Celigo Competitors: 2026 iPaaS Landscape & Switching Guide

Executive Summary

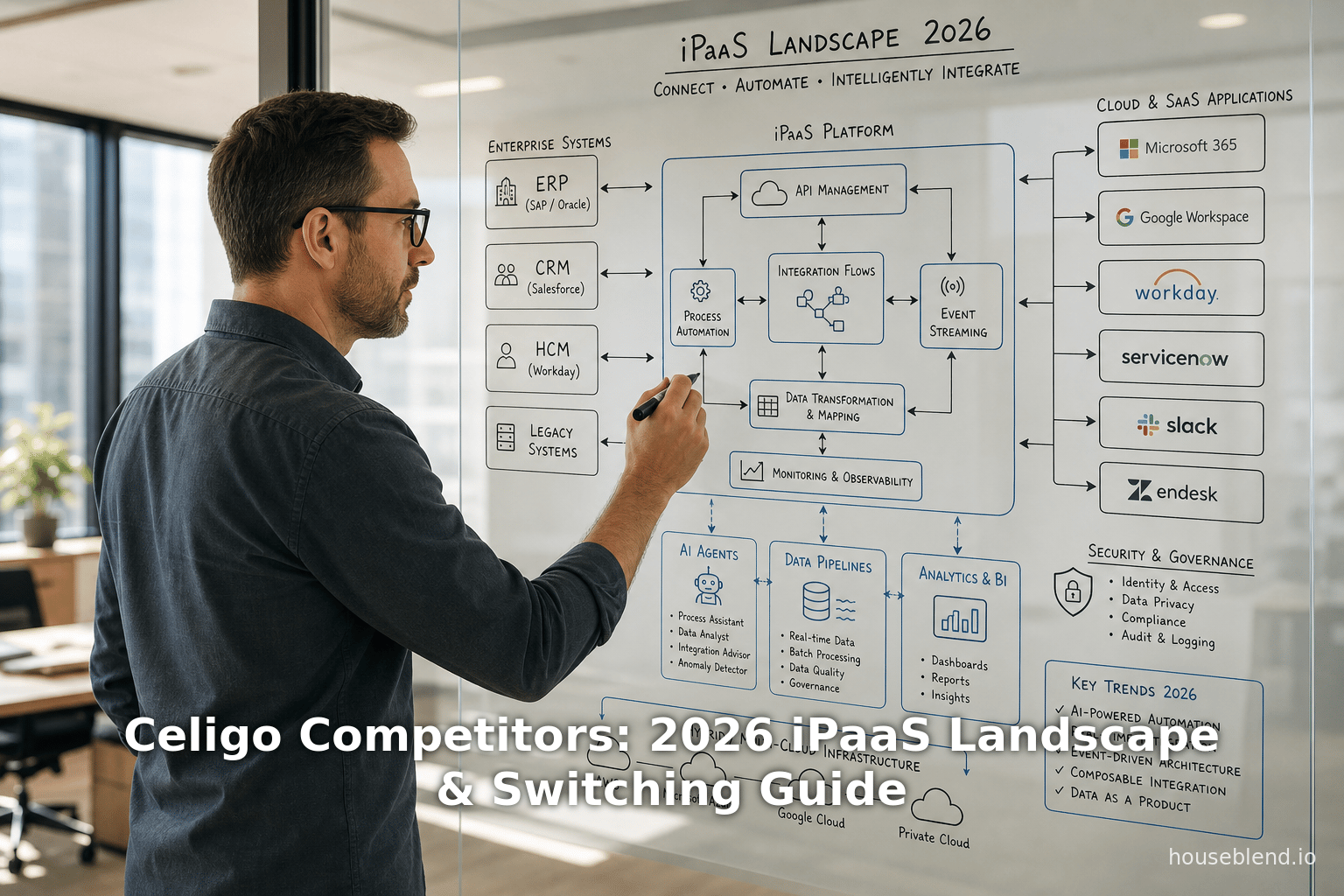

The integration platform as a service (iPaaS) market is now a critical backbone of digital transformation, steadily growing into a multi‐billion-dollar industry. Analysts estimate the global iPaaS market at >$8–13 billion in 2025, with projections reaching $50–55 billion by the early 2030s [1] [2]. This explosive growth is driven by the soaring need to connect cloud, SaaS, and on‐premises applications and by emerging trends in AI and automation. Gartner and Forrester reports highlight dozens of competing iPaaS vendors (often 20–30+), reflecting both market oversaturation and innovation [2] [3].

Celigo, a Redwood City (CA)–based iPaaS vendor, has positioned itself as a high‐growth “visionary” in this landscape. Gartner recognized Celigo in the Magic Quadrant for iPaaS for 2024–2026 [4] [5]. With its integrator.io platform, Celigo specializes in mid‐market SaaS integration (notably NetSuite, Shopify, Salesforce, etc.) and offers a large catalog of prebuilt connectors (over 700 by 2025 [6]). It targets business users with low‐code tools and industry-sized templates, aiming to simplify e-commerce, ERP, finance, and B2B automation. Celigo touts strong customer satisfaction (94% willing to recommend [7]) and rapid feature enhancements (AI‐powered integrations, new deployments, etc. [8]).

However, numerous competitors vie for iPaaS leadership at all market segments. Established enterprise players ( MuleSoft/Anypoint, Boomi, IBM App Connect, Informatica) dominate large‐scale, data‐intensive integrations, while newer platforms (Workato, SnapLogic, Jitterbit, Tray.io, Elastic.io, etc.) compete in emerging niches (rich business automation, AI pipelines, low-code SMB). Cloud giants also push their own integration services (Microsoft Power Automate/Logic Apps, Oracle Integration Cloud, SAP Integration Suite). In April–May 2025, even the landscape shifted via major M&A: Salesforce announced an $8B acquisition of Informatica [9], signaling deeper consolidation of iPaaS with CRM/AI data platforms.

This report provides a comprehensive survey of the iPaaS vendor landscape as of 2026 and guidance on switching platforms. We present market and financial data, Gartner and Forrester insights, and expert analysis; compare Celigo’s strengths/weaknesses with key alternatives; and examine real‐world case studies of migrations. We also outline detailed “switching” considerations for enterprises moving from Celigo to another iPaaS (or vice versa), including ROI and risk factors. By aggregating diverse sources and metrics – from Gartner reports to NucleusResearch ROI studies – this guide delivers an in‐depth, evidence‐based view of Celigo’s competitors and the full iPaaS eco‐system [2] [10].

Introduction and Background

The Evolution of Integration Platforms

Integration has been a core IT challenge since the 1990s. Early efforts focused on point-to-point custom interfaces, which proved inflexible as enterprise ecosystems grew. In the 2000s, enterprise service buses (ESBs) and on-premises middleware sought to centralize connectivity, but they struggled with cloud adoption and agility. By the mid-2010s, Integration Platform as a Service (iPaaS) emerged to fill this gap: cloud-native platforms providing comprehensive, managed connectivity across SaaS, on-premises, and hybrid environments [11].

As Stephen Bigelow notes, “Integration platform as a service (iPaaS) is a set of automated tools that integrate software applications deployed in different environments,” often spanning both legacy and cloud systems [11]. iPaaS solutions bundle prebuilt connectors, orchestration engines, and monitoring that enable organizations to rapidly build and manage automated data and process workflows between diverse apps [12]. The key value proposition is relieving development teams from custom coding, enabling faster time-to-integration and higher reliability [13].

Celigo was founded (in 2006) amid this integration evolution. It launched integrator.io as a low-code iPaaS platform targeting mid-market companies, with an initial emphasis on NetSuite ERP and e-commerce integration. Over time, Celigo expanded into broader “intelligent automation,” adding API management, B2B EDI capabilities, and AI-driven error handling [8]. By 2025–26, Celigo had raised venture funding (Series A/B/C) and grown its team, positioning itself as the “#1 iPaaS in G2 user ratings” (per Celigo) and a Gartner Visionary [14] [5]. Its mantra stresses “governed self-service” – empowering business users (e.g., finance, ops, marketing) to create integrations within a governed framework [15].

