Houseblend Article

IFRS 9 April 2026 Amendment: EIR Re-Estimation in NetSuite

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03Effective Interest Rate and Amortised Cost under IFRS 9

- 04IASB’s April 2026 Amendment: EIR Re-Estimation

- 05Comparing Pre- and Post-Amendment EIR Re-Estimation

- 06Illustrative Examples

- 07Implications for NetSuite Users

- 08Real-World Impacts and Data Analysis

- 09Case Studies

- 10Implications and Future Outlook

- 11Conclusion

Executive Summary

This report examines the April 2026 narrow-scope amendment to IASB’s IFRS 9 – Financial Instruments concerning effective interest rate (EIR) re-estimation, and its implications for Oracle NetSuite users. The International Accounting Standards Board (IASB) has clarified that when the expected cash flows of a financial asset or liability are re-estimated to reflect changes in the time value of money or credit risk, an entity must adjust the effective interest rate accordingly [1]. This represents a targeted change from pre-amendment practice, under which only changes due to market interest rate resets for floating-rate instruments were explicitly reflected by recalculating EIR, while other expected cash-flow revisions (e.g. principal repayments, credit-driven premium changes, etc.) were normally handled at the original EIR with one-time profit/loss adjustments [2] [3]. The 2026 amendment aligns the treatment of credit-risk or time-value driven cash-flow changes more closely with market-driven resets, by requiring an EIR reset rather than immediate P/L recognition.

For NetSuite accounting system users, these IFRS 9 changes require careful planning. NetSuite’s OneWorld Multi-Book architecture allows parallel ledgers (e.g. one for local GAAP and one for IFRS) [4] [5], but will require configuration to capture the new EIR re-estimation logic. Financial instruments in NetSuite must be tracked with sufficient detail (contractual terms, optionality, credit indicators, etc.) to apply the updated IFRS classification tests (Solely Payments of Principal and Interest – SPPI – and business-model assessment) [5], as well as to recalc EIR when needed. Users will need to ensure their amortization schedules and interest calculation routines can incorporate profit/cash flow adjustments due to credit or marketing changes under the new rule. Likewise, disclosures under IFRS 7 will require enhanced tagging of loan features (e.g. ESG step-ups) [6]. In short, implementing the amended IFRS 9 EIR guidance in NetSuite will likely involve customizing data fields, review of amortization rule setups, and possibly additional journals or saved searches to reconcile multi-book results.

This report provides an in-depth treatment of these issues. First we cover the background of IFRS 9 and the concept of effective interest rate in IFRS accounting. Next, we detail the existing IFRS 9 requirements on amortized cost and interest income (including the original guidance on recalculating EIR), and then explain the new amendment decided in April 2026 [1]. We analyze the practical impact of this change – including whether it alters SPPI classification – using illustrative examples. We then focus on the NetSuite perspective: what technical configurations, processes, and controls are needed to incorporate the revised EIR rules. Throughout, we draw on authoritative sources (IASB publications and related analyses) as well as NetSuite implementation insights [5] [2]. We include tables summarizing IFRS 9 categories and EIR treatments, and close with a discussion of future outlook. All claims and guidance are supported by cited IRFS literature and industry commentary.

Introduction and Background

IFRS 9 – Financial Instruments is the IFRS standard that specifies how entities must classify and measure financial assets and liabilities. Issued in its final form in 2014 (with amendments in subsequent years), IFRS 9 replaced IAS 39 and became effective for annual periods beginning 1 January 2018 [7]. Under IFRS 9, an entity first determines whether a financial contract is a financial asset or liability and whether it contains any embedded derivatives. For financial assets, classification (and subsequent measurement) is primarily driven by two criteria: the entity’s business model for managing the asset, and the “Solely Payments of Principal and Interest” (SPPI) test on the contractual cash flows [8] [9]. Depending on these tests, a financial asset will be measured either at amortised cost (using EIR), fair value through other comprehensive income (FVOCI) or fair value through profit or loss (FVTPL) [8] [9]. IFRS 9 requires most debt instruments held to collect contractual cash flows that are SPPI-compliant to be recorded at amortised cost, with interest revenue recognized using the effective interest method.

