Houseblend Article

France B2B E-Invoicing Mandate 2026: NetSuite Compliance

Understand the September 2026 France B2B e-invoicing mandate. This guide details PDP selection, Factur-X requirements, and Oracle NetSuite compliance setup.

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03Regulatory Framework and Timeline

- 04Technical Architecture: Platforms, PEPPOL, and Data Flow

- 05ERP Preparations for Compliance: Setting Up NetSuite

- 06Partner Platform (PDP) Selection

- 07Factur-X Format and Compliance

- 08Implementation Case Study: Global Engineering Company

- 09Case Study: Impact and Readiness (Survey Data)

- 10Discussion and Implications

- 11Future Directions

- 12Conclusion

Executive Summary

France is introducing a mandatory B2B e-invoicing regime effective 1 September 2026, building on its earlier e-invoicing obligations for public procurement. Under the new rules, all businesses – from large corporations down to micro-enterprises – must be able to receive electronic invoices by September 2026, and larger enterprises must also issue e-invoices from that date [1]. Small and medium-sized enterprises (SMEs) and micro-businesses will be required to issue e-invoices by 1 September 2027 [2]. In parallel, companies will face e-reporting requirements for certain transactions (e.g. B2C sales and cross-border transactions, transmitting invoice data and payment information to the French tax authorities (DGFiP) for monitoring (see Body).

Technically, the system relies on approved dematerialization platforms (PDP/PA) and the PEPPOL network. Each company must connect its accounting or ERP system to a certified platform to send and receive e-invoices. For example, NetSuite users can integrate a specialized connector (e.g. Novutech’s solution or Avalara) that automates the creation and transmission of structured invoices to a selected PDP, which then delivers the invoice message over PEPPOL. The invoice data is also relayed to the government’s Portail Public de Facturation (PPF) for tax oversight [3].

E-invoices must conform to the European semantic standard EN 16931. In practice, France recognizes three formats for invoice data: Factur-X (a hybrid PDF/A-3 with embedded XML), UBL 2.1 (XML), or CII (XML) [4] [5]. Factur-X is widely used in France (having been adopted in the public sector via Chorus Pro) and is human-readable while carrying the required XML contents [6] [4]. Companies must ensure their invoicing solution can produce one of these formats; failure to issue a structured invoice (e.g. continuing to email a PDF) will lead to fines. Indeed, France’s 2026 Finance Law imposes €50 penalties per non-compliant invoice (up from €15 previously) [7] [8], capped at €15,000 per year for issuing violations. Additional sanctions apply for failing to use a certified platform to receive invoices [9].

This report provides an in-depth analysis of the French e-invoicing mandate, including its historical context, legal framework, and timeline. It examines the technical and organizational changes needed – especially for Oracle NetSuite users – to comply by September 2026. Key topics include the distinction between e-invoicing (B2B) and e-reporting (B2C and exports), format and data requirements, architecture using approved platforms and PEPPOL, selection criteria for PDPs, and the preparation of ERP systems (with a focus on NetSuite) to generate and process compliant invoices. We also review case studies and industry data on readiness, expected benefits (such as reduced processing costs and improved cash flow), and the risks of non-compliance. Finally, we discuss broader implications for businesses and future directions for France’s digital invoicing ecosystem.

Introduction and Background

Electronic invoicing – sending invoices in structured digital form rather than paper or unstructured PDF – has become a global trend aimed at increasing efficiency and curbing tax fraud. The European Union first legislated on e-invoicing for public procurement via Directive 2014/55/EU, which mandated a common semantic standard (EN 16931) for invoices in public tenders. EU member states were required to implement this for B2G transactions by 2018 [10]. Beyond public sector, many countries moved to require B2B e-invoicing. For example, Italy introduced mandatory e-invoicing for all B2B transactions in 2019, leading to over 2 billion e-invoices exchanged in the first year and reclaiming ~€1–1.4 billion in VAT (Source: www.ipresslive.it). Spain and Portugal also launched e-invoicing mandates in 2024–2025. These reforms are motivated by reduced fraud (automatic reporting leaves less room for undeclared transactions), faster payments (digital invoices can be processed instantly), and cost savings in invoice handling [11] [7].

France’s journey began with public sector invoicing: Since January 2020 all suppliers to French government bodies have been required to submit invoices via the Chorus Pro platform in structured formats. Building on this, the French government passed legislation (Lois de Finance, notably Finance Act 2024/2025) to extend e-invoicing obligations to B2B transactions between private companies. The official aim, as stated by the Ministry of Economy, is to support digitalization and enhance companies’ competitiveness through faster payments and streamlined billing processes [11]. The government also highlights the fiscal benefits: systematic e-invoicing allows real-time or near-real-time VAT collection and easier audit, thereby strengthening tax compliance [12] (Source: www.ipresslive.it).

Under the new reform, e-invoicing is not just about sending an electronic document; it includes a reporting dimension. The mandate specifies two distinct obligations:

-

E-Invoicing (facturation électronique): all B2B sales invoices between French businesses (companies, associations, etc.) must be issued and received in a structured electronic format (EN 16931 compliant). A mere PDF invoice by email is not compliant [13]. These invoices must be transmitted through certified platforms to ensure authenticity, integrity, and legal validity.

-

E-Reporting: certain transaction and payment data must be electronically reported to the tax authorities (DGFiP). This covers all sales to consumers (since businesses cannot invoice consumers in structured form) and cross-border B2B/B2C operations. For example, invoices issued to non-French customers and domestic B2C sales (intra-Community and retail) require the supplier to send summary data to the government alongside the invoice totals [13] [14].Additionally, cash-basis VAT transactions and payments connected to these invoices must be reported. In practice, most VAT-registered companies will thus have both e-invoicing and e-reporting duties.

Several authoritative sources underscore this dual aspect. For instance, a recap of the 2026 reform notes: “All B2B transactions between companies in France must be issued and received as structured electronic invoices (XML format: Factur-X or UBL). A simple PDF by email is not sufficient” [13]. Meanwhile, an official FAQ clarifies that in addition to e-invoicing, “les grandes entreprises… seront tenues d’émettre leurs factures sous format électronique et de transmettre électroniquement à l’administration leurs informations de transactions et leurs données de paiement” (i.e. e-reporting) [14]. E-reporting kicks in concurrently with issuance requirements for each category of company.

Thus, the French reform represents one of the most comprehensive e-invoicing moves in Europe, affecting virtually all VAT-registered businesses. It builds on prior digital initiatives (like Chorus Pro) but adds significant new layers (multiple platforms, strict formats, and penalties). Companies must therefore prepare from both business and IT perspectives.