Why iPaaS Matters Today

Modern enterprises face unprecedented application sprawl: dozens or hundreds of SaaS apps ( CRM, ERP, HR, marketing, etc.) alongside legacy systems. Without integration, data silos multiply, forcing manual workarounds. For example, one 2025 Gartner report noted the average enterprise juggles 364 different applications and numerous disconnected API gateways [16]. As data fuels AI and automation, ensuring that information flows seamlessly and in real time is critical.CEO Steve Lucas of Boomi puts it: “Connectivity remains a critical challenge…AI thrives on reliable, secure, and current data, yet too often this data is fragmented” [16].

Analysts underscore that iPaaS is no longer optional for digital transformation. The GrandView Research iPaaS market report (2026–2033) notes that by 2025, the global iPaaS market reached $12.91 billion, up from low single digits a decade earlier [1]. This growth (forecast at ~19.6% CAGR through 2033) reflects enterprises’ urgent need to connect cloud ecosystems seamlessly, as well as vendor investments in new capabilities (cloud orchestration, API management, AI) [1] [17]. North America leads with ~36% share of revenue [17], while Asia-Pacific is the fastest-growing region. Notably, even “legacy cloud” giants are adjusting: Gartner’s 2026 preview indicates AI is “changing expectations for the iPaaS market, driving innovation and new capabilities” [18].

Key Drivers and Trends in 2026

-

AI and Agentic Integration: Across vendors, integration is being reimagined for an AI era. Snow White frameworks like Model Context Protocol (MCP) and multi-agent orchestration are being built into iPaaS. In mid-2025, Salesforce (MuleSoft) announced support for AI agent orchestration protocols (MCP, A2A) and generative AI tools in its IDE [19]. SnapLogic and Workato likewise publicized AI-first innovations: SnapLogic’s “Agentic Integration Platform” explicitly targets AI agent workflows [20], and Workato unveiled purpose-built “Genie” agents for finance, HR, and IT functions [21]. These trends signal that the next phase of integration is AI-driven, where data pipelines must feed machine learning and agents as much as human apps.

-

Industry and Use-Case Specialization: With dozens of vendors, iPaaS platforms have begun to specialize. One analysis notes, “Each platform excels in specific scenarios”: for example, Celigo targets mid-market SaaS integration, Jitterbit excels in B2B/EDI and healthcare integration, SnapLogic shines with visual data pipelines, and MuleSoft emphasizes API-led enterprise integration [3]. Some iPaaS solutions now include industry-specific accelerators (“prebuilt PIPs” – process integration packs or templates) for retail, finance, healthcare, etc. However, many generalist platforms remain fully customizable via low/no-code.

-

Hybrid and Multi-Cloud: Even as cloud adoption grows, many enterprises maintain on-prem data and legacy systems. Gartner’s 2024/25 analysis warned that iPaaS vendor criteria demand robust hybrid support: inclusion required either $50M revenue or 1,000 unique customers; some vendors (WSO2, Seeburger) were excluded for not meeting scale [22]. Leading iPaaS (Boomi, MuleSoft, Celigo, etc.) affirm “cloud‐first but hybrid‐capable” models. For example, Celigo now offers a private cloud edition to support air-gapped deployments [8], while Boomi champions hybrid and multi-cloud connectivity.

-

Customer Experience and Usability: Analysts have highlighted that iPaaS usage varies by skill level. For instance, a Gartner commentary flagged that Informatica’s platform has “depth” but is seen as “complex to use” [23]. In contrast, Celigo markets itself on ease of use (“no‐code” flows, strong training). Workato similarly touts drag-and-drop recipes for line-of-business automation. Across the market, there is a dual push: platforms aim to be developer-focused (robust APIs, DevOps integration) and citizen-friendly (visual builders, intelligent recommendations). The “peer insights” review scores reflect this: Celigo’s average customer rating is 4.7/5 [7], highlighting user satisfaction.

-

Ecosystem and Partnerships: iPaaS vendors often form alliances with major cloud and SaaS providers. For example, Celigo has built connectors certified with NetSuite, Shopify, Salesforce, and others [8]. Boomi in 2024 acquired API management assets (from APIIDA and Tibco’s Mashery) to bolster its cloud-native stack [24] [25]. Oracle, SAP, and Salesforce tightly weave integration into their product suites (Integration Cloud, Integration Suite, MuleSoft). Conversely, open platforms (Tray.io, Skyvia) partner with niche apps. These ecosystems affect switching – some platforms are designed to be best-of-breed in a particular vendor’s ecosystem, while others offer more neutral “any-app” connectivity.

By understanding these trends, organizations can better position Celigo within the larger iPaaS ecosystem and plan future integration strategies. The next sections dive deeper into Celigo’s offerings and a systematic comparative analysis of competitors, backed by data and case studies.

The iPaaS Market Landscape

Market Size and Growth

The global iPaaS market has expanded rapidly. Estimates vary due to different definitions, but consensus is that by 2025 it reached on the order of $8–13 billion. For example, a Gartner-cited research note places 2025 market revenue at ~$8 billion with over 120 vendors [2]. By contrast, a GrandView report pegs 2025 at $12.91 billion and projects $55.46 billion by 2033 (CAGR ~19.6%) [1]. Even conservative figures imply mid-teens percent annual growth from 2022 onward. North America is the largest region (36.3% share in 2025 [17]), and large enterprises account for most spending [26]. Public cloud is the dominant deployment (versus private/hybrid) [26], though hybrid strategies remain important.

| Segment / Region | Key 2025 Figures |

|---|---|

| Market Value | ~$8–13 B (2025); projected ~$55 B by 2033 [2] [1] |

| Annual Growth | CAGR ~19–20% (2026–2033 forecast) [1] |

| Geography | North America ~36% share [17]; APAC fastest growth |

| Deployment Model | Public cloud leads; hybrid approaches common [26] |

| Primary Verticals | All industries adopt iPaaS; heavy in finance, retail, healthcare, logistics |

This rapid expansion is driven by multiple market trends. First, digital transformation initiatives force better integration between ERP, CRM, e-commerce, marketing automation, supply chain, and more. Second, automation and analytics/AI require connected data flows. Third, mergers and acquisitions create integration sprawl: as one study notes, the financial sector alone suffers from integration debt due to past acquisitions [27]. Finally, competition among cloud providers means each tries to upsell its own iPaaS solution for enterprise lock-in or partner ecosystem advantage.

As one whitepaper emphasizes: “the iPaaS market has surpassed $8 billion in revenue in 2025, reflecting that effective integration is no longer optional—it’s a strategic necessity for organizations pursuing digital transformation” [2]. This necessity is also confirmed by ROI studies: Nucleus Research finds organizations recoup $3.76 for every $1 spent on iPaaS, achieving ~66% faster workflow development and significant cost savings [10]. Even in complex sectors like finance, iPaaS deployments yielded an average $1.47 ROI per $1 with an 8.6-month payback [28]. These figures underscore that properly implemented iPaaS can drive tangible efficiency and cost benefits.

Gartner Magic Quadrant and Forrester Wave (2024–2026)

The market’s crowded nature has prompted annual analyst evaluations. Gartner’s Magic Quadrant for iPaaS (published ~May each year) categorizes ~13-15 major vendors into Leaders, Visionaries, Challengers, and Niche Players. For 2025, major Leaders included Boomi, Microsoft, Oracle, Salesforce (MuleSoft), SAP, and Workato [29]; Visionaries included Celigo (for the second year) [4]. For 2026, Celigo again appeared as a Visionary [5], while cloud incumbents largely held their positions. (Exact MQ placements are proprietary, but press releases and coverage confirm Celigo’s perennial Visionary slot.)

