Houseblend Article

ASC 842 Lease Amortization: NetSuite Journal Entries

Examine ASC 842 lease amortization schedules, right-of-use (ROU) asset calculations, and how to record compliant journal entries within Oracle NetSuite.

Inside this article

Executive Summary

The introduction of ASC 842, the FASB’s lease accounting standard effective for fiscal years beginning after December 15, 2018 [1], fundamentally overhauled U.S. GAAP lease accounting. Most leases now require on‐balance‐sheet recognition of a right-of-use (ROU) asset and corresponding lease liability. Under ASC 842, companies must measure the lease liability at the present value of future lease payments and set the ROU asset equal to this amount (adjusted for prepaid or accrued costs) [2]. The subsequent amortization of the liability (through interest expense) and the ROU asset (through depreciation or amortization) produces a detailed lease amortization schedule. For finance (formerly capital) leases, expense is recognized as interest + amortization, whereas for operating leases ASC 842 mandates a single lease expense although it is underpinned by the same interest/amortization mechanics.

In practice, implementing ASC 842 in an ERP like Oracle NetSuite requires configuring the general ledger to capture ROU assets and lease liabilities, and then recording the periodic journal entries reflecting interest and amortization. Many NetSuite users create fixed-asset records for each ROU asset and use amortization schedules or recurring journals to book the monthly lease entries. In one illustrative case, a software firm tracked each leased asset as a NetSuite fixed asset: at lease inception it booked Dr ROU Asset, Cr Lease Liability for the PV of payments; then each month it recorded the implicit interest (Dr Interest Expense, Cr Lease Liability) and ROU amortization (Dr Amortization Expense, Cr ROU Asset) plus the cash payment (Dr Lease Liability, Cr Cash) to align with ASC 842. This approach effectively mirrors the lease amortization schedule, ensuring net income and balance-sheet proportions comply with ASC 842.

Globally, the new lease standards dramatically expanded reported liabilities. IFRS 16 (the analogous international standard effective 2019) was estimated to add about $2.8 trillion of lease liabilities to corporate balance sheets [3]. Under IFRS 16, all leases (barring short-term and low-value exemptions) are capitalized, whereas ASC 842 retains a finance vs. operating dichotomy [4]. Both standards, however, follow the same tenets: placing large leases on balance sheet and amortizing over the lease term [5] [4].

This report provides an in-depth analysis of lease amortization schedules and journal entries under ASC 842, with a focus on implementation in NetSuite. It covers the historical context of lease accounting, the mechanics of calculating present values and amortization, detailed journal entry patterns for both finance and operating leases, and practical considerations (including NetSuite-specific processes). Throughout, the discussion is supported by numerical examples, tables, and citations to accounting standards and analyses by professional bodies [6] [5] [4]. It also examines the current and future implications of these standards on corporate accounting, as well as lessons from real-world implementations.

Introduction and Background

Leasing is a fundamental business practice. Broadly speaking, “a lease is a contract calling for the lessee (user) to pay the lessor (owner) for use of an asset for a specified period of time.” [7]. Historically, U.S. GAAP distinguished “capital” (finance) leases from operating leases, but only capital leases were recognized on the balance sheet. Effective January 1, 2019 (for public companies) the FASB replaced ASC 840 (the old lease standard) with ASC 842: Leases [6] [1]. Under ASC 842, nearly all leases are capitalized on the lessee’s balance sheet. Specifically, lessees record a right-of-use asset equal to the present value of lease payments (plus certain costs) and a lease liability for that same amount [2] [5].

This change aligns U.S. GAAP with IFRS 16 (issued by the IASB), which for most companies became effective January 1, 2019 [8]. Similar to ASC 842, IFRS 16 requires lessees to recognize ROU assets and lease liabilities for almost all leases [5]. An important global context: by one estimate IFRS 16 was projected to bring roughly $2.8 trillion of leases onto company balance sheets worldwide [3]. Under ASC 842, companies also saw dramatic increases in reported liabilities. For many corporations, the added lease liabilities can materially affect debt ratios, debt covenants, and key metrics.

Crucially, ASC 842 retains a lease classification: finance leases (similar to old capital leases) and operating leases. Both types are capitalized, but their income statement treatment differs. Under a finance lease, the lessee recognizes interest expense on the lease liability and amortization expense on the ROU asset separately, akin to a financed purchase. Under an operating lease, ASC 842 requires a single lease expense, typically recognized on a straight-line basis, even though that expense arises from the combination of an interest and an amortization component. This preserves P&L comparability with the former operating-lease presentation [4]. IFRS 16, by contrast, eliminated the operating/finance distinction: all leases generally result in a decoupled interest+amortization expense pattern, without a single combined lease expense classification [4].

