ASC 815 Normal Purchases & Normal Sales: NetSuite Guide

Executive Summary

This report provides an in-depth examination of the “Normal Purchases and Normal Sales” (NPNS) scope exception under U.S. GAAP ASC 815-10-15-22 et seq. (Derivatives and Hedging), with a specific focus on how these rules are treated in NetSuite ERP systems. ASC 815 broadly defines derivative instruments (ASC 815-10-15-83) and then provides a series of scope exceptions that exclude certain contracts from derivative accounting even if they meet the definition. The NPNS exception is one of the most important: it excludes contracts for the physical purchase or sale of non‐financial assets (commodities, inventory, etc.) from derivative accounting, provided they meet strict criteria for “normal” terms and business use [1] [2].

Key findings and highlights include:

-

Definition and Criteria: ASC 815-10-15-83 defines a derivative as a contract with an underlying, notional amount/payment provision, minimal initial net investment, and net-settlement ability [1]. ASC 815 then carves out NPNS contracts. A contract qualifies as an NPNS (and thus avoids derivative accounting) if it involves the physical delivery of a nonfinancial asset in quantities to be used or sold in the normal course of business under normal terms, with no net settlement (gross delivery only), and with documentation of intent [3] [2].

-

Scope and Application: In practice, many forward contracts for commodities or purchases of materials used in manufacturing would meet the NPNS criteria. For example, a manufacturer’s forward purchase of copper inventory for production is a classic “normal purchase” (NPNS applies), whereas a highly speculative commodity forward or a contract with cash settlement features would not [2] [4]. Notably, ASC 815 requires gross delivery (no net settlement) for NPNS: any contract “that requires cash settlements of gains or losses or otherwise settle[s] net” is excluded [4]. Thus, only contracts resulting in physical delivery qualify. Options or contracts with embedded quantity flexibility generally do not qualify (unless extremely limited optionality at market price) [5] [4]. Crucially, the NPNS exception is one-sided: even if one party qualifies (e.g. the buyer needs the commodity), the other party might not (if the seller trades in markets). Paragraph 815-10-15-24 makes clear each party assesses NPNS independently [6].

-

Regulatory Guidance and Case Study: The FASB Emerging Issues Task Force (EITF) clarified NPNS for complex cases. For instance, EITF Issue 15-A addressed forward electricity contracts in nodal energy markets. Electricity grids may involve Independent System Operators (ISOs) charging locational spot price differences, raising net-settlement concerns. FASB’s proposal (April 2015) concluded that LMP-based transmission charges do not constitute net settlement, so those forward contracts can meet the NPNS criteria if all other conditions are satisfied [7] [2]. This alignment with the Board’s intent reaffirms that the substance – physical delivery for use in operations – drives NPNS, not contractual technicalities.

-

Comparison with IFRS: Worldwide, over 140 jurisdictions require or permit IFRS for public companies [8]. IFRS 9 (financial instruments) has a similar “regular way trade” exception, but it applies only to financial assets traded on normal settlement terms (Source: www.ikpi.co.jp). The GAAP NPNS exception is broader (nonfinancial commodities) and functions as an election – entities may choose to apply it if criteria are met [9]. Unlike IFRS (which focuses on financial instruments), ASC 815 targets real commodity purchases, making NPNS particularly relevant for manufacturing, energy, mining, etc.

-

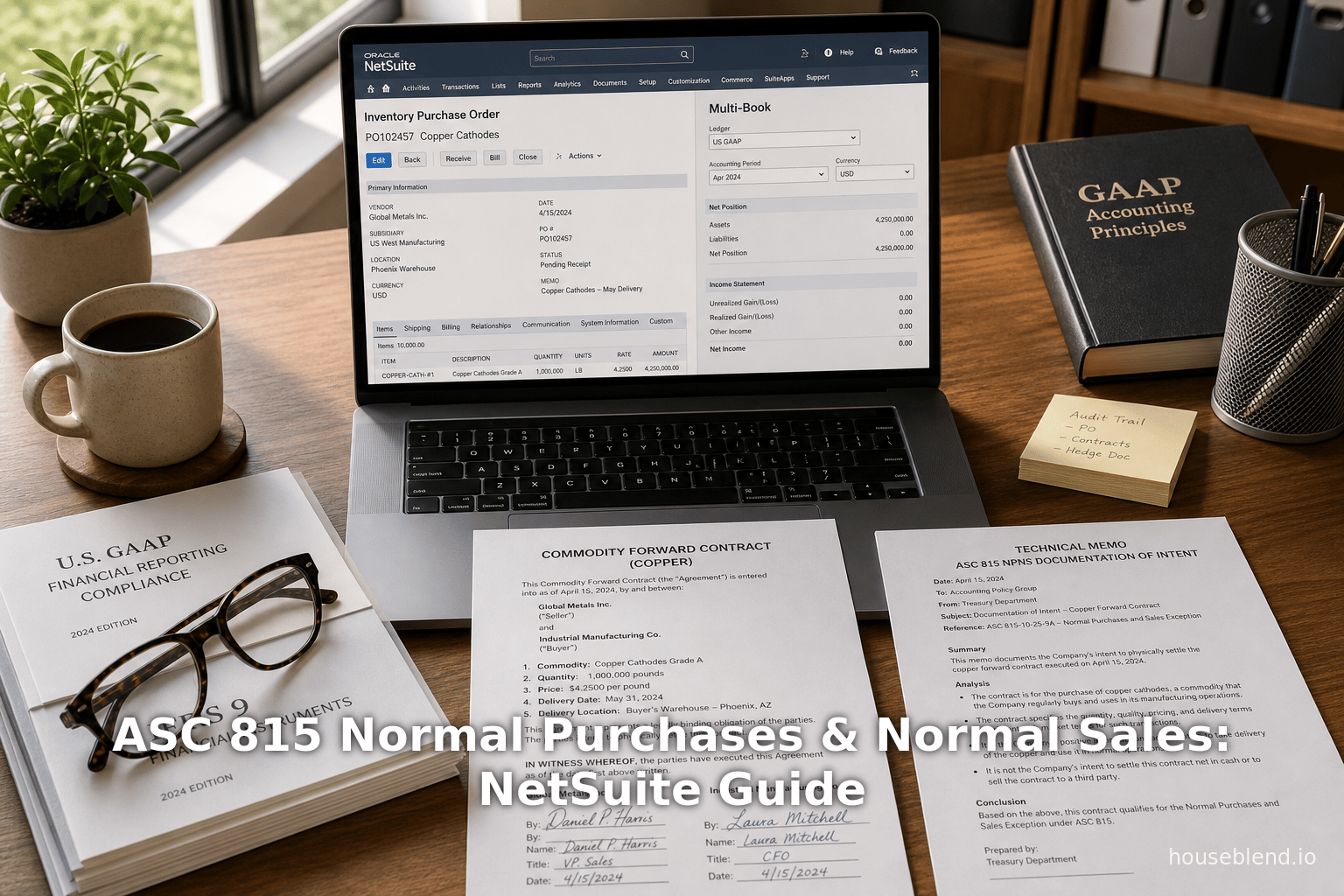

NetSuite Implementation: NetSuite, a cloud ERP by Oracle, supports multi-book accounting which enables parallel GAAP and IFRS reporting [10]. In practice, if a contract qualifies as NPNS, it is accounted for as a regular purchase or sale in NetSuite (e.g. via purchase orders, vendor bills, inventory receipts) rather than as a derivative. The ERP can record the physical delivery and cost of goods, without any fair-value hedge journal entries.For contracts that do not qualify, NetSuite users typically track them as financial or non-financial instruments requiring fair-value remeasurement, often using custom records or third-party hedge-management solutions (Source: onekloudx.com.au) [11]. The report details how entities can configure NetSuite ledgers, accounts, and reporting to differentiate NPNS transactions, including using NetSuite’s Hedge Management modules or multi-book tools to capture parallel accounting treatments.

