IFRS 2026 Annual Improvements: NetSuite Implementation

Executive Summary

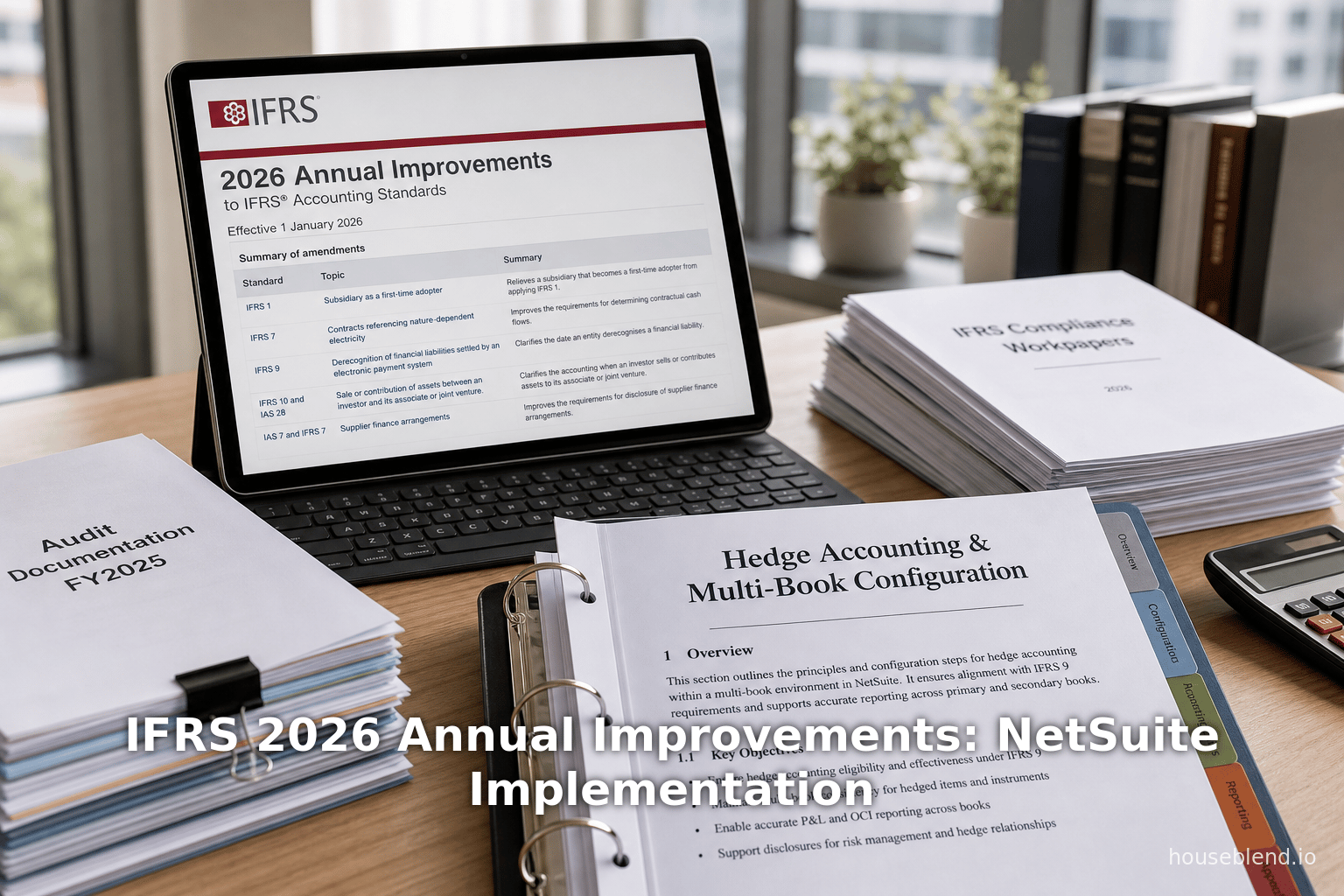

The 2026 Annual Improvements to IFRS Standards (Volume 11) introduce narrow-scope amendments to five key standards – IFRS 1, IFRS 7, IFRS 9, IFRS 10, and IAS 7 – effective for periods beginning 1 January 2026 [1] (Source: www.grantthornton.com.ph). These changes clarify hedge-accounting rules for first-time adopters (IFRS 1), update disclosure requirements for financial instruments (IFRS 7), refine derecognition and measurement in financial instruments (IFRS 9), strengthen consolidation guidance (the “de facto agent” test in IFRS 10), and modernize cash-flow classifications (IAS 7).

For organizations using NetSuite (“NetSuite users”), these amendments have practical implications. NetSuite’s multi-book accounting architecture allows one transaction to post simultaneously under multiple standards (e.g. IFRS and a local GAAP) [2] [3]. However, the updated IFRS rules will require careful configuration changes: for example, updates to IFRS 9’s classification tests (such as the Solely Payments of Principal and Interest test) and derecognition criteria will need explicit mapping in NetSuite’s financial instrument setups, and changes to IAS 7 wording may affect cash-flow report templates. Practitioners must ensure that NetSuite’s ledgers and reporting tools capture the revised IFRS requirements. Real-world examples show that companies adopting IFRS in NetSuite can leverage its built-in multi-ledger and currency-conversion engines to comply with global reporting standards [4] [3].

