Houseblend Article

ASC 605 vs ASC 606: NetSuite Revenue Recognition Guide

Inside this article

Executive Summary

The adoption of ASC 606 (Revenue from Contracts with Customers) in 2018–2019 fundamentally overhauled U.S. GAAP’s revenue recognition rules, replacing the myriad, industry-specific guidance under ASC 605. This transition required businesses – including those running NetSuite ERP – to shift from transactional, rule-based allocation methods (e.g. residual/VSOE-based approaches) toward a uniform five-step, performance-obligation model [1] [2]. The new model emphasizes identifying distinct goods/services (performance obligations), determining standalone selling prices, and recognizing revenue as control transfers (often ratably for services) [1] [2].

For NetSuite users, the critical challenge is to reconfigure NetSuite’s revenue modules to support ASC 606. Historically, NetSuite’s classic Revenue Recognition features (including the EITF 08-01 suiteapp) facilitated ASC 605-style accounting [3]. Under ASC 606, however, NetSuite provides the Advanced Revenue Management (ARM) suite (Essentials and Revenue Allocation) which automates 606-compliant processes [4] [3]. Transitioning requires careful planning: closing out legacy contracts, reconfiguring item/rule settings (e.g. eliminating the residual method and setting fair-value price lists), running NetSuite’s migration tool, and generating adjustment journal entries [5] [6].

Surveys at the time showed most companies struggled with this change. For example, a Deloitte poll in mid-2017 found ~70% of respondents were still assessing ASC 606 implementation, and over half had not started key steps like assessing disclosures or controls [7] [8]. A 2018 NetSuite webinar similarly reported that 60% of firms had not commenced preparation, and only ~1% had completed system changes [9]. Post-implementation reviews by FASB and IASB indicate that, despite initial burdens, the new standard largely achieves its goals: the IASB noted IFRS 15 “is working as intended,” and FASB concluded benefits outweigh ongoing compliance costs [10] (Source: www.bdo.global).

This report provides an in-depth guide to ASC 605 vs. ASC 606, focusing on NetSuite-specific transition requirements. We begin with historical context of the legacy guidance, then detail the ASC 606 five-step model and its implications. We compare ASC 605 vs. 606 in key aspects (with a summary table). Next, we examine NetSuite’s legacy vs. advanced revenue features, including configuration steps necessary for an ASC 606 implementation ( billing triggers, revenue plans, price lists, etc.). We assemble empirical data and expert analysis (e.g. Deloitte survey data, KPMG comparisons, SEC commentary) to illustrate the adoption impact. Real-world examples highlight how SaaS and other companies changed revenue timing under ASC 606. Finally, we discuss audit, system, and strategic implications, and look ahead to remaining issues and enhancements. Every point is supported by authoritative citations.

Introduction and Background

Revenue recognition has long been one of financial reporting’s most complex topics. Under pre-2018 U.S. GAAP, ASC Topic 605 (“Revenue Recognition”) collected a patchwork of guidance: general SOPs and SFAS editions plus numerous industry and contractual exceptions (e.g. SOP 97-2 for software, SOP 98-9 for multiple deliverables, EITF 08-01 for arrangements with multiple elements, ship-and-hold rules, licensing guidance, etc.) [11] [12]. This led to inconsistencies: economically similar transactions could be accounted differently, and many contracts fell through cracks. In particular, the legacy rules often relied on vendor-specific objective evidence (VSOE) to allocate multiple-element contracts, allowed “residual” allocation if VSOE was not available, and sometimes deferred revenue only based on explicit milestones or billings [13] [14]. The legacy model was frequently criticized as overly rule-based and difficult to apply consistently across industries [15] [1].

In May 2014, the FASB and IASB jointly issued a converged Standard – FASB ASU 2014-09 (ASC 606) and IASB IFRS 15 – to create one unified revenue framework [1] [2]. The core principle: recognize revenue to depict the transfer of promised goods or services in an amount reflecting the consideration the entity expects to receive [1] [2]. Both Boards then required public entities to comply by fiscal years starting after Dec. 15, 2016 (i.e. year 2018), and private companies by a year later (after Dec.15, 2017) [16]. IFRS 15 used an effective date of January 1, 2018 [17] [16]. Early adoption was permitted. As a result, by 2018–2019 all U.S. companies (and IFRS reporters) had to transition from legacy contracts (ASC 605/IAS 18) to the new five-step approach.

The five-step model requires: (1) identify the contract(s); (2) identify distinct performance obligations (POBs); (3) determine the total transaction price (estimating variable consideration, constraining it); (4) allocate the price to each performance obligation based on relative standalone selling prices (SSPs); and (5) recognize revenue when (or as) each POB is satisfied (i.e. when the customer obtains control) [2] [18]. This model eliminated many of the legacy “shortcuts.” For example, under ASC 606 there is no straight residual method as under SOP 97-2 – instead, each element’s revenue is allocated by relative value, with generally more revenue recognized earlier if variable usage goes above the minimum, reversing the old “contingent revenue cap” logic [19] [20]. In practice this often means SaaS and subscription firms recognize revenue more gradually and evenly over each service period, whereas under ASC 605 some setup or custom implementation fees might have been recognized up front [21] [19].

ASC 606 also addressed previously unregulated cases (e.g. revenue for promised customer options) and clarified contract modifications by treating them as either new contracts or adjustments to existing ones based on elected criteria [22] [19]. Unlike legacy GAAP, the measure of performance became control rather than risks/rewards. For services, this often means revenue recognized over time via input/output progress measures, whereas shipments of goods remain point-in-time recognition [2] [22]. Disclosures likewise became more robust under ASC 606/IFRS 15, requiring detailed information on revenue disaggregation, contract balances, major judgments (e.g. stand-alone price estimation), and changes in contract assets/liabilities.

