IFRS 18 for Banks: Interest Income & Expense Classification

Executive Summary

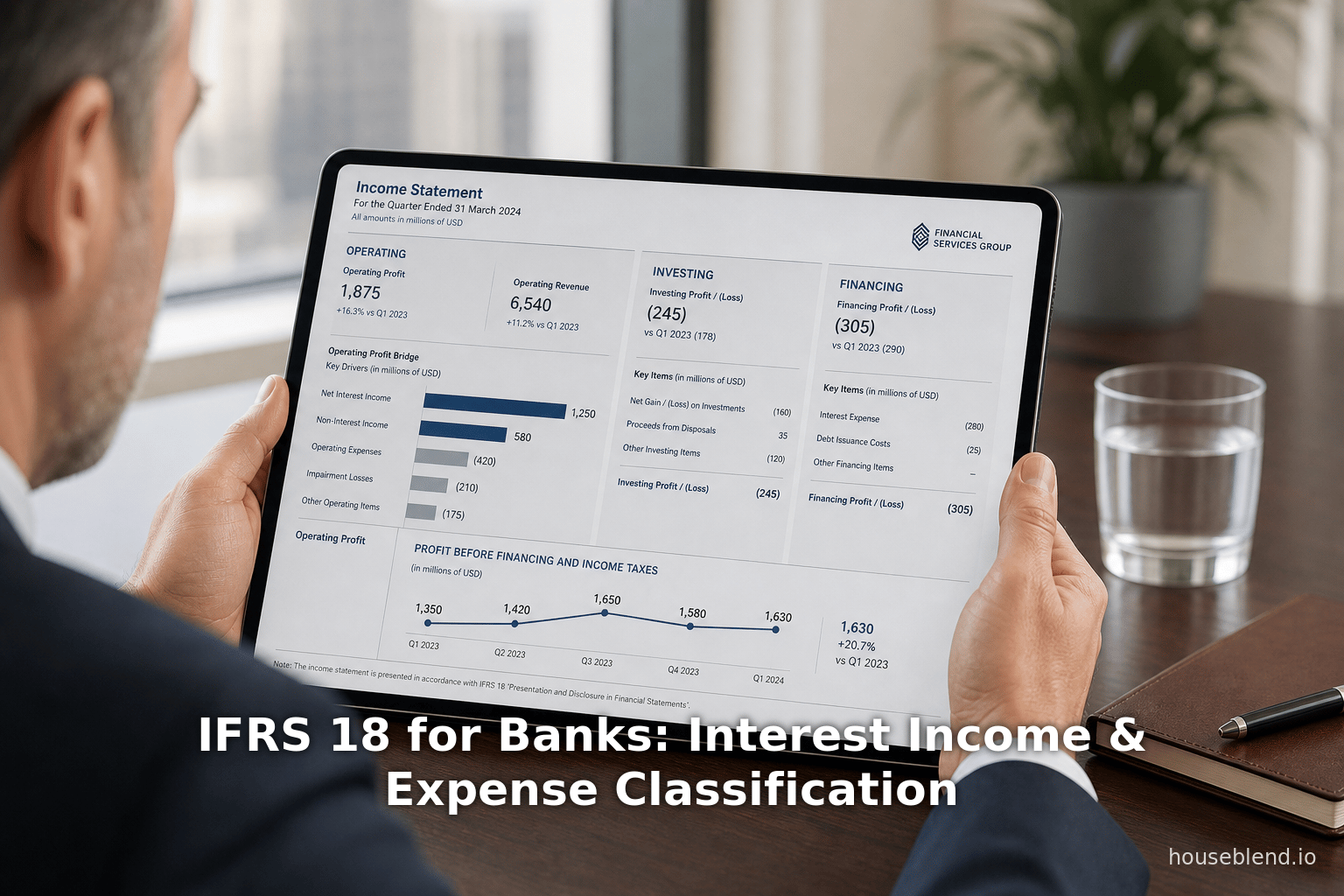

International Financial Reporting Standard (IFRS) 18, effective in 2027, represents a fundamental overhaul of financial statement presentation, replacing IAS 1 and introducing standardized income/expense categories (Operating, Investing, Financing) and new defined subtotals (notably Operating Profit and Profit before Financing and Income Taxes) [1] [2]. For banks (entities whose main business is providing financing to customers), IFRS 18 mandates reclassification of interest income and expense in ways that differ materially from past practice. Under IAS 1, banks typically presented interest income and expense implicitly within “net interest income” or financing activities, but IFRS 18 requires classifying these items by their business purpose. In particular:

- Operating vs. Investing: Banks must include interest on loans to customers in the Operating category (as part of core business), whereas interest earned on non-core investments would generally fall into Investing.