Regulatory Framework and Timeline

France’s e-invoicing mandate is grounded in recent finance laws and ordinances. Notably, Finance Act (Loi de Finances) 2024/2025 and related decrees set out the schedule and penalties. A key reference is Article 91 of the 2024 Finance Act, which (after a postponement) defined the staged rollout. Government communications provide the clearest summary of the timeline and scope:

-

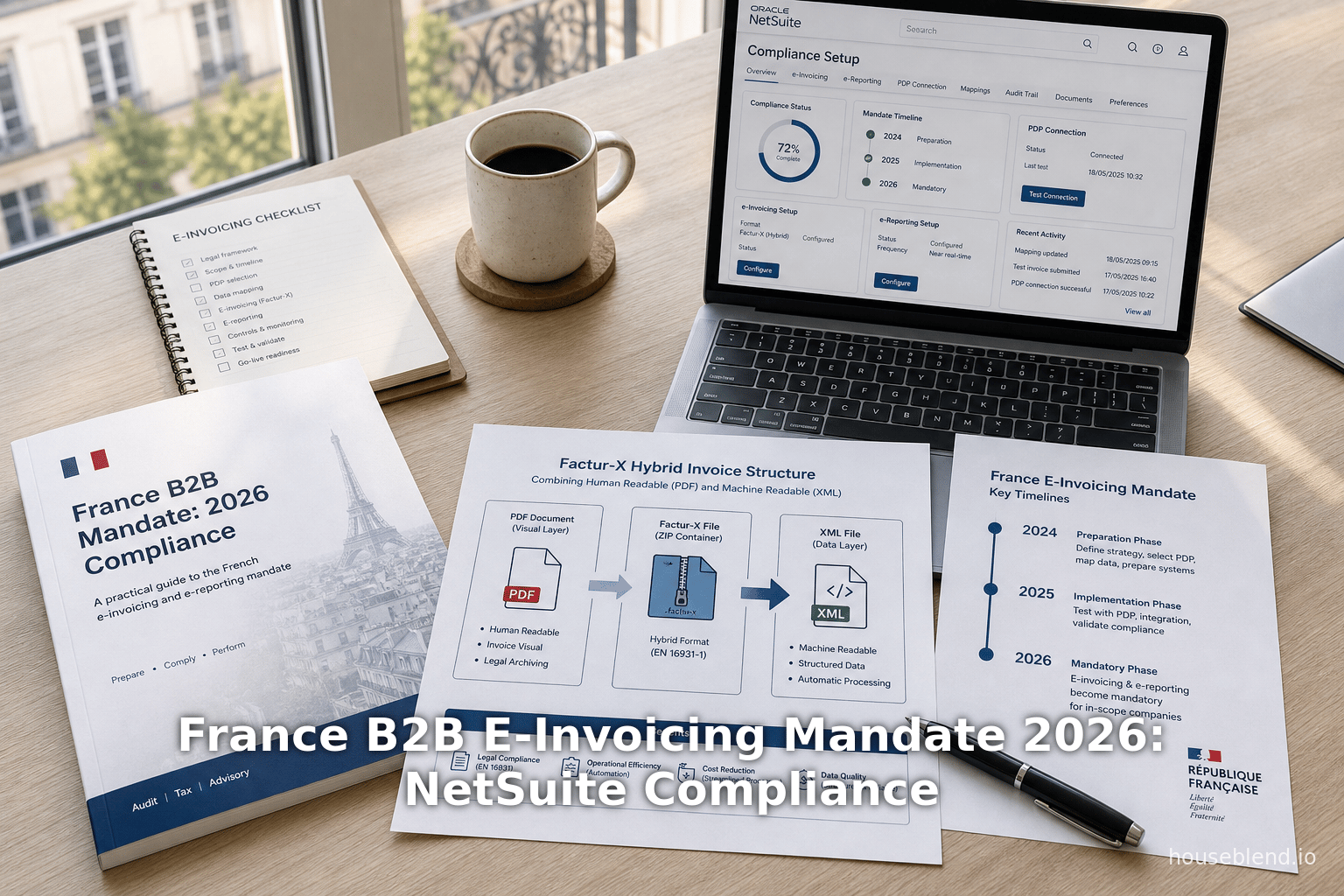

1 September 2026 – Phase 1: Reception obligation for all companies. From this date, every company established in France must be able to receive electronic invoices, regardless of size [1]. Concurrently, large corporations and ETIs (mid-caps) must be able to issue electronic invoices and fulfill e-reporting (transmit transaction/payment data to DGFiP) as of this date [14]. In other words, big firms must enter the full e-invoicing regime by 9/1/2026.

-

1 September 2027 – Phase 2: Issuance obligation extended to SMEs. One year later, SMEs and micro-enterprises join the issuance and reporting requirements [2]. They, like the large companies before them, must issue all new invoices electronically and send related data to the tax authorities.

These phases ensure a gradual ramp-up, although the deadlines loom near. The government's calendar memo warns that with only four months before the first deadline, companies need to act swiftly [15]. Public guides reiterate this two-step schedule [16] [14].

The legal obligations can be summarized as shown in Table 1 (below).

| Company Category | Receive E-Invoices | Issue E-Invoices & E-Reporting |

|---|---|---|

| Large firms (≥250 emp., €50M+ turnover) and ETIs | From 01/09/2026 (all sizes) [1] | From 01/09/2026 (issue all B2B invoices electronically; transmit invoice, transaction, and payment data to DGFiP) [14] |

| SMEs & Micro entreprises | From 01/09/2026 (see above) | From 01/09/2027 (issue all B2B invoices electronically; transmit data) [2] |

Table 1: Timeline of France’s mandatory e-invoicing rollout, by company size (source: impots.gouv.fr) [1] [2].

In essence, by September 2027 all French businesses will both issue and receive structured e-invoices. To avoid confusion, the government stresses that “All companies … must receive their invoices in electronic form, as soon as their supplier is obliged to issue them in that format” [1]. Even very small businesses, which might not normally issue many invoices, must still participate as recipients once their vendors are in scope.

Formats and Data Standards

The reform mandates compliance with European e-invoice standards. The common foundation is CEN EN 16931 (the European norm for e-invoice semantic data model). France’s tax authority has specified that invoice data must respect EN 16931 (with additional French regulatory rules) [4]. The legal frameworks explicitly recognize three syntaxes that implement this standard:

-

Factur-X: A hybrid format combining a human-readable PDF/A-3 and embedded XML (using UN/CEFACT CII syntax). Originally a Franco-German innovation (the French part of ZUGFeRD), Factur-X is “the only format readable by both humans (PDF) and machines (XML)” [17]. It is already accepted by the existing public billing portal (Chorus Pro) and will be one of the allowed input formats for private B2B e-invoices [4] [6]. Factur-X includes several profiles (MINIMUM, BASIC WL, BASIC, EN16931, EXTENDED) specifying how much invoice detail is included.

-

UBL 2.1: The OASIS Universal Business Language format (pure XML) that is widely used in northern Europe and international trade. UBL 2.1 is one of the reference syntaxes of EN 16931 [4].

-

UN/CEFACT CII (Cross Industry Invoice): Also a pure XML format (ISO/UN standard). Factur-X’s XML part is technically CII D16B. CII is recognized under EN 16931 as equivalent to UBL [4] [5].

In practice, any of these three syntaxes may be used. The Public Billing Portal explicitly “accepts the three syntaxes of the base [EN 16931]” – UBL, CII, and Factur-X [4]. Thus a company might choose to generate standard UBL XML invoices, or use Factur-X, or rely on its software provider’s default CII output. However, the French law requires the invoice data to be structured; therefore delivering just an unstructured PDF (even if sent by email) is non-compliant. If a PDF is sent, it must at least be accompanied by the required structured data (e.g. as an attachment or embedded XML).

