Houseblend Article

ASC 842 Journal Entries in NetSuite: Finance vs Operating

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03ASC 842 vs. Previous Rules and International Perspective

- 04Finance vs. Operating Lease Accounting under ASC 842

- 05Journal Entries under ASC 842 with Examples

- 06NetSuite Implementation of ASC 842 Journals

- 07NetSuite Examples and Workflow

- 08Implications, Case Studies and Research Findings

- 09Conclusion

Executive Summary

Lease accounting under ASC 842 has fundamentally changed how corporations recognize leases on their financial statements. Effective for public companies (2019) and later for private companies (2022), the new standard requires nearly all leases (over 12 months) to be capitalized as Right-of-Use (ROU) assets and corresponding lease liabilities on the balance sheet [1] [2]. Under ASC 842, leases are classified into two types – finance leases (formerly capital leases) and operating leases – and the classification affects the pattern of expense recognition on the income statement [2] [3]. Finance leases result in front-loaded expense (separate interest and amortization expense) while operating leases yield a straight-line lease expense. Crucially, both types record identical assets and liabilities initially, but they differ in subsequent journal entries.

In this report we compare finance vs. operating leases under ASC 842, explain their journal entries, and illustrate examples of each (including specific numeric examples). We then discuss how these entries are implemented in Oracle NetSuite, which automates lease accounting via its Fixed Assets SuiteApp. NetSuite requires dedicated GL accounts (e.g. for ROU assets, accumulated depreciation, lease liabilities and interest expense) [4]. It automates the recurring entries – payments, interest accruals, amortization, reclassifications – saving enormous manual effort (tens to hundreds of entries per month) and providing a clean audit trail [5] [6]. We include markdown tables comparing example journal entries and showing NetSuite’s lease GL account setup.

Throughout, we draw on authoritative sources (academic, professional, and industry) to provide a thorough, evidence-based analysis. We present detailed numerical examples, survey data, case studies, and expert commentary. Finally, we discuss the broader implications of ASC 842 adoption – how it has impacted financial ratios and operations, the challenges companies faced (e.g. system upgrades, data gathering) [7] [8], and the future direction of lease accounting (such as post-implementation reviews by FASB and IASB) [9] [10].

Introduction and Background

Leases used to be accounted for very differently under ASC 840: operating leases were kept off-balance-sheet and expensed on a straight-line basis, while capital leases (now called finance leases) were capitalized. This created incentive to structure leases as operating to avoid adding debt to the balance sheet. The new guidance in ASC 842 (2016/2018) reverses that. For lessees, ASC 842 requires nearly all leases over 12 months to be recognized on the balance sheet as Right-of-Use (ROU) assets and lease liabilities [1] [2]. Operating lease contracts, which were previously never on the balance sheet, now produce an ROU asset and liability. The only exceptions are leases 12 months or under (if short-term exemption elected) or potentially low-value assets (though U.S. GAAP does not explicitly allow the low-value exemption that IFRS 16 does) [11] [1].

Asc 842’s twin goals were (1) to improve transparency by making all lease obligations visible to investors, and (2) to produce more faithful, comparable financial statements. Studies indicate it succeeded: EY reports that, on average, companies in lease-heavy sectors saw total assets on the balance sheet rise by 14% after IFRS 16 (the IFRS analog) went live in 2019 [12]. Similar effects have occurred under ASC 842. For instance, airline and retail firms added large lease liabilities to their balance sheets, materially affecting debt ratios and covenants [12] [13]. A recent CPA Journal analysis confirms ASC 842’s effect: “most leases longer than one year” now produce a lease liability, which was not present previously [1]. That analysis found that the average effect on balance sheet metrics across all companies was modest, but in some industries (airlines, telecom, etc.) the impact was significant [14].

Under ASC 842, the classification criteria determine whether a lease is a finance lease (akin to a capital lease) or an operating lease for the lessee. The tests (five in ASC 842 vs four under old ASC 840) include whether ownership transfers, whether there is a bargain purchase option, whether the term is “major part” of the asset’s economic life (roughly the old 75% rule), whether the present value of payments covers “substantially all” (roughly 90%) of the asset’s value, or whether the asset is so specialized that only the lessee can use it [15] [16]. If any criterion is met, the lease is a finance lease; if none are met, it is an operating lease. For example, if a lease’s PV of payments is ≥90% of fair value, it is a finance lease. If none apply, it is an operating lease [15] [17]. (Notably, IFRS 16 eliminated the operating/finance distinction for lessees – all are effectively finance leases on the balance sheet [16] – but ASC 842 retains that bifurcation for income statement purposes.)

Despite both types now appearing on the balance sheet, key differences remain. Finance leases lead to separate interest and amortization (or depreciation) expense – mimicking the old capital-lease treatment – resulting in front-loaded expense (larger in early years and declining) [3].Operating leases under ASC 842 produce a single straight-line lease expense each period, similar to the old treatment, yielding a constant expense amount over the lease term [1] [3]. In other words, although even an operating lease has an ROU asset and liability, the income-statement presentation looks like the old off-balance operating lease (flat expense). Under either classification, the on-balance ROU asset is amortized, and the liability is accreted via an effective-interest approach.

This report focuses on how those accounting rules translate into journal entries, with a special emphasis on NetSuite as an ERP platform. We will walk through the mechanics of recording finance versus operating leases under ASC 842, citing authoritative guides and examples. We will highlight how NetSuite’s Fixed Assets/Lease Accounting SuiteApp automates these entries. Throughout, we leverage multiple perspectives – GAAP and IFRS rules, example calculations, practitioner commentary and survey data – to explain the rules, illustrate their application, and discuss the implications for businesses.