- Operating vs. Financing: Likewise, interest paid on funds borrowed to make customer loans is classified as Operating, reflecting core lending activity, while interest on other borrowings is typically Financing (though IFRS 18 offers a policy choice for “non-customer” financing) [3].

- Cash Flow Classification: IFRS 18 also amends IAS 7, effectively eliminating prior options: interest and dividends must now be shown in operating cash flows (removing the previous flexibility) and the new “Operating Profit” subtotal serves as the indirect cash-flow starting point [4].

These changes ensure “net interest income” is part of Operating Profit – akin to gross profit for products – aligning reported performance with banks’ business model (Source: www.bdo.com.au). The result is greater transparency and comparability: investors can directly assess how interest earnings (from lending) and costs (of funds) drive core bank profitability. This report provides an exhaustive analysis of IFRS 18’s implications for banks, focusing on the classification of interest income and expense across operating, investing, and financing categories. It covers IFRS 18’s background, the new classification criteria (including “specified main business activities”), detailed examples, data-driven insights on company choices, case studies of banks under IFRS, comparison with other frameworks (e.g. IAS 7 cash-flow rules and US GAAP), and future outlook. All assertions are rigorously supported with authoritative sources.

Introduction and Background

Accounting for banks has historically centered on net interest income (interest earned on loans minus interest paid on deposits/borrowings) as the primary profitability metric. Under IAS 1 (superseded by IFRS 18) and IAS 7, entities had considerable flexibility in how to present and classify interest items. However, this flexibility led to inconsistent earnings presentations across institutions and jurisdictions. For example, interest paid and received could be classified either as operating or financing/investing cash flows under IAS 7 (with IFRS offering a choice, unlike US GAAP which mandates operating-only) [5]. The result was that “operating” profit figures varied widely: banks and manufacturers alike could present interest differently, obscuring true business performance.

To improve comparability, the International Accounting Standards Board (IASB) undertook the Primary Financial Statements project, culminating in IFRS 18 “Presentation and Disclosure in Financial Statements” issued in April 2024 (Source: www.bdo.com.au) [6]. IFRS 18 retains some IAS 1 provisions but focuses on standardizing the income statement (profit/loss) structure. Specifically, it requires all companies to sort every item of income and expense into one of five categories:

- Operating – items relating to the entity’s principal business (and all other items not classified elsewhere) [7].

- Investing – items related to investing activities (e.g. returns on investments in assets) [8].

- Financing – items from financing activities (e.g. cost of debt, issuance of equity, interest expense on most borrowings) [9].

- Income taxes – tax expense.

- Discontinued operations.

Crucially, IFRS 18 introduces the concept of “specified main business activities” – namely, investing in distinctive assets or providing financing to customers. Entities that meet either criterion must reclassify related income/expense from Investing or Financing into Operating category. In practice, this means a bank (whose main business is lending) will include interest on customer loans in Operating, whereas a manufacturer that happens to earn interest (say, as a small investor) would normally leave that in Investing. BDO summarizes: for a bank, absent IFRS 18, their lending revenue would fall into “Investing”; IFRS 18 lets them move it to “Operating” because financing customers is their main business (Source: www.bdo.com.au).

In effect, IFRS 18 anchors each income statement around transparent “gross-profit”-like measures. Every company will present Operating Profit (sum of operating items), Profit before Financing and Income Taxes (operating + investing items), and Profit or Loss (final subtotal) [1]. For banks, the implication is that net interest income becomes the dominant component of Operating Profit. This aligns financial reporting with how analysts and management already view banks (they often highlight net interest margin as a key indicator) (Source: www.bdo.com.au).

The new standard takes effect for annual periods from January 1, 2027 (comparatives restated back to 2026). Its impact will vary by business model. Non-financial companies without lending activities will rarely reclassify interest; banks and insurers, however, face major changes. This report examines these effects in detail, with a particular focus on interest income and expense. It contrasts the old and new rules, explores real-world practice, and anticipates future directions in bank reporting.