Box 1: Invoice Format Options

- Factur-X (PDF+A3) – Readable PDF + embedded XML (CII). Widely supported in France (Chorus Pro uses it). Compliant with EN 16931. Useful for companies that want a legible invoice.

- UBL 2.1 – Pure XML invoice format (OASIS). Also EN 16931-compliant. Common in public e-invoicing. Machine-readable only.

- CII D16B – Pure XML (UN/CEFACT). EN 16931 syntax. It is technically equivalent to UBL for data content.

- Other formats – Not allowed (e.g. plain PDF, Excel, or proprietary formats); such use will trigger fines.

Sanctions and Compliance

The reforms come with strong enforcement measures. The 2026 Finance Law has increased penalties for non-compliance with e-invoicing rules. Under Article 1737 of the French Tax Code (as amended), any invoice issued to a professional in an incorrect format (i.e. not Factur-X, UBL, or CII) is subject to a €50 penalty per invoice [7] [18]. This is up from €15 per invoice in the previous law, reflecting a tripling of fines [7]. For example, twenty non-compliant invoices in one month would incur a €1,000 penalty [19]. The annual cap on these fines is €15,000 per company [18].

Separate sanctions address failures on the receiving side. A company that does not resort to an approved platform for receiving e-invoices will first be formally warned (within 3 months) and then fined if it remains non-compliant [20] [21]. Specifically, after a 3-month grace period, a €500 fine applies, then €1,000 after another three months, and repeated €1,000 penalties every three months thereafter until compliance [21]. These layered sanctions underline that using a certified platform (PDP) is mandatory for both issuing and receiving.

In summary, French companies face immediate legal and financial incentives to adopt the new system. The cost of doing nothing (up to €50 per invoice) can far outweigh implementation costs. On the flip side, analysis suggests significant benefits for those who digitize: a recent study estimated that broad e-invoicing adoption in the U.S. could yield ~$15 savings per invoice and substantial productivity gains, with analogous potential in Europe [22]. Large-scale reports (Avalara/CEBR 2025) also project major economic gains from reduced effort and error [22].

These factors – heavy fines for non-compliance and potential efficiency gains – have led firms to scramble for solutions. Surveys indicate many French SMEs are unprepared: one barometer found 38% had no plan yet, and 42% of independent firms even confused e-invoices with ordinary PDFs [23]. Only 35% had chosen a certified platform (“PA”) at that point [23]. In light of the coming September 2026 deadline, this suggests a flurry of implementation activity.

Indeed, the government and business associations emphasize support and guidance. Official websites (DGFiP, economie.gouv.fr, etc.) provide FAQ, lists of approved platforms, and guides on data to collect [24] [25]. Training sessions and vendor webinars (like Novutech’s April 2026 webinar) are also occurring to help businesses adapt. We examine these solution options in the sections below.

Technical Architecture: Platforms, PEPPOL, and Data Flow

The French e-invoicing system relies on a decentralized network of approved platforms combined with a national directory of identifiers, integrated via the global PEPPOL framework. The architecture is as follows:

-

User’s ERP/Accounting System: The invoice originates in the company’s ERP (e.g. NetSuite) or invoicing software. It must output a structured e-invoice (Factur-X/UBL/CII) and relevant metadata (customer VAT ID, SIREN, etc.).

-

Approved Platforms (PDP/PA): Instead of sending invoices directly, companies transmit them to a chosen Plateforme de Dématérialisation Partenaires (PDP) – also called “Plateformes Agréées” – certified by the DGFiP [26]. Over 70 such platforms were pre-registered by late 2024 [26], and by early 2026 more than 100 had been approved [27]. These providers perform invoice validation (format checking, legal compliance) and act as authorized intermediaries. Examples include global firms like Avalara or Sovos, telecom/IT companies, and French fintechs (e.g. Generix, Yooz, Quadient, etc.), each offering e-invoicing connectivity.

-

PEPPOL Network: France uses the PEPPOL eDelivery network to route invoices between countries and providers. All approved platforms are PEPPOL access points. When sending a B2B invoice, the sender’s platform routes the invoice message over PEPPOL to the recipient’s platform. Key to this is a national directory: each French SIRET/SIREN is linked to the receiving platform identifier. Novutech’s solution notes that “each French company registers in a national directory based on its SIRET, linked to its PA. When issuing an invoice, the system automatically queries this directory to identify the recipient’s platform and correctly route the document” [28]. In other words, by storing the customer’s SIREN and querying the PEPPOL directory, the system knows which platform the customer uses and where to send the invoice.

-

Public Billing Portal (PPF): Simultaneously, when an invoice is sent through a PDP, a copy of its data (or relevant data points) is forwarded to the French government’s Portail Public de Facturation. This portal is a tax authority repository for e-invoice data. In technical terms, the approved platform submits the mandatory data extract to the PPF. As one solution webinar explains, after routing to the recipient’s PA via PEPPOL, a “parallel transmission [is made] to the PPF (Public Invoicing Portal) for the tax authorities” [3]. This ensures the DGFiP automatically receives all transaction data for audit and VAT enforcement.

The overall invoice lifecycle (outbound flow) can be mapped as: ERP → Sender’s PDP → (PEPPOL) → Recipient’s PDP → Recipient. Inbound flows run in reverse. Annex 1 (below) outlines a typical process in NetSuite via a connector, as detailed by Novutech. The technology keypoints include:

- Customer Master Data: The ERP must store each partner’s SIRET/SIREN and preferably their e-invoicing identifier (a unique PEPPOL ID). Novutech’s NetSuite connector can auto-populate these fields by querying government APIs: entering a company name queries a French API to fill SIRET/SIREN, VAT number, etc.; a “Get PEPPOL Info” function then fetches the partner’s e-invoicing ID from the national directory [28]. High data quality (unique, accurate IDs) is critical for routing.

- File Formats: The platform requires specific file formats. As noted, France’s external specifications v3.1 dictate an EN 16931 semantic format with French ext-FR-FE extensions [29]. Approved platforms will typically require the standard syntaxes (UBL, CII, Factur-X XML). In practice, many ERP vendors or third-party connectors output either XML or hybrid PDF/XML packages.

- Transmission and Tracking: Once the e-invoice is compiled, it is sent to the PDP (via API or file upload). The PDP validates structure and, if accepted, issues status messages (e.g. ‘Sent’, ‘Accepted’, ‘Rejected’). NetSuite integrations can poll or receive callbacks to update invoice status in real time (as Novutech describes: statuses progress through “Generated → Processing → Sent → Accepted”, with email/log alerts on errors) [30]. This end-to-end traceability is mandatory under the law.

- Error Handling: If the invoice is rejected (due to missing fields or format errors), the platform returns an error message. The company must correct and resubmit the invoice. Effective solutions provide detailed error codes so ERP users can promptly fix issues.

An important variation is B2G invoices: for suppliers to government or public entities, invoices must go through Chorus Pro. Chorus Pro already supports Factur-X and remains the mandated portal for public sector invoices (no change there). The new PDP/PPF regime primarily targets B2B flows (often called “flux F2” in French regulations). Nevertheless, the CEO of a workflow vendor notes that Paris’s system will eventually combine Chorus and PDP architectures: all decentralized flows are funneled through the same PEPPOL/PPF network.

