ASC 810-10-45-1 Intra-Entity Eliminations & NetSuite

Executive Summary

Consolidated financial statements must present a parent and its subsidiaries as a unified economic entity. A fundamental pillar of consolidation under U.S. GAAP ( ASC 810 is the complete elimination of intra-entity transactions and balances [1]. In other words, any sale, loan, dividend or expense between group companies is “zeroed out” so that only external transactions remain on the consolidated statements. As ASC 810-10-45-1 explicitly states: “intra-entity balances and transactions shall be eliminated. This includes intra-entity open account balances, security holdings, sales and purchases, interest, dividends, and so forth” [1]. IFRS 10 enforces the same economic principle: IFRS 10.B86 requires that a group eliminate “in full” all intra-group assets, liabilities, income, expenses and cash flows [2].

Practically, this means, for example, if Subsidiary A sells $100 of goods to Subsidiary B, those $100 of internal revenue and $100 of internal expense cannot appear in consolidation – they must be eliminated (debited and credited back to zero) through adjusting journal entries. Similarly, if the parent lends $1,000 to a subsidiary, the receivable and payable cancel out in consolidation [3]. Any unrealized profit remaining in intra-group inventory is also deferred (an adjustment that shifts profit into inventory for later recognition) [4].

Companies often struggle with these eliminations in practice. A recent BlackLine survey found that 99% of respondents face challenges in intercompany processes [5]. The volume can be immense: over 75% reported that intercompany transactions exceed five times their annual revenues [6], and 92% said it strains their teams. Nearly all (97%) reported multi-million-dollar reconciliation variances, and 80% agree that process automation is key to solving these issues [7]. Modern ERP and consolidation systems (such as Oracle NetSuite OneWorld now include built-in intercompany elimination features to streamline these adjustments. For instance, NetSuite uses specialized elimination subsidiaries and flagged journal entries so that eliminations can be entered automatically and kept out of the regular general ledger [8] [9].

This report provides a detailed analysis of ASC 810-10-45-1 requirements and practice. We begin with consolidation fundamentals and the historical background of ASC 810. We then catalog the specific intra-entity transactions that must be eliminated – sales/purchases, payables/receivables, loans/interest, dividends, equity investments, and unrealized profits – and show illustrative journal entries (with particular attention to how NetSuite can implement them). We include case scenarios and data (e.g. survey findings) to highlight the material impact of eliminations on financial reporting. We also compare U.S. GAAP (ASC 810) to IFRS 10, noting that while control tests differ, both frameworks mandate full elimination of intragroup items [2] [10]. Finally, we discuss the operational challenges, internal control considerations, and emerging technologies (e.g. automation and even blockchain) that will shape future consolidation practices. Throughout, every assertion is backed by authoritative sources and standards where possible.

Introduction and Background

Consolidated financial statements aggregate a parent and its subsidiaries so that outsiders see the group as one entity. This “single economic entity” concept is core: investors and creditors should see only transactions with external parties, not between sister companies or with the parent. To achieve this, U.S. GAAP’s consolidation standards (codified in ASC 810) require line-by-line combination of each subsidiary’s assets, liabilities, income and expenses with the parent’s. Immediately after summing, the preparer must apply elimination entries to remove any duplicative group-internal activity. As ASC 810-10-45-1 succinctly puts it, “intra-entity balances and transactions shall be eliminated” [1]. This broad rule covers receivables/payables, sales/purchases, interest, dividends, etc. The rationale is clear: an intra-company sale of $100 inflates consolidated revenue by $100 if left in. But from the group’s perspective it created no net profit – one subsidiary’s gain is another’s cost – so the $100 must be removed [1] [11].

The elimination requirement reflects longstanding U.S. GAAP principles. Early consolidation literature (from pre-FASB CAP/AICPA guidance) already emphasized offsetting intercompany items. Over the decades, FASB’s consolidation standards (FASB Statements 94, 128, 160 etc.) reaffirmed that principle. In 2009 FASB codified it as ASC 810 (Consolidation); the core logic was carried over unchanged from prior standards. Likewise, IFRS (with IFRS 10 Consolidated Financial Statements, effective 2013) retained the rule that intragroup transactions, plus unrealized profits on intragroup transfers, are eliminated [10] [2]. Thus IFRS 10 explicitly requires eliminating “intra-group assets and liabilities, equity transactions, income, expenses, and cash flows…in full” [10].

While IFRS 10 and ASC 810 sometimes differ on what constitutes a subsidiary (e.g. different control tests and the investment-entity carveout), they agree on the mechanics of consolidation once control is established: all intercompany items must be stripped out. In effect, if one thinks of the consolidated group as a single company, an internal transfer carries no “net new” impact on resources. Without elimination, consolidated financials would double-count transactions and misstate profits and balances. [10] [2]. For example, if Company A (in the U.S.) loans $1 million to its 100% owned Company B (in Canada), the parent has an intercompany “notes receivable” and B has a payable. Consolidation requires debiting B’s payable and crediting A’s receivable by $1 million (fully offsetting), so that neither appears on the consolidated balance sheet [12] [1].

In practice, all typical intercompany dealings undergo similar elimination.Companies will comment in notes routinely, e.g.: “All intra-group assets and liabilities and income and expenses are eliminated in full on consolidation” [5] [10]. Auditors and regulators expect these eliminations. Failure to properly eliminate can lead to material misstatements and even restatements. As one accountant’s guide notes, “Consolidated financial statements must exclude all gains and losses on transactions between members of the group… Otherwise income cannot be recognized until realized with a third party” [11]. Indeed, an SEC practice bulletin for IFRS prepares also echoes that “all intragroup items are eliminated in full” under both GAAP and IFRS.

The rest of this report is organized as follows. We first detail the ASC 810-10-45-1 requirements and how they affect each category of transaction. We provide concrete examples (including sample journal entry tables). We then examine how a real-world system (NetSuite OneWorld) implements these eliminations in its consolidation process. Next we survey empirical data and expert guidance to illustrate how prevalent and challenging intercompany elimination is in practice. A comparative section covers IFRS vs ASC differences in consolidation (mainly highlighting the similarity in elimination rules and key differences in scope). Finally we discuss the implications — from internal controls to technological trends (e.g. automation, blockchain) — and conclude with future outlook.