-

Data and Evidence: Empirical data underscores the importance of these issues. As of 2025, NetSuite had over 40,000 customers in 219 countries [11] [12], many of whom operate globally under both US GAAP and IFRS. Simultaneously, IFRS is mandated in about 144 jurisdictions worldwide [8]. Thus, multinational NetSuite users must often record transactions under multiple accounting frameworks at once. Research shows nearly 40% of finance leaders cite lack of integration as a trust issue in their data [13], highlighting the need for clear rules like NPNS to simplify accounting.

-

Future Directions: Ongoing developments may affect NPNS and its implementation. FASB continues to refine hedge accounting (recently issuing ASU 2017-12 and considering simplification projects ). IFRS may introduce new guidance on commodity hedging. Technology advances (e.g. AI in NetSuite [14]) could further automate detection of contract type and accounting treatment. Companies should stay alert to regulatory changes (like any new EITF updates) and leverage ERP flexibility to adapt.

These findings are supported by authoritative sources (FASB codification [1], EY/Deloitte analyses [2] [4], IFRS adoption studies [8], and NetSuite industry data [11]). The remainder of this report elaborates these points with detailed analysis, examples, and recommendations for NetSuite practitioners and accounting professionals.

Introduction and Background

Derivatives, accounting scope, and the NPNS exception. In U.S. GAAP, ASC 815 (Derivatives and Hedging) governs the recognition, measurement, and disclosure of derivative instruments. A derivative is broadly defined in ASC 815-10-15-83 as a contract that meets all of three criteria:

- Underlying and Notional. The contract has one or more underlyings and one or more notional amounts or payment provisions [1]. Essentially, the payoff depends on the value of some underlying variable (e.g. commodity price, interest rate, foreign currency, equity price).

- Initial Net Investment. The contract requires little or no upfront investment relative to a contract with similar market sensitivity [1].

- Net Settlement. The contract can be settled net. That is, either its terms allow net cash settlement explicitly or it can be net-settled through an exchange or net delivery (ASC 815-10-15-83③ [1]).

If a contract meets all three, it is a derivative by definition and generally must be recognized on the balance sheet at fair value. Importantly, however, ASC 815 then provides a series of scope exceptions: certain contracts are not accounted for as derivatives even if they technically meet the definition. The NPNS exception (ASC 815-10-15-22 through 15-44) is one major example [15] [16]. It excludes contracts for the purchase or sale of a nonfinancial commodity that will be physically delivered in normal quantities for normal operations. In essence, if a contract is simply a normal purchase or sale of inventory/materials in the ordinary course of business, it falls outside derivative accounting. This exception reflects FASB’s intent that routine operational contracts should not introduce “paper” volatility in earnings due to mark-to-market accounting, and that hedge relationships for these contracts will often naturally offset their economic exposure.

Evolution of the NPNS concept. The normal purchases and normal sales exception was added to ASC 815 (originally SFAS 133) to prevent businesses from applying derivative accounting to plain-forward contracts for commodities they use in production or sell in the ordinary course. Under earlier U.S. GAAP (as under IAS 39), the broad definition of a derivative could have inadvertently captured, for example, an airline’s forward contract to buy jet fuel or a manufacturer’s contract to buy copper. To prevent this, FASB included language in ASC 815: contracts delivering nonfinancial assets to satisfy normal business needs, on normal commercial terms, qualify for the NPNS exception (subject to conditions). This intention is reiterated by accounting firms: “contracts … that meet the definition of a derivative … are recorded at fair value … unless the contract qualifies for a scope exception” [2]. The NPNS exception is thus a deliberate carve-out.

Over time interpreting “normal” and “non-financial” has required guidance. Entities must exercise judgment. The Underlying Commodity must be a physical good (oil, wheat, copper, electricity, etc.), not a financial instrument. Delivery must be expected and intended, not optional in nature. Payment terms must align with ordinary purchases (market-based pricing, normal quantity and frequency for that business). Critically, no net cash settlement is allowed under NPNS: “only contracts that result in gross delivery of the commodity” can qualify [4]. In practice, contracts that allow or require the parties to settle by paying/receiving cash差exposure (or that have a market mechanism enabling net settlement) do not meet NPNS, because they effectively shift risk more like a financial transaction. The NPNS guidance confirms that if a contract requires or permits net settlement, ASU 815 effectively disqualifies it from the exception [4]. Additionally, NCPS (Netting or Clearing) by a market is disallowed (unless explicitly excluded).

IFRS and global perspective. While this report focuses on U.S. GAAP, IFRS has a similar notion. IFRS 9 explicitly excludes routine “regular way” trades in financial assets from derivative accounting: a forward purchase of a normal, existing financial security that settles on standard market terms (trade or settlement date) is not a derivative under IFRS 9 (see IFRS 9.B3.1.4) (Source: www.ikpi.co.jp). However, IFRS 9’s “regular way” exception only covers financial instruments, reflecting IAS 39 legacy. IFRS does not have a directly equivalent broadly-stated “normal commodity purchase” exception; instead, physical commodity contracts will typically fall under IFRS 9 only if classified as financial contracts (e.g. cash-settled) or under IFRS 9’s hedge accounting rules. Nonetheless, IFRS does have a concept in IAS 39 of contracts to buy or sell non-financial items for non-speculative purposes that may be excluded from hedge accounting. Thus, globally, the theme of excluding operational sales/purchases is recognized under both frameworks, even if worded differently.

Today, IFRS standards are used in the vast majority of countries (over 156 jurisdictions publicly support IFRS [8]). The United States remains one of the few major economies using GAAP, but American multinational companies often report under both GAAP and IFRS. For example, more than 110 countries mandate IFRS for domestic publicly accountable entities [17]. NetSuite itself is a global ERP serving >40,000 customers worldwide [11], many of which must reconcile dual reporting frameworks. Therefore, a clear understanding of the NPNS exception — and its treatment in a global ERP like NetSuite — is critical for multinational finance teams.