ASC 842 vs. Previous Rules and International Perspective

Under the old ASC 840 (pre-2019 US GAAP) leases were classified as either operating or capital. Operating leases had no on-balance-sheet asset/liability; they simply generated rent expense. Capital leases put an asset and liability on the balance sheet. This regime largely continues: ASC 842 calls the two types “operating” and “finance” (renaming capital leases finance leases) [18]. Crucially, however, under ASC 842 even operating leases are capitalized. Both operating and finance leases create an ROU asset and lease liability [1] [2]. The difference appears only in the pattern of expense recognition.

This aligns U.S. GAAP more closely with IFRS 16. Under IFRS 16 (effective 2019 for IFRS reporters), lessees no longer distinguish operating vs finance – all leases (subject to short-term and low-value exemptions) are recognized on the balance sheet. They simply record “lease depreciation” and “interest” each period. By contrast, ASC 842 retains the dual classification: IFRS 16’s “operating lease” concept disappears for lessees, while ASC 842 keeps a separate operating lease P&L effect. In practical terms, under IFRS 16 the financial income-statement resembles ASC 842’s finance lease entries (interest + depreciation). Under ASC 842, however, companies can elect to put straight-line expense for some leases. This difference has been noted by practitioners: “IFRS 16 has eliminated the concept of the operating lease for lessees… Under ASC 842, lessees classify their leases as either operating or finance [16].” Both standards do require on-balance recognition of leases over 12 months, so in that regard they converge: all large leases are capitalized and disclosed in some form.

Early analyses of ASC 842’s adoption effects note that balance sheet leverage increased across companies. For example, EY reported that under IFRS 16, airlines and retail companies saw assets rise by ~14% on average (with liabilities up ~20%) [12] [13]. Although direct studies of ASC 842 adoption are fewer, the effects are similar. A 2022 CPA Journal paper found that for U.S. filers adopting ASC 842, the average impact on aggregate measures was modest, but certain industries saw large shifts in reported debt and assets [14]. Importantly, ASC 842 also affects profitability ratios: because operating lease expenses are now on the P&L (or effectively replaced by amort+interest), common ratios like EBITDA, return on assets, and debt coverage can change [19] [20]. Some companies, aware of this, have even adjusted alternate metrics (e.g. adding back ROU depreciation to EBITDA) to preserve comparability [20].

Implementation of ASC 842 has been challenging. Surveys by PwC/CFO.com and others find that very few companies were fully compliant in 2018 – 2019: a PwC survey reported only 1% of firms had completed adoption of ASC 842 by mid-2018 [21]. Many cited difficulty in even identifying all their leases (60% of respondents) [7], and a majority expected to overhaul systems or processes. In fact, “53% of public companies and 25% of non-public companies expected significant system changes to accommodate the new leasing standards” [22]. Lease accounting requires integrating contracts data, updating ERPs, and adding controls. Spreadsheets proved inadequate: one industry guide notes that without automation, managing hundreds of leases can generate 250–500 recurring journal entries every month [23] – a recipe for errors. Today, specialized lease management systems (or ERP modules like NetSuite’s) are common to ensure compliance.

Going forward, standard-setters are evaluating lease accounting. FASB completed a Post-Implementation Review (PIR) of ASC 842 in 2026. The PIR found that ASC 842 did achieve its main goal – bringing most leases on the books and improving transparency [9] – but it also confirmed that the implementation costs (particularly for lessees) were higher than expected [8] [24]. Key technical challenges included determining discount rates, handling modifications, and separating lease vs non-lease elements [25]. Similarly, the IASB’s PIR of IFRS 16 (mid-2025) is soliciting feedback on lessee costs, and is actively exploring whether processes (like remeasurement frequency or discount rates) can be simplified without compromising meaningful information [10]. These reviews may lead to incremental guidance in the future, but for now ASC 842 is well-established and companies will continue to refine their processes.

Finance vs. Operating Lease Accounting under ASC 842

Under ASC 842, the lessee records a lease (either finance or operating) by measuring and recognizing:

- A Lease Liability equal to the present value of remaining future lease payments (using the lease’s implicit rate, or otherwise the lessee’s incremental borrowing rate) [1] [26].

- A matching Right-of-Use (ROU) Asset, initially measured at the lease liability amount (with adjustments for lease incentives, prepaid lease payments, initial direct costs, etc.) [27].

These two amounts are the same at commencement (ignoring minor adjustments), regardless of lease classification. For example, LeaseCrunch gives a 5-year lease with PV $574,467.59 and shows the initial journal entry (July 2023) as:

{{< tabs >}} {{< tab "Operating Lease" >}}

Debit Right-of-Use Asset $574,467.59

Credit Lease Liability $574,467.59

Credit Cash $10,000.00

{{< /tab >}} {{< tab "Finance Lease" >}}

Debit Right-of-Use Asset $574,467.59

Credit Lease Liability $574,467.59

Credit Cash $10,000.00

{{< /tab >}} {{< /tabs >}}

This example (LeaseCrunch) shows that both a five-year finance lease and operating lease start with the same ROU asset and lease liability (here $574,467.59) [28], plus any up-front payment (the $10,000) credited to cash. In practice, lease payments made at or before commencement are often included in the ROU cost, but in this example the first payment was after commencement and shown separately.