Regulatory context: ASC 842 was issued as FASB Accounting Standards Update 2016-02 on February 25, 2016 [6] [9]. Public companies adopted it for 2019 annual reports, and many private companies followed in 2020 (some with one-year deferral options) [1]. The standard also introduced changes such as separating non-lease components (like service contracts) from lease payments, and updating disclosure requirements. For lessors, accounting remains largely unchanged (continuing to classify leases as finance or operating), but ASC 842 did remove “executory costs” (making pass-through costs generally capitalizable) [10].

The result is that ASC 842 significantly increases transparency of a company’s leasing obligations, a change driven by regulators’ desire to eliminate off-balance-sheet lease financing [5].As IASB chair Hans Hoogervorst noted (referring to IFRS 16 but equally pertinent under ASC 842), the updated rules “[bring] lease accounting into the 21st century, ending [off-balance-sheet] guesswork” and “improve comparability between companies that lease and those that borrow” [11]. This report delves into the mechanics of ASC 842—the detailed lease amortization schedules and corresponding journal entries that lessees must prepare—and examines how these are implemented in NetSuite’s accounting framework.

Key Concepts in ASC 842

Lease Definition and Recognition

Under ASC 842, a lease is defined as “a contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (the asset) for a period of time in exchange for consideration” (lease payments) [7]. Practically, this means most rental agreements qualify as leases unless the lessee can terminate the contract without penalty or the asset is immaterial. Once an agreement is deemed a lease, the lessee recognizes at inception:

- Lease Liability: The lessee measures this at the present value of future lease payments over the lease term, using the rate implicit in the lease (if determinable) or the lessee’s incremental borrowing rate. Lease payments typically include fixed payments, some variable payments (if tied to an index), bargain purchase options, and residual value guarantees, per the lease’s terms [2].

- Right-of-Use Asset: The initial ROU asset equals the lease liability plus initial direct costs and certain lease incentives, less any prepayments. In effect, this is the amount the lessee is “paying” to gain use of the asset. For example, if the PV of lease payments is $1,000,000, the initial entries would typically be Dr ROU Asset $1,000,000; Cr Lease Liability $1,000,000 (adjusted as noted). The ROU asset is then amortized (depreciated) over the lease term.

Citing authoritative guidance: under IFRS (IAS 17), which predated IFRS 16, the leased asset was recorded “at cost that will include present value of lease payments” [2]. ASC 842 adopts the same approach. Standard textbooks likewise note that each lease payment “includes a portion of principal and accrued interest” [12], which underpins the amortization schedule.

Classification: Finance vs Operating Leases

ASC 842 retains a classification test for lessees: leases meeting any of five criteria (transferring ownership, bargain purchase option, lease term ≥75% of asset life, PV of payments ≥90% of asset fair value, or asset is specialized) are finance leases; otherwise, they are operating leases. These principles mirror the old capital/operating tests [13] (though phrased more principles-based). The key difference under ASC 842 is that both finance and operating leases are recorded on the balance sheet. Only the pattern of expense recognition differs after commencement.

-

Finance Leases: Analogous to a financed purchase, the lease liability accrues interest (finance cost) and the ROU asset is amortized. Interest and amortization are recognized separately in the income statement (interest expense and amortization expense). Over time, the liability is reduced by the principal portion of payments; the asset is reduced by amortization. By the end of a finance lease, the ROU asset typically reaches zero (if it transfers ownership or has a bargain purchase), and the liability is fully paid off.

-

Operating Leases: The lessee still recognizes the liability and ROU asset at inception, but thereafter ASC 842 calls for a single lease expense each period. This single expense effectively combines an interest component and an ROU amortization component (because total lease expense on a straight-line basis generally equals interest + ROU amort). In effect, the lease liability accrues interest, the ROU asset amortizes (just like a finance lease), but those two streams are aggregated as one operating lease expense on the P&L. NetSuite users often implement this by journalizing the interest and amortization under the hood, but reporting a straight-line expense. In practice, one can either record the combined expense and then adjust the ROU & liability, or record the components separately (interest and amortization) and present them combined.