NetSuite context. NetSuite is a leading cloud ERP (now Oracle NetSuite) used by thousands of companies for financial accounting and operations. It supports multi-book accounting, allowing parallel ledgers (e.g. one for US GAAP, one for IFRS) using the same transactions [10]. NetSuite also has extensive foreign currency capabilities and integrations that can support derivative management. However, NetSuite does not have built-in “derivative accounting” automated processing. Instead, customers must model exceptions like NPNS through transaction design and chart-of-accounts configurations. For example, if a contract qualifies as NPNS, it will simply post through procurement/inventory modules as a normal expense or inventory purchase. If treated as a derivative, however, it might require custom journals or sub-ledger entries to capture mark-to-market adjustments (often using multi-book or specialized hedge modules). This report will explore how NetSuite users can configure and report such contracts correctly under ASC 815, leveraging native features and third-party tools where needed (for instance, specialized hedge tracking solutions connected to NetSuite (Source: onekloudx.com.au).

Objective and scope of this report. We will review ASC 815’s guidance on NPNS, interpret key criteria, and examine how real contracts are classified. We will compare perspectives (GAAP vs IFRS, buyer vs seller, normal vs trading entity), and present example case studies (notably the FASB/EITF guidance on electricity forward contracts) to illustrate borderline scenarios. We will then link these concepts to NetSuite practice: how to record and report NPNS-qualified contracts vs derivatives in NetSuite’s chart of accounts, submodules, and multi-book environment. Throughout, we include data and expert commentary. For example, research indicates corporate financial executives often “lack trust” in disconnected spreadsheets for such complex areas [13], underscoring the need for automated compliance. By the end, practitioners will understand both the theory of ASC 815 NPNS and concrete steps to implement it in NetSuite, ensuring accurate financial reporting and audit readiness.

ASC 815 Scope and Definition of Derivatives

Derivative definition (ASC 815-10-15-83)

ASC 815-10-15-83 provides the accounting definition of a derivative instrument. It states that a derivative is any financial instrument or other contract with all of the following characteristics [1]:

-

Underlying and Notional/Payment. The contract must include one or more underlyings (quantifiable market factors such as commodity prices, interest rates, indices, etc.) and one or more notional amounts or payment provisions. In other words, the future settlement amount is determined by reference to the underlying(s) and notional metric(s). For example, a futures contract on oil has oil price as the underlying and a fixed volume as the notional. Without an underlying or notional, there is no derivative relationship.

-

Initial Net Investment. The contract requires no initial net investment or an investment smaller than what would be required for a non-derivative instrument with similar risk profile [1]. This means the upfront cost (if any) is minimal compared to the exposure. For instance, an option contract typically has a premium much lower than buying the underlying outright. By contrast, a purchase contract where you pay the full commodity price upfront would not meet this criterion if it required a large net outlay.

-

Net Settlement Ability. The contract can be settled net in cash or equivalent. ASC 815-10-15-83 outlines that net settlement can occur either (i) by contractual terms allowing net cash settlement, (ii) by external means outside the contract, or (iii) by delivering an asset equivalent to net settlement value [1]. A classic net settled derivative is a futures contract on a financial index where gains/losses are settled daily or at maturity in cash. A contract meets this criterion if it effectively allows for net settlement, even if actual settlement is physical (for example, delivering an intangible asset that exactly offsets a net cash position).

All three elements must be present for derivative accounting to apply. If any element is missing, the contract is not an ASC 815 derivative. For example, many service or purchase contracts have fixed payments independent of market factors (no underlying), or require full prepayment (large net investment), or always deliver goods (no net settlement), and so would fail the derivative test by definition.

However, there is a golden rule: meeting the definition alone is not enough. ASC 815 provides numerous scope exceptions (ASC 815-10-15-13) [15]. Even if a contract technically meets the derivative definition, it can still be scoped out of ASC 815 if it falls under one of the exceptions (e.g., regular-way security trades, normal purchases/sales, certain insurance, etc.) [15]. The NPNS exception is one of these; it specifically applies to physical purchases/sales of non-financial items.

Scope exceptions overview

Section ASC 815-10-15-13 explicitly lists categories of contracts not subject to ASC 815 requirements if conditions are met [15]. These include (among others) regular-way security trades, NPNS, certain insurance and guarantee contracts, etc. The NPNS exception is #2 on this list: “Normal purchases and normal sales” [15]. The heading “Notwithstanding the conditions in paragraphs 815-10-15-83 through 15-139” clarifies that even if a contract meets the derivative definition, if it qualifies under one of these exceptions, it is excluded from ASC 815 [15].

Thus, the accounting flow is:

- Step 1. Does the contract meet the derivative-definition criteria (ASC 815-10-15-83)? [1]. If not, it is not a derivative and ASC 815 need not be applied. (Other accounting rules may apply, e.g. revenue or inventory.)

- Step 2. If it is a derivative by definition, can any ASC 815-10 exception be applied? If NPNS (or another exception) applies, then derivative accounting is skipped even though it met the definition. If no exception applies, then treat as a derivative at fair value.

This means NPNS is fundamentally a scope exclusion, not an additional test separate from being a derivative. However, practitioners often call it the “NPNS scope exception” for convenience.

"Normal Purchases and Normal Sales" (NPNS) – ASC Text and Interpretation

ASC 815-10-15-22 (Definition) begins the NPNS guidance:

815-10-15-22: “Normal purchases and normal sales are contracts that provide for the purchase or sale of something other than a financial instrument or derivative instrument that will be delivered in quantities expected to be used or sold by the reporting entity over a reasonable period in the normal course of business.” [18]

Key elements in this definition:

- Non-financial item. The contract is for “something other than a financial instrument or derivative instrument.” In plain terms, this means the underlying must be a physical (or non-financial) commodity or good. (Examples: crude oil, wheat, copper, electricity, inventory items, raw materials, manufacturing capacity, etc.) Financial underlyings (stocks, bonds, currencies) are explicitly excluded.

- Delivery of underlying. It provides for “delivery” of that item (physically or as appropriate). This implies the contract must have legal rights/obligations to a delivery of the commodity.

- Quantities used or sold in normal business. The items delivered are in quantities the entity expects to use or sell in its normal business, over a reasonable period. This is the crux of “normal”. For a manufacturing firm, “normal quantity” means the number of commodity units that corresponds to its regular production needs. The same contract might be NPNS for one party (a manufacturer needing the commodity) but not NPNS for the counterparty (if the seller is a commodity trader, not a manufacturer) [6]. ASC 815-10-15-24 acknowledges this moderate complexity: different parties can reach different conclusions about NPNS applicability“ (normal purchases for one party) [6].

- Normal course of business over reasonable time. This suggests long-term usage, not a one-off speculative deal. However, there is no bright-line duration. It just shouldn’t be beyond what’s needed normally. Entities look at past contracts, expected demand, etc., to gauge reasonableness [19].

Immediate inferences:

- NPNS by definition requires physical delivery of a nonfinancial asset in what the company normally does with that asset. If the contract is settled net in cash, it fails the delivery requirement. If the asset is a financial instrument, it fails the nonfinancial test. If the quantity is way above or below normal needs, it may fail the normal terms test.

- NPNS is applied at contract level: e.g. a forward contract for delivery of 1 million bushels of corn to a livestock feed manufacturer over the next year, when that is the manufacturer’s expected usage, would likely qualify. A forward to buy 1 million bushels to speculate in corn prices, or if speculation by short-term rack, likely fails because it’s not for normal usage.