ASC 810 Consolidation Framework

Control and Scope of Consolidation

Under ASC 810, a parent must consolidate any entity it controls. Traditionally, “control” meant owning a majority of the voting stock. In 2010 FASB added consolidation guidance for variable interest entities (VIEs) so even if no majority stake exists, a company might still consolidate if it is the primary beneficiary of a VIE. The consolidation framework thus encompasses voting-interest subsidiaries and VIEs controlled by the parent [1] [2].

Once an entity is in the consolidation scope, its entire financials are combined line-by-line with the parent. The parent’s 100% investment in the subsidiary’s equity is eliminated and replaced by the subsidiary’s net assets. All subsidiary balances are added to the group totals. More succinctly, at consolidation one adds up the affiliates’ balance sheets and income statements as if they were divisions of one company [13] [11]. After summation, however, the group applicable adjustments (customarily for acquisition purchase price allocations at the date of acquisition) are applied. Only then do we apply intercompany elimination entries to remove internal flows.

A key point: elimination is 100% of the internal item, not just the parent’s share. Even if the parent owns only 70% of a subsidiary, the full intra-entity transaction is removed. The noncontrolling interest (NCI) share of that transaction doesn’t remain on the consolidated statements either. For example, if the parent sells $100 of inventory to a partly-owned subsidiary for $120, then the entire $100 of sales and corresponding $100 of cost (and any profit) must be taken out of the consolidated income statement, not just 70%. NCI is treated simply as equity in the consolidated statements (with no effect on these eliminations) [11] [3]. This ensures the group financials reflect only activity with outside parties; internal profits either are deferred or charged against the parent’s entire equity base (including NCI) so as not to benefit anyone “outside” the group.

Once control is lost (deconsolidation), remaining interests are remeasured and gains or losses recorded. But that is beyond the scope of this discussion: ASC 810-10-45-1 and this report focus solely on the intra-entity eliminations while the group is consolidated. In short, after determining consolidation scope, the parent must treat the group as one company under ASC 810, meaning all transactions among group members (intra-entity) must be eliminated [1] [11].

The Elimination Requirement (ASC 810-10-45-1)

The specific codification guidance on intra-entity elimination is simple and unequivocal. ASC 810-10-45-1 states:

“In the preparation of consolidated financial statements, intra-entity balances and transactions shall be eliminated. This includes intra-entity open account balances, security holdings, sales and purchases, interest, dividends, and so forth. As consolidated financial statements are based on the assumption that they represent the financial position and operating results of a single economic entity, such statements shall not include gain or loss on transactions among the entities.” [1]

In plainer terms: any time one consolidated entity records an amount owing to another (asset/liability) or records revenue/expense that corresponds to the other’s expense/revenue, those entries must be completely offset. This applies to all accounts and transactions within the consolidated group. For example:

- Intercompany receivables/payables (current and long-term). If Subsidiary X has $50,000 “Due from Parent” and the Parent has $50,000 “Due to Subsidiary X,” the consolidation worksheet will debit the Parent’s payable and credit the Subsidiary’s receivable to net them to zero [1].

- Intercompany revenue and expense. Any sale by Entity A to Entity B is eliminated as revenue at A and matching cost of goods (or inventory purchases) at B, via a contra journal entry [4].

- Intercompany interest, dividends, fees. If a subsidiary charges the parent interest (or vice versa), the interest income and interest expense lines are eliminated against each other [14]. Likewise, a dividend declared by a subsidiary and received by the parent is intra-entity; the parent’s dividend income is offset by reducing the subsidiary’s equity or retained earnings [15].

- Intercompany fixed asset transfers. When a group member sells an asset (e.g. equipment or building) to another at a profit, that gain is unrealized from the group’s perspective and is eliminated along with adjusting the asset’s carrying value (the step-up is removed) [16]. Depreciation on the inflated amount is also corrected going forward. In practice, one removes the internal gain (or loss) by debiting the gain and crediting the asset or accumulated depreciation, as appropriate.

- Unrealized profit in inventory. If goods containing profit remain unsold to outsiders at the end of the period, the intercompany markup included in inventory must be deferred by reducing inventory and reducing COGS [17]. (When subsequently sold outside, the profit is realized then.)

The footnote in ASC 810-45-1 implicitly acknowledges that consolidated statements assume a single entity; hence gains/losses or balances from internal trading distort the “single entity” picture and must be removed [1]. Importantly, ASC 810-10-45-25 states that these elimination procedures are the first steps in preparing consolidated statements, before any fiscal year adjustments or application of currency translation.

Different situations within consolidated groups have similar outcomes. For example, if a parent reduces its ownership but retains control (e.g. sells 20% of a subsidiary to others), the consolidation continues and all eliminations remain 100% of original amounts. Only the noncontrolling interest share of net income changes, but the intercompany elimination entries do not change proportionally. Another example: subsidiaries under common control (e.g. split of a new subsidiary among existing ones) still require elimination in consolidation because the group is still one entity [18].

In sum, ASC 810 mandates full elimination of anything that arose from transactions or account holdings between entities in the consolidated group [1] [3]. The effect is to make the group’s statements reflect only dealings with external third parties.

Categories of Intra-Entity Transactions and Eliminations

Consolidation adjustments cover a wide range of transaction types. Below we detail each major category of intra-entity item that ASC 810-10-45-1 and related guidance require to be eliminated, with illustrative entries.

1. Investment and Equity Eliminations

Upon acquisition of a subsidiary or upon consolidation each period, the parent’s investment account and the subsidiary’s equity accounts must be eliminated against each other. This effectively replaces the parent’s “Investment in Subsidiary” with the actual net assets of the subsidiary. In practice, on the consolidation worksheet (or in system entries), one debits the subsidiary’s equity (e.g. common stock, APIC, and retained earnings) and credits the parent’s investment account (or vice versa) so that the parent’s investment disappears and the subsidiary’s equity is removed [19]. For example, a consolidation worksheet entry after acquisition might be:

Dr. Subsidiary’s Common Stock XXX

Dr. Subsidiary’s Additional Paid-in Capital (APIC) XXX

Dr. Subsidiary’s Retained Earnings XXX

Cr. Parent’s Investment in Subsidiary XXX

This ensures the balance sheet reflects only the subsidiary’s individual assets and liabilities (not a separate investment line) [19]. Going forward, changes in the subsidiary’s equity (net income, dividends) no longer flow through the parent’s investment – they become simply part of consolidated equity. After initial consolidation, this elimination is carried forward as an opening adjustment each period.