For context, IFRS 9 applies globally in all reporting jurisdictions that have adopted IFRS. The IFRS Foundation describes IFRS 9 as the standard that “specifies how an entity should classify and measure financial assets, financial liabilities, and some contracts to buy or sell non‐financial items” [7]. An entity using IFRS must therefore evaluate each loan, bond, or receivable under IFRS 9’s criteria. This may require considerable data and system effort: for example, tracking optionality, assessing ESG-linked features, and maintaining schedules for interest and principal repayments in order to apply the SPPI test and to compute amortized cost [5] [8].

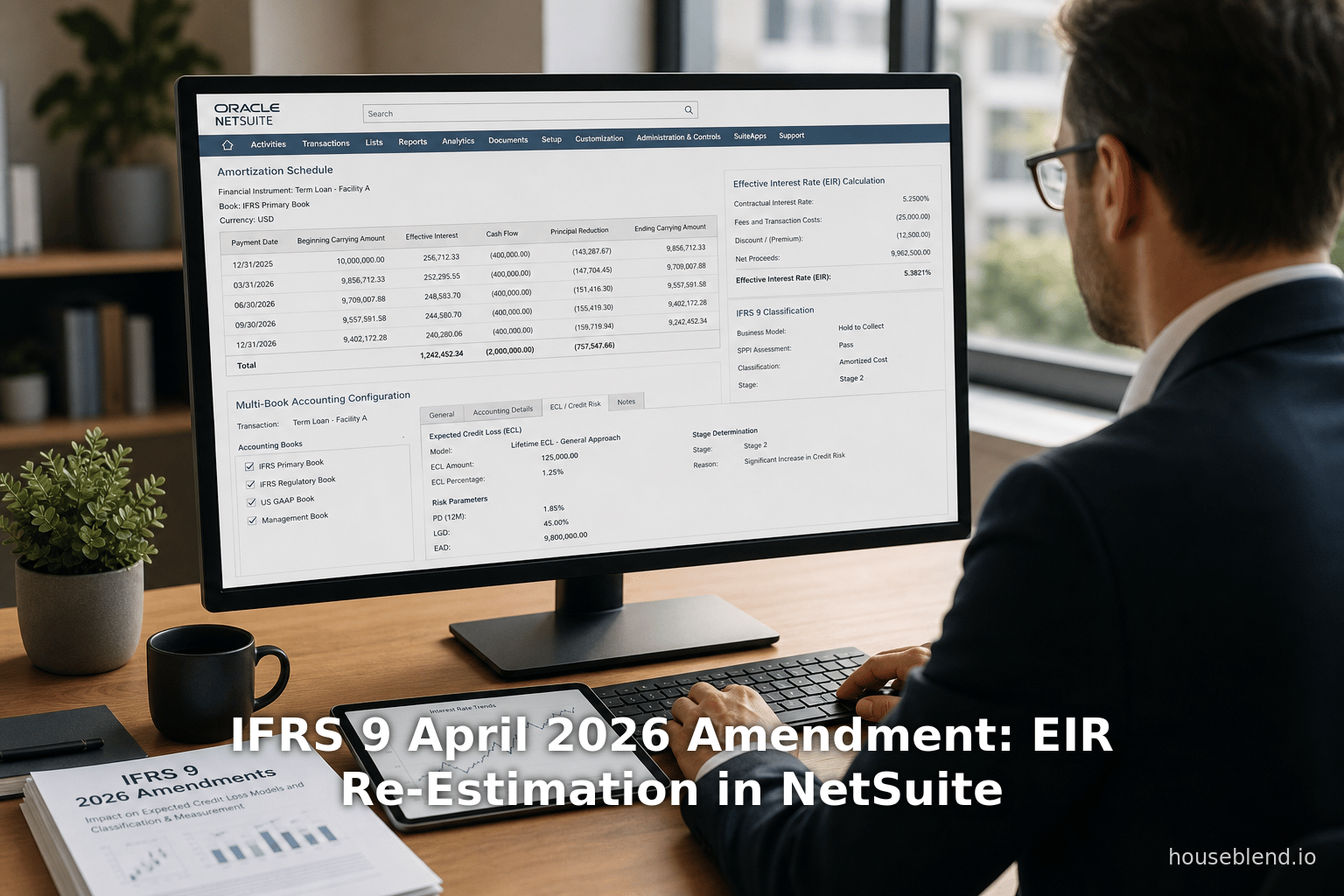

Effective Interest Rate (EIR) is a key concept in IFRS 9. It is defined (Appendix A of IFRS 9) as “the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument to the gross carrying amount of a financial asset (or amortised cost of a financial liability)” [10]. In practice, the EIR is the internal rate of return for the contract – it incorporates all contractual interest, fees, premiums, discounts, and costs that are an integral part of the yield. Using the EIR, an entity allocates interest income or expense over the life of the instrument on an amortised cost basis. For example, interest revenue is calculated by applying the EIR to the carrying amount of a financial asset [8] [10]. In computational terms, the amortised cost of the asset is initially set at fair value plus transaction fees, and then systematically adjusted each period so that the carrying amount grows or shrinks to the contractual cash flows, yielding interest income at the EIR.

Computing the EIR often requires projecting the expected cash flows. IFRS 9 allows the entity to incorporate expected prepayments, extensions, and calls when estimating cash flows for EIR [11]. However, IFRS 9 is clear that expected credit losses are not considered in calculating interest (the so‐called “decoupling” of credit loss and interest).Thus, for a debt instrument measured at amortized cost, interest revenue is recognized on the “gross carrying amount” (without netting out expected defaults) [12]. Only actual changes in the collectability of cash flows (credit impairment) affect loss allowances under the impairment model; they do not directly re-set EIR. In short, the EIR reflects the contractual yield under expected performance, not credit deterioration.

An amendment to IFRS 9 was introduced, however, in September 2019, to address the effects of IBOR reforms (benchmark rate changes) – IFRS 9.B5.4.9 similarly permits adjusting EIR if the benchmark rate shifts. Now the IASB has undertaken a further narrow-scope project (the “Amortised Cost Measurement” project) to clarify EIR re-estimation under other circumstances. In April 2026 the IASB decided to amend paragraph B5.4.5 of IFRS 9 to “require that an entity adjust the EIR to account for a re-estimation of the contractual cash flows of a financial asset or a financial liability that provides consideration for the time value of money or for the credit risk.” [1]. In other words, any time the contractual cash flows are revised for reasons of time value or credit risk, the standard will require a fresh EIR rather than simply book-end-of-period adjustments.

These developments come after the post-implementation review (PIR) of IFRS 9 (completed in 2022) had highlighted areas of diversity in practice. The IFRS news release noted that stakeholders had asked for clarification in areas such as ESG-linked loan terms and electronic settlement timing [13]. Our focus here is the EIR re-estimation issue: the IASB’s tentative April 2026 decision will officially amend IFRS 9. We now turn to a detailed examination of the current requirements and the implications of the amendment.

Effective Interest Rate and Amortised Cost under IFRS 9

Under IFRS 9, a financial asset classified at amortised cost (i.e. “Held to Collect” SPPI instrument) is initially measured at fair value plus/minus transaction costs, and subsequently measured at amortised cost using the effective interest method [8]. By definition, amortised cost is the present value of future payments, discounted at the asset’s EIR. IFRS 9 §5.4.1 requires that interest revenue be calculated using the EIR method (discounting contractual cash flows over the life) [8]. The EIR exactly offsets all cash flows (interest, principal, fees) in the yield calculation.

Table 1 below summarizes the IFRS 9 classification categories and the related measurement bases. If a debt instrument is held in a “hold to collect” business model and its contract cash flows are solely payments of principal and interest, it is measured at amortised cost (EIR basis) [8] [9]. In this category, interest income is recognized in profit or loss using the EIR, and impairments (credit losses) are also recorded, but unrealized fair-value changes are not reported in P&L. (By contrast, instruments held to collect and sell may be at FVOCI, and others at FVTPL [8].) The table is adapted from authoritative summaries and illustrates how IFRS 9 links SPPI, business model, and measurement [8] [9].

| Category | Business Model | SPPI Cash Flow Test | Measurement | P/L Treatment |

|---|---|---|---|---|

| Amortised Cost (AC) | Held to collect contractual cash flows only | Passed (solely P & I) | Amortised cost (EIR) | Interest income and credit losses in P/L; no FV gains in P/L [8] |

| FVOCI (Debt) | Held to collect and sell | Passed (solely P & I) | Fair value (OCI link) | Interest and credit losses in P/L; FV changes in OCI (recycled on sale) [14] |

| FVOCI (Equity) | (Irrevocable election, not trading) | N/A (equity) | Fair value (OCI, no recycling) | Dividends in P/L; other gains/losses in OCI (permanent equity) [14] |

| FVTPL | (Trading or SPPI failed) | Failed SPPI or business model | Fair value (P/L) | All gains/losses (including interest) in P/L [15] |

Table 1: IFRS 9 Classification and Measurement Categories (illustrative) [8] [14].