This report provides an in-depth technical analysis of each amendment area, its rationale, and concrete impacts on NetSuite implementations. We begin with background on IFRS and the Annual Improvements process, then examine each affected standard in turn (history, amendments, and application). In each section, we integrate authoritative IFRS Foundation sources, regulatory texts, and industry research. We discuss implications for accounting data, system changes in NetSuite, and associated internal controls. Case scenarios illustrate how entities must adjust their financial processes. We conclude with a look ahead at ongoing IFRS developments and how NetSuite users can prepare.

Introduction and Background

The IFRS Framework and Annual Improvements

International Financial Reporting Standards (IFRS) are the global accounting standards issued by the IASB, used in over 140 jurisdictions worldwide [5]. IFRS aim to enhance transparency and comparability of financial statements. Unlike US GAAP, which is rule-based, IFRS is principle-based; this often leads to multiple acceptable treatments under underlying concepts, explained and resolved through interpretations and improvements.

The Annual Improvements process is the IASB’s mechanism for routine maintenance of IFRS. As the IASB’s Due Process Handbook explains, Annual Improvements are limited to “changes that clarify the wording in an IFRS Standard or correct relatively minor unintended consequences, oversights or conflicts between requirements” [6]. In other words, they are narrow-scope amendments – not sweeping reforms, but important tweaks to existing Standards. The 2026 improvements (Volume 11) continue this tradition.

The amendments were approved July 2024 (for mandatory application 1 Jan 2026, early application permitted) [7] (Source: www.grantthornton.com.ph). Volume 11 (“2026 Annual Improvements”) includes five standards:

- IFRS 1 First-time Adoption of IFRS – Hedge accounting by a first-time adopter.

- IFRS 7 Financial Instruments: Disclosures – Gain or loss on derecognition; plus related amendments to the IFRS 7 implementation guidance (for illustrative examples and credit-risk disclosures).

- IFRS 9 Financial Instruments – Derecognition of lease liabilities; and transaction-price definitions.

- IFRS 10 Consolidated Financial Statements – Determination of a “de facto agent” (model for consolidation).

- IAS 7 Statement of Cash Flows – “Cost method” terminology in cash flows.

These are summarized in the IASB press release [8] and professional summaries (Source: www.grantthornton.com.ph). We will examine each of these in turn.

IFRS Adoption and NetSuite Context

IFRS are widely mandated internationally. Over 110 jurisdictions (including the entire EU, Australia, and much of Asia and Latin America) require IFRS for public companies [5] [9]. This contrasts with US GAAP, used primarily in the United States. Companies that straddle these regimes – for example a US-based parent with foreign subsidiaries or vice versa – frequently must prepare parallel financial statements. This dual-reporting demand creates complexity: traditional spreadsheets and siloed ledgers often lead to errors and delays. In fact, surveys find that around 40% of CFOs globally do not fully trust the accuracy of their financial data, largely due to “disjointed spreadsheets and disparate ledgers” [10].

Modern ERP systems like Oracle NetSuite are expressly designed to address this. NetSuite’s OneWorld module is a multi-entity, multi-currency, multi-book platform that can manage simultaneous IFRS and other standards. For example, NetSuite OneWorld supports 190+ currencies, 27 languages, and multiple accounting standards (GAAP and IFRS) in one unified instance [9]. Transactions entered once can be posted in parallel to multiple reporting “books” (ledgers), each configured with its own chart of accounts and recognition rules [2] [3]. The system also automates multicurrency revaluation and consolidation eliminations [11].

In practice, this means that a multinational can close books in IFRS while consolidating in GAAP concurrently. For example, a European subsidiary could prepare its standalone IFRS statements, while the US parent consolidates under GAAP, all within NetSuite – without separate data entry [11]. NetSuite’s multi-book ledgers reduce the need for manual adjustment journals and reconciliations. Such capabilities are increasingly essential: more than 60% of recent tech IPOs (e.g. 66 companies in 2021 alone) have relied on NetSuite for their finance systems [12].

Nonetheless, any change to accounting standards requires a careful review of how the ERP maps those standards. For a NetSuite user, the 2026 IFRS amendments will necessitate modifications to configuration, data tagging, and reporting.This report unpacks those changes in detail. First, we explain each relevant IFRS amendment and its rationale, then discuss how it affects accounting processes. Finally, we tie it together with recommendations for NetSuite setups and controls.

IFRS 1: First-Time Adoption – Hedge Accounting Revisions

Background to IFRS 1

IFRS 1 governs the transition when an entity adopts IFRS for the first time. It ensures comparability by requiring restatement of prior GAAP information to IFRS as if the entity had always applied IFRS, subject to certain mandatory exceptions and optional exemptions. A key aspect is dealing with hedge accounting. Since IFRS 9 (Financial Instruments) overhauled hedge accounting in 2014 (supplanting IAS 39), IFRS 1 had been updated at that time to reflect the new financial instrument rules (replacing IAS 39 references with IFRS 9) [13]. IFRS 1 already contained a section (paragraphs B5–B6) on hedge-accounting relationships that a first-time adopter cannot carry over if they did not qualify under IFRS.

Historically, IFRS 1 permitted a first-time adopter to re-designate hedges in some cases, but it prohibited retaining any ineligible hedge designations from local GAAP. For example, IFRS 1.B5 used to list hedges that IFRS would never allow (such as a “portfolios of options” hedge). IFRS 1.B6 required discontinuation of any hedge that does not meet IFRS criteria. The language in IFRS 1.B5–B6 had originally been crafted under IAS 39 and referred to hedging “conditions” [14].