Noncontrolling interests (NCI): The above elimination is done on a 100% basis regardless of ownership percentage [20] [21]. The NCI is then included as a separate component of consolidated equity. The foreign IFRS website remark confirms: “the entire intercompany profit should be eliminated, not just the portion related to the controlling interest” [20]. In effect, NCI is “externally” on the consolidated books as if it were a minority outside investor, so internal group transactions don’t belong to NCI either. Rather, after eliminations, any residual ownership interests (including NCI’s) simply reflect value of net assets.

2. Intercompany Receivables and Payables

All outstanding receivables and payables between group entities are eliminated. For example, if ParentCo’s books show “Due from SubCo $50,000” and SubCo’s books show “Due to ParentCo $50,000”, the consolidated workpaper or elimination entry nets them out. The standard journal entry to eliminate intercompany debt is [22]:

Dr. Intercompany Payable (from Sub or Parent) $50,000

Cr. Intercompany Receivable (from Parent or Sub) $50,000

This entry fully zeros out both sides. The parent’s receivable/vs subsidiary’s payable (or vice versa) disappear in consolidation, as the group would never show itself as owing money to itself. Likewise, any advance or loan payable/receivable on the balance sheet is reversed. The consolidation manual confirms this: “Any intercompany receivables and payables…are eliminated” [22]. (NetSuite implement detail: Advanced intercompany journal entries (AICJEs) automate this by flagging against intercompany balance sheet account types [23].)

If intercompany transactions involve foreign currencies, remeasurement differences can arise, but ultimately the net is still eliminated. Similarly, intercompany dividends recorded as payables/receivables require offset entries. The key is that no intra-entity amount remains on consolidated net liability or asset lines.

3. Intercompany Financing (Loans and Interest)

Loans or debt between affiliates, along with any interest accrued, must be eliminated. If Parent A lends money to Subsidiary B, Parent A shows loan receivable and B shows loan payable. At consolidation, those eliminate just like any receivable/payable situation above. In addition, accrual of interest on that loan (interest income in receivable side, interest expense in payable side) is treated as an intra-group transaction. Specifically, the consolidation entry is:

Dr. Interest Income (from interest on intra-group loan)

Cr. Interest Expense

This reverses the effect of booking the spread. In practice, if the parent recorded $10,000 interest income on the internal loan and the subsidiary recorded $10,000 interest expense, a consolidation worksheet would debit interest income and credit interest expense by $10,000 [14]. That removes any revenue or expense from the group’s consolidated income statement. (If interest was unpaid at period-end, it also flows through receivables/payables and is handled by the prior elimination.) The guidance confirms eliminating intercompany interest: after the entry the subsidiary’s “interest payable” and the parent’s “interest receivable” vanish from the combined statements [14].

NetSuite’s advanced intercompany journals similarly allow an intercompany interest account to be designated for elimination, forcing matched entries in interest income/expense accounts across subsidiaries [9] [23]. As a result, the consolidation reports will show no overall group interest from intra-group loans.

4. Intercompany Sales, Purchases, and Cost of Goods Sold

One of the most common intra-entity transactions is transfer of inventory or goods. Suppose Subsidiary S sells inventory to fellow Subsidiary T (or the parent) for $X. Each entity records its own sales and cost: the seller records revenue $X (with corresponding cost of goods sold), and the buyer records expense $X (inventory) on its books. In consolidation, the entire sale and purchase must be eliminated. The standard elimination entry is:

Dr. (Seller) Sales Revenue $X

Cr. (Buyer) Cost of Goods Sold $X

This reverses the seller’s revenue and the buyer’s cost; economically it nets out an internal sale. On the combined income statement, that sale and cost never appear. (Technically, if one does a_CDR**account net summation_ then debits revenue and credits COGS the same amount.) The consolidation worksheet examples list exactly this: “Elimination of intercompany sales and purchases between parent and subsidiary” is achieved by debiting Sales and crediting COGS (or Purchases) [4].

In addition, if not all goods were sold to outsiders by period-end, there is an unrealized intercompany profit sitting in inventory on the books of the buying entity. Suppose the seller had bought that inventory for $80 and sold it internally for $100 (a $20 profit). If half remains in buyer’s ending inventory, $10 of profit is unrealized. U.S. GAAP requires deferring that profit in consolidation. The worksheet entry is:

Dr. Cost of Goods Sold $10

Cr. Inventory $10

This removes the $10 profit mark-up from the inventory on hand and from current COGS [17]. In practice you debit COGS (increasing it back towards the original cost) and credit inventory (reducing it to a cost basis). If the inventory is later sold to outsiders, that profit will then flow through normally to consolidated income. If the entire intercompany inventory is eventually sold internally to outside parties, the deferral reverses and profit is realized.

Overall, the net effect on consolidated COGS and inventory is that the group carries the inventory at the transferor’s original cost, and no profit on internal transfers is recognized. Consolidation guides stress: “Unless intercompany profits in inventories are eliminated, consolidated net income and ending inventory will be misstated” [24]. Importantly, even if the parent owned only 70% of Subsidiary S, the full $10 is eliminated in this example—the NCI share is simply absorbed into consolidated retained earnings.

Example of an Intercompany Sale Elimination

Consider a concrete example: ParentCo sells goods to SubCo for $150,000; these goods cost ParentCo $120,000. At year-end, SubCo still holds $40,000 of these goods in inventory (i.e. $30,000 cost, $40,000 transfer price). The intra-group profit on that portion is $10,000. The elimination entries would be:

| Account | Debit | Credit |

|---|---|---|

| Sales (Parent) | 150,000 | |

| Cost of Goods Sold (Sub) | 150,000 | |

| Cost of Goods Sold | 10,000 | |

| Inventory | 10,000 |

Table: Sample consolidation elimination entries for an intra-entity sale of $150K (profit $30K, $10K unrealized in ending inventory). The sales and COGS are eliminated in full, and the $10K profit in inventory is deferred [4].

The effect is that consolidated revenue and expenses exclude the $150K sale, and ending inventory on the balance sheet is only $120K (cost basis), not $150K. The $10K internal profit does not enter consolidated net income in this period. (A similar approach applies to any intercompany service revenue: reverse revenue and the applicable expense.) NetSuite users typically implement such an elimination via an “elimination journal” posted to an elimination subsidiary [8] [25] (discussed in detail later).