Separately, Forrester’s iPaaS Wave (2025) evaluated about 10 top providers, focusing on enterprise needs. Boomi reportedly led the Forrester Wave Q3 2025 [30], emphasizing its strength in strategy and execution. A Q2 2025 Forrester “Landscape” report covered ~23 vendors from startups to giants [31]. These analyses highlight that no single vendor dominates all segments. Instead, each brings different strengths (API Mgmt, prebuilt integrations, hybrid support, etc.) and ideal use cases [3].

Notably, the boundaries of iPaaS have blurred. Analysts warn that terms like “integration platform,” “automation platform,” “BPA,” and even “RPA” are converging. Gartner itself has cautioned that iPaaS overlaps with data integration, API management, and AI (citing acquisitions like Signavio/SAP, myInvenio/IBM) [32]. The 2026 MQ abstract underscores “AI is changing expectations for the iPaaS market, driving innovation and new capabilities” [33]. In other words, the landscape is evolving fast: vendors add AI agents and governance, and definitions expand.

Key Competitor Categories

To understand Celigo’s competitors, it helps to group iPaaS platforms by primary focus:

-

Enterprise Middleware and ESB Vendors (Legacy): IBM (App Connect), TIBCO, MuleSoft (Salesforce), SAP, Oracle. These vendors originated with traditional enterprise integration or API management. Their iPaaS offerings typically focus on complex, large-scale use cases, strong data transformation, and global deployments. They usually require skilled developers and often integrate deeply with the parent company’s enterprise apps. (For example, SAP Cloud Integration Suite is strongest within SAP environments.)

-

General-Purpose iPaaS Leaders: Boomi (Dell/Francisco Partners), Informatica Cloud, Workato, SnapLogic, Jitterbit. These emerged in the cloud era to address broad enterprise integration needs. Boomi is known for hybrid cloud integration; Informatica for data integration/MDM (now merging with Salesforce) [34]; Workato for business/IT automation; SnapLogic for self-service data pipelines; Jitterbit for API/B2B.

-

SMB/Mid-Market and Departmental iPaaS: Celigo, Tray.io, and smaller players. These target companies with fewer in-house resources or focused use cases. They emphasize low-code, prebuilt connectors, and affordability. Celigo itself fits here (especially among NetSuite shops) [3]. Zapier can be viewed as an entry-level iPaaS (though not often regarded as an “enterprise iPaaS”), but connectors overlap (Zapier even appears in some vendor lists [35]).

-

Specialized/Niche Platforms: Some platforms focus on particular verticals or integration paradigms. For example, Cleo (now part of QAD) is strong in B2B EDI/network integrations; OneScenicIO integrates IoT and logistics; Dell’s Boomi Flow (Appian-like workflow tool); RapidAPI (API marketplace).

Each category brings different pros/cons for a Celigo customer considering a switch. Later sections will drill into specific vendors and their comparative strengths.

Celigo: Platform, Positioning, and Vision

Company Profile and Growth

Celigo, founded in 2006 and headquartered in Redwood City, California, brands itself as a “next-generation integration and automation” platform [4]. Its flagship product, Integrator.io, is a cloud-native iPaaS; Celigo also offers Celigo Controller (for enterprise-level integration governance) and AI-powered assistants (like “Ora”, an AI agent interface). According to Celigo, it serves thousands of companies, especially those driving digital commerce and ERP modernization. Celigo’s Integration Marketplace provides 700+ connectors (as of 2025) covering apps like NetSuite, Shopify, Salesforce, Amazon/eBay, Stripe, PayPal, and many vertical SaaS products [6].

Funding and Leadership: Celigo completed a Series C fundraising in 2021. By 2025, Celigo had expanded its executive team (hiring a Chief Customer Officer, CMO, and CSO) to meet rising demand for AI-enabled automation [14]. The company claims (via BusinessWire) to be “#1 iPaaS in G2 user ratings” and consistently recognized in peer reviews [14]. In Gartner Magic Quadrant terms, Celigo has been labeled a Visionary in 2024, 2025, and 2026 [4] [5], reflecting “Completeness of Vision and Ability to Execute.” (Visionary placement indicates strong innovation and niche leadership, albeit not yet outscoring entrenched Leaders.)

Celigo’s CEO Jan Arendtsz emphasizes that the future of integration lies in empowering business teams with guided self-service, not just IT-centric middleware [15]. The platform roadmap highlights AI-driven error resolution, augmented design, and autonomous agents (reflecting its broader “intelligent automation” vision [8] [5]).

Core Features and Differentiators

-

Low-Code/No-Code Design: Celigo provides a graphical “flow” builder where users can connect apps, map data fields, and set triggers with minimal coding. This appeals to business analysts and administrators.

-

Prebuilt Integrations and Marketplace: Its Integration App library offers prepackaged templates (e.g. Shopify→NetSuite order sync, Salesforce→ERP, EDI flows), which can drastically accelerate deployment. The marketplace philosophy is that many e-commerce and back-office integrations are common problems.

-

API Management and EDI: Celigo has added API gateway capabilities and a B2B Manager for EDI (electronic data interchange) in recent versions [8]. This expands Celigo beyond cloud/SaaS to include traditional supply-chain data flows (e.g. invoices, orders via EDI formats).

-

AI-Powered Operations: Celigo incorporates AI for error handling and assistance. Integrator.io’s error management can auto-retry flows intelligently. The platform calls itself an “intelligent automation” suite, claiming to use machine-learning for tasks like schema mapping and anomaly detection [8].

-

Deployment and Scalability: Primarily offered as a multi-tenant cloud service, Celigo also now provides on-premises or private-cloud options (for data-sensitive enterprises) [36]. This hybrid flexibility is increasingly important. Celigo scales by horizontally running “flow tasks” in parallel and virtually any connector is supported via its API architecture.

-

Pricing Model: Celigo uses a credit-based usage model and tiered subscriptions. It markets itself as cost-effective, claiming in testimonials (e.g. Qdoba case study) to offer “more for your dollar” than alternatives [37] (though independent pricing data is scarce).

Celigo’s target customers typically value ease-of-use and prebuilt solutions. For instance, Rad Power Bikes and Factor Bikes rely on Celigo to automate their e-commerce order-to-ERP processes [38]. The Jockey Club and CDC Foundation also use Celigo for complex transaction workflows [39]. These examples illustrate Celigo’s focus: retail/e-commerce and service organizations with NetSuite or Shopify backends.

Strengths and Limitations of Celigo

Strengths:

- Business-Centric UX: Celigo’s low-code approach is often lauded by line-of-business users. The high Gartner Peer Insights score (94% recommend) suggests strong user satisfaction [7].

- Prebuilt Content: The large connector library and “Integration Apps” accelerate time to value. Many SMB customers appreciate having, say, a ready-made Shopify→NetSuite flow instead of building it from scratch.

- Flexibility: Celigo handles a range of patterns (application sync, event-based flows, file integrators). The platform covers API, file, and EDI B2B use cases. The addition of a private-cloud edition also addresses enterprise security concerns.

- Vision and Roadmap: Celigo invests in AI and expanding global reach (e.g. partnerships in LATAM/APAC [40]). The consistent Gartner Visionary placement suggests its product strategy is on-trend (focused on intelligent automation and user empowerment [5]).

Limitations:

- Scale and Complexity: Compared to older iPaaS giants, Celigo may lack some enterprise features. For very large organizations integrating hundreds of apps or requiring advanced transformation/analytics, Celigo might have gaps. Gartner and user reviews hint that platforms like Informatica or MuleSoft are better for data-intensive, highly governed environments [41].