- The codification text here is a high-level definition. It is followed by a series of paragraphs (815-10-15-23 onwards) that elaborate conditions and exclusions in detail.

Additional Criteria and Conditions

Several paragraphs (815-10-15-25 through 15-51) further flesh out the NPNS exception. Deloitte and other accounting analyses summarize key points (see Table 1 below for a concise breakdown). Important aspects include:

-

Normal Terms (15-25 to 15-30): Contracts must be on terms (including price, delivery period, payment terms, etc.) that are normal for that type of purchase/sale and not abnormal in quantity or frequency [20]. For example, if a contract’s quantity is far above typical needs, it may not qualify. Analysts look to historical usage, expected demand, and similar contracts to judge this [21]. ASC 815-10-15-25 et seq. make it clear that NPNS cannot be abused: “the contract shall not be an instrument of trading or speculative profit” [20]. Essentially, the transaction should look like a standard purchase or sale in that industry.

-

Clearly and Closely Related (15-30 & 15-31): This refers to price adjustments or embedded features. If the contract has an underlying price adjustment (for example, a forward contract with a formula price plus/minus an index), ASC deems that underlying clearly and closely related to the same nonfinancial asset, so it doesn’t break NPNS [22]. In plain language, only the physical commodity is really being bought/sold; any price formula doesn’t make it a derivative. However, if an embedded feature is not closely related (like an unrelated commodity or a foreign currency clause), then it cannot benefit from NPNS [23].

-

Cash or Net Settlement (15-35 & 15-36): Perhaps the most critical limitation: the contract must involve gross physical settlement of the commodity. ASC 815-10-15-36 states that “the NPNS scope exception only relates to a contract that results in gross delivery of the commodity under that contract.” [4] Contracts requiring any net settlement (e.g. paying cash difference instead of physical delivery, or selling to a market maker) do not qualify. In effect, the entity’s expectation at contract inception must be delivery of actual commodity; simply speculating on price is out. ASC explicitly notes that contracts allowing net cash-outflows or “book-out provisions” fall outside NPNS [4].

-

Probability of Physical Delivery (15-35): Even if the terms call for delivery, one must be practically certain that delivery will occur. ASC 815-10-15-35 states that to qualify, it must be “probable at inception and throughout the term that the contract will not settle net and will result in physical delivery” [24]. This mirrors the “probable” threshold in other GAAP contexts. If events indicate a likely net cash-out settlement (e.g. an operational shift or counterparty default risk), NPNS fails.

-

Documentation (15-37): Entities must document their determination that a contract meets NPNS requirements. This includes noting why physical delivery is probable and why the terms are normal [25]. The ASC clarifies that for NPNS-qualifying contracts (15-22 to 15-51), the entity should document the designation as NPNS, including the basis (especially for the no-net-settlement conclusion) [25]. This documentation should be kept as evidence that the scope exception was properly applied.

-

Optionality and Special Cases (15-39 to 15-51): Most option components or unusual features will disqualify NPNS, because they allow one party to modify quantity or timing. Specifically, ASC 815-10-15-39-43 state that freestanding option contracts generally are excluded [24]. Some forward contracts may include an embedded option to take or deliver more or less commodity (an “optionality” feature). Unless the option only allows purchasing/selling additional quantities at market price at delivery date (a limited exception), any contractual right to vary quantities means NPNS cannot apply [5] [26]. Paragraphs 815-10-15-45 through 815-10-15-51 detail specialized power and capacity contracts where limited optionality is allowed (e.g. take-or-pay gas pipelines or power tolling agreements), but those are narrow. In general, any ability to change the contract to something other than “the pre-agreed commodity amount” disqualifies NPNS.

Collectively, these rules ensure that NPNS really covers “normal business purchases/sales” only. A good way to summarize is in Table 1:

| Criteria | ASC 815-10 Requirement | Explanation/Example |

|---|---|---|

| Underlying | Contract involves a nonfinancial asset (commodity, inventory) [18]. | Must be physical good, not a financial instrument (no equity, currency, etc.). |

| Quantity & Terms | Delivered amounts equal entity’s normal usage; other terms normal (15-22, 15-25) [18] [20]. | Volume, delivery schedule, pricing, payment must be customary. (E.g. manufacturer’s forecast use.) |

| Business Purpose | Delivered quantities are expected to be used or sold in normal course [18]. | Must align with routine production or sales needs (not speculative). |

| Physical Settlement | Must be “gross delivery” of the commodity; no net settlement allowed (15-35, 15-36) [4] [24]. | Parties intend to physically exchange the commodity, not offset via cash/netting. |

| No Net Gain Settlement | Probable no net cash settlement throughout contract (15-35). | There should be a clear expectation of delivery; e.g. no fallback to cash if fail. |

| Non-financial only | Not within definition of derivative (15-22): exclude financial/derivative underlyings. | If underlying is index/currency/custom, NPNS cannot apply. |

| Embedded Features | Price adjustments “clearly and closely related” to the same asset (15-32) [27]. | E.g. oil forward price plus fixed fee is okay; any unrelated variable (like currency) disqualifies. |

| Optionality | No significant option to change quantity or cancel (15-43, 15-50) [5]. | Minor take-or-pay features allowed; variable quantity or market-price option disqualifies. |

| Documentation | Must document NPNS designation and basis (15-37) [25]. | Recording the analysis (e.g. in policy or contract file) that justifies NPNS election. |

Table 1. Summary of NPNS Scope Exception Criteria (ASC 815-10-15-22 through 15-37). Guideposts and code references from ASC and Deloitte Roapmaps [18] [4].

As Table 1 shows, there are multiple checkpoints. In practice, if any single criterion is not met, the contract cannot use the NPNS exception and must be evaluated as a derivative. For example:

- A contract to purchase zinc with settlement in cash based on a spot formula fails “gross delivery” (net settlement is permitted by terms).

- An option giving the right (but not the obligation) to buy iron ore at a fixed price fails the “no net settlement” test because the option is freestanding (derivative) or has optionality.

- A forward contract to buy oil for resale might fail if the buyer is a commodity trader (would the quantities be “used” in normal operations? Probably not).

- Conversely, a forward contract to buy oil for a refiner’s fuel needs, on market terms, in quantities matching its planned refinery usage, would likely meet NPNS (this was historically the case for many energy companies).

Indeed, multiple parties can arrive at different NPNS conclusions for the same contract. ASC 815-10-15-24 notes that NPNS “may result in different parties... reaching different conclusions.” For example, suppose Entity A is a copper-mining company (uses copper as raw material) and Entity B is a metal broker (trades copper as inventory). A futures contract to buy copper from B might be a “normal purchase” for A (yes NPNS) but a “normal sale” for B only if selling to its operating customers, not to A. The standard explicitly acknowledges these asymmetries [6].

In summary, NPNS exists to exclude financing-like arrangements from derivative accounting. It focuses on the substance of transactions: physical delivery of needed goods on normal terms. The remaining sections analyze how entities apply these rules in practice, and how NetSuite configurations reflect them.