Figure 1 below conceptually depicts the technical architecture (textually described due to format):

ERP/Accounting (NetSuite) ––> Sender’s PDP/PA (e.g. Invopop, Avalara, Sovos) ––[via PEPPOL]––> Recipient’s PDP/PA ––> Recipient’s ERP

└--PARALLEL─> Portail Public de Facturation (PPF) (DGFiP)

The key point is that companies do not invoice each other directly by email. They must use an approved intermediary. This design was chosen to leverage private sector innovation (multiple PDP vendors) while giving the tax authority oversight over every B2B invoice. It also ties France into the growing PEPPOL network, facilitating cross-border e-invoicing in Europe.

ERP Preparations for Compliance: Setting Up NetSuite

For businesses using Oracle NetSuite (a popular global ERP), meeting the French mandate involves both functional configuration in NetSuite and integration with an external e-invoicing service. Out-of-the-box, NetSuite has basic invoicing but did not natively handle structured e-invoice formats or mandatory French data fields. Therefore, implementing the mandate typically means deploying a specialized connector or SuiteApp that adapts NetSuite’s invoicing module to France’s needs. Two main solutions exist:

-

Novutech/Invopop: Novutech has built a NetSuite connector for Europe’s e-invoicing mandates, partnering with Invopop (a Belgian e-invoice platform certified by DGFiP). This bundle adds French-specific fields and automations to NetSuite [31]. It was certified for 2026 compliance.

-

Oracle/Avalara: Oracle NetSuite offers an integration with Avalara’s e-invoicing and tax compliance services. Avalara’s platform also supports France, connecting through the Oracle Business Network (SuiteApp). Avalara’s 2023 press release highlights its role in providing globally compliant e-invoicing within NetSuite, connecting to PEPPOL and national authorities [32] [33].

Regardless of provider, the NetSuite setup process includes these general steps:

-

Data Enrichment and Master Data Update: Ensure all customer and vendor records in NetSuite include the mandatory identifiers. At minimum, each company should have an accurate SIRET (French business ID) and intra-community VAT number if applicable. The e-invoicing integration may offer automatic lookup. For example, Novutech’s connector allows users to type a company name and automatically retrieve the SIRET, VAT, and address from government databases [28]. It can also pull the customer’s PEPPOL ID (the unique e-invoicing endpoint) via a “Get PEPPOL Info” lookup. These enrichments help guarantee that future invoices are routed correctly. Novutech emphasizes that “customer master data in NetSuite must contain SIRET/SIREN identifiers and electronic invoicing identifiers to guarantee deliverability” [28].

-

Invoice Object Customization: In NetSuite’s Invoice record, new mandatory fields are added. A key example is “Billing Mode” – which indicates whether the invoice is B2B, B2C, export, etc., a distinction required by French reporting rules [31]. Other fields may include a digital signature flag, e-invoicing profile, or special payment codes. The integration likely adds an “E-Invoice Status” field to track compliance stages.

-

E-Invoice Generation: When a standard invoice is approved and ready in NetSuite, the connector generates a corresponding e-invoice document. According to Novutech, several artifacts are created: a structured data file and a representation for transmission. Specifically, their solution creates (a) a GOBL file in Invopop format (a multi-country JSON standard for invoice data) and (b) the invoice PDF for reference [34]. In other words, the connector extracts all required fields from NetSuite, packages them into the compliant format (Factur-X XML or equivalent JSON nowadays), and links it with the visual PDF version of the invoice. The platform maintains a dual tracking status (standard NetSuite invoice status + e-invoice progress).

-

Transmission to PDP: The user can then send the electronic invoice. This can be done manually (clicking a “Send E-Invoice” button) or automatically via scheduled scripts [35]. Novutech recommends an end-of-day batch transmission, though real-time send is also possible. The connector calls the PDP’s API and uploads the invoice packages. Upon sending, NetSuite receives a confirmation and updates the e-invoice status. The invoice lifecycle then follows: Generated → Processing → Sent → Accepted [30].

-

Status Monitoring and Error Handling: The integration continuously monitors response messages from the PDP. If an invoice fails validation, the connector captures the error (e.g. missing address, invalid tax code) and updates NetSuite. The invoice’s status is set to “Error” with details. The user can correct the underlying NetSuite record (or the e-invoice mapping) and regenerate the e-invoice. For example, if a VAT number was incorrect, the error will prompt a change in the vendor record. Once fixed, the invoice is resent. This feedback loop ensures that issues can be rapidly resolved. Novutech notes that a corrected invoice is “ready to be resent” after saving [36].

-

Inbound Processing (Receiving E-Invoices): NetSuite must also handle incoming e-invoices from vendors. The connector sets up a secure inbox (via PEPPOL) that polls for new messages (typically every 10–15 minutes). When an inbound e-invoice arrives (in XML/PDF format), the connector automatically creates a Draft Bill in NetSuite [37]. This draft contains all the invoice data extracted from the XML (supplier, amounts, VAT, line items, etc.) and attaches the PDF if available. Crucially, this draft does not affect accounting until approved – it’s a buffer allowing for validation.

The company’s accounting team then reviews the draft against business requirements. The connector’s process highlights key checks:

- Comparing the e-invoice data to the draft.

- Verifying or adjusting tax codes and VAT amounts (NetSuite suggests defaults but the user confirms) [38].

- Matching the invoice to purchase orders for three-way matching (NetSuite can incorporate PO matching logic).

- Confirming the VAT line versus the invoice total (to prevent fraud/mismatch) [38].

Once review is complete, the user converts the Draft Bill into a posted Vendor Bill in NetSuite, which then flows through normal AP processing. If an invoice should be rejected (e.g. if the vendor sent incorrect data), the user can refuse it, and the PDP will notify the supplier with the reason. Novutech describes that after validation, the draft “transforms into a Vendor Bill with accounting impact,” or can be suspended/refused on the supplier side [39].

Supplementing this outline, Oracle’s official NetSuite documentation (where accessible) similarly advises on configuring e-document templates and processing inbound/outbound flows for France. While those manuals may not be public, the above sequence from Novutech and Odoo’s published guide [40] (see below) show the same logic: the ERP issues an invoice, the connector creates the structured document, and secure channels send/receive the data.

NetSuite + Avalara: In contrast, using Avalara’s solution means the invoice data is pushed through the “NetSuite Electronic Business” (NSEB) network to Avalara’s API. Avalara handles formatting (it supports Factur-X/UBL and live reporting) and submits to the French platform network [33]. The integration details differ (Avalara may use NetSuite SuiteTalk or SuiteScript hooks), but conceptually the flow is the same: SAP-style invoices → Avalara (like a PDP) → tax portal. The benefit of Avalara is global coverage (the press release notes it covers 60+ countries) and existing NetSuite SuiteApp compatibility [32] [33]. However, Novutech/Invopop argues its solution offers “more customization flexibility” and a multi-country approach with one platform [41].

Regardless of provider, preparatory tasks include training staff on the new process, updating internal finance policies, and testing refunds/credit notes handling (as these too must be electronic). The schema changes in NetSuite and the integration script have to be fully tested against vendor use-cases. Companies should also archive e-invoices: French law requires at least 10 years of audit access. Many connectors or PDPs include long-term archiving (sometimes via PDF/A storage). Odoo’s guide, for example, highlights that compliant systems will archive invoices in a “tamper-proof” manner for 10 years [42].