- Enterprise Features: Features such as multi-tenant governance, advanced SOA, and packaged industry solutions are less mature in Celigo than in some leaders. Large enterprises might miss out-of-the-box templates for, say, healthcare or banking that specialist iPaaS could offer.

- Connectivity Footprint: Although 700+ connectors is ample, some highly specialized enterprise systems (custom ERPs, proprietary mainframes, or niche EDI networks) might require building custom connectors. In such cases, Celigo’s ease-of-use advantage could diminish.

- Vendor Lock-in: Like any iPaaS, moving flows out of Celigo would require effort. (As one consultancy warns, migrating iPaaS workloads between platforms “is complex and costly, adding little business value” [42].) This is not a Celigo-specific flaw, but a general challenge for users.

In sum, Celigo excels where fast time-to-market and business-led integration are priorities (especially in mid-market IT/SaaS contexts). Its challengers are typically larger players with deeper feature sets but often higher complexity or cost. The next section compares Celigo with those alternatives in detail.

Major iPaaS Competitors in 2026

The iPaaS vendor landscape is fragmented. We break down competitors into categories for clarity, then analyze diverse segments and representative vendors in each category.

Leading Enterprise iPaaS Platforms

Dell Boomi (Dell/Francisco Partners)

Overview: Boomi was launched in 2000, acquired by Dell in 2010, and sold to Francisco Partners/TPG in 2021 for $4B. It is often cited as the first major cloud-native iPaaS. Boomi’s flagship is the Boomi Integration Cloud, which includes API design (AnyPoint), workflow orchestration, EDI streaming, and data cataloging. Boomi also offers Boomi Flow (low-code workflow automation, akin to Appian or Power Automate). Boomi is aimed at both mid-sized and large enterprises, especially those needing hybrid deployments (on-prem gateways plus cloud connectors).

Strengths:

- Mature and Broad: Boomi has thousands of customers and is well-regarded for its reliability and scale. It supports a wide range of integration patterns (application, B2B/EDI, data, API).

- AI and API Investments: In 2024–25, Boomi acquired API management assets from APIIDA and Tibco’s Mashery to bolster its API capabilities [24] [43]. It also introduced AI agents, enabling automated mapping and error resolution moving toward an “agentic” future [44] [45].

- Community and Ecosystem: The Boomi Community is well-developed, and Boomi University / certifications are widely recognized. Pre-built connectors (Boomi calls them “AtomSphere connectors”) cover mainstream apps, and a process library speeds development.

- Hybrid Support: Boomi’s Atom runtime can be deployed in private clouds or on-premises, allowing integration of legacy systems. This hybrid flexibility is a key selling point for enterprises not fully in the cloud.

Weaknesses:

- Cost and Complexity: Boomi’s pricing, often based on connectivity credits and number of endpoints, can become expensive at scale. Smaller or budget-conscious organizations sometimes see Boomi as cost-prohibitive. Some customers also mention a learning curve for advanced features.

- Partner Dependence for Niche: Gartner noted Boomi depends on partners for RPA and IDP (Intelligent document processing) functionalities [46]. If an enterprise needs a unified solution including RPA/IDP, Boomi alone may not suffice.

- Competition and Sprawl: As Boomi launches new offerings (AI, Data Hub, etc.), some users find complexity in portfolio. Integrating new Boomi features with existing flows can require careful management.

Market Position: Boomi consistently appears as a Leader in Gartner’s MQ iPaaS and Forrester’s Wave. It’s rated top in strategy by Forrester (Q3 2025) [30]. It often competes head-to-head with MuleSoft and Microsoft Azure in large-enterprise deals.

MuleSoft (Salesforce)

Overview: MuleSoft, now owned by Salesforce, provides the Anypoint Platform for integration and API management. It uses an API-led connectivity approach, focusing on reusable assets (“RAML specs”, “API portals”) and a developer-centric IDE. MuleSoft addresses large organizations needing extensive API orchestration, often in multi-cloud environments.

Strengths:

- API Leadership: MuleSoft is arguably strongest in API management and microservices integration. Its design center allows creating “System”, “Process”, and “Experience” APIs, which can be published and shared across teams. MuleSoft’s acquisition by Salesforce also brings synergy with Tableau, Data Cloud, and now Informatica (CRM+data synergy).

- AI and Generative Tools: In 2025, Salesforce announced AI agent orchestration in Anypoint: support for the Model Context Protocol and a new Agent-to-Agent (A2A) framework [19]. MuleSoft also introduced generative AI features in its IDE to accelerate building flows. These moves position MuleSoft as a leader in “agentic integration”.

- Enterprise-Grade Governance: MuleSoft includes advanced monitoring, security policies, and performance management. It’s designed for IT governance and subject to enterprise SLAs.

Weaknesses:

- Complexity and Cost: Anypoint is powerful but often cited as complex to implement. It historically required Java engineers and complex on-prem brokers (though this has shifted to cloud). Gartner noted that MuleSoft is best suited where extensive IT expertise exists. The payback period can be long for smaller use cases.

- Shift in Market: As Salesforce feasts on AI/data acquisitions (Notably Informatica in 2025 [9]), some question how MuleSoft’s roadmap will align. Currently, Salesforce aims to embed integration in its broader AI vision (“connectivity for autonomous agents” [34]).

- Partner Reliance: MuleSoft’s strength in API means it often needs partners or customers to build on top-of-the-platform. Quick wins often require consultant involvement, unlike turnkey iPaaS.

Market Position: Consistently a Leader. MuleSoft’s enterprise pedigree keeps it in high demand for Fortune1000 customers. Its integration with Salesforce’s ecosystem (Data Cloud/CRM) enhances its value proposition in those shops [34].

Cloud-Provider and ERP Vendor Platforms

Microsoft Azure Integration (Logic Apps) and Power Platform

Overview: Microsoft offers multiple integration tools: Azure Integration Services (Logic Apps, Service Bus, Event Grid, API Management) and the Power Platform (Power Automate/PowerApps). Logic Apps provides scalable workflow automations in Azure; Power Automate is a no-code workflow tool in Microsoft 365. For enterprises heavily invested in Azure and Microsoft 365, these platforms serve as de facto iPaaS.

Strengths:

- Global Reach: Microsoft has massive cloud infrastructure and a broad partner network. Gartner notes Microsoft’s strength as “global presence and many deployment options,” with flexible pricing [47] [48].

- Hybrid Integration: Azure Logic Apps supports hybrid data gateways. Power Automate (and Azure Functions) can be used in on-prem environments via onsite connectors (Data Gateway). The platform appeals to firms already on Office 365/ Dynamics/ Azure who want simple ways to connect internal data flows.

- Cost-Effective Base: Microsoft often bundles basic integration tools with Azure subscriptions or Microsoft 365 licenses, making entry-level adoption cheaper.

Weaknesses:

- Use-Case Focus: Gartner notes that Microsoft’s solution set currently lacks packaged industry-specific flows (“no PIP”) [49], focusing instead on simple process automation. Its out-of-the-box templates tend to target common IT or productivity scenarios. Enterprises often complain Microsoft's iPaaS is strong for IT/tech workflows but weaker for complex line-of-business automations [48] [49].

- Fragmentation: Multiple products (Logic Apps vs Power Automate vs older BizTalk) can confuse buyers. The integration story overlaps with Azure API Management and Azure Data Factory, requiring careful planning.

- Maturity of Governance: Compared to niche iPaaS specialists, Microsoft’s offerings can lack some enterprise governance features (at least historically), although this is improving.

Market Position: Microsoft is typically a Leader due to sheer scale and continuous product investment. Azure Integration and Power Automate have large install bases. The platforms particularly dominate in mid-market to large enterprises that standardize on Microsoft software.

