Houseblend Article

IFRS 18 Implementation Roadmap: 12-Month CFO Guide

Inside this article

Executive Summary

IFRS 18 “Presentation and Disclosure in Financial Statements”, issued by the IASB in April 2024, marks the most significant overhaul of financial statement presentation since the introduction of IFRS (originally IAS 1) over 20 years ago [1] [2]. Effective for annual periods beginning 1 January 2027 (early application permitted) [2], IFRS 18 fundamentally restructures the statement of profit or loss and related disclosures to enhance comparability and transparency. It mandates two new subtotals – “Operating profit (or loss)” and “Profit (or loss) before financing and income tax” – and requires companies to classify all income and expenses into defined categories (Operating, Investing, Financing, Income Taxes, and Discontinued) [3] [4]. Importantly, IFRS 18 also compels disclosure of management-defined performance measures (MDPMs) (often known as Alternative Performance Measures) in the financial statements, with clear reconciliations to IFRS measures [5] [3].

For a mid-market CFO, these changes will affect nearly every aspect of financial reporting – from chart of accounts and accounting policies to budgeting, covenants, and external communications. The “CFO Playbook” presented here outlines a 12-month roadmap to full compliance, beginning with immediate impact analysis and project planning, and carrying through system updates, training, and phased implementation. Key steps include: designating a project leader and cross-functional team; performing a gap analysis of existing statements; redefining financial KPIs (e.g. EBITDA, EBIT) in line with IFRS 18 categories; updating accounting and ERP systems; drafting the revised primary statements; and rolling out new disclosure templates (including MDPM notes and reconciliations) [6] [5].

Throughout, the CFO must engage stakeholders – finance staff, audit committee, board, investors and lenders – to explain the new structure and terminology [7] [8]. Extensive preparation is critical: regulatory guidance notes that interim reports prepared after IFRS 18’s effective date must already adopt the new headings and subtotals [9], and good practice dictates completing most preparatory work well before mandatory application [10]. In summary, IFRS 18 is not a cosmetic change but a transformational shift in financial reporting. A deliberate, well-resourced 12‐month implementation plan will help a mid-market company’s CFO turn compliance into an opportunity to strengthen financial controls, improve external communications and ultimately support better decision-making by investors and managers alike [11] [12].

Introduction and Background

International Financial Reporting Standards (IFRS) were established to harmonize financial reporting globally, improving comparability across companies and jurisdictions. To date, over 140 jurisdictions (including the EU, Japan, Australia, and many others) mandate or permit IFRS for publicly accountable entities [3] [13]. Amid ongoing evolution, the IASB has periodically updated IFRS. For example, IAS 1 Presentation of Financial Statements has been amended multiple times since its 1975 inception, most recently through the Disclosure Initiative (2014) and Classification of Liabilities (2021) projects [14] . IFRS 18 is the latest outcome of this evolution. Officially titled “Presentation and Disclosure in Financial Statements”, IFRS 18 replaces IAS 1 and packs several previously scattered amendments into a unified standard [15] [16].

The IASB explicitly designed IFRS 18 to address long-standing investor and preparer concerns over the comparability and clarity of financial statements [1] [3]. Investors have noted that companies often present their income statements variably, using differing subtotals and aggregation approaches that make cross-company analysis difficult [8] [1]. IFRS 18 introduces defined categories and subtotals precisely to solve this problem.Rather than leaving subtotals (like “operating profit”) up to arbitrary choice, the new standard mandates two defined subtotals (Operating profit and Profit before financing and taxes) and categorizes every line item into one of five sections [17] [3]. As one analysis notes, IFRS 18 “ushers in the most significant change to the statement of profit or loss since IFRS Accounting Standards were introduced” [1], highlighting its scope and ambition. Furthermore, the IASB added strict rules on aggregation and disaggregation, requiring companies to present information in a structured way and discouraging one-off line items or overly broad grouping [15] [18].

A second major element of IFRS 18 is addressing the use of non-IFRS performance metrics by management. Companies often communicate supplemental metrics (e.g. EBITDA, adjusted EPS, etc.) to investors, but without IFRS oversight these could be inconsistent or opaque. IFRS 18 requires all material management-defined performance measures (MDPMs) that appear in public communications to be disclosed in the financial statements, along with purposes, calculations, and reconciliations to the nearest IFRS subtotal [5] [3]. In effect, IFRS 18 brings alternative performance measures (“APMs”) under the audit trail. As the ICAEW explains, these disclosures will “help companies better communicate their financial performance, in turn helping investors make better decisions” [11]. Preparers have actually welcomed this, noting that it validates their use of customized metrics while imposing needed transparency and discipline [19].

IFRS 18’s scope also extends beyond the income statement. It subsumes several pending amendments to IAS 1 and IAS 7. For example, under the new standard goodwill must be presented on the face of the statement of financial position (rather than buried in intangible assets) [20]. The IASB concurrently updated IAS 7 (Cash Flow Statements) so that indirect cash flow statements start with IFRS 18’s operating profit subtotal [21], and removed optionality for interest and dividend classification (dividends paid are now always financing, etc.) [22]. In addition, interim financial reports issued after adoption must adopt IFRS 18 formats (including the new headings/subtotals and MDPM disclosures) to ensure investors see a consistent structure throughout the year [9].