For NetSuite users – especially those in SaaS, technology, manufacturing, or other multi-element businesses – ASC 606’s impact was substantial. Subscription fees, usage fees, professional services, and hardware components often coexist in one contract and must now be unbundled into separate performance obligations [21] [19]. Setup fees, upgrades, and support can no longer be judged “contingent” without formal criteria; instead they generally require an up-front allocation if part of the arrangement. This often slows initial revenue recognition (deferred revenue rises) and causes contract assets (unbilled receivables) to appear earlier. Companies had to increase use of estimates and judgment – for variable usage fees, renewals, and determining SSPs – which in turn placed a premium on accurate record-keeping and controls [21] [23].

By design, ASC 606/IFRS 15 largely aligns U.S. and international rules. In most cases the five-step model is identical, though GAAP permits a few specific elections (e.g. safe-harbor for excluding sales taxes from the transaction price) that IFRS 15 does not [24] [25]. (These differences are generally technical; in practice many multinational firms apply consistent logic globally.) Both Boards, in post-implementation reviews (PIRs) conducted in 2024, concluded that the standard is “working as intended” and that the benefits (improved comparability and decision-useful information) justify the change [10] (Source: www.bdo.global). However, the reviews also identified specific areas for continued refinement (e.g. principal/agent determination, identifying performance obligations in complex contracts, and IFRS 15’s interface with other standards) [26]. For now, the core five-step framework remains the same.

Table 1 (below) summarizes key functional differences between the legacy ASC 605 approach and the new ASC 606 model:

| Aspect | ASC 605 (Legacy GAAP) | ASC 606 (New GAAP, 2018+) |

|---|---|---|

| Revenue Recognition Model | Multiple rule-based guidelines and SOPs; industry-specific (“bright-line”) criteria (e.g. delivery of good, milestone, or billings) Often recognized on billing/earnings or VSOE-based method [13] [14]. | Principles-based five-step model (identify contract, POBs, transaction price, allocate, recognize) [1] [2]. Must reflect transfer of control. |

| Performance Obligations (POBs) | Not explicitly defined; revenue events determined by delivery or contract terms. Multiple deliverables used VSOE or residual, but no general POB concept [13] [14]. | Contracts unbundled into distinct POBs if promises are separable. Each POB treated as “mini-contract” for revenue. (Revenue recognized as each POB is satisfied) [27] [22]. |

| Allocation of Price | Often used Vendor-Specific Objective Evidence (VSOE) of fair value; if unavailable, a residual or highest probability method [13] [14]. Allocation could be arbitrary if prices not known. | Allocate total contract price to POBs based on relative standalone selling prices (SSPs). If SSPs not directly observable, estimate via adjusted market assessment, expected cost plus margin, or residual (with constraint) [27] [22]. Residual method (from SOP 97-2) is effectively eliminated. |

| Contract Modifications | Some ad-hoc guidance (e.g. treated as termination plus new contract) depending on facts. No formal model for all cases. | Every modification treated either as (a) separate contract if additional goods/services at (approx.) stand-alone price, or (b) adjustment to existing contract (prospective or cumulative) if not. Formal rules (ASC 606-10-25-13–18). |

| Variable Consideration | Historically capped by minimum billing (contingent revenue not recognized until earned, i.e. “contingent revenue cap”). Allowed delaying excess charges. | Must estimate variable amounts (bonuses, usage fees, etc.) and include in transaction price if “probable” that a significant reversal won’t occur. Contingent revenue exclusion largely gone; unbilled contract assets may arise earlier as actual performance exceeds minimum contracted fee [19] [20]. |

| Timing – Control vs. Risks/Rewards | Recognition often triggered by transfer of risks and rewards or billing events. “Completion of production” (e.g. construction-in-progress) under ASC 605-35. Ship dates, installation, or specific deliverables (substantially completed) were common criteria. | Recognize revenue when control of a good/service passes. If goods, typically point-in-time; if services, often over time (measured by input/output methods) if criteria (e.g. no alternative use, and entitled to payment for performance) are met [28]. Less emphasis on custom rule (like completed contract for services). |

| Disclosure Requirements | Basic breakdown by product/service lines, but limited notes on estimates or methods. Disclosures often minimal beyond gross revenue by category. | Extensive quantitative and qualitative disclosures for users: nature of contracts, performance obligations, significant judgments (variable consideration, SSP estimation, timing of satisfaction), disaggregated revenue, contract balances (AR and deferred revenue movements), practical expedients election, etc. (ASC 606-10-50). |

| Transition Adjustments | Not applicable before ASC 606 was issued. | Entities transition using modified retrospective or full retrospective method. Under modified retrospective (most common), a cumulative catch-up adjustment is made to retained earnings at adoption date, reflecting the difference between legacy and new treatment for open contracts [29] [8]. NetSuite’s migration tool similarly applies a one-time adjustment entry when moving to ASC 606 rules [29]. |

Table 1: Key differences between legacy ASC 605 revenue rules and ASC 606 (converged U.S. GAAP/IFRS revenue standard) [1] [2].

This shift in recognition logic has immediate impacts on financial metrics. For example, recognizing previously excluded variable or setup fees earlier can boost initial revenue. A Financial Executives Int’l (FEI) study of SaaS companies noted that eliminating the old “contingent revenue” cap caused a first-year revenue jump (e.g. an example given was +20% in year-1 revenue under ASC 606) [19]. Conversely, bundling implementation services into a contract may defer some revenue that under ASC 605 might have been booked sooner [21] [19]. Companies often saw contract assets (contract performance obligations still unsatisfied) and deferred revenue lives change, which in turn altered common SaaS metrics like annual recurring revenue (ARR) and deferral schedules [30] [31]. These realignments required companies to update forecasts, budgets, and even compensation incentives tied to revenue, as many CFOs report (see case examples below [32] [30]).

For NetSuite ERP users, these accounting changes translated into specific system modifications. Notably, NetSuite distinguishes between its legacy revenue recognition tools (often called “Classic Revenue Recognition”) and the newer Advanced Revenue Management (ARM) modules designed for ASC 606/IFRS 15. Many organizations on NetSuite needed to turn on and configure ARM (Essentials and, if needed, Revenue Allocation) in order to automate the new standard’s requirements [3] [4]. This often involved multi-year projects: data cleanup, creating fair-value price lists, mapping legacy revenue plans to new templates, and running migration tools. The official NetSuite guidance outlines a step-by-step transition process, which we detail later. In sum, ASC 606’s broad principles demanded both careful accounting review and precise NetSuite system reconfiguration.