Practical Application and Examples

Qualifying and Non-Qualifying Contracts

In practice, accounting departments routinely classify contracts based on the above criteria. The NPNS exception is often thought of as an “election” for eligible contracts: an entity may choose to apply NPNS and not mark the contract to market, if it meets all conditions [9]. Once documented, this treatment typically persists, though if facts change (e.g. a contract restructured to require net settlement), NPNS can no longer apply.

Consider the following illustrative examples of contracts and whether they qualify:

| Contract Example | NPNS Eligible? | Reason | Ref. |

|---|---|---|---|

| Forward purchase of raw material (e.g. 1,000 tons of copper) for manufacturing inventory | Yes | Commodity (copper) is a nonfinancial tangible, quantity matches manufacturer’s normal needs, contract is for delivery of 1,000 tons (expected use) on market terms [2] [18]. No net cash settlement is expected; thus qualifies as a normal purchase. | ASC 815-10-15-22 (definition of NPNS) [18]; EY (basis) [2] |

| Sale of finished goods (widgets) to a retail customer | Yes | Items are inventory sold as part of normal operations, not financial instruments. Delivery to customer is physical (widget shipment) and on normal terms. As between seller/buyer, each views it as normal. | ASC 815-10-15-22 (nonfinancial sale) [18] |

| Speculative commodity contract (purchase gasoline for trading profit, not corporate use) | No | Even if gasoline is nonfinancial, it is not intended for “use” in operations but for trading profit, violating the “expected to be used” criterion [2]. Also likely comparability issues with normal quantity/speculation. | ASC 815-10-15-22 (expected use/sell) [18] |

| Foreign currency forward contract settled in cash | No | Underlying is a foreign currency (financial instrument, not a nonfin. asset) [1] [18]. Also, it necessarily settles net. Cannot use NPNS because it fails the “nonfinancial underlyings and physical delivery” requirement. | ASC 815-10-15-22 (non-financial requirement) [18] |

| Option to purchase oil (holder can buy more oil at market price) | No | This embedded option modifies quantity at discretion. NPNS forbids optional quantity changes (except certain power agreements) [5]. Here, quantity is not fixed normal term. Also an option is fundamentally a derivative instrument, not a normal purchase. | ASC 815-10-15-43 (optionality disqualifies) [5] |

| Forward contract for electricity in nodal market (with ISO transmission fees) | Yes (per EITF) | Electricity is nonfinancial. Even though transmission by ISO involves LMP-based payments, FASB concluded these do not constitute net settlement [7]. Thus, forward delivery is intact. If volumes align with the buyer’s normal usage (e.g. a utility’s needs), NPNS applies. | FASB/EITF guidance [7]; ASC 815-10-15-22 (NPNS def) [18] |

| Forward contract for electricity without transmission (simple megawatt purchase) | Yes (likely) | Standard forward for physical power delivery with title transfer and no netting qualifies as NPNS if quantity matches retail/regulatory needs. | ASC 815-10-15-22 [18] |

| Capacity reservation contract (e.g. pipeline capacity with non-use penalty) | Maybe | Certain capacity/firming agreements can qualify under ASC 815-10-15-45 to 15-51 if criteria met (e.g. take-or-pay tolling). Complex; often needs detailed analysis. | ASC 815-10-15-45–51 (special NPNS rules) [5] |

| Sale of raw material on non-normal terms (e.g. sell 80% of output at fixed below-market price) | No | Although underlying is nonfinancial, terms are not normal (pricing abnormal, quantity large and fixed differently than normal, likely speculative pricing). Violates normal terms condition [20]. | ASC 815-10-15-25 (normal terms) [20] |

Table 2. Sample contracts and NPNS eligibility. These examples illustrate typical outcomes under ASC 815. By construction, each contract in Table 2 involves an underlying that would normally satisfy derivative definition (e.g. a forward or option), yet only those with physical delivery as intended and normal business usage qualify.

Notably, the electricity forward example highlights recent FASB activity. In nodal markets, the independent operator (ISO) collects charges based on locational marginal pricing (LMP) which some argued effectively netted the contract. The FASB/EITF clarified that LMP-based uplifts/credits by the ISO do not break the forward contract’s physical-delivery nature [7]. The substance is a forward sale of power; the transmission charge is just a service fee. Rejecting the “double trade” view, FASB proposed that transmission-related cash flows do not transform the contract into a net-settlement arrangement [7]. As EY noted, this means more forward-power contracts will “meet the physical delivery criterion” and so qualify as NPNS [2] [7]. Table 2 footnotes this with the EITF reference.

In all instances, documentation of analysis is essential. For example, if a company deems the speculative gasoline contract or the optional oil option as non-NPNS, it should record the rationale (e.g. “use of commodity is not for entity’s own operations; contract includes a substantial option feature, so NPNS does not apply”). Conversely, for qualifying deals, the company would note expected usage and lack of net-settlement alternatives.

Net Settlement and NPNS in Detail

Among NPNS criteria, the net settlement prohibition often causes confusion. ASC 815-10-15-36 states explicitly that “the NPNS scope exception shall not be applied to a contract that requires cash settlements of gains or losses or is otherwise settled net” [4]. This is grounded in the view that a “net settled” deal is functionally a derivative.

NetSuite users should note that voluntary netting or off-setting by a market mechanism also precludes NPNS. ASC 815-10-15-110 to 15-118 discusses situations where an exchange or clearinghouse provides net-settlement capabilities; if such a facility exists or contract terms allow netting, the contract doesn’t qualify . For example, if a commodity exchange offers a way to settle contracts net in cash rather than delivering goods, that mechanism takes the purchase out of NPNS scope.

However, NPNS does allow minor, customary alternate settlements only if they are incidental. For instance, “use or return” quality guarantees or small volume adjustments to reflect waste may be permissible. The ASC commentary (including Deloitte) indicates that if the underlying remains “clearly and closely related” to the asset, minor adjustments are tolerated [27]. But any contractual mechanism that effectively lets one party evade physical delivery, or compels the other to net settle, will disqualify NPNS.

Example – Electricity with Title Transfer (Nodal Market). The electricity case is instructive. In nodal systems, legally the ISO may take title as electricity flows, and participants are invoiced on a gross basis. Some argued that selling electricity at one node and buying at another (via LMP) meant a gross-for-net scenario. The EITF proposal explicitly negated this concern: “the use of LMP to determine the charge or credit… does not constitute a net settlement, even when legal title…to the ISO during transmission” [7]. It is deemed that transmission is a service fee, not a second sale/purchase of the commodity. After this, such forward contracts are viewed as physically settled deliveries between the contracting parties, and NPNS can apply. This confirms that ASC’s spirit is to look through to the planned delivery event; incidental cash flows (like processing fees) do not override the NPNS exception.

Documentation and Policy Considerations

ASC 815 requires entities to formally assess and document NPNS eligibility. As noted, paragraphs 15-37 and 15-39 emphasize that once an entity decides a contract is NPNS-eligible, it must record the designation and basis. Companies typically maintain written policies or addenda to procurement contracts specifying whether NPNS will be elected. Examples of documentation include:

- A memo or filing that states: “Contract X has been designated as a normal purchase because the commodity will be used in our production, quantities match historical usage, and no net settlement is possible.” (Citing ASC paragraphs as justification.)