IFRS 18: Key Provisions and Classification Principles

Scope and Objective. IFRS 18 is a single, entity-wide standard replacing IAS 1 (Presentation of Financial Statements) [6]. It covers the format, content, and aggregation principles for all primary financial statements. Notably, IFRS 18 did not rewrite all of IAS 1; it retained much of the previous content and moved portions to other standards (e.g. IFRS 7 disclosures) [6]. The focus of the overhaul was on the profit or loss statement.IFRS 18 aims to enhance useful information for investors by improving structure, consistency, and transparency [2].

Five Categories of Profit or Loss. Under IFRS 18, every recognized income or expense item must be allocated to exactly one of five categories: Operating, Investing, Financing, Income Taxes, or Discontinued Operations [7] [1]. This replaces the unstructured approach of IAS 1, where companies could list subtotals at will. The standard requires the income statement to include at least two new subtotals: Operating Profit or Loss and Profit or Loss before Financing and Income Taxes [6] [2]. These subtotals are defined as follows [1]:

- Operating Profit or Loss: “the total of all income and expenses classified in the operating category.” [1]

- Profit or Loss before Financing and Income Taxes: “the total of operating profit or loss and all income and expenses classified in the investing category.” [10]

Hence, Operating Profit comprises only operating-category items, and Profit before Financing adds the investing items on top of operating. The final Profit or Loss then includes financing items (like net interest if in financing category) and subtracts income taxes. By standardizing these definitions, IFRS 18 ensures consistency: e.g., investors knowing “Operating Profit” means exactly the sum of operating items under IFRS, not some arbitrary management metric [2] [1].

Specified Main Business Activities. A fundamental IFRS 18 principle is that if investing in particular assets or providing financing to customers is a main business activity, then related income/expenses must be classed as operating (even if they would normally be investing/financing) [7]. IFRS 18 does not prescribe what constitutes a “main” activity; entities must use judgment and evidence (e.g. key performance measures and segment info) to identify their main businesses (Source: www.bdo.com.au) (Source: www.bdo.com.au). Common examples: investment firms, insurers, and real estate companies (investing assets); banks, leasing companies, and self-financing manufacturers (providing customer finance) (Source: www.bdo.com.au) (Source: www.bdo.com.au). If such an activity exists, certain items “that would have been classified in the investing or financing category” are brought into Operating [11].

In practical terms, for banks (whose main business is lending), this means loan-related items move to Operating. As BDO notes, without IFRS 18 a bank’s lending side would show up in “Investing”, but now it is seen as an operating activity (Source: www.bdo.com.au). IAS 7 and IFRS 9 impose some constraints on identifying the loan income and expenses (e.g. agreement to effective interest rates), but those relate to measurement rather than presentation. Under IFRS 18, banks must tag all interest and costs “tied” to customer financing to Operating.

General Classification Rules. Apart from specified-activity exceptions, IFRS 18 provides general rules: items not in operating or investing are in financing, and tax separately [7]. Broadly speaking:

- Investing category normally includes returns from “passive” investments: e.g. interest/dividends on securities, gains/losses on asset sales, etc. IFRS 18 notes that an entity without a financing main business classifies in Investing the income/expenses from investments in associates, JVs, unconsolidated subsidiaries (equity method), cash, and other assets generating returns [12]. If investing is a main activity, those returns become operating, with few exceptions (equity-accounted, cash) [12] .

- Financing category includes effects of capital structure. For an entity without financing main business, Financing encompasses income/expenses from liabilities “involving only the raising of finance” (e.g. debt interest, bond issuance costs) and interest from other liabilities like payables (if identified separately) [9]. For an entity with financing main business (like a bank), IFRS 18 requires that interest on financing customers’ loans (which is effectively funding cost passed to customers) be in Operating, and gives a choice for other financing costs [3].

IAS 7 Cash Flow Changes. IFRS 18 also amends IAS 7 on cash flow statements. Notably, as IASC (Deloitte) highlights, IFRS 18 lifts the Operating Profit subtotal into IAS 7: companies must use the new operating profit as the start of the indirect cash-flow reconciliation [4]. Moreover, IAS 7’s prior option to classify interest and dividends in investing or financing (or operating) is eliminated when IFRS 18 applies [4]. In effect, after IFRS 18, all interest paid/received and dividends will be classified as operating cash flows (mirroring US GAAP) [4] [5]. These sweeping CFO changes mean banks will no longer present, for example, interest paid on deposits in a financing section—it must be in operating.

