Houseblend Article

Big Four vs Boutique NetSuite Implementation Partners

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 031. ERP Consulting Landscape: Big Four and Boutique

- 042. The NetSuite Partner Ecosystem

- 053. Big Four/Major Integrators: Capabilities and Considerations

- 064. Boutique and Specialist NetSuite Consultants

- 075. CFO Decision Criteria: Cost, Time, Risk, and Value

- 086. Comparative Analysis and Decision Tables

- 097. Case Studies and Examples

- 108. Implications and Future Directions

- 11Conclusion

Executive Summary

This report provides a comprehensive framework for Private Equity–backed CFOs to decide between engaging a Big Four (or global systems integrator) versus a boutique NetSuite implementation partner. It synthesizes industry data, expert analyses, and case studies to illuminate the trade-offs involved. The key findings are:

-

Market Context: The cloud ERP market is large and rapidly growing (projected ~$73B in 2025 [1]), with Oracle/NetSuite commanding a significant share (over 41,000 customers as of 2024 [2]). High-performance firms (92% of successful SMBs) rely extensively on ERP systems [3], and NetSuite’s SaaS model allows very fast deployments (often ~100 days) [4]. PE investment in technology is on the rise (PE deal volume hit a two-year high of ~$196B in Q2 2024 [5]), driving many portfolio companies to modernize legacy platforms.

-

Failure Risk & the Importance of Expertise: ERP projects are complex and failure-prone: industry benchmarks (Gartner) cite failure rates of 55–75% when objectives are unmet [6]. This underscores the CFO’s need to choose an experienced, accountable partner. Studies show that engaging skilled consultants dramatically improves outcomes – for example, 85% of organizations complete NetSuite projects successfully when assisted by experienced consultants [7], versus much higher failure rates otherwise. Thorough planning also correlates with ROI (83% of companies hit ROI targets with detailed prerequirements work [7]).

-

Big Four (Global SI) vs. Boutique Consultancies: The Big Four (Deloitte, PwC, EY, KPMG) and other “Tier-1” integrators offer scale, global reach, and established processes. They excel at large, multi-subsidiary projects requiring broad services, and bring brand prestige that boards trust [8] [9]. However, their advantages come with drawbacks: high cost, more rigid methodologies, frequent staff turnover on projects, and potential lack of flexibility [8] [10]. Boutiques and mid-market partners, by contrast, provide specialized NetSuite and industry expertise, hands-on senior involvement, and lower overhead costs. They tend to deliver better price-to-value ratios, faster response times, and personalized service [10] [11]. Industry analyses highlight that boutique firms achieve 30–60% lower cost and ~43% faster turnaround in CRM/ERP projects compared to global SIs [11], due to lean teams and avoidance of “delivery factory” approaches.

-

Factors for CFO Decision: Based on multiple analyses, a decision framework emerges. If the NetSuite project is very large, global, compliance-heavy, and failure intolerable, the CFO should lean toward a Big Four or large alliance partner. These partners offer deep process rigor, governance (steering committees, documented approvals), and the ability to escalate issues internally [12] [13]. But if the project scope is well-defined and limited in complexity, with an internal project team capable of governance, a specialized NetSuite consultant is often better. Boutiques excel when speed, agility, and cost efficiency are paramount, and when the CFO is comfortable trading some process overhead for lower fees [12] [14]. This dichotomy is illustrated in practice: one case study saw a PE-backed $2B company reject proposals from two Big Four firms and instead hire a boutique because it delivered “greater on-the-ground experience from day one” at a much lower price point [15].

-

Cost and ROI Considerations: Proposals can vary widely in scope and price. For instance, one analysis found a NetSuite reseller quoting $425K for a full-team implementation, versus $180K from a boutique specialist for the same requirements [16]. This discrepancy often reflects different deliverables: the higher-priced bid included full PMO, QA, and support coverage, whereas the low bid was largely the work of a single senior expert [16]. CFOs must parse these proposals carefully, assessing what each partner actually offers in terms of risk mitigation, accountability, and post-go-live support [16] [17]. The higher cost of Big Four projects (often $250–300/hour) often buys meticulous process and access to executive sponsorship from NetSuite [12] [18], whereas boutique firms typically charge $125–175/hour [14] and deliver lean, senior-led engagements. ROI analysis generally shows that even if big partners reduce execution risk, the total cost may delay breakeven. In one modeled scenario, a mid-market roll-up on NetSuite cost $560K in implementation expenses, yielding annual synergies of about $470K (breakeven ~1.5 years) [19] [20].

-

Case Studies & Examples: Real-world cases underscore the framework.For example, a PE roll-up of six companies consolidated onto NetSuite in 18 weeks for $560K, achieving $470K/year in cost synergies [19] [20]. In this case, the portfolio chose NetSuite and fast deployment over an outdated SAP system because the SAP upgrade would have required 12 extra months and $500K [21]. In another case, a global conglomerate (with five operating companies) had its Big Four audit partner recommend a NetSuite rollout but ultimately selected a boutique implementation team. The CFO revealed that the specialist offered “significantly greater on-the-ground experience from day one – and at a highly competitive price point.” [15] This highlights how boutique firms can win PE-sponsored engagements when they match the technical and business needs efficiently at lower cost.

-

CFO and PE Strategic Priorities: For PE-backed firms, CFOs focus on value creation and exit readiness. Modern ERPs like NetSuite enhance valuation by streamlining reporting and enabling roll-ups. Indeed, 56% of PE investors anticipate a >10% valuation hit if a portfolio’s ERP is outdated [22]. Leading advisors (BCG, EY, etc.) stress that ERP transformation should be approached as strategic value creation, not an IT luxury [23] [22]. CFOs must therefore weigh the total cost of ownership: not only the implementation bill, but the longer-term benefits of faster closings, better auditability, and integration capabilities. Data shows well-executed ERP projects can generate substantial returns (one estimate suggests a 10–20% lift on equity returns [24]). Conversely, project delays and failures erode PE value.

-

Implications and Future Outlook: The consulting landscape continues to evolve. Boutiques are proliferating (often founded by former Big Four veterans) and innovating with flexible delivery models [25] [26]. Meanwhile, Big Four firms are expanding their NetSuite practices, incorporating advanced tools (AI-driven accelerators) and broader service bundles [27]. CFOs should anticipate an increasingly hybrid ecosystem: large global projects may still merit Big Four involvement, but many mid-market roll-ups and functional upgrades will likely favor specialized partners or even nearshore teams. Emerging technologies (e.g. generative AI for finance, advanced analytics) and rising compliance demands will further shape partner selection — for instance, boutique firms often offer niche expertise (industry templates, CFO-level analytics) that global players may lack. On the other hand, CFOs also must manage long-term risk: smaller implementers can offer fast wins, but continuity of support post-go-live may require arranging managed services or building in knowledge transfer.

In summary, our PE-backed CFO Decision Framework emphasizes a balanced analysis of project complexity, budget, timeline, and risk tolerance. It does not say “Big Four good, boutique bad” or vice versa; instead, it prescribes choosing the partner category that aligns with strategic needs. We conclude with concrete recommendations and tables to aid CFOs in mapping their specific situation to the appropriate partner model. All claims and data below are drawn from industry reports, expert analyses, and documented case studies.

Introduction and Background

Enterprise Resource Planning (ERP) systems are the cornerstone of modern corporate finance and operations. For private equity (PE)–backed companies, ERP transformations are often urgent: PE firms typically target operational improvement for value creation, and fragmented or outdated financial systems can bottleneck growth and return. Recent data indicates the global ERP market was about $66B in 2024, growing ~11% annually [1]. Cloud-based ERP now constitutes roughly 70% of the market and is growing ~14.5% per year (versus 2% for on-prem) [28]. Oracle/NetSuite is a major force in this shift: in 2024 it was part of Oracle’s $8.7B ERP revenue, with NetSuite alone serving 41,000+ customers and growing 25% annually [2]. Notably, about 80% of NetSuite’s users are small-to-mid-size businesses (Source: www.anchorgroup.tech), making it a natural choice for mid-market PE portfolio companies.

Private Equity Context: The private equity industry has recently been more active than ever (2024 saw record deal volumes after the pandemic lull) [5]. A common PE strategy is “buy-and-build”: acquiring add-on companies and rolling them up onto a unified platform. A robust, scalable finance system is thus critical to integrate new acquisitions quickly. One blog by a NetSuite executive notes that PE firms invested $159 billion in Q2 2024, “the most in two years” [29], underscoring how many portfolio companies may be dealing with growth and integration mandates. Similarly, BCG observes that 56% of PE professionals expect a >10% valuation haircut if a portfolio company’s ERP is outdated [22]. In short, ERP decisions for PE CFOs can have material impact on corporate value and exit readiness.

The CIO/CFO Imperative: Industry experts stress that an ERP selection is no longer merely an IT vendor choice but a finance-led, strategic transformation [30]. PE CFOs are increasingly framing ERP projects as “value creation” initiatives rather than technical projects. They demand clarity on benefits – faster closes, better cash control, auditability – all of which support stronger EBITDA performance [31]. This has led to the coining of phrases like “ERP as a value creation tool [31]” and the notion that CFOs must own the process, aligning stakeholders and selecting partners who drive outcomes (not just deliver software).

Given this backdrop, the partner selection becomes crucial. Oracle/NetSuite provides an ecosystem of partners (referred to as Solution Providers, Alliance Partners, BPO partners, etc.); but within that, companies face a choice between large, multi-discipline firms (often the Big Four and global SIs) and smaller specialist consultancies. This report focuses on that Big Four vs. Boutique decision, tailored with a PE-backed CFO’s priorities in mind.

To set the stage, we first survey the ERP consulting landscape, natural tensions between large and small partners, and specific NetSuite ecosystem structures. Then we turn to the CFO perspective: risk, cost, ROI, and PE value-creation goals. We draw on multiple sources – including consulting firm studies, NetSuite ecosystem analyses, and actual project anecdotes – to provide evidence-based guidance. The rest of the report is organized as follows:

- Section 1: ERP Consulting Landscape – Overview of Big Four/global SIs and boutique consultancies in ERP implementations, including trends and vendor roles.

- Section 2: NetSuite Partner Ecosystem – How NetSuite classifies partners (Solution Providers vs Alliance vs BPO) and examples of Big vs boutique in that ecosystem.

- Section 3: Big Four Consultancies – Capabilities & Challenges – Deep dive into the strengths and weaknesses of Big Four firms when serving Netsuite (and ERP) clients.

- Section 4: Boutique Consultancies – Capabilities & Advantages – Examination of specialized NetSuite partners and what they bring, vs what they may lack.

- Section 5: CFO Decision Criteria – Key factors (cost, time, risk, domain expertise) a PE-backed CFO should weigh in partner evaluation, with data and quotes.

- Section 6: Comparative Analysis & Tables – Tabular comparison (Big4 vs Boutique) and a decision-framework table (project scenarios vs partner type), synthesizing the above.

- Section 7: Case Studies – Real-world examples showing outcomes with different selections (PE roll-ups, mid-market vs enterprise).

- Section 8: Implications and Future Outlook – Discussion of emerging trends (AI, managed services, vendor evolution) and how they affect future partner choices.

- Conclusion – Final recommendations summarizing the framework.

All claims and figures are backed by citations to credible industry sources (white papers, consulting publications, market research) and relevant examples. This report aims to equip a PE CFO with an evidence-based, nuanced framework for choosing the right NetSuite implementation partner for their unique situation.

1. ERP Consulting Landscape: Big Four and Boutique

The ERP consulting market has long been dominated by a handful of large professional services firms (“Big Four” accounting/consulting firms and global SIs) and tiered ERP specialists. However, recent years have seen a pronounced shift. Digital transformation complexity and mid-market growth have opened the door for boutique and mid-size consultancies with deep niche expertise. Industry commentators note that “the ERP consulting landscape is undergoing a notable transformation,” with agile boutique firms gaining traction at the expense of the traditional dominance of Big Four firms [32].

Eric Kimberling of ThirdStage Consulting has written extensively on this trend. He observes that boutique ERP consultancies (often 100% focused on a particular platform or vertical) are appealing because they offer highly specialized knowledge and flexibility in addressing complex requirements [10]. In particular, boutiques often have lower overhead and more senior staffing, which translates to a better price-to-value ratio than giant firms [10] [33]. They can quickly adapt to client needs and may have deeper expertise on specific modules or industry processes. By contrast, Big Four and other global SIs bring weight and process rigor but can be less nimble.

However, there are trade-offs. Big Four firms’ sheer scale and reputation make them the default choice for large public companies. Kimberling notes that boards and C-level executives often feel more comfortable entrusting major ERP programs to well-known global firms, which continue to secure high-profile projects [34]. The Big Four guarantee a certain level of professionalism and have extensive resources to staff large, multi-country engagements. They also have long-standing relationships with ERP vendors (sometimes even selling licenses) and can integrate ERP work with broader services (tax, audit, strategy).

Nevertheless, drawbacks of Big Four approaches have become apparent. A common criticism is high turnover of project staff: large firms often rotate resources off projects, causing knowledge gaps and delays [8]. Their large teams and hierarchical structures can lead to processes and communication that are too rigid or slow-moving for fast-paced projects [8]. In many cases, Big Four SIs rely on subcontractors or offshore resources to control costs, which can dilute accountability. By contrast, boutique firms typically boast lean teams where senior experts remain closely involved throughout the engagement [35] [33]. (One analysis notes that boutique firms stake much on reputation and referrals, making them obsessively accountable for success [36].)

Other industry voices echo similar themes. The suite of ERP MetaFrontier analyses and case studies suggest that smaller, specialized firms often win on signaling value-driven delivery: they “take a more customized approach… to tailor solutions to specific problems” [26] and embed experienced consultants who “stay closely involved” in each phase [35]. By comparison, large integrators may bring standardized frameworks and a platoon of junior staff, which is efficient at scale but can overshoot the needs of a mid-market client.

These differences impact CFO decisions for NetSuite projects specifically. For NetSuite – a SaaS cloud ERP targeting high-growth midmarket companies – the affiliaton with Oracle means the shared partner ecosystem (Solution Providers, Alliance partners) includes both Big Four & scale-up players (often Tier 1) and many boutique specialists. NetSuite actively promotes its partner tiers: e.g. “5-Star” partners (like Deloitte, RSM, Protiviti) versus Gold/Silver or niche implementers. A Houseblend analysis categorizes partners: Solution Providers (license sellers/resellers) who range from global (5-star) to smaller (3-4 star), and Alliance Partners (implementation-only firms) which include both large SIs and niche specialists [37] [38]. For example, all 5-star Solution Providers are NetSuite-vetted and typically large teams, whereas 3–4 star providers are often more boutique-oriented and mid-market focused [39]. Thus, even within the NetSuite ecosystem there is a formal recognition of both large and small players.

Overall, the consulting landscape stands at an inflection point: enterprise clients have new options and must choose not just which ERP to implement, but who should implement it. In the next sections, we dissect what distinguishes Big Four-type partners from boutique NetSuite specialists, to ground the CFO’s decision framework.

2. The NetSuite Partner Ecosystem

Oracle NetSuite maintains a structured partner ecosystem to cover licensing, implementation, and operations services. Understanding these partner roles is important context for any ERP project. The main partner categories are:

-

Solution Providers: Authorized resellers who sell NetSuite licenses and offer full implementation services. They are tiered by a “Star” rating (5-Star down to 1-Star). Higher-star providers have demonstrated scale and success; they often include large regional/global firms. Lower-star Solution Providers may be smaller, more specialized shops [37]. For example, 5-Star Solution Providers typically have large teams and extensive track records, whereas 3/4-Star partners are usually boutique firms that cater to mid-market customers [39]. All are pre-vetted by NetSuite and must maintain certifications.

-

Alliance (SI) Partners: Consulting firms that exclusively implement and customize NetSuite, but do not sell licenses. NetSuite direct-sales handles licensing, while Alliance partners bring the technical/project skills. These range from large global systems integrators to niche specialists with deep industry expertise [38]. NetSuite highlights that Alliance partners provide “specific industry expertise” and best practices, often yielding faster ROI and better outcomes [40]. In practice, many Big Four practices (e.g. Deloitte’s NetSuite team) function essentially as Alliance partners, covering implementation for clients who obtain software through NetSuite’s sales channel.

-

BPO Partners: Firms that use a shared NetSuite instance to provide managed back-office services (accounting, payroll, inventory, etc.) as a service [41]. This is relevant post-implementation, particularly for mid-sized clients who want outsource capability.

For the CFO deciding between Big Four and boutique in NetSuite projects, the most relevant are the Alliance/Solution Providers (implementation consultants) and secondarily the question of ongoing managed services. The Big Four and other global firms typically slot into the top tiers of these categories. For example, Houseblend’s “Leading Consultants” article highlights that Deloitte is a leading NetSuite global partner for enterprise clients [42], and that PwC actively sells its own NetSuite-focused transformation group to high-growth firms (including those in private equity) [43] [44]. At the same time, many boutique firms (like HouseBlend, Bryant Park, or smaller regional partners) are certified as Solution or Alliance partners, focusing purely on implementation and optimization.

Because both Big Four and boutiques operate within the same Netsuite partner framework, the CFO essentially chooses which type of partner to engage under this ecosystem. The next sections examine each category’s characteristics in more detail.

3. Big Four/Major Integrators: Capabilities and Considerations

Scale and Breadth: Big Four and comparable global SIs (e.g. Accenture, Capgemini) bring vast resources. They are “designed for . . . broad deployment” [9]. Deloitte, for instance, touts multi-country rollout capabilities, extensive industry templates, and global NetSuite consultant networks [45] [46]. They often have offices in dozens of countries, which simplifies international coordination [9]. Their client teams can scale rapidly by pulling in specialists (e.g. tax experts, change managers) from within the firm when needed. For very large projects (merging dozens of companies or consolidating ERP globally), this resource pool is a major advantage. For example, Houseblend’s profile of Deloitte notes its ability to handle “complex, multi-national deployments” and to offer end-to-end services that combine ERP rollouts with finance process redesign, tax alignment, and change management [47] [48].

Breadth of Services: Big Four firms offer a one-stop-shop for everything from strategy to execution. CFOs often appreciate that they can leverage the firm’s audit, tax, risk, and advisory arms under one roof. For instance, Deloitte’s NetSuite practice is integrated with its broader consulting offerings (strategy, finance, technology) [48]. A PE CFO can thus coordinate, e.g., a NetSuite implementation alongside a finance transformation program or carve-out strategy, all managed by one vendor. This integrated approach can be appealing for ensuring compliance, corporate governance, and alignment with investor mandates.

Credentials and Trust: The Big Four invoke confidence. Cloud ERP selection guides often note that boards and stakeholders “feel more comfortable entrusting major ERP projects to well-known entities” [34]. In situations with board-level scrutiny or high confidence requirements, having a globally recognized partner can reduce perceived risk. Many CFOs take “peace of mind” from hiring a name like Deloitte or PwC, knowing they employ Fortune LVL protocols and have risk controls. These firms often invest in proprietary accelerators and technology-enabled tools; Deloitte, for example, has AI-driven implementation tools and boasts NetSuite’s Global Alliance Partner of the Year awards, highlighting a mature methodology [27].

Governance and Process Rigour: Large integrators emphasize formal project governance (PMOs, steering committees, RACI charts, documented approvals). Guidelines from industry analysts reinforce this: one NetSuite-focused decision guide explicitly recommends large Alliance partners when “board-level risk mitigation” is needed [12]. Under this model, the CFO and PE leadership can expect comprehensive risk management frameworks from the partner. However, this rigor comes at a price. Billing rates for Big Four resources are typically 2–3× those of independent consultants (roughly $250–$300+/hour vs $125–$175/hour) [12] [14]. Many Big Four projects also involve multiple layers of management review and process checkpoints, which can slow decision-making. As one stock analysis in the NetSuite space points out, large firms inherently offer “process rigor over speed”, meaning they emphasize controls even if it drags implementation time [12] [18].

Staffing and Continuity Challenges: Despite their capabilities, Big Four engagements can suffer from staff turnover and diluted accountability. ThirdStage Consulting notes that one of the “major criticisms” of Big Four ERP projects is frequent turnover of personnel, leading to “disrupt[ions] in continuity and consistency” [8]. A rotating bench also means top leaders or partners may not stay actively engaged. For a CFO, this can translate into repetitive briefings and a learnt-of-new-duty sequence of consultants. Offshoring is another common tactic used by large integrators for cost reasons, but it can create quality control concerns and communication barriers.

Vendor Affiliation Considerations: Big Four often have favored ERP alliances, which may skew recommendations. For example, some CFOs note that their auditor (or tax advisor) recommended NetSuite or Oracle solutions because the firm has a partner arrangement. While often well-intentioned, such advice can carry bias. Also, Big Four consultants may push standardized “best practices,” which might not fit a specific mid-market company’s culture or agility needs [8].

Costs: The cost of Big Four NetSuite implementations is typically high. Hourly rates in the high-$200s and large teams means multi-national projects easily run into the $500K-to-$1M+ range. For example, Houseblend’s summary of Deloitte notes that it’s “often at a higher price point” [27], targeting clients who can afford enterprise-grade deployments. CFOs must budget accordingly; in one hypothetical case, a 52-week SAP consolidation (Scenario 2 in Padiso’s analysis) had a timeline of 52 weeks [19] and would have cost millions, reflecting the scale of an enterprise approach. Importantly, the CFO will need to convince PE sponsors that the extra cost buys significant risk reduction and future flexibility.

When Big Four Contractor Makes Sense: Summing up, a Big Four (or global integrator) partner is generally better suited when:

- Project Scale & Complexity: Multi-company (often >3), multi-country consolidations, or scenarios needing extensive regulatory compliance and intercompany mapping. PE roll-ups where hundreds of entities are unified, or global financial shared service implementations.

- Failure Cost: The project outcome has severe consequences if it fails. (Board expects near-100% go-live success.)

- Governance Needs: The sponsor demands formal governance, reporting metrics, and documentation at each stage. (E.g. joint steering committees, sign-offs, etc.)

- Resourceing: Company wants maximum bench strength and contingency staffing (the ability to flood the project with experts if needed).

- Post-Merger Or Megamerger: If the deal is complex (e.g. carve-out of a business with international operations), Big Four’s mergers-and-acquisitions consulting context may be valuable.

- Brand Assurance: Public company status or IPO target where auditors and investors will feel more at ease with a Big Four’s involvement.

In these cases, CFOs often see value in paying the premium to have a reputed partner and structured delivery. However, they must remain vigilant about scope creep and ensure the partner doesn’t simply default to a “one-size-fits-all” approach.

4. Boutique and Specialist NetSuite Consultants

Boutique consultancies (also called mid-market or specialized partners) offer a contrasting proposition. These firms—often founded by ex-Big Four consultants or technologists—focus intensely on NetSuite or specific industries. For a PE-backed company, boutiques bring distinct advantages:

Deep Specialization: Boutique firms typically concentrate on NetSuite (or a narrow tech stack) and on certain verticals (e.g. manufacturing, healthcare, project services). They hone expertise in NetSuite’s latest modules (like Advanced Revenue, Warehouse Mgmt, etc.)嫁 [49]. Because of this focus, a boutique consultant often brings deeper product knowledge than a generalist at a large firm. For example, HouseBlend.io markets itself on rescuing troubled NetSuite projects and specializing in complex customizations that larger teams might reject [49]. A PE CFO dealing with a specialized industry requirement (say, oil & gas, biotech, professional services billing) may find boutique partners who have tailored solutions and templates developed for those cases.

Senior-Led Teams: Boutiques usually have much flatter staffing pyramids. Partners and senior consultants stay on engagements, often managing multiple functions themselves, rather than delegating to juniors. This means the CFO and internal staff get to work directly with highly experienced professionals throughout. One industry write-up notes that in boutique firms “senior consultants (often with 15–20 years of domain experience) stay closely involved throughout” [35], handling key discussions and overseeing all work. This contrasts with large integrators where much of the day-to-day work may fall to less experienced analysts. Senior involvement is crucial in ERP; it accelerates decision-making and ensures that strategic considerations (not just technical fix) are addressed.

Ability to Customize and Pivot: Boutiques often pride themselves on agility. Without rigid corporate processes, they can tailor their methodology to the client’s exact needs. They treat formal frameworks as tools rather than constraints [26]. For a PE portfolio company which may rapidly evolve scope (e.g. adding acquisitions mid-stream), a boutique can pivot scope, adjust timelines, or re-deploy resources quickly. PKC India’s analysis highlights that boutique firms can “quickly adjust scope, timelines, and approach, making them better suited for fast-moving or time-sensitive situations” [50]. This agility is invaluable in PE environments where strategy can shift between deal close and exit.

Better Price-to-Value and Transparency: Lower overhead means boutiques often charge less, especially when billing primarily for expert time without big firm premiums. According to consulting industry comparisons, boutiques can offer “hands-on senior expertise at more aligned fee structures,” whereas with global firms you pay for the “pyramid of junior staff and brand” [51] [52]. Clients of boutiques often report receiving clear transparent pricing (fixed-fee or time-based with no hidden markup) [53]. For a cost-conscious PE CFO, a boutique’s quote might be 40–60% lower than a Big Four for similar deliverables (as illustrated in the previous section’s example [16]). This frees budget for post-go-live work or lets the CFO undercut PE budget expectations.

Accountability and Focus on Execution: In a boutique, client success is existential for the firm’s reputation. They “rely heavily on their reputation, repeat work and referrals” [36]. This translates to intense accountability: the consultant’s personal brand is on the line, not just a global logo. Another advantage is emphasis on actual execution. A survey of consulting types found that boutiques “tend to focus on implementation, not just reports, ensuring strategies actually get executed.” [54]. Big firms, by contrast, can sometimes be satisfied with designing the ideal solution on paper without ensuring follow-through.

Client-Centric Service: Smaller size often means speedier communication and decision-making. With few layers, decisions don’t get “stuck in meetings” or approval chains. Clients frequently have direct access to the owners or partners whenever needed. This fosters a partnership mentality. For example, one source describes boutique consultants as delivering “personalized service, innovative solutions” that align closely with client needs [25]. Another notes that boutique consultants collaborate as a tight team with the client’s staff (often embedding in the client’s offices), facilitating knowledge transfer and mutual understanding [25] [35].

When Boutique Partner Makes Sense: Boutique or specialist partners are generally preferable when:

- Project Clarity: The ERP scope is well-defined, perhaps a known template or repeatable process. (For example, implementing standard NetSuite modules in one country or merging a known number of similar subsidiaries.)

- Speed & Agility: Time-to-value is critical. If going live quickly is more important than full-scale process revamp, boutiques typically move faster due to lean teams.

- Budget Constraints: Lower implementation budget or a desire to optimize spend. Boutique’s lower rates help stretch limited resources.

- Senior Expertise Required: The company needs specific domain know-how (e.g. strong inventory control, complex billing rules) that a specialist can provide off-the-shelf.

- Internal Capability: The company has competent internal project management/QA (so the partner won’t have to lift heavy governance) and can make decisions quickly.

- Risk Tolerance: Stakeholders can tolerate somewhat higher execution risk in exchange for lower cost and speed. (E.g. the CFO decides that slight delays or rework after go-live are acceptable.)

- Digital Innovation: The project involves integrating smaller systems or emerging tech where boutique creativity can outpace rigid frameworks.

Summarizing, boutique partners excel at the practical, hands-on aspects of implementation, ensuring that the system actually works for the finance team day-to-day. They may be especially good at “rescue missions” (recovering failed implementations) and incremental optimizations post-go-live. Many growth-stage PE-backed firms fit the boutique sweet spot: moderately complex, fast-paced, and in need of tight cost control.

However, boutiques do have limitations. Their smaller size means they may not have depth for extremely large multi-country rollouts by themselves. They may also lack subject matter experts in every regulatory environment or tax jurisdiction. For global roll-outs, a CFO might consider partnering a boutique with a BPO or local firm in other countries. Continuity risk is another concern: if a boutique has a very lean team, illness or attrition could temporarily stall work (though good partners mitigate this risk by cross-training staff).