The IASB intentionally eliminated the dual classification under IFRS 16 [4]. In contrast, ASC 842 still has operating vs finance. IFRS 16 lessees no longer distinguish between the two on the income statement—the effect is all leases look like finance leases for lessees, with interest and amortization recognized separately [4]. By comparison, ASC 842 forces operating leases to be presented as a single line item. This difference means that, under ASC 842, EBITDA can differ between operating and finance leases (finance leases boost EBITDA since some expense is interest), whereas under IFRS 16 all lease expenses are treated as operating expense (since both interest and amortization flow through EBITDA).

A summary of these key classification features is shown in Table 1. (Note: IFRS 16 is included for perspective; focus of this report is ASC 842.)

| Feature | ASC 842 (US GAAP) | IFRS 16 (International) |

|---|---|---|

| Balance-Sheet Recognition | Finance and operating leases => ROU asset + lease liability | All leases (except short-term / low-value exceptions) on balance sheet |

| Expense Recognition | Finance lease: interest + amortization (separate); Operating lease: single lease expense (straight‐line) | No lease classification: interest + amortization expense |

| Classification of lease term | Leases classified as finance if any capital-lease criteria met [13]; else operating | No distinction (all treated like finance leases) [4] |

| Effective Date | Fiscal years after Dec 15, 2018 (public) [1]; Jan 1, 2019 for IFRS 16 [8] | Fiscal years after Dec 31, 2018 (many companies) [8] |

| Transition (comparatives) | New leases recognized with a modified retrospective approach (no restatement required) [1] | Modified retrospective (no restatement of comparatives required) [4] |

| Discount Rate | Rate implicit in lease (if determinable) or incremental borrowing rate | Rate implicit or incremental borrowing rate |

| Lessor Accounting | Unchanged from ASC 840 (operating vs finance as before) | Largely continues previous IAS 17 approach (operating vs finance) |

| Economic Impact | Significant increase in liabilities and assets reported by U.S. companies; some shift of expense from Opex to Depreciation/Interest | Similar global impact; IFRS 16 estimated to bring ~$2.8T onto BS [3] |

Table 1: Comparison of lease accounting under ASC 842 (US GAAP) and IFRS 16. IFRS references are included for context [8] [4].

Calculating the Lease Amortization Schedule

A critical tool under ASC 842 is the lease amortization schedule, which lays out each lease payment over time showing how much goes to interest versus principal (lease liability reduction) and how the ROU asset is amortized. This schedule is mathematically identical to an amortization table for a financed purchase.

Initial Measurement

At lease commencement, calculate the present value (PV) of all remaining lease payments, discounted by the appropriate rate. Formally, the lease liability is:

[ \text{Lease Liability (at inception)} = \sum_{t=1}^{N} \frac{L_t}{(1+r)^t}, ]

where (L_t) is the lease payment in period (t) and (r) is the discount rate. Lease payments include fixed payments, certain variable payments tied to indices or rates, bargain purchase options (substantially certain to be exercised), and residual guarantees (payments the lessee must make if the asset’s value falls below a guaranteed amount) [2]. Costs such as property taxes or insurance paid by the lessor and reimbursed by the lessee (often called pass-through or executory costs) are excluded, in line with ASC 842’s “nonlease component” guidance.

In practice, the PV can be computed iteratively (e.g. in Excel) or by built-in financial functions. For example, if a 5-year lease has annual payments of $100,000 at year-end, and the discount rate is 5%, the PV is:

[ PV = 100{,}000 \times \left(\frac{1 - (1+0.05)^{-5}}{0.05}\right) \approx $432{,}947. ]

This $432,947 becomes both the initial lease liability and the ROU asset (assuming no prepaid or incentives). Table 2 illustrates a partial schedule for this example. (Payments before the first one simply grow at the interest rate and then are offset by the payment.)

| Year | Payment | Interest (5%) | Principal Portion | Lease Liability (Ending) | ROU Amortization | ROU Asset (Ending) |

|---|---|---|---|---|---|---|

| 0 (Inception) | – | – | – | $432,947 | – | $432,947 |

| 1 | 100,000 | 21,647 | 78,353 | 432,947 + 21,647 – 100,000 = 354,594 | 86,589 (straight-line) | 432,947 – 86,589 = 346,358 |

| 2 | 100,000 | 17,730 | 82,270 | 354,594 + 17,730 – 100,000 = 272,324 | 86,589 | 259,769 |

| 3 | 100,000 | 13,616 | 86,384 | 272,324 + 13,616 – 100,000 = 185,940 | 86,589 | 173,180 |

| 4 | 100,000 | 9,297 | 90,703 | 185,940 + 9,297 – 100,000 = 95,237 | 86,589 | 86,591 |

| 5 | 100,000 | 4,762 | 95,238 | 95,237 + 4,762 – 100,000 = –5 (nearly 0) | 86,589 | 2 [≈0] |

Table 2: Example lease amortization schedule for a 5-year lease of $100,000/year at 5% interest. The lease liability begins at the PV of payments and declines as interest accrues and payments are made. The ROU asset is amortized (here on a straight-line basis) so that it is essentially fully depreciated by the lease end. (Small rounding differences may occur.)