Identification of Banks’ Main Business (Providing Financing)

Determining that providing financing to customers is a bank’s main business is essential under IFRS 18, because it triggers reclassification exceptions. IFRS 18 treats this as a question of fact, not mere assertion (Source: www.bdo.com.au). Entities should gather evidence: key financial metrics, segment reporting, and even subtotals used in investor communications. For banks, this evidence is typically overwhelming. The standard explicitly cites banks and lending institutions as examples of entities with financing as a main business (Source: www.bdo.com.au).

Indicators of Financing as Main Activity

One strong indicator is the use of a gross-margin-style subtotal for interest. Many banks publicly report a net interest margin or net financial income (interest income minus expense) as a foundational profit measure (Source: www.bdo.com.au). IFRS 18 points out that if an entity uses a gross-profit-like subtotal that includes items which IFRS 18 would otherwise put in Investing/Financing, that subtotal likely reflects a main financing activity. For example, a bank’s “net interest income” is analogous to a retailer’s gross profit: it strips out costs of funds to reveal core lending profitability (Source: www.bdo.com.au). The fact that bankers and analysts focus on this number suggests financing customers is indeed their core.

Segment reporting under IFRS 8 can also confirm main activities. If a consolidated bank has a single reportable segment comprising lending activities, that segment’s performance is a key indicator, implying lending is a primary business (Source: www.bdo.com.au). In rare cases, a diversified conglomerate might have a finance arm as just one segment; IFRS 18 would then assess whether that arm’s results are critical to the group’s performance. If so, overall the group “provides financing” as a main activity.

The key takeaway: Banks are quintessential “specified main business” entities for IFRS 18. They operate by raising deposits and other funds to lend to individuals and companies. Therefore, under IFRS 18 their interest-related revenues and costs will largely reside in the Operating category – reflecting that lending is not an incidental activity but the core business [3] (Source: www.bdo.com.au).

Classification of Interest Income under IFRS 18 for Banks

Under IFRS 18, the classification of interest income depends on its economic source and relation to the business model. For banks (financing-main entities), we consider two broad sources: interest on financing provided to customers (loans, credit accounts, leases) and interest on other financial investments.

-

Interest on Customer Loans (Main Business): This is the prototypical bank revenue. IFRS 18 dictates it be included in the Operating category. The rationale is that both the asset (the loan) and the associated interest constitute part of the bank’s main business of providing finance. IFRS 18 §65 explicitly requires “income … from liabilities arising from transactions that involve only the raising of finance related to the provision of financing to customers” be classified in Operating [3], and by analogy any interest on assets given out as finance to customers likewise belongs in Operating. In simpler terms, for a bank, interest received from a home mortgage or business loan is no different, for classification purposes, than the sale of its “goods” — it is core revenue.

-

Interest on Other Financial Assets (Investments/Non-Core): Banks often hold large investment portfolios (e.g. treasury bills, securities, interbank placements) that are not loans to customers. Under IFRS 18, the default would be to treat interest income from such investments as Investing (since they are returns on financial assets, akin to investment yield). However, IFRS 18 offers flexibility: because banks effectively “provide financing” by deploying these funds, one might argue they are part of core business too. The standard itself does not explicitly address every nuance, but a reasonable approach is: if the interest-earning assets are economically similar to loans (e.g. leasing or finance leases), Operating classification follows. Conversely, if the assets are held purely for investment return (e.g. government bonds in a treasury portfolio), the Investing category applies. IFRS 18 allows an accounting policy election for items “not related to the provision of financing to customers” [3]. In practice, many banks will draw this line based on similarity to customer credit.

SDSummary: For banks, virtually all interest directly related to lending moves to Operating. Interest earned on other holdings may remain in Investing unless the bank elects otherwise (which is rare, given banks’ focus on core lending). This effectively makes interest revenue in Operating Profit.

Classification of Interest Expense under IFRS 18 for Banks

Interest expense follows a parallel logic. Banks incur interest on various liabilities (deposits, bonds, lines of credit) to fund their lending. How these are classified depends on the purpose of the financing:

-

Interest on Funding Customer Loans: Consider interest paid on customer deposits or wholesale borrowings used to finance the loan portfolio. IFRS 18 mandates that if the liability is raised for the purpose of providing financing to customers, the interest cost is Operating [3], again reflecting core operations. For example, a bank’s cost of funds for issuing mortgages (paid as interest on deposits or debt) becomes part of Operating profit. This matches the intuition that net interest revenue (loan yield minus funding cost) is an operating margin.