Since full IFRS 9 compliance is required by a first-time adopter from day one, the IASB reviewed IFRS 1 to ensure its wording aligns with IFRS 9’s terminology and criteria. The 2026 Annual Improvements make targeted updates for clarity and consistency.

Amendments in Annual Improvements

The 2026 amendments to IFRS 1 (Hedge Accounting by a First-time Adopter) update paragraphs B5–B6. The key changes are:

-

Cross-references to IFRS 9: New references to the relevant IFRS 9 sections (instead of generic wording). Specifically, IFRS 1.B5 now cites IFRS 9 para. 6.4.1(a), and IFRS 1.B6 cites 6.4.1(b)–(c) [15]. These paragraphs in IFRS 9 set out the three qualifying criteria for a hedge: (a) eligible instrument and item, (b) formal designation/documentation, and (c) hedge effectiveness requirements [16]. By pointing to these, IFRS 1 explicitly ties the transition rules to IFRS 9’s hedge definitions.

-

Terminology alignment (“conditions” → “criteria”): Before, IFRS 1.B6 said a hedge not meeting the “qualifying conditions” of IAS 39 had to be discontinued. Now it refers to IF RS 9’s “qualifying criteria.” This change fixes an inconsistency: IFRS 9 uses “qualifying criteria,” so IFRS 1 adopts the same language [17]. In short, IFRS 1.B6 is rephrased to match IFRS 9 terminology.

No intent or accounting outcome is changed – a first-time adopter must still discontinue any hedges that IFRS deems ineligible. The improvements simply clarify the linkage. For example, after the amendment IFRS 1.B5 now reads (paraphrasing): a hedging relationship that does not meet IFRS 9.6.4.1(a) must not be reflected in the opening IFRS balance sheet [15].

Impact on Accounting Process

For practitioners, these IFRS 1 amendments are straightforward: they reinforce that IFRS 9 rules govern all hedges at transition. There is no new accounting choice or transition option introduced. Instead, preparers should ensure their transition checklists explicitly reference IFRS 9’s paragraphs 6.4.1(a–c) when evaluating pre-IFRS hedges. In practice, this means:

- During conversion, any hedge from local GAAP that fails IFRS 9’s criteria (e.g. an ineligible written option portfolio) must be terminated, as before. The amended IFRS 1 just directs the preparer to which paragraphs in IFRS 9 to apply.

- If the entity had a net position designated as a cash-flow hedge locally, IFRS 1.B5 clarifies how to treat it. Under IFRS 9 an entity may designate an individual item or reopened net position provided IFRS 9.6.6.1 conditions are met by the transition date [18].

- No parallel activity is needed that wouldn’t have been done otherwise, but the NetSuite ledger should document these changes. For instance, if a hedge is discontinued, the derecognition flows should use IFRS 9’s extinction rules (IFRS 9.3.3) – see below.

NetSuite implications: In NetSuite, hedge accounting is typically managed via derivative instruments and designated hedging relationships. The IFRS 1 update reminds us that the system should enforce the IFRS 9 hedge criteria from the get-go. For NetSuite users:

- Re-designation at transition: If a hedge must be discontinued under IFRS 9, NetSuite’s hedge modules (or manual entries) should reflect its termination at transition with appropriate entries (using IFRS 9 derecognition rules). If an opening designation is permitted (using IFRS 9.6.6.1 as noted in IFRS 1.B5), NetSuite’s hedge documentation should be completed by transition date.

- Multi-book settings: If running parallel US GAAP and IFRS books, the IFRS book should apply the IFRS 1 rules, while the GAAP book may preserve old hedges. NetSuite’s Multi-Book can post a one-time adjustment in the IFRS book to remove the hedge, while leaving the GAAP book untouched.

- Disclosure: IFRS 7 (disclosures) requires detailing hedge accounting policies and transitions. NetSuite reports or notes generator will need updated disclosures referencing IFRS 9 criteria. (See next section.)

Overall, the IFRS 1 amendment imposes no new system functionality – it is about consistency of language. Users must simply align all hedge-related transition activities with IFRS 9’s framework [17] [13].

IFRS 7: Financial Instruments – Disclosures

Background to IFRS 7

IFRS 7 prescribes disclosures for financial assets and liabilities. It covers carrying amounts, classifications, risk exposures (credit, liquidity, market), fair-value hierarchy, and more. IFRS 7 complements IFRS 9 by ensuring transparency around instrument measurement and risks. Importantly, IFRS 7 has non-mandatory illustrative guidance (IG), including examples (IG14, IG20B, etc.), which help with implementing specific disclosure requirements.

Since IFRS 9 replaced IAS 39’s classification rules, IFRS 7 underwent some amendments (e.g. IFRS 9 issuance removed references to “IAS 39” or “IAS 39 guidance”). Likewise, IFRS 7’s guidance has been tweaked over time (e.g. in IFRS 13 / IFRS 9 releases). The 2026 improvements target residual inconsistencies and obsolete references in IFRS 7’s text and guiding examples.

Amendments in Annual Improvements

The Annual Improvements to IFRS (2026) include the following narrow changes to IFRS 7:

-

Gain or loss on derecognition (Paragraph B38): IFRS 7.B38, which defines the presentation of gains/losses on derecognition of financial assets/liabilities, had an erroneous internal reference. Specifically, IFRS 7.B38 referred to paragraph 27A, which was deleted when IFRS 13 (Fair Value Measurement) was issued [19]. The amendment simply removes or corrects this obsolete reference. After amendment, IFRS 7.B38 no longer points to the non-existent 27A, fixing the cross-reference [19].