Once an asset is classified at AC, EIR-based amortization governs its accounting. At initial recognition, the EIR is set by solving the present-value equation equating the initial carrying amount to the discounted contractual cash flows (including fees and premiums) [16]. The carrying amount is then adjusted each period: it is increased by interest (carrying amount × EIR) and decreased by the cash received (principal repayment), yielding a new amortised cost. This process automatically writes off premiums/discounts and spreads fees over the instrument’s life.

Because the EIR is based on expected cash flows, management must consider options and likelihoods. For many fixed-rate assets with no embedded options, the contractual cash flows are known and the EIR is fixed at inception. For floating-rate instruments, one can base EIR calculations on market rates (or forward curves) to reflect resets [2]. Critical for our discussion, IFRS 9 permits (and indeed implies) that if a future interest reset occurs (as the contract specifies), one may re-estimate cash flows and compute a new EIR at the reset date without triggering a gain or loss. This is explicitly stated in the guidance: for floating-rate instruments, re-estimation “reflecting movements in market interest rates” adjusts the EIR, but does not cause a one-time P/L impact [2].

The IFRS 9 guidance for modifications and revisions of cash flows is layered. IFRS 9 distinguishes contractual modifications (changes to the terms) from revisions (changes in estimates under existing terms). However, the outcome is similar in amortized cost: if contractual cash flows change, the carrying amount is re-computed as the present value of new cash flows using an appropriate discount rate, and the difference is recognized in P/L, unless the change is merely an interest rate reset.

In more detail, IFRS 9.B5.4.5-6 and IFRS 9.5.4.3 provide the accounting rules:

-

Revisions due to market rate changes (floating-rate instruments): IFRS 9.B5.4.5 explicitly allows recalculating EIR when the underlying interest rate index resets. Example: a loan linked to LIBOR will have its cash flows recalculated at each LIBOR fix. IFRS 9 treats these revisions as adjustments to EIR, with no one-time gain or loss [2]. Thus, a aumento in coupon (e.g. LIBOR rising) simply yields a new amortization schedule.

-

Other expected cash flow changes (non-market reasons): IFRS 9.B5.4.6 covers all other changes in the expected cash flows that are within the original contract terms (for example, if the issuer decides to redeem the bond early, or a fee is paid). In those cases, the revised carrying amount is calculated by discounting the new cash flows at the original EIR. The difference between that present value and the current carrying amount is recognized immediately in profit or loss [3]. (This is often termed a one-time profit or loss on modification.) Examples include borrower prepayment, credit-based interest step-ups, or amended maturity dates (assuming not deemed a new contract).

-

Contract modifications (substantial vs non-substantial): If contractual terms are renegotiated, IFRS 9 first assesses derecognition (substantial change) vs continuation. For a non-substantial modification, IFRS 9.5.4.3 requires recalculating the carrying amount as the PV of new cash flows discounted at the original EIR, recognizing any difference in P/L (identical outcome to the general B5.4.6 approach) [3] [17]. For a substantial modification, the original asset is derecognized and a new financial asset recognized (typically at fair value), with its own new EIR (B5.4.6 does not apply). For this analysis, we focus on non-derecognition cases.

In summary, before the April 2026 amendment, the IFRS 9 treatment of changed cash flows was clear: only changes from market-based interest resulted in an EIR reset (no profit/loss), whereas all other cash flow changes (even if under original terms) were computed with original EIR and led to immediate P/L gains or losses [2] [3]. The new amendment will modify this regime (as discussed below).