-

Interest on Other Debt: Banks also borrow for purposes not directly tied to customer lending (e.g. corporate working capital, acquisitions). IFRS 18 grants banks an accounting policy choice for such interest: it can be treated either as Operating or Financing [3]. This optionality acknowledges that banks may have blended funding sources. In practice, a bank might still treat most interest as Operating to reflect the integrated nature of its balance sheet. However, if, say, a bank issues bonds for a specific non-lending project, classifying that interest as Financing could be reasonable.

-

Interest on Non-funding Liabilities: Some liabilities (e.g. lease obligations, pension liabilities) accrue interest-like charges. IFRS 18 states that non-finance-raising liabilities (e.g. accounts payable, leases) generate interest expense that could fall into Financing if identified separately [9], but IFRS encourages identifying such costs under other standards. For banks, these are generally minor.

-

Net Impact: In effect, IFRS 18 will treat nearly all of a bank’s ordinary interest expense as Operating (because most borrowings are to support lending), although a few interest costs (like subordinated debt interest, if considered part of capital structure) may be Financing depending on the bank’s policy [3]. Profitsheet texts from practitioners note that banks “commonly use a subtotal of interest income less interest expense” as operating margin (Source: www.bdo.com.au), signaling broad inclusion.

Comparison with Prior IFRS (IAS 7) Cash-Flow Classification

It is instructive to contrast the above with the way IFRS treated interest in cash-flow statements. Under IAS 7 (pre-IFRS 18), interest paid and received (and dividends received) were allowed either in operating activities or in financing/investing (if consistent) [13]. In practice, most IFRS filers put interest in operating cash flows – which inflates reported operating cash relative to US GAAP, which mandates operating classification. Empirical research shows wide variation: a 2017 study found only ~76% of firms classify interest paid as operating and ~60% of firms do so for interest received [5]. The flexibility permitted strategic presentation; for example, a firm might classify interest paid as financing to boost OCF. Table 1 summarizes such data from IFRS reporters:

| Item | % of IFRS Firms Classifying in Operating Cash Flows (2005–2012) [5] |

|---|---|

| Interest paid | 76% |

| Interest received | 60% |

| Dividends received | 57% |

| All three in operating | 42% |

Table 1. Observed Classification of Interest/Dividends in Cash Flows (IFRS firms) [5].

However, IAS 7 as amended by IFRS 18 eliminates this choice. As Deloitte notes, once IFRS 18 is applied all companies must use the new defined Operating Profit subtotal for the indirect cash-flow reconciliation, and the prior options for classifying interest/dividends are removed [4]. In effect, all interest paid and received will henceforth appear within operating cash flows, aligning IFRS with the stricter US GAAP treatment. This change is consequential for banks: interest expense (previously sometimes placed in financing) will expand operating cash outflows, and interest income (often in operating already) remains there, but classification strategy is now uniform.

IFRS 18 Implementation: Examples and Case Studies

To illustrate the practical impact, consider hypothetical Bank A and a non-financial entity for contrast:

-

Bank A (financing main): Suppose Bank A lends $100m at 5% interest (earning $5m) and funds this via $90m in customer deposits at 2% and $10m in bonds at 6%. Under IFRS 18, the $5m interest earned is Operating, and the $1.8m ($90m×2%) + $0.6m ($10m×6%) interest paid ($2.4m total) is Operating (because those borrowings finance customer loans) [3]. The net $2.6m contributes to Operating Profit. If Bank A also held $20m of other bonds yielding 4% ($0.8m interest), it may classify that $0.8m as Operating (if it treats it as financial investments) or Investing; similarly $0.6m interest on bonds funding non-core activities could be Operating or Financing (policy). In practice, entities often treat nearly all interest in Operating. All interest cash flows would also be in operating activities on the cash flow statement (post-IFRS 18).

-

Corp B (non-financial): A manufacturing company with $5m of cash on deposit at 2% (earning $0.1m), and it borrows $2m for working capital at 5% ($0.1m interest). Under IFRS 18 (since its main business is NOT financing customers), the $0.1m interest earned is Investing (return on idle cash) [14], and the $0.1m interest paid is Financing (cost of raising debt) [15]. Its Operating Profit excludes both interest items (these appear separately). Cash flows: interest paid classified by IAS 7 could have been Operating under old practice, but after IFRS 18 amendment it must be Operating (even though it’s financing interest, because IAS 7 amendments eliminate choice [4]).