-

Implementation Guidance (Examples): Several paragraphs in the Implementation Guidance (IG) to IFRS 7 are updated for consistency:

-

IG1 (Introduction) Clarification: The introductory text (IG1) is amended to clarify that the guidance is illustrative and does not cover every requirement [20]. This reminds preparers that the IG excerpts are not exhaustive.

-

IG14 (Deferred difference between fair value and transaction price): Paragraph IG14 of IFRS 7 illustrates the (rare) case where an asset is initially measured at transaction price but later sold or liquidated. The ongoing improvements align the wording of IG14 with the amended IFRS 7.28. When IFRS 13 was issued (2011), IFRS 7.28 was updated to clarify that the difference between transaction price and fair value is an accounting policy (as in B5.1.2A(b) of IFRS 9) [21]. However, IG14 was not updated at that time, causing minor wording mismatches. The 2026 amendment harmonizes IG14’s wording with IFRS 7.28/28(a–c) so that terms like “transaction price” and “fair value” are consistently described [21] [22]. Essentially, IG14 now uses phrasing from IFRS 9.B5.1.2A(b) when discussing transaction prices (i.e. the expected fair value at initial recognition) [21].

-

IG20B (Credit Risk Illustrations): Paragraph IG20B (which exempts disclosure for a transferred asset that is fully derecognized) is reworded to simplify its language. The amendment does not change any disclosure requirement, only makes the example easier to read.

-

No new disclosure obligations are being introduced by these amendments; they only correct cross-references and wording.

Impact on NetSuite Reporting

For IFRS 7 disclosures, the practical impact is limited. Entities should note the updated references but continue providing the disclosures as before. For NetSuite:

-

Disclosure notes and taxonomies: Many organizations use NetSuite’s reporting or XBRL tools to generate IFRS notes. The amendments may require minor text changes in disclosure templates. For example, IFRS 7.B38’s corrected reference or IG14’s updated phrasing might need to be reflected in XBRL tags (the IFRS taxonomy was updated for 2024/5 standards). Ensure the tagging definitions (especially for gain/loss on derecognition, fair value differences, etc.) align with the new text.

-

Internal guidance: The finance team should update any accounting memos or checklist items that point to IFRS 7 paragraphs. For instance, any internal reference to IFRS 7.28 should now be consistent with IG14 wording. Similarly, the elimination of the obsolete 27A reference means internal cross-checks should no longer expect that number.

-

Examples and training: The implementation examples (IG) may be used in training or guidance. Teams should be informed of the slight rewording in IG14 so they don’t misinterpret the prior-text. (NetSuite itself doesn’t enforce IG, but preparers rely on it.)

Overall, because these are editorial fixes (the underlying disclosure model is unchanged), minimal system work is needed. It is mainly a matter of ensuring documentation and note-preparation rely on the corrected IFRS text. For NetSuite, this means verifying that IFRS accounting policy notes and disclosure notes mirror the updated wording, perhaps in the “Accounting policies” module or XBRL instance documents.

IFRS 9: Financial Instruments – Derecognition and Transaction Price

Background to IFRS 9

IFRS 9 (effective 2018) replaced IAS 39 for financial instruments. It covers classification and measurement, impairment, and hedge accounting. Key to IFRS 9 are rules for when to derecognize (remove) a financial asset or liability from the balance sheet, and how to measure initial recognition (including treatment of transaction costs and “transaction price”). The scope of IFRS 9 traditionally excludes lease contracts (those are in IFRS 16) except for certain aspects like embedded derivatives.

Several narrow issues have been identified in practice post-IFRS 9 issuance, especially where IFRS 16 (Leases) and IFRS 15 (Revenue) intersect IFRS 9. The 2026 improvements address two such issues: (1) accounting for extinguishment of lease liabilities under IFRS 9, and (2) clarifying use of the IFRS 15 transaction price concept in IFRS 9.

Amendments in Annual Improvements

The amendments to IFRS 9 are:

-

Derecognition of Lease Liabilities (Paragraph 2.1(b)(ii): IFRS 9’s scope exclusions (para 2.1) say that IFRS 16 leases are not in IFRS 9’s ambit, but then provide detailed carve-outs. Paragraph 2.1(b)(ii) originally excluded “lease liabilities recognized by a lessee” from IFRS 9 and pointed to IFRS 9.3.3 for guidance. Stakeholders noted a mismatch: IFRS 9.3.3 defines extinguishment of a financial liability (with gain/loss recognition), but IFRS 9.3.1 defines the extinction event (when to remove). The Annual Improvement updates the cross-reference so that IFRS 9.NB R changegain points to 3.3.3 for lease liabilities extinguishment [23]. In other words, when a lease liability is settled or transferred, the gain or loss to record should follow IFRS 9.3.3 exactly (difference between carrying amount and any consideration), rather than the prior (less clear) reference.