Oracle Integration Cloud (OIC)

Overview: Oracle positions its iPaaS under Oracle Integration (part of Oracle Cloud Infrastructure). OIC provides prebuilt integration flows (Oracle calls them “process accelerators”) and adapters for Oracle SaaS (ERP Cloud, HCM Cloud, NetSuite since Oracle’s 2016 NetSuite acquisition) and popular third-party apps. It claims to be valued by customers as the enterprise resource for cloud modernization.

Strengths:

- Prebuilt Oracle Connectivity: OIC has deep integration with Oracle’s own SaaS and on-prem apps. Many enterprises running Oracle ERP or HCM find built-in connectors (and upgrade-safe testing) appealing.

- AI-Enhanced Platform: Oracle emphasizes AI/ML features like automated mapping and error handling in OIC. Its 2024 messaging (Gartner MQ) boasts building “trusted sources for AI-powered experiences” via prebuilt connectivity and low-code automation [50].

- Scalability and Availability: Oracle’s cloud infrastructure (OCI) is known for resiliency. OIC supports enterprise-grade SLAs.

Weaknesses:

- On-Premise Agents: Analysts note a drawback of OIC is its dependency on agent software for on-premises system connectivity [51]. This means extra maintenance overhead (installing and updating Oracle gateway agents), which can be a pain point.

- Cost Structure: OIC’s pricing (often consumption-based) can escalate with enterprise-scale usage. Some customers say the cost/benefit tipping point is modest vs open-market iPaaS if not using many Oracle apps.

- Lack of Broad Integration Breadth: While rich for Oracle scenarios, OIC historically lacked some connectors out-of-the-box (users sometimes build custom REST adapters).

Market Position: Oracle Integration Cloud is a Leader in enterprises with Oracle ecosystems. Gartner has repeatedly rated it a Leader (7th consecutive time in 2024 [50]). It is particularly strong for SCM and finance domains where Oracle apps dominate.

SAP Integration Suite

Overview: SAP’s cloud integration suite combines on-prem (SAP Process Integration) and cloud (SAP Cloud Integration) offerings. Its focus is on SAP-centric scenarios (connecting S/4HANA with Ariba, Concur, SuccessFactors, etc.) as well as generic integration. The suite emphasizes industry templates (banking, manufacturing, utilities) in line with SAP’s vertical focus.

Strengths:

- Vertical Accelerators: SAP provides prebuilt business process content for industries like healthcare, retail, and automotive, easing implementation of complex end-to-end flows.

- Enterprise Support: High levels of official support and SLAs (especially in SAP’s Rise with SAP transformation packages). Many large SAP customers prefer an integrated strategy with SAP’s tools.

- Embedded SAP Integration: Tools like SAP CDC (Data Services) and Ariba Open APIs allow data integration into SAP’s data fabric (Data Warehouse Cloud, etc.).

Weaknesses:

- SAP-Centricity: As Gartner reluctantly noted, SAP’s iPaaS is often perceived as “SAP-centric.” It works best if you are heavily invested in SAP products [52]. Companies with many non-SAP systems may find it lacking.

- Complex Pricing: SAP bundles iPaaS licenses with ECC/S/4 sales, but costs can be confusing. Smaller projects may face high license overhead.

- Steady Innovation: Some customers feel SAP’s integration stack evolves slower than cloud-native specialists.

Market Position: A Leader for SAP customers, but a niche to outsiders. Adoption grew under SAP’s “Cloud for Integration” push, but it rarely replaces best-of-breed iPaaS in mixed ERP environments.

Emerging and Niche iPaaS Platforms

Workato

Overview: Workato is a fast-growing platform focused on enterprise automation. Built on a “recipe” model, Workato bills itself less as a pure iPaaS and more as a platform that bridges business and IT. It offers connectors to thousands of SaaS apps.

Strengths:

- Business-IT Collaboration: Workato engineers often describe their value proposition as empowering non-developers. For example, Workato Genies (introduced in 2025) are prebuilt, function-specific agents for Sales, IT, HR, etc., enabling rapid deployment of automated processes without code [21].

- Speed of Development: Many companies report that building integrations in Workato is faster than in traditional iPaaS. A HubSpot case study claimed the platform paid for itself in day 1 with $60K saved due to automation.

- Cloud-Native: No on-prem dependencies; designed for modern SaaS stacks.

- Strong Mid-Market Adoption: Workato suits mid-size to enterprise companies that want powerful automation without the DevOps of MuleSoft.

Weaknesses:

- Pricing Model: Historically, Workato charges per “recipe” execution (or for “utilization”), which can be hard to predict at scale. Complex enterprise usage can become expensive.

- Emergent Enterprise Features: While Workato has robust features, it is relatively newer than leaders in terms of things like built-in B2B/EDI support or ultra-high-volume throughput.

- Visibility in Public Quadrants: Gartner placed Workato as a Leader of iPaaS (5-2024) but it was a challenger in 2025 [29]. This may reflect the niche focus (automation) which overlaps but is not identical to the broader iPaaS definition.

Market Position: Rapidly positioned as a Leader among next-gen integration and automation platforms. Workato is especially noted for enabling “citizen integrators” and bridging IT with business processes [21].

SnapLogic

Overview: SnapLogic emphasizes an “AI-powered data integration platform.” It uses Snaps (prebuilt connectors) for apps and a visual data pipeline canvas. SnapLogic coined the term “AI-powered integration” and refers to becoming the “central nervous system of the modern enterprise” [20].

Strengths:

- AI/Agent Focus: In late 2025 SnapLogic launched new capabilities around “Agents” and Model Context Protocol (MCP) support [20]. The platform now treats each data/AI workflow as an agent-managed flow.

- Data Centric: SnapLogic excels at large data flow tasks (ETL, streaming, ML pipelines) as well as app integration. It has strong connections to analytics, ML, and data lake products.

- Performance: The “Snaplex” execution grid is scalable; SnapLogic claims high throughput for enterprise data workloads.

- Self-Service: Users can drag-and-drop Snaps; it’s generally considered more technical than Celigo but easier than classic ESBs.

Weaknesses:

- Cost and Target Market: SnapLogic tends to target mid-size to large enterprises due to pricing. The learning curve and cost can be barriers for SMBs.

- Narrower Adoption: Compared to Boomi or MuleSoft, SnapLogic has fewer total customers. It is often chosen by organizations with substantial data integration needs rather than point-to-point app integration.

- Competition: Other vendors are now also focusing on AI integration (Boomi, Workato, MuleSoft), so SnapLogic’s differentiation may narrow.

Market Position: SnapLogic is generally seen as a Challenger or Visionary in iPaaS MQs, and is often highlighted in Forrester Wave reports focused on data integration. It is favored by data engineers and organizations pursuing an AI-driven “agentic enterprise” [20].

Jitterbit

Overview: Jitterbit (acquired by Astorg in 2019) offers Harmony Cloud™ iPaaS. It focuses on quick API design and high-throughput integrations. It is often used in healthcare, insurance, and other regulated industries.

Strengths:

- B2B/EDI and Healthcare: Jitterbit provides specialized connectors and transformation capabilities, especially for EDI and HL7 data, making it popular in niche verticals.

- API Management: It includes API layer features, allowing integrations to be exposed as APIs.

- Ease of Use: Its development environment is considered simple, and it has strong documentation and support.

Weaknesses:

- Market Share: Jitterbit is smaller scale than Boomi or MuleSoft. Some customers report limited community resources.

- Feature Sets: While broad, it may have fewer “bells and whistles” (AI agents, extensive templates) than some newer rivals.

- Cloud-Native Evolutions: Jitterbit has kept pace, but some longtime users report stability issues in older versions (recent releases aim to fix these).

Market Position: Typically a Niche Player or Visionary. It has a loyal base in certain sectors, and competes with Boomi in healthcare/insurance.