For mid-market companies, which may have more limited resources than large multinationals, these sweeping changes present a significant challenge. Systems, processes and budgeting models designed around the old IAS 1 presentation will have to be revamped. The financial close process will require new controls and checklists. Financial analysts and investors will need education on the meaning of “operating profit” under IFRS 18 versus any legacy measures. On the other hand, IFRS 18 can be seen as an opportunity to sharpen internal reporting and disclosure – aligning mid-market companies’ reports with investor expectations of consistency. In any case, early planning and a disciplined implementation approach are essential to meet the January 2027 deadline [23] [24].

Key Provisions of IFRS 18 and Their Effects

Statement of Profit or Loss: Categories and Subtotals

IFRS 18 restructures the income statement into five categories and mandates new subtotals. All income and expenses must be classified into one of: Operating, Investing, Financing, Income Taxes, or Discontinued Operations [3]. This classification must be based on an entity’s main business activities (or its closest analog for investing companies) [4] [25]. For example, KPMG notes that a manufacturing firm might assign its core revenues and costs (from operations) to the Operating category, equity-method income from affiliates to Investing, and interest expense to Financing [26] [4].

Within each category, IFRS 18 requires defined subtotals. Most notably, the standard introduces "Operating profit or loss" (the total of Operating category amounts) and "Profit or loss before financing and income taxes" (Operating profit plus Investing category profit, or equivalently Operating profit plus loss) [3] [17]. These two subtotals were not explicitly required by IAS 1. By standardizing them, IFRS 18 ensures every company reports, for example, an Operating profit figure on the face of the P&L, facilitating like-for-like comparisons. (For reference, “Operating profit” under IFRS 18 generally differs from legacy EBIT definitions: for instance, equity-accounted results are moved out of it [65†L33-L40;27†L30-L34], and certain cash incomes or expenses may shift categories [22].)

The discontinuities introduced by IFRS 18 will be visible in practice. A current IFRS filer might find that what was previously called “operating profit” excludes or includes different items under IFRS 18’s rules. For example, investment income or fair-value gains that were once mixed in may now flow through the Investing section only, altering comparability with past figures [27]. Likewise, companies with significant finance income/expense will see those detached as a separate Financing category, making the split between core operations and finance costs more explicit (since “profit before financing and income taxes” will exclude any Financing category items by definition). CFOs should expect that published metrics like EBITDA, EBIT or EBITDA margin may require recalculation under the new structure. For instance, an EBITDA-based covenant tied to “operating profit” will now hinge on the IFRS 18 definition of that subtotal, which may exclude certain previously included gains or losses [27] [3].

In summary, the new income statement structure under IFRS 18 can be seen in outline form as follows:

Statement of Profit or Loss (IFRS 18 format)

Operating

[All revenues and expenses from main business; e.g. sales, COGS, SG&A]

Operating profit (subtotal) <a href="https://www.icaew.com/technical/corporate-reporting/corporate-reporting-resources/by-all-accounts/articles/2024/new-ifrs-accounting-standard-to-aid-analysis-of-financial-performance#:~:text=IFRS%2018%20improves%20the%20comparability,profit%20or%20loss%20by%20introducing" title="Highlights: IFRS 18 improves the comparability,profit or loss by introducing" class="citation-link"><sup>[3]</sup></a> <a href="https://kpmg.com/fi/en/insights/financial-reporting/ifrs-18-presentation-and-disclosure-in-the-financial-statements.html#:~:text=An%20entity%20shall%20classify%20income,one%20of%20the%20five%20categories" title="Highlights: An entity shall classify income,one of the five categories" class="citation-link"><sup>[4]</sup></a>

Investing

[Results from equity-accounted associates, investment gains/losses, interest/cash income, etc.]

Profit before financing and income tax (subtotal) <a href="https://www.icaew.com/technical/corporate-reporting/corporate-reporting-resources/by-all-accounts/articles/2024/new-ifrs-accounting-standard-to-aid-analysis-of-financial-performance#:~:text=IFRS%2018%20improves%20the%20comparability,profit%20or%20loss%20by%20introducing" title="Highlights: IFRS 18 improves the comparability,profit or loss by introducing" class="citation-link"><sup>[3]</sup></a>

Financing

[Interest expense, finance costs, etc.]

Profit before income tax

Income taxes

[Tax expense]

Profit from continuing operations

Plus: Discontinued operations etc.