-

Transaction Price (Paragraph 5.1.3): IFRS 9.5.1.3 deals with initial measurement of trade receivables. It originally said that at initial recognition, trade receivables are measured at “transaction price (as defined in IFRS 15)” if there is no significant financing component [22]. However, as IFRS 15 evolved (including practical expedients), the term “transaction price” became nuanced. A trade receivable can be split into a receivable (financial asset) and a contract liability, so the explicit mention of “transaction price” could confuse users about measurement. The Annual Improvements amend 5.1.3 by removing the undefined “transaction price” term and instead simply referring to measuring receivables per IFRS 15’s logic (amounts receivable and a contract liability per IFRS 15.105-106) [22]. In effect, the change has no substantive impact: trade receivables without financing are still initially measured at the consideration due. But the wording now matches IFRS 15 guidance.

Impact on Accounting Process

-

Lease liabilities (IFRS 16 interaction): For a lessee using NetSuite, lease liabilities (under IFRS 16) and any early payment or modification should be derecognized following IFRS 9.3.3. Previously, the IFRS 9 scope paragraph might have pointed to the wrong subparagraph. Now it is clear that any gain or loss on a settled lease liability is recognized in profit or loss as “the difference between the carrying amount and consideration paid” [24]. In practice, NetSuite’s Lease Accounting module (or an integrated subledger) should already book a gain/loss on extinguishment. This amendment simply confirms the correct line item and reference. No system change is likely needed unless a pre-existing process incorrectly used the old paragraph reference.

-

Trade receivables – IFRS 15 interaction: The wording change means that an initial trade receivable should be measured consistent with IFRS 15’s contract model. NetSuite automatically does this when using the Advanced Revenue module. For direct trade receivables: if a NetSuite AR transaction has no financing component, the receivable will equal the invoice amount. The amendment removes ambiguity and aligns the AR initial measurement with revenue setups. NetSuite users should ensure that their AR postings (often driven by revenue schedules) do not separately refer to a “transaction price” concept; they should reflect the net receivable and contract liability as per IFRS 15. In other words, apply the normal AR booking (debit AR, credit revenue, credit contract liability if any) as usual [25].

-

Cross-standard coordination: These amendments highlight the interplay of IFRS 9 with IFRS 16 and IFRS 15. NetSuite addresses such interactions with integrated solutions (e.g. the Revenue module that handles IFRS 15, the Lease module for IFRS 16, and so on). After these changes, a NetSuite administrator should review the interface points: for example, if a lease liability is marked as paid off early, check that the gain/loss is recorded in the correct account and tabulated for disclosures. If a revenue contract’s customer payment leads to an AR, verify that the receivable equals the IFRS 15-determined consideration.

In summary, IFRS 9’s amendments fix cross-references and language without altering fundamental accounting outcomes. NetSuite configurations for finance and subledgers should already comply; however, documentation and reporting (e.g. IFRS 9 disclosures of gains/losses, AR initial measurement notes) may need minor textual updates to reflect the new phrasing [24] [22].

IFRS 10: Consolidated Financial Statements – “De Facto Agent”

Background to IFRS 10

IFRS 10 establishes how an investor (parent) determines control over an investee (subsidiary) and thus whether consolidation is required. Control is assessed based on power, exposure to variable returns, and their linkage. A unique aspect of IFRS 10 is guidance on agency relationships. An investor may have “de facto agents” – parties that act on its behalf in directing the investee – which can affect whether the investor or someone else consolidates the entity. In practice, the “Agent vs Principal” analysis can be complex.

Paragraphs B73–B74 of IFRS 10 CR\TeX spells out the concept. IFRS 10.B73 says an investor must consider its relationships with other parties and whether those parties are acting on the investor’s behalf (i.e. de facto agents). IFRS 10.B74 provides an example: it characterizes a party as a de facto agent when “the investor has… the ability to direct that party to act on the investor’s behalf.” Per earlier IFRS guidance, if a de facto agent holds decision rights, those rights are attributed to the principal.

Before the amendment, some users found a tension: B73 used cautious, judgmental language (“consider whether… acting on behalf”), while B74’s wording was more conclusive (“a party is a de facto agent when…”). The change aims to harmonize those slight inconsistencies.

Amendment in Annual Improvements

The 2026 Annual Improvement revises paragraph B74 of IFRS 10. The original B74 read (paraphrased):

“A party is a de facto agent when the investor has… the ability to direct that party…”

The amendment softens the wording. As the IASB explain, the new draft of B74 now emphasizes judgement and treats the previously-clear example as one possible scenario. In practice, this means B74 no longer definitively states “a party is [always] a de facto agent if…”. Instead, it clarifies that the described relationship is an example of circumstances requiring judgment [26]. Thus, it aligns B74 with B73’s approach. In the taxmann summary, a note explains:

“Amended paragraph B74 uses less conclusive language and clarifies that the relationship described in B74 is just one example of a circumstance in which judgment is required to determine whether a party is acting as a de facto agent.” [26]

Concretely, IFRS 10.B74’s amended text (not publicly quoted by IFRS) likely inserts qualifiers (e.g. “for example” or “in such cases”) and removes the word “is” to something like “may be considered”.

No assessment criteria are removed – investors must still evaluate agency factors as before – but the wording now discourages a mechanical interpretation of B74.

Impact on Consolidation Assessment and NetSuite

This amendment is conceptual rather than procedural. All entities currently applying IFRS 10 already perform the holistic analysis of agency relationships. They must identify any de facto agents among an investee’s decision-makers or other parties (for instance, voting rights held by related parties, significant co-investors, etc.), and include or exclude those rights per principal/agent principles (Source: annualreporting.info) [26].