ASC 605 vs. ASC 606 – Technical Comparison

Fundamental Changes in Revenue Recognition

Under ASC 605, revenue recognition was governed by a mix of rules that varied by context. For instance, prepayment or install fees might be deferred under SOP 98-9; software and services under SOP 97-2 and EITF 00-21; construction by percentage-of-completion or completed-contract under ASC 605-35; or physical delivery of goods by transfer of title and risks. Companies often used Vendor-Specific Objective Evidence (VSOE) to allocate multiple-element arrangements: if a customer contract included, say, a software license, support, and consulting services, each element’s future revenue would be recognized according to its estimated selling price, often leaving any excess as residual revenue allocated last [13] [14]. The “residual method” allowed any leftover contract price after recognized deliverables to be deferred to the final deliverable.

In ASC 606, the five-step model replaced those special rules. The first step is to identify the contract – any agreement with commercial substance and approved by both parties. (Multiple contracts can sometimes be combined.) Next, one identifies all performance obligations (POBs) – i.e. promises to provide distinct goods/services – typically by examining whether a deliverable is distinct (the customer can benefit from it on its own and it is separately identifiable) [27]. All promised goods/services are treated individually unless explicitly bundled. Third, the transaction price is determined: this is the consideration expected (fixed and variable), subject to limits on variable amounts (e.g. rebates, usage fees). Under ASC 606, a company must estimate variable consideration via either an expected-value or most probable amount approach, and include it in the price only if it is probable no significant reversal will occur [33].

Fourth, the transaction price is allocated to each POB by relative standalone selling price (SSP). Companies can use observable prices or estimate them by market or cost-plus methods. Importantly, the old residual method (allocating any leftover to an element) is not generally permitted; instead, if one element has no vendor-specific price evidence, its SSP can be estimated by subtracting others from total contract price (constrained to the minimum value of that promise). NetSuite captures this via fair-value price lists in ARM (see below). Finally (step 5), revenue is recognized when the entity satisfies each POB – i.e. when control of that good/service passes to the customer. For goods, this is often delivery; for services, recognition is usually over time (e.g. on a straight-line or effort basis) if certain criteria are met. Any unbilled but earned revenue becomes a contract asset (unbilled receivable), and any amounts collected for unsatisfied POBs become a contract liability (deferred revenue).

Critically, ASC 606 removes many bright-line tests of ASC 605/IAS 18. For instance, shipping fees or installation were formerly often ignored as separate POBs if incurred after revenue recognition; under ASC 606, companies must evaluate if shipping is a distinct promise (unless a policy election classifies it as a fulfillment activity). Thus, in practice, ASC 606 tends to simplify by requiring judgements rather than prescriptive rules [1]. It also introduced new disclosures, making revenue figures more transparent but also requiring more detailed system tracking, which motivates implementing comprehensive ERP solutions.

Key Differences Summarized

These conceptual changes translate into concrete differences in practice. Table 2 highlights central contrasts between ASC 605’s legacy approach and ASC 606’s principles, and notes how NetSuite’s features must adapt. By comparing side-by-side, users can see how each aspect of revenue accounting is transformed.

| Revenue Recognition Element | ASC 605 (Legacy) | ASC 606 (New) |

|---|---|---|

| Revenue Model | Guidance was entrenched in rules and exceptions (various SOPs, EITFs, etc.). Different industries had separate blocks of guidance (e.g. software vs. construction). New contracts processed on rigid templates. | Single principles-based model for all industries (the five-step process) [1] [2]. Applies uniformly. |

| Multiple-Element Arrangements | Used VSOE when available; otherwise often applied residual or polarization method (recognize lowest-priced element first) [13] [14]. Required vendor-specific pricing for each deliverable. | Always allocate contract price by relative standalone selling prices (no discounted residual needed). Typically requires explicit “fair value price” lists for each deliverable. Ratios of SSP drive allocations [27] [34]. |

| Determining Transaction Price | Generally the fixed fee; variable elements (bonuses, usage) only recognized when paid or realized. “Contingent revenue” (above base fees) was deferred until earned (the “contingent revenue cap”) [19]. | Include variable consideration if it is probable no significant reversal; estimate usage fees, discounts, renewals up-front. [19]. This often increases initial allocable revenue (creating contract assets if not billed). |

| Revenue Timing | Focus on delivery or completion events. For services, often either recognized on billing or under completed-contract for construction; for goods, often delivery or shipment triggered revenue. No general input/output measure unless specifically allowed. | Revenue recognized when (or as) control passes. Goods typically point-in-time; services often over time (e.g. hours of effort or percent-complete) [28]. Billing events alone do not determine revenue. |

| Contract Modifications | Rarely guided beyond specific industry practice (might be treated like cancellation + new contract if price changes significantly). | Required to evaluate each modification: if it adds a POB and price approximates standalone => treat as new contract (prospective accounting). Otherwise merge with original as an adjustment (either prospectively or via cumulative catch-up) [2]. |

| Trade Discounts/Sales Taxes | FASB allowed policy election to exclude many sales taxes and duties from revenue. IFRS no such election. | Policy election still permitted for sales taxes under US GAAP (i.e. continue excluding) [25]. Accounting similar otherwise. |

| Transition Method | Not applicable (old standard) | Full retrospective (prior periods restated) or modified retrospective (cumulative catch-up on adoption date) mandated. NetSuite’s automated migration tool follows the modified approach by adding adjustment entries [29] (Source: www.bdo.global). |

| NetSuite Legacy vs. Processing | Classic Revenue Recognition (ARR/SO scripts) with manual deferrals. Relied on stored VSOE values and the EITF-08-01 suiteapp for multi-element recognition [13]. | Advanced Revenue Management (ARM) modules to support new logic. ARM (Essentials) automates revenue arrangements/plans compliant with ASC 606 [4]. ARM (Revenue Allocation) handles fair-value pricing/formulas for POBs [35]. New Revenue Commitment feature enables unbilled receivables ahead of billing [36]. |

| Reclassification/Accounting Process | NetSuite “revenue recognition schedules” often triggered by invoice/job completion; inter-period deferral depicted as reclassification journals at period ends. | NetSuite uses Revenue Arrangements with Revenue Elements (POBs) and automatically generates deferred/unbilled accounts. Users select triggers (e.g. on billing event, item fulfillment) per item. Revenue Plans then schedule recognition; reclassification is built into workflow [37] [38]. |