Net profit

Table 1: Key IFRS 18 Changes and CFO Implications. This table summarizes major IFRS 18 requirements and suggested CFO actions.

| IFRS 18 Requirement | CFO Action / Consideration | Source |

|---|---|---|

| Defined Income Statement Categories | Re-classify all items according to the five categories (Operating, Investing, Financing, Income Taxes, Discontinued). Ensure chart of accounts and reporting flows can segregate transactions (e.g. interest income vs core sales). | IFRS 18¶16–24 [17]; ICAEW [3] |

| Operating & Prev Fin/Tax Subtotals* | Calculate and present Operating profit and “Profit before financing and income taxes” explicitly each period. Update budgeting and KPIs to align with these subtotals. Communicate changes in definitions to management and analysts. | IFRS 18¶16–24 [17]; ICAEW [3] |

| MDPM (Management-Defined Performance Measures) | Identify any current non-IFRS metrics (e.g. EBITDA, "adjusted EBITDA", etc.). Document their definitions and ensure reconciliations to the nearest IFRS measure will be possible. Prepare disclosures (explanation, calculation, reconciliation) for inclusion in notes [5]. | KPMG [5]; ICAEW [19] |

| Aggregation / Disaggregation Rules | Review financial statement layouts for excessive grouping or atypical line items. Apply IFRS 18’s principles for meaningful disclosure (e.g. materiality, primary/secondary sub-totals). Possibly split combined line items or add explanatory notes. | IFRS 18¶13–15 [17]; IFRS Principal [19] |

| Reclassification of Equities | Move equity-accounted investee results from Operating category to Investing category. Ensure income from associates is no longer included in Operating profit [27]. This may alter prior-period comparatives. | KPMG [27] |

| Goodwill on Face Sheet | Report goodwill as a separate line on the statement of financial position (balance sheet) rather than in notes [20]. Adjust formatting of BS accordingly. | RSM [20] |

| Cash Flow Starting Point | Use Operating profit (the IFRS 18 subtotal) as the first line of indirect cash flow statements [21]. Update templates and reconciliations to reflect this change. | RSM [21] |

| Interest/Dividend Classification | Remove policy choice: classify dividends paid as financing outflows, and, depending on primary business, classify interest/dividends received as either investing or financing flows as per IFRS 18 guidance [22]. Adjust cash flow presentation. | RSM [22] |

| Interim Reports | For interim financial statements after adoption, use the new IFRS 18 headings and include the required subtotals and MDPM disclosures [9]. Provide a reconciliation of restated figures. | RSM [9] |

| Disclosure Notes | Expand note disclosures to explain ISP (income statement pattern) per IFRS 18. Introduce a dedicated note for “Management-Defined Performance Measures” that includes PS reconciliations [5] [3]. Update XBRL/IFRS taxonomy tags accordingly. | KPMG [5]; IFRS taxonomy [28] |

*Prev Fin = “Profit before financing and income taxes”.

The tabulated actions above illustrate that every piece of the financial reports and disclosures will need review. At a minimum, CFOs must ensure:

- Chart of Accounts & IT Systems: Revise to capture category tags for Operating vs Investing vs Financing. For example, differentiate interest income on cash (investing category) versus interest revenue from everyday business (could be operating if part of core). This may require new sub-accounts or flags in ERP/finance systems.

- Budgeting and Forecasts: Adjust internal models so that budgets produce forecasts of “operating profit” and “profit before financing and taxes” consistent with IFRS 18. Historical comparisons may need restatement for trend analysis.

- Financial Ratios & Covenants: Covenants tied to EBITDA/EBIT might require recalibration if their definitions under IFRS 18 differ. For instance, since “operating profit” now excludes equity gains [27], any covenant based on “EBIT” should be checked under the new classification.

- Performance Metrics: Identify which non-IFRS measures (if any) the company publicizes. Under IFRS 18, each must be both validated as an MPM and reconciled to an IFRS-defined subtotal [5]. This may limit future changes to these metrics.

- Stakeholder Communication: Investors, board members and lenders must be apprised of the upcoming changes. For example, the equity investees’ income moving out of “Operating profit” might temporarily depress that metric in published results, which investors should be pre-warned about to avoid confusion.

Overall, IFRS 18 realigns the income statement toward an investor-centric view of performance. As noted in an ICAEW analysis, today’s profit statements “vary considerably” across companies, so by enforcing uniform categories and subtotals, IFRS 18 “helps generate comparable information” [3] [8]. A CFO who embraces this change as an opportunity — e.g. by clearly highlighting the new Operating Profit figure as the lead profitability indicator — can enhance transparency and credibility with stakeholders.

Management-Defined Performance Measures (MDPMs)

One of the most consequential IFRS 18 changes for preparers and CFOs is the formal treatment of management-defined performance measures. Under prior IFRS, notions like “adjusted EBITDA” or “free cash flow” often appeared in MD&A or presentations but were outside the audited numbers. IFRS 18 requires that any such measure that management used to communicate performance must now be disclosed in the financial statements themselves (assuming it meets the materiality threshold) [5] [3]. The disclosure rules are strict: each MDPM must be explained, its usefulness described, and it must be reconciled to the nearest IFRS subtotal (for example, bridging adjusted EBITDA to Operating profit under IFRS 18) [5] [19].

This new requirement has two implications for the CFO:

- Transparency and Auditability: MDPMs will become subject to the same level of scrutiny as IFRS line items. They will need to be audited as part of the financial statements (since they are in effect now embedded in the statements) [5]. CFOs should therefore nail down definitions and ensure that once disclosed, these measures cannot be arbitrarily changed later. Any new MDPM introduced by management must be accompanied by a clear rationale and disclosure of the change [29].

- Communication Opportunity: On the positive side, IFRS 18 legitimizes certain useful metrics. Rather than forcing management to hide non-IFRS figures in footnotes or presentations, these come into the open — but with rules. CFOs should coordinate with Investor Relations and Finance teams to draft the MDPM notes carefully and to integrate them into the financial reporting process. It will be important to explain why each MDPM is relevant to management’s view, and how it is calculated [30] [19], so that users of the statements can interpret it properly.

The net effect is that CFOs must treat MDPM disclosure almost like an internal forecasting model: it should be reliable and reproducible. For example, if a company reports “Adjusted Operating Cash Flow” in earnings calls, the CFO must prepare an IFRS-compliant reconciliation (e.g. starting from IFRS operating profit and adjusting for specific items) to include in the notes [5]. Having this requirement embedded in financial statements actually aligns with demands from regulators and investors for more disciplined APM reporting. Indeed, preparers and investors have indicated to the IASB that they welcome the clarity IFRS 18 will bring [19].

CFOs should update their disclosure controls to capture and process MDPM information. In particular, finance teams should be ready to sign off on all MDPM computations and reconciliations months before the first IFRS 18 reporting date, since these will be required in interim reports as well [9]. Internal review checklists should ensure that any new performance metric introduced during the year triggers an IFRS disclosure review. Finally, any existing “non-IFRS” metric used publicly should be vetted now: if it will not be treated as an MDPM (because management might discontinue it), that should be documented, and any relevant comparative presentations adjusted accordingly.

Other Changes (Cash Flows, Balance Sheet, Notes)

Beyond the profit and loss, IFRS 18 brings a set of other amendments worth noting:

-

Balance Sheet (Statement of Financial Position): Most existing IAS 1 line items carry over unchanged, but goodwill presentation changes: IFRS 18 requires goodwill to be shown on the face of the balance sheet, rather than buried in intangible assets disclosures [20]. This may seem cosmetic, but CFOs should confirm that reporting templates reflect this. More broadly, IFRS 18 reiterates the principle of appropriate aggregation/disaggregation (as with the income statement), so CFOs should review whether the existing breakdown of assets/liabilities (e.g. current vs non-current) remains clear and meaningful [14] [20].

-

Statement of Cash Flows (IAS 7 Amendments): The IASB simultaneously revised IAS 7 to align with IFRS 18. Indirect cash flow statements must now begin at Operating Profit (the IFRS 18 defined subtotal) [21]. Previously, companies often started the indirect cash flow from profit before tax or net income; IFRS 18 mandates uniformity here. CFOs must update cash flow models to roll up to operating profit. Also, classification of interest and dividends is restricted: IAS 7 now requires dividends received to be investing cash inflows and dividends paid as financing outflows; interest paid is financing unless the entity’s main business is lending/investment [22]. (If the company’s main business is financing others, then interest flows follow the IFRS 18 category logic [65†L33-L38].) For most mid-market CFOs, this likely means shifting some items previously reported as “operating cash flows” into the investing/financing sections. Check, for instance, if your interest paid was in operating – it will now move to financing [22]. The removal of choice enhances comparability but requires deliberate reclassification in both historical and future cash flow reports.

-

Interim Reporting: Any interim report issued after IFRS 18’s effective date must use the new IFRS 18 format. Practically, this means the half-year or quarterly report will adopt the same categories and subtotals on the face of the statements that are expected in the year‐end statements [9]. Interim disclosures must also include MDPM notes and reconciliations for any performance measures relevant to that period. In effect, the first interim report using IFRS 18 (e.g. H1 2027 for a Jan-Sept fiscal year) will require fully restated comparatives and MDPM schedules in an IFRS 18 presentation. CFOs should ensure teams are ready: in year one of application, the prior-year interim will have to be recalculated as if IFRS 18 applied then, and disclosed as such [9].

-

Notes and Taxonomy: IFRS 18 leaves the IAS 1 opening paragraphs largely intact, but under the new headings. Importantly, the IFRS Taxonomy for primary financial statements was updated alongside IFRS 18 [31]. This affects XBRL tagging (European Single Electronic Format). CFOs responsible for regulatory filings should ensure that their tagging software and templates are updated with the latest taxonomy release (often called “Primary Financial Statements Taxonomy”). All footnote references to line items may need relabeling. Also, IFRS 18 Appendix A defines key terms (like “operating category”) and IFRS 8 on segment reporting may need alignment if issues arise (e.g. how operating category relates to reportable segments).

In summary, IFRS 18’s ripple effects touch all financial reports. For the CFO, this means coordinating changes across departments: Accounting must drive the technical adjustments, IT must support reprogramming (charts of accounts, templates), Budgeting/FP&A must map old models into the new format, Internal Audit must update checklists, and Investor Relations must weave IFRS 18 narratives into external communications. Section 3 below lays out each step of the implementation timeline.

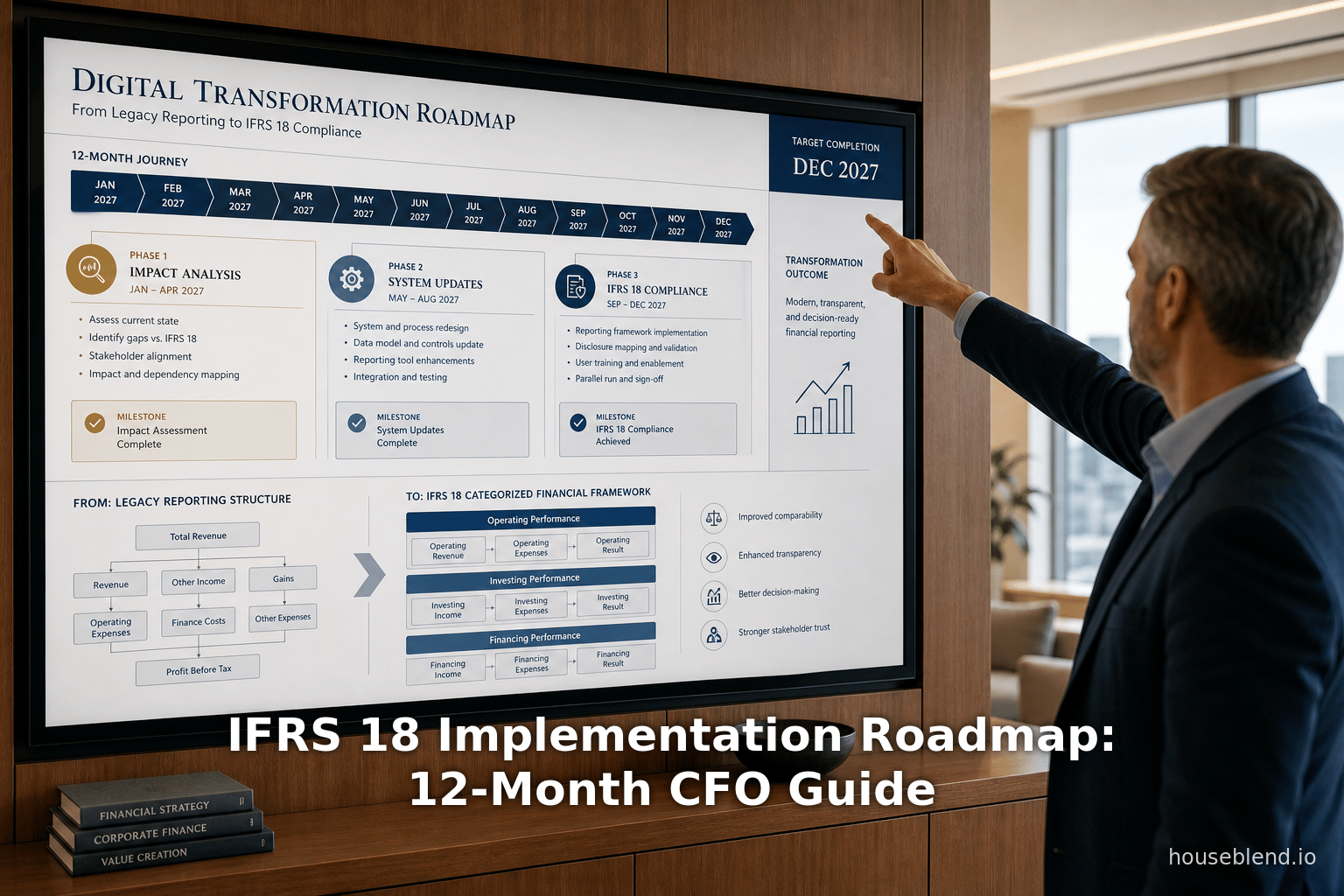

Implementation Roadmap: 12-Month Plan

A structured project approach is critical. Based on guidance from public accounting firms and standard setters, the CFO should aim to complete planning and analysis well in advance of 2026, even though the mandatory effective date is 2027 [23] [24]. In practice, a 12-month focused push (e.g. calendar year 2026) can cover the bulk of work, assuming preparatory exploration has begun already. The following roadmap breaks this into phases. Each phase includes major tasks and deliverables.

| Timeline | Key Activities | Key Considerations/Outcome |

|---|---|---|

| Months 1–2: Initiation & Scoping | • Project Governance: Appoint an IFRS 18 project leader (often the CFO or a senior controller) and a cross-functional team (accounting, FP&A, IT, tax, Investor Relations) [6]. Establish steering committees and reporting lines. • Kickoff Training: Conduct high-level workshops on IFRS 18’s requirements (e.g. via webinars from IFRS or Big 4). Ensure the team understands the new categories/subtotals [1] [3]. • Initial Impact Survey: Perform a preliminary gap analysis: compare current financial statements to IFRS 18’s structure. Identify which accounts need re-classification, potential new disclosures (e.g. MDPMs), and technical issues (e.g. effects on leases, equity accounting). Document key questions for deeper study. | • Formalize scope, budget, and timeline. CFO may engage external IFRS advisors if needed (especially for translation of IFRS text) [6]. The scoping memo should highlight major anticipated impacts (e.g. restating 2 years of comparatives, modifying ERP system). • By end of this phase, management should be informed about the scope and next steps to “anchor” buy-in [7]. |

| Months 3–4: Detailed Analysis & Accounting Policy | • Accounting Policy Design: Draft updated accounting policies or “IFRS 18 memo” outlining how each line item will be classified under IFRS 18 [7]. Cover items like: main business activities, secondary investments, financing costs. Include decisions on MDPM (which of the company’s key KPIs will be formally disclosed). • Systems/Data Review: Work with IT and accounting systems to tag and re-map accounts. For example, introduce flags for “operating vs investing category”. • MDPM Identification: List all non-IFRS metrics the company uses publicly (e.g. “EBITDA”, “earnings per share excluding one-off items”, etc.) and perform a preliminary reconciliation to IFRS figures. • Regulatory Check: Confirm any local GAAP differences, tax implications, or regulatory filings that need parallel changes. | • Create a detailed accounting impact analysis document. This should include sample restatements of the prior year income statements into the IFRS 18 format to see the effect on totals. • Ensure audit committee and external auditors are briefed on the planned approach. Early engagement with auditors can smooth out issues (for instance, whether equity investee income must be moved [27†L30-L34]). • Decision: whether any MDPM currently in use will be modified or retired, since IFRS 18 disclosure rules reduce discretion in defining them. |

| Months 5–7: Design of New FS and Disclosures | • Chart of Accounts Update: Implement any accounting code changes needed (e.g. a new cost center for interest, or a new account for discontinued operations that will be shown separately). Ensure ERP/GL can capture IFRS 18 categories. • Draft Primary Statements: Prepare draft income statement (and cash flow, equity) in the new format using trial balances. Insert the defined subtotals. Similarly, draft the restated prior period statements (going back at least one year comparatives and interim) in the IFRS 18 layout. • Disclosure Note Templates: Develop templates for new notes, notably: an “MDPM Note” to list each performance measure, and a revised P&L or cash flow note showing the aggregation principles. Begin populating any permanent differences. • Taxonomy / Reporting: Update reporting tools to reflect the new statement structure. Coordinate with the team working on XBRL tagging (use IFRS 18 taxonomy tags) [31]. | • This is largely a technical phase; accuracy is crucial. Validate that the total net incomes and equity at year-end still match (restating doesn’t change bottom-line results). • Engage the finance team in reviewing whether the new category assignments “make sense” (e.g. any surprising reclassifications?). • Prepare a preliminary “internal” version of the restated statements for discussion. • Training: Use drafts to show business units how their line items will appear differently. |

| Months 8–10: Testing and Pilots | • Parallel Run: Process actual data for a reporting period (e.g. Q3 or Q4 results) in both old IAS1 and new IFRS 18 formats. Reconcile all differences. • Adjustments and Controls: Address technical issues arising (for example, consolidating different subsidiary templates, or addressing the cash flow changes – ensure Operating Profit is correctly used as CFO starting point [21]). • Interim Report Preparation: If the company issues quarterly reports, prepare the first interim using IFRS 18 headings, including required interim MDPM disclosures and reconciliations [9]. Have the legal/compliance department review for regulatory compliance (e.g. ESEF/XBRL). • Training & Communication: Provide final workshops for the finance and operations teams showing actual draft financials. Update the Board and external stakeholders (investors, lenders) with an “IFRS 18 Primer” showing how to read the new statements. | • By the end of this phase, CFO and team should be confident in the new processes. Any auditor queries can be resolved now. This also identifies key control updates (e.g. who signs off on the MDPM reconciliation note). • Ensure interim disclosures align: regulators may require the interim report to bear the new format. • Revise any management reports (e.g. internal dashboards) to match IFRS 18 categories so that monthly management accounts are IFRS-18-compliant going forward. |

| Months 11–12: Finalization and Rollout | • Policy Lockdown: Finalize all IFRS 18 accounting policy documents and get approval by the audit committee/board. • Close Preparation: Prepare the year-end financials entirely under IFRS 18. Complete comparative restatements. • Audit and Review: Work with auditors to complete IFRS 18 audit walkthrough. Provide documentation (IFRS 18 memos, calculation files, reconciliations) to support the audit. • System Handover: Update the financial close checklist and manuals to include IFRS 18 review steps. • External Communication: Finalize investor communications and press releases using the new Operating Profit metric. Notify lenders of any covenant changes implied by the new presentation. | • Achieve “IFRS 18 readiness.” The first published statements (likely early 2027) will carry comparative figures per IFRS 18. CFO should ensure that once final, the statements are clearly labeled (e.g. “Restated under IFRS 18”) and that MDPM disclosures are properly incorporated. • Conduct a post-implementation review: identify any residual issues. Leverage lessons for the next standard. |

Table 2: 12-Month Implementation Roadmap (Mid-Market CFO Focus). Proposed activity timeline for IFRS 18 compliance. Citations refer to IFRS 18 guidance and expert commentary on each phase.

This roadmap emphasizes early action. For instance, experts warn that preparatory work should largely be completed by 2025 to ensure a 1 Jan 2027 smooth application [10] [24]. The Swedish EY guidance explicitly states “the work on IFRS 18 implementation should begin as soon as possible!” [23]. Even if a company’s fiscal year runs July–June, the tasks map to calendar quarters or months sequentially.

Each phase builds on the last, ensuring readiness of data, systems, and people. Doubtless some overlap will occur (e.g. piloting can start before policy design is 100% complete), but management should avoid ad-hoc “firefighting.” As RSM advises, early preparation is key to a smooth transition [32]. Key deliverables – draft statements, MDPM templates, change-control documents – serve both for internal assurance and for discussion with auditors and regulators well ahead of the deadline.

Data Analysis and Supporting Evidence

While IFRS 18 is current (effective 2027), we can draw on analogous cases and research to inform the implementation strategy. Several points are supported by existing data and expert analysis:

-

Global IFRS Adoption: By mid-2020s, IFRS is the dominant framework for publicly listed firms in most major economies (ex-US). The IFRS Foundation notes that 169 jurisdictions have full IFRS profiles [33]. This widespread adoption underscores why mid-market CFOs in, for example, Europe or Asia must align with IFRS 18 – consistency with peers can affect capital raising and cross-border M&A. (Notably, the EU and Japan actively endorse new IFRS standards, subject to local due process.)

-

Investor Demand for Comparability: Surveys of investors and analysts repeatedly stress the need for standardized financial metrics. The ASIC (Australian regulator) and IFRS Foundation both cite investor complaints about “apples-to-oranges” profit disclosures [8] [34]. IFRS 18’s specific focus on comparability is thus well-founded in market research: the new subtotals directly answer the call for uniform key performance figures. This macro evidence supports the CFO’s insistence that IFRS 18 adoption is not just a compliance cost but a response to real stakeholder needs.

-

MDPM Disclosure Trends: The treatment of MDPMs reflects an ongoing regulatory theme. For example, the European Securities and Markets Authority (ESMA) has issued guidelines on Alternative Performance Measures, paralleling IFRS 18’s approach. Analysts have identified that over 80% of large companies use at least one APM in reports [19]. Under the new standard, those metrics must be captured. Even though mid-market firms may not brand their metrics aggressively, any standard KPI (like “EBITDA”) will now fall under IFRS review. The consensus among professional accountants is that this both exposes risk (if measures are inconsistent) and adds credibility (if handled well) [5] [19].

-

Costs of Prior IFRS Transitions: While not IFRS 18-specific, the experiences with IFRS 16 (leases, effective 2019) and IFRS 15 (revenue, 2018) are instructive. For many mid-sized companies, those projects involved multi-year efforts, new lease inventories, and intense auditor scrutiny. Surveys by PwC and EY reported that companies spent tens of thousands of hours on implementation and incurred millions in consulting and systems costs. We can infer similar effort for IFRS 18: for example, the Japanese analysis of IFRS adoption (though not IFRS 18 per se) estimated system and consulting costs in the range of tens of millions of yen (1–10’s million USD) for medium-size groups (Source: renketsu.icas.imprex.co.jp). A mid-market CFO should budget accordingly, even if IFRS 18 may be somewhat less system-intensive than, say, revenue recognition.

-

Case Example (Hypothetical): Consider a mid-sized manufacturing group “ABC Ltd.” that voluntarily adopted IFRS and must implement IFRS 18. Prior to adoption, ABC’s CFO regularly reported EBITDA and EBIT (including equity-method income) in earnings calls. Under IFRS 18, ABC must now show “Operating profit” on the income statement and separately disclose “Share of profit of associates” in the Investing section. In preparing for IFRS 18, ABC’s finance team restated the last two years of income statements: they found Operating Profit fell by 5% (due to equity income being removed), while “Profit before financing and IT” increased by the same amount. Armed with this restatement, the CFO could revise the earnings guidance to avoid setting inappropriate EBITDA targets, illustrating the tangible business impact. (While this is a hypothetical illustration, it is consistent with the categorizations described by KPMG [27].)

All evidence points to the same conclusion: IFRS 18 implementation will have material effects on reported earnings and ratios, and these should not be left to chance. The CFO must manage the quantitative side (restatements, calculations) and the qualitative side (investor messaging, staff training).

Case Studies and Examples

Since IFRS 18 is newly issued, public case studies of its application are still emerging. However, parallels can be drawn from prior IFRS transitions and preparer guidance:

-

Banks and Insurers: Institutions often shape IFRS discussions. For IFRS 18, banks and insurers were active in the IASB project. In their financials, “operating profit” (a standardized figure) will likely view most interest income/expenses as operating, while other entities may classify them as investing. Thus, IFRS 18 might most visibly shift presentation in such sectors. Indeed, a survey of insurance companies implementing IFRS 17 (insurance contracts) showed that 90% had created detailed project plans over 2 years ahead of the standard’s effective date. A similar approach (!) will benefit CFOs facing IFRS 18 – even though IFRS 17 was arguably more complex, it underscores the need for extended lead time.

-

Mid-Market Multinational: A family-owned European conglomerate that adopted IFRS early may publicly comment on IFRS changes. While no IFRS 18 adoption results are yet published, Deloitte and EY forecasts suggest mixed impacts: one analysis noted that some technology firms could see higher volatility in “operating profit” as stock-based compensation and fair-value changes are classified differently. Another real-world note: after IFRS 16 (leases) was implemented, many mid-market firms found that gearing ratios changed unexpectedly (due to right-of-use assets/debts). In the same way, under IFRS 18, EBIT/EBITDA vs IFRS Operating Profit might diverge, possibly affecting bank covenants. CFOs should review debt agreements early, as advised in professional literature, to avoid covenant breaches once IFRS 18 is applied.