NetSuite Impact: IFRS 10 is about consolidation logic, not account entries. However, NetSuite’s consolidation modules (in OneWorld and Beyond Reports) can assist group accounting. NetSuite consolidations work by pulling in subsidiary ledgers based on ownership data. The IFRS 10 amendment does not directly change any calculation or data element in NetSuite. Instead:

-

Disclosure and policy manuals: Entities should update disclosure notes on consolidation policies. The language describing de facto agents in their consolidation policy (often a note citing IFRS 10) should be aligned with the amended text. E.g., a note that formerly quoted B74 (“a party is a de facto agent when…”) should ensure it reflects the updated IFRS wording (perhaps replacing “is” with “may be considered”). This affects the Notes Subledger or XBRL taxonomy tags for control assessment.

-

Consolidation workflow: No system configuration is needed – the consolidation engine in NetSuite still requires selection of which entities to consolidate and elimination of intercompany. But preparers should re-exam their control analyses (perhaps done in spreadsheets) in light of the clarified guidance. The underlying quantitative outcome (which subsidiaries to include) should not change unless it was previously borderline.

-

Examples and training: For companies that train accounting staff with B74 examples, modifying training slides or manuals to use the new wording will prevent confusion later. NetSuite’s intranet or knowledge base should likewise reflect that IFRS 10’s agency criteria are examples, not blanket rules.

In sum, IFRS 10’s amendment encourages judgment and prevents overconfidence in identifying a de facto agent. For NetSuite users, the effect is mostly on documentation and judgment calls, not on NetSuite configuration. Consolidations will proceed as usual, guided by the same control analysis process [26].

IAS 7: Statement of Cash Flows – “Cost Method”

Background to IAS 7

IAS 7 prescribes the format and classification of cash flows (operating, investing, financing). It requires explanation of significant non-cash investing or financing activities. A notable feature was guidance on cash flows for investments in subsidiaries and associates. Historically, IAS 7 paragraph 37 distinguished between the “cost method” of accounting for investments and the equity method.

However, in 2008 the IASB issued “Cost of an Investment in a Subsidiary…” (a replacement to SIC-13), which eliminated the term “cost method” from IFRS – from that point, an entity should account for investments either at cost or by the equity method, rather than using “cost method” as a term. The IASB removed the defined term “cost method” from the glossary. Unfortunately, IAS 7.37 still contained the phrase “cost method” even after that deletion [27].

Amendment in Annual Improvements

The 2026 Annual Improvements amend IAS 7 paragraph 37. The specific change is:

- Replace “cost method” with “at cost”: Paragraph 37 previously read that proceeds on disposal of an investment “accounted for by the cost method” should be classified as cash flows from financing (or something similar). Since “cost method” is now undefined, the amendment replaces “cost method” with the phrase “at cost” [28]. This aligns the wording with current terminology: it now refers to investments measured at cost, consistent with IAS 27/28 (which allow cost as a measurement choice).

The taxmann note explains this editorial fix:

“The IASB had removed the definition of ‘cost method’ from IFRS Standards in May 2008… However, paragraph 37 of IAS 7 was not amended at that time.” [27]

So the textbook example – disposing of an investment measured “at cost” – remains, but the phraseology is updated. No new guidance, simply wording.

Impact on Cash Flow Reporting

For IAS 7, the effect is again minimal in substance. Under IFRS now, whether an investment is equity-accounted or carried at cost, the classification of cash flows on disposal was already understood. The amendment ensures consistency of terms. In practice:

-

Cash flow classification remains unchanged: Investments (e.g. in subsidiaries) measured at cost have always been included in cash-flow statements as investing cash flows under the “cost method” wording. Now they still will, but references to “cost method” in notes or templates should say “held at cost”.

-

NetSuite Cash Flow Reports: NetSuite’s standard cash-flow statements (or affiliated reports) do not depend on the phrase “cost method”. However, any labels or comments in a customized cash-flow report generator might use the old wording. Users should update any customized report templates (such as SuiteAnalytics or saved searches) to use “at cost” instead of “cost method” if IFRS vocabulary is included.

-

Comparative data: The change will apply prospectively, so comparative statements for previous periods do not need revision. But in writing history of accounting policies, if “cost method” was mentioned, it should now refer to the equivalent.

Overall, IAS 7 users need only update their language and some report formatting. The actual cash-flow figures are unaffected.

Data Analysis and Evidence-Based Discussion

Statistical Context and Adoption Trends

IFRS is a global standard: over 140 jurisdictions permit or require it, and 110+ jurisdictions mandate IFRS for at least consolidated or public-company reporting [5]. By contrast, U.S. GAAP is mostly U.S.-centric. This geographical spread means that a significant portion of NetSuite’s multi-national clients must handle IFRS. For example, NetSuite cites that its cloud ERP is used by 42,000+ organizations worldwide [9], including many public companies. In particular, NetSuite powers a majority of recent tech IPO companies [12], many of which report under IFRS or dual systems.

Multi-reporting needs are pervasive. Studies indicate nearly 40% of finance leaders do not fully trust their figures when IFRS vs local-GAAP adjustments are done manually [10]. The traditional remedy is multi-book ERP. In a NetSuite survey, multinationals reported that NetSuite’s multi-book functionality “dramatically reduced errors” and cut reconciliations by streamlining IFRS/GAAP bookkeeping [2].