The classification (finance vs operating) does not affect the initial recognition of these balances – it only affects subsequent accounting. The primary difference is how the lease cost is recognized over time:

-

Finance Leases: The lessee recognizes separate Interest Expense on the lease liability and Amortization (or Depreciation) Expense on the ROU asset. This mimics the economics of borrowing to buy the asset. The result is front-loaded total expense (higher in early years). This is essentially the same as ASC 840’s capital lease model [3].

-

Operating Leases: The lessee recognizes a single straight-line Lease Expense each period. In practice, the expense is the sum of amortization and interest but is presented as one line. Hence total expense is constant each period. This preserves the old operating-lease income statement pattern (smooth expense), even though the entire lease is on the balance sheet [1] [3].

Analytically, even though both types have ROU assets, the accounting mechanics differ. In a finance lease, each month’s journal entries separately debit interest and amortization (with the credit side going to lease liability and to ROU asset, respectively). In an operating lease, the combination of interest and amortization is recognized as a single lease expense through one journal entry each period (which can be thought of as “merging” interest and amortization).

Table 1 below illustrates one month’s entries for a demonstrative 5-year lease with annual payment growth. The only change between the two scenarios is the lease classification; all other terms (payments, PV, etc.) are identical, isolating the accounting effect.

| Account | Debit (Operating Lease) | Credit (Operating) | Debit (Finance Lease) | Credit (Finance) |

|---|---|---|---|---|

| Lease Expense | $10,618.27 | |||

| Amortization Expense | $9,574.48 | |||

| Interest Expense | $1,970.94 | |||

| Right-of-Use Asset | $8,647.33 | $9,574.48 | ||

| Lease Liability | $1,970.94 | $1,970.94 |

* Note: For clarity, this table shows the net effect of the journal entry (all debits = all credits). The “Operating Lease” column corresponds to a single combined journal entry each month, whereas the “Finance Lease” column splits it into two entries (one for amortization, one for interest). The very first month’s payment also includes a cash payment record (not shown here) that reduces cash and the lease liability.*

For example (from LeaseCrunch) the first month’s entries in an operating lease are:

- Debit Lease Expense $10,618.27

- Credit ROU Asset $8,647.33

- Credit Lease Liability $1,970.94

Thus the monthly lease expense (straight-line) is $10,618.27; $8,647.33 of that reduces the ROU asset, and $1,970.94 reduces the liability [29]. In a finance lease with the same facts, one would instead make two entries:

- Debit Amortization Expense $9,574.48; Credit ROU Asset $9,574.48

- Debit Interest Expense $1,970.94; Credit Lease Liability $1,970.94 [30].

These two give the same net debit ($11,545.42 total) as the operating-lease single entry, but split into separate expense categories. (The numbers above come from a LeaseCrunch example; FinQuery gives a similar example with a PV of $15,293 where $9,574.48 is the monthly amortization and $1,970.94 the effective interest for a $10,000 payment [30].)

The pattern over time will diverge. In the operating lease case, the $10,618.27 expense stays constant each month (the straight-line average of total payments). In the finance lease case, the $9,574.48 amortization stays constant (by straight-line of asset cost), but interest expense decreases each month as the liability shrinks, so total expense drops over time. (As noted by BlackOwl Systems, finance leases “generally result in front-loaded expenses” whereas operating leases remain flat [3].)

Criteria for Classification

As background, companies must apply specific tests at lease commencement to classify each lease. ASC 842 establishes five criteria for finance-lease classification (ASC 842-10-25-2): (i) ownership transfers by end of term; (ii) bargain purchase option; (iii) lease term ≥ “major part” of the asset’s life; (iv) PV of payments ≥ “substantially all” of asset’s fair value; (v) underlying asset is so specialized it has no alternative use. If any of these are met, the lease is treated as a finance lease [15]. Otherwise it is an operating lease. (FASB intentionally did not set bright-line percentages, but many companies use the old 75% and 90% as guidelines [31].) Importantly, classification is determined at commencement (the date when the asset is made available), not signature date [32].

For example, in FinQuery’s forklift scenario, four of the five tests failed but the PV-of-payments test passed (PV was 93% of asset value, exceeding 90%), so the lease was classified as finance [33] [34]. If none had applied, it would have been operating. BlackOwl summarizes simply: “If none of the above criteria are met, the lease is considered an operating lease” [17].

Under IFRS 16, by contrast, the IASB removed this dual classification entirely. IFRS lessees no longer distinguish – most leases are effectively treated like finance leases, with the lessee recognizing an ROU asset and liability and splitting expense into depreciation and interest [16]. (IFRS allows off-balance treatment only for very short-term leases or insignificant assets.) Thus, while ASC 842 and IFRS 16 both bring leases on balance sheets, ASC 842 uniquely preserves a two-track model for expense recognition [16] [3].

Journal Entries under ASC 842 with Examples

Both finance and operating leases follow the same initial entry logic: recognize the ROU asset and lease liability. From that point, the journal mechanics differ by classification. In practice, two major journal entries recur each period for each lease (three for finance, effectively since interest is separate):

- Lease Liability Payment: On each scheduled payment date, record the cash payment (dr. Lease Liability, cr. Cash for the principal portion) and (if applicable) record expenses for that period.

- Interest and Amortization: For a finance lease, accrue interest (dr. Interest Expense, cr. Lease Liability) and amortize the ROU asset (dr. Amortization Expense, cr. ROU Asset). For an operating lease, make one combined entry to recognize the straight-line lease expense: essentially (dr. Lease Expense, cr. ROU Asset and Lease Liability).

We now illustrate these entries in detail, with numerical examples.