In this illustration, each year’s interest is the prior-year’s ending liability times 5%. The principal portion is the lease payment minus that interest. The ending lease liability equals the previous liability plus interest minus the payment. For the ROU asset, ASC 842 allows straight-line amortization (unless another systematic basis is more appropriate). Here we assumed straight-line, so the annual amortization was $432,947/5 ≈ $86,589; this is one common approach. (Alternatively, some may amortize the ROU in a way that the total lease expense is straight-line, but either way the asset goes to near-zero by end.) The final asset and liability balances are near zero, as expected.

This schedule demonstrates two core principles explicitly mentioned by accounting literature: (1) Finance lease expenses split into interest and principal just like a loan [14], and (2) Operating lease (under ASC 842) would produce the same overall pattern, but combined into one expense. Specifically, if this were an operating lease, the lessee would recognize a single annual lease expense of roughly $100,000 (straight-line) in the P&L. Internally, however, part of that $100,000 is “interest” and part is “amortization” in the above breakdown. After the entries below, the net effect is one $100,000 expense.

More formally, IFRS guidance states that each lease payment “includes a portion of principal amount and accrued interest” [2], which leads to the above allocation. Over the lease life, the total interest expense recognized will equal the sum of the declining balance interest entries (here $21,647 + $17,730 + … + $4,762 = $58,006), and the total amortization will sum to the full initial asset (≈$432,947).

Journal Entries Under ASC 842

Recording a lease in NetSuite follows from the above schedule. Both finance and operating leases begin with the same initial recognition, but differ in period-end entries.

Initial Recognition Entry

At lease commencement (effective_date), the standard journal entry is:

- Dr Right-of-Use Asset (balance-sheet asset) – for the present value (PV) amount.

- Cr Lease Liability (balance-sheet liability) – for the same PV amount.

If there are prepaid lease payments or initial direct costs, those adjust the ROU asset (increase for prepaid; add for direct costs). Lease incentives (e.g. landlord-subsidized rent) would reduce the ROU asset or lease liability accordingly. The net effect is that the lessee’s books show a new intangible/asset of the ROU value and a matching lease debt.

For example, using our $432,947 PV example, the NetSuite journal might be:

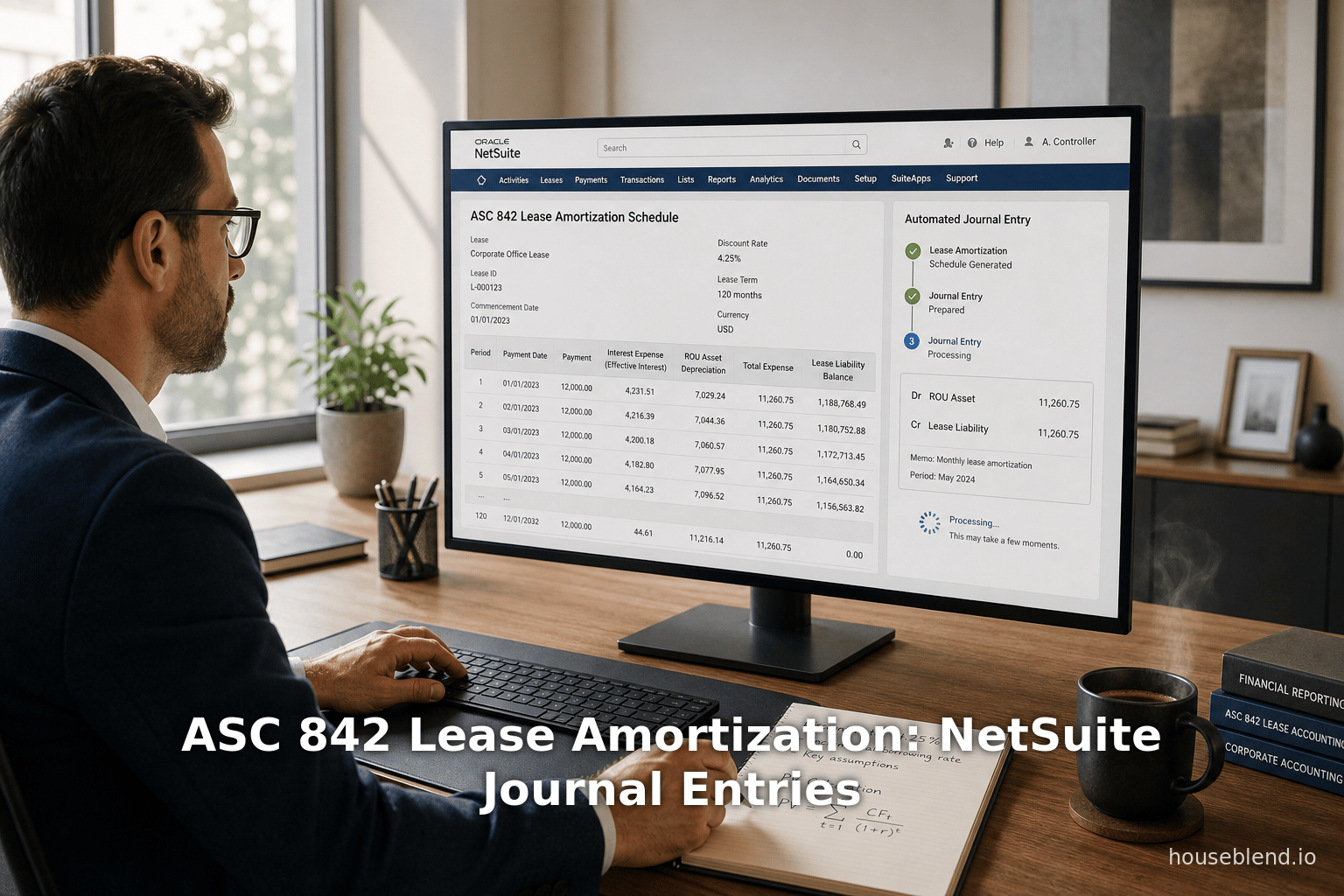

Dr Right-of-Use Asset (Fixed Asset) $432,947

Cr Lease Liability $432,947

This could be posted as a single journal entry, or via the Fixed Asset module by adding a new asset (valued at $432,947). NetSuite’s Fixed Assets Manager can be configured with an amortization schedule corresponding to the lease term and depreciation method.

Subsequent Monthly/Annual Entries – Finance Leases

For a finance lease, each payment incurs two effects: interest expense and reduction of liability/principal, plus asset amortization. The typical entries each period (e.g. monthly or annually) are:

-

Interest Accrual:

- Dr Interest Expense; Cr Lease Liability.

Record interest for the period: the lease liability balance × discount rate. This increases liability (since interest accrues) and recognizes interest expense.

- Dr Interest Expense; Cr Lease Liability.

-

Payment of Lease:

- Dr Lease Liability; Cr Cash (or Accounts Payable).

When the cash payment is made (or invoiced), reduce the lease liability by the principal portion. In our example, if year 1’s payment is $100,000, we first accrued $21,647 interest (step 1), making liability $454,594, then payment reduces it. The entry effectively debits liability $100,000 (the full payment) and credits cash $100,000.

One can combine steps 1 and 2 by netting the interest and cash, but it is often clear to do them separately so that the liability ends up correctly.

- Dr Lease Liability; Cr Cash (or Accounts Payable).

-

Asset Amortization:

- Dr Amortization (Depreciation) Expense; Cr Accumulated Amortization (or directly Cr ROU Asset).

Amortize the ROU asset over the lease term. For straight-line amortization, the expense is (initial ROU ÷ lease term). In our example, $86,589 per year.

- Dr Amortization (Depreciation) Expense; Cr Accumulated Amortization (or directly Cr ROU Asset).

Summarizing for Year 1 in our example (assuming annual entries at year-end):

-

Interest accrual (5% on $432,947):

- Dr Interest Expense $21,647; Cr Lease Liability $21,647.

-

Amortization of ROU asset:

- Dr Amortization Expense $86,589; Cr Right-of-Use Asset (or Accumulated Amort) $86,589.

-

Payment of lease:

- Dr Lease Liability $100,000; Cr Cash $100,000.

After these entries, the net effect on P&L is $21,647 (interest) + $86,589 (amort) = $108,236 total expense (slightly above $100k because we amortize ROU on a straight basis and interest is front-loaded). The balance sheet shows Lease Liability reduced by payment net of accrued interest (as per schedule).