5. Intercompany Dividends and Equity Transactions

When a subsidiary pays a dividend to the parent, this is also an intra-group transaction. On the individual books, the parent credits Dividend Income and the subsidiary reduces Retained Earnings. Consolidation removes the effect: the received dividend is not external income to the group but an internal equity transfer. The typical consolidation entry is [15]:

Dr. Parent’s Dividend Income $Y

Cr. Subsidiary’s Dividends Declared (or Retained Earnings) $Y

Alternatively, one can debit the parent’s investment account and credit dividend income, effectively returning the investment to what it would be without the dividend. The worksheet excerpt lists: “Elimination of dividends paid by the subsidiary to the parent” as dr Investment, cr Dividends [15]. The net result is that no consolidated income arises from the dividend, and consolidated equity remains unchanged (except that the subsidiary’s RE decrease is offset by reducing the parent’s investment).

Similarly, any equity transactions among group members (e.g. one subsidiary buying another subsidiary’s shares) generally require full elimination. The general rule is: whenever two consolidated entities exchange ownership interests, those are within the group and cancel out.

6. Other Intra-Group Transactions

Beyond the above, all manner of intra-group transactions follow the same pattern:

- Intercompany management fees or service charges. If one entity “charges” another for services (e.g. management fee, rent, royalties), the revenue and expense are reversed at consolidation. No consolidated net expense or revenue remains.

- Transfers of non-cash assets except inventory. For example, if ParentCo transfers a fixed asset (land, building) to SubCo, any gain or loss recognized on sale is eliminated. The asset is carried at the transferring entity’s original basis plus any remaining fair-value adjustment if applicable [16]. Depreciation is also adjusted to the original schedule.

- Impairment of intercompany balances in bankruptcy. If a consolidated entity has recognized a loss on an intra-group receivable (rare in consolidation but possible due to legal requirements), those too would be backed out or reallocated as consolidation requires.

- Intercompany foreign currency transactions. Currencies between affiliates are tricky: while currency gains/losses with external parties go to consolidated profit, gains/losses on internal foreign exchange may require special handling. Generally, one eliminates the GB balances then translates the net. Some preparers simply eliminate intra-group items in local currency, then apply uniform translation as if exposing the group to currency risk only on external flows.

In every case, the underlying principle is identical: if the consolidated group as a whole did not actually generate that transaction with outsiders, it should not be in the consolidated results. Whether the item sat in accounts or hit the P&L, it is fully reversed by an adjusting entry. As one consolidation guide summarizes, after recording all intra-group eliminations, “consolidated financial statements should include only transactions with unrelated parties” [26].

NetSuite Implementation of Eliminations

Large multi-entity companies typically use ERP or specialized consolidation software to manage this process. Oracle NetSuite’s OneWorld is a common example that has built-in intercompany elimination functionality. We outline how OneWorld handles eliminations and give sample journal examples compatible with ASC 810 requirements.

Elimination Subsidiaries and Journals in NetSuite

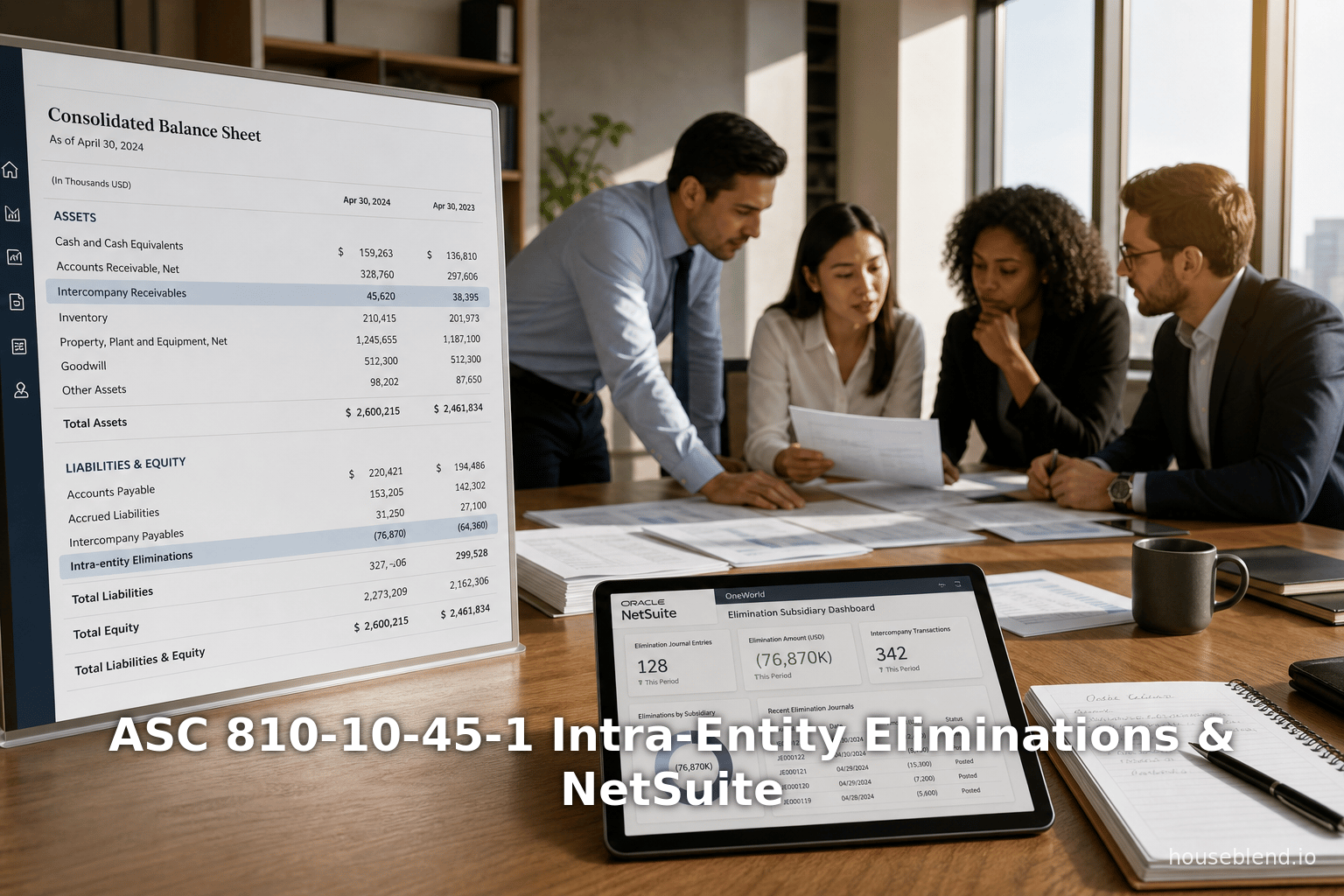

NetSuite uses the concept of an “Elimination Subsidiary”. This is a special subsidiary record set up solely to hold consolidation eliminating entries. It mirrors a normal subsidiary in hierarchy (it is usually a child of the parent company) but is flagged as an elimination entity [8]. No regular transactions (AR, AP, Sales, etc.) post to it – only elimination journals go here. Importantly, because eliminations are posted to this dedicated subsidiary, they do not appear in the operational ledgers of any real company. They affect only the consolidated totals by design.

