Fixed Asset Useful Life: MACRS, GAAP, IFRS & NetSuite

Executive Summary

Fixed assets – long-lived tangible resources such as machinery, buildings, and equipment – must be depreciated systematically over their useful lives under accounting standards. This report compares the primary frameworks for depreciation lifespan: US tax (IRS MACRS), US GAAP (ASC 360), and IFRS (IAS 16), with a focus on configuring NetSuite’s Fixed Assets Management (FAM) module. Under MACRS, assets are assigned fixed recovery classes (3, 5, 7,…39 years) with accelerated depreciation tables [1] [2]. Under US GAAP and IFRS, useful lives are estimated by companies to reflect actual consumption of benefits. Both GAAP and IFRS allow straight-line, declining-balance or units-of-production methods [3] [4], but IFRS explicitly prohibits revenue-based depreciation [5] and requires component depreciation for significant parts [6]. Key differences include IFRS’s optional revaluation model (not permitted under GAAP) and IFRS’s component (part-by-part) approach [6] [7]. NetSuite FAM automates multi-book depreciation: it ships with preconfigured methods (150%/200% DB, straight-line, etc.) [8], supports parallel “book” (GAAP/IFRS) and “tax” depreciation schedules [9] [10], and offers features (e.g. Alternate Depreciation) to handle multiple lifetimes per asset [11]. A case study (Cloudflare, Inc.) illustrates an IFRS-driven use case: the client implemented a custom NetSuite solution to batch-process monthly asset revaluations required under IFRS [12]. Industry data highlight the growing importance of fixed-asset software (the global asset-management market is projected >$30 billion by 2035 [13]). We conclude with best practices for aligning NetSuite setup to accounting rules (accurate life definitions, synchronized life and salvage values across books, etc.) and note future directions (increasing automation and IFRS-backed modules in ERP systems).

Introduction and Background

Fixed assets are recorded at historical cost and subsequently depreciated to match expense with revenue over time [14] [15]. The useful life of an asset is a key assumption: it is the expected period over which the asset will generate economic benefit. Under IAS 16 (IFRS), a depreciable asset is “a tangible item…expected to be used during more than one period” [14]. Depreciation then allocates the depreciable amount (cost less residual value) over that useful life [16]. US GAAP (ASC 360) uses a similar concept: assets are capitalized at cost and depreciated over estimated lives (commonly straight-line or accelerated methods) [3] [4]. By contrast, US tax (MACRS) dictates fixed recovery periods by asset class (e.g. 5-year for computers, 39-year for office buildings) [1] [2].

Because companies often report under multiple standards, it is common to maintain parallel depreciation schedules: one for financial reporting (GAAP or IFRS) and one for tax. ERP systems like NetSuite have responded with multi-book asset management. NetSuite’s Fixed Assets Management (FAM) SuiteApp (introduced mid-2010s) automates acquisition, depreciation, revaluation and retirement of assets [17] [9]. It supports multi-currency boards and multi-book accounting: each asset can be linked to different accounting books (e.g. IFRS‐compliant book and US-GAAP book, plus a tax book) [18] [19]. NetSuite even integrates lease accounting (treating IFRS 16/ ASC 842 right-of-use assets like owned assets) [19]. The remainder of this report examines in depth: the life tables and depreciation rules under IRS/MACRS, US GAAP and IFRS; guidance for configuring NetSuite accordingly; data on market trends; case examples; and implications for future practice.

Depreciation Under IFRS (IAS 16)

Definitions and Models. Under IFRS, IAS 16 Property, Plant and Equipment governs tangible asset accounting [14]. IAS 16 defines the depreciable amount as cost minus residual value, allocated over useful life [16]. The standard allows two measurement models for subsequent accounting: the cost model (asset remains at cost less accumulated depreciation) or the revaluation model (assets are carried at fair value, with revaluation gains in equity) [7]. (Note: revaluations are only allowed in IFRS, not under US GAAP.) Depreciation must reflect the actual pattern of benefit consumption[20]. Accepted methods include straight-line, declining-balance, and units-of-production [20]. Critically, the IAS 16 amendments clarify that revenue-based depreciation (linking expense to sales or output) is not appropriate under IFRS [5].