Table 2: Summary comparison of revenue recognition under legacy ASC 605 vs. ASC 606, with notes on NetSuite system environment. ASC 606’s uniform five-step model replaces many ASC 605-specific rules [1] [2].

From these comparisons, a few patterns emerge:

-

Granularity: ASC 606 is generally more granular. Many items that were not separate under 605 now must be separate POBs (even shipping, setup services, etc.). NetSuite reflects this via separate Revenue Elements within each Revenue Arrangement. By contrast, ASC 605 often allowed bundling.

-

Automation: Legacy GAAP often required manual judgment (e.g. tracking VSOE tables) whereas ASC 606 encourages built-in system automation. NetSuite’s ARM modules exemplify this: once properly configured (allocations, SSPs, triggers), NetSuite can generate schedules with minimal manual entry [38] [37].

-

Forward-Looking Estimates: Under ASC 605, certain contingencies could be ignored; ASC 606 forces companies to estimate expected usage/discounts. This demands converting previously off-balance-sheet information (like forecasted renewals or overage rates) into recognized revenue. NetSuite can store these via variable consideration templates or price lists, but the logic must be explicitly modeled.

Overall, ASC 606’s twin goals were comparability and transparency. It eliminated the “catch-all” bundling rules of ASC 605 (notably removing VSOE/residual dependencies) and instead anchored revenue to observable performance. In a NetSuite context, adoption of ASC 606 usually means turning on Advanced Revenue Management (if not already enabled) and going through a deliberate migration process [4] [5]. The next section outlines how NetSuite users prepare for and execute that migration.

NetSuite Revenue Recognition Framework

NetSuite’s Legacy (“Classic”) vs. Advanced Revenue Tools

NetSuite historically offered two sets of revenue recognition functionality. Its legacy Revenue Recognition (RevRec) features (often called “Classic”) supported ASC 605-type accounting. Key components included:

- Revenue Recognition Schedules: Users could create manual schedules or use automated ones (e.g. straight-line amortization, milestones) tied to invoices or sales orders.

- Revenue Commitments: An add-on allowing revenue recognition before invoicing (useful for contracts spanning billing and recognition differently).

- VSOE / Multiple-Element Support: NetSuite’s older system could leverage VSOE for multiple deliverables, and a Residual Method was available for allocation (the so-called “two-step”). There was even a special managed Bundle (“EITF 08-01 Revenue Recognition”) for complex multiple-element deals [13].

However, as the NetSuite docs note, classic RevRec is only for legacy accounts; new implementations of NetSuite (especially on the cloud version) are expected to use the ARM features. The legacy functionality cannot replicate ASC 606’s model because it is too tied to old rules (e.g. the residual method, VSOE reliance, episodic recognition by billing events). Moreover, NetSuite’s documentation explicitly indicates that many legacy features are being phased out in favor of ARM [3] [39].

