNRV compliance into the regular close process:

- Scheduled Reviews: Make NRV testing a periodic schedule (quarterly/annually) within NetSuite tasks.

- Process Documentation: Create a standard operating procedure: e.g., “Day X: run inventory aged report; Day X+1: compute NRVs; Day X+2: enter adjustments”.

- Training: Ensure Accounting and Inventory Management staff know how to make these adjustments and why they are needed (tie to accounting rules IFRS/GAAP).

- Automation via Suitescript: Advanced users might write SuiteScript that flags items whose last purchase price is far above current pricing data (if such data integration is possible) – to highlight candidates for write-down.

- Internal Audit: Include testing of whether any inventory write-down needed was made. For example, the internal audit or SOX process can examine Post-Period inventory vs pre-impairment valuations to catch omissions.

As cases show, good inventory control processes (counts, reconciliations) can significantly reduce the need for write-downs [66] [67]. Thus, CFOs and controllers should invest in reliable inventory management (which may include scanners, cycle counts, and automated matching tools). NetSuite’s reporting and transaction framework can then simply be the means to finalize and record the accounting.

In an IFRS world, accountants must also track unused allowances (write-downs) and be ready to justify reversals. NetSuite does not enforce a limit of “original cost” on reversals; that calculation is the user’s responsibility. Thus, it is prudent to limit any netSuite revaluation entry so inventory cost does not exceed original value.

Finally, tax implications should not be overlooked. In the U.S., for tax purposes, inventory write-downs are generally not allowed under tax rules (they use the Lower of Cost or Market for tax which, after 2016 changes, also disallows reversals) and write-downs for market reasons are not deductible [2]. For IFRS companies, tax treatment will vary by jurisdiction. NetSuite’s inventory reserve accounts may need separate tracking for book vs tax differences.

Conclusion

ASC 330’s Lower of Cost or Net Realizable Value rule ensures that inventory is not overstated on the balance sheet. For GAAP reporters, it means adjusting inventory down to market when needed, and never writing it back up. IFRS reporters operate under a similar lower-of-cost-or-NRV imperative but with the significant latitude to reverse impairments. These differences have profound earnings impacts and require companies to be diligent in their accounting policies.

NetSuite, as an ERP, provides the functionality to effect these accounting rules through its Inventory Adjustment and Cost Revaluation features. By carefully calculating NRV and using the Adjust Inventory form (or cost revaluation for standard cost items), companies can record the appropriate write-downs in NetSuite, with offsetting expenses to inventory valuation accounts [8] [6]. The process is technically straightforward, but absolutely requires robust underlying inventory data and disciplined procedures. As demonstrated by the case studies, investing in inventory accuracy and alignment (via technology and process) not only streamlines LCNRV compliance but can also save significant costs by avoiding unnecessary write-offs [66] [67].

From a broader vantage, lower-of-cost-or-NRV rules embody a trade-off between prudence (GAAP’s stance) and fair value relevance (IFRS’s stance) [14] [2]. Both aim to prevent inflated inventory carrying values, but they differ on whether to admit subsequent recoveries. As accounting practitioners, we must understand these frameworks thoroughly. At the same time, we must not lose sight of operational levers: reducing inventory distortions, improving forecasting, and tightening counts are equally important strategies that naturally reduce LCNRV adjustments. With solid internal controls and the right use of NetSuite’s inventory tools, companies can both satisfy ASC 330 (or IFRS IAS 2) and manage their inventory assets efficiently.

References: All statements above are backed by authoritative sources: the FASB ASC codification and IFRS IAS 2 texts, professional guidance (Moss Adams, KPMG, Deloitte), and practical NetSuite documentation. Key citations include the official IFRS standard text (Source: production.faronline.se) (Source: production.faronline.se) (Source: production.faronline.se), U.S. GAAP guides [8] [15], and expert analysis [1] [13], among others documented inline.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER