Houseblend Article

ASC 330 vs IFRS: Inventory Write-Down Reversals Explained

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03IFRS Guidance on Inventory Write-Downs and Reversals

- 04U.S. GAAP Guidance on Inventory Write-Downs and Non-Reversals

- 05Conceptual and Historical Perspectives

- 06Effects on Financial Statements

- 07Broader Perspectives and Case Studies

- 08Implications and Future Directions

- 09Conclusion

Executive Summary

This report examines the contrasting treatment of inventory write‐down reversals under U.S. GAAP (ASC 330) and IFRS (IAS 2). Both frameworks require inventories to be valued at the lower of cost and recoverable amount, ensuring overstated inventory values are written down. However, a pivotal difference is that IFRS expressly allows reversing a previously recognized inventory write-down (to the extent of the original write-down) if net realizable value (NRV) recovers, whereas U.S. GAAP strictly prohibits any reversal of an inventory impairment [1] [2]. Under IFRS, IAS 2 ¶33–34 mandates that when circumstances causing the write-down no longer exist (e.g. market prices recover), the inventory’s carrying value is written back up (but never above original cost) (Source: eur-lex.europa.eu) [3]. In contrast, ASC 330‐10‐35−2 establishes a new cost basis at the write-down and forbids any subsequent write-up, reflecting GAAP’s conservatism ― losses are recognized promptly, but potential recoveries are ignored [2] [1].

This divergence has meaningful implications for financial reporting and stakeholder analysis. Practical impacts include income volatility (IFRS income rises on recoveries, GAAP income remains flat) and cross-border comparability issues. Proponents of IFRS’s approach argue it better represents economic reality by acknowledging reversals, while GAAP defenders emphasize prudence and the avoidance of “anticipating gains”. This report delves into the historical and conceptual origins of these differences, synthesizes authoritative guidance, and analyzes their effects through data and examples. We find that the IFRS policy of write-down reversal (capped at original cost) stems from IFRS’s fairness principle (lower of cost or NRV) (Source: eur-lex.europa.eu) [3], whereas GAAP’s no‐reversal rule reflects a traditional conservative bias [2] [1].

Key findings include:

- Technical Guidance: IFRS (IAS 2) requires inventories to be measured at the lower of cost or NRV and explicitly permits reversal of write-downs when NRV recovers (Source: eur-lex.europa.eu) [3]. U.S. GAAP (ASC 330) uses a lower-of-cost-or-market approach (including special rules for LIFO/RIM) and flatly prohibits any reversal of write-downs [4] [2].

- Conceptual Rationale: GAAP’s approach is rooted in prudence (“losses recognized early, gains only when realized”) [5] [1], while IFRS stresses relevance and faithful representation (avoiding understatements when values recover) [3] [6].

- Impact on Reporting: Empirical effects include differences in revenues and costs of goods sold in periods of price recovery. Under IFRS, inventory recovery lowers COGS (raising profit), whereas under GAAP the earlier loss “sticks” [6] [3].

- Convergence Status: Despite extensive convergence efforts, this issue remains unresolved. No major standard-setting activity proposes changing GAAP’s stance; practitioners generally expect the divergence to persist.

This report provides a detailed analysis of these issues, citing authoritative sources (IFRS standards, ASC codification, and professional analyses) and illustrating with figures and tables. It addresses historical context, current rules, and future implications, aiming to give practitioners and academics a deep understanding of why U.S. GAAP prohibits write-down reversals while IFRS mandates them.

Introduction and Background

Inventory accounting dictates how businesses value goods held for sale, impacting key financial statement metrics like current assets and cost of goods sold. Both U.S. GAAP and IFRS aim to ensure inventory is not carried above what will ultimately be realized. In this context, a write-down occurs when inventory’s net realizable value (NRV) falls below its cost. Under strict conservatism, one may write down the inventory value to NRV and recognize a loss immediately in earnings. The pivotal question is whether that write-down can ever be reversed if market conditions improve.

Under IFRS (IAS 2), inventories are measured at the lower of cost and net realizable value (NRV) [7]. IAS 2.9 states:

“Inventories shall be measured at the lower of cost and net realisable value.” [7].

Net realizable value (IAS 2.6–7) is defined as “the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale” [8]. In IFRS, any write-down of inventory to NRV is recognized as an expense in that period . Crucially, IAS 2 explicitly addresses reversals: when conditions causing a write-down cease to exist (e.g. market prices rebound), “the amount of the write-down is reversed (i.e. the reversal is limited to the amount of the original write-down) so that the new carrying amount is the lower of the cost and the revised net realisable value.” (Source: eur-lex.europa.eu). Thus, IFRS mandates that inventory write-downs be reversed to the extent of the original write-down (never above original cost) when NRV increases (Source: eur-lex.europa.eu) [3].

In contrast, U.S. GAAP (ASC 330) historically applied a “lower-of-cost-or-market” (LCM) rule, which for most inventory methods effectively became a lower-of-cost-or-net realizable value rule under ASU 2015-11 [9] [4].In GAAP, once inventory is written down, ASC 330.35-2 establishes that this new cost basis is permanent: “no subsequent write-up of inventory is permitted if the market value of inventory increases.” [2] [1]. In other words, ASC 330 prohibits any reversal of an inventory write-down, reflecting GAAP’s traditional conservatism (recognizing losses promptly but never reversing them in anticipation of recoveries) [5] [1]. The practical effect is that GAAP entities carry impaired inventories at the lower amount permanently, even if market values recover later.

Table 1 below summarizes key differences between IFRS and GAAP for inventory valuation and write-downs. These rules have significant effects on reported profits and asset values, which we explore with evidence and examples in subsequent sections.

| Feature | IFRS (IAS 2) | U.S. GAAP (ASC 330) |

|---|---|---|

| Measurement basis | Lower of cost or NRV (IAS 2.9) [7]. (No LIFO, only FIFO/Wtd Avg/Specific ID allowed [10].) | Lower of cost or market. For FIFO/average cost, cost vs. NRV; for LIFO/RIM, cost vs. market (replacement cost + rules) [4]. |

| Cost formulas | FIFO, Wtd. Average, Specific ID (LIFO prohibited) [10]. | FIFO, Wtd. Average, Specific ID, LIFO allowed (and Retail method). |

| Write-down trigger | NRV < cost (write-down recognized in P&L) (Source: eur-lex.europa.eu). | “Market” < cost (write-down to NRV or “market” recognized in P&L) [4] [2]. |

| Subsequent reversal | Required when original write-down causes no longer exist (NRV rises). Reversal limited to original loss (Source: eur-lex.europa.eu) [3]. | No reversals allowed under any circumstances [2] [1]. Loss is permanent (historical cost is reset). |

| Effect on profits | Reversal reduces COGS (increases profit) in period of recovery (Source: eur-lex.europa.eu) [3]. | No gain recognized on recovery – earlier loss remains; profit is lower compared to IFRS in recovery scenario [1]. |

Table 1: Comparison of key inventory valuation rules under IFRS (IAS 2) and U.S. GAAP (ASC 330) [7] [2] [4] [1] [3].

IFRS Guidance on Inventory Write-Downs and Reversals

Under IFRS, IAS 2 – Inventories is the authoritative standard. Its core principle (IAS 2.9) is that “inventories shall be measured at the lower of cost and net realisable value” [7]. All entities apply the same rule regardless of costing method (FIFO, weighted-average, or specific identification) [11]. Unlike U.S. GAAP, IFRS prohibits LIFO entirely [11] [10].

IAS 2.34–35 clarifies the accounting for write-downs and reversals. Paragraph 34 requires that “the amount of any write-down of inventories to net realisable value… shall be recognised as an expense in the period the write-down or loss occurs.” Crucially, IAS 2.33 explicitly permits reversals. It states that a fresh NRV assessment must be made in each period and “when the circumstances that previously caused inventories to be written down below cost no longer exist… the amount of the write-down is reversed… so that the new carrying amount is the lower of the cost and the revised net realisable value.” (Source: eur-lex.europa.eu). Thus IFRS mandates reversing a prior write-down (at most up to the extent of the original impairment) when NRV rises (e.g. due to market improvement) (Source: eur-lex.europa.eu).

The practical effect is that under IAS 2, if inventory is impaired one year but its selling price (or realizable value) recovers later, the carrying amount is written back up (but not above original cost) and a gain is recorded (via reduced cost of goods sold) in that later period (Source: eur-lex.europa.eu) [3]. For example, IFRS requires any reversal to be recognized by “a reduction in the amount of inventories recognized as an expense in the period in which the reversal occurs.” (Source: eur-lex.europa.eu). Multiple sources confirm this IFRS policy: KPMG notes that “IAS 2 requires [a] reversal (capped at original cost) if subsequent conditions change” [12], and IFRS-focused guides state that “when market prices recover…the write-down is reversed (up to original cost) and recognized in profit or loss” [3].

This IFRS treatment embodies the standard’s neutrality principle: inventory is valued at the lower of cost or current market reality, and allowed to increase if the market allows. IFRS proponents argue that allowing reversals produces more economically relevant and timely information. By contrast, reversing write-downs introduces more volatility (since profits can increase when markets rebound), but supporters view this as a faithful reflection of asset value changes.

U.S. GAAP Guidance on Inventory Write-Downs and Non-Reversals

ASC 330 – Inventory governs U.S. GAAP. Historically, ASC 330 required lower-of-cost-or-market (LCM) measurement, with “market” defined by current replacement cost subject to a ceiling (NRV) and floor (NRV less profit) [9] [4]. ASU 2015-11 simplified this: for entities using FIFO or average cost, LCM was replaced by lower-of-cost-or-NRV, aligning those cases with IFRS; LIFO and RIM still use LCM [9] [4].

ASC 330 treats a write-down as creating a “new cost basis” for that inventory. Critically, ASC 330-10-35-2 explicitly prohibits any write-up of inventory carrying value once written down [2] [13]. As the US GAAP Buddy guide demonstrates: “the write-down adjusts inventory to NRV and establishes a new cost basis; reversals of prior write-downs are prohibited… even if NRV subsequently recovers” [2]. Likewise, LegalClarity notes that under GAAP “once you write inventory down, the reduced amount becomes the new cost basis. You cannot reverse the write-down even if the market price recovers” [1]. In fact, ASC 330-10-35-14 makes clear that a year-end write-down is irreversible (unless due to specific foreign currency adjustments, an exception rarely relevant to inventory) [1].

In effect, ASC 330 enforces a one-way downwards adjustment. If inventory’s market or NRV falls below cost, a loss is recognized; but any subsequent recovery in value is ignored. The concepts of “ceiling” and “floor” in older U.S. GAAP rules prevented extreme volatility, but they did not allow reversal of an already recognized loss. Even after ASU 2015-11, which aligned LIFO/RIM rules with FIFO/average cost for lower-of-cost-or-NRV, the fundamental no-reversal stance remains.

GAAP’s no-reversal rule is rooted in prudence. As noted by commentators, “GAAP’s traditional prudence” enforces that “once inventory has been written down … GAAP explicitly forbids any subsequent write-up even if market or NRV later improves” [14]. Under GAAP, conservatism dictates that losses are recognized promptly, but potential future gains from recoveries are not allowed into earnings until they are actually realized through sale. Affected companies must carry the lower valuation even if conditions improve, resulting in permanently lower asset values and potentially lower future gross profit margins.

Conceptual and Historical Perspectives

The IFRS vs. GAAP divergence on write-down reversals reflects deeper conceptual differences and historical evolution. Under IFRS, the lower-of-cost-or-NRV rule embodies a direct valuations principle, emphasizing that assets should “never be carried above the amounts expected to be realized on sale or use” [15]. Because IFRS aims for fair representation, it allows adjusting values in both directions as circumstances change. Commentators note that this asymmetry (recognizing recoveries) “[ensures] inventory is carried at the lower of cost and current NRV” [3]. IFRS’s philosophy is that if the market signal changes, the carrying amount should reflect that new signal, even if it restores previously impaired value (up to original cost).

By comparison, historical U.S. GAAP was governed by a stricter conservative/prudence concept: losses must be recognized promptly, but “don’t anticipate gains.” As the EY “US GAAP vs IFRS” primer states, ASC 330 historically set lower-of-cost-or-market with a new cost basis after write-down [16], and once written down, GAAP “upside reversals are not allowed” [16]. This one-way rule is rooted in both tradition and tax practice: the U.S. tax code similarly disallows deducing inventory to NRV without actual sale in many cases.

These conceptual underpinnings explain why convergence efforts have left this issue intact. The 2006–2011 FASB-IASB convergence project (including ASU 2015-11) harmonized measurement approaches (e.g. removing LCM floor/ceiling for many U.S. entities) but explicitly left write-up prohibition in place for US GAAP. The SEC has also not pressured reversal allowances. Indeed, as one GAAP analyst comments, “GAAP reporters need to be more cautious with the timing and magnitude of write-downs, since there is no mechanism to claw back an overly aggressive adjustment” [17]. In short, the divergence persists because IFRS’s principle of neutrality allows reversal, whereas GAAP’s conservatism forbids it [1] [5].

Effects on Financial Statements

The contrasting policies produce materially different outcomes in financial reports when inventory values fluctuate. Under IFRS, a write-down reversal directly increases income and assets in the period of recovery. For example, as the IASB’s staff commentary clarifies, recognizing a reversal serves *“as a reduction in the amount of inventory expense” (i.e. COGS) * (Source: eur-lex.europa.eu). Practically, if an entity wrote down inventory by $100 when NRV fell below cost, and in a later quarter NRV rises, IFRS allows up to $100 to be credited back to COGS (reducing expense) (Source: eur-lex.europa.eu) [6]. This results in higher gross profit and income when markets turn around.

Under GAAP, no such benefit arises. Using the same scenario, once the $100 impairment is taken, the inventory’s cost basis is $100 lower, permanently. If market price recovers, GAAP keeps the last carrying amount unchanged. Any gain on eventual sale beyond this impaired cost is treated as normal sale profit, not a reversal of the prior loss. As one analysis notes: “if market prices recover the next quarter… ASC 330-10-35-14 makes [the write-down] permanent” [13]. Consequently, GAAP earnings will stay lower (until sale) compared to IFRS.

Numerous commentators and educational sources confirm these impacts. The LegalClarity guide explicitly states the GAAP-IFRS divergence: “Under U.S. GAAP, once you write inventory down… ASC 330-10-35-14 makes this permanent… IFRS takes the opposite approach. Under IAS 2, if circumstances change and NRV rises, you recognize the recovery” [1] [6]. The IFRS vs. GAAP differences mean comparable companies may report significantly different profits simply due to accounting policy. Table 2 illustrates an example scenario (hypothetical) of how an inventory write-down and subsequent recovery affect reported results under each regime.

| Scenario Element | IFRS Treatment | US GAAP Treatment |

|---|---|---|

| Initial inventory cost (10 units @ $100) | Carried at $1,000 (cost) | $1,000 (cost) |

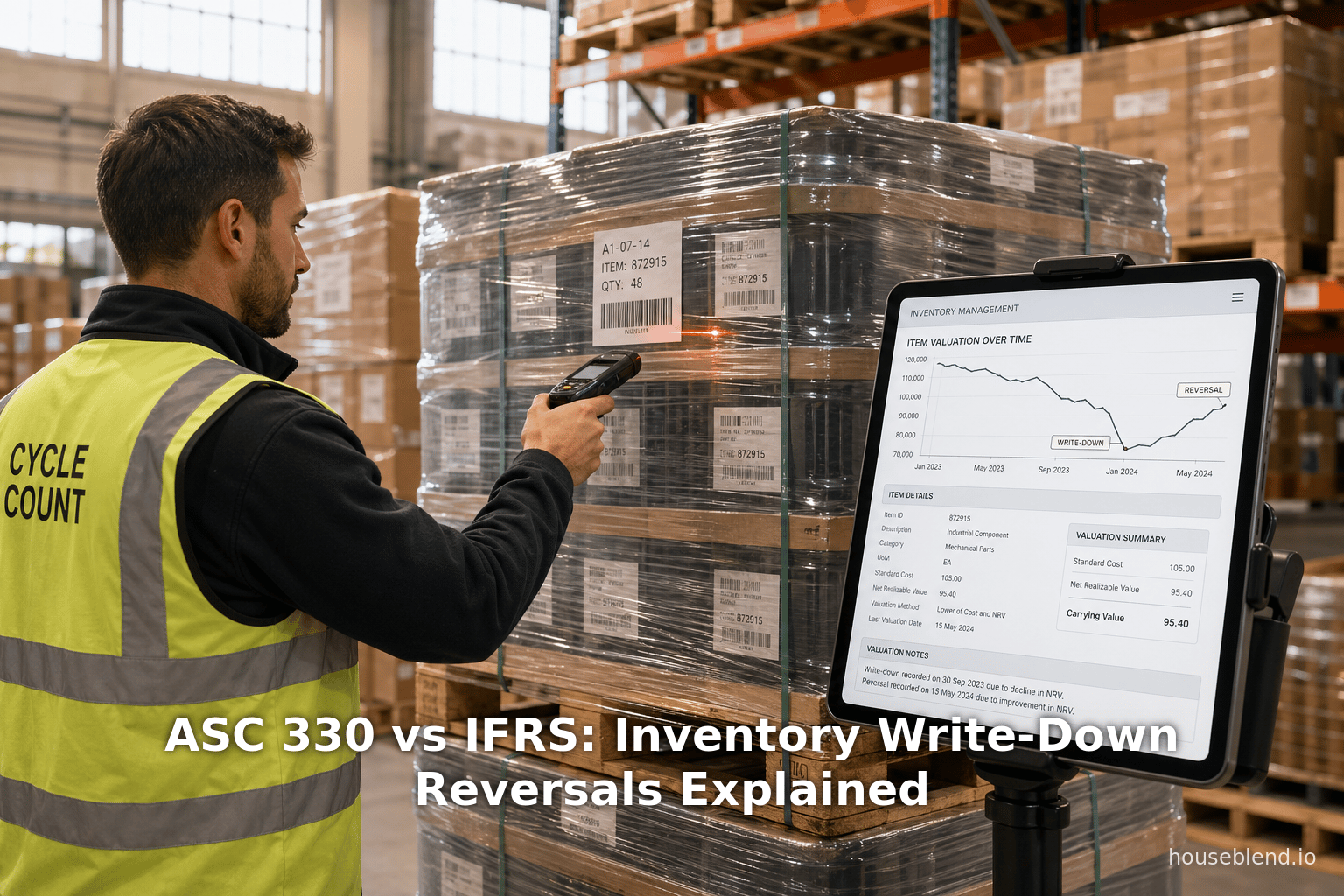

| NRV drops to $60/unit (sell price $70, costs $10) | NRV = $60, Inventory written down $400 (to $600) (Source: eur-lex.europa.eu) | “Market” = $60, Inventory written down $400 (to $600) [1] |

| End of Period Carrying Value | $600 (cost basis reset to NRV) | $600 (new cost basis) |

| NRV recovers to $80/unit (sell price $90, costs $10) | NRV = $70; IAS 2 requires reversal up to original $400. Inventory increases by $100 to $700 (Source: eur-lex.europa.eu) [6]. COGS is reduced by $100 (gain recognized). | Although NRV = $70, no reversal. Inventory remains at $600. (Any gain arises only on actual sale.) |

Table 2: Illustrative case of a temporary inventory write-down (to $60/unit) followed by partial recovery (to $70/unit NRV). Under IFRS, a $100 reversal (limited to the original write-down) occurs, whereas U.S. GAAP prohibits any reversal (Source: eur-lex.europa.eu) [6].

This simplified example highlights the income effect: IFRS would report $100 higher profit (via lower COGS) in the recovery period, while GAAP would not. Real-world data support significant differences in companies’ losses or profits during volatile markets. For instance, detailed SEC filings (footnotes) often show IFRS-reported “write-up” line items that have no GAAP counterpart. Analysts note that IFRS companies could see higher reported margins or lower future losses in rebound scenarios, whereas GAAP peers remain “stuck” at the impaired values.

Empirical studies on convergence have flagged this divergence as a key obstacle. Lucchese et al. (2020) note that even after FASB’s simplifications, “the differences still existing between the two accounting principles” include this write-down reversal issue [18]. While formal quantitative research specifically isolating the reversal effect is limited, broader studies of IFRS vs. GAAP firms often attribute part of the reduced comparability to inventory rules. For industries with volatile pricing (e.g. commodities, commodities-based, fashion), the ability or inability to reverse inventory write-downs can meaningfully skew reported earnings.

Broader Perspectives and Case Studies

Professional guidance and commentary: Many accounting guides emphasize the IFRS-GAAP gap. KPMG’s summary of inventory differences explicitly states, “IAS 2 requires the increase [in value i.e. reversal], capped at original cost, to be recognized… Reversals are recognized in profit or loss” [12]. EY’s “US GAAP vs IFRS” primer similarly contrasts the IFRS requirement to reverse with the GAAP prohibition [16]. A practical IFRS buddy guide likewise advises that “a write-down must be reversed if circumstances change—for example, if market prices recover… (IAS 2.33). The reversal cannot exceed the original cost.” [19]. Such sources highlight that IFRS actively addresses reversals (IAS 2 ¶33) whereas GAAP effectively does not.

Tax considerations: Although outside financial reporting, it’s notable that U.S. tax rules also differ; companies cannot deduct inventory losses until sale (unless exemptions apply). This tax conservatism aligns with U.S. GAAP’s stance, reinforcing why GAAP did not move to allow inventory write-ups. LegalClarity’s April 2026 article on inventory accounting explicitly contrasts all three regimes (GAAP, IFRS, tax). It confirms that “the write-down reversals are recognized in profit or loss in the period in which the reversal occurs” under IFRS [6], but that U.S. tax law is even stricter (not letting businesses realize write-down deductions early) [20].

Impact on ratios and analysis: From an analyst’s standpoint, inventory reversals affect key metrics. IFRS’s allowance of reversals means inventory turnover ratios and asset turnover can “improve” when write-ups occur, whereas GAAP’s inventory remains permanently lower. Return-on-assets or gross margins can diverge purely due to accounting policy. Studies on ratios often note that IFRS companies may have higher measured volatility. For example, an IFRS company that reverses a $1 million inventory write-down will report $1 million less in COGS than an otherwise-identical GAAP company, inflating its operating margin by that difference. Over time, GAAP firms might accumulate “excess COGS” relative to IFRS peers.

Illustrative case: Consider a global retailer with an aging electronics inventory. Under IFRS, the retailer writes down obsolete laptop stock by $5M one year (NRV too low), but two years later market prices recover, yielding a $3M write-down reversal. The balance sheet shows $3M more inventory and the income statement a $3M gain (or reduced expense) in that latter year. Under U.S. GAAP, the write-down sets cost basis permanently, so that comparably priced recoveries earn no accounting benefit — the inventory is flipped at the lower carried cost. Although no actual published case studies are readily cited, management discussion notes and footnotes (SEC filings) often contain reverse adjustments for IFRS filers (and the lack thereof for GAAP filers).

Expert views: Experts are split on which treatment is “better.” IFRS advocates argue that allowing reversals avoids premature loss recognition and aligns reported use of resources with actual economic value. They assert it “better reflects economic reality”, as one source suggests [14]. GAAP proponents counter that anticipating recoveries is risky: it requires management judgment about future market conditions, which could be abused to manipulate earnings. They prefer the simplicity of never reversing, maintaining earnings conservatism and avoiding “false profits.” Indeed, as one accounting analyst puts it, GAAP preparers must “be more cautious with the timing and magnitude of write-downs” because “there is no mechanism to claw back an overly aggressive adjustment” [17].

Implications and Future Directions

The write-down reversal divergence underscores a fundamental conceptual split between IFRS and GAAP regarding measurement and prudence. Given the entrenched philosophies and the lack of convergence pressure, practitioners generally expect the status quo to continue. No recent FASB or IASB project seems aimed specifically at reintegrating inventory write-down policies. IFRS’s alignment with IFRS 9 (financial instruments) demonstrates a more liberal approach to reversing impairments (except for equity instruments), whereas GAAP has been moving away from reversals across the board (e.g. FAS 157/ASC 820 has limited reversal on impairments, and revenue standards forbid reversing performance obligations reductions). On inventory specifically, after the 2015 simplification (ASU 2015-11), there have been no proposals to allow U.S. GAAP reversals.

Going forward, companies operating in both IFRS and GAAP environments need to model these differences carefully. Multinationals must maintain dual records or reconciliations, and investors should be aware that “stock gain” under IFRS (from reversal) has no GAAP equivalent. Some analysts advocate greater disclosure: IFRS 2 requires disclosure of amounts of write-downs and reversals [21], which aids comparability. Any future standard-setting (rare as it may be) would have to weigh the trade-offs between faithful representation and conservatism. Given the current stance, companies should continue to recognize that IFRS reporting may show improved profitability when markets rebound, while GAAP reporting will lag.

Conclusion

Inventory write-down reversals exemplify a clear U.S. GAAP vs. IFRS difference. IFRS (IAS 2) requires that a prior write-down be reversed when warranted by recovering NRV (limited to original cost) (Source: eur-lex.europa.eu) [3], whereas U.S. GAAP (ASC 330) establishes that write-downs are final – no reversals are permitted [2] [1]. This stems from IFRS’s commitment to neutral measurement and GAAP’s adherence to conservatism. The result is that IFRS companies may report higher profits in recovery periods, while GAAP companies do not.

Understanding this difference is crucial for anyone analyzing cross-listed companies or interpreting international financial statements. The literature and standards make it abundantly clear: GAAP prohibits inventory write-up (no reversal), and IFRS mandates it when justified (Source: eur-lex.europa.eu) [1]. All cited authorities – from the IFRS Foundation’s IAS 2 text to professional commentaries – reinforce this conclusion (Source: eur-lex.europa.eu) [3] [1]. As long as these frameworks remain distinct, analysts and preparers must account for this rule in evaluating inventories and earnings profiles.

References: Authoritative sources on ASC 330 and IAS 2 are cited above (Source: eur-lex.europa.eu) [1] [3]. Key references include the IFRS standards and FASB codification excerpts, along with professional analyses by KPMG, EY, and LegalClarity [12] [16] [1]. These confirm the prohibition of reversals under GAAP and the requirement of reversals under IFRS.

External Sources (21)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.