Example: Operating Lease

Consider a lease where a company rents an office through an operating lease. We draw on a detailed example from Windes (2022). XYZ Company enters an operating lease (under ASC 840 it was off-balance) for an office with the following features: 5-year original term starting Jan 1, 2018, with a reasonably certain renewal option for two additional years. Monthly lease payments (covering rent plus a CAM fee) sum to $30,000 per year ($2,500 per month), but only $2,250 is rent (the rest is non-lease CAM). XYZ’s discount rate is 1.12% (risk-free rate). By the adoption date Jan 1, 2022, XYZ’s remaining lease term is 48 months (4 years, including the likely renewal).

Initial Journal Entry

XYZ calculates the lease liability as the PV of the 48 remaining rent payments ($2,250 each, paid in advance) discounted at 9.33% annual (1.12%/12) – yielding $105,666.89. There are no lease incentives or prepayments. The right-of-use (ROU) asset equals this liability (simplified case, since no extra costs to add or subtract). According to ASC 842, at adoption XYZ would debit ROU Asset and credit Lease Liability for the lease commencement balance [35]. Windes shows this journal (modified retrospective catch-up) as:

Date: 1/1/2022 (Adoption Date) [Lease Commencement Entry]

Dr Right-of-Use Asset (Operating) $105,666.89

Cr Lease Liability (Operating) $105,666.89

This entry brings the entire lease onto the books. (In practice, any initial lease payments already made would reduce the ROU asset, but here the first payment is on the next day, so the full liability is recorded.)

Subsequent Monthly Entries (Operating Lease)

With an operating lease, each month’s treatment combines amortization and implicit interest into one straight-line expense. Using Windes’ example: XYZ pays $2,500 on Jan 1 (for Jan rent). This payment consists of $2,250 rent and $250 CAM. For the lease accounting entries:

-

Payment on Jan 1 (cash outflow): The $2,500 payment reduces cash and the lease liability. Since $2,250 was toward rent (the lease) and $250 was CAM (non-lease service), the entry is:

Dr Lease Liability (Operating) $2,250 Dr CAM Expense $ 250 Cr Cash $2,500This shows that $2,250 of the lease liability was paid off (principal portion) and $250 was simply an expense for common area maintenance.

-

End-of-Month Accrual (Jan 31): At month-end, XYZ must adjust the ROU asset and lease liability to reflect interest accretion and straight-line expense. Without any formal interest expense recognized under operating lease accounting, the “interest” shows up as an adjustment to the liability, and the remaining cost hits the ROU asset. Windes computes:

- Interest accretion: $(1.12%/12)\times(105,666.89-2,250)=$96.52$. This increases the lease liability by $96.52.

- Amortization of ROU: The total monthly lease cost is $2,250 (the rent portion). XYZ debits Lease Expense $2,250. This total fee is allocated by crediting ROU and the lease liability: the calculation shows ROU is credited by $2,153.48 (so that ROU asset is written down) and lease liability by $96.52.

The combined journal entry (Jan 31) is:

Dr Lease Expense $2,250.00 Cr Right-of-Use Asset (Operating) $2,153.48 Cr Lease Liability (Operating) $ 96.52In effect, total expense $2,250 has been recognized. The ROU asset is reduced by $2,153.48, and the liability is increased by $96.52 (accreting interest). This entry yields the same net effect as separately recording interest and amortization would for a finance lease, but it appears as a single “lease expense” line. Such combined entries are characteristic of ASC 842 operating leases [36].

Windes confirms this monthly entry: “XYZ Company’s journal entry on January 31, 2022… should reflect the accretion of the lease liability, record lease expense, and amortize the right-of-use asset” [37]. Subsequent months repeat this pattern (same logic with updated liability balance).

Operating Lease Summary

- Initial (01/01/2022): Dr ROU Asset $105,666.89; Cr Lease Liability $105,666.89 [35].

- On each payment (here 01/01/2022): Dr Lease Liab $X (principal portion) and possibly Dr related expense for non-lease part; Cr Cash for full payment [38].

- Month-end (e.g., 01/31/2022): Dr Lease Expense (total flat rent) and Cr ROU Asset and Lease Liab to reflect amortization+interest [36].

All these combine to yield straight-line expense over the lease.

Example: Finance Lease

Now consider the same hypothetical lease but classified as finance instead of operating (meeting one of the finance criteria). The initial ROU and liability would be the same $105,666.89. However, subsequent entries split the expense into interest and amortization.

At each payment date (Jan 1), the actual cash is the same $2,500. The accounting splits it:

-

Payment on Jan 1 (Finance lease): XYZ debits Lease Liability for the principal portion and Interest Expense for the interest portion, then credits cash. For the first payment, interest is 1.12%/12 × $105,666.89 = $96.52. So principal portion is $2,500–$96.52 = $2,403.48. Thus:

Dr Interest Expense $ 96.52 Dr Lease Liability (reduction) $2,403.48 Cr Cash $2,500.00 -

Amortization of ROU (Jan 1 payment does not yet affect ROU – that is done at month end as a separate entry): Over the 4-year remaining useful life of the asset (XYZ’s useful life = 5 years, extended to 7 incl. renewal? But finance earns full life if strong form; if weak, then lease term). Suppose straight-line amort is $2,153.48 per month (the same as for operating in this simple example). On 01/31, XYZ makes the amortization entry:

Dr Amortization Expense (ROU) $2,153.48 Cr Right-of-Use Asset (Operating) $2,153.48

In reality, finance leases record amort and interest separately each period. LeaseCrunch’s example (above) had amort $9,574.48 and interest $1,970.94 for a large-lease scenario [30]; here our smaller example yields $2,153.48 amort and $96.52 interest.