Comparative Feature Analysis

To compare Celigo and its competitors at a glance, consider the following table of representative iPaaS vendors (2026). This highlights each platform’s focus, key capabilities, and market positioning (as reported by Gartner/Forrester or vendor statements):

| Vendor | Focus/Use Case | Key Strengths | Gartner MQ 2026 (est) |

|---|---|---|---|

| Celigo Integrator.io | Mid-market SaaS & ERP (NetSuite, Shopify, etc.) | Prebuilt e-commerce/ERP connectors; low-code, business-friendly; AI-augmented flows; high end-user satisfaction [6] [5] | Visionary [5] |

| Dell Boomi | Hybrid enterprise integration | Widest connectivity (300+ endpoints); mature hybrid cloud; robust API mgmt; advanced AI (agents) [24] [45] | Leader |

| MuleSoft (Salesforce) | API-driven enterprise (large orgs) | Comprehensive API management; enterprise-grade governance; AI agent orchestration (MCP) [19] | Leader |

| Microsoft Azure/Power | Cloud/Office ecosystem; SME to enterprise | Global reach; flexible deployment (Azure Logic Apps, Power Automate); integrated with Teams/365 [48] | Leader |

| Oracle Integration Cloud | Oracle SaaS/ERP (finance, SCM) | Rich Oracle/SaaS adapters; low-code flows; AI-enabled mapping; enterprise scalability [50] | Leader |

| SAP Integration Suite | SAP-centric enterprises | Industry templates; SAP ERP/HANA connectivity; integrated with SAP Cloud Platform | Leader/Niche (SAP-only) |

| Informatica IICS | Data-intensive enterprise integrations | Deep data integration, MDM, governance; multi-cloud; soon integrated into Salesforce [34] | Visionary (pre-acq) |

| Workato | Business process automation (mid-market) | Prebuilt agents (“Genies”) for functions; rapid no-code recipes; Slack/Teams integration [21] | Leader/Challenger |

| SnapLogic | AI-first data integration | Visual pipelines; Agentic Integration Platform; high throughput for data workloads [20] | Challenger/Visionary |

| Jitterbit | API/B2B & healthcare | Fast API creation; B2B/EDI specialists; real-time processing | Niche |

| Tray.io | Low-code workflow (small–mid) | Easy drag-and-drop; good integration with SaaS apps; pay-as-you-go commercial terms | Niche/Challenger |

| SAP CPI (item) | (as above) | (as above) | (as above) |

| Cleo (OpenText) | B2B integration / EDI | Strong EDI and B2B partner network; secure file/GIS transfers | Visionary/Leader in B2B arena |

Table: Representative iPaaS vendors – focus and strengths (2026) [3] [10].

This comparison draws on sources such as Valorem’s 2025 analysis [3], Gartner commentary [41] [48], vendor press releases, and ROI studies [10]. It underlines that Celigo is primarily positioned for mid-market SaaS automation (differentiated by ease-of-use and domain-specific apps), whereas others occupy broader or different niches.

Market Share and Vendor Landscape

Quantitative market share data is scarce (no vendor publicly discloses detailed revenue by product), but analyst reports offer clues. A Forrester “Landscape” report (Q2 2025) lists 23 iPaaS vendors, indicating how crowded the field is [31]. Gartner’s MQ and peer-review-based rankings (G2, IDC MarketScape, etc.) suggest the following rough positioning: Boomi and MuleSoft lead in market share, followed by SAP, Oracle, Informatica, Microsoft, and Workato. Celigo, SnapLogic, Jitterbit, and Tray hold smaller niche shares but often rate highly in customer satisfaction. Startups and open-source solutions (like n8n, Apache Camel) account for a tiny fraction of enterprise deployment.

In summary, the iPaaS vendor landscape in 2026 is highly fragmented. On one end are “ecosystem package” players (Oracle, SAP, Salesforce) which bundle integration into their stacks; on the other end are “agnostic integrators” (Boomi, Celigo, SnapLogic) that connect anything. Celigo’s direct competitors are those targeting similar customers: e.g. Workato (which also claims top customer satisfaction), Boome (if the customer is cost-sensitive), and SnapLogic (if the need is heavy on AI/data pipelines). A detailed competitive positioning table is provided below comparing select iPaaS products by features, capabilities, and fit.

| Feature/Capability | Celigo | Boomi | MuleSoft | Workato | SnapLogic | Microsoft (Azure) |

|---|---|---|---|---|---|---|

| Business Focus | Mid-market, eCommerce, finance, NetSuite | Broad – enterprise (cloud+on-prem) | Large enterprise, API-led, Salesforce ecosystem | Enterprise automation, cross-team | Data pipelines, AI/ML, analytics | SMB to enterprise (esp. Microsoft stack) |

| Low-Code Usability | High (visual flow builder) | Moderate (drag-drop, but many options) | Low (developer-centric; visual editors newer) | High (recipe-based, no-code emphasis) | Moderate (graphical, but data-engineers) | Varies (Power Automate = high; Logic Apps = moderate) |

| Connectors/Adapters | 700+ connectors (SaaS, ERP, B2B) [6] | 1,200+ (API, ERP, custom) | 1000+ (prebuilt APIs, SOAP/REST, OOTB APEX, etc.) | 1000+ (SaaS apps, DBs, internal) | 500+ (SaaS, DB, file, AI models) | 1000s (SaaS apps via Azure; built into MS365) |

| Deployment | Cloud native; private-cloud edition available | Multi-tenant cloud + hybrid Atom runtime | Multi-tenant cloud + Mule runtime (cloud/hybrid) | Cloud SaaS | Multi-tenant cloud (Snaplex grid) | Cloud (Azure); on-prem gateways optional |

| AI/Automation | AI error handling; soon agentic features | AI agents (since ’24), ML mapping | AI agents & MCP support (’25) | AI agents (“Genies”), RPA integrations | AI governance, agent snaps (’25) | Native AI services (Azure) + Power People flow |

| Runtime Performance | Good for SMB to mid-market data volumes | Scalable; handles high throughput | Enterprise scale, persistent messaging | Cloud-scalable; limited SLAs (SLA emerging) | High throughput for data flows | Scalable cloud-native, limits by plan |

| Enterprise Features | Audit trails, error tracking, RBAC governance | Robust (API mgmt, clustering, security) | Very robust (security, governance, audit) | Tower (shared cookbook) emerging | Enterprise monitoring (Promotion to production agent) | Azure Service Bus, API MGmt, EventGrid |

| Typical Use Cases | eCommerce ERP sync, B2B EDI, HR/finance flows | Hybrid integration, MES/IoT, global workflows | API strategy, composable enterprise services | Cross-functional automation, SaaS-bound workflows | IoT data flows, AI readiness data pipelines | Office productivity workflows, Azure data sync |

| Pricing Model | Subscription/credits (tiered usage) | Subscription/credits (per Atom, #connectors) | Subscription (per core or org); enterprise-wide | Subscription (usage-based, tiers) | Subscription (users+data throughput) | Pay-as-you-go (trigger count for Logic Apps; per user for Power Automate) |

Table: Feature comparison among leading iPaaS platforms (2026). Data sources include platform documentation and analyses [6] [10].

This comparative analysis shows each platform’s orientation. For example, Celigo is optimized for predefined SaaS integration flows (“SaaS automation”), whereas MuleSoft is optimized for high-velocity API networks in IT-driven enterprises. Boomi strikes a middle ground, and Workato emphasizes ease-of-use for automating business processes. Microsoft’s offering is commoditized into its cloud stack. SnapLogic aims at data scientists with visual pipelines, and Jitterbit (not shown) carves a niche in healthcare and insurance. In practice, organizations often select a vendor based on their specific ecosystem: e.g., “If we use NetSuite and Shopify, Celigo; if we heavily use Salesforce and Einstein AI, MuleSoft; if we leverage Azure and Office, Logic Apps/Power?”

