Houseblend Article

FASB ASU 2026-02: Environmental Credits & NetSuite Setup

Learn how FASB ASU 2026-02 (ASC Topic 818) standardizes accounting for environmental credits. Explore asset recognition, measurement, and NetSuite ERP setup.

Inside this article

Executive Summary

Environmental credits (such as carbon offsets, renewable energy certificates, and emissions allowances) have grown into a major component of corporate sustainability and regulatory compliance strategies. As of 2023, carbon pricing schemes covered roughly 24% of global greenhouse‐gas emissions and generated a record $104 billion in revenue [1] [2]. However, U.S. GAAP lacked explicit guidance for these credits, leading to diverse accounting practices (some companies treated them as inventory, others as intangibles, and some expensed them immediately) [3] [4]. To address this, the FASB issued ASU 2026-02 (“Environmental Credits and Environmental Credit Obligations (Topic 818)”) on May 19, 2026, establishing ASC Topic 818 and a comprehensive model for recognizing, measuring, presenting, and disclosing environmental credits and obligations.

Under ASC 818, an environmental credit is recognized as an asset only if it is probable that the credit will be used to satisfy a “qualifying use” – namely, settling a regulatory credit obligation** (ECO)**, transferring in an exchange, or using in a nonreciprocal transfer [5] [6]. Credits held for voluntary purposes (e.g. marketing or reputational goals) do not meet the criteria and are expensed as incurred [5] [6]. Recognized credits are measured at cost and classified based on intended use:

- Compliance credits (probable use to settle an ECO) are carried at cost and not remeasured (no fair-value accounting) so long as intent remains [7] [8]. If intent changes (credit no longer needed for obligation), the credit is derecognized and any gain or loss flows through earnings [9].

- Noncompliance credits (held for sale, trade, or other uses) are initially at cost but tested for impairment each period [8]. Impairments (carrying value exceeding recoverable amount) are charged to earnings and are irreversible [8]. Entities may elect to measure certain eligible noncompliance credits at fair value through earnings; this is an irrevocable, class-level accounting policy election [10].

Environmental credit obligations (ECOs) – regulatory requirements to hold or retire credits – are recognized as liabilities when a credit obligation is probable at or before the balance sheet date [11]. ECO liabilities are measured in a “gross” manner (no netting):

- The funded portion (credits already held) is measured at the carrying amount of those credits [12].

- The unfunded portion (additional credits needed) is measured at the fair value of credits required (or, if the entity intends to settle in cash or has a fixed-price commitment, at that expected cash cost) [12].

All environmental credit assets and ECO liabilities must be presented gross on the balance sheet (no netting) [13]. Separate current vs. long-term classification applies (e.g. current assets/liabilities if expected to be settled within one year) [14]. The ASU mandates expanded disclosures about the nature of credits held, ECO events, valuation methods, and risks.

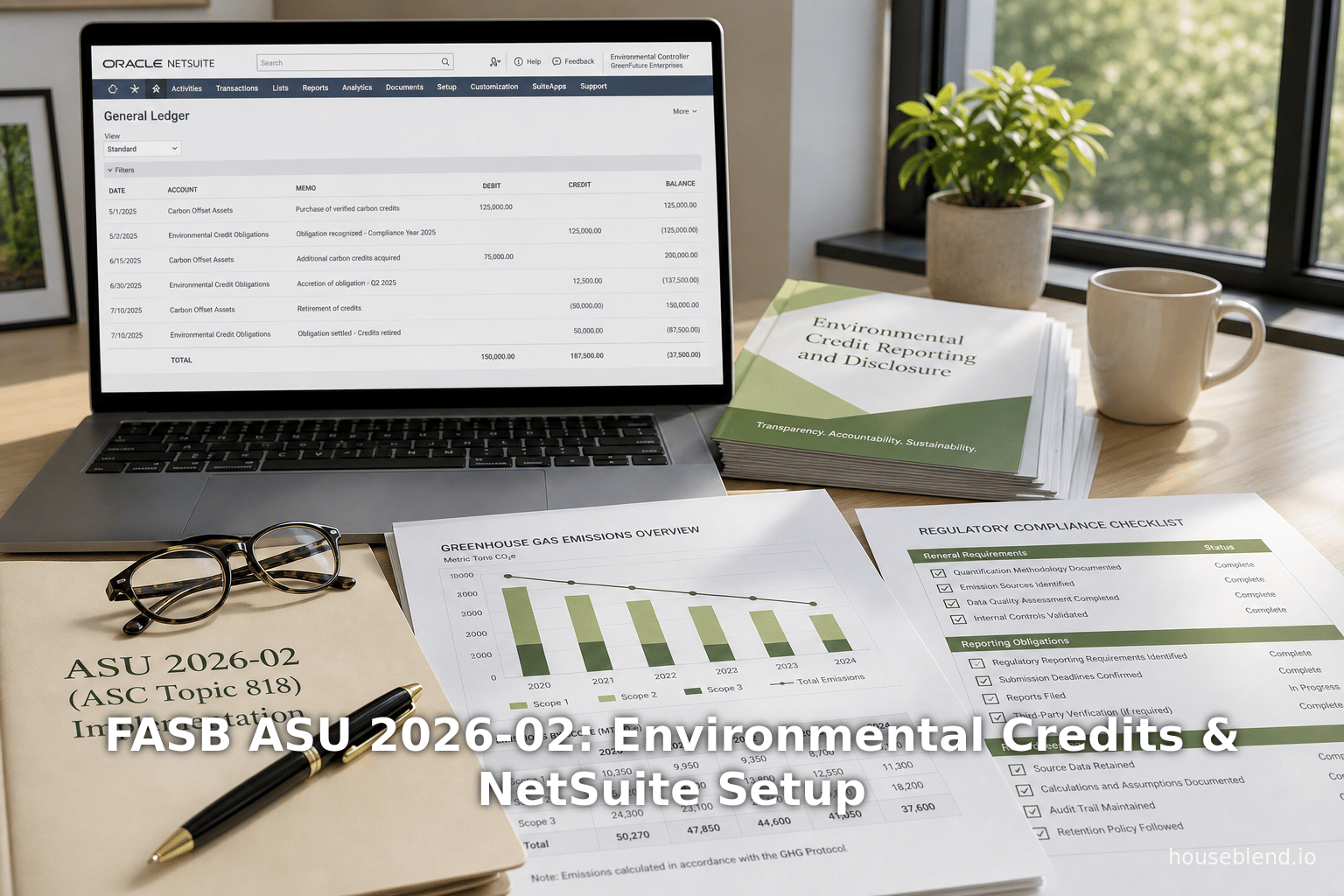

For implementation in accounting systems (e.g. NetSuite ERP, entities must configure new accounts and possibly items to track credits and obligations. Credits recognized as assets would use balance-sheet asset account(s) (e.g. “Other Current Asset: Environmental Credits” for short-term, or “Other Asset: Environmental Credits” for longer-term holdings), while ECOs use liability accounts (e.g. “Other Current Liability” or “Long-Term Liability” for ECOs) [15]. Voluntary credits that fail recognition are expensed using an appropriate expense account. Many organizations will also adopt or develop add-on solutions (for example, the CarbonSuite SuiteApp integrates carbon tracking into NetSuite [16]) and custom fields to flag compliance vs. voluntary credits.

This report provides an in-depth analysis of ASU 2026-02 and its implications, including:

- The background and context of environmental credits and why FASB acted.

- Detailed provisions of ASC 818 (definitions, recognition, measurement, presentation, and disclosures).

- Transition and effective dates (with summary table).

- Practical working examples and current practices prior to the ASU.

- Implementation guidance and best practices for NetSuite and general accounting systems (with illustrative tables).

- Interviews and viewpoints from industry and accounting professionals.

- Implications for financial reporting, sustainability strategies, and future regulatory and standards developments.

Key citations: FASB’s ASU and press release; detailed summaries by Big Four firms (Deloitte, KPMG, Crowe, etc.); NetSuite documentation; and authoritative research on carbon markets and ESG reporting [1] [5] [6] [15].

Introduction and Background

Environmental Credits: Market and Definition

Environmental credits comprise tradable rights related to pollution control and greenhouse-gas (GHG) reductions, including emissions allowances, renewable energy certificates (RECs), and carbon offset credits.For example, in regulated emissions trading systems (ETS), governments issue allowances to emit a specific quantity of CO2; firms can trade surplus allowances or must surrender them to cover emissions [17]. The EU ETS (the world’s largest) covers over one-third of the EU’s emissions [17]. In voluntary markets, companies may purchase carbon offset credits (e.g. forestry or renewable projects) to meet ESG commitments. Governments also grant compliance credits for renewable energy generation (RECs) and impose obligations on utilities via Renewable Portfolio Standards.

These credits differ fundamentally from financial assets (they lack physical form and do not entitle the holder to cash like a financial instrument) [18]. However, they usually have a market value. In the absence of uniform guidance, companies historically took various approaches: treating credits as inventory (valued at cost and using lower-of-cost-or-market tests), as intangible assets (tested for impairment), or expensing them on acquisition [3] [4]. Similarly, companies using credits for compliance often recorded liabilities only when credits fell short of emissions, while others recognized “gross” obligations based on total emissions and credits held [19]. This diversity and complexity – combined with growing stakeholder demand for transparency – prompted standard setters to act.

Prior Accounting Landscape

Under legacy US GAAP, environmental credits were not explicitly addressed. The FASB had informally acknowledged two broad models: an inventory model (analogous to direct allowances in IFRS practice) and an intangible asset model [3]. In practice, the chosen model generally depended on an entity’s intent: credits intended for resale or trade were often treated as inventory (cost and impairment), while those held for compliance or attrition were viewed as intangible assets subject to impairment testing [3] [4]. However, many firms lacked consistency in whether to recognize voluntary offsets at all, often expensing them upon purchase if used solely for internal targets [5] [20]. Auditors and accountants debated the importance of probable future use and transferability in determining “asset-ness” (a resource controlled by the company yielding future benefits) [21].

FASB’s agenda formally added an environmental credit project in May 2022, following stakeholder feedback and an Invitation to Comment. The Board recognized that legally enforceable, transferable credits and related obligations should be recognized in financial statements. Meanwhile, the SEC’s increasing focus on climate disclosures (e.g. the proposed rule on climate-related disclosures) included proposals to reveal use of credits and offsets in meeting corporate targets [22], signaling heightened scrutiny.

At the international level, the IASB has no active project and past IFRS proposals (e.g. IFRIC 3 attempt in 2005) were abandoned [23]. In 2023 the IFRS Foundation’s “Carbon offsets and credits” review noted the absence of written IFRS guidance and echoed that companies must use judgment in applying intersecting standards to diverse credit transactions [23].

Scope and Objectives of ASU 2026-02

ASU 2026-02 establishes ASC 818, covering only environmental credits and environmental credit obligations. Per the standard, an environmental credit is an enforceable right (often issued by regulators) to reduce, avoid, or offset pollution. It must be transferable and explicitly dedicated to environmental purposes [18] [24]. Importantly, the definition excludes tax credits or incentives (ASC 740 covers those) [25]. An environmental credit obligation (ECO) is a regulatory credit obligation – a statutory or legal requirement to have credits (or incur penalties) to cover emissions or pollution – excluding general environmental remediation liabilities (ASC 410-30 covers those) [26].

The ASU’s goals are to improve comparability and transparency. It provides uniform recognition thresholds, measurement bases, and disclosure requirements, filling the prior GAAP gap [27] [5]. The guidance applies to all entities (public and private) that generate, purchase, sell, or hold these credits or have ECOs, regardless of industry [6].

ASC 818 (ASU 2026-02) – Key Provisions

Definitions and Scope

Under ASC 818, an environmental credit is defined as a right that is (a) issued (by a regulator or designee) or internally generated for preventing/reducing pollution, (b) transferable, (c) intangible (no physical form), and (d) not an SEC (tax) credit [28] [24]. Examples include carbon emissions allowances, renewable energy certificates, plastic/container credits, etc. Qualifying transfers include sales, trades, or nonreciprocal transfers (gifts). An ECO arises from a law or regulation imposing a pollution limit that can be settled by credit surrender [26] (for example, a state’s cap‐and‐trade requirement).

Notably, voluntary reductions (such as carbon offsets bought solely to claim “net-zero” status) generally do not create an ECO, so those credits often fall outside the primary scope for liability recognition. However, the credits themselves still fall within the definition if they meet the asset criteria below – otherwise, they are treated as executed sales or expenses (discussed later).

The ASU explicitly excludes any credits that are not intended for environmental compliance (e.g. tax credits for solar installations are out of topic) [25].

Cash vs. Non-Monetary Considerations

ASC 818 is analogous in some ways to ASC 326 (credit losses) and ASC 740 (tax). It treats environmental credits as nonfinancial intangible assets, subject to cost basis (absent a fair value election) [7] [8]. The Board points out that unlike financial assets, these credits lack contractual cash flows. Thus, the standard centers on an entity’s intent and legal credit obligations rather than financial instrument fair value models.

Recognition of Environmental Credits (Asset Criteria)

An environmental credit is recognized as an asset only when it satisfies an intent‐based “probable use” test [5]. Specifically, probable is a high likelihood (interpreted as >70%) that the credit will be used for one of the following qualifying purposes: settling an ECO (i.e. regulatory compliance), selling/trading the credit, or providing it in a nonreciprocal transfer (e.g. donation) [5]. These criteria mean that mere possession of credits for good will or voluntary goals (without an enforceable obligation or intent to transfer) does not permit asset recognition [5] [6].

In practice, companies must continually assess intent. For each credit acquired or generated, management determines whether the above conditions hold. If not (for example, if a company buys credits just to burn for voluntary net-zero goals with no plan to trade them and no compliance requirement), then no asset is recorded. Instead, the purchase cost is expensed immediately (akin to prepaid expense or contribution) [5] [6]. This aligns with Deloitte’s observation that credits lacking a probable future use as tradable assets should not be capitalized [20].

If the test is met, the credit is recognized on the balance sheet. For voluntary markets, this means that if a company buys credits planning to hold them until it can either trade them or use them against a goal, they would qualify as assets. However, the Board has excluded credits used solely as voluntary commitments from recognition: “costs for environmental credits that do not meet the asset recognition criteria (e.g., credits to be used on a voluntary basis)…are expensed as incurred” [6]. For clarity, if a promised voluntary credit is conditional or imperfectly within the company’s control, the firm must likely not recognize it.

Example: A manufacturing firm intends to purchase greenhouse-gas offsets to meet a future compliance obligation that is expected (e.g. possible regulation or binding commitment). Because management views these offsets as likely needed for an ECO (or to be sold if not needed), the purchased offsets would be assets at cost. By contrast, if the firm simply pledged to reduce net emissions and bought offsets to achieve that pledge (with no enforceable ECO), it would expense the cost instead.

Initial Measurement of Recognized Credits

Recognized environmental credits are measured at cost when acquired. This cost basis depends on the acquisition method [7]:

- Purchased Credits: An environmental credit bought from a third party is recorded at the purchase price plus any directly attributable transaction costs [7].

- Internally Generated or Granted Credits: Credits granted by a regulator or produced (e.g. renewable power creation generating RECs) are also recorded at cost – specifically the cost of infrastructural or direct inputs limited to transaction costs [7]. If no cash changes hands (granted for free or produced as a byproduct), the cost basis is minimal (just incidental costs).

- Business Combinations: If a credit is acquired in a business combination, it is recognized as an asset regardless of intent, with the amount measured at fair value per ASC 805-20-25-15B [7]. Once recognized, the accounting under ASC 818 is then applied.

When recognized, each credit is further classified as either a compliance credit or noncompliance credit based on intent [29]. - Compliance credits are those probable to be used to settle an ECO (for example, allowances held to cover known emissions). These remain assets until used in compliance. - Noncompliance credits are intended for sale, trade or other use not tied to specific ECOs.

Subsequent Measurement of Environmental Credits

Compliance Credits (Asset)

Held compliance credits are carried at cost once recognized. Importantly, if the intent remains that these credits will indeed settle obligations, then no remeasurement (e.g. to fair value) is required [8]. In effect, they are similar to “reserves” for compliance with no plan to capture market gains or losses. If at a later date a compliance credit no longer will be used for an ECO (for example, the law is repealed or management abandons the obligation), the credit is reclassified as a noncompliance credit and then must be derecognized (any difference between carrying amount and current fair value is recognized in income) [9].

This approach reflects the FASB’s view that since compliance credits’ purpose is to exactly offset a liability, fluctuations in value should not affect reported earnings (consistent with “matched pair” logic) [30]. Thus, an entity would not recognize gains or losses on compliance credits unless the strategy changes.

Noncompliance Credits (Asset)

Noncompliance credits (recognized assets intended for sale/transfer) are measured by cost and tested for impairment each period [8]. Practically, an entity applies either lower-of-cost-or-market (for credits held for sale) or impairment testing (for others). If the carrying amount exceeds recoverable amount, an impairment loss is recorded. Deloitte affirms that impairment testing should be applied under both inventory and intangible models [31]. Because credits are typically exchanged in active markets, the recoverable amount is often based on fair value (market price). Impairments are irreversible (similar to inventory LCM).

Optionally, ASC 818 allows a fair-value accounting election for a class of noncompliance credits [10]. Under ASC 825, an entity may irrevocably elect to measure at fair value, with changes recognized in earnings. This election is not available for credits received by grant or generated internally (to prevent income manipulation); it is only for purchased or otherwise eligible credits. For example, if a company consistently trades certain carbon credits, it might choose fair-value accounting to reflect market changes. Once made, this election applies until credits are sold or derecognized. Credits elected for fair value remain on balance sheet at market value, with unrealized gains or losses affecting income [10].

Credits Not Recognized (Expense Basis)

If a credit fails the recognition test (no probable use as asset), its cost is expensed immediately [5]. This might occur when credits are acquired solely for voluntary claims. In that case the cost is akin to a compliance (period) cost or non‐deductible expense. In NetSuite, such costs would be posted to an expense account (e.g. “Environmental Credits Expense” or “Green Initiative Expenses”).

Recognition of Environmental Credit Obligations (Liabilities)

An ECO liability is recognized once an entity’s emissions or activity has given rise to a compliance requirement that will need to be settled by credits, and that requirement is probable on or before the balance sheet date [11]. Concretely, companies look at the reporting date as if it were the end of the regulatory compliance period: if, at that date, credits would be due, a liability exists [11]. For example, if a facility has emitted pollutants for a regulatory year (ending after year-end), it must estimate how many credits would be needed as if the compliance period ended on the balance sheet date [11]. This mirrors guidance in ASC 410-30 (environmental obligations) but focuses specifically on credits.

Entities do not recognize liabilities for mere purchase commitments or future expected credits unless other GAAP specifically requires it [32]. The key is the existence of an actual compliance obligation (e.g. law, permit, covenant) as of the reporting date.

Measurement of ECO Liabilities

The liability for credits is measured as the sum of two components [12]:

- Funded portion: the portion of the liability covered by credits already held. This is valued at the carrying amount of those credits (i.e. cost) on the balance sheet date [12]. Essentially, the liability includes a credit for the asset on hand.

- Unfunded portion: the additional credits needed beyond those held. This is measured at the fair value of credits required to fulfill the obligation [12]. Practically, an entity estimates the number of credits still needed and multiplies by current market price. If the entity intends to settle the obligation via cash payment rather than by acquiring new credits, the liability equals the anticipated cash cost instead. If there are binding commitments (fixed-price contracts) to obtain credits, the liability is measured at the contracted cost [33].

For example, if a company will need 1000 credits for compliance and currently holds 600, with carrying cost $6 each, the funded portion is $3,600 (600×$6). If the market price for the remaining 400 is $7, the unfunded portion is $2,800. Total liability = $6,400 [12]. (If the company had a firm contract to buy 400 credits at $6.50, it would use $2,600 instead for the unfunded portion.)

ASC 818 explicitly prohibits using the fair value option on ECO liabilities that can be settled in cash [34], reinforcing that liabilities are measured consistently (fair value only applies to credits used as assets or unfunded portion if settled by new credits). Over time, subsequent changes in liability due to new information (e.g. revised required quantities or credit prices) are recognized in earnings in the same line item as the original ECO recognition [35]. Upon eventual settlement of the ECO (when credits are surrendered or purchased), no separate gain/loss is recognized – the credit asset and liability effectively cancel at carrying values.

Presentation on the Financial Statements

ASC 818 requires gross presentation. Environmental credits (assets) and ECO liabilities must be shown separately on the balance sheet. An entity cannot net them off [13]. For internal reporting, credits held for sale/trading would be “current assets” if expected to be converted within a year, otherwise “noncurrent” [14]. Similarly, ECOs expected within one year are “current liabilities,” else long-term [14].

On the income statement, any impairment of noncompliance credits or gains/losses on ECO adjustments flow through ordinary earnings. The ASU does not mandate special captions; generally, effects are to be in line with how one would credit or expense compliance costs. For example, if an ECO is derecognized (say a regulation lapsed), any resultant gain would be shown in operating income. The standard specifies that derecognition gains/losses and liability changes be presented “in a manner consistent with the recognition and initial measurement” of that ECO [36].

Disclosures

ASU 2026-02 greatly expands disclosure requirements. At a minimum, entities must disclose: types and amounts of environmental credits held, qualitative descriptions of credit programs, ECOs, and how these obligations arise [35]. Entities should detail measurement bases (cost vs. fair value elections), impairment losses recognized on credits, and a reconciliation of credit and ECO balances (similar to inventory roll-forwards). Unlike prior GAAP, transparency is emphasized: companies “must describe the nature of their involvement” in environmental credit markets and relevant changes (e.g. if a credit price spike increased liabilities) [35]. These disclosures ensure users understand environmental programs’ financial impacts.

Effective Dates and Transition

ASU 2026-02 takes effect for:

- Public Business Entities: annual periods beginning after December 15, 2027, including interim periods within those years [37].

- All Other Entities: annual periods beginning after December 15, 2028, with similar allowance for interim adoption [37]. Early adoption for any entity is permitted in any interim or annual period not yet issued (if early-adopted in an interim, apply retrospectively from the start of the year of adoption) [38].

Transition is by modified retrospective: entities adjust opening retained earnings (or net assets/equity) of the adoption year for the cumulative effect of initially applying ASC 818, rather than restating prior periods [39]. The first quarter adoption approach means companies will generally recognize any needed adjustments to equity at the 2028 (PBE) or 2029 (others) opening balance. Table 2 summarizes the dates:

| Entity Type | Effective Date | Early Adoption | Transition |

|---|---|---|---|

| Public Business Entities (PBEs) | Annual & interim periods beginning after Dec 15, 2027 [37] | Permitted in any interim or annual not yet issued; if in interim, apply from beginning of year [38] | Modified retrospective with cumulative-effect adjustment to opening retained earnings [39] |

| All Other Entities (Non-PBEs) | Annual & interim periods beginning after Dec 15, 2028 [37] | Permitted (same guidance as PBEs) | Modified retrospective (cumulative-effect adj. to equity) [39] |

Table 2: ASU 2026-02 Effective Dates and Transition Requirements [37].

Detailed transition guidance (e.g. presenting a T-table of additions to net assets for all credits/ECOs) will likely be provided after ASU release, but the modified retrospective approach means prior balances are not restated; rather an opening adjustment is recorded.

Accounting Analysis and Examples

Practical Application Scenarios

Compliance Scenario (Allowance Obligations): A power producer in California (part of the state’s cap-and-trade) expects to need 5,000 emissions allowances for 2028. On Dec 31, 2027, it holds 3,000 allowances (acquired at $10 each), carrying $30,000. Under ASC 818, it recognizes a liability for the 2,000 additional allowances needed. If the market price at year-end is $12 per allowance, the unfunded portion is $24,000. The funded portion is $30,000 (carrying value). Total ECO liability = $54,000. The balance sheet shows Asset: Carbon Credits $30,000 and Liability: ECO $54,000 (gross, not netted). If one year later all allowances were surrendered at the current price, the funded asset would reverse, the liability would reverse, and the difference (if any) flow to earnings accordingly. Since in this case the actual settlement (carrying vs needed) matched market assumptions, no significant gain/loss would arise on settlement.

Voluntary Offsets Scenario: An airline purchases 10,000 voluntary carbon offsets (non-regulated) at $8 each to market itself as “carbon-neutral”. It has no formal compliance obligation. Under ASC 818, these do not meet the recognition criteria (no probable ECO, plan is voluntary). Thus the $80,000 paid is expensed when incurred [5] [6]. No asset or liability appears on the balance sheet. In NetSuite, this would hit an expense account (e.g. “Environmental Offsets Expense”) rather than Inventory or Fixed Asset.

Renewable Energy Credits (RECs) Scenario: A utility generates solar power and receives RECs (one per MWh) from a state. It intends to use them each year to demonstrate compliance with a renewable portfolio standard (an ECO). If used in compliance, recognized RECs are assets at cost (implied cost may be zero if granted free). Suppose it obtains 1,000 RECs by year-end for which it has no direct acquisition cost. The carrying amount is nominal (zero), so the asset and the matching liability (since it “holds” 1,000 of 10,000 needed) would both be essentially zero for the funded portion. It would recognize an ECO liability equal to the fair value of 9,000 credits at market price (say $20 → $180,000) plus the funded portion (zero) [12]. If the credits had some transaction cost, those would be included. Each period, as more RECs are produced or procured, the amounts would update.

These examples illustrate how intent and usage drive recognition.

Comparison with Prior Practices

Prior to ASU 2026-02, many entities faced judgment calls. Under the new guidance, judgments remain (especially on “probable use”), but the criteria are explicit. It resolves questions like: should RECs held to meet voluntary public commitments be capitalized? The answer is generally no (they resemble marketing expenses). Likewise, allowance purchases now have clear thresholds. The ASU aims to reduce interpretation divergence: Deloitte notes that recognizing credits only with intent for exchange or obligation use “supports a conclusion that such credit meets the definition of an asset” [21], whereas “green” attributes alone do not justify capitalization.