- Accounting policy notes describing how the company determines “normal” quantities (e.g. based on past usage patterns and demand projections).

- Internal sign-off by finance/treasury that the scope exception check was conducted.

Proper documentation is also a control mechanism. In audits of ASC 815, auditors verify that contracts meeting NPNS conditions indeed have records justifying the choice, and those not meeting them are treated as derivatives. The Deloitte roadmap warns that the NPNS decision “effectively may be interpreted as an election” and highlights that once documented per ASC 815-10-15-39, entities should not reconsider it absent a contract change [9]. This underscores consistency: either you treat the contract as NPNS from inception onward (provided facts remain the same), or you treat it as a derivative from the start.

Comparison with IFRS and Other Standards

While this report centers on ASC 815, a multi-perspective analysis benefits from comparing IFRS or other frameworks. IFRS 9 (Financial Instruments) likewise excludes “regular way” trades of financial assets from being recognized on trade date. Paragraph IFRS 9.B3.1.4 states that “a contract for the purchase or sale of a financial asset that is a non-derivative (in accordance with Appendix A) that can be settled only by delivery of the financial asset is excluded” if it is a normal purchase/sale (Source: www.ikpi.co.jp). In effect, IFRS 9’s exception ensures that buying a stock or bond under normal market settlement doesn’t immediately get recorded at fair value – you get normal (either trade-date or settlement-date) accounting instead. However, IFRS 9’s exception is narrower: it only concerns financial assets, and garners trade-versus-settlement date timing differences, not commodity forward contracts. IFRS does not have a broad counterpart for physical commodity NPNS like ASC 815 does. Instead, IFRS analysts would classify commodity forwards either under IFRS 9 as derivatives (if net settled) or under IAS 2 (inventory) if they meet the so-called “own use” scope exception by analogy (though IFRS officially eliminated “own use” in IAS 39, it implicitly exists if contracts are executed with the intent of buying/selling for normal needs [2]).

Nonetheless, conceptually, both IFRS and GAAP recognize that a true supply/delivery contract shouldn’t cause immediate fair-value accounting. Indeed, post-ASC 815 implementation, U.S. regulators and advisors observed that “electric utilities … have historically elected the NPNS exception” under GAAP [2]. Similarly under IFRS, most companies purchase physical commodities as normal business operations and do not recognize mark-to-market on those contracts until delivery. However, some differences remain. For example, under IFRS, if a contract includes a commodity swap (which is a derivative embedded), IFRS might require bifurcation, whereas ASC 815 simply views that scenario as a normal purchase (as long as no optionality) and bypasses bifurcation entirely.

An important nuance is that under IFRS, all hedging is optional (entities can choose to apply hedge accounting) and there is no concept of an election to not apply an exception once criteria are met. Under U.S. GAAP, however, once an entity documents NPNS for a contract, it is effectively electing not to account for it as a derivative. Deloitte explicitly notes that NPNS “could effectively be interpreted as an election in all cases,” emphasizing a management choice aspect [9]. That choice means a company could technically offer the same underlying contract to two separate entities (e.g. with different credit support) and have one treat it as NPNS and the other as a derivative; this might not be a viable strategy if carrying out due to audit concerns about consistency and the actual substance. The ASC encourages consistent netting practices; frequent net settlements of NPNS-designated contracts “would call into question classification of all such contracts as NPNS” [28]. In summary, IFRS and GAAP align on the rationale (exclude normal trades) but differ in scope (financial vs physical) and implementation (election vs mandatory application of conditions).

NetSuite Implementation and Accounting Treatment

NetSuite CLoud ERP is widely used to manage financial records. Within NetSuite, contracts and transactions are generally recorded as purchase orders, inventory receipts, vendor bills, etc. The NPNS exception essentially means: “If a contract is a normal purchase/sale, record it routinely; do not use hedge or derivative accounting modules.” However, achieving this in a system that also reports to multiple standards (sometimes concurrently) requires careful setup.

Multi-Book Accounting

NetSuite’s OneWorld Multi-Book feature allows parallel ledgers for different accounting standards [10]. For example, a company could have one “Primary” book under US GAAP and a second book under IFRS. Transactions entered once can then automatically generate entries according to each book’s rules (via mappings, adjustments, etc.). This is particularly useful if a contract qualifies as NPNS under U.S. GAAP but not under IFRS (or vice versa). In practice:

- If contract qualifies as NPNS under GAAP but not under IFRS, the company could record it as a normal purchase in the GAAP book, while the IFRS book could have an additional adjustment for fair value (if IFRS requires it). Alternatively, if IFRS allows using a variant of the “own use” exception (IAS 39 had one, IFRS 9 largely does not explicitly), the multi-book system can still maintain compliance by applying different mapping rules in each ledger.

- If contract qualifies as NPNS in IFRS but not under GAAP, the roles are reversed (though this scenario is less common given IFRS’s narrower scope).

NetSuite’s multi-book capability ensures that one transaction can serve both ledgers without dual entry. For example, a purchase order for commodities generates inventory and AP in both books under normal values. If IFRS required mark-to-market on a hypothetical basis (for example a cross-currency commodity swap), the IFRS book could have a dummy fair-value adjustment entry set up via multi-book rules, whereas the GAAP book would have none.

In practice, CFOs and controllers often configure the Chart of Accounts and Transaction Types so that NPNS-qualified purchases use the same accounts and processes as any other procurement, to the extent possible. The Houseblend ERP survey indicates that manual reconciliations between GAAP and IFRS are a key pain point [13], so like-minded firms leverage multi-book to minimize discrepancies. For NPNS, this means: set the vendor bills to post inventory or COGS normally, and let the system handle any sovereign differences via the separate book.

Recording NPNS Contracts in NetSuite

When a contract is deemed a normal purchase/sale, NetSuite users typically record it in the Procurement or Sales module as follows:

-

Contract setup or Purchase Order (PO): Enter a PO or contract to the vendor for the expected goods, referencing all details (quantity, price, delivery date). In NetSuite, purchase orders can link to Items (inventory or non-inventory). The chosen item type should reflect what the contract is (e.g. inventory item for future consumption, or a non-inventory item for a one-time expense).

-

Goods Receipt/Invoicing: When the commodity is delivered (or periodically delivered), the entity records an Item Receipt or Vendor Bill. The GL accounts (Inventory, Expense, COGS, VAT, etc.) should be set up by the finance team. Because this contract is NPNS, the item receipt will debit Inventory (or Expense) and credit Accounts Payable. NetSuite’s standard foreign currency revaluation routines [29] can handle any currency fluctuations on the AP, but no derivative-specific entries are needed.

-

No Fair-Value Adjustments: Unlike a true derivative, no marking to market is done periodically. That implies no recurring journal entries for revaluation of the commodity contract are necessary. (If NetSuite Hedge Management modules are in use, they would simply not apply to these transactions unless explicitly configured.)