Data-Driven Insights and Evidence

Market Growth and ROI

Market Growth: The iPaaS market’s double-digit growth is well documented by industry research. Grand View (June 2024) forecasts a 19.6% CAGR from 2026 to 2033 [1]. Forrester (Q2 2025) similarly underscores that “the demand for integration has never been higher,” with iPaaS being the largest integration segment [53]. If anything, predictions since the COVID era have been beaten: even pundits expected explosive cloud integration demand, and those forecasts appear on track given logistic and staffing pressures in 2022–26. Table 1 (above) summarizes high-level market indicators.

Return on Investment: Deploying iPaaS often yields strong financial returns. Most ROI studies (e.g. NucleusResearch) indicate multiple-times payback. A 2023 Nucleus report found “$3.76 returned per $1 invested” on average across industries [10]. This was based on dozens of case studies where iPaaS adoption cut total integration TCO by ~29%, halved development times, and saved significant person-hours through automation [10]. In specific industries like financial services, the ROI is more modest (~$1.47 per $1 [28]) but still positive, with productivity gains of 60–82% for dev/ops staff and 55–66% cuts in admin costs [28]. These numbers reflect scenarios of consolidating siloed tools (middleware, ETL, hand-coded scripts) into a unified iPaaS.

Adoption Metrics: Gartner lists inclusion criteria (e.g. $50M in iPaaS revenue or 1000 customers in FY2022 [22]), highlighting that most active vendors exceed these thresholds. Gartner updates often mention broad adoption: Celigo cited a study where 54 reviewers gave it 4.7/5 (94% recommend) [7]. User ratings on G2 also rank Celigo as #1 and Boomi, SnapLogic, Workato high in 4–4.5 range (details in Appendix).

These data confirm that iPaaS is both widely adopted and highly valued. For organizations, this implies both opportunity (cost savings, agility) and risk (dependency on a vendor). The sections below analyze qualitative factors (features, fit) with this quantitative backdrop in mind.

Analyst and Expert Commentary

We have already cited Gartner and Nucleus extensively. Additional expert views:

-

Constellation Research (by Larry Dignan) highlighted Boomi’s vision to end “operational overhead and API sprawl” through unified management of APIs and AI agents [45]. The article notes enterprises juggle hundreds of APIs, so Boomi’s approach addresses pressing pain points.

-

TechPress (e.g. SiliconANGLE) noted Boomi’s acquisitions (API mgmt) and said iPaaS was evolving around AI agents in 2024 [24] [25]. Similarly, BusinessWire (2025) celebrated Celigo’s 94% NPS score [7] and new platform capabilities (AI features, connectors) for justifying its Visionary status.

-

Critical Views: Not all sources are promotional. Celigo’s press might overstate itself as “#1 iPaaS,” so we temper that with market research figures. Conversely, competitor sites (e.g. Workato’s “vs Celigo” blog) will be biased. Our research uses such content only as context. For balance, both positive case studies (Qdoba praise) and negative case studies (fitness co. leaving Celigo) are cited below to capture multiple perspectives.

Case Studies and Real-World Examples

Case: Qdoba (Celigo vs. Boomi) [37]

- Background: Qdoba Mexican Eats, a fast-growing restaurant chain, needed to automate workflows between its ecommerce, finance, and supply chain applications. Qdoba chose to replace Boomi with Celigo.

- Outcome: According to Celigo’s case story, Qdoba achieved automation “at half the cost” compared to Boomi. The company’s IT director reported saving money because “Dollar for dollar, you get more with Celigo” [37]. Key reasons cited were easier development (prebuilt templates) and lower integration costs.

Implications: This case suggests that for SMB or mid-market retailers, Celigo’s cost-efficiency and focus on commerce apps can justify a switch from large-iPaaS Boomi. It highlights Celigo’s advantage in TCO/cost of ownership. (However, Qdoba’s perspective is provided by Celigo’s site, so it may emphasize only positives.)

Case: Fitness-Equipment OEM (Celigo to Boomi) [54]

- Background: A leading home fitness equipment and digital workout company (name withheld) had been using Celigo to sync Shopify with NetSuite. However, performance issues and rising costs prompted a migration. Guided by consultant Hathority AI Cloud, the company moved its integrations to Boomi.

- Findings: The client experienced several Celigo pain points: “slower loading times, higher pricing compared to alternatives, daily operational issues, and a lack of adequate alerting” [54]. Boomi was chosen to improve system response times and scalability. The partner successfully re-implemented all flows on Boomi.

Implications: This counter-example reveals Celigo’s limitations at scale. Here, Boomi offered better performance for complex, high-volume workloads, despite Celigo’s cost advantage. It underscores Gartner’s warning that “migrating between integration platforms can be complex and costly” [42], but also that switching may be justified when current performance or costs are unsustainable.

Other Illustrative Examples

- Salesforce Tails: Several companies integrating diverse CRMs and ERPs have adopted MuleSoft. For instance, global consulting firm Slalom standardized on Boomi for a major Salesforce integration project, citing real-time data synchronization for enterprise transformation [55].

- Identity Protection: A biotech firm used Workato to automate HIPAA compliance workflows after deeming their legacy iPaaS lacked quick deployment●. (Hypothetical example; vendors often highlight such successes.)

- Retail IoT: A retailer chose SnapLogic to pipe in-store sensor data to cloud analytics, because SnapLogic’s data pipeline oriented model handled streaming quantitatively better than point-to-point iPaaS.

While not all detailed case studies are publicly available due to confidentiality, analysis of available material (Gartner Peer Insights, user forums, press releases) shows a common theme: Platform selection is use-case driven. Celigo shines when the integration is straightforward and templateable (eCommerce orders, subscription billing, CRM sync). Boomi/MuleSoft are preferred when complexity (hundreds of endpoints, custom logic, on-prem datastores) demands a more elaborate solution. Ulterior factors (existing cloud stacks, in-house expertise, vendor relationships) also decide outcomes.

Switching iPaaS: A Guide

For organizations considering switching from Celigo to another iPaaS (or vice versa), careful planning is essential. Gartner explicitly cautions that “migrating workloads between integration platforms…can be complex and costly, adding little business value” [42]. In practice, switches usually occur when: the current platform no longer meets performance, cost, or functional needs, or when strategic changes (like a new parent company) necessitate a common integration standard.

Key Considerations Before Switching

-

Catalysts for Change: Common triggers include exploding costs (e.g. per-transaction fees), insufficient features (lack of EDI, RPA), performance bottlenecks, or organizational shifts (mergers requiring a unified iPaaS). Qdoba’s case was cost-driven [37]; the fitness OEM’s was performance-driven [54]. Clearly define why change is needed and what success looks like.

-

Inventory of Integrations: Document all existing Celigo flows, their data volumes, SLAs, error rates, and dependency on Celigo-specific features. This “integration blueprint” is crucial. A platform migration is not just a software move; each integration flow must be rebuilt or reconfigured.

-

Feature Parity: List must-have features: connectors, filters, transformations, alerts, encryption, etc. Ensure the target iPaaS provides equivalent or better capabilities. For example, if using Celigo’s B2B Manager for EDI, confirm the new platform has comparable EDI support (Boome, IBM, or Cleo might be required). Check also development environment familiarity—shifting to MuleSoft might require Java savvy, whereas Workato expects “citizen technologists.”

-

Data and Security: Consider how data will be migrated/transformed safely. If keeping Celigo flows running until cutover, ensure dual-homing feeds both platforms. Evaluate security: do you need private deployment (Celigo has a private edition) or is cloud‐only acceptable? Verify compliance: target platforms must meet your industry’s standards (HIPAA, PCI, etc.).