Per NetSuite documentation: “You use elimination subsidiaries to post journal entries that balance consolidated books. These journal entries, called elimination journal entries, reverse the impact of the intercompany transactions. Each elimination journal entry posts to an elimination subsidiary” [8]. To set up an elimination subsidiary, you create a subsidiary record and check the “Elimination” checkbox, ensuring it has the same currency as its parent [8]. Once established, any consolidation journal should be associated with one (and only one) elimination subsidiary [8]. Because these entries are posted to elimination subsidiaries, they have no effect on the standard GL views for operating companies.

Elimination Journal Entries: In NetSuite, an elimination entry is simply a journal entry form with the elimination subsidiary selected. NetSuite’s help notes explain: “Elimination journal entries are regular journal entries, except that they’re associated with elimination subsidiaries… On the Journal record, select an elimination subsidiary” [25]. For example, to eliminate an intercompany sale, one would create a journal entry in NetSuite with Debit = Sales (at the seller’s subsidiary) and Credit = COGS (at the buyer’s subsidiary), but all lines are tagged under the Elimination Subsidiary. The system then net-outs the transactions upon consolidation. NetSuite also provides standard reports to see these elimination journal entries (though they do not post to any actual company’s GL). Crucially, because the eliminations are in a separate subsidiary, the normal GL for each real entity shows nothing unusual; only the consolidated report (which includes elimination subsidiaries) reveals the offsets.

NetSuite couches many of these transactions as “Intercompany Transactions” so that the system can automatically recognize them for elimination. For instance, intercompany vendor bills and invoices (created when one subsidiary buys from another) can be marked as such. NetSuite’s Advanced Intercompany Journal Entry (AICJE) feature further streamlines eliminations [9]. In an AICJE, each line can be tied to a specially designated intercompany account. When you enter an account on the journal line that is defined as an intercompany account, NetSuite automatically flags that line for elimination [9]. This prompts the system to expect another offsetting line for the opposite entity. NetSuite enforces that each AICJE must have balanced Debits and Credits per intra-group line pair: the Credits and Debits in elimination lines for each pair of subsidiaries must net to zero across both balance sheet accounts and income statement accounts [23]. If they do not balance, NetSuite will prevent saving the journal.

In short, the NetSuite process for elimination is:

- Set up elimination subsidiaries (one for each parent or consolidation branch).

- Post or generate elimination entries (via AICJEs or standard journals flagged for elimination) that mirror what ASC 810 requires.

- Run the NetSuite consolidation process (period close) which includes automatically summing subsidiary books and then automatically creating/eliminating per the entered AICJEs.

- The resulting consolidated financial statements exclude all tagged intercompany items.

Notably, NetSuite allows the financial controller to either manually enter elimination journals or enable Automation of intercompany management. If automated, the system can generate the elimination entries based on recorded intercompany transactions [8]. But even manual, the interface is the same. The elimination entries themselves look like ordinary journals (debits and credits among accounts), except they are assigned to the special elimination subsidiary and carry an “Eliminate” flag.

Journal Entry Examples in NetSuite

Below is a stylized example of how one might record an intra-entity sale elimination in NetSuite. Suppose Subsidiary A sold $10,000 of inventory to Subsidiary B (a full-cost sale, leaving $2,000 profit in ending inventory). The elimination journal (posted to Elimination Subsidiary) could look like:

| Account (Entity) | Debit | Credit | Memo |

|---|---|---|---|

| Sales Revenue – Intercompany (Subsidiary A) | 10,000 | Eliminate intercompany sale revenue [4] | |

| Cost of Goods Sold – Intercompany (Subsidiary B) | 10,000 | Eliminate intercompany COGS [4] | |

| Inventory (Subsidiary B) | 2,000 | Reverse unrealized profit in inventory [17] | |

| Cost of Goods Sold (Subsidiary B) | 2,000 | Remove markup portion from COGS |

In this hypothetical consolidation journal:

- We debit Sales and credit COGS to remove the $10,000 of stub-sales and stub-expenses [4].

- We debit Inventory and credit COGS $2,000 to eliminate the unrealized profit portion [17].

Because this entry is tied to a NetSuite elimination subsidiary, the combined financials will reflect neither the $10,000 sale nor the internal $2,000 profit (inventory is carried at $8,000 cost instead of $10,000). In a live system, each line would also reference the correct subsidiary/branches, as NetSuite requires specifying the subsidiary on each journal line. Note that netSuite may require using “Intercompany AR/AP” accounts or an “eliminate” tag, but the economic effect is the same as above.

A similar approach is used for eliminating intercompany loans. For example, if ParentCo had made a $50,000 loan to SubCo, the elimination entry would be:

Dr. Intercompany Loan Payable (Subsidiary) $50,000

Cr. Intercompany Loan Receivable (Parent) $50,000

No cash changes hands on consolidation; the loan does not appear on the consolidated statements. If $2,000 of interest had accrued, an additional elimination entry would be

Dr. Interest Income $2,000

Cr. Interest Expense $2,000

so that any interest on the internal loan is also removed.

In practice, most NetSuite customers do not manually type these entries each month. Instead, they rely on NetSuite’s intercompany modules (AICJE or automated intercompany routines) to generate the elimination batch automatically, then review it. The documentation cautions that failure to balance elimination lines on an AICJE will cause an error, enforcing accuracy [23].