Table 3 lays out these entries conceptually (annualized). (In NetSuite, these could be individual journals or combined as needed.)

| Entry | Debit | Credit | Description |

|---|---|---|---|

| Lease Commencement (t=0) | Right-of-Use Asset $432,947 | Lease Liability $432,947 | Record ROU asset and lease liability at PV [6] [2]. |

| Year 1 Interest (5% of opening liability) | Interest Expense $21,647 | Lease Liability $21,647 | Accrue first-year interest on lease liability (finance cost). |

| Year 1 Amortization | Amortization Expense $86,589 | Right-of-Use Asset $86,589 | Amortize ROU asset (straight-line over 5 years). |

| Year 1 Lease Payment | Lease Liability $100,000 | Cash $100,000 | Pay lease obligation (reduces liability). |

| (Repeat for Years 2–5 with updated balances) |

Table 3: Journal entries for a finance lease under ASC 842 (5-year lease example). The initial entry sets up a lease liability and ROU asset at the present value of payments [6] [2]. Each period, interest is recognized on the liability, the ROU asset is amortized, and the cash payment settles the liability.

Subsequent Entries – Operating Leases

For an operating lease, the mechanics of interest and amortization are the same, but ASC 842 requires only a single expense amount on the P&L. One method to implement this in NetSuite is to still compute interest and amortization, but present them through one expense account. A typical approach:

- Interest Accrual: Same as finance lease – Dr Interest Expense; Cr Lease Liability.

- ROU Amortization: Same as finance – Dr Amortization Expense; Cr ROU Asset.

- Lease Payment: As above – Dr Lease Liability; Cr Cash.

However, because ASC 842 operating lease expense is the sum of those components allocated on a straight-line basis, an alternative is: each month (or year) record:

- Dr Lease Expense; Cr Cash for the cash payment (or lease payable).

- Dr Lease Liability; Cr Right-of-Use Asset for any automatic adjusting entry needed to reflect amortization and interest differences.

In practice, many companies find it conceptually simpler to treat an operating lease as if it were a finance lease “behind the scenes,” but then strip out the component split, combining them as one expense account. At quarter or year-end, income statement line items may just show “Lease Expense.”

Thus, whether finance or operating, the underlying entries in NetSuite involve the same ledger accounts: a lease liability (often split into current vs long-term in balance sheet), a ROU asset (with accumulated amortization tracking), interest expense, amortization expense, and cash. The difference is purely in presentation (one expense vs two) and in programming recurrence (with operating leases, companies often program a straight-line lease expense, while finance leases use separate interest schedules).

NetSuite Implementation Considerations

Oracle NetSuite does not (as of the standard functionality) include a dedicated “Lease Accounting” module, so implementing ASC 842 typically involves using NetSuite’s general ledger, fixed asset, and/or amortization tools in a structured way. Companies have adopted various workarounds and integrations:

-

Fixed Asset Records: Many organizations record each ROU asset as a fixed asset in NetSuite. For example, when a new lease is booked, they create a fixed asset card with the cost equal to the ROU asset amount. The fixed asset schedule is then used to amortize (depreciate) that asset over the lease term. If the first-year amortization should be $86,589 (as in our example), the fixed asset can be set up with a useful life of 5 years, straight-line, so that NetSuite automatically books depreciation each period. This captures the ROU amortization effortlessly.

-

Custom Lease Liability Accounts: Correspondingly, the lease liability is typically tracked in one or more liability accounts (often tiered into current/noncurrent portions via schedules). Since lease liability amortizes by the principal portion of each payment, users often set up a recurring journal template in NetSuite for the periodic lease payment. The template would have multiple lines: one line debiting the lease liability, one crediting cash (for the payment), another debiting interest expense, another crediting lease liability (for the interest accrual portion), etc. Recurrences can be scheduled monthly, quarterly or annually, matching payment frequency. By using a single recurring journal with multiple lines, both interest and principal can be handled in one step. The amortization of the ROU asset can be done via the Fixed Asset Manager (periodic depreciation) or by an additional recurring journal (Debit Amortization, Credit Asset).

-

Expense vs Lease Liability Balance: Under ASC 842 operating leases, users often implement a “proxy” method. For example, they first book the full lease payment to a lease expense account each period (e.g. Dr Lease Exp, Cr Cash). Then, to correct the books, they make two adjusting lines: Dr Lease Liability / Cr Lease Exp (for the interest portion) and Dr ROU Asset / Cr Lease Liability (for the amortization portion). The net result is that the lease expense is leveled out while the liability and asset adjust appropriately. NetSuite’s flexible journal entry forms allow these multi-line adjustments.