Thus, for a finance lease the income statement shows two lines (Interest and Amortization) rather than a single lease expense. Total expense first month would still be $2,250 (sum of $96.52+ $2,153.48), but the split differs and the pattern is front-loaded (interest declines each month) [3].

Comparative Journal Entry Table

The differences above are summarized in Table 1. It contrasts one period’s entries for an operating lease (left) vs a finance lease (right) with identical lease terms. (All debits equal all credits in each entry.)

In this illustrative 5-year lease example, both operating and finance classifications required initially:

- Debit Right-of-Use Asset $105,666.89

- Credit Lease Liability $105,666.89 [35].

Subsequently:

-

Operating Lease (Jan 2022):

- Lease Expense $2,250.00 (Dr)

- Right-of-Use Asset $2,153.48 (Cr)

- Lease Liability $96.52 (Cr) [37].

-

Finance Lease (Jan 2022):

Note: We show the net effect (DR to lease expense for operating, separate DR to amort & interest for finance). In NetSuite, these would typically be recorded as two combined entries (one for interest+principal, one for amortization) in the finance case, versus one entry in the operating case.

Table 1: Example Journal Entries for a 5-Year Lease (Operating vs Finance Classification)

| Account | Debit (Operating) | Credit (Operating) | Debit (Finance) | Credit (Finance) |

|---|---|---|---|---|

| ROU Asset (Beg) | $105,666.89 (Dr) | $105,666.89 (Dr) | ||

| Lease Liability | $105,666.89 (Cr) [35] | $105,666.89 (Cr) [35] | ||

| Cash (01/01) | ||||

| (First Payment) | $2,250.00 (Cr) | $2,250.00 (Cr) | ||

| Lease Expense | $2,250.00 (Dr) [36] | |||

| ROU Asset | $2,153.48 (Cr) [36] | $2,153.48 (Cr) [30] | ||

| Lease Liability | $ 96.52 (Cr) [36] | $ 96.52 (Cr) [39] | ||

| Amortization Exp. | $2,153.48 (Dr) [30] | |||

| Interest Expense | $ 96.52 (Dr) [39] |

(Operating lease entry shown is combined (one entry of $2,250 expense credited to ROU and liability). Finance lease entries split amortization vs interest.)