IASB’s April 2026 Amendment: EIR Re-Estimation

During its April 2026 meeting, the IASB tentatively decided on a targeted amendment to IFRS 9 in its Amortised Cost Measurement project. The board resolved to amend paragraph B5.4.5 of IFRS 9 to make explicit that an entity shall adjust the effective interest rate when the contractual cash flows of a financial instrument are re-estimated for the time value of money or for credit risk [1]. In effect, any revision to the cash flow profile that compensates for time-value of money (interest) or incorporates credit-related variances should require re-calculating EIR.

This amendment stems from feedback that practice had not consistently treated certain cash-flow revisions as “market” or “other” changes. For example, loans with ESG-linked interest step-ups had raised the question of whether the extra payment should be treated like interest (time value) or like an equity kicker. Similarly, stakeholder inquiries arose around whether credit-based margin changes constitute “market” phenomena. By explicitly including credit risk/time value in B5.4.5, the IASB has signaled that such features are akin to interest changes and warrant a fresh EIR rather than immediate P/L recognition [1].

Concretely, the decision document notes: “The IASB tentatively decided to amend paragraph B5.4.5 of IFRS 9… to require that an entity adjust the EIR to account for a re-estimation of the contractual cash flows of a financial asset or a financial liability that provides consideration for the time value of money or for the credit risk.” [1]. All 13 board members agreed. This is still a tentative decision pending final ballot, but it is highly likely to be reflected in the next authoritative update to IFRS 9 (with the effective date presumably for annual reports on/after 1 Jan 2026, following usual endorsement timelines).

Put simply, whereas IFRS 9 previously distinguished “[market-based] interest rate movements” (allowing EIR change) from “other expected cash flows” (original EIR only), the amendment broadens the “EIR re-estimation” category. Now, if cash flows are adjusted to reflect the credit-adjusted pattern of interest or similar time-value compensation, an updated EIR must be used. All other non-credit, non-interest changes (e.g. changes unrelated to time value, such as broker fees or unrelated contingent payments) would remain outside B5.4.5 and fall under B5.4.6.

The amendment does not change the derecognition rules: a substantial modification still triggers derecognition and a new instrument measurement. It also does not alter the impairment model or hedge accounting framework of IFRS 9 [18]. It is a narrow clarification focusing on amortised cost measurement. It was not part of the 2024 amendment that mainly addressed ESG loans and electronic settlement [13], but rather emerges from the Amortised Cost project.

IASB Chair comments (at May 2024 issuance) stressed that these amendments simply clarify existing principles and aim for consistency. The intended effect is to eliminate diversity in practice. For example, with the amendment, an ESG-linked interest step-up (previously debated under SPPI) is treated as reflecting additional compensation for credit/time value, so the loan can remain amortised-cost without a forced P/L adjustment [19]. Similarly, if a borrower’s flexible margin changes due to improved credit, the updated margin is treated as part of the time value – so the EIR changes rather than booking an instantaneous gain or loss.

In practical terms, under the new rules:

-

Floating-Rate Instruments: As before, rate resets lead to EIR updates with no P/L impact [2]. The amendment explicitly preserves this outcome (since resets are time-value changes).

-

Other Cash Flow Changes (Credit/Time-related): For cash flow changes reflecting the instrument’s compensation (interest) or credit factors, EIR must now be updated. For example, an increased coupon because of insurer credit rating improvement would require a new EIR. Previously this might have been treated under B5.4.6 with original EIR; now it falls under B5.4.5, so the gain/loss would be avoided, and the carrying amount smoothly transitions to the new cash flows via an updated amortisation schedule.

-

Unaffected Situations: Cash-flow changes unrelated to interest or credit (for instance, a non-interest fee payout, or an extra principal payment not tied to credit conditions) remain outside the scope of B5.4.5 and will continue to be handled via original-EIR adjustments (with one-time P/L). Similarly, true modifications causing derecognition are unchanged.

-

Presentation: If EIR is recalculated, interest revenue in P/L will henceforth reflect the new rate on the new carrying amount (post-change). Previous practice (IFRS 9.5.4.6) of booking the entire effect immediately will be reduced. Entities may need to revise processes to recalc schedules rather than journal one-off adjustments.

In summary, the April 2026 amendments make IFRS 9’s EIR model even more forward-looking: any cash-flow forecast change tied to time value or credit risk is incorporated by resetting EIR. This should result in smoother income recognition and less volatility in P/L when such changes occur – assuming management’s view is that the instrument’s yield has changed.