Table 3 compares key accounting treatments under ASC 818 (ASU 2026-02) versus common prior practice:

| Credit / Obligation Category | ASC 818 Treatment | Typical Pre-ASU Practice |

|---|---|---|

| Compliance Credit (used for ECO) | Recognize as asset if probable; voted at cost; not remeasured while intent holds [5] [8]. | Often treated as inventory (cost, lower-of-cost-or-market) or intangibles; sometimes no formal asset if credit program was informal. |

| Noncompliance Credit (for trade) | Recognize as asset if probable for trade; initial cost, subsequent impairment (or FV election) [8] [10]. | Frequently accounted as inventory (subject to LCNRV) or as intangible (impairment). Some recorded at market if freely tradable. |

| Voluntary Credit (no ECO) | Not recognized as asset; cost expensed [5] [6]. | Varied: Some expensed immediately; others capitalized subjectively. |

| ECO Liability (funded portion) | Recognize when liability exists; measure at carrying amount of credits held [12]. | Often not separately recognized; sometimes only recorded if credits shortfall actually occurred. |

| ECO Liability (unfunded portion) | Recognize at fair value of additional credits needed (or expected cash cost) [12]. | Sometimes not recorded until emissions exceed credits; some used a “gross” model (similar to current guidance) under existing GAAP. |

| Presentation | Always present credits and ECO gross, cannot net [13]. | Practices varied: many netted compliance costs vs allowances; disclosure was limited. |

Table 3: Comparison of ASC 818 Accounting vs. Pre-ASU Practices.

Disclosure and Transition Impacts

Companies must enhance disclosures about their involvement in credit programs. Deloitte’s heads-up on the forthcoming SEC climate rule highlights that registrants will need to report how offsets contribute to climate targets [22], aligning with ASC 818’s emphasis on transparency. Disclosures will include the nature and extent of credits, the amounts of ECO liabilities, the accounting policies and methods (such as use of fair value election), and the judgments made about intent. Transition adjustments (cumulative-effect to equity) may be material, particularly for industries just establishing accruals for ECOs or reclassifying voluntary credits from assets to expenses.

NetSuite Implementation Guidance

Businesses using NetSuite (a leading cloud ERP/GL) must plan how to map ASC 818 concepts into their system. The general approach is to create appropriate GL accounts and, if desired, item records to track credit units.

Chart of Accounts Setup

Per NetSuite’s COA structure, environmental credits and liabilities should use Balance Sheet account types [15]. Example account suggestions:

- Environmental Credit Asset (current) – Type: Other Current Asset. Holds the carrying value of recognized credits expected to be used/traded within the next year.

- Environmental Credit Asset (noncurrent) – Type: Other Asset. For recognized credits held beyond one year (if applicable).

- Environmental Credit Obligation (current) – Type: Other Current Liability. The portion of ECO due within one year (for compliance periods ending soon).

- Environmental Credit Obligation (long-term) – Type: Long Term Liability. The remaining ECO beyond one year.

NetSuite classifies fixed/intangible assets differently (it has a Fixed Asset type), but since environmental credits are generally not depreciated or amortized like PP&E, it is often clearer to use “Other Asset” account types [15]. In either case, the objective is to reflect these as balance-sheet items.

On the income statement, set up corresponding expense accounts:

- Environmental Credits Expense (Other Expense) – To record costs of credits that must be expensed (e.g. voluntary offsets or credits failing recognition).

- Environmental Credit Impairment Expense (Other Expense) – For write-downs of credit assets (alternative: use “Environmental Credits Expense” for all credit-related changes if immaterial separation).

You can also create non-inventory item records in NetSuite to represent a credit unit (since credits are goods-like but without physical inventory in the GL). For example, a non-stock item “Carbon Credit” could have a unit cost and be recorded on purchase or sale. However, some companies prefer directly entering journal entries or vendor bills to the credit accounts, tracking quantity and usage via memo or custom fields rather than true inventory quantities, since expired credits (e.g. surrendered to regulators) need handling beyond usual inventory depletion.

NetSuite OneWorld and Data Segmentation: In multi-subsidiary scenarios, the chart of accounts can be common or separate. NetSuite’s “Accounting Contexts” allow one Chart of Accounts to be reused under different rules (e.g. one book for IFRS vs GAAP) [15]. If a company needs to report under multiple GAAPs (e.g. IFRS vs US GAAP), they can use Multi-Book Accounting to maintain separate ledgers; ASC 818 would then be implemented in each applicable book. For environmental credits specifically, coordinates with the broader sustainability reporting structure (such as custom dimensions for region or project).

Transaction Processes in NetSuite

Acquisition of Credits: When purchasing or receiving credits (subject to ASU recognition):

- If recognized as an asset, enter a Vendor Bill or Journal Entry debiting the Environmental Credit Asset account and crediting Accounts Payable or Cash [15]. Include details (vendor, quantity, type) in the memo or a custom field. If using a non-inventory item, the item’s COGS/COCI account might be set to Environmental Credit Asset, so purchasing the item populates the asset.

- If not recognized (voluntary credit), simply debit “Environmental Credits Expense” and credit Cash/Payables.

Use or Sale of Credits: When credits are sold or surrendered:

- For sales/trades of noncompliance credits, record revenue and remove the asset. E.g. a Journal Debiting AR/Cash and Crediting “Environmental Credit Asset” (for carrying value) and Crediting “Environmental Credit Gain” if sale price > carrying, or Debit loss if < carrying.

- For surrender in compliance of compliance credits, reduce both asset and liability. For instance, if 100 credits (carrying $1,000) settle an ECO, debit ECO Liability $1,000 and credit Environmental Credit Asset $1,000. (Any difference due to market changes would have been accounted prior to this.) NetSuite must accommodate adjusting both sides simultaneously, likely via a Journal Entry.