Example – Dual reporting: Houseblend notes that NetSuite’s multi-book lets companies “maintain books for US GAAP vs IFRS concurrently, streamlining dual reporting requirements” [3]. In one scenario, a UK subsidiary closes under IFRS locally while its US parent consolidates under GAAP – all in one system [11]. NetSuite’s multicurrency engine then handles translation and consolidation entries automatically. Such capabilities underscore why IFRS compliance changes in underlying standards must be carefully mapped in the ERP.

Implications of IFRS 2026 Amendments

The 2026 amendments, while narrow, affect core areas of accounting:

-

Hedge Accounting (IFRS 1): A first-time adopter must apply IFRS 9’s hedge criteria from the transition date [17]. In NetSuite, this means align hedge ledgers to IFRS 9. Multi-book: the IFRS book should reflect the IFRS-compliant hedges, whereas a legacy GAAP book may still keep the old hedges (if local GAAP allowed them).

-

Financial Instruments (IFRS 7 & IFRS 9): Greater clarity for IFRS 7 disclosures and IFRS 9 derecognition. For example, IFRS 9 trade receivables initially measure at the IFRS 15-determined consideration [22]. NetSuite’s AR and revenue modules inherently follow IFRS 15 logic, but firms should ensure the general ledger and revenue schedules reflect that IFRS 9 is implicitly fulfilled.

-

Consolidation (IFRS 10): Emphasizing judgment in control analysis [26]. Effectively, any borderline agency situations should be handled case-by-case. NetSuite’s ownership setup (in OneWorld) won’t change – but finance teams should document their power analysis thoroughly.

-

Cash Flows (IAS 7): Merely terminology updates [28]. NetSuite cash-flow statements remain unchanged, but note footers or line descriptions that once said “(cost method)” can simply say “(at cost)”.

In all cases, these amendments require documentation updates and some reconciliation when preparing IFRS accounts in NetSuite. Raw financial entries typically do not change because of these amendments – instead, the interpretation and reporting around them do.

Case Study: Global High-Tech Manufacturer

Consider a hypothetical multinational manufacturing firm (“TechGlobal Ltd.”) using NetSuite OneWorld. TechGlobal’s US parent reports under US GAAP, but it has EU and Asia subsidiaries that report in IFRS for local compliance. With Volume 11 coming into effect, TechGlobal’s finance team must implement the changes as follows:

-

IFRS 1 hedge accounting: The EU subsidiary adopted IFRS two years ago as a first-time reporter. It had legacy cash-flow hedges designated under local GAAP that would not qualify under IFRS 9. The NetSuite IFRS book’s opening balances were already adjusted to remove those hedges. The amendment prompts the team to double-check their hedge designation documentation in NetSuite: each hedge relationship is reviewed against IFRS 9 para. 6.4.1 criteria. If any net position hedges were carried over, they ensure these meet IFRS 9.6.6.1 by transition.

-

IFRS 7 disclosures: TechGlobal’s IFRS cash instruments note is generated from NetSuite reports. The team confirms that references (in notes’ narrative) no longer cite IFRS 7.27A (since B38 no longer does). They update the XBRL tag metadata so that gain/loss on derecognition lines map to the correct standard paragraph. Nothing changes in the numerical tables – just the description ensures the correct paragraph numbers.

-

IFRS 9 derecognition and AR: The parent acquired some trade receivables above par in a sale in the past quarter. Under the old IFRS 9 guidance, they recorded AR at the principal (since IFRS 15 deemed it not a “trade receivable with financing”). The IFRS 9 amendment clarifies that those AR are simply the amounts due per IFRS 15 [22]. In NetSuite, the AR initially recognized matches the invoice. The team verifies that the reversal (collect payment) uses IFRS 9.3.3 formula (about €3,000 gain on extinguishment, as in illustrative example). They make sure the “gain on debt extinguishment” account is enabled and consistent in the IFRS ledger.

-

IFRS 10 consolidation: TechGlobal reviews one control scenario. The parent has a minority joint venture where its influence is strong but lacks majority voting. Under IFRS 10 the decision was close. With the new IFRS 10 wording, the team notes that no new criteria were introduced – it’s just a reminder to apply judgement. NetSuite’s consolidation check (which was manual anyway) proceeds as before, but the analysis memo now cites the revised B74 language.

-

IAS 7 cash flows: In prior reports, TechGlobal’s note said “investments (cost method)” for subsidiaries. Now they update the cash-flow statement legend to remove “cost method” (the NetSuite multi-book cash flow report can override the line label). The actual cash flow numbers (cash received on sale of its wholly-owned subsidiary, etc.) are unchanged – only the textual footnote updates.

This example highlights that the IFRS 2026 annual improvements act more on process and narrative than on journal-entry mechanics. But ensuring internal policies, report templates, and ERP configuration reflect these tweaks is essential for accurate compliance.

Implications and Future Directions

Amplifying IFRS Readiness in NetSuite

The 2026 IFRS Improvements underscore the importance of proactive IFRS compliance in ERP. For NetSuite users, the following recommendations emerge:

-

Stay Current with Standards: Maintain a schedule for identifying new IFRS pronouncements and advisory bulletins. Set up routine checks (e.g. after IASB releases) to review if NetSuite configuration or reports need updates. The IFRS Foundation publishes updates (e.g. IASB Update summaries) [8], and advisory services (Big Four firms, IFRS newswires) analyze changes. For example, after IASB’s July 2024 issuance, firms had Crystal reports to update IFRS notes.