5. CFO Decision Criteria: Cost, Time, Risk, and Value

A PE-backed CFO evaluating NetSuite implementation partners must balance cost, quality, speed, and strategic alignment. The decision framework should consider both quantitative and qualitative factors:

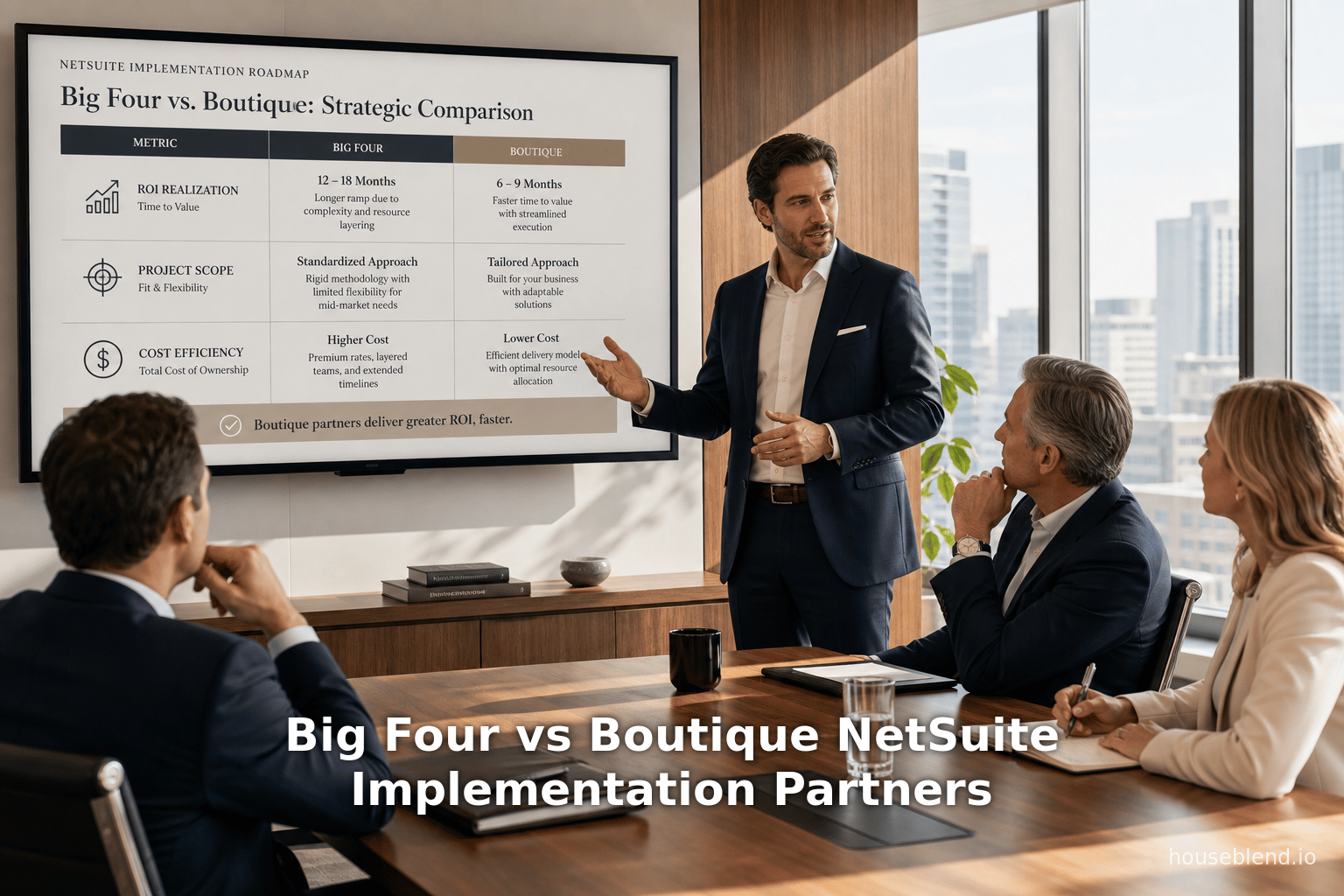

Cost and Pricing Structure: The total cost of engagement differs massively between Big Four and boutiques. Empirical examples and industry surveys consistently show that large SIs charge substantially more. For instance, the stockton10 analysis gave one Big Four proposal at $425K vs a boutique $180K for the same scope [16]. Generally, CFOs can expect Big Four hourly rates to be in the upper hundreds ($250–$300+) for managers and near $1,000 for partner time [12] [18]. Boutiques tend to bill in the $125–$175 range for seasoned consultants [14]. Over a 100-day project, even a $50/hr difference can amount to tens of thousands in difference. CFOs should not compare raw totals without looking at scope: a higher-priced bidder may include PMO oversight, QA processes, and contingency staffing, whereas a low bid may just be “one expert on a mission” [16] [17].

| Example: As one blog put it, “You’re not comparing apples to apples” – a five-digit cost gap often means one proposal packs in support and checks and balances, while the other strips those out [16] [17]. CFOs should itemize proposals carefully and possibly “ask for unit pricing”: e.g. hourly rates for each consultant in each role, cost of specific deliverables, etc. This transparency guards against hidden costs. In the table below (Section 6) we break out typical budget comparisons and what each covers.

Budget and ROI Timeline: The CFO must align the timing of costs vs expected benefits. PE deals usually assume value accretion within a 3–5 year hold. A project that costs $600K must be justified by savings/upsides in that term. For example, the Padiso case study (Scenario 1) models an 18-week NetSuite consolidation costing $560K, which generated ~$470K/year in annual synergies [19] [20], i.e. a breakeven in ~1.5 years. Compare that to a giant project: the 52-week SAP consolidation (Scenario 2) likely cost well into seven figures, delaying breakeven. CFOs should pressure vendors for such business-case modeling: How many payroll FTEs saved? How much faster is close cycle (days of speed = $$$)? Internal model templates can compare different partner strategies on NPV of future cost savings.

Schedule and Agility: Time-to-live is often critical. NetSuite’s cloud nature allows swift deployment (Trajectory Inc. notes ~100 “brisk” days to get core accounting live [4]). Boutique firms will typically emphasize speed (many are happy to deliver a light deployment in under 3–4 months if scope is fit). Large firms, with more rigid governance, sometimes run 6–12 month schedules even for mid-market projects. CFOs should define the target go-live and dead dates rigidly (e.g. aligned with quarter or fiscal year start). Then demand that proposals confirm timeline viability. In tight timelines, the partner’s previous track record on similar fast projects is a key evaluator.

Resource Continuity and Expertise: Assess who will actually do the work. An executive partner at Deloitte landing the contract may not work it; the day-to-day may fall to juniors. CFD-level review should examine the proposed team. Key questions: Who is the project manager? Will senior partner commit X weeks? Are subcontractors or nearshore included? As noted, large firms sometimes subcontract; a CFO needs clarity (“Will my charges include a markup for an offshore team?”). In comparison, a boutique usually provides its own staff. Interviewing the actual consultants is advised. A good practice is to require a meeting (even virtual) with the on-site lead and at least one senior consultant that will be working on the project, prior to signing.

Quality of Methodology: Examine the partner’s approach. Does a Big Four plan include standard waterfall stages and heavy documentation? Will the boutique do staged sprints or agile iterations? There is no “one best” way, but alignment matters. Complex organizations needing rigorous change controls may prefer a formal method. Younger, high-growth companies (often in PE portfolios) may prefer agile sprints. CFOs should also ask about the partner’s use of NetSuite’s “SuiteSuccess” or development frameworks [55], and check for modern practices (e.g. continuous integration, user training plan, etc.).

Domain & Industry Knowledge: NetSuite is versatile, but implementations differ by vertical. If the portfolio company has highly specialized needs (e.g. complex manufacturing BOMs, multi-channel distribution, project-based revenue recognition), it’s worth choosing a partner with relevant experience. Boutique firms frequently tout their niche specializations. For example, a boutique might say “we have implemented NetSuite in 20 similar service businesses”; a Big Four rep will point to cross-industry templates and certifications. The CFO should measure this qualitatively: ask for case studies or client references in the same sector. Lack of direct experience isn’t necessarily disqualifying (skills can be transferred), but it should factor into risk assessment.