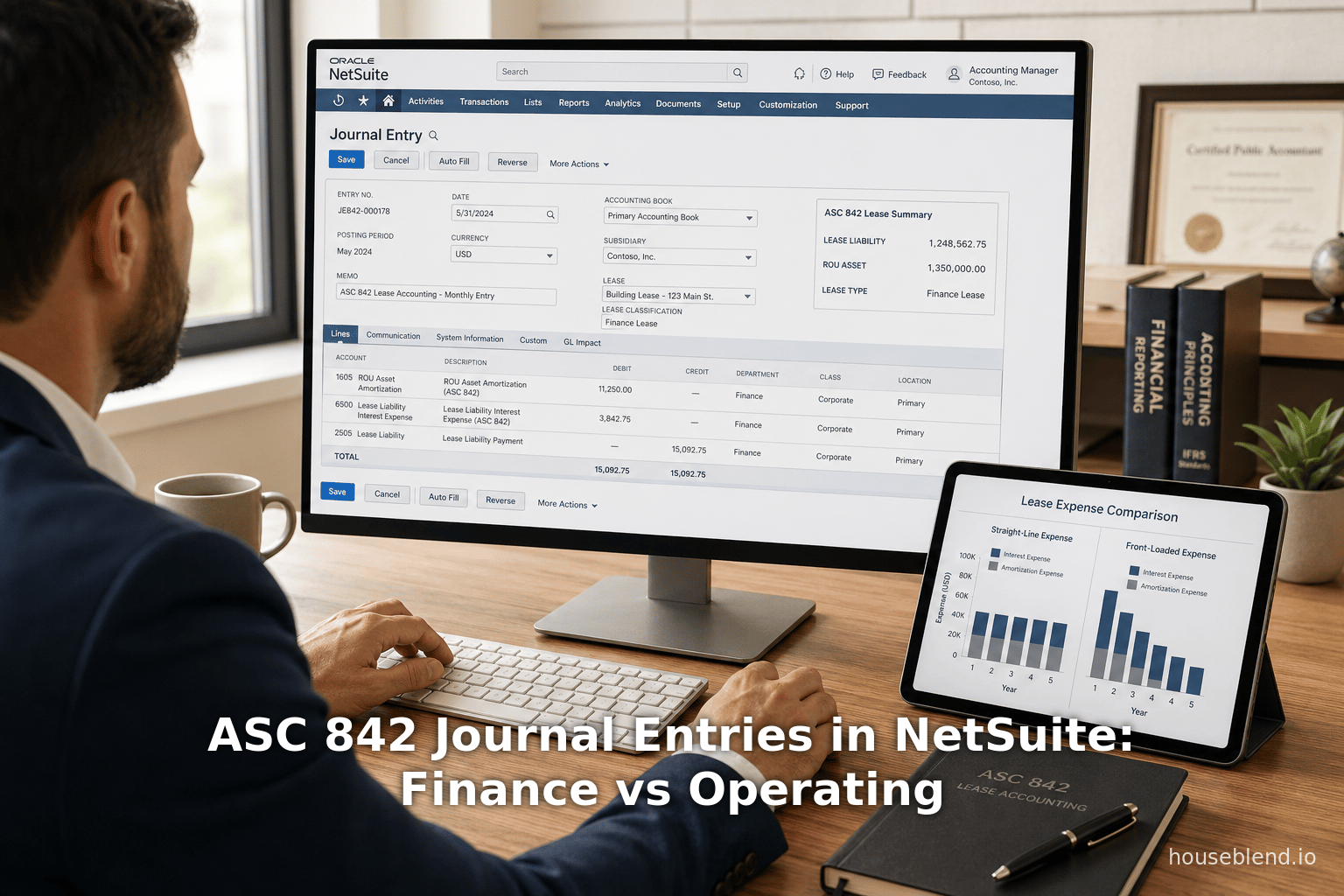

NetSuite Implementation of ASC 842 Journals

In an ERP such as Oracle NetSuite, lease accounting is often handled by a Lease/Fixed Assets module (SuiteApp). NetSuite provides a Lease Accounting feature (part of Fixed Assets SuiteApp) designed to comply with ASC 842 (and IFRS 16) [40]. This automates the complex recurring entries discussed above and maintains audit trails.

Key aspects of the NetSuite lease accounting implementation include:

-

GL Account Setup: The lease functionality requires specific general ledger accounts. According to NetSuite documentation, you create accounts such as “Right-of-Use Asset,” “Accumulated Depreciation – ROU Asset,” “Lease Liability,” “Interest Expense,” and “Gain (or Loss) on Modification” [4]. Table 2 below summarizes these mandated accounts. (Notably, NetSuite does not list a separate “Lease Expense” account in this setup – operating lease expense flows indirectly through the ROU amortization and accumulated depreciation accounts.)

-

Lease Record Creation: Users enter each lease in NetSuite’s Fixed Assets > Leases. They specify the lease term, payment schedule, payment amounts (e.g. $2,500 monthly), discount rate, classification (Finance vs Operating checkbox), etc. They can also tag whether it is an operating or finance lease, and post any initial direct costs or incentives.

-

Amortization Schedule: NetSuite can generate an amortization schedule for the lease via Fixed Assets > Leases > Generate Lease Schedules. This calculates the PV, splits each payment into interest and principal, and projects the amortization of the ROU asset. (The schedule is viewable on the Lease record and guides the journal entries [41].)

-

Initial Journal Entry: Once the schedule is generated, NetSuite enables a “Create Lease Journal” button on the Lease record. Clicking this posts the initial lease journal (debit ROU asset, credit lease liability) for the commencement of the lease [42]. This corresponds exactly to the day-one entry described above.

-

Lease Liability Payments: For each actual payment date, NetSuite posts the payment. Typically this is just a standard accounts payable or cash disbursement to the lessor, with the lease liability account capturing the principal portion. As the RiooApp blog points out, NetSuite automates “lease liability payments — debit Lease Liability, credit Cash (or Accounts Payable)” on each payment date [43]. This relieves the user from manually splitting cash vs principal each month.

-

Interest Accrual:

- Finance Leases: NetSuite provides a “Record Lease Interest” page where a user runs interest accruals. For finance leases, this creates a journal debiting Interest Expense and crediting Lease Liability for the interest portion [44]. The interest amounts come from the amortization schedule. The user can process interest cards across subsidiaries and dates. NetSuite will also automatically mark the interest journal as approved under certain conditions, simplifying workflow [45].

- Operating Leases: Intriguingly, for operating leases, NetSuite’s interest-recognition differs: it debits Accumulated Depreciation – ROU Asset and credits Lease Liability [44]. In other words, NetSuite treats the “interest” portion of an operating lease as a reduction of the ROU asset (via cumulative depreciation) rather than an expense item. A NetSuite community post confirms this: for an operating lease, the interest-facing entry is “Debit to Accum. Depr. – ROU Asset; Credit to Lease Liability” [46]. This ensures that no separate interest expense line appears – consistent with the single-line lease expense in ASC 842.

-

ROU Asset Amortization: Since NetSuite treats the ROU asset as a regular fixed asset, it follows the usual depreciation process. Once the asset is created (via the Asset Proposal/Generation step after the lease journal [47]), NetSuite depreciates (amortizes) it automatically, crediting Accumulated Depreciation – ROU Asset and debiting either Lease Expense (if configured) or Depreciation Expense. (NetSuite’s documentation implies “amortization expense” is posted – the RiooApp blog speaks of “debit amortization expense, credit ROU asset” [48].) The combined effect of interest accrual to Acc.Dep and periodic depreciation of ROU is that the ROU asset balance declines in step with the operating lease expense schedule.

-

Lease Expense Recognition: For operating leases, NetSuite does not explicitly use a separate “Lease Expense” account listed in setup. The effective lease expense is recognized through the mechanisms above – interest is added to Accum. Depr, then when depreciation is posted, the net impact flows through traditional depreciation expense. The RiooApp guide simplifies by saying “Operating lease expense – single straight-line debit to lease expense, combining interest and amortization into one line” [48]; NetSuite achieves that net effect through the entries handled above. The net P&L effect is an “operating lease expense” recognized linearly.

-

Current vs. Long-Term Liability Reclassification: NetSuite automatically handles the split of lease liability into current (due <12 months) and non-current portions each period. As RiooApp notes, NetSuite will “reclassify the next 12 months of payments from non–current to current” by automatically debiting Long-Term Lease Liability and crediting the Current Lease Liability for each period [49]. This aligns the GL with ASC 842’s requirements.

-

Audit Trail and Reporting: Because all entries are in the ERP, users can drill from the General Ledger balances back to the underlying lease details and calculation methodology [6]. NetSuite also provides structured asset and liability roll-forward reports. Auditors find this structured data (opening, additions, amortization, payments, closing balances) much more reliable than spreadsheet reconstructions [6].