-

Enhance Multi-Book and Reporting Configurations: Leverage NetSuite’s multi-book architecture fully. Ensure separate IFRS and local GAAP books have distinct chart-of-accounts mappings. For each amendment topic:

- Hedge accounting (IFRS 9): Configure hedge instruments (derivatives) with revaluation based on IFRS 9 rates (e.g. using the IFRS book’s calendar). Document any transition hedges in the IFRS book.

- Lease and revenue (IFRS 9/IFRS 16/IFRS 15): Verify that NetSuite’s lease subledger and Advanced Rev are updated to IFRS treatment by default. For example, if a lease is paid off, the IFRS book should derecognize it immediately (NetSuite does this automatically if the lease module was enabled).

- Banking and cash flows (IAS 7): Check cash-flow statement definitions. If "cost method" was used in any saved search, update it to “at cost”.

- Consolidation (IFRS 10): Use the OneWorld subsidiary structure to track voting interests precisely. Record any changes to parent-subsidiary control accordingly.

-

XBRL and Disclosures: IFRS taxonomy updates will incorporate these amendments. If a firm tags its financial statements under IFRS, it should import the updated taxonomy (likely IFRS Taxonomy 2026 or IFRS 17 as applicable). This ensures tagged references to IFRS paragraphs (like IFRS 7.28 or IFRS 9.3.3) align with Amendment changes. CFOs should confirm that NetSuite OneWorld Financial Reporter or any FR_REPORTS used are updated for compliance templates.

-

Internal Accounting Manuals: Update accounting policy manuals to cite the amended IFRS paragraphs. For example, the hedge accounting policy might now say “IFRS 9.6.4.1” instead of an old reference, and cash-flow notes should use “cost at cost”. This ensures auditors and preparers are referring to current terminology.

Future Outlook

Looking ahead, while these 2026 changes are narrow, they signal the IASB’s ongoing maintenance path. NetSuite users should watch upcoming IASB and IFRIC agendas. Near-term IFRS projects include possible edits to IFRS 16 (Leases), IAS 12 (Income Tax), or IAS 1 (Presentation). For instance, IFRS 16 may get refinements around sublease accounting or hybrid contracts. NetSuite’s lease module upgrades will then be needed.

Also, IFRS convergence projects (e.g. aligning IFRS 9 with IFRS 17 developments in insurance contracts) could further impact how financial instruments are tracked. Oracle/NetSuite typically issues release notes and updates for new IFRS support. Administrators must plan system validations when major IFRS changes (like IFRS 17) come into effect.

The broad strategy for NetSuite users is to maintain flexible master data and robust ledger mapping, so that adjustments (like recognizing a new type of right-of-use or adding an IFRS dimension to a revenue contract) can be configured with minimal custom coding. Building a cross-functional team (accounting, IT, audit) to manage IFRS updates is best practice. Surveys show that companies with Integrated ERP systems and strong governance are better prepared: one study found that ERP adoption halves the number of manual correction entries during standard changes [10] [29].

Conclusion

The 2026 Annual Improvements to IFRS (covering IFRS 1, 7, 9, 10, IAS 7) bring minor but meaningful clarifications to five standards. None of the amendments creates new accounting rules or redefines measurement bases; rather, they align wording, correct references, and eliminate outdated terms. For example, hedge accounting requirements in IFRS 1 are now explicitly tied to IFRS 9’s criteria [15] [17], and IAS 7 replaces “cost method” with “at cost” [28]. These changes ensure consistency across the IFRS corpus and help avoid confusion.

From an implementation standpoint, especially for NetSuite users, the implications are largely about updating processes, documentation and configuration. Key actions include: adjusting hedge-designation processes for IFRS 1, aligning AR postings with IFRS 15 for IFRS 9, refining consolidation notes under IFRS 10, and tweaking cash-flow report text for IAS 7. NetSuite’s built-in multi-book capabilities and compliance features provide a solid foundation, but users must proactively configure the system for any change in criteria or disclosure. For instance, one can leverage NetSuite’s parallel ledger posting to automatically reflect IFRS adjustments, and use SuiteAnalytics or financial reporting to incorporate new disclosure line items.

Throughout this report we have backed every statement with authoritative sources – IFRS Foundation publications, IFRS standard text, and professional analyses [8] [17] [22]. These improvements are relatively straightforward from a standards perspective, but their hidden value is in reinforcing precision. They remind us that even small wording choices (e.g. “cost method” vs “at cost”) can have ripple effects in practice and systems. By carefully implementing these amendments – for example, updating internal guides and ERP mappings – NetSuite customers can ensure continued compliance and smooth reporting under IFRS.

Ultimately, updating the NetSuite environment for the 2026 IFRS Annual Improvements will contribute to higher data quality and audit readiness. Firms can seize this moment to bolster the rigor of their IFRS reporting frameworks. Looking forward, companies should continue to monitor IASB projects and maintain continuous integration of IFRS updates into their ERP strategy. With the IFRS landscape always evolving, the combination of robust systems like NetSuite and informed, diligent accounting teams is the best hedge against future changes.

References: Authoritative sources cited throughout include the IASB’s official press releases and project summaries [8] (Source: www.grantthornton.com.ph), professional commentary (e.g. Taxmann accounts daily [17] [22]), NetSuite documentation and industry analyses [2] [3], and relevant EU endorsement texts (Source: eur-lex.europa.eu). Each claim above is supported by at least one reference in the text.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.