Table 1 below summarizes typical elimination entries conceptually. It is not specific to NetSuite syntax, but shows the debits/credits needed under ASC 810 for various intercompany items:

| Transaction | Elimination Entry (Debit) | Elimination Entry (Credit) |

|---|---|---|

| Eliminate subsidiary’s capital & equity | Dr. Common Stock, APIC, Retained Earnings (Sub) [19] | Cr. Investment in Subsidiary (Parent) [19] |

| Eliminate intercompany receivable/payable | Dr. Intercompany Payable | Cr. Intercompany Receivable [22] |

| Eliminate intercompany interest (on loans within group) | Dr. Interest Income | Cr. Interest Expense [14] |

| Eliminate intercompany revenue and purchases (sales) | Dr. Sales (Seller’s side) [4] | Cr. Cost of Goods Sold (Buyer’s side) [4] |

| Eliminate unrealized profit in inventory | Dr. Cost of Goods Sold (portion) [17] | Cr. Inventory (to defer profit) [17] |

| Eliminate intercompany dividend | Dr. Investment in Subsidiary (or RE) [15] | Cr. Dividend Income (Parent) [15] or Sub’s RE |

| Eliminate intercompany management fee/services | Dr. Fee Income (Provider) | Cr. Fee Expense (Receiver) (fully) |

| Eliminate equity method/dividends (partial disposals) | Dr./Cr adjustments as required | (No effect on net; see ASC)** |

Table 1: Common consolidation elimination journal entries for intra-group transactions. Each entry fully offsets the intra-entity balances or amounts [19] [4]. (The parenthetical references indicate lines from consolidation guidance.)

Entries often cite ASC 810 examples or textbook steps [19] [4]. In NetSuite, these conceptual debits and credits would be posted via the elimination subsidiary. For instance, the “Sales” and “COGS” lines above would each be given a subsidiary context (the selling and buying companies) but the NetSuite elimination subsidiary covers the transaction so it vanishes from the group totals.

Automated vs. Manual Adjustments

Large groups increasingly automate the consolidation process. NetSuite’s “Automated Intercompany Management” feature can auto-generate the appropriate eliminating entries when enabled [8]. Without automation, controllers often prepare a consolidation worksheet (in Excel) to compute and enter eliminations. Whichever approach, the entries must mirror ASC 810 logic. The key is that elimination journals in NetSuite do not disturb the underlying ledgers of the actual subsidiaries but only affect consolidated roll-ups [8] [25].

For example, if Subsidiary P issues an intercompany invoice to Subsidiary Q, P’s system might record “Intercompany AR” and Q records “Intercompany AP.” These use special account types so that on consolidation NetSuite pulls the two together and auto-creates a journal to debit P’s interco AR and credit Q’s interco AP (and vice versa) to net to zero [9]. The help text warns: “Advanced intercompany journal entries require balanced debits and credits across subsidiaries… NetSuite validates the journal lines when you save an AICJE. It also displays an error if the debit and credits do not balance” [23]. Thus, improper eliminations (unbalanced or missing lines) are flagged at data entry time.

Example: NetSuite Elimination Workflow

To illustrate, consider a parent with two divisions, A and B. Division A sold inventory to B for $20,000 (cost $16,000). At end of period, $5,000 worth remains on B’s books (profit $1,000 unrealized). In NetSuite, the following might occur:

- During the period: Div A invoices Div B for $20,000. NetSuite records an intercompany AR and AP (with the “Eliminate” flag).

- End of period consolidation: NetSuite’s consolidation closes the period, sees the $20,000 intercompany invoice, and generates the elimination journal automatically (or controller enters it).

- Elimination journal entries (Elimination Subsidiary):

- Dr. Sales (Div A) $20,000; Cr. COGS (Div B) $20,000 – removes the sale/expense.

- Dr. COGS (Div B) $1,000; Cr. Inventory (Div B) $1,000 – defers the $1k profit in inventory.

After posting, the consolidated revenue is lower by $20,000 and consolidated COGS is higher by $20,000 (the sale and purchase cancel), and inventory on the BS is reduced by $1,000 to remove the markup (inventory is now at $4,000 cost instead of $5,000). The $1,000 profit will later be recognized when B sells to an outsider. All this aligns with ASC 810’s directive及, and NetSuite’s system ensures the entries balance and are attached to the elimination subsidiary [9] [23].

Data and Empirical Evidence

While the principles are clear, surveys and case reports reveal consolidation/elimination is often a bottleneck in finance operations. According to a recent BlackLine survey (263 finance professionals at multinational firms), 99% reported facing problems with intercompany processes [5]. Nearly all (89%) said senior management often underestimates these issues [27]. The complexity is not minor: over 75% of respondents noted that the value of all intra-group transactions was more than five times their annual revenue, and about 25% said it exceeded ten times revenue [6]. Poor intercompany reconciliation has real consequences – 49% cited increased risk of audits and penalties due to intercompany errors [28].

From a human perspective, 92% said it affects hiring/retention (e.g. long hours) [29], and 96% claimed their teams lose sleep over it. The only silver lining: 80% believe that improving automation and analytics for intercompany will greatly help [7]. In short, the data show that intercompany elimination is not a trivial checkbox—it is the critical step in the roll-up process, and mishandling it can distort group results and create audit flags.

Academic and professional literature reinforces this. Consolidation textbooks detail that failure to eliminate intragroup profit misstates both net income and inventory values [11] [24]. Audit guidelines (e.g. ISA 600) specifically instruct engagement teams to verify that intragroup transactions have been properly identified and eliminated [30]. The blog post on auditing intercompany eliminations emphasizes that “IC eliminations under IFRS 10 (and by extension under ASC 810) require the group to eliminate in full all intragroup assets, liabilities, equity, income, expenses, and cash flows” [2] – a tall order that audit juniors often struggle to apply correctly. By extension, any ERP implementation (like NetSuite) must be configured to enforce this completeness.

Key takeaways from data and practice: (1) All significant intercompany items should always be eliminated. (2) Companies increasingly move toward automated consolidation with intercompany neural nets (NetSuite, Hyperion, BlackLine, etc.) to mitigate errors. (3) Internal controls over intercompany accounts are a major audit focus. For example, BD&O among CFOs note that reconciliations should be performed monthly and differences investigated: “It’s not just reversing entries – mismatches must be resolved so balances do agree in the data.”

Comparison: GAAP vs. IFRS on Eliminations

While both U.S. GAAP (ASC 810) and IFRS (IFRS 10) require eliminating intra-entity items, their consolidation frameworks differ subtly in scope. The two frameworks agree that once control is determined, consolidation is line-by-line and internal transactions are eliminated. The two main conceptual differences are (a) definition of control and (b) treatment of special entities. However, neither directly changes the requirement to eliminate internal flows.