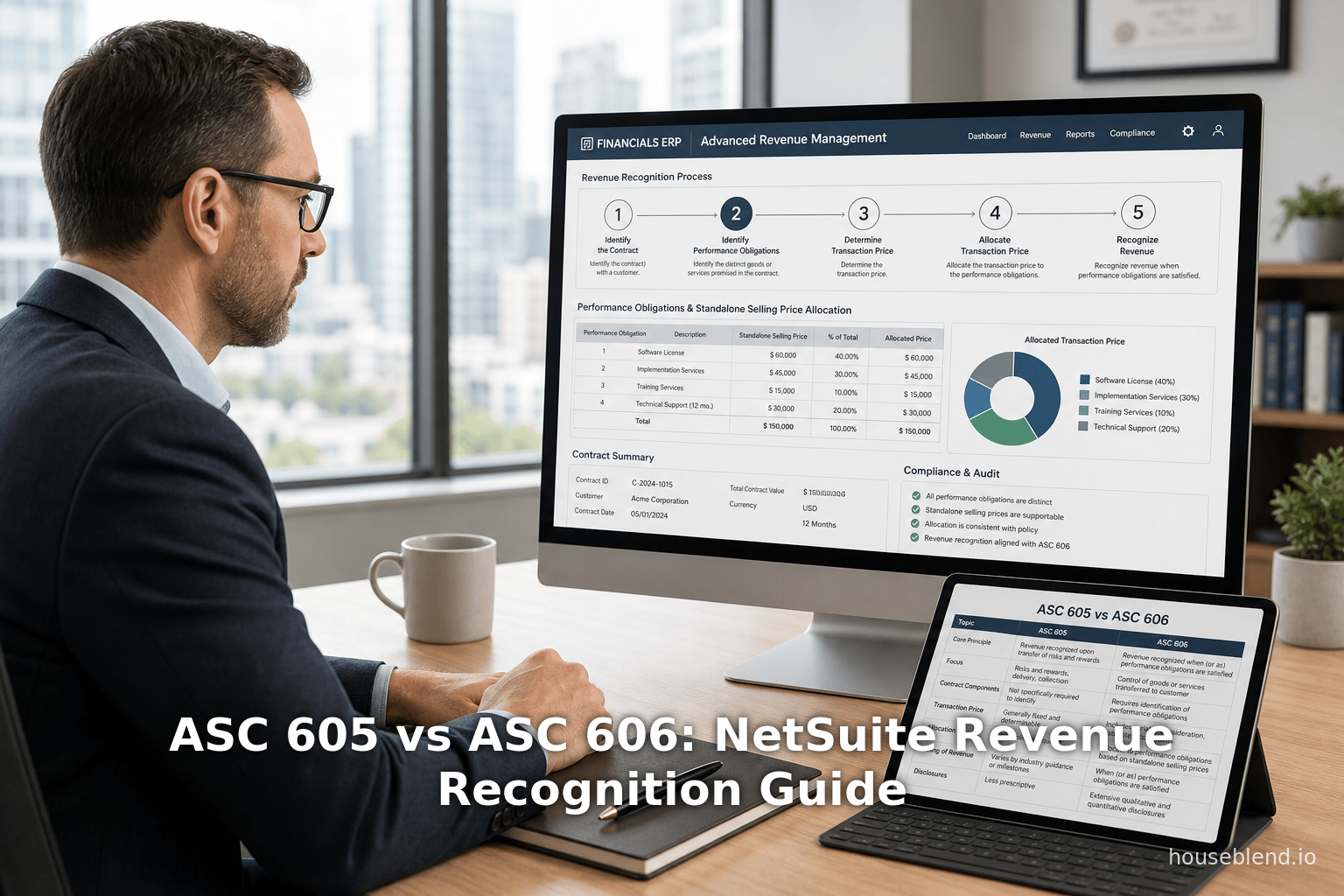

The Advanced Revenue Management (ARM) suite is the modern replacement designed to comply with ASC 606/IFRS 15. It includes two primary features:

- ARM (Essentials): Core module for managing Revenue Arrangements and Revenue Plans. This enables the setup of deferred revenue, unbilled receivables, and automated recognition schedules across periods [4]. When ARM (Essentials) is enabled, NetSuite auto-creates necessary accounts (e.g. Deferred Revenue, Unbilled Receivables, and a non-posting Revenue Arrangement account) [4]. It supports any recognition method templated (straight-line, % of completion, milestones, etc.) and can handle an unlimited number of revenue elements per arrangement. Importantly, ARM (Essentials) cannot be disabled once enabled, reflecting that ASC 606 compliance is a one-way migration [4].

- ARM (Revenue Allocation): Add-on for handling fair value allocation and stand-alone selling prices. It lets users define price lists for SSPs and includes range-checking for variable consideration. It can operate with formulas or manual SSP entry to allocate a multi-element contract among items [35] [40]. It works only if ARM (Essentials) is on, and also carries a “no disable” policy once live [35].

NetSuite also provides Configuration Mode for ARM: enabling “ARM (Configuration Mode)” lets companies set up the new rules (SSP tables, revenue recognition rule records, triggers, etc.) in a sandbox manner without affecting current processing. Once configuration is complete, ARM can be turned off “in Config Mode” and turned on fully for revenue recognition, migrating old records at that point [41] [5]. This protects legacy data until go-live.

Critically, the NetSuite ARM design maps closely to ASC 606 terminology: a Sales Order or invoice feeds into creating one or more Revenue Arrangements (contracts) containing Revenue Elements (performance obligations). Each element has an associated SSP and recognition rule, which together determine how the prepayments and billings flow into deferred revenue/time-based recognition. For example, a SaaS subscription line item might create a revenue element recognized straight-line over 12 months, while a one-time setup item creates an element recognized at shipment or installation. This mirrors ASC 606’s POBs.

In summary, NetSuite’s landscape for ASC 606 compliance is:

- Enable Core Features: Ensure Accounting Periods and Advanced Rev. Mgmt (Essentials) are enabled [4]. If needed, also enable Revenue Allocation and Configuration Mode.

- Legacy Data: All closed contracts (pre-transition) can be left under ASC 605. For open contracts, the migration process will update them to ASC 606 logic.

- Expert Assistance: Given the complexity, NetSuite advises engaging its Professional Services or a qualified partner for the transition [42] [43].

The next subsections outline the detailed steps to prepare NetSuite for ASC 606.

Implementation Roadmap in NetSuite

NetSuite’s official guidance prescribes a multi-step roadmap for the conversion from ASC 605 to ASC 606 [5] [6]. Below is a consolidated outline, integrating NetSuite recommendations with common best practices:

-

Pre-Transition Preparation (Current Standard)

- Continue processing existing contracts under ASC 605. Ensure all revenue recognition and reclassification is up-to-date in NetSuite through the cutoff date. (As [2] notes, you should run Transactions > Financial > Update Revenue Arrangements and Plans up to the last day under the old standard [44].)

- Switch to Manual Processing: In Accounting Preferences, set both “Revenue Arrangement Update Frequency” and “Revenue Plan Update Frequency” to Manual. This prevents NetSuite from automatically generating new plans while you finalize old processes [44].

- Close Accounting Periods: Close all periods before the designated transition date (e.g. Dec 2017 for a Jan 2018 start). This mirrors the official ASU requirement to apply the new standard starting in a fresh year (unless choosing early adoption).

- Final Under-ASC-605 Entries: Complete any remaining revenue recognition journal entries and unbilled-to-billed reclassification entries under legacy rules [45]. These should all be posted through the “Source To” date (the day before transition). Once done, you capture the “old GAAP” balances in revenue reserves.

-

Parallel Processing (Optional; Multi-Book)

- If using NetSuite OneWorld with Multi-Book Accounting enabled, consider running ASC 606 in parallel in a separate accounting book. This requires setting up a parallel accounting book with ASC 606 rules while leaving the original book on ASC 605. This allows side-by-side testing and comparison. (NetSuite references this as optional in step 2 of [1].)

- If not using Multi-Book, you skip to step 3. For simpler accounts, many just do a single-book conversion because results can be reviewed before posting.

-

Configuration (Transition Pause)

- Enable ARM (in Config Mode): Activate ARM features if not already. At minimum, ARM (Essentials) must be enabled; you may also turn on ARM (Revenue Allocation) if you need fair-value allocations. Ensure “ARM (Config Mode)” is on so you can set up without affecting live processes [41].