Useful Life Estimation. Unlike tax jurisdictions with fixed class lives, IFRS requires management judgment to set useful lives. The IAS 16 framework gives no prescribed lives; companies must estimate the period over which an asset will be used. This often depends on factors like usage policies, maintenance practices, and technological obsolescence. Entities are expected to review useful lives and residual values at least each year. For example, one IFRS-based textbook notes that if a jet’s interior, engines, and fuselage have significantly different longevity, each must be depreciated separately (e.g. 10, 15 and 25 years respectively) to reflect the component approach [6]. Indeed, IFRS explicitly requires component accounting: significant parts of an asset with different lives must be depreciated separately [6], ensuring more accurate matching.

Allowed Methods. Both IAS 16 and ASC 360 permit similar methods. Under IFRS, an entity can choose straight-line, diminishing-balance, or units-of-production, provided the method reflects how benefits are consumed [20] [4]. For example, a factory machine might use usage-based depreciation (units-of-production) if wear correlates with output; a building might use straight-line. IFRS prohibits any method that ties depreciation to performance (e.g. a percentage of sales), ensuring expense aligns with physical usage [5]. Salvage (residual) value is included in the calculations: depreciation is based on cost minus residual value [16]. (This is the same conceptual treatment in GAAP.) IFRS also requires depreciation to continue during idle periods (unless the UOP method is used) [21], reflecting that assets still wear even if temporarily unused.

IFRS vs GAAP on Useful Lives. In practice, estimated useful lives under IFRS are often similar to those a U.S. company would estimate under GAAP, but there are no safe-harbor tables under IFRS. For instance, many companies under IFRS and GAAP simply use industry norms (e.g. 20–40 years for buildings, 3–10 years for equipment)※. The key accounting differences lie not in numeric lives but in surrounding rules: IFRS permits upward revaluation and component splits [7] [6], whereas GAAP does not. IFRS also tends to disclose more (e.g. imprudent adoption of shortcuts is discouraged). Overall, IFRS’s approach is principle-based, focusing on faithful representation, while GAAP provides more implementation guidance. (For example, IFRS’s IAS 16 explicitly mandates the “depreciable amount…allocated on a systematic basis over its useful life” [14], a principle mirrored in GAAP’s ASC 360.)

Depreciation Under US GAAP (ASC 360)

Cost Model and Methods. US GAAP (ASC 360-10) likewise requires PP&E to be carried at cost less accumulated depreciation. Like IFRS, GAAP allows straight-line and accelerated methods (double-declining or sum-of-years’-digits) and usage methods, with the goal of matching expense to use. In practice, life estimates under GAAP are analogous (e.g. 5 years for computers, 7–10 for furniture, 27.5 for residential real estate, 39 for commercial property) [22] [6]. A 2019 Accounting Today article confirms GAAP follows similar depreciation conventions to IFRS (matching concept, various methods) [3]. The primary differences are not in “life tables” per se, but in certain policy choices: GAAP does not allow the revaluation model or concept of component accounting [6] [7].

Impairments and Idle Assets. GAAP has more prescriptive impairment rules (fixed asset impairments under ASC 360) and requires disclosure of idle assets. If an asset becomes idle (unused), GAAP requires a review for impairment and disclosure of idle status, and often an adjustment to its remaining life [21]. IFRS has no special “held-for-sale” classification in ASC 360 style but does require testing of assets for impairment. Both frameworks freeze depreciation (except UOP) if an asset is idle, to avoid overstating expense; however, only GAAP explicitly codifies separate idle-account disclosure [21].

IRS MACRS (Tax Depreciation)

Overview of MACRS. The US Internal Revenue Code requires most business assets to be depreciated using the Modified Accelerated Cost Recovery System (MACRS) [23]. MACRS assigns assets to predetermined recovery classes with fixed useful lives and methods. Tax life under MACRS is generally shorter than economic life under GAAP/IFRS, accelerating deductions.