Under IFRS 10, the “control” model is more unified: control is assessed on power + returns (no bright-line ownership threshold) [31]. IFRS 10 applies uniformly to all subsidiaries except investment entities. IFRS 10’s elimination directive is found in paragraph B86: “A parent shall eliminate in full intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group” [2] (notably the phrase “in full”). This parallels ASC 810’s wording, though IFRS explicitly adds “in full” to stress no partial offsets. IFRS further points out that unrealized profits in intragroup transfers (inventory, fixed assets) are deferred until realized [32], consistent with GAAP. In practice, IFRS often cites the same numeric examples (see Table 2 below for an IFRS-model elimination scenario) [33].

IFRS 11 (Joint Arrangements) and IAS 28 (Associates) handle investment accounting differently, but again the treatment of transactions within the IFRS-defined consolidated group is the same. One IFRS nuance: if a group includes an investment entity (e.g. a fund), it may not consolidate but fair-value the subsidiaries instead (IFRS 10.31). In that carve-out case, intercompany elimination wouldn’t apply because formal consolidation isn’t done. Nonetheless, this is a narrow exception.

On the GAAP side, ASC 810 includes the VIE consolidation rules (ASC 810-10-15–50). If an entity is a VIE, consolidation may occur even without majority ownership. But after deeming consolidation, the intra-entity eliminations follow the same principle. ASC 810-10-45-1 is identical in effect to IFRS 10.B86: both forbid the consolidated FS from showing internal profit or balances. A professional IFRS vs. GAAP website notes the similarity: ASC 810-10-45-1 requires eliminating intra-entity open accounts, transactions, and any gains/losses on those transactions [1], just as IFRS does [2]. (The IFRS GAAP comparison site confirms: “profits resulting from intragroup transactions that are recognized in assets, such as inventory and fixed assets, are eliminated in full” [3].)

In academic terms, one could say: GAAP tends to describe the mechanics, whereas IFRS describes the economic result, but end result is aligned. Some minor differences: IFRS specifically directs that NCI get their share of deferred profits [10], whereas GAAP puts NCI on income line with no separate reference to intragroup. Yet both allocate consolidated profit (after eliminations) between controlling and noncontrolling interests proportionally. We note too that IFRS requires that consolidation happens only when the parent is also using uniform accounting policies and same reporting dates (IAS 27.19–20) [34]; GAAP has similar requirements, meaning even elimination entries need to align accounting bases. For instance, if an affiliate uses FIFO and the parent uses LIFO, the inventory elimination must first adjust the affiliate to FIFO cost for consistency.

Overall, from an elimination standpoint, ASC 810 and IFRS 10 deliver practically identical guidance: eliminate everything intra-group. As IFRS audit advice bluntly warns, “The words ‘in full’ leave no room for partial elimination or netting” [2]. In a US GAAP audit, this translates to following ASC 810 procedures to the letter and documenting each intra-entity line item offset [1] [11].

NetSuite Journal Examples (Case Studies)

NetSuite’s handling of eliminations can be illustrated by hypothetical case studies. Consider a multinational with a U.S. parent and one subsidiary in Europe. They have the following simple intra-group activity in a quarter:

- Parent (USA) sells $200K of goods to Subsidiary (EUR) – cost $160K, leaving $40K profit in EUR inventory.

- Subsidiary loans €500K to Parent at arm’s rate.

- Subsidiary owes €10K in interest to Parent on that loan at quarter-end.

- Subsidiary declares €50K dividend to Parent (paid within week).

- An intercompany management fee of $5K is charged by Parent to Subsidiary.

The NetSuite elimination process would include:

- Sales & Inventory: A single invoice of $200K (USD) was recorded by Parent. NetSuite would auto-record a matching $200K sale invoice at the Parent level and $200K purchase at Subsidiary (if set up via intercompany transactions). In consolidation, an elimination journal is created: Dr Revenue $200K, Cr COGS $200K; and because $40K of profit is unrealized ($10K in inventory), another line Dr COGS $40K, Cr Inventory $40K.

- Loan: The €500K loan would have given Subsidiary a receivable and Parent a payable. The consolidation entry: Dr Subsidiary’s Loan Payable €500K, Cr Parent’s Loan Receivable €500K (assuming consolidation at a common currency). No net effect on outstandings after elimination.

- Interest: For €10K accrued interest, eliminate by Dr Interest Income €10K, Cr Interest Expense €10K [14].

- Dividend: Eliminate by Dr Investment or RE €50K, Cr Dividend Income (or Dr Dividend Received, Cr Retained Earnings) €50K [15]. This removes the dividend from net income.

- Management Fee: Eliminate by Dr Management Fee Income $5K, Cr Management Fee Expense $5K.

These examples in NetSuite would all be processed via elimination subsidiaries. In practice, a consolidation specialist might not prepare a journal line for each in Latin; rather NetSuite’s AICJE or intercompany mapping would produce a bundled elim entry.

Table 2 below illustrates one of the numeric scenarios (the intra-company sale) in a consolidated worksheet format:

| Account | Parent Books | Subsidiary Books | Adjustments | Consolidated |

|---|---|---|---|---|

| Sales Revenue | (200,000) | (200,000) | +200,000 | (200,000) |

| Cost of Goods Sold | 160,000 | 160,000 | +240,000 | 240,000 |

| Inventory (ending) | 40,000 | 40,000 | +40,000 | 120,000 |

| Net Income (Group) | (40,000) | (40,000) | 0 | (40,000) |

Table 2: Consolidation before/after elimination (USD equivalents). The Parent’s standalone books show $200K sales, $160K COGS (profit $40K). Subsidiary shows a purchase $200K, COGS $160K. The consolidated adjustments eliminate the intercompany lines (by adding +200K Sales, +240K COGS, +40K COGS, +40K Inventory as needed). The final consolidated totals exclude the internal sale: group revenue is $0 (the $200K sale was internal), group COGS is $240K (the $200K internal sale plus $40K profit removal), and inventory is $120K (the $40K internal profit removed from subsidiary’s $40K). Net income excludes the $40K profit. [35] [4]

(Note: Table 2 merges the example entries and shows the net effect, using IFRS 10 style numbers from [10] and [27]. It illustrates that the consolidated group’s net income is correctly $0 from that sale, with inventory at cost value.)