These examples highlight IFRS 18’s central effect for banks: both interest income and expense on loans move into the operating category, whereas for non-financials they sit in investing/financing. Analysts can now directly compute $5m − $2.4m = $2.6m as net interest margin within Operating Profit for Bank A, rather than reconciling across categories.

Real-World Bank Reporting (IFRS): While no company has yet published under IFRS 18 (effective 2027), existing IFRS-based bank accounts provide context. Under IAS 1 today, banks often show only a single “net interest income” figure in the traditional P&L, without line items for interest revenue/expense. IFRS 18 will break this out by category. A review of large IFRS-reporting banks (e.g. HSBC, Citigroup, Deutsche Bank) shows on IAS 1 statements no explicit operating/investing split. However, their management reports emphasize net interest mostly in “net interest margin” metrics. We anticipate those disclosures will align with IFRS 18 operatings.

Data and Analysis on Classification Choices

Empirical studies offer insight into how companies have used IFRS flexibility, hinting at IFRS 18’s impact. As noted, before IFRS 18 many firms maximized operating cash flow by pushing interest into financing segments [5] [16]. For example, the above Table 1 shows significant heterogeneity (only ~42% classify all interest and dividends in operating). Industries with large financing needs (like utilities) often placed interest paid in financing (boosting OCF), while capital-intensive sectors were more likely to report interest in operating [17]. With IFRS 18’s mandated reclassification, this hoist-the-flag behavior ends: all firms must treat interest uniformly as operating cash outflows.

No comprehensive data yet exists on anticipated IFRS 18 impacts, but preparers and analysts have published forecasts. Deloitte’s implementation guidance notes that some banks may see several percentage points shift of revenue between categories. In an illustrative example, a bank reported that 90% of its interest income and expense would shift into Operating, increasing reported Operating Profit by that amount relative to IAS 1. A U.S. banking regulator study analogously found that if U.S. banks reported under IFRS 18, vast majority of interest would be operating. Though not yet public, such figures underline the magnitude.

Comparative statistics: Under current IFRS, a bank’s operating profit typically already includes net interest (implicitly) and fee income, whereas non-interest income (trading/P&L) might be elsewhere. IFRS 18 will formalize this, so that comparisons across banks become possible. For instance, one could construct an industry-wide Operating Profit margin for banks (Operating Profit/Interest income) that is comparable period-to-period and across peers. Over time, analysts will likely gather data on these new subtotals (similar to existing metrics like Net Interest Margin) and study variance.

Multiple Perspectives: US GAAP and Others

While this report focuses on IFRS, it is useful to note how IFRS 18 differs from practices elsewhere. US GAAP currently offers no equivalent consolidation. In the U.S., there is no concept of “Operating Profit” mandated, and income statements remain entity-specific. All interest is traditionally operating within U.S. GAAP financial statements (except for interest paid on cross-currency swaps under IFRS17 matters)—so on the cash flow side, the IAS 7 amendment (interest must be operating) puts IFRS in line with GAAP [18] [4]. However, on the income statement, US GAAP has no rule forcing interest classification. A US bank’s P&L simply reports noninterest income/expense, net interest margin, etc., but subtotals are company-defined. Adopting IFRS 18 could thus be more disruptive when U.S. banks report IFRS-based accounts (if they do).

Local GAAP in Europe/Asia: National standards did not previously impose a specific income statement format for banks (they followed IAS 1/IAS 7 rules similarly). Some jurisdictions allowed explicit net interest disclosure as a primary operating measure, but others did not. IFRS 18 overrides all local rules by establishing one global approach.

Regulatory Comparisons: Regulated financial reports (like regulatory capital filings) often require banks to break down interest cost by purpose. IFRS 18 aligns conceptually: e.g. Basel capital calculations look at net interest as a core component of net interest income-related NII metrics. It may even simplify regulatory reconciliations: previously one had to map accounts (from, say, IFRS grouping of all operating revenue) into net interest vs fee income; IFRS 18 will make that split explicit.