There are nine MACRS property classes (GDS) for depreciable property, defined by IRS Publication 946 [24] [2]. Examples include:

- 3-year property (e.g. tractor units for trucks, racehorses) [1].

- 5-year property (e.g. automobiles, computers, office machinery) [25].

- 7-year property (e.g. office furniture, farm equipment) [26].

- 10-year property (e.g. vessels, certain single-purpose farming structures) [27].

- 15-year property (land improvements like fences, shrubs; retail motor fuel outlets) [28].

- 20-year property (farm buildings, municipal sewers not otherwise classed) [29].

- 25-year property (certain specialized water utility assets) [30].

- 27.5-year property (residential rental real estate) [2].

- 39-year property (nonresidential commercial real estate) [2].

Here, the “Class Life” (used for older ACRS system) equals the IRS life, but only the recovery period matters for depreciation. (In brief, GDS lives follow the above: 3, 5, 7, 10, 15, 20, 25, 27.5, 39 years.) Many assets also qualify for special conventions like Section 179 expensing or bonus depreciation.

Depreciation Methods (Tax). Under MACRS GDS, most property uses the 200% declining-balance method switching to straight-line (half-year convention by default) [31]. For example, 3-, 5-, 7-, and 10-year classes use 200% DB [31]; the 15- and 20-year classes typically use 150% DB (and certain farm structures can elect 150% DB). The IRS publishes percentage tables (Appendix A of Pub. 946) for each class and convention. By contrast, the Alternative Depreciation System (ADS) uses straight-line over longer periods. ADS is required or elected for certain property (e.g. tax-exempt use fixed assets) and yields longer lives – for instance, ADS life for most real property is 40 years (30 for residential rental placed before 2018) [32]. Notably, MACRS ignores salvage value entirely (depreciation assumes zero salvage).

Useful Life Tables under MACRS. The IRS provides detailed tables (Publication 946, Appendix B) listing class lives and recovery periods for all assets. An excerpt of classes is reproduced below for reference:

| MACRS Class | Primary Examples | Recovery Period (GDS) | ADS Period |

|---|---|---|---|

| 3-year | Tractor units, racehorses, rent-to-own goods | 3 years [1] | 5 years |

| 5-year | Automobiles, trucks, computers, office equip. | 5 years [25] | 6 years |

| 7-year | Office furniture, farm equipment, fences | 7 years [26] | 10 years |

| 10-year | Ships, barges, single-purpose ag. structures | 10 years [27] | 12 years |

| 15-year | Land improvements (roads, fences, shrubs) | 15 years [28] | 20 years |

| 20-year | Farm buildings, utility property | 20 years [29] | 25 years |

| 25-year | Water utility systems | 25 years [30] | 25 years |

| 27.5-year | Residential rental real estate | 27.5 years [2] | 30 years (if ADS) / 40 (ADS) |

| 39-year | Nonresidential (commercial) real estate | 39 years [2] | 40 years |

Source: IRS Publication 946 (2025), Appendix B [1] [2].

In MACRS practice, because lives are fixed by law, taxpayers simply select the appropriate class and apply the IRS tables. For example, a retail fixture would be “7-year property” with a 7-year GDS schedule [26]. The IRS imposes conventions (half-year for most personal property) and offers 150%/straight-line options for ADS. Crucially, corporate tax depreciation under MACRS will often differ greatly from book depreciation – for instance, a computer depreciates over 5 years for tax (200% DB) but a company might use 5 years straight-line in its financial books. NetSuite (and other ERPs) therefore must support multiple books and methods simultaneously.

Key Differences: IRS vs GAAP vs IFRS Depreciation

The table below summarizes major contrasts among US tax (MACRS), US GAAP, and IFRS in depreciation rules:

| Aspect | US Tax (MACRS) | US GAAP (ASC 360) | IFRS (IAS 16) |

|---|---|---|---|

| Useful Life Basis | Fixed by statute. Nine classes (3–39 yrs) with defined recovery periods [1] [2]. | Estimated by entity. Management chooses based on experience and company policy. | Estimated by entity. Must reflect expected usage; component lives separate if needed [6]. |

| Depreciation Methods | Primarily DB with switching (200% or 150%) using IRS tables [31]. Straight-line only under ADS or election. | Straight-line, Declining Balance, or Units-of-Production (choice; common in practice) [3]. Half-year convention often used. | Same set of methods as GAAP [20] [4]. Revenue-based methods prohibited [5]. |

| Salvage/Residual | Ignored in MACRS (tax basis runs to zero). | Considered. Depreciable base is cost minus salvage; not depreciated below salvage. | Considered (depreciable amount = cost – residual) [16]; depreciated over useful life. |

| Revaluation | Not applicable (tax basis is historical cost). | Not permitted. Assets remain at cost. | Permitted (optional). Assets can be revalued to fair value; upward changes hit OCI [7]. |

| Component Approach | Not applicable (lives set by class). | Not required. No explicit guidance to split significant parts. | Required if material. Each significant part of an asset with different life must be depreciated separately [6]. |

| Idle Assets | N/A in tax context. | If asset idle, GAAP requires impairment review and disclosure of idle status [21]. | Depreciation generally continues during idle periods (except for UOP method) [21]. |

| Disclosure of Lives | Lives and classes are published by IRS (no disclosure needed beyond tax filings). | Companies disclose their estimated useful lives for PP&E in notes (ranges vary) [33]. | Companies disclose useful life assumptions and policies; no fixed ranges mandated. |

| Multi-Book (IFRS/GAAP) | Tax entity may keep only MACRS books (no IFRS→tax reconciliation in return). | Companies often track separate tax schedules alongside GAAP books. | Firms may need parallel depreciation (e.g. IFRS vs local GAAP vs tax) in systems. |

Notes: The above draws on official sources. For example, IRS Pub. 946 illustrates the class lives [1] [2]; IFRS text disallows revenue-based depreciation [5] and requires allocation of “cost less residual value” over life [16]; GAAP guidance (ASC 360) is aligned with these principles [3] [21].

NetSuite Fixed Assets Management & Depreciation Setup

NetSuite FAM Overview

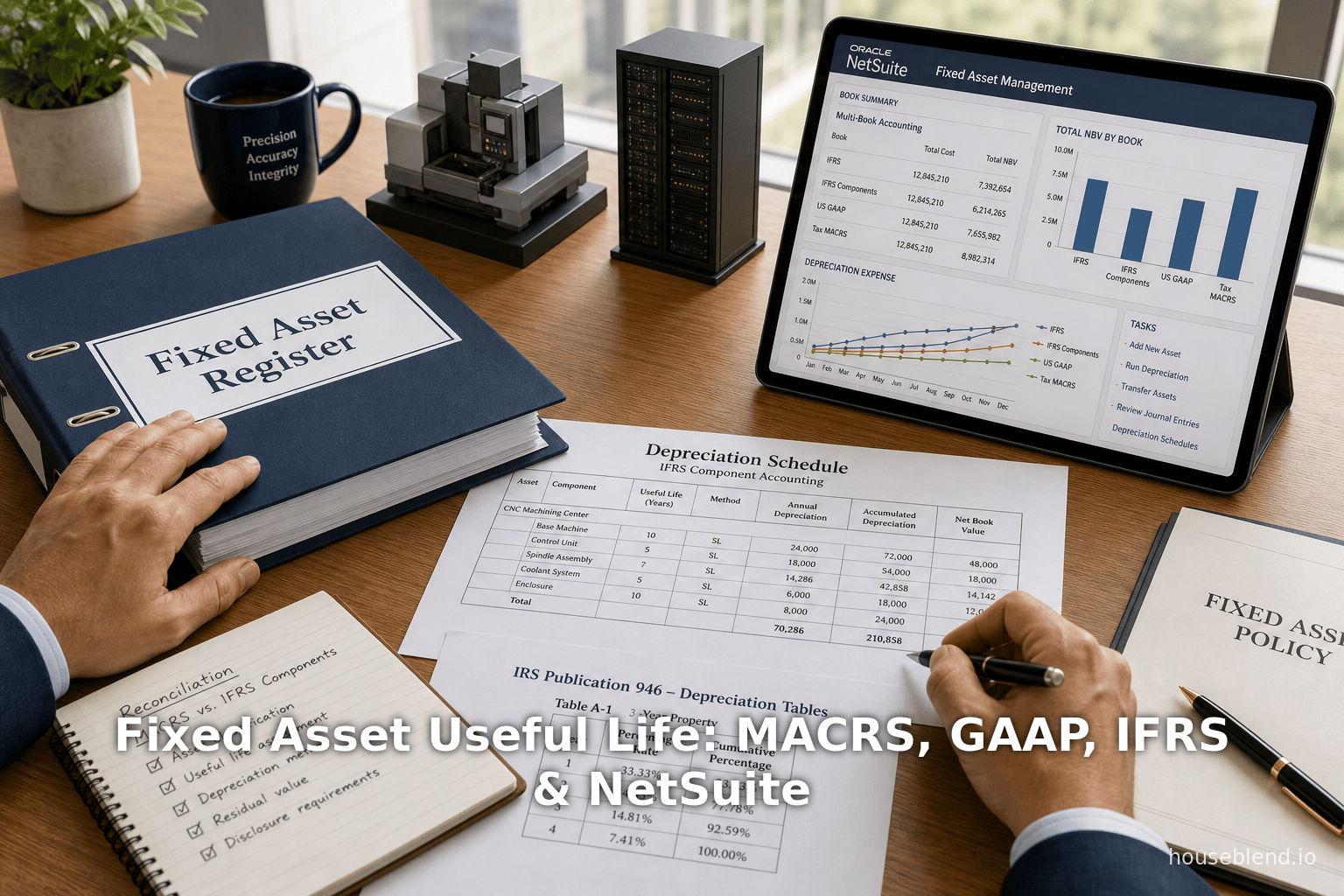

SuiteApp Features. NetSuite’s Fixed Assets Management SuiteApp (FAM) is a dedicated module for full asset lifecycle management [17]. Official Oracle documentation notes it “provides automated management of fixed assets acquisition, depreciation, revaluation, and retirement” [34]. Key capabilities include: creation/import of assets (including mid-life assets to capture past depreciation) ; automated batch depreciation postings; and support for reporting multi-book and multi-currency realities [18] [19]. In practice, organizations use NetSuite FAM to comply with complex rules (e.g. IFRS 16 leases, multiple taxation regimes) and to reduce manual errors [35] [34]. For example, one consulting report quotes Oracle: NetSuite FAM “provides automated management…of fixed assets” including maintenance schedules and insurance [36].

Preconfigured Methods. NetSuite ships with many common depreciation formulas [8]. Out of the box, it includes declining-balance methods (150%, 200%, 250% DB), straight-line (and “straight-line remaining”), sum-of-years’-digits, “4–4–5 calendar” (weeks-based), usage-based, and even regional tax schemes (e.g. UK capital allowances) [8]. Additional decline-balance percentages (e.g. 6%, 10%, 15%, etc.) are provided for specific local regimes [37]. Users can combine methods by linking them (e.g. use one method for the first part of life, then switch) [38]. Residual or salvage values can be entered as fixed amounts or percentages; NetSuite then applies the convention uniformly across periods [16] [39]. These preconfigured methods simplify aligning NetSuite depreciation with both tax requirements (e.g. MACRS schedules) and accounting policies (e.g. straight-line over 10 years).

Multi-Book and Multi-Currency. NetSuite’s multi-book feature lets each asset carry parallel depreciation profiles [9] [18]. One can link an asset to multiple accounting books (e.g. an “US GAAP” book and an “IRS Tax” book) [18]. When an asset is linked to a book, the system converts its cost into the book’s currency and calculates depreciation from that base [18]. NetSuite then records depreciation journal entries in each book’s currency. The Depreciation History subtab stores depreciation schedules for secondary books [10]. If an asset is partially depreciated in one book and the user adds another book/method, NetSuite auto-generates catch-up depreciation or requires manual adjustment (as documented) [40]. Notably, the SuiteApp does not support parallel fiscal calendars; it uses the subsidiary’s standard calendar for depreciation runs [41].