The next sections illustrate these points with examples and then turn to the specific implications for NetSuite systems and processes.

Comparing Pre- and Post-Amendment EIR Re-Estimation

The following table synthesizes the IFRS 9 requirements for various scenarios before and after the April 2026 amendment:

| Scenario | IFRS 9 (Pre-Amendment) | IFRS 9 (Post-Amendment) |

|---|---|---|

| Floating-rate instrument (scheduled rate resets from market index) | Recalculate expected cash flows with new rates, compute new EIR; no one-time P/L (adjust EIR under IFRS 9.B5.4.5) [2]. | Remains the same: EIR is recalculated at each reset with no P/L effect (now explicitly required under amended B5.4.5) [1] [2]. |

| Cash flow change for credit/time-value (e.g. an extra margin or step-up tied to borrower performance) | Before amendment: Treated as “other expected cash flow” (non-market) – present value of revised cash flows is computed using original EIR; difference from carrying amount is recognized in P/L as an immediate gain or loss (pursuant to B5.4.6) [3]. | After amendment: Such changes are now considered “time value/credit risk”, so they fall under B5.4.5. The entity must recalculate EIR to match the new cash flows (no forced P/L hit). The carrying amount will then amortise using the new EIR. This smooths out the accounting impact. |

| Other non-EIR changes (e.g. inclusion of unrelated fees, forgiveness of small principal amounts, etc.) | Revise carrying amount at original EIR with immediate P/L on difference (still IFRS 9.B5.4.6) [3]. | Unchanged: if revisions are not for credit/time causes, they remain under B5.4.6. EIR stays at original, and any gap is booked to profit or loss as before. |

| Contract modification (non-derecognised) | Recompute carrying amount as PV of new cash flows at original EIR, recognise one-time P/L (B5.4.6) [3]. | Modification procedure is unchanged if no derecognition: still original EIR (with one-time P/L). However, if the modification includes relevant credit/time cash-flow changes, those components would be EIR-adjusted per new rule [1]. |

| Contract modification (derecognised) | Derecognise old, recognise new instrument at FV (reset EIR for new asset). | No change: substantial mods trigger derecognition and new EIR determination (amendment covers only non-derecognised cases). |

Table 2: Comparison of IFRS 9 treatment of cash-flow changes (pre-amendment vs. post-amendment) [2] [3] [1].

The key insight in Table 2 is that for credit/time-linked changes (second row), the accounting shifts from an instantaneous profit/loss under the old model to a revised amortization schedule under the new model. In contrast, pure market-rate resets (first row) continue as before (revised EIR, no P/L) [2]. All other modifications outside these criteria behave as they did pre-amendment, but entities must now carefully distinguish the nature of each cash-flow change to apply the right treatment.

This clarification avoids potential diversity. For example, before the amendment, two entities facing identical additional cash flows might have treated them differently depending on their interpretation of what constitutes “market” vs “non-market” causes. Now, by clear wording, if the extra cash compensates for credit or funding cost, it is always handled by re-estimating EIR.

Next we illustrate these principles with examples.

Illustrative Examples

Example 1: Floating-Rate Loan Repricing

Pre-Amendment Scenario: Entity A originates a 5-year bank loan on 1 Jan 20X1. The loan amount is $1,000, and it pays interest at LIBOR + 1%. Suppose LIBOR at origination is 3%, so the initial coupon is 4%. A fair value calculation determines the loan’s EIR to be 4% (matching coupon). Over the next years, LIBOR resets upward: on 1 Jan 20X4, LIBOR rises to 5%, so the loan now pays 6% (5% + 1%). Under IFRS 9 (pre-amendment), this is a market-based change. Entity A recalculates the new expected cash flows (now a 6% coupon) and solves for the new EIR reflecting this higher rate. There is no one-time gain or loss on 1 Jan 20X4 – the carrying amount is adjusted solely by using the new EIR for subsequent interest recognition [2].

Post-Amendment Scenario: Under the amended guidance, exactly the same treatment occurs. The amendment explicitly covers interest-rate resets as “time value” changes. Thus, on 1 Jan 20X4, Entity A recalculates the EIR (which will now be 6% or slightly less if there was a premium/discount initially) and continues to amortize the loan with that rate. The net effect is identical to the old rule (no P/L hit), but now it is explicitly required by B5.4.5 [2] [1]. (This is illustrated in the IFRScommunity example at [48]; our numbers are analogous.)