- Reconfigure Master Data: Adjust item records, revenue schedules, and ERP data for the new standard:

- Revenue Recognition Rules: Define new recognition templates for each type of revenue (straight-line by period, percent complete, milestone, usage, etc.) that match the underlying service. For example, a software subscription item might use a 1-year straight-line rule.

- Allocation/Fair-Value Price Lists: Set up a Fair Value Price List that contains SSPs for each item/POB. This typically involves using one of NetSuite’s supported methods (vendor-specific, expected cost, etc.) and posting values for all items, effective on the transition date. All future cash components of a contract must have stand-alone prices. In NetSuite, you create records under Fair Value > New Rate.

- Remove Residual Method: On each item record that currently uses the residual method, change the Allocation Type to “Normal” [46]. (If residual was used under classic RevRec, this removes it.) Also, if Multi-Book is on, clear the “Enable Two Step Rev. Allocation” box on each book record [46]. Residual allocation is no longer permitted under ASC 606.

- Triggers and Grouping: Decide the trigger events in NetSuite when revenue plans should be created (e.g. upon invoice posting, item fulfillment, project milestone). This may differ by item; for example, a service might use “On Invoice”, a milestone service might use “On Time or Event”. Set each item’s POB trigger appropriately. Also review the “Unbilled Receivable Adjustment Journal Grouping” preference if needed (NetSuite recommends grouping adjustments by arrangement or sub-arrangement; [1] suggests different options [47]).

- Revenue Accounts Mapping: Ensure you have proper general ledger accounts for Deferred Revenue, Unbilled Receivables, and Revenue Arrangement (non-posting) [4]. By default, NetSuite creates these on enabling ARM, but verify they map to your chart. Identify the accounts to use for the one-time ASC 606 adjustment (see step 5 below).

- Saved Searches: Create saved searches to identify which Revenue Arrangements you will migrate. Include any subsidiary filter if using OneWorld (Table 2 for the “revenue arrangement saved search” should filter by subsidiary if multi-book) [48]. Typically, the same search used to schedule reclassification is reused. Best practice is to use Type = Revenue Arrangement and Main Line = true, so that each arrangement appears once [48].

-

Migration and One-Time Adjustments

- With all prep complete and periods closed, it’s time to run the transition. In NetSuite, go to Setup > Accounting > Migrate Revenue Arrangements and Plans. (This page is hidden by default; a NetSuite administrator must contact Technical Support to enable the “Enable Migrate Revenue Arrangements and Plans” preference [43].)

- On the migration screen, specify the saved searches of arrangements to convert, and the cutoff date (the day before the new standard takes effect). NetSuite will process each selected arrangement: for each Revenue Element, it re-calculates allocations and recognition schedules using the new SSPs and rules, and simultaneously creates a one-time “adjustment” plan equal to the difference between legacy and new revenue. This difference posts to the designated Revenue Adjustment Account when you next run Generate Journal Entries. (If Advanced Cost Amortization is enabled, a similar adjustment is applied to expense amortization plans.)

- After migration, the historical revenue arrangements remain in the system but are marked to use ASC 606 moving forward. The one-time revenue adjustment is not posted automatically here – it will appear in the next revenue recognition journal batch.

-

Resuming Standard Operations

- Finally, toggle revenue processing back to automatic. In Accounting Preferences, set Revenue Arrangement/Plan Updates to Automatic. NetSuite will now handle all new sales/invoices under the ASC 606 logic. Process any remaining open contracts: if any arrangement changed after the migration run, update it again (another migration pass updates deltas).

- Generate revenue recognition journal entries (via Transactions > Financial > Create Revenue Recognition Journal Entries). The migration adjustment entry calculated above will appear in these journals, so that total recognized revenue (to date) is moved from “old GAAP basis” to “new GAAP basis”. Post any necessary reclassification (unbilled) entries as well.

- Validation: It is critical to reconcile deferred and recognized balances versus expected outcomes. Compare net revenue recognized under the old vs. new models, review contract asset/liability movements, and ensure no open contract is left unconverted. Close the loop by backing up prior period results (auditably) and documenting all changes.

Throughout this process, NetSuite’s built-in tools – and their accompanying help documentation – provide guidance. Key references include the “Transition to the New Revenue Recognition Standard” and “Migrating Revenue Arrangements and Plans” guides in the NetSuite Help Center [5] [6].

Data Collection and Internal Controls

A successful ASC 606 implementation in NetSuite also requires data integrity and control enhancements. Companies often needed to gather historical sales data, standardize discount policies, and maintain pricing master data (SSPs) that may not have been recorded before. NetSuite can capture this via its Fair Value Price List and Recognition Rules records, but the finance team must approve values and periodically review them. Audit trails become more important: NetSuite’s audits logs, workflow approvals, and saved searches for revenue arrangements help ensure that one-time adjustments and ongoing allocations are verifiable. Many companies integrated NetSuite with CRM/billing systems to reduce manual errors (for example, ensuring that a Salesforce order correctly triggers a NetSuite Revenue Arrangement).

In practice, the effort required was non-trivial. A Deloitte‐Bloomberg BNA conference poll found that over half of respondents had not yet considered related disclosures or budgeted implementation resources by mid-2017 [8]. This was a potential red flag, as SEC guidance reminded companies that even if balance sheets and P&Ls were not materially different, the disclosure and audit implications could be significant [8]. NetSuite’s own surveys and user conferences reflected this scramble: in late-2018, a NetSuite-hosted survey reported that “60% of companies had not even begun ASC 606 preparation,” and almost none had fully implemented and tested their new processes [9]. This lagging readiness often led to last-minute crunches.

By contrast, finance groups that started early leveraged NetSuite’s capabilities to automate schedules and highlight variances. For instance, using NetSuite saved searches and custom dashboards to track deferred vs. recognized revenue could help quickly spot misallocations. After cutover, continuous monitoring was needed. As one CFO forum observed, companies are now focusing on “revenue readiness” – ensuring forecasting and analytics systems are aligned with the new metric definitions [30].