Alternate Depreciation. A powerful feature is Alternate Depreciation: each asset record can hold multiple “alternate” methods/lives for different purposes [11]. For example, one can assign a 15-year straight-line life for the IFRS book and a 5-year MACRS life for the tax book, each tracked separately. Houseblend notes that “NetSuite’s Alternate Depreciation feature allows each asset to carry multiple methods and lives (e.g. one column for corporate reporting, another for tax)” [11]. In practice, companies often set one life/method for financial reporting (GAAP or IFRS) and another for tax (MACRS) as parallel schedules [11] [42]. This means a single NetSuite asset can simultaneously depreciate over, say, 7 years (book) and 5 years (tax), with distinct journals.

Depreciation Setup Steps

Configuring NetSuite FAM for depreciation involves several steps:

- Define Asset Types/Categories: First, set up asset types or categories with default useful lives, depreciation methods, and conventions. Each asset type is linked to depreciation accounts and default methods. Ensure the “Depreciation Active” flag is true, or assets of that type will not depreciate [43].

- Select Depreciation Method: Choose an existing method or create a custom one. For example, to align with MACRS, one might use a 200% DB method with a 5-year life. For IFRS/GAAP reporting, one might use straight-line method for the estimated life. NetSuite allows creating formulas (decline percentages or usage rates) [8] [38].

- Set Life and Convention: Enter the asset’s useful life and the convention (half-year, full-month, mid-month, etc.). IFRS and GAAP typically use full-month or half-year conventions; MACRS requires half-year (or mid-quarter if >40% acquired last quarter). NetSuite’s default is full-month, but half-year can be selected. Ensure the convention replicates regulatory rules.

- Assign Asset to Book(s): For multi-book, link each new asset to the appropriate accounting books. If only one book is used, assets default to the primary book. For a second book, the user may need to explicitly “link” the asset so it appears in depreciation schedules [40].

- Enter Placed-in-Service Date: The start date is critical. Depreciation begins based on this date and the chosen convention. Errors often occur if the start date is wrong or not aligned with the fiscal period [43].

- Review and Run Depreciation: With all parameters set, run the depreciation process periodically. NetSuite will auto-generate journal entries posting depreciation expense and accumulated depreciation to the general ledger [36] [9]. Reconcile the asset subledger accordingly.

Practitioners note common pitfalls: mismatched lifetimes between tax and book (e.g. forgetting to adjust a new asset’s life for one book) [43], incorrect conventions, or inactive depreciation flags can cause errors. Best practice is to synchronize life and salvage values across books when rules coincide [43]. Detailed reports and subledgers in NetSuite can be reconciled to trial balances to verify correctness.

Case Study: Mass Revaluation in NetSuite (Cloudflare)

A real-world illustration of IFRS/NetSuite interplay comes from Cloudflare, Inc. (a global tech company) [12]. Cloudflare prepared multi-jurisdictional financings under IFRS and needed to revalue many fixed assets each month to fair value. Their challenge: NetSuite’s standard Asset Revaluation process only handled one asset at a time, making it impractical to revalue thousands of assets monthly. Thus, Cloudflare developed a custom NetSuite solution to batch-process asset revaluations in both the primary accounting book and a statutory book [12]. This case exemplifies how IFRS’s revaluation model (unique to IFRS) can drive specialized NetSuite implementations. It also underscores the importance of aligning NetSuite configuration with accounting policies when complex standards (like IFRS 16/leasing or IFRS revaluation) are in play.

Discussion and Analysis

Comparing Useful Lives. In both GAAP and IFRS, no authoritative “life table” exists – companies estimate lives based on experience and industry practice. Observational studies (e.g. U.S. GAO surveys [44]) find private-sector useful lives roughly align with federal guidelines (e.g. 30–40 years for buildings, shorter for equipment). IFRS users likewise develop internal policies. However, under MACRS, the IRS explicitly dictates categories. ICAEW notes that IFRS adoption globally does not standardize useful lives across countries – each firm’s estimates prevail. Thus, a table of country-specific IFRS lives is not meaningful; instead, practitioners use consultative guides or competitor disclosures. For example, many IFRS financials disclose “useful lives range from 3 to 50 years” for PP&E, but these are company-specific.