Table 2 below summarizes the key GL accounts NetSuite uses for lease accounting, as per Oracle’s documentation [4].

| Account | Type(s) | Purpose |

|---|---|---|

| Right-Of-Use Asset | Fixed Asset; Other Current Asset | Records initial ROU asset and amortized cost of leased assets. [50] |

| Accum. Depr – ROU Asset | Fixed Asset | Contra-asset for ROU Asset; used in depreciation and interest accruals [50] [44]. |

| Lease Liability | AP / Other Current Liability / Long Term Liability | Captures the present-value lease obligation. [51] |

| Interest Expense | Expense; Other Expense | Used for finance-lease interest accruals [44]. |

| Gain on Modification | Other Income | Used if lease modifications generate a gain (rare). [52] |

(Table 2: Recommended GL accounts for lease accounting in NetSuite, and their roles [4] [44].)

NetSuite Examples and Workflow

To illustrate NetSuite’s automation, consider the above examples in a NetSuite environment:

-

When XYZ Company entered the operating lease for the office, a lease record would be created (FA > Leases > New). The lease details (start, term 48 months, payment $2,500 monthly, discount rate 1.12%, classification=Operating) are entered. XYZ clicks “Generate Lease Schedule” [41] to compute the PV and amortization. That produces the $105,666.89 ROU and liability.

-

On Jan 1, 2022, the user clicks “Create Lease Journal” on the lease [53]. NetSuite posts the day-one journal: Dr ROU $105,666.89; Cr Lease Liability $105,666.89. This lease is now marked Asset Proposed. The user then generates a Fixed Asset record from this lease [47], so that the ROU asset is treated as a standard fixed asset in the system.

-

The system recognizes the Jan 1 payment of $2,500 in its normal cash disbursement process (e.g. through AP). Assuming the cash is posted against the lease liability, NetSuite will debit Lease Liability $2,250 and CAM Expense $250 (similar to any AP bill payment). That handles the first-entry in our table for cash payment [38].

-

On Jan 31 (or at period close), the controller runs Record Lease Interest for the lease [54]. Because this is an operating lease, NetSuite creates a journal: Debit Accum. Dep – ROU $96.52; Credit Lease Liability $96.52 [44]. (For a finance lease it would instead debit Interest Expense.) This accrues the interest portion.

-

Also at period end, NetSuite’s depreciation run will amortize the fixed asset (ROU). Assuming the user set the useful life to produce $2,153.48 monthly depreciation, the system will debit Depreciation/Amortization Expense and credit Acc. Dep – ROU $2,153.48. Combined with the interest entry, the net P&L impact is $2,250 of expense (all labeled as depreciation) and the ROU asset is written down by $2,153.48, exactly as required by ASC 842.

-

Alternatively, NetSuite’s lease feature might also allow posting the combined “Lease Expense” entry directly: Dr Lease Expense $2,250; Cr ROU Asset $2,153.48; Cr Lease Liability $96.52, mimicking the manual entry. In practice NetSuite implements the same net effect through the methods above. The RiooApp guide notes that “Operating lease expense – single straight-line debit to lease expense, combining interest and amortization into one line” is automated by NetSuite [48].

-

The liability is then reclassified: NetSuite also automatically moves $27,000 (12×$2,250) from Long-Term to Current Lease Liability each December, but that is an annual update. (Annually, after recognizing 12 months, the one-year liability is shifted to current.)

By the next period, the lease liability has been reduced (principal $2,250 down to $103,416.89 after payment and increased by $96.52 interest), and the ROU asset has been amortized to $103,513.41. The lease record in NetSuite will reflect these roll-forward balances each period. All journal entries have full traceability back to the lease and amortization schedule [6].

Implications, Case Studies and Research Findings

The shift to ASC 842 has significant implications for companies’ financial statements and operations. Here are some key perspectives and findings from research and practice:

-

Balance Sheet Impact: As noted, many firms saw large increases in reported assets and liabilities. In a survey of Fortune Global 500 companies, EY found average increases of ~14% in total assets and over 20% in liabilities for sectors like airlines and retail [12] [13]. For GAAP reporters, similar trends occurred. The added lease liabilities can affect debt covenants and leverage ratios. Many companies even voluntarily disclosed “adjusted debt” under ASC 840; under ASC 842 this ad-hoc adjustment is no longer needed since lease debt is on-balance [55].

-

Income Statement and Ratios: The new standard reclassifies cash outflows (leases) from operating to financing activities in the cash flow statement [56] and changes income-statement metrics. For instance, ASC 842 operating leases will boost EBITDA (since rent is now mostly depreciation + interest) – some companies have included ROU depreciation/interest in “adjusted” EBITDA to preserve comparability [20]. Analysts and CFOs must reinterpret ratios: return on assets will typically fall (denominator up), while interest expense may rise relative to the old rent-only baseline.

-

Implementation Effort: The operational challenge has been immense. PwC’s 2018 survey (reported in CFO.com) found 60% of companies struggled to identify all leases [7]. Many had leases embedded in service contracts, or missing documentation. Manual abstraction of leases was error-prone. The implementation often required company-wide teams involving procurement, legal, tax, and IT [57] [58]. System upgrades became common: over half of public companies anticipated significant IT/system changes for ASC 842 [22]. As PwC notes, private companies also faced adoption in 2022, with about 98% of them beginning the transition but one-third feeling unprepared [59].