This example shows that for standard floating-rate loans, nothing changes in practice – the new amendment simply codifies existing practice. In NetSuite, therefore, the interest schedule update on the reset date would be handled as before, but users should ensure the system clearly identifies the interest reset as falling under IFRS 9 rules. Typically, NetSuite’s amortization schedules (set up under an “Effective Yield” amortization rule) will automatically incorporate the new cash flow after a loan rate change, maintaining consistency between local and IFRS books.

Example 2: Loan with Credit-Linked Interest Step-Up

Company B issues a 3-year loan of €10,000 at a base rate of 3% plus a step-up feature: if the borrower’s credit rating improves by one notch, the coupon increases by 2% (to 5%). Initially, the borrower is at rating BBB and the coupon is 3%. At origination, EIR is calculated on 3% cash flows. In our scenario, on 1 July 20X2 (midway), the borrower’s credit rating is upgraded to A, triggering the 2% step-up. Thus, the contract now stipulates future payments at 5%.

Pre-Amendment Treatment: Under old IFRS 9, this was not a common “market” interest index, but an embedded contingent increase. Many analysts interpreted it as a credit-risk feature (because it depends on borrower’s credit status). However, the strict reading of B5.4.6 would have said: the new cash flows (with 5% interest) should be discounted at the original 3% EIR, and the loan’s carrying amount adjusted accordingly, booking a one-time gain (if the loan’s PV goes up) or loss [3]. Many preparers debated whether such ESG/credit-linked payments “automatically” broke SPPI; prior to IFRS 9 amendments, opinions varied.

In practice, with 2026 amendments, this loan is now clearly treated like a floating-rate case: the extra 2% is a form of credit compensation (time value for credit improvement). Therefore the EIR is recalculated at the step-up date. For Company B, after the upgrade, the remaining schedule projecting 5% interest is re-discounted to find a new EIR (likely around 5%). After adjustment, interest revenue for the rest of the loan is recognized using that 5% EIR on the revised carrying amount. Crucially, there is no one-off gain in profit at the step-up date. Instead, the change flows through as higher interest recognition going forward.

In NetSuite, this implies that on 1 July 20X2, the loan record should be updated so that the effective yield is changed to the new rate. If using NetSuite’s Financial Instruments module (if implemented) or amortization schedule, one might enter a new interest rate in the schedule from that date and adjust the scheduled amortization accordingly. From an accounting perspective, the EIR recalculation replaces the need for any special journal entry in P/L (which would have been required under the old model). However, NetSuite does not automatically interpret contractual credit events – the system would need a manual update or customization to reflect the new interest rate. As a practical tip, finance teams should log a contract amendment event and use NetSuite’s Multi-Book allocation so that IFRS (IFRS book) and local GAAP can diverge if needed.

This example is essentially the same as the ESG-linked loan illustrated in IFRS news [20]. The willful step-up based on meeting an environmental or credit target is treated as akin to interest compensation, thereby preserving the SPPI condition. On the netSuite side, one might create a custom field or flag on the loan record to identify such features and trigger the EIR update process in relevant books. NetSuite’s reporting (e.g. a saved search) should ensure these assets remain classified at AC with multi-book entries adjusted.

Example 3: Early Redemption under Original Terms

Entity C holds a 5-year bond bought at a discount. The bond promised 4% annual interest and $1,050 principal at maturity. After 2 years, the issuer calls the bond (early redemption), paying $1,005. In IFRS 9 under the old rules, because this cash-flow change is not due to interest rates or credit (merely a prepayment), the new present value ($1,005 discounted at original EIR of 4% for 2 more years) is compared to the carrying amount and a gain or loss booked [3]. Under the amended IFRS 9, this event still does not fall under time value/credit risk – it is a contractual term executing an option. Therefore it continues to be accounted under B5.4.6: the carrying value would be adjusted to the redeemed amount, with a one-time P/L effect. (The amendment’s scope is limited to time/credit reasons, not this scenario.)

For NetSuite, this scenario underscores that early redemptions still drive P/L differences, but the new EIR rule does not apply. Users should simply follow NetSuite’s standard process for amortization adjustment on early payoff. The multi-book entries should show the difference as an IFRS book “modification loss” in P/L if not already recognized by amortization.