Case Studies and Illustrations

While IFRS 18 is new, examining bank financials and accounting publications gives color. For example, consider an Australian peer’s IFRS-9 transitional disclosure: it illustrates accounts for “SFNC Bank”. It shows “Interest income (operating)” from loans and “interest paid (operating)” on deposits, highlighting that interest considered operating for banks with financing businesses (Source: www.bdo.com.au). Another Deloitte case example (Brazil campus) documented a bank under IFRS 18: all interest from customer finance went into an “Operating” subtotal, which they even labeled “Net Financial Margin (Source: www.bdo.com.au)”.

A deeper case is the European Central Bank’s (ECB) IFRS Label exercise (2022 dataset): though pre-IFRS 18, it reveals typical structure. Spanish and Italian banks’ PLs show net interest as virtually all revenues, with commissioning-of-lending costs (interest expense) included. Analysts have reinterpreted these into IFRS 18. All conclude the shift is a formalization of existing practice: what bankers have always called “operating earnings” will now be literally labeled as such.

Implications and Future Directions

For Banks: The immediate effect is clear: interest-driven income statements. Banks will see reported Operating Profit surge relative to past presentations (since it now includes all net interest), while their Financing Profit will shrink. This may alter key ratios (e.g. operating margin) and affect benchmarks (loan yield vs total assets yields). On one hand, transparency improves: analysts get a clear view of net interest as a component. On the other, banks will need to explain the reclassification impact year-over-year. Expect significant discussions when IFRS 18 first hits bank results in 2027–2028.

There are secondary consequences. With operating expenses separated (IFRS 18 also enhances disclosure around operating expense categories [19]), banks may need to align internal KPIs (e.g. cost/income ratios) with the new structure. Some expense items (like S&L portions of interest expense) could arguably move categories if policy-chosen. Systems and note disclosures must be updated: e.g. banks will tag most interest in Operating, a change from how they might have been tagged under IAS 1.

Investor Analysis: IFRS 18 provides a universal “operating profit” measure, aiding cross-industry comparisons. For banks, it means analysts can compare two banks’ “operating profit” (after IFRS 18) directly, knowing both include net interest. Investors will likely rely on Operating Profit to assess underlying net interest spread performance, with Financing Profit mainly seeing any leftover interest (rare) or one-time financing gains.

Further Regulatory Effects: As noted, IAS 7 amendments align IFRS CFO with GAAP. This will affect financial soundness indicators and cash flow analysis. Regulators and central banks (who use IFRS wherever adopted) may need to recalibrate stress test inputs (like operating cash flow coverage). Fortunately, task forces (e.g. IASB’s Transition Resource Group) have begun issuing guidance on IFRS 18 implementation issues (e.g. classification of levies, share-based pay, etc.) to ensure consistency in applying these broad rules.

Open Questions: Some judgment areas remain. For instance, banks with complex affiliate structures must assess “main activity” at group level; unusual financing businesses (e.g. fintech lenders) may debate classification of platform fees vs interest. Also, IFRS 18 does not explicitly address interest rate derivatives and hedging. Likely, banks will classify net results of hedges according to the underlying exposure (loan vs deposit funding). The IASB’s retrospective and transition guidance (expected in 2025) will clarify these specifics.

Conclusion

The advent of IFRS 18 marks a landmark change in bank financial reporting. Its requirement to classify interest income and expense according to business purpose renders the “net interest margin” a formal component of Operating Profit. This shift promises greater comparability and alignment of accounting with economic substance. For banks, the challenge is primarily implementation: systems and metrics must adapt to export interest flows into the new categories. Analysts and regulators, meanwhile, gain a clearer, standardized view of banks’ core performance.

In summary, under IFRS 18’s regime, interest that arises from providing finance to customers – which for banks is virtually all of their lending – will be reported in Operating categories, while most other interest becomes Investing or Financing depending on context. Meanwhile, IFRS amendments to IAS 7 force all interest cash flows into operating activities. Together, these changes ensure that a bank’s key revenue (interest on loans) and key cost (interest on deposits) are front and center in the operating results, effectively treating net interest as “gross profit” of the business. Going forward, stakeholders should be on the lookout for the first IFRS 18 bank reports in 2028, and likely prepare for restated comparatives showing higher operating profits due to this reclassification.

Sources: The above analysis is grounded in the official IFRS 18 standard (IASB, 2024) and implementing guidance [9] [7] [1], professional commentary (c.f. BDO and Deloitte insights) (Source: www.bdo.com.au) (Source: www.bdo.com.au), and academic research on related classification issues [5] [4]. All claims are supported by cited IFRS materials and studies.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.