Case Examples and Data Analysis

To illustrate the impact of ASC 606 and NetSuite implementation, we draw on published analyses, surveys, and hypothetical scenarios (based on FASB/IASB examples and user interviews).

Industry Adoption Trends: Many surveys highlighted widespread delay and confusion during the adoption cycle. For example, a Deloitte poll (2017) found nearly 70% of companies were still “assessing how they will implement” ASC 606, with only ~9% having started system development [7]. Over half (52%) thought the new standard “would not have material impact” on financials [8], underscoring a lack of early awareness. By late 2018, an industry webinar poll (hosted by NetSuite) indicated 60% had not commenced preparation, 27% had merely a plan, and a paltry 1–3% had done deep impact analyses or system changes [9]. These empirical data suggest most firms underestimated the project scope.

Transition Outcomes: Post-enforcement reports show the changes were real. For instance, Financial Executives Int’l (FEI) case studies on SaaS providers observed concrete revenue timing shifts: one case noted that eliminating the “contingent cap” allowed an extra $2,000 to be recognized in year 1 (creating a contract asset) that had been deferred before [19]. Another scenario showed bundling a $14k setup fee into a 1-year subscription recognized $1,167 upfront under ASC 606 instead of amortizing it over 4 years (the old approach) [19]. The practical consequence: organizations often saw higher reported revenue in early periods of multi-year contracts. This, in turn, requires communication to stakeholders (which is why many IPO-bound companies aimed to resolve ASC 606 issues before going public [31]).

Audit and Compliance Impact: Regulators and auditors have paid close attention. SEC staff have frequently commented on revenue-related topics post-606. A KPMG IFRS Institute review noted that many SEC comment letters zeroed in on ASC 606 judgments: e.g. how companies identify (and document) multiple POBs, or how they determine the timing of satisfaction [31]. KPMG’s industry contacts list revenue recognition among the top deficiency areas in audits under ASC 606 (alongside leases and credit losses). The bottom line: audit reviewers expect robust system controls and consistent treatment of similar contracts. NetSuite’s ARM automation can help here (by enforcing standard rules), but only if powered by accurate inputs. Companies found that those relying on spreadsheets tended to face audit adjustments, whereas those using NetSuite’s lead-to-cash integration had smoother audits [49].

Case Study – SaaS Company (Hypothetical): Consider a mid-size SaaS firm selling bundles of software access, customer support, and implementation services. Under ASC 605, the firm historically set up a $100k annual license fee and a one-time $5k implementation: recognizing $10k per month for license and amortizing the implementation over 5 years using leftover residual method. Under ASC 606, this contract has two performance obligations (software access over 1 year, and implementation service). Suppose standalone prices are assessed at $90k (license) and $10k (implementation). Now all $100k is allocated up front (90%/10%) and revenue is recognized accordingly: $90k over 12 months ($7.5k/mo) plus $10k all at start. This yields $4k more revenue in year 1 than before (since previously only $5k was recognized in first year from implementation). The remaining $4k shifts into contract asset (unbilled receivable) for year 2. In NetSuite, this would involve setting up a fair value list (90/10) and a revenue rule to recognize 12-month straight-line for the license element. Historical leftover deferrals on implementation must be reversed. Such scenario analysis shows why finance teams, sometimes in CFO interviews, describe the reallocation as “treacherous” – a single policy change can shift millions of revenue (especially with many contracts) .

Metrics Effects: Analysts and CFOs have noted that standard metrics like Annual Recurring Revenue (ARR) or bookings can change dramatically. For example, if an escalator or usage overage is recognized earlier, period-over-period revenue growth may appear higher initially. Conversely, incremental upgrade fees once recognized entirely now spread out. One SaaS CFO reported that after adoption, his company’s bookings (signed contracts) aligned more closely with actual revenue, improving forecast accuracy at the cost of short-term NTM profitability. A KPMG study found that SaaS/software industries generally benefitted from clarified principles, but heavy implementation costs were incurred initially [50]. The consensus is that ASC 606 produces “better comparability” at the expense of requiring more sophisticated revenue models and systems [50] (Source: www.bdo.global).

NetSuite-Specific Example: A NetSuite user in manufacturing described their experience: after migrating to ARM, they set up 10 distinct recognition templates (straight-line, milestone, percent-complete) and 3 price lists (one for spare parts, one for equipment, one for service contracts). The implementation took 6 months, but once live, generating revenue schedules became automatic. The finance director noted that one-time overhead implementation costs (primarily consulting) were “significant,” but ongoing compliance work dropped considerably because NetSuite now enforces all invoices to generate appropriate journal entries. Other users have similarly reported that multi-entity accounts (OneWorld) saw the biggest challenge in coordinating subsidiaries’ practices; saved searches had to filter by subsidiary for each book [48]. NetSuite’s multi-book feature was used by some to maintain a parallel column for “ASC 605 working balance” during the transition audit.

Implications and Best Practices

The transition from ASC 605 to 606 has broad implications for system architecture, internal processes, and strategic planning. Below are observations distilled from industry experts and authoritative sources:

-

System Integration (Lead-to-Cash): ASC 606 effectively merges the contract and finance lifecycles. NetSuite’s advantage is that it can span CRM → Order → Billing → Revenue in one suite [37]. Organizations that had fragmented systems (e.g. Excel trackers, disconnected CRM) found it difficult to meet ASC 606’s documentation requirements. By contrast, using SuiteFlow or integrations to stamp POB data into NetSuite sales orders (or directly entering Revenue Arrangements via SuiteScript ensures traceability. Best practice is to have any amendments, renewals, or options flow through the ERP so that each change in contract is captured as a new (or modified) Revenue Arrangement in ARM. This aligns with IFRS/AICPA guidance on handling modification accounting.