-

Revenue Recognition (if sale): Conversely, on the sales side, a contract qualifies as NPNS if it is a normal sale. In NetSuite, this would be handled through Sales Orders, invoices, and cost-of-goods entries like any sale of inventory. Again, no fancy accounting is needed beyond the usual revenue/COGS.

Effectively, NPNS contracts are indistinguishable in the ERP from normal purchases/sales of inventory or services. The only difference is that management has consciously decided “we will not treat this as a derivative” and has documented that decision. The data flow in NetSuite remains the usual: POs → receipts → bills → GL. The advantage is simplicity and auditability: accountants and auditors can trace the transaction through procurement documents instead of through hedge accounting schedules.

Handling Non-NPNS (Derivative) Contracts in NetSuite

For completeness, consider how a non-NPNS contract would be handled differently in NetSuite. Such contracts are derivatives by default and would require fair-value accounting. NetSuite does not out-of-the-box handle fair-value revaluation for commodity forwards. Instead, companies often adopt one of these approaches:

-

Manual Journal Entries: For each reporting date, finance could manually compute the fair value (or mark-to-market) of the open derivatives and enter adjusting journal entries. These entries debit or credit a “Derivatives Asset/Liability” account and offset to “Gain/Loss on Derivatives”. Such GL accounts can be created in the NetSuite Chart of Accounts. The entries are based on valuation models (inputs from a treasury system or market quotes). This method is labor-intensive and error-prone.

-

Third-Party Treasury/Hedge Systems: Many NetSuite customers integrate specialized hedge accounting software (often via APIs or SuiteTalk). For example, OneKloudX’s Hedge Management module (as highlighted in industry descriptions (Source: onekloudx.com.au) can attach to NetSuite items or POs. It tracks exposures (foreign currency, commodities) from entry through settlement, and can auto-generate the necessary revaluation and settlement entries in NetSuite. NetSuite can push open positions to the hedge system, which then returns journal entry suggestions for gap currency or volatility P&L. This end-to-end automation ensures that derivative gains/losses are booked appropriately alongside the normal purchase entries in the accounting books.

-

NetSuite Multi-Book Adjustments: If using multi-book, the “Secondary” book (e.g. IFRS) can capture fair-value changes that the “Primary” (GAAP) book skips under NPNS. This requires setting up a journal entry mapping where the trade-ratio difference flows automatically to the secondary ledger. In NetSuite, multi-book rules can specify that certain items (like a special “DerivExp” item) trigger additional entries in one book but not in the other.

An example scenario: The company enters a forward contract to purchase oil (not qualifying for NPNS, perhaps because it includes a large optionality or is purely for trading). In NetSuite, one might represent this by a memorandum record (non-posting) or a custom “derivative instrument” record with no initial GL impact. At period end, the finance team revalues it. They create a journal: DR “Oil Forward Contract Asset” (an ERP liability account, e.g. 15xxx) and CR “Unrealized Gain/Loss” (account 40xxx) for the fair-value increase, reversing previous sign. NetSuite’s reporting will then include this mark in net income or OCI as required by ASC 815 hedge rules.

NetSuite Best Practices for NPNS (Normal) Treatment

To ensure consistent application of NPNS, NetSuite users often adopt these best practices:

-

Account Naming Conventions: Use distinct GL accounts for “normal” commodity purchases vs hedge accounts. For example, set up an Inventory or COGS account specifically for physical commodity purchase. Do not mix it with a generic “Inventory” if hedging is also recorded there. This helps segregate NPNS vs non-NPNS.

-

Use of Item Types: In NetSuite, define Item Records for each commodity or category. If the commodity is expected to qualify NPNS, mark it as “Inventory” or “Non-Inventory Resale” item, so that POs and receipts automatically post to the correct accounts. If a contract is non-NPNS (derivative), avoid posting it via an Item receipt; instead, track it via a separate records or even an Non-Inventory item that posts to the derivative GL accounts.

-

Multi-Book Design: Enable multi-book and create one book under GAAP and one under IFRS (or other needed standards). For NPNS purchases, map them normally. For hedging positions, configure adjustments in the book where hedge accounting is applied. NetSuite’s documentation recommends defining accounting preferences (Setup > Accounting) that specify how multi-book transactions are managed [10].

-

Periodic Reconciliation: Even with NPNS, companies undertake periodic reconciliations of committed purchases vs received. NetSuite’s “pending settlement” reports can highlight how much of a forward contract remains undelivered, confirming that physical obligations are on track (consistent with NPNS’s “probable delivery” test).

-

Insurance of NetSuite Features: Make sure the Foreign Currency Revaluation feature is active if the NPNS contract involves foreign currency. Though not strictly NPNS-related, it ensures the net currency exposures are booked properly [30]. Other NetSuite accounting features (like the SuiteTax or VAT rules) should be applied normally to NPNS purchases as well.

-

Leverage NetSuite Reporting: Use saved searches and reports (e.g. “Outstanding Purchase Orders by Item”) to track NPNS-eligible contracts. Tag them (via a custom field) as NPNS so that management reports can separate NPNS from derivative transactions. This aids in audit trails. For example, a saved search could filter POs where Item Type = Inventory and a checkbox “NPNS-flag” = yes, thereby listing all NPNS contracts.

-

Audit and Controls: Maintain the documentation within NetSuite (attachments or custom records) that support the NPNS election. One could attach the ASC 815-10-15-37 checklist to the vendor bill or to the PO in NetSuite’s “Files” subtab. Automatic alerts can be set (Workflow) for when a new commodity contract is created, prompting the finance team to verify NPNS criteria.

By configuring the system this way, a NetSuite implementation can cleanly segregate normal purchases from derivatives. The end result is that users input contracts in the usual modules, and the ERP (with or without minimal intervention) posts them in compliance with ASC 815. Many success stories in practice stress aligning ERP configuration with accounting policy: e.g. “By centrally defining which transactions are scope exceptions, our ERP automatically bypasses hedge accounting on those lines” (Source: onekloudx.com.au) [11].

Implications, Challenges, and Future Directions

Business and Financial Reporting Impact

The NPNS exception has significant impacts on financial statements and risk management. By excluding “normal” contracts from fair-value accounting, it avoids introducing volatility in earnings that would otherwise stem from day-to-day commodity price changes. In effect, the cost of goods sold (COGS) or inventory valuation remains at historical cost (the contracted price) until delivery. This tends to smooth earnings in industries like manufacturing or energy. Failure to apply NPNS when eligible would unnecessarily inflate earnings volatility (as yet-unsettled contracts fluctuate in value). Conversely, inappropriately applying NPNS to speculative trades could mask risk and conflict with ASC 815 intent.

From a risk management perspective, NPNS-qualifying contracts are often the main business risk exposures (e.g. an airline’s fuel needs, a refiner’s crude requirements). These companies usually naturally hedge (by operating characteristics) their net exposures. For example, an oil refiner’s forward crude purchase lock in input costs and simultaneously his product deliveries (gasoline/diesel) lock in revenues, creating a built-in economic hedge. Because they account these as normal purchases/sales, the hedge is like a natural hedging. Accounting-wise, any mismatch gain or loss is nil (net zero in theory). However, if the company also takes separate speculative positions (not NPNS), those must be accounted as derivatives.