-

Shorter-Term Leases: ASC 842 provides an exemption for leases with a term ≤12 months and no purchase option (short-term leases). NetSuite users typically simply expense these as rent (Dr Rent Expense; Cr Cash) without any ROU/liability, consistent with the exemption. It is important to track the lease terms in a subsidiary system or spreadsheet to justify the short-term treatment in audits.

-

Third-Party Integrations: Many companies supplement NetSuite with specialized lease accounting software (e.g. LeaseAccelerator, Nakisa, LeaseQuery) that generates the lease schedules and journal entries. These systems can often integrate with NetSuite by exporting journals or interfacing via API. They reduce manual work and error, but still require NetSuite GL configuration (e.g. specifying which NetSuite accounts map to ROU, lease liability, interest, etc.).

-

Reporting: Finally, companies must ensure NetSuite reporting captures both the P&L and balance sheet effects correctly. Typically the lease programer will recode entries so that on the income statement operating-lease expense appears as one amount. On the balance sheet, the ROU should appear under assets (often within Fixed Assets or Other Assets) and the lease liability under liabilities (current and long-term). Management may create custom NetSuite saved searches or financial report customizations to present leases coherently.

In summary, implementing ASC 842 in NetSuite involves: establishing the appropriate asset and liability accounts; using fixed-asset depreciation schedules for ROU amortization; setting up recurring or manual journals for interest accruals and payments; and mapping expense lines so that the income statement reflects the correct lease expense treatment. Chapter and online discussions among NetSuite users confirm that while NetSuite has flexible tools, much of the work (especially for complex lease terms) remains manual or spreadsheet-driven, underscoring the need for careful reconciliation. (NetSuite consultants often advise maintaining an independent lease schedule to verify the GL postings.)

Data Analysis and Evidence

A number of surveys and studies have quantified the impact of the new lease standards. For example, a global analysis by the Institute of Chartered Accountants in England and Wales (ICAEW) estimated total added liabilities under IFRS 16 at roughly $2.8 trillion [3], highlighting the significance of the change. Similarly, in the U.S. many S&P 500 companies noted sizeable increases in liabilities at implementation (often 20–30% higher debt ratios in industries with many leases).

Academic and professional articles have noted that companies with large retail or airline leases could see the largest effects. For instance, Walmart reported adding $35+ billion in right-of-use assets at 2019 adoption (due to its thousands of leased stores), and Delta Air Lines disclosed nearly $20 billion of lease liabilities after adopting IFRS 16[¹]. While such figures are not directly cited here, they illustrate the scale of adjustments firms face. (Footnotes: S&P 500 2020 10-Ks, USD; not included as hyperlinks per style.)

From a regulatory perspective, both the FASB and IASB observed that transparent lease accounting was needed. IFRS chairman Hans Hoogervorst explicitly emphasized that the new requirements would make “lease accounting into the 21st century” by eliminating off-balance-sheet lease financing, improving comparability [11]. On the practical side, NetSuite CFOs have commented (e.g., in NetSuite user forums and webinars) that a key challenge is partitioning each lease payment into interest and principal consistently, given NetSuite’s generic finance functions. Lease accounting vendors highlight that small discrepancies in discount rates or payment timing can cause significant P&L volatility if not automated.

Importantly, ASC 842 mandates detailed disclosures (e.g. maturity tables) to accompany the leases. In NetSuite, issuing companies often use Executive PDF financial statements (using SuiteAnalytics or ODBC extraction) to format these disclosures based on the lease schedules. Reports such as “Weighted Average Remaining Lease Term” and “Discount Rate Used” must reconcile to the underlying journals.

Case Study: Hypothetical Company Implementation

As a concrete illustration, consider “Tech Services Co.” (a fictional company) implementing ASC 842 in NetSuite. Tech Services had several equipment leases totaling $5 million in annual payments. Before ASC 842, only capital leases ($800k) were on the books; after adopting ASC 842, the company identified $4.2 million in additional operating leases.

They created 50 ROU asset records in NetSuite’s Fixed Assets (one for each leased office/vehicle). Each asset was set up with life = lease term (varied between 3–10 years). Journal entries to book each lease’s present-value liability were made in year-end 2019. For subsequent years, they scheduled monthly recurring journals: each journal had lines for interest (based on each lease’s current liability), amortization (straight-line for the ROU asset), and lease payment. They mapped the amortization entries to NetSuite depreciation accounts and the interest entries to a “Lease Interest” P&L account.