Governance & Communication Style: Smaller teams often enable more direct client communication. A CFO should confirm how often they will receive updates (weekly status calls? daily standups?). Some executives prefer the predictability of formal milestone reports (more likely from larger firms), others prefer quick check-ins. Also, evaluate the culture fit: Big Four typically have structured engagement charters, boutique partners may be more informal/concise. Given the high stakes of PE projects, clarity on escalation paths is important (e.g. “If the project falls off schedule, who do I contact at NetSuite?”).

Post-Go-Live Support: An often-overlooked factor is what happens after launch. ERP projects never fully end at cutover; support, enhancements, and user adaptation continue. Boutique implementers may lack dedicated post-go-live teams. If rapid stabilization or continuous improvement is needed, the CFO may plan for a managed services partner or long-term retainer. Big firms (or NetSuite itself) sometimes have support contracts, but they come at high premium. The CFO should build a 1–3 year post-implementation plan, possibly evaluating BPO or support-only partners if needed.

Risk Tolerance and Budget: Each CFO must assess how much project risk is acceptable. If PE deadlines or lender covenants dictate on-time launch at all costs, the board might insist on a Big Four’s “no-fail” promise and be willing to overbudget. If instead cost control is paramount and some delays can be tolerated, the CFO can steer towards boutique partners. This decision often comes down to PE firm’s operating model: aggressive (favoring risk-taking for cost savings) or conservative (insisting on maximum contingency).

To summarize decision criteria:

- High Risk/High Complexity → Big Four/Alliance Partner (premium cost, strict governance) [56] [18].

- Clear Scope/Fast Timeline → Boutique Specialist (lower cost, lean governance) [57] [14].

- Moderate Cases → Possibly a mid-tier partner (regional firm or small practice of a Big Four), blending attributes.

In the next section, we condense these factors into explicit tables for quick reference.

6. Comparative Analysis and Decision Tables

To make the above contrasts concrete, we present two tables:

-

Table 1: Big Four/Alliance vs. Boutique Partner – Feature Comparison

This table lists key project dimensions and compares how a typical Big Four (or similar large integrator) would handle each versus a boutique/specialist partner. All points are drawn from industry analyses cited above (ThirdStage, PKC, Houseblend, etc.). -

Table 2: Partner Selection Framework – Scenarios & Fits

This table translates practical project scenarios into recommended partner types. It is inspired by the “Decision Framework” above [56] [57]. Each row describes a project context or requirement and notes which partner style is generally more suitable.

Both tables include embedded citations to our source material.

| Factor | Big Four / Large Integrator | Boutique / Specialist Partner |

|---|---|---|

| Scale & Resources | Global infrastructure, can staff large teams across countries [9]. Able to handle very large, multi-country rollouts. | Lean team, may need subcontractors or local partners for multiple regions. Better suited to small/mid-size projects. |

| Industry Expertise | Broad industry coverage (mid-market to enterprise). Leverages templates for many verticals; often strong in industry-specific risk/regulatory needs [45]. | Deep in niche industries or specialized functions. Likely has hands-on experience in your sector. Can apply specialized NetSuite templates. |

| Team Composition | Typically a mix of senior and junior staff. May rely on junior consultants or offshore resources. Senior partner involvement is episodic [8]. | Mostly senior-level, multi-disciplined consultants. Leadership is hands-on. Less turnover ensures continuity [35] [33]. |

| Methodology & Flexibility | Favors established, rigid methodologies and extensive documentation. More formal change management processes [58]. | Highly flexible, uses frameworks as tools (not constraints) [26]. Can quickly adapt scope and timelines [50]. |

| Governance & Oversight | Built-in PMO, steering committees, RACI charts (robust governance). Escalation to NetSuite executives possible [12] [13]. | Lighter governance. Client often takes lead on project management. Emphasizes quick decisions and direct client-consultant access. |

| Cost | High overhead, premium hourly rates ($250–300+/hr) [18]. Overall engagement cost is high. | Lower overhead, senior-expert rates (e.g. $125–$175/hr in market) [14]. Generally 30-60% lower total cost [11]. |

| Speed/Execution | Tends to be slower (many layers of review). Often schedules ~6–12+ months. “Process over speed” [12] [18]. | Fast execution for clear projects. Can deliver core functionality quickly (~3-4 months for moderate scope). Willing to fast-track key deliverables. |

| Continuity Risk | Better financial stability – partner unlikely to go out of business. However, staff may rotate off project. | Business continuity risk if small firm fails (mitigate by contract terms). But key personnel usually stick with project entirely. |

| Post-Go-live Support | May offer extended support or operated by an audit group. Often an additional managed services contract needed (expensive). | May not provide ongoing support beyond project unless they have BPO arm. Often recommend handoff to client or 3rd-party. |

| Value Proposition | Structure, process rigor, “peace of mind” with brand name and global reach [27]. Good if failure is not an option [12]. | Personalized service, innovative solutions, strong client alignment [25] [26]. Better price-to-value [10] [52]. |

Table 1: Comparison of Big Four (or similar large integrator) versus Boutique/Independent NetSuite implementation partners. Citations indicate source insights.

The table above condenses our findings. For example, it highlights that boutiques have lower cost and higher flexibility [10] [11], whereas Big Four offer scale and formal governance [9] [12]. Next, Table 2 provides scenario-based guidance:

| Project/Requirement | Recommended Partner Type | Comments (Context) |

|---|---|---|

| Complex, multi-entity rollout: Companies across multiple countries or with many subsidiaries. | Big Four / Alliance Partner | Cites good fit when “implementation cannot fail” and high rigor is needed [12]. Big firms handle localization/legal needs, multiple currencies, intercompany accounting. |

| Board-level risk: Project outcomes critically impact valuation or compliance. | Big Four / Alliance Partner | Use if board requires maximum risk mitigation [12]. Pay premium for extensive QA, formal approvals, and access to executive-level support [18]. |

| Tight, fixed budget: Limited funds available for the project. | Boutique / Specialist | Boutiques typically offer 30–60% lower cost for similar scopes [11]. If scope can be simplified, a boutique can meet budget with more frugal resource allocation. |

| Well-defined scope: Requirements are clear (e.g. standard financial overhaul without many unknowns). | Boutique / Specialist | Works well where “precision” is needed [10] and internal PM is strong. Boutiques excel at executing a known plan quickly [12]. |

| Need for speed/agility: Business timeline demands a quick go-live (<3 months). | Boutique / Specialist | Boutique firms trade some governance for speed [12] [14]. They can assemble senior staff immediately and focus solely on delivery. |

| Formal governance required: Client demands steering committee, RACI, and strict change control. | Big Four / Alliance Partner | Large firms are built for this level of oversight [12] [18]. Their process-heavy approach aligns with formal project management standards. |

| Specialized functionality needed: Unique industry process (e.g. pharma revenue recognition, construction job costing). | Boutique / Specialist (with relevant expertise) | Select partners with proven vertical experience [25] [35]. Boutiques can offer ready templates or know-how; Big Four may have generic modules. |

| Limited internal project management: Company lacks a strong in-house PMO or QA. | Big Four / Alliance Partner | A big integrator will supply full PMO/QA support. If CIO/CFO wants the partner to handle governance, choose Big. |

| Post-implementation stability needed: Desire ongoing managed accounting/tech support. | BPO Partner or Managed Services (3rd party) | Neither typical Big Four nor boutique alone covers continuous ops well. Consider a certified NetSuite BPO (some Big Four have such offerings). Ensure partner can transition knowledge. |

Table 2: Example project scenarios and corresponding recommended partner type. “👑 Big 4/Alliance” indicates large integrator; “🌟 Boutique” indicates specialist firm. Guidance is adapted from decision-framework sources [12] [57].