NetSuite plays a strategic role by integrating procurement, production, and finance. Automating NPNS means less manual accounting. For large global manufacturers, like those quoted in ERP studies, the ability to run one integrated system for all subsidiaries (in 219 countries [12]) with multi-standards is a key advantage. A NetSuite configuration that seamlessly differentiates NPNS vs derivatives helps assure global controllers and auditors that accounting is consistent across jurisdictions.

Audit and Controls Perspective

Auditors pay special attention to NPNS. A misclassification could lead to misstatements. For example, failing to recognize an embedded option can result in required restatements (the contract should have been net-settled derivative). The checklist in ASC 815 and company policy (and accompanying NetSuite controls) serve as evidence for auditors. The detailed documentation requirement (ASC 815-10-15-37) is designed to ensure audit trails.

From a control standpoint, companies often formalize approval workflows for commodity contracts. In NetSuite, a workflow might be implemented so that high-quantity or high-value purchases automatically require review of NPNS status. For contracts that fail NPNS, additional posts or even a separate subledger could be mandated. Use of signature policies (at the ERP or in procurement systems) ensures proper vetting of contract terms relative to accounting.

Future Considerations

Looking ahead, several trends and developments could influence NPNS and its treatment:

-

Accounting Standard Updates: FASB periodically reviews ASC 815. The recent ASU 2017-12 simplified hedge accounting but did not directly change NPNS. However, FASB remains interested in simplifying hedge accounting further to reduce complexity . Any changes to the core derivative definition or scope exceptions (unlikely but possible) would directly affect NPNS. IFRS Standards also continue evolving after IFRS 9 (e.g. IFRS 17 insurance, IFRS 16 leases); a future IFRS project could potentially reintroduce a “own use” concept. NetSuite customers should watch for FASB “on the radar” updates – for instance, FASB’s 2026 project on hedging recognized an issue of “paper volatility” that NPNS was designed to address . If standards were to allow more aggregation (e.g. portfolios of commodities) or provide relief for certain optionality features, implementation practices would shift accordingly.

-

ERP and Treasury Integration: Technology offers new solutions. NetSuite’s own product roadmaps increasingly emphasize cloud-based and AI-driven features [14]. Future NetSuite modules may embed derivative/hedge functionality (for example, the new Alloy.ai (Net Stock AI for inventory optimization & hedging recommendations). Integration with treasury systems (like Kyriba, Reval, or internal modules) is growing. For NPNS, one could imagine a NetSuite module that automatically flags potential net settlement triggers (e.g. when FX swaps are used to pay vendors) and warns users. Similarly, workflow approvals could leverage machine learning to detect contracts that deviate from normal patterns and thus require extra scrutiny.

-

Geopolitical/Economic Trends: Fluctuations in commodity markets (e.g. energy price shocks, supply chain disruptions) drive companies to use forwards and options more actively. The NPNS exception will continue to matter for many industries. Moreover, tax and regulatory differences across regions might affect contract structuring (for instance, some jurisdictions tax forward contracts as financial derivatives even if physically settled); NetSuite implementations must be flexible to account for such nuances. But in any case, the core accounting logic from ASC 815 will still govern GAAP reporting for US entities.

-

Entity Strategies: From a strategic standpoint, CFOs and treasurers must decide when to use NPNS. Some may choose not to apply it even when available, in order to pursue hedge accounting for consistency or risk reporting (e.g. an integrated company might want all forward positions on the balance sheet to centralize treasury). However, most large corporate policies favor applying NPNS whenever legitimate, as it aligns economic substance to accounting. Future CFO considerations will include how to handle increasingly complex supply contracts (e.g. offtake agreements, renewable energy certificates, crypto hedges) within the NPNS framework.

Conclusion

The Normal Purchases and Normal Sales scope exception in ASC 815 is a cornerstone of commodity and operational risk accounting. It allows businesses to keep routine, business-driven contracts off the lungs of derivative accounting, thereby avoiding artificial volatility in earnings. This exception demands careful analysis of contract terms, business needs, and settlement mechanics.

For users of NetSuite ERP, the key takeaway is to model NPNS contracts as standard purchases/sales within the system. By doing so, the normal procurement/distribution workflows in NetSuite suffice to capture these transactions – no specialized hedge entries are needed on top of them. NetSuite’s multi-book capability further ensures that any differential accounting treatment (between GAAP, IFRS, or other frameworks) can be achieved simultaneously. IT and finance teams should work together to configure NetSuite’s Item records, Chart of Accounts, and possibly custom fields or workflows, so that NPNS transactions “flow through” like any other inventory purchase. This approach matches both the letter and spirit of ASC 815.

Critically, all NPNS designations must be backed by evidence. ASC 815 mandates documenting the basis for exception treatment [25], and auditors will inspect that work. NetSuite can aid compliance by storing contract copies, analysis docs, and by flagging transactions for review.

In sum, meticulously understanding ASC 815-10 NPNS criteria, and reflecting that understanding in NetSuite, ensures accurate financial reporting. Entities maintain transparency by applying NPNS only where intended (actual physical deliveries for operational use) and by isolating derivative exposures for mark-to-market accounting where required. By aligning ERP processes with these rules, companies achieve both regulatory compliance and robust risk management.

Key takeaway: “If it’s just a normal business purchase, process it normally in your ERP and document why it isn’t a derivative”. Conversely, “If it’s a speculative or option-laden deal, treat it as a derivative with its fair-value changes logged separately”. NetSuite provides the technical flexibility to implement this distinction, but it requires clear policies and diligent mapping. With that integrated approach, organizations can confidently handle ASC 815 NPNS in practice, drawing on established guidance [2] and leveraging technology effectively.

References

- FASB ASC 815-10 (Derivatives and Hedging), including paragraph 15-83 (derivative definition) and 15-22 through 15-51 (NPNS criteria) [1] [4].

- Deloitte, Derivatives and Hedging Roadmap, Scope Exceptions (2019), including discussion of NPNS [18] [4].

- EY, “To the Point: Applying the normal purchases and normal sales exception to power contracts in nodal energy markets” (Apr. 24, 2015) [2] [7].

- IFRS Foundation, Analysis of use of IFRS Accounting Standards around the world (2018) – adoption statistics [8].

- Houseblend, NetSuite Multi-Book Accounting: GAAP and IFRS Guide (2026) – overview of GAAP vs IFRS in NetSuite [10] [31].

- OneKloudX, NetSuite Hedge Management Automation (2026) – commodity/FX exposures in NetSuite (Source: onekloudx.com.au).

- Ekwani Consulting, Top 15 Oracle NetSuite Stats for 2025 – NetSuite adoption and usage stats [11] [12].

- Oracle NetSuite Documentation: Foreign Currency Revaluation and Multi-Book Accounting [29] [11].

- Corporate Finance Institute / CFO Club surveys (on IFRS adoption overlaps) [17].

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.