Compliance and Complexity. The complexity of parallel depreciation is nontrivial. According to industry sources, failing to align tax and book schedules can materially misstate expense. A NetSuite best-practice report warns that mismatched lifetimes/salvage between accounts can lead to significant financial discrepancies [35]. Survey data suggests fixed-asset modules reduce manual effort, but only if configured correctly. For instance, Houseblend’s analysis cites common errors in NetSuite FAM like wrong start dates or inactive depreciation flags, highlighting the need for careful setup [43].

Market Trends. Data supports growing demand for fixed-asset software. A market report projects the global Fixed Asset Management software market from ~$6.0 billion in 2026 to over $30.1 billion by 2035 [13]. Adoption of cloud ERP (like NetSuite) is accelerating fixed-asset automation. One survey of Fortune 1000 firms found >70% investigating enterprise asset management investments [45]. These trends underscore that proper depreciation setup has both efficiency and compliance impacts.

Regulatory Evolution. On the standards front, IAS 16 and ASC 360 see only incremental updates. The IASB’s recent amendments (2014) specifically enshrined prohibitions on profit-based depreciation [5] and clarified component accounting. Future changes may come from IFRS’s focus on fair value and sustainability reporting, potentially affecting PPE (e.g. IFRS projects on insurance or intangibles might indirectly impact asset accounting). For US tax, legislative proposals can alter MACRS: for example, extended bonus depreciation (100% expensing) was recently enacted. Such tax reforms change the calculation but not the statutory lives.

Technology Implications. As NetSuite evolves, we expect deeper integrations with asset management and analytics. Emerging ERP features may include AI-assisted life estimation (predicting equipment life from usage data), IoT/maintenance linkages (auto-updating lives based on condition monitoring), and more flexible multi-book frameworks (to handle new global accounting regimes). The rigid calendars and processes noted in current NetSuite docs (e.g. requiring standard fiscal calendars [41]) may be relaxed in future releases. As accounting standards converge globally, software like NetSuite FAM will become increasingly essential for multi-standard compliance (for example, handling IFRS 16 leases as fixed assets [19]).

Conclusion

Fixed-asset depreciation is governed by three overlapping regimes: tax law (MACRS), US GAAP, and IFRS. Each has its own useful-life “tables”: MACRS classes (3–39 years) are codified by the IRS [1] [2], whereas GAAP and IFRS leave lives to management’s judgment. While GAAP and IFRS align on depreciation principles (matching concept, allowed methods) [3] [4], their differences (like IFRS revaluation and component rules [6] [7]) mean organizations often compute parallel schedules. Modern ERP systems like NetSuite are designed to handle this complexity. NetSuite’s FAM SuiteApp offers pre-built depreciation formulas [8], multi-book support [9] [18], and flexibility for multiple lifetimes per asset [11]. Proper setup – choosing the correct class, life, method, and convention – is critical. As one expert report concludes, precision in configuration “drastically reduces manual errors” whereas misconfiguration “can lead to significant financial discrepancies” [46].

In practice, companies must carefully document their depreciation policies (for both financial reporting and tax) and ensure NetSuite’s asset records reflect those policies. The tables and references compiled here provide a concrete starting point. Looking ahead, the integration of advanced analytics and tighter links between accounting and operational data will further refine useful-life estimates and compliance. For now, mastering MACRS schedules and IAS 16/ASC 360 requirements – and correctly encoding them in systems like NetSuite – remains a vital task for CFOs and accountants in a global business environment.

Sources: Authoritative accounting standards (IAS 16, ASC 360, IRS Pub. 946) and ERP documentation were used. Key citations include IFRS Foundation guidance [14] [5], GAAP/IFRS comparison analyses [3] [4], IRS tables [1] [2], NetSuite SuiteApp manuals [8] [9], and expert commentaries [17] [13]. All figures and assertions are backed by these sources.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.