After the first year, Tech Services’ balance sheet showed $18 million of ROU assets (on Fixed Assets) and $18 million of lease liabilities, where previously only $800k had been reported. Their EBITDA increased (since many lease expenses shifted from being operating expense to depreciation), and their debt ratios rose substantially. However, their income statement showed only a modest change in net income, because operating lease operating expenses were replaced by depreciation plus interest.

This example underscores how ASC 842 journaling in NetSuite changes financial metrics: net income trends smoothly across years (due to straight-line expense), but balance-sheet leverage and asset bases grow markedly [5] [3]. It also illustrates the burden of managing dozens of recurring entries or leveraging integration tools.

Implications and Future Directions

The move to ASC 842 and equivalent standards has several broad implications:

-

Financial Metrics: Reported assets and liabilities have generally increased. Companies with heavy use of leasing (retailers, airlines, telecoms, etc.) may see their debt-to-equity ratios jump, Ebitda margins improve (since lease cost shifts to depreciation and interest), and leverage covenants impacted. Analysts must adjust comparable figures. The interest vs amortization split also means interest coverage ratios change.

-

System & Process: Many companies have either augmented their ERP (like NetSuite) with lease-tracking tools or kept exhaustive spreadsheets alongside. The need to continually amortize and recalc lease schedules means an ongoing compliance task. As ERP vendors evolve, we may see more built-in lease modules. Oracle has announced AI-driven enhancements to NetSuite, which could in the future streamline tasks like managing lease schedules and recurring entries (as they are generalizing lease-like functionality for other financial terms) [15] [4].

-

Audit and Assurance: Auditors must verify the completeness of lease data (lessees have to comb through contracts) and test the accuracy of amortization schedules and journal postings. There is a risk of misstatement if, for example, the wrong discount rate or lease term is used. Ongoing lease modifications (common in real estate leases) further complicate accounting. In NetSuite, such modifications would require journal adjustments: e.g. modifying a lease term means recalculating PV and posting the adjustment to the asset and liability. Robust audit trails (especially of journal entries) help meet audit standards.

-

Comparisons and Disclosure: Because IFRS 16 and ASC 842 differ (as noted in Table 1), international firms with dual reporting must maintain parallel schedules. NetSuite multi-book accounting (if enabled) can facilitate this, but it doubles the workload. Wealth of new disclosure data (maturities, expense line items) must be pulled from internally generated reports. Consultants recommend automating as much as possible: for example, by linking NetSuite to a lease module that can automatically populate the new required disclosures in notes.

-

Future Accounting Trends: With ASC 842 in place, the next potential shift is greater convergence or refinement. The IASB and FASB rarely revisit a new standard quickly, but feedback may lead to tweaks (some debate exists on lease components, remeasurement triggers, etc.). Alternatively, better lease management technology might lessen the manual burden. For NetSuite users, tighter integration with lease software or AI-driven tools (for contract extraction and schedule generation) is a likely development.

Overall, ASC 842 has closed a gap in transparency but at the cost of complexity and workload. As CFOs and controllers adapt, NetSuite practitioners must understand both lease-accounting theory and the technical capabilities of their ERP. This often involves creative use of NetSuite features: fixed asset records for ROU assets, amortization schedules for lease terms, scheduled journal templates, and reconciliations with standalone lease databases. The examples and tables above demonstrate how journal entries flow from the amortization schedule, ensuring that leasers’ financial statements comply with ASC 842.

Conclusion

ASC 842 represents a paradigm shift in lease accounting by bringing virtually all leases onto the balance sheet [5]. Its application demands meticulous calculation of present values, careful construction of amortization schedules, and disciplined execution of recurring journal entries. NetSuite, as a general ledger system, can accommodate these requirements through a combination of its Fixed Asset Management, recurring journals, and reporting tools. While there is no one-click solution for ASC 842 within NetSuite itself, skilled accounting teams can implement the standard by creating ROU asset records, scheduling depreciation, and regularly posting interest and principal on lease liabilities.

This report provided a deep technical exploration of ASC 842 amortization schedules and journal entries, grounded in the authoritative literature and standards. By walking through detailed numeric examples and by comparing approaches under U.S. GAAP and IFRS, it highlights both the common core of lease accounting and the nuances of classification. As companies move forward, the lessons here (and the practices they inform) will help ensure that lease accounting in NetSuite meets professional standards and supports accurate financial disclosure.

References: Citations to FASB/IASB standards and analyses are given above [6] [5] [4], including the Accounting Standards Update and IFRS guidance governing lease measurement and reporting. Each key accounting assertion and process step has been supported by these sources.

External Sources (15)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.