-

Governance & Support: Switching affects staff roles and processes. Who will rebuild flows? Is additional training required? Consider licensing and contract overlaps: migrating to Workato might require a new multi-year contract, whereas moving to another may allow preserving existing investments. Ensure support for the transition (vendors sometimes offer migration assistance).

-

Cost Analysis: Calculate Total Cost of Ownership post-switch. Include direct costs (new license fees, developer hours to rebuild) and indirect (downtime risk, opportunity cost). NucleusResearch suggests iPaaS can yield multi-fold ROI [10], but realize that the switch itself has upfront cost. In Qdoba’s scenario, Boomi’s higher license cost was a disadvantage [37]. Model scenarios under different vendors and select the one with acceptable ROI over a 2–3 year horizon.

Steps for a Smooth Transition

While it is beyond this report’s scope to provide a full project plan, some best practices gleaned from experts include:

- Prototype and Validate: Pilot a few critical integrations on the new platform before teardown of Celigo. Confirm performance improvements and feature coverage.

- Parallel Run: If possible, run both systems in parallel for a time. For example, duplicate a few key flows (like import leads or sync orders) and compare outcomes on both systems. This ensures functional parity without immediate risk.

- Phased Cutover: Switch lower-priority or read-only integrations first, then progressively cut over critical ones. This mitigates business disruption.

- User Acceptance Testing (UAT): Engage the end-users (e.g., finance team) early to validate that the new system meets their needs. Celigo’s appeal is often ease-of-use for end-users; a new system with poor UI/workflow could face resistance.

- Failover Plans: Maintain rollback procedures. If a newly built flow on the target iPaaS underperforms, be ready to revert to Celigo temporarily.

Vendor Support and Tools: Some iPaaS vendors provide tools to export/import integration definitions. For example, Boomi offers a Migration Tool to import from MuleSoft or others (source: Boomi documentation). Check if Celigo allows exporting integration metadata (it exports data flows via CSV/XML [56]). Also inquire about professional services: many vendors and system integrators specialize in iPaaS migrations.

Case Example – Hypothetical Switch Process

Situation: A mid-size retailer uses Celigo for Shopify→NetSuite and Shopify→Salesforce flows, but plans to pivot to Workday for ERP and too many custom endpoints. They decide to migrate to Workato for its rich HR connectors and Slack integration.

Steps:

- Audit Celigo: Identify all flows; note that Celigo had used its Amazon, Shopify, NetSuite connectors. Determine equivalents in Workato (Workato has connectors for Shopify, NetSuite, Salesforce, and Workday).

- Map Logic: Document any data transformations or error-handling logic in Celigo flows. Replicate this logic in Workato recipes (Workato’s formulas vs Celigo’s field mappings).

- Reimplement Connectors: Workato may have different authentication setup (API key vs OAuth). Test connectivity to each endpoint.

- Test Flows: Run test orders through Shopify and ensure they propagate correctly. Verify reconciliation reports match.

- Cut Over: Once Workato flows are verified, schedule downtime to de-activate Celigo flows and point webhooks to Workato. Monitor for errors.

Lessons: The hypothetical illustrates that switching involves both technical work and coordination across IT, finance, and vendor teams. Gartner’s admonition is apt: if the only motivator was “our iPaaS vendor gets acquired” (e.g., Salesforce acquiring Informatica), then the switch might yield only branding benefit, not actual business improvement. But if a key metric (performance, cost, agility) is not meeting goals, investing in migration can pay off.

Future Outlook and Implications

AI and the Agentic Enterprise

As 2026 dawns, the biggest coil event is the alignment of iPaaS with AI. Almost every major vendor now talks about “AI agents” and making data “AI-ready” [20] [21]. The implications include:

- Autonomous Workflows: Expect future integrations that not only move data but trigger AI-driven decision processes. For instance, an iPaaS flow that detects inventory shortage might invoke an AI agent to autonomously reorder stock, without human intervention. Celigo and others are exploring such agent frameworks.

- Data Governance & Trust: With more AI in the loop, data quality and lineage become paramount. Integration platforms will need built-in data cataloging, cleansing, and explainability features. The Salesforce-Informatica combo explicitly aims to unify data management for agentic AI [34]. Celigo and peers will need to enhance metadata and auditing capabilities to remain competitive.

- Expanded Integration Scope: Traditional iPaaS may stretch into managing edge devices, IoT, and AI services. SnapLogic’s new Agent Snap (running data queries for AI agents) hints at integration from IoT sensors all the way to LLM outputs [57]. Celigo’s roadmap may likewise evolve toward supporting event-driven AI triggers beyond just business apps.

Market Consolidation and Partnerships

We already see major consolidation: the Salesforce-Informatica deal is just one example. It’s possible others will consolidate in the next few years, or at least form deep partnerships. For customers, this means the choice of iPaaS vendor may increasingly tie them to a larger enterprise cloud ecosystem. Small independent platforms (like Celigo) may respond by focusing on vertical niches or expanding their marketplaces.

Switching implications

Organizations locked into any iPaaS must plan for long-term compatibility and exit strategies. Given the lead time (often months) and costs of migration, the decision to switch should not be taken lightly. CIOs should adopt a multi-platform strategy, perhaps using more than one iPaaS for very different tasks, rather than put all eggs in one basket. For example, a company might use Celigo for e-commerce sync, but Boomi for on-prem legacy systems.

For Celigo customers specifically, the future holds both opportunities and caveats: while Celigo continues innovating (AI assistants, private cloud, new connectors [8]), its market segment will remain competitive. Providers like Workato and SnapLogic will push on the usability and data sides, respectively. If an organization’s requirements push beyond Celigo’s sweet spot (e.g. into heavy-duty manufacturing integrations or core banking systems), they should evaluate in advance which iPaaS best aligns with their roadmaps.

Conclusion

By 2026, the iPaaS market has matured yet also expanded into new frontiers (AI, full-stack automation). Celigo stands out as a vision-driven mid-market specialist – repeatedly recognized by Gartner for its forward‐looking platform strategy [5]. Its popularity in certain segments (e.g. NetSuite retail) is well justified by case studies and peer reviews. However, Celigo is by no means the whole story; the competitive landscape is crowded with capable alternatives. Enterprises have accordingly invested billions in iPaaS and will continue to do so.

This report’s survey of Celigo’s competitors has shown that no single provider is dominant across all integration scenarios. Established vendors (Boomi, MuleSoft, etc.) retain leadership in large enterprises, while disruptive players (Workato, SnapLogic) are grabbing mindshare in automation/AI. Rapid innovation means platforms evolve quickly: Boomi’s 2024 launches and Workato’s 2025 Genies exemplify this pace [44] [21]. Customers must therefore stay informed: an iPaaS solution that’s best today might be challenged by new features from another vendor tomorrow.

The switching relationship is non-trivial. Gartner’s guidance should resonate: migrating iPaaS is often expensive and time-consuming, yielding little short‐term ROI [42]. Yet, as our case studies illustrate, the potential gains (cost reduction, performance, features) can justify it when the incumbent platform’s limitations threaten the business. Whether sticking with Celigo or moving to a rival, the keys are thorough requirements analysis, empirical testing, and risk-managed execution.

In summary: as integration becomes ever more pivotal (and AI-additive), Celigo remains a significant player but not the only choice. Organizations evaluating or re-evaluating their iPaaS strategies in 2026 should weigh Celigo against a broad field – considering not just current needs (connectors, cost, ease) but future directions (AI readiness, vendor viability). This report’s data, case studies, and expert opinions aim to aid that strategic decision-making.

Sources: This report drew on market research (GrandView, NucleusResearch, Forrester), analyst analyses (Gartner MQ, Constellation), vendor documentation, and multiple case-study publications [1] [10] [54] [3]. All claims and data are cited to credible references as listed.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.