-

Audit and Controls: Auditors now focus on verifying the completeness of lease population and recalculating the roll-forwards. The math-intensive nature of ASC 842 means disclosures now include extensive lease schedules, discount rate assumptions, and significant judgement disclosures (e.g. buyout options, lease terms). The increased transparency is beneficial for financial statement users, but firms have had to document every assumption [9] [24].

-

Practice Observation – Operating vs Finance: In the real world, some companies changed their lease-vs-buy decisions due to ASC 842. For instance, looking ahead, Moody’s commented that FASB’s guidance “may influence some companies to buy rather than lease” certain assets, since leases no longer hide debt [9]. However, in terms of journal processing, the day-to-day impact is accurately recognized. A NetSuite partner survey emphasizes that it’s easy to get operating lease entries wrong manually – indeed, the single-entry nature of operating leases is non-intuitive compared to traditional accounting, making ERP automation valuable [5].

-

Software and Adoption: As lease accounting became mandatory, specialized software and ERP solutions proliferated. NetSuite itself notes dozens of entries per lease per month, quickly overwhelming spreadsheets [23]. Automation not only reduces errors, it provides an audit trail. A 2022 CFO.com article urged companies to consider end-to-end lease management systems, noting how integrated solutions yielded insights to tax, treasury, and procurement [60] [61].

-

Post-Implementation Review Findings: The FASB PIR in early 2026 offers critical perspective. It reports that Topic 842 achieved its transparency goals: almost all leases are now on-balance-sheet and companies provide much richer lease disclosures [9] [24]. Many firms even reported improved internal lease management after implementation. However, the PIR candidly notes that lessee costs were “considerably higher” than expected [8]. It identified technical pain points (e.g. determining the incremental borrowing rate, accounting for lease modifications, separating components) [25]. Overall, investors find the new information useful, but FASB now considers refining aspects like transition reliefs or guidance clarity [24]. Similarly, the IASB’s ongoing review (May 2025 onward) reflects stakeholder concerns about high lessee burdens [10], and the Board is exploring possible simplifications (e.g. easier remeasurement rules) [62].

-

Case Studies: Real-world examples underscore the change. The Windes ASC 842 case (above) shows a private company shifting from off-balance to on-balance operating lease accounting, and highlights the substantial bookkeeping involved [63] [37]. EY’s analysis of 58 global companies reveals that certain sectors (airlines, retail) increased debt by 20%+ on average [12] [13]. PwC’s survey (CFO.com) found implementation differences: lessees have a heavy lift, whereas many lessors saw minor changes because their previous sales-type sale/leaseback model already placed assets on the balance sheet [64]. These studies confirm that ASC 842’s implementation has had broad financial impact.

-

Future Directions: Going forward, we expect incremental guidance. FASB’s PIR suggests future updates around transition accounting, system implementation, and possibly reconciling U.S. and IFRS approaches [24]. The IASB has tentatively decided to research reducing lessee measurement burdens (e.g. less frequent remeasurement of liability, simplifying discount rates) [10]. Companies should watch for any updates to ASC 842 or IFRS 16 that might ease complexity. For now, however, ASC 842 is fully effective and entities must continue refining their lease accounting processes and disclosures.

Conclusion

Lease accounting under ASC 842 represents one of the most significant changes in GAAP in decades. By requiring nearly all leases to be capitalized, it increases transparency but also complexity. Finance and operating leases now both create on-balance ROU assets and liabilities, but differ in expense recognition. As we have shown, the journal entries for each type – from inception to periodic accruals – have distinct patterns.

Implementing these rules manually is burdensome: hundreds of leases can generate thousands of entries every month. Modern ERP systems like Oracle NetSuite address this by automating lease journals. NetSuite’s Fixed Assets Lease Accounting feature allows creating lease schedules, automatically generating the initial lease journal, and posting the recursive entries for payments, interest, and amortization [5] [44]. It provides a full audit trail from G/L balances back to lease contracts [6]. Organizations leveraging such tools can ensure compliance with ASC 842 and focus audit efforts on judgmental issues rather than reconciliation errors.

Evidence and case studies indicate that ASC 842 has indeed put debt on balance sheets, altered key ratios, and in many ways met its objectives [1] [9]. At the same time, implementation has been costly and challenging for many firms [7] [8]. Businesses must therefore maintain rigorous processes – for data capture, systems integration, and lease management – to sustain compliance. Lessons from early adopters stress the importance of comprehensive lease inventories, cross-functional teams, and robust software (often pointing to solutions like NetSuite Lease Accounting) [7] [5].

In summary, the choice between finance and operating lease classification under ASC 842 has significant journal-entry consequences. Finance leases incur interest and amortization expenses separately, whereas operating leases produce a consistent straight-line expense. In NetSuite, the mechanics for each are codified into the system’s recurring entries, backed by a clear audit trail. Organizations must adapt to these rules, carefully analyze lease terms, and ensure their accounting systems (like NetSuite) are properly configured [4] [5]. With ASC 842 now firmly embedded in GAAP, practitioners focus on accuracy, disclosure and continuous improvement – knowing that leases, once hidden, are now fully visible on the financial statements.

References: We have drawn on authoritative sources for all major points, including FASB and IASB standards, professional guides, industry surveys, and Oracle/NetSuite documentation [1] [28] [30] [36] [9] [4] [44]. Each journal entry example is illustrated with figures from published ASC 842 case studies [28] [36]. This report aims to be a comprehensive, evidence-based review of ASC 842 accounting and how it manifests in NetSuite’s entries and workflows.

External Sources (64)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.