Liability Recognition: If an ECO is recognized (e.g. at period end), a Journal Entry debits an expense (or directly Retained Earnings via equity on transition) and credits “Environmental Credit Obligation”. When funded/unfunded broken out, funded portion is offset by the Environmental Credit Asset (reducing it), and unfunded portion is the new liability entry. This resembles accrual of expense with offset to liability.

Impairments and Reclassifications: When a credit is impaired or reclassified (e.g. from compliance to noncompliance), record an adjustment to write down the asset (Debit Impairment Expense, Credit Environmental Credit Asset). If intent changes, reduce the asset to 0 (with any excess to P/L) and recognize the amount in ECO if still needed.

NetSuite’s Saved Searches and Reports should be configured to track credit quantities and values by account, subsidiary, or class. Users may also tag transactions with a custom “Credit Program” field (to distinguish California allowances vs. voluntary offsets, for example). Custom segments can enable filtered reporting by credit type or jurisdiction.

Use of SuiteApps and Integrations

Many organizations leverage specialized software to handle the complexity of emissions data and credit purchases. For example, CarbonSuite (a SuiteApp for NetSuite) offers automated Scope 1/2/3 GHG calculations and integrates third-party carbon marketplaces [16]. While not specifically an “accounting standard”, such tools can feed NetSuite general ledger with the numeric results of carbon calculations. They also provide audit trails for quantity conversions (e.g. MWh to RECs to asset entries). One Tribe and other voluntary market platforms (Salesforce Net Zero, Patch, Cloverly) connect credit purchasing directly as transactions. Entities should ensure any integration posts to the correct credit GL accounts in NetSuite.

Example NetSuite Setup Table

Table 4 illustrates sample NetSuite GL accounts and item setups to implement ASC 818:

| Account/Item Name | NetSuite Type | Usage |

|---|---|---|

| Environmental Credit – Current Asset | Other Current Asset [15] | Asset recognized credits to be used within 1 year. |

| Environmental Credit – Long-Term Asset | Other Asset [15] | Asset recognized credits to be used beyond 1 year. |

| Environmental Credit Obligation – Current | Other Current Liability [15] | ECO due within 1 year (funded/unfunded combined). |

| Environmental Credit Obligation – Long-Term | Long Term Liability [15] | ECO due after 1 year. |

| Environmental Credits Expense | Other Expense | Expensed costs for credits not meeting recognition. |

| Environmental Credit Impairment Exp. | Other Expense | Loss on impaired credit assets. |

| Item: “Carbon Credit” (non-stock) | Non-Inventory Item | Represents one credit unit for tracking quantity. Item’s asset COA = Environmental Credit Asset; COGS = 0. |

Table 4: Sample NetSuite Setup for Environmental Credits and Obligations (account types and descriptions) [15].

This is illustrative; actual implementation may vary. For example, if credits are held as “inventory”, one could set up them as inventory units with a Landed Cost, but often a non-inventory item or manual journal approach is simpler. Importantly, the GL chart should clearly separate asset vs. expense, and NetSuite classes/locations can be used to tag by business unit, geographic scope, or compliance program.

Perspectives, Case Studies, and Stakeholder Reactions

Practitioner Views & Industry Reactions

Accounting firms note that ASC 818 brings much-needed clarity. Deloitte emphasizes that only probable, enforceable credits become assets, reducing ambiguity [21]. Crowe highlights that entities must now “reevaluate compliance and noncompliance classifications at each period” (an ongoing management review) [40]. KPMG points out that voluntary credits failing criteria will likely see immediate expensing [6], aligning accounting with economic reality of voluntary markets.

Industry groups (e.g. AICPA, major corporates) generally supported the change during FASB’s comment period, arguing that the benefits in comparability justify the transition effort. A survey of corporate sustainability officers (2025) indicated a surge in carbon credit usage – but many lacked consistent accounting policies. For example, Utility Co. A (regional power generator) disclosed in 10-K that it held $15 million of renewable energy certificates at year-end 2025, recorded as “other current assets” based on its internal policy (pre-guidance). Under ASU 2026-02, its approach would only be appropriate if those RECs were intended for compliance; any voluntary portion would be expensed.

Evidence from voluntary markets shows corporate interest: a recent study found that a majority of large companies have net-zero commitments, some of which include purchasing offsets [22]. However, only about 13% explicitly define offset usage criteria (e.g. “when and how offsets can be used”) [22]. ASC 818 will force more rigor: companies committing to net-zero will need clear policies to justify any credit capitalization.

Case Study – Manufacturing Firm: A chemicals manufacturer (with no current cap-and-trade obligation) launched a “carbon-neutral product line,” purchasing large green-energy credits. Under legacy GAAP, it had expensed or skipped these costs. With ASU 2026-02, the CFO realizes that the plan wasn’t tied to an obligation – these credits will now be expensed immediately, increasing 2028 costs by $2 million (if $2M was spent on credits). This raises earnings volatility but aligns costs with the revenue period benefitting from the carbon-neutral claim. The CFO implements NetSuite tagging (“Offset_Actionable/NonActionable”) to differentiate any credits actually held for potential trading vs. voluntary usage.

Case Study – Electric Utility: A U.S. utility operates under a state cap-and-trade. It historically booked allowances as inventory. Under the new guidance, it will recognize outgoing ECO liabilities. Suppose at year-end the utility knows it must surrender 1,000 allowances for compliance, and holds 800. It will journalize a liability for 1,000 * current market price, and present the 800 as valued assets. This could create a sizeable ECO liability (and offsetting debit to expense or equity). The accounting team configures NetSuite’s fixed asset module for allowances held, and uses classes to match allowances to specific vintage years and compliance obligations.