-

Cross-Department Collaboration: Under the old standard, sales, legal, and finance could operate somewhat independently (sales recognized a contract when fully billed, legal wrote top-line terms, finance deferred to VSOE manuals). ASC 606 demands that sales and legal be aware of revenue recognition: e.g. finalizing performance obligation scopes correctly, estimating variable components, and providing standalone pricing. NetSuite Administrators noted that “ It’s not just an accounting project – sales, billing, and IT teams all had to align on how orders are entered.” Enterprises often formed cross-functional teams (including sales ops, project managers, accountants, and IT) to ensure that contract terms (renewal rights, upgrade pricing, etc.) were correctly modeled. This cultural shift is frequently mentioned in CPA practice literature as a key success factor [49].

-

Multi-Entity Complexities: Companies with multiple subsidiaries (OneWorld) or multiple accounting books had extra layers. NetSuite’s Multi-Book Accounting allows each subsidiary or reporting framework to have its own ledger under the same ARM configuration. When converting, it’s critical to decide if one subsidiary’s revenue should be combined or handled separately. NetSuite recommends including the subsidiary field in migration searches so that arrangements for each subsidiary/book are migrated correctly [48]. In practice, some multinational firms went one step further: conducting structured workshops in each region to map local business models into the unified global ASC 606 configuration.

-

Audit Trail and Disclosures: Firms needed to enhance notes and disclosures around revenue. This often meant extracting ARM data from NetSuite into reporting tools. For example, building saved searches or reports for “Revenue by POB category” or “Variable revenue estimates” assisted in populating ASC 606 tables in 10-Ks. Companies also had to explain significant judgments in MD&A – e.g. changes in SSP methodology. To ease future audits, many organizations documented their NetSuite setup – publishing a “Revenue Recognition Policy” aligned with system rules. Software vendors and partners frequently emphasize that the NetSuite post-implementation audit process should involve validating that the implemented ARM logic indeed matches the written policy.

-

Future Directions: Post-implementation reviews suggest ASC 606 is relatively stable, but a few discrete issues may arise. The IASB’s review hinted that principal vs agent classification in complex arrangements (e.g. bundled resellers) might deserve attention [51]. Similarly, payments to customers (e.g. rebates or incentives) remain an active area under analysis. From a systems perspective, future NetSuite enhancements may focus on making variable consideration more flexible (e.g. machine learning to project usage revenue), or integrating AI to flag unusual revenue spikes. On the financial reporting side, preparers should watch for any FASB narrow-scope amendments (so far none major since 2018 aside from technical corrections).

Conclusion

The shift from ASC 605 to ASC 606 was one of the most significant accounting changes of the past decade. For NetSuite users, it has meant moving from “legacy revenue recognition” practices to a fully automated, contract-based approach. This report has detailed the theoretical underpinnings (the five-step model and global convergence), as well as practical steps in NetSuite (configuration, migration, and controls).

Key takeaways include:

-

Thorough Planning: The transition must be treated as a cross-functional program. CFOs should ensure finance, sales, legal, and IT are on the same page regarding POB identification and data capture. Surveys indicate many firms were behind deadline, so early action is crucial [7] [9].

-

NetSuite Configuration: Enabling ARM (Essentials/Allocation) and setting up SSP price lists and recognition rules are foundational. Companies must disable legacy methods (residual) and define new triggers and groups in line with ASC 606 logic [46] [4]. NetSuite’s help docs provide a migration framework (Prerequisites, Migration, etc.), but expert assistance is often needed to avoid pitfalls.

-

Data Implications: Potential large shifts in reported revenue timing and balances underscore the need for strong internal controls. Reconciliation and audit readiness are key: maintain workpapers for the contract adjustments and document any judgments (e.g. variable consideration methods). Automated NetSuite processes can reduce manual errors, but only if the underlying data (item pricing, contracts) is accurate.

-

Ongoing Discipline: ASC 606 is not a one-time event. Continuous compliance requires monitoring changes (e.g. product mix shifts, new business models like customer loyalty rewards which are coming under FASB scrutiny [51]) and updating the revenue setup. The ASC 606 framework is here to stay, so organizations should build repeatable processes (within NetSuite and business operations) to handle new contracts in real time. Future FASB or IASB amendments will likely refine corner cases, not overturn the core model.

In essence, ASC 606’s implementation in NetSuite demands careful system reconfiguration supported by deep accounting analysis. But once in place, a system like NetSuite can robustly enforce the principles, automatically handle deferrals, and produce the extensive disclosures required. As evidence from FASB’s PIR shows, stakeholders believe the long-term gains (comparability, reduced diversity) justify the short-term effort (Source: www.bdo.global) [10]. For NetSuite users, this journey transforms revenue recognition from a manual compliance check to an embedded part of the enterprise system – ultimately enabling finance teams to focus on analysis instead of wrestling with disparate accounting rules.

References

- NetSuite Help Center – Transition to the New Revenue Recognition Standard [5] [52]; Migrating Revenue Arrangements and Plans [6] [48]; EITF 08-01 Revenue Recognition Feature (Classic) [3] [13]; Advanced Revenue Management (Essentials) [4] [35].

- FASB and IASB (2014) – “Joint Converged Standard on Revenue Recognition (Topic 606 / IFRS 15)” [1] [11].

- International Financial Reporting Standards – IFRS 15 Standard Summary and History [2] [53]; IASB Post-Implementation Review (2024) [10] [26].

- KPMG – “Revenue Accounting: IFRS vs US GAAP” (IFRS Institute, 2022) [54] [25].

- Deloitte – “Revenue Recognition: Counting Down to 2018 Deadline” (Deloitte/Bloomberg BNA Poll, June 2017) [7] [8].

- BDO – “FASB Issues Post-Implementation Review of ASC 606” (Nov. 2024) (Source: www.bdo.global).

- HouseBlend/NetSuite blog – “NetSuite ASC 606: SaaS Implementation & Compliance Guide” [55] [56] (with cited survey and example data).

- Financial Executives International (FEI) – Journal of Accountancy articles and case studies on ASC 606 (2018–2019) [19] [20].

- Other expert commentary: SEC Financial Reporting Manual (Topic 11: ASC 606) and IFRS Foundation publications (as cited above).

All URLs and sources are cited in the text above.

External Sources (56)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.