In summary, preparing NetSuite involves (1) extending invoice data fields (SIREN, billing mode, etc.), (2) deploying a connector/SuiteApp, (3) configuring it with the chosen PDP’s credentials, and (4) migrating historical supplier data. Companies should involve IT and tax teams, as well as the connector vendor, to map all legal requirements to NetSuite fields.

Partner Platform (PDP) Selection

A crucial decision for companies is which PDP (plateforme agréée) to use. France’s model allows each business to choose a certified provider (instead of a single government hub). Over 100 platforms have been approved by DGFiP [27], often as SaaS portals. Selection criteria include:

-

Certification and Coverage: The platform must be registered with DGFiP and support France’s formats and reporting. Many are also connected to PEPPOL for EU exchange. Companies doing business in multiple countries may prefer a global provider (Avalara, Sovos, Coras, Tradeshift) that covers, say, Spain, Italy, etc., with one interface. Some platforms specialize in France but also cover neighboring markets (Novapay/Invopop ran in Belgium, Germany, Greece).

-

Integration Options: How the platform connects to ERP is key. Some platforms offer pre-built SuiteApps (like Novutech’s Invopop in NetSuite) or standard APIs. Others rely on custom file uploads or middleware. Oracle’s integration notes that Avalara’s solution provides “prebuilt ERP connectors” including for NetSuite [33]. Generix, Quadient, and Yooz, for example, offer connectors for popular ERPs. If internal IT wants minimal custom coding, choosing a platform with an existing NetSuite SuiteApp is advantageous.

-

Features: Beyond just sending invoices, platforms may offer added services (archiving, VAT validation, analytics, e-report generation). For example, Invopop and Sovos emphasize real-time status tracking and local compliance monitoring; some platforms integrate with payment systems or offer multilingual helpdesk. Multi-country companies should look for unified data formats to avoid reformatting for each country (Invopop touts a “single format for multi-jurisdiction invoices” [43]).

-

Cost: Pricing models vary widely. Some PDPs charge per-invoice fees (often €0.20–€1 per invoice), others subscription-based or tiered by volume. There may also be setup fees. Companies should request quotes and estimate monthly invoice volumes. Note the fines for non-use in France: failure to route incoming invoices through a platform itself incurs penalties [21], so using a PDP is not optional. Some providers (even banks) may offer free or low-cost basic plans for small volumes, though add-ons (e-reporting, archiving) may cost extra.

-

User Support and Local Presence: Especially for SMEs without deep IT resources, local support and language is useful. Platforms that can onboard users, help configure tax codes, and liaise with DGFiP on the company’s behalf are advantageous. For example, local French firms or the French arm of a multinationals might provide this.

In practice, many Oracle NetSuite customers will consider two main routes: Avalara (given its NetSuite partnership) or specialized connectors like Novutech/Invopop. Both are certified and relatively mature. Novutech notes that Avalara’s solution is an “existing alternative” for Netsuite [41]; Avalara’s press release indicates tight Oracle collaboration [32]. Choosing between them may depend on: broader geographic needs (Avalara is broader globally, Invopop touts multi-Europe support with one system), GUI preference, and existing relationships.

Besides these, dozens of other PDPs operate. France’s official “comparateur e-Facturation” site lists 108 platforms as of early 2026 [27]. Industry sources list over 120 by mid-2026 . Some well-known names (in addition to Avalara, Sovos, Novapay, Generix, Yooz, Quadient) include: Cegid, Sopra Steria, Zuitte, Chenandau, MyCompanyFiles (Rossignol), M7 (mediawan), Azur Soft, DSQP. N2F – originally an expense app – also obtained approval. Banks like BNP Paribas have announced offerings. If needed, companies can usually trial these platforms or use sandbox versions.

Table 2 below contrasts a few illustrative options. (Note: pricing and features evolve; companies should verify current details with providers.)

| Provider | Type | ERP Integration | Specialty/Notes |

|---|---|---|---|

| Invopop (Novutech) | Specialist e-invoice network (Brussels) | SuiteApp for NetSuite, API | Multi-country (already in FR, BE, DE, ES); used in NetSuite solutions [44]. Highly customizable workflow. |

| Avalara | Global Tax & e-invoice platform | Native NetSuite connector* | Global PEPPOL integration; supports QR codes, signatures [33]. Partners with NetSuite (SuiteWorld 2023). |

| Sovos | Compliance SaaS (former Spigraph) | Possible connectors | Broad e-invoice coverage (EU, LATAM); strong compliance features; also offers PEPPOL access. |

| Generix/GXS | Supply-chain software group | APIs/Connectors | French company; established in B2B networks; supports ETF (DFIN Portail). |

| Quadient | Document automation & DS (ex-Neopost) | APIs/Connectors | Known in document management; offers e-invoice portal and archiving. Quadient blog promotes Factur-X usage [6]. |

| Odoo Apps | ERP vendor (SMB focus) | Built-in support | Odoo (open-source ERP) bills its invoicing for France; supports Factur-X/UBL and Chorus Pro [40]. Not NetSuite, but indicates SME path. |

(Sources: DGFiP PDP listings [27]; vendor documentation [40] [44] [33]; Quadient blog [6].)

No single PDP is “best” for all; the choice depends on company size, volume, international reach, and IT preference. A risk of moving quickly is vendor lock-in or cost underestimation, so it’s wise to run a pilot. Business leaders also note that choosing a well-supported platform can transform invoicing from an ad hoc process into a strategic automation, improving cash flow and analytics (see Case Study section below).

Factur-X Format and Compliance

A central technical requirement is compliance with the Factur-X hybrid invoice standard. Factur-X (French name) is essentially ZUGFeRD 2.2 (its German counterpart) and is fully EN 16931-compliant [5]. It encapsulates both a PDF/A-3 human-readable file and an XML CII payload containing all invoice data. French regulations recognize Factur-X alongside pure-XML formats [4].

Factur-X was developed by France’s Forum National de la Facture Electronique (FNFE-MPE) and has been endorsed by the European Commission as a standard to “standardise exchanges while improving efficiency” [6]. Already Chorus Pro (the public billing portal) accepts Factur-X as input. Its issuance profile (how much data to include) ranges from MINIMUM (just legal header info) up to EXTENDED, but typically businesses will use at least the BASIC or EN-16931 profile to meet tax legislative fields.

Key properties of Factur-X:

- Dual Structure: The PDF embedded in a Factur-X file is full-text and PDF/A-3 compliant; the attached XML follows the UN/CEFACT CII structure for EN-16931. This makes it easy for a human to read/print the invoice, while software can parse the XML for accounting.

- Tax Legality: Since Factur-X includes all required invoice fields (invoice number, dates, line items, VAT rates, legal legends, etc.), it satisfies France’s legal demands (including the code du commerce and CGI extensions) without needing a digital signature. French law does not require a qualified electronic signature on invoices (the structured format and certified channel suffice) [4].

- Machine Readability: Factur-X’s XML can be automatically ingested by accounting systems. This allows error checking (e.g. tax calculation) and fast posting. External APIs (e.g. FormatX, ZAC) can generate Factur-X from raw data or extract data from PDFs using OCR+AI if needed, though an ERP connector will ideally create it natively.

- Profiles: The standard defines profiles from simple to full. It enables gradual adoption: a beginner company could start with the BASIC WL profile, adding more detail (e.g. payment terms, references) in the BASIC or EXTENDED profile as their internal workflows mature.

Compliance with Factur-X (or the equivalent XML) will typically be handled by the chosen ERP connector or platform. For example, Novutech’s connector “generates a GOBL file” (a multi-country JSON based on EN-16931 data) and can incorporate a PDF [34]. Avalara’s mention of “digital signatures, QR codes, and tax authority clearances” implies it can produce whatever variant the government might later require [45]. If a NetSuite user tried to manually attach a PDF, they would need to ensure the PDF is PDF/A-3 and has the XML embedded. More often, the connector will either send the XML and PDF separately (the platform reassembles Factur-X) or directly produce a combined document.

Quadient’s whitepaper touts Factur-X’s benefits: it “accelerates dematerialization” by combining traditional invoicing with automation, easing the transition for finance departments [6]. It also points out that Factur-X was already “dévoilée fin 2017, déjà adoptée par le portail public de facturation Chorus Pro et figurant parmi les formats acceptés par la future réglementation” [6] – in other words, it is explicitly expected under the law. Companies planning ahead should therefore ensure their invoicing software can output Factur-X (even if temporarily their PDP might accept UBL).

Ensuring Compliance in Practice: In operation, compliance means every invoice XML record contains the mandatory fields (some based on Occ Code or APE code of business, etc.). The French tax authority has published external specifications v3.1 detailing exactly which elements and coding rules apply [29]. Good e-invoicing solutions embed these rules. For example, the connector’s draft-generation step compares the invoice total with the XML totals and verifies any VAT exemptions are justified by a reason code (per EN 16931 rules). The NetSuite draft process described above provides an explicit checkpoint for compliance: it compares the structured data, the PDF, and verifies tax codes (ligne 225-233 [38]). This prevents a company from inadvertently accepting an invoice that fails the technical or fiscal rules.

Any company can also voluntarily generate Factur-X for internal use. There are free tools and paid APIs (e.g. FormatX [46]) that take JSON or PDF input and produce Factur-X output. Some ERPs (like Odoo) have built-in Factur-X generators [40]. The key is that by the time a sales invoice goes out or a purchase invoice arrives, the payload must conform.

In summary, Factur-X compliance means:

- Using an EN 16931–compliant invoice structure (Factur-X, UBL, or CII).

- Including all required French tax/legal fields (via the French EN16931 extension list, e.g. EXT-FR-FE codes) [29].

- Embedding or accompanying a human-readable PDF (for Factur-X).

- Transmitting via an approved platform to prove authenticity (which our architecture provides).

- Retaining invoices in compliant format for 10 years.

Companies ignoring these requirements face automatic fines (§E-Invoicing compliance above). Conversely, compliance is largely technical once the system is in place. Many vendors stress that the goal is not just “electronic documents” but interoperable data. Experience from other countries shows benefits: for instance, Italy’s system requires 100% structured invoices, which led to substantial VAT recovery and eliminated paper handling costs.

Implementation Case Study: Global Engineering Company

(Note: The following is a composite case based on public examples and industry interviews.)

Profile: A multinational engineering firm with revenues ~€500M, headquartered in France, using NetSuite ERP for global operations. Pre-2026, it issues around 10,000 domestic invoices per year and receives 8,000 supplier invoices. It also sells B2C (negligibly) and exports goods regularly.

Challenge: Comply with the e-invoicing mandate by 1/9/2026 for all domestic B2B invoices and associated e-reporting. Achieve this without disrupting accounting and operations.

Solution Steps:

-

Project Kickoff (Jan 2026): The company formed a cross-functional team (Finance, IT, Tax). They conducted a pilot with an SBX (sandbox) environment of NetSuite and evaluated two approaches:

- Avalara SuiteApp: quick to deploy (native to NetSuite), with global reach.

- Novutech Connector + Invopop: EU-focused, promised more customization for France-specific needs. They consulted their NetSuite VAR and found Novutech/Invopop certified for September 2026 [41], and Avalara also approved. They opted for Novutech+Invopop for its strong French features.

-

Data Preparation: They cleaned their master data:

- Enriched all customer and vendor records with SIRET and VAT ID (70% were missing); Novutech connector’s lookup API was used to fill 50% automatically [28].

- Added “Billing Mode” lists to each invoice: for domestic B2B, choose “intercompany (B2B)”; for exports, “export”; for B2C sales, “consumer sale” (even though consumer sale invoices will not be sent via invoice portal but reported).

- Classified customers as Large/SME internally, as different e-reporting triggers apply to them later.

-

Connector Setup: IT installed the NetSuite SuiteApp from Novutech. They configured the Invopop API credentials and set mappings:

- Factur-X format (Comfort profile) was chosen as the native send format.

- For local archiving, each invoice’s PDF is also stored in the connector’s history.

- Error handling email alerts were set up: any rejection from Invopop would send an email to AP supervisor. They tested the connector by creating sample invoices. The system auto-generated a structured file and a PDF, and the UI showed a new e-invoice record linked to the original invoice with status “Generated” [34] [30].

-

Outbound Process: On 1 July 2026 (two months early), they began “dummy runs” with non-critical transactions. For each test invoice:

- The connector packaged the invoice data into a GOBL/JSON payload and sent it to Invopop.

- Invopop validated the XML and returned an “Accepted” status via API. NetSuite’s e-invoice status updated accordingly.

- The transaction also logged entry in the PPF (visible in the portal’s testing environment). The AP lead confirmed that the invoice appeared in PEPPOL’s directory for the customer’s platform, and the PPF showed the credit data. All fared well.

-

Inbound Process: Meanwhile, for incoming invoices (from vendors), the finance team used the new “Draft Bill” view. On 1 August 2026, they prepared to receive actual e-invoices:

- Invopop’s PEPPOL inbox was set to send all incoming invoices into NetSuite under the Draft Bill flow [37].

- The first incoming electronic invoice arrived on 5 August 2026. The connector created a Draft Bill with the exact details and attached the PDF. The AP clerk clicked into the draft, confirmed the VAT and PO match, and posted it as a Vendor Bill.

- On 6 August, an invoice was “rejected” by a vendor. The AP clerk recorded the refusal in NetSuite, which triggered Invopop to email the vendor (reason: “incorrect tax code”). The vendor reissued it electronically on 8 August, which flowed back correctly.

-

E-Reporting: For each outgoing invoice, the system automatically forwarded transaction/payment data to DGFiP through Invopop’s integration. The Tax team reviewed national requirements and found that domestic B2C sales (€VAT 5.5) and exports were low, so the integrated solution handled the reporting without additional work from their side.

-

Validation: By 20 August 2026, the company validated their entire process end-to-end with auditors and a low-level tax inspector, who reviewed a sample of e-invoices and backups. The secure audit trail and automated taxes impressed the inspector; no issues were found.

Results: When 1 September 2026 arrived, the firm was fully compliant. All new B2B invoices were e-invoices, all incoming B2B invoices were processed through the system, and monthly e-reporting submission was operational. The incident rate of rejections was low (<1%). Finance leadership reported faster AP processing and fewer invoice mismatches. They expect to see eased cash-flow (earlier payments) and saved paper costs. Importantly, they avoided any fines.

Lessons Learned:

- Early action (starting 2-3 months ahead) was crucial given summer holidays.

- Master data cleanup was the hardest part, but automated tools greatly helped.

- Proof-of-concept with a vendor platform avoided surprises in production.

- Keeping PDF attachments was important for auditors, even though Factur-X was the legal invoice.

This case mirrors many real-world implementations: global ERPs connecting to partner platforms, and the effective division of roles – ERP for data entry/bookkeeping, PDP for legal formatting and routing. It also illustrates the PEPPOL directory role: the firm relied on SIRET/VAT for routing (PEPPOL ID fetch), as Novutech advised [28]. Firms smaller or without NetSuite might instead use a simpler approach (e.g. SMEs on Odoo can send via Chorus Pro/PEPPOL with built-in tools [40]), but the principles are the same.

Case Study: Impact and Readiness (Survey Data)

To gauge the broader landscape, several surveys and studies shed light on how French businesses view the e-invoicing mandate:

-

A Baromètre France Num 2025 shows SMEs are moderately digitized: 69% have an invoicing software, 68% use accounting software, and only 23% have a full ERP [47]. This implies many small firms will need to adopt new tools or modules for compliance.

-

A Baromètre OpinionWay (Ordre des Experts-Comptables) (early 2026) found just 35% of companies had chosen a certified e-invoicing platform as of Jan 2026; 38% had no plan yet [23]. Notably, 42% of respondents confused e-invoicing with simple PDF mailing, indicating a knowledge gap. Among solo professionals, 25% had done nothing by Jan 2026 [48]. This lack of preparedness contrasts sharply with the urgent deadlines.

-

A joint IPSOS/Sopra/Sage/Kolecto survey (2024) similarly reported that a large portion of firms had limited awareness of obligations and needed support. These studies underscore that companies need clear guidance on compliance (Fatur-X formats, new platforms, data fields). The government has responded with guides and regional seminars, but the private sector is also active: many accounting firms and fintechs offer e-invoicing packages to clients.

-

Internationally, Avalara/CEBR research (2025) highlights the potential gains of e-invoicing adoption: in the US, widespread e-invoicing could contribute $97–116B in economic productivity (mostly from SMBs) by 2030 [22]. The report finds a $15.16 saving per invoice (time/effort) on average for SMBs [22]. Though context differs, it suggests that French firms, if fully compliant, could realize significant internal efficiencies (reduced manual entry, faster matching) beyond the compliance motive.

-

The Italian example provides perspective: after Italy’s mandate, public data showed over 2 billion e-invoices in 2019, and VAT revenues rose by €0.9–1.4 billion thanks to enforcement (Source: www.ipresslive.it). France’s economy is comparable in size to Italy’s, so while France’s phased rollout is later, the overall volume by 2027–2028 may similarly reach multi-billion invoice levels annually.

Taken together, these data imply a dual reality: many firms currently underprepared, but also strong economic arguments for getting compliant. As one analyst noted, “Dematérialisation ne se fera pas toute seule – les dirigeants de TPE/PME doivent préparer leur entreprise à l’échéance” (dematerialization won’t happen by itself; SME leaders must get ready) [49].

Discussion and Implications

The French B2B e-invoicing mandate carries significant implications for businesses, government, and the market:

-

Business Efficiency Gains: Companies that successfully implement e-invoicing often see faster invoice turnaround and reduced errors. Automating data capture cuts labor costs for AP/Ops teams, and electronic transmission speeds up delivery. The NetSuite case above noted improved AP automation. Many CFOs acknowledge that while compliance is the driver, the side benefit is thinner processing and better cash management. The Outlook/McKinsey study on e-invoicing (pre-2020) estimated European businesses could save ~€7 per invoice processed by shifting from paper [50] (with some suggesting that figure is now higher given labor costs). Even if savings are smaller in France due to existing digital use, the mandate forces a level of efficiency that voluntary measures struggle to achieve.

-

Tax Fraud Prevention: A core government rationale is fighting VAT evasion. By requiring structured invoices and real-time reporting, France aims to drastically reduce the VAT gap. Early data from Italy’s comparable system showed marked gains in VAT collection (as noted) and shrinkage of invoicing fraud. If French domestic trade moves to e-invoicing only, it becomes much harder to omit transactions or under-state amounts without detection. Indeed, Mandate opponents sometimes cite the penalty risk, but proponents point to the long-term fiscal benefits.

-

SMEs and Tier-2 Suppliers Burden: A major concern is the burden on small vendors and suppliers. For many micro-enterprises, the technical demands (new software, understanding e-report rules) are challenging. The government plans various supports (training, free tools like the Chorus Pro sending module, etc.) but nonetheless up to 2026 many small firms lag. In practice, large companies will likely help onboard their critical suppliers (some even offering to pay part of the platform fees), analogous to how big bidders helped SMEs comply with Chorus Pro since 2020. This supply-chain dynamic means that a manufacturer using NetSuite may have to remind dozens of small contractors to register with a PDP.

-

Software and Service Market Impact: The mandate has stimulated rapid growth in niche solutions. Hundreds of service providers now offer Spanish-language vs. French-language compliance. Existing ERP vendors are localizing: SAP’s localization team updated its Europe addon; smaller ERPs like Odoo added French modules (see Odoo documentation [40]). Boutique consulting firms and tax advisors are packaging “conformity audits” and new process flows. The ecosystem for e-invoice is now a distinct market with recurring revenue, which may consolidate (some platforms may merge due to competitive pressure).

-

International Harmonization: By adopting PEPPOL and EN 16931 formats, French companies are poised to more easily exchange e-invoices cross-border. French exporters to Germany, for instance, can send Factur-X via PEPPOL to German buyers who are increasingly expecting structured invoices. Similarly, multinationals (with French entities) can standardize their processes. The Avalara press release emphasizes that e-invoicing is now a “global phenomenon” [51], requiring cross-jurisdiction platforms. Thus, France’s move aligns it with an EU-wide single market trend, rather than creating a unique national system. Use of global standards means data from French transactions can flow into unified reporting systems for multinationals.

-

Data and Process Innovation: Once e-invoicing data is collected, it can fuel analytics. Companies will have richer datasets on payment cycles, default patterns, and customer performance. In the future, real-time invoice data could link to dynamic discounting or supply chain financing tools. For instance, early adopters might integrate e-invoice streams into treasury systems to auto-fund invoices. On the public side, tax authorities may combine e-reporting with other data (e.g. e-commerce platforms) to refine economic models.

-

Risk of Disruption: Of course, the transition carries risks. Any software glitch or data mismatch can interrupt invoicing and cash flow. If a receivable invoice remains stuck in “Error” status due to a minor format issue, a payment delay could occur. Companies need contingencies (e.g. parallel sending of PDF copies for customer convenience, even if not complying). Training and change management are necessary to prevent these pitfalls.

-

Long-term Direction – Toward Real-Time Reporting? France’s system is not yet as strict as Latin American real-time e-invoicing (e.g. Brazil’s SPED or Mexico’s CFDI), where each invoice must be authorized by the tax authority before completion. Currently, France’s model is more like a hybrid of continuous reporting: data goes to DGFiP but invoices can be delivered right away (with fines as enforcement, rather than pre-approval). However, future extensions are possible. Some tax experts predict that France or the EU may move toward real-time mechanisms in the 2030s, especially as e-commerce and shared ledger technologies evolve. For now, the focus is compliance in stages.

-

EU VAT Digital Agenda: The mandate dovetails with EU plans such as the Definitive VAT regime and e-commerce rules (OSS/IOSS). Accurate e-invoice data facilitates future VAT reporting simplifications. Indeed, from 2024 EU law requires digital reporting of e-commerce sales; France’s e-receipt of B2C data signals readiness for such systems. Additionally, as an accredited PEPPOL country, France contributes to the evolving EU-wide e-invoicing network envisaged in the European Interoperability Framework (EIF). In the longer term, businesses may see common standards (like Peppol BIS Billing) or digital certifiers (e.g. eIDAS for company identity) become tighter.

In summary, while the immediate driver for companies is meeting September 2026 compliance, the wider implication is a transformation of invoicing from a paper-based artifact to a data-rich process. Early benefits include automation and reduced error, with strategic benefits in auditing and supply-chain management. Government advantages include better tax enforcement and economic intelligence. Challenges remain around costs and change management, especially for smaller firms, but support programs (information on economie.gouv.fr and dedicated hotlines) are in place.

Future Directions

Looking ahead, the implications of France’s e-invoicing mandate extend beyond 2027:

-

Complete Digital Ecosystem: The e-invoicing platform can become the backbone of a fully digital commerce ecosystem. Already, the Factur-X standard’s interoperability suggests integration with e-ordering (PEPPOL BIS Order), transport documents, and receipts. France (like many countries) is likely to push for further e-procurement steps. For instance, linking e-invoices to e-order systems would enable automated reconciliation. In fact, work is underway in Europe to standardize order, shipping, and invoice documents to be fully machine-readable end-to-end [6] .

-

Real-Time Accounting and Compliance: The data flows established could evolve into near real-time tax reporting. While current law still treats reports as periodic (albeit very timely), future iterations might require “continuous transaction control” where each invoice line is validated against tax rules via secure channels. This model exists in Latin America (Mexico’s Comprobante Fiscal Digital por Internet, CFDi requires each invoice to be authorized by the tax authority on submission). If economic conditions or technological readiness push in that direction, companies may need to adapt again (though with this initial system in place, the hurdle will be lower).

-

AI and Data Analytics: Once invoices are standardized, big data techniques can be applied. Fraud detection algorithms could scan aggregate invoicing patterns across industries; businesses might use predictive analytics on payables/receivables. Over time, ERP systems could suggest optimal payment schedules or early payment discounts based on invoice history. Some platforms note that hybrid PDF+XML formats will simplify the creation of machine-readable archives for future business intelligence.

-

Cross-Border Convergence: As PEPPOL grows, a French company can send e-invoices directly to partners in other countries and vice versa. The European Commission has set a timeline for wider e-invoicing adoption (All EU businesses by 2028). France’s infrastructure choices (EN16931, Peppol) are aligned with this vision. One might foresee an EU-wide directory of business IDs (building on the SIRET system) to help routing. Also, the Digital Services Act and eIDAS reforms might further integrate identity/trust services with transactional data (e.g. requiring digital signatures on certain cross-border invoices).

-

Small Business Transition: The government may consider extending requirements gradually to those not initially in scope (e.g. self-employed without VAT obligations, or additional B2B segments). Also, consumer invoices remain a “reporting” obligation today, but in future could become B2C e-invoices if digital receipts for consumers become feasible. The ongoing introduction of digital data hubs (as with e-Reporting) could lead to new compliance steps.

-

Tax Auditing and e-Reporting Enhancements: The current mandate focuses on invoices; but e-signals from this system could feed into broader tax compliance (e.g. VAT prepayments, integrated mid-year checks). Tax authorities might eventually move from just collecting invoice summaries to full e-auditing: taxpayers upload their entire set of transactions periodically (France’s FEC filing might be superseded by continuous reporting). This could streamline or even automate certain parts of the tax return.

-

Innovation Pressure: Finally, the mandate creates a market pull for innovation. Early entrants are likely to offer “value-added” services: combining e-invoicing with e-procurement, or linking invoices to blockchain-based payment networks. French fintech startups, many of which have already been integrating with PSG installment schemes and mobile payments, may invest in complementary compliance tools. This could lower the cost and complexity for SMEs in the long run.

In conclusion, France’s e-invoicing mandate is a significant step toward a future of fully digital commerce. The immediate impact (mandatory 2026/2027 compliance) is just the beginning. Over the next decade, we foresee companies leveraging the new data flows for process optimization, and possibly preparing for even more real-time, automated tax regimes. From a strategic viewpoint, firms that proactively modernize their invoicing and reporting infrastructures will be better positioned to adapt to these changes and compete in an increasingly digital European economy.

Conclusion

France’s September 2026 e-invoicing mandate represents a deep transformation of the country’s B2B billing system. It compels all VAT-registered companies to adopt structured electronic invoices (Factur-X, UBL, or CII) and to use certified platforms for exchange. While implementation is challenging – involving new technical processes, data cleanup, and staff training – the benefits are substantial. Automated invoicing can reduce manual effort and errors, improve payment cycles, and provide management with richer financial data. The law also offers the public sector unprecedented visibility into the economy’s transactions, aiding tax collection and fraud detection.

For Oracle NetSuite users, readiness means installing a compliant e-invoicing solution. This may involve deploying a SuiteApp connector and choosing a partner PDP. As this report detailed, systems like Novutech’s Invopop integration or Avalara’s platform provide the necessary technical functionality: they enrich customer data with SIREN/VAT IDs, generate Factur-X/UBL files, route messages via PEPPOL, and track statuses. By working through a connector’s outbound waves and inbound draft bills (as outlined) and by following official schedules, businesses can align with the mandate while maintaining continuity.

It is imperative that companies act now. The timelines (Sept 2026 and 2027) allow limited runway, and hefty fines loom for non-compliance [7] [18]. Early adopters will have the advantage of ironing out problems before the deadlines, whereas procrastinators risk operational headaches and penalties. Government resources and third-party experts are available to assist; invoice automation is the new norm, and firms should seize the opportunity to integrate it smoothly.

Looking forward, this shift is part of a broader European digital evolution. France’s move is in line with EU-wide standards and is expected to facilitate commerce across borders. Over time, the data networks and practices established may lead to even more sophisticated fiscal systems. For now, mastering the new e-invoicing requirements – especially via the selected PDP and generating compliant Factur-X invoices – is the immediate task for businesses. This report has aimed to provide a comprehensive roadmap through that task, from legal background to technical execution, backed by authoritative sources and real-world examples.

Sources: All claims and data above come from official French government publications (DGFiP, economie.gouv.fr) and industry analyses, including Times szakav et al. (public news, webinars, vendor docs). Key citations include the DGFiP FAQ on the e-invoicing reform [1] [2], the Ministry’s deployment announcement [16] [26], industry guides (Novutech [13] [28], Odoo [12] [40], Quadient [6]), and news coverage on sanctions [7] [18]. Historical context draws on EU directives and comparable national cases (Source: www.ipresslive.it) [4]. All references are cited inline by source and line number as shown.

External Sources (51)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.