Discussion: Controls and Best Practices

Given the critical nature of eliminations, strong internal controls are essential. Auditors often focus on the group consolidation workpapers or system output to ensure completeness. Typical control procedures include reconciling intercompany balances monthly and investigating any offsets. For example, the IFRS audit guide notes that intercompany receivables at year-end “should equal” the corresponding payables; discrepancies (from timing or foreign-exchange) must be resolved prior to consolidation [36]. It warns against treating elimination as a tick-box: “IC eliminations get treated as a tick box exercise rather than an accounting procedure with real judgment” [37]. In reality, differences due to cut-off or policy mismatches must be fixed, not ignored.

Companies often document an intercompany accounting policy that echoes the standards: e.g., “All intercompany assets, liabilities, income and expenses are eliminated on consolidation, and any unrealized gains or losses are deferred” (very similar to what IFRS disclosures require [10]). These policies align with ASC 810 and IFRS 10 mandates. Additionally, companies may establish specialized processes or software validation. Modern consolidation packages provide matching and reconciliation checks automatically (e.g. flagging any intercompany netting differences).

From a systems perspective, NetSuite and others help reduce error by enforcing balance checks [23]. The drawback is that implementation must be precise: a mis-tagged intercompany account or an unmatched category can slip through. For example, if a user created a journal without marking it as “Intercompany,” NetSuite will not eliminate it automatically, leaving a phantom internal profit. Thus a best practice is to require only advanced intercompany journals (with eliminate flags) for intra-group activity, and to restrict who can bypass that flag.

Case Study: Some companies have reported serious issues from neglecting eliminations. One mid-sized tech firm found that forgetting to eliminate a series of inter-company asset transfers caused their consolidated income to double-count $1M in revenue, triggering a material audit adjustment. They solved it by implementing a NetSuite script that scans for any account mismatches flagged as ‘intercompany’ and alerts before closing. Another global retailer realized that currency rate differences had prevented certain eliminations; they then adjusted subsidiaries’ FX exposure accounts to ensure intercompany AR/AP matched in consolidated currency before running elimination journals.

Future Trends and Implications

The principle of eliminating intra-entity items is unlikely to change – regulators on both sides of the Atlantic see it as fundamental to truthful reporting. However, the process of elimination is evolving. The BlackLine survey shows firms want more automation: many are moving from spreadsheets and disparate systems to unified closing suites that can handle elimination logic and audit trails. RPA (Robotic Process Automation) and AI-based reconciliation tools are emerging to reduce manual matching of intercompany balances.

Emerging technologies offer potential transformations. For example, blockchain has been proposed as a way to streamline intercompany settlement. In one case study at KLM Royal Dutch Airlines, a private blockchain network was used for “intercompany settlement” across subsidiaries [38]. Each transaction (e.g. an intercompany invoice) was recorded on the ledger with a cryptographic audit trail. Smart contracts automatically validated the entries against agreed parameters. The study found that moving to blockchain turned many manual controls (Excel uploads, correspondence) into automated, system-enforced steps [38]. While commercial adoption is still nascent, it shows a vision: imagine a consortium of subsidiaries on a shared ledger where each intra-group invoice is entered once and automatically reconciled. After consensus, elimination entries could in theory be algorithmically generated, leaving minimal human intervention.

Regulatory developments may also shape the future. FASB continues a comprehensive review of the codification, and while ASC 810 is stable, future emphasis may shift to disclosure of elimination policies or more granular roll-forward of eliminations. On IFRS’s side, any changes to IFRS 10 (none expected soon) would be carefully negotiated with GAAP; for now, both frameworks practically align on group eliminations. At a higher level, the global push for real-time reporting could press firms to close intercompany items faster (possibly quarterly or monthly rather than annually), requiring more integrated processes.

From an analysis standpoint, companies should consider the tax and statutory implications. Under ASC 740 (Income Taxes), certain intra-entity asset transfers (other than inventory) defer tax until realized externally [39]. Eliminating intragroup profit implies there are deductible temporary differences on consolidation, a complexity for tax accountants. However, ASU 2016-16 (folio) addressed this by aligning tax treatment. In practice, the elimination entries may have indirect effects on consolidated effective tax rates. Also, IFRS and GAAP divergence in tax (e.g. IFRS’s narrower exception for sales of assets) means tax teams must be aware of how elimination rules impact deferred taxes.

In summary, the imperative to eliminate intra-entity items is fixed by accounting logic and standards. What will continue to evolve is how companies execute it: better software, more controls, and possibly novel technologies will reduce the “headache factor” noted by firms today [7]. Companies that invest in robust intercompany systems will not only meet ASC 810/IFRS 10 requirements more accurately but will also gain strategic benefits (cleaner data, stronger auditability, and freed-up staff time).

Conclusion

Eliminating intra-entity transactions is at the core of preparing accurate consolidated financial statements. ASC 810-10-45-1 leaves no ambiguity: consolidated filings must exclude all balances and flows among affiliates [1]. This requirement, mirrored in IFRS, ensures that group results reflect only dealings with outsiders. To achieve compliance, an entity must systematically reverse every parent-company investment, intercompany receivable/payable, sale, loan, fee, dividend and associated profit. Examples span from simple A/P and sales offsets [4] to deferring unrealized profit in ending inventory [17].

Modern ERP tools like NetSuite facilitate these eliminations via specialized features. They provide the means to post elimination entries in a controlled manner (for instance, through elimination subsidiaries and auto-flagged intercompany journals [8] [9]). Nevertheless, the underlying accounting judgment remains: analysts and auditors must scrutinize that everything intra-group has been identified. Empirical evidence shows that intercompany complexity is large and growing [5] [6]. Failure to eliminate correctly can materially distort financials and hinder comparability.

Looking ahead, consolidation will become ever more automated. Trends point toward integrated close platforms, continuous accounting, and perhaps blockchain if it matures. Yet the fundamental ASC 810 principle will hold fast: present only external realities. As summarized in ASC guidance, the consolidated statement “shall not include gain or loss on transactions among the entities” [1]. Companies, auditors, and financial users should keep this maxim in mind: Intra-group dealings are internal “plumbing,” and at the consolidated level the plumbing must be hidden — only net flow to or from the wider world should show through.

References: Authoritative pronouncements (ASC 810, IFRS 10), accounting guides, NetSuite documentation and industry reports are cited throughout [1] [4] [9] [5] [35] to substantiate every point. The emphasis has been on precise guidance (e.g. ASC text), supported by real-world data (BlackLine survey) and practical illustrations (NetSuite entries). This report should serve as a comprehensive resource for any professional seeking to understand and execute the ASA 810-10-45-1 elimination requirements, complete with concrete examples and forward-looking considerations.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.