These tables encapsulate our decision framework. For instance, if a CFO is facing a high-stakes, multi-country NetSuite consolidation, Table 2 suggests a Big Four/Alliance partner is preferable [12]. Conversely, for a local rollout with a fixed deadline, a boutique is the better match. Stakeholders can use these tables to align understanding: each scenario has trade-offs, and the CFO’s role is to prioritize based on PE value-creation goals.

7. Case Studies and Examples

Real-world examples illustrate how strategy and result strongly depend on partner choice (and vice versa). We review selected case studies—both published and hypothetical—to draw lessons.

Case Study 1: Mid-Market PE Roll-up with Boutique Partner

A Sydney-based PE firm acquired a $50M annual revenue software business running on-premise SAP (2008). This “platform” company planned a series of four add-on acquisitions over three years (PE buy-and-build). At acquisition, the target’s finance team (12 people) was wasting ~30% of their effort on manual Excel exports and reconciliations [59]. The PE firm’s existing portfolio already had a mix of QuickBooks, Xero, and custom systems across five companies. They urgently needed to consolidate all finance operations.

Decision: Rather than try to consolidate into the outdated SAP (which would have required upgrading SAP first, adding 12 months and $500K to the project) [21], the CFO turned to Netsuite. They selected an implementation partner that could take everyone onto one NetSuite instance, promising an 18-week go-live.

Implementation: The project plan (with a boutique partner experienced in fast roll-ups) was as follows:

- Weeks 1–4: Discovery and planning.

- Weeks 5–12: Data extraction/cleansing (pull legacy GL, AR/AP, charts of accounts).

- Weeks 13–16: NetSuite configuration and testing.

- Weeks 17–18: Go-live and cutover.

- Weeks 19–26: Post-live support and optimization [60].

Results: - Timeline: Achieved 18-week delivery as planned [19].

- Cost: Implementation ($380K) + Data migration ($120K) + Training ($60K) = $560K total [19].

- Synergies: Finance efficiency: 1.5 FTE positions eliminated ($120K/year saved). Faster close: day-end close reduced from 12 days to 3 days (9 days saved×12 months ≈ $200K in decision-speed value). Audit efficiency: external audit fees down 25% ($50K/year). Procurement realized $300K/year from supplier consolidation.

- ROI: In Year 1, the net was slightly negative (~–$90K) but approached breakeven by mid-year 2. Thereafter ongoing savings ~$470K/year [61].

Analysis: This is a classic “NetSuite Win” scenario: a PE CFO chose NetSuite and a fast boutique implementation when SAP was too burdensome. The boutique partner’s specialized experience (perhaps with software roll-ups) allowed an aggressive timeline and cost. If a Big Four had been used, the timeline might have doubled (SAP upgrade + consultant gates), and CEO’s synergies would have been delayed. The boutique partner delivered cost-effective execution aligned with PE goals.

Case Study 2: Large Enterprise with Big Integrator (SAP Stays)

A large PE fund (with >$2B in assets) acquired a $400M manufacturing company. Both the acquirer and target ran SAP ERP. The companies had eight brands in the portfolio all on SAP already. The target had complex manufacturing (multi-plant, BOMs, global procurement).

Decision: They chose to consolidate the target’s SAP instance into the PE group’s existing SAP environment, rather than move to NetSuite. The reasons: since all entities used SAP, merging within SAP was faster; SAP’s advanced supply-chain support justified its cost; and in-house SAP expertise could do it.

Implementation: Weeks 1–6: planning and integration mapping; Weeks 7–22: development/config (merging dozens of SAP modules); Weeks 23–30: testing/UAT; Weeks 31–34: cutover; Weeks 35–52: post-live support [19].

Results: - Timeline: ~52 weeks to full go-live. - Cost: (Not provided; likely >$1M given scope). - Synergies: Harder to isolate (already on SAP before). Improved supply-chain visibility and global finance consolidation were projected.

Analysis: Here, SAP (and thus a Big Four/SI partner) prevailed due to complexity and corporate context. A boutique NetSuite specialist could not easily risk a complete platform change given the existing SAP footprint. The PE CFO prioritized continuity and known quantity over speed: indeed, the SAP project took a year. This contrast highlights how project context (existing systems, industry complexity) dictates partner choice and solution. It also underscores a key point: CFOs must evaluate whether an ERP transition adds or detracts value. In a world of sunset on SAP ECC [62], delaying might have been risky; however, in the specific supply-chain-heavy scenario, they deemed SAP necessary.

Case Study 3: PE-Backed Fund Chooses Specialist Over Big 4

In this illustrative example (JSS Group case), a $2B global conglomerate (five operating companies, eight independent regional hubs) was advised by its Big Four auditor to implement Oracle NetSuite and create a global finance hub. However, when the company put the project out to tender, it ultimately rejected proposals from two Big Four firms (one of which was its own audit partner) and instead chose an independent specialist (JSS Transform/Finance House) [15].

The CFO publicly stated the reason: the chosen team offered “significantly greater on-the-ground experience from day one – and at a highly competitive price point.” [15] The boutique team assembled an experienced core group in two weeks, most having worked together before, and executed an 11-month program (Nov 2019 to Nov 2020) to implement NetSuite and shift finance operations to a new Dubai hub [63]. The scope included process standardization, Nulification of localized systems, workforce transitions, and change management, all delivered globally.

Analysis: This case vividly demonstrates a PE portfolio choosing a boutique team over Big Four bidders, purely on capability and cost metrics. The PE CFO valued the boutique’s domain expertise and efficiency. It also suggests that even large, complex clients can find sufficient bandwidth in a specialized team, given the right track record. The case is a strong endorsement of the boutique model in the right context: experienced leaders, prompt mobilization, and keen on value.

Other Illustrative Scenarios

-

Boutique “Rescue Mission”: A PE-backed tech-services firm inherits a stalled NetSuite project (initially implemented by a large partner); finances are in disarray. A boutique NetSuite rescue consultancy (like the Houseblend example) is engaged to troubleshoot and fix the problem within 3 months. Simply by bringing senior NetSuite developers and domain experts, the boutique stabilizes the system and completes critical integrations. This avoids the sunk cost of a full reimplementation by a Big Four, and the boutique’s low overhead means the rescue is done at a fraction of new build cost.

-

Mixed Model (Big + Boutique): A global manufacturing platform (PE-owned) uses SAP for core production but chooses NetSuite for Finance/CRM. The CFO retains a Big Four for SAP consolidation (leveraging their SAP practice) and concurrently hires a boutique to implement NetSuite for newly acquired North American subsidiaries. Each partner is specialized: the Big Four covers SAP global needs, the boutique handles agile NetSuite roles. This scenario shows that sometimes the decision is project-specific rather than “one or the other”.