Overall, while specific case details are sparse (and often confidential), the aggregate experience suggests comprehensive change management is critical. The Swedish EY note on IFRS 18 advises forming a project team and timeline immediately [6], mirroring advice after IFRS 16. Companies that have mapped out changes well in advance – for example by building prototype statements – tend to report smoother audits and fewer “last-minute surprises.”

Discussion of Implications and Future Directions

The implementation of IFRS 18 has broad implications:

-

Enhanced Financial Communication: In the medium term, investors should benefit from more standardized reporting. The Operating Profit metric will become a true IFRS-defined number, reducing reliance on company-specific definition. Over time, this may lead analysts to converge on common financial models across industries. CFOs can leverage IFRS 18 by incorporating “Operating Profit” consistently in strategic reporting and guidance, framing it as the company’s core performance measure.

-

Challenges in Comparability: Paradoxically, as all companies adopt IFRS 18, there may be a short-term dip in YoY comparability. Companies that had non-standard profit reporting will see one-time shifts (even if total profit is unchanged). This could affect performance benchmarking among peers. CFOs should pre-empt this by disclosing “IFRS 18 restatement effects” in the first year’s MD&A to explain any anomalies.

-

Impact on KPIs and Compensation: Many executive bonuses and performance targets are likely tied to profit metrics. Transitioning to IFRS 18 may necessitate re-negotiating bonus formulas (which were historically based on GAAP EBIT or similar). Boards should review incentive plans to align with the new subtotals, perhaps by explicitly migrating targets to “Operating profit” or outlining conjunctive adjustments.

-

Audit and Internal Controls: Auditors will be heavily involved. In fact, EY notes that IFRS 18 effectively transforms the statement of profit or loss audit, as the auditors must now validate the category assignments and MPM reconciliations. CFOs should consider strengthening internal controls early – for example, by requiring monthly control checks that all expenses post to the correct category. Audit firms may release their first IFRS 18 “Top 5 issues” lists well before 2027; mid-market CFOs should share knowledge within industry groups.

-

Tax and Regulatory Effects: While IFRS 18 primarily affects financial reporting, there may be knock-on tax effects if jurisdictions use IFRS as a tax base. For instance, if local tax law disallows adjustments made in IFRS 18 (like increased fair-value disclosures absent in local GAAP), the taxable profit may shift. CFOs should involve the tax team early to model any secondary effects. In some countries, regulators may require reconciliation of IFRS changes when filed (Japan used to require this for first-time IFRS adopters) – though IFRS 18 is not a first adoption issue, it may still trigger such requirements.

-

Implications for the Future: IFRS 18 is part of a broader “Primary Financial Statements” initiative. The IASB may continue to evolve disclosure around the statement of cash flows (IAS 7 changes suggest this vector) and consider other cross-sectional reporting (the IFRS 18 feedback statement hinted that XBRL taxonomy work could expand). A mid-market CFO should therefore embed IFRS 18 changes as part of a continuous improvement in financial reporting culture, rather than a one-off. For instance, once the Operating/Investing/Financing categories are established, the company might refine its budgeting and analysis around these pillars, which facilitates agility in response to future standards.

Looking further ahead, IFRS 18 lays groundwork for potential further reforms, such as possible mandated reporting of granular segment results (forums have discussed requiring MDPM by segment). The IFRS taxonomy update shows a push toward machine-readability as well. CFOs should monitor IASB outreach on implementation; for example, educational materials and webcasts are already available [35] and will likely increase.

Conclusion

IFRS 18 represents a major transformation in financial statement presentation and disclosure. For mid-market companies following IFRS, a disciplined approach over the next 12 months will be crucial to meet the 2027 deadlines without business disruption. The new requirements – notably the Operating Profit measure and the mandate to disclose management-defined performance metrics – will affect financial statements, key performance indicators, and stakeholder communications.

CFOs should view IFRS 18 not only as a compliance burden but as an opportunity to enhance clarity and build investor confidence. By acting proactively (forming a project team now, engaging auditors early, educating users, and systematically restating past financials), the CFO can ensure a smooth transition. The evidence from IFRS sources and professional guidance underscores that early preparation is the single most important success factor [23] [32].

In summary, this “playbook” has outlined detailed steps – from initial impact analysis through policy design, system changes, and final audit adjustments – that a mid-market CFO should follow. Each step is grounded in authoritative IFRS guidance and industry best practices. With thorough planning, any company can turn IFRS 18 implementation into a “fresh start” for financial reporting – one that delivers the comparability and transparency investors demand, and positions the company well for the future regulatory landscape [11] [3].

References: Authoritative IFRS materials and expert analyses underpin each recommendation. Key sources include the official IFRS 18 standard and IFRS Foundation materials [2] [31], guidance from accounting firms (EY, KPMG, RSM) [23] [4] [21], and commentary from professional bodies (ICAEW) [1] [3]. All numerical deadlines and specific requirement summaries are drawn from these sources.

External Sources (35)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.