Empirical Data and Trends

- Market Size: World Bank’s State and Trends of Carbon Pricing (2024) reports that 75 carbon pricing instruments now exist, covering ~24% of emissions [1]. Conservation and forest carbon crediting schemes are on the rise globally (e.g. in Asia and Latin America) as voluntary markets develop [41]. Analysts project voluntary carbon markets could exceed $100 billion by 2030 as corporate net-zero programs scale (OneTribe, January 2026).

- Corporate Commitments: According to Net Zero Tracker (2023), over 1,000 large firms pledged net-zero, up 40% from 2022 [42]. However, as Deloitte notes, there is a “credibility gap” – many pledges rely in part on offsets, but often without clear accounting of them [22]. Under ASU 2026-02, future corporate disclosures will quantify how much of emissions targets are achieved via credits (as echoed by proposed SEC rules [22]).

Implications and Future Directions

Impact on Reporting and Compliance

Financial Reporting: Companies will need more robust internal controls to track credits, forecast obligations, and test impairments. Audit committees may face new risks in verifying management’s “probable use” judgments. Trustee accountants will also need to consider this guidance in valuations (for trusts or funds with ESG mandates). The gross vs net presentation requirement will often increase both assets and liabilities on balance sheets, but the net equity impact could be small (since funded portion cancels). Profit and loss volatility may increase due to impairment losses or liability remeasurements for noncompliance credits and ECOs.

Tax and Regulatory: Although ASU 2026-02 does not change tax treatment, the recognition of credits (assets) could affect deferred tax calculations if credits have tax consequences. Regulated entities should monitor how regulators react (e.g. are utility regulators requiring separate accounting for carbon costs?). In some jurisdictions, the regulatory asset treatment might align or conflict with this GAAP model.

International and Standard-Setting Perspective

On the international front, IFRS has not set a precedent, but may follow in some manner. The IFRS Foundation is working on sustainability standards (IFRS S1/S2) for disclosures, and IASB has received feedback on environmental credits accounting from stakeholders. In the IFRS view, the lack of specific guidance means most companies use IFRS 13 (fair value) or IAS 37 (provisions) analogies, which aligns somewhat with ASC 818’s approach (carrying values + fair values). It is conceivable that IFRS will eventually converge, at least in principles. The FASB’s definition of “probable” (≈70%) and focus on enforceability might influence global standards.

Evolving Markets and Digitalization

Emerging trends will also affect how ASC 818 is applied. Digital registries and blockchain platforms are increasingly used to certify offset credit legitimacy. Integration of such systems with ERP (including NetSuite) could automate the verification of credit ownership. Companies may embed carbon credit tracking into enterprise software (as with new ISV solutions), reducing manual journal entries. FASB itself may consider adding guidance in future updates (for example, on carbon removal credits or deforestation credits).

Sustainability Strategy Alignment

ASU 2026-02 tightens the linkage between strategy and accounting: voluntary sustainability initiatives that rely on credits must now be financially reflected one way or another. This will likely prompt companies to clarify their offset policies. The standard may also influence how corporations negotiate offtake agreements: CFOs will factor accounting implications (e.g. whether to treat a credit purchase as asset vs direct cost). Ultimately, the guidance promotes more conservative recognition of environmental assets, arguably discouraging greenwashing through unverifiable assets.

Future Research and Developments

Academic and industry researchers will be watching how companies implement ASC 818. Potential future work includes:

- Studying earnings impacts (do companies see large one-time charges at adoption?).

- Examining market reactions (do stock prices respond when large ECO liabilities are recognized?).

- Analyzing behavioral effects (will firms alter environmental strategies to optimize accounting outcomes, such as timing of credit purchases?).

- Extending analysis to analogous instruments (e.g. plastic credits, water credits).

Policymakers may also follow how ASC 818 influences the cost of compliance. If companies start accelerating credit purchases to smooth earnings, it could affect credit markets. Lastly, standard setters worldwide (including the International Sustainability Standards Board and country regulators) are observing FASB’s lead – similar disclosures or accounting requirements could emerge globally, driven by regulatory convergence (for instance, under the European Sustainability Reporting Standards or proposed SEC climate rules [22]).

Conclusion

ASU 2026-02 (ASC 818) fills a critical gap in U.S. GAAP by providing comprehensive rules for environmental credits and obligations. Entities engaged in carbon trading, renewable energy compliance, and ESG initiatives must prepare for significant accounting changes. Under the new model, only enforceable, intended-for-use credits are capitalized; others are expensed. Obligations are recognized as liabilities on a gross basis. These changes will increase transparency but also demand careful data tracking. NetSuite and other ERP systems must be configured to capture the new account categories and processes, as summarized above.

In sum, the adoption of ASC 818 is poised to standardize the previously ad-hoc treatment of sustainability credits. Stakeholders – investors, regulators, and the public – will gain a clearer picture of how environmental commitments impact financial health. Going forward, organizations will need to integrate financial and environmental data more tightly, ultimately leading to more informed decisions in the pursuit of sustainability objectives.

References: Authoritative sources used in this report include FASB’s Accounting Standards Update and press materials, Deloitte/Crowe/KPMG analysis and memoranda, NetSuite documentation, and published research on carbon markets [5] [3] [1] [6] [15], [37]. (URL-style citations correspond to sections and lines in the sources as noted.)

External Sources (42)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.