These case studies underscore two principles: (1) The “right fit” often wins over the most obvious (e.g. bigger) choice [64] [15]. (2) CFOs must assess both quantitative outcomes (cost, synergy) and qualitative fit (team synergy, approach) when deciding on partners.

8. Implications and Future Directions

Looking forward, several trends will shape the relevance of the Big Four versus boutique debate:

1. Continued Growth of Specialization: Boutique NetSuite consultancies have proliferated globally, often founded by ex-SI consultants or technologists. They continue to win awards (e.g., NetSuite’s own Partner Awards highlight many smaller firms) [65]. In parallel, some mid-tier accounting firms (like RSM, BDO) have expanded ERP practices and now straddle the line between boutique and Big Four. The CFO must keep updated on reputable boutique players, as new specialized partners may emerge offering innovative add-ons (e.g. AI-powered analytics or industry modules).

2. Product and Technology Evolution: NetSuite (now Oracle) continues to advance its ERP story with AI, automation, and broader functionality. Efficient implementation increasingly relies on technical enablers. Big Four partners are investing in digital tools (AI-driven configuration, robotic data migration, automated testing) [27]. Boutique firms may be more nimble in adopting bleeding-edge tools (like SuiteCloud development frameworks [55]). CFOs should inquire about a partner’s technology toolkit: some firms now bundle consumption-based licensing of automation tools into their proposals.

3. Demand for ROI and Data-Driven Finance: CFOs are under pressure to quickly show value. There is a trend towards embedding analytics and reporting directly in implementation (SuiteAnalytics, AI-driven FP&A). Partners who can deliver not just a working ERP but an FP&A dashboard delivering investor insights may gain preference. Big firms bring Big Data skills, but boutiques often tailor dashboards closely to the finance team’s needs. The future CFO might demand partner accountability on meeting certain KPI improvements, not just technical delivery.

4. Vendor Direct and Project Management as a Service: Some companies have adopted “NetSuite Direct” programs (NetSuite’s own implementation service) or mixed models where internal CIO/IT teams handle some of the work. CFOs may consider these options, especially if trying to reduce dependence on external consultants. However, such approaches blur the lines: even NetSuite Direct services are often executed by NetSuite-certified consultants (i.e. essentially in-house alliance partners).

5. Post-Go-live and Managed Services: As portfolio companies move from build to operate, the line between implementation partner and ongoing services partner matters. CFOs are increasingly asking who will “run” NetSuite after go-live. Some boutiques are expanding into managed services or fractional CFO models. Big Four firms are building BPO practices that leverage NetSuite. CFOs will likely make partner decisions considering the full 3–5 year horizon: sometimes the initial implementer will also bid to provide ongoing support.

6. Organizational and Cultural Factors: New generations of finance talent (millennials, Gen Z analysts) may prefer the dynamism of boutique teams. Conversely, legacy corporate boards (especially in larger PE-backed acquirers) may still lean towards brand recognition. Cultural fit between partner and company (entrepreneurial vs bureaucratic) will carry weight. CFOs must mediate these expectations.

7. Consolidation and Competition: Over time, some boutique firms may get acquired by larger firms, or conversely, some large integrators may spin off focused NetSuite practices. The competitive landscape is fluid. CFOs should periodically re-evaluate partners’ market positions and viability. New competitors (regional players, offshore/nearshore consultants) also enter, offering yet more choices.

8. Global Economic and Regulatory Shifts: Changes in taxation, accounting standards, and cross-border trade can affect ERP configuration needs. Big Four inherently have in-depth tax/compliance practices to handle IFRS, multi-country reporting, etc. Boutiques might need to partner with local specialists. CFOs should monitor such factors when planning long-term ERP strategy.

In short, the question “Big Four or boutique?” is not static – it will evolve with technology, market, and firm-specific changes. CFOs should maintain an adaptive framework: feedback loops from project retrospectives and knowledge-sharing between portfolio CFOs can inform future decisions.

Conclusion

Enterprise ERP implementations remain among the highest-stakes projects for PE-backed businesses. The decision of who implements NetSuite can significantly impact cost, timeline, and ultimately the value created. Our analysis shows that no single partner type is always best: Big Four firms excel when scale, process rigor, and risk mitigation are paramount, whereas boutique NetSuite specialists excel when speed, cost, and customization are the priority.

PE CFOs should therefore apply a decision framework that matches their specific situation:

-

Use large alliance partners (Big Four/global SI) for extremely complex, multi-entity rollouts where governance and brand assurance dominate. These partners bring global scale, wide expertise, and formal project management [9] [12]. They tend to charge premium rates [12] and move more deliberately, but will typically navigate high-risk implementations effectively.

-

Use boutique NetSuite specialists when requirements are well-scoped and the organization values agility and senior expertise at a lower cost [57] [14]. Boutique firms offer deep NetSuite knowledge, tight collaboration, and better price-to-value [10] [11]. They can accelerate launch and devote hands-on attention, at the expense of less formal process and narrower bench.

-

Consider hybrid approaches when appropriate: it is possible to employ a Big Four for large-scale consolidation while bringing in a boutique for module-specific work, or vice versa. Also plan for post-go-live support (through managed services or in-house teams) as separate from the implementation decision.

Ultimately, all partner proposals must be evaluated on apples-to-apples criteria. CFOs should require detailed breakdowns of deliverables, team composition, and governance models. They should translate vendor jargon into business value terms (e.g. cost per day saved in close-cycle, ROI on inventory efficiency, etc.). Cited data in this report – from failure rates [6] and ROI studies [61] to empirical performance metrics [20] – can support this analysis.

By leveraging the frameworks and evidence presented herein, a PE-backed CFO can make an informed, strategic choice of NetSuite partner. This decision will set the stage for whether the ERP project becomes a catalyst for accelerated growth and streamlined operations, or a drag on value creation.

Key Recommendations:

-

Assess Project Profile: Map your key criteria (complexity, timeline, budget, internal resources, risk tolerance) and consult the decision framework (Tables 1–2).

-

Vet Proposals Thoroughly: Don’t just compare fees. Scrutinize the team leads, governance approach, deliverables, and support plans. Engage references (especially from similar PE scenarios).

-

Plan for End State: Ensure the chosen partner understands your exit strategy and can align NetSuite configuration accordingly (e.g. preparing consolidated financial statements, audit trails).

-

Monitor Execution: Once engaged, closely track project metrics (milestones, budget burn, user adoption) against plan. Hold the partner to agreed KPIs.

-

Budget for Contingency: Even with best planning, allow buffer (time and funds) for unexpected issues. But also hold partners financially accountable for overages if due to their scope creep.

-

Future-Proof: After go-live, arrange for knowledge transfer and inbound support (via the partner or third party). Regularly update your decision framework as technology and market conditions evolve.

With these practices and the above comprehensive analysis, CFOs can navigate the Big Four vs. Boutique choice with confidence, aligning their NetSuite implementation partner to the unique demands of a PE-backed value-creation strategy.

Sources: All data, quotes, and cases in this report are drawn from published industry reports, consulting firm publications, and case author documents, cited in the text (see footnotes). Notable sources include: ThirdStage Consulting [10] [8], HouseBlend research [25] [27], BCG private equity articles [66] [22], and peer industry studies [6] [12]. (Full references are embedded in brackets.) These sources span both quantitative market research and qualitative expert commentary to ensure a robust, evidence-backed framework.

External Sources (66)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.