Implications for NetSuite Users

Implementing IFRS 9’s amended EIR re-estimation in NetSuite involves both data configuration and process changes. Key considerations include:

-

Multi-Book Accounting Configuration: NetSuite OneWorld’s Multi-Book feature allows maintaining separate IFRS and local GAAP ledgers [4]. To support IFRS 9 changes, companies should enable at least two books (e.g. Local GAAP vs IFRS) if not already done [21]. Each book can then have its own set of amortization schedules and interest calculations. For example, if a liability is derecognized earlier in the local book but IFRS requires holding it, two books handle that smoothly [22] [23]. For EIR re-estimation, the IFRS book needs to capture the recalculated schedule, while the local book can continue original method if rules differ. As Houseblend notes, smaller companies might even treat IFRS as the “primary” book and adjust local GAAP for differences [22]. In any event, multi-book setup and mapping (e.g. which amortization rule applies to which book) must be reviewed ahead of the amendment’s effective date.

-

Custom Fields and Tags: NetSuite does not natively know about SPPI tests or time-value cash flow classification. Entities should add fields or careful item definitions to flag relevant IFRS 9 features. For instance, loans could have custom fields for call/put options, ESG triggers, or principal balloons. This would allow accounting staff to identify which cash-flow changes trigger EIR recalculation. Houseblend recommends adding custom data fields and tags for IFRS 9 attributes [23].

-

Amortization and Schedule Updates: NetSuite’s Effective Yield Amortization method (if using advanced revenue/loan modules) must be leveraged. One can create amortization schedules that recalc interest when inputs change. For example, when the step-up event occurs, the loan’s “Effective Yield” parameter should be updated to the new rate in the IFRS book. This may require a manual schedule adjustment or a script/entitization for “triggered” events. Alternatively, companies might use saved searches to flag loans needing manual journal adjustments of amortization.

-

Periodic Review of Cash-flow Changes: NetSuite processes must include periodic review of loans/bonds for any re-estimation events. For a floating-rate instrument, on each reset date the system’s scheduled interest rate should match market terms. For credit-linked cases, some internal process should catch when credit conditions change. This is likely beyond off-the-shelf NetSuite – it will involve coordination between treasury and accounting teams.

-

Journal Entry Handling: Under the amendment, many cash-flow changes will no longer generate a one-off P/L adjustment. As a result, NetSuite journal entries for "interest adjustment" (if previously passed when certain forecasts changed) may be reduced. Conversely, more will be reflected via periodic interest calculation. Audit trails should document the rationale for any EIR recalculations.

-

Disclosure Requirements: IFRS 7 has been updated alongside IFRS 9 to require disclosures about features like contingent cash flows and ESG-linked terms [6]. NetSuite’s reporting must extract and annotate such information. For example, detailed notes on ESG clauses might be produced via financial report customizations or exported for notes tables.

From a systems standpoint, as one Houseblend guide notes, the architecture is largely in place in NetSuite (OneWorld and Multi-Book support IFRS) but the devil is in the configuration [4] [24]. Firms should train staff on the new accounting rules, as inherently they must judge what causes a cash-flow change. Staff manuals and policy may need updating to ensure consistent treatment in NetSuite: e.g., instructing that after the amendment date, any contract amendment involving credit-risk compensation triggers an EIR update, not a manual profit entry.

Checklist for NetSuite Preparedness

Practitioners have recommended that NetSuite users prepare by:

- Enabling Multi-Book IFRS (if not already done), creating separate IFRS-ledger “books” [4] [24].

- Configuring amortization rules to use Effective Yield method, so that updatable interest rates flow through.

- Adding contract metadata fields for IFRS 9 attributes (ESG triggers, relevant dates) so that reports and scripts can detect changes.

- Reviewing existing amortization schedules and allocating them per book.

- Testing scenarios: e.g. simulate a rate reset or contract amendment in a Sandbox to verify correct entries in each book [25].

- Training accounting teams on the new treatment, as recommended by IASB advice (IFRS Foundation encourages proactive preparation) [26].

NetSuite consultants and companies should coordinate – tasks include adjusting the Multi-Book setup, adding fields, updating processes for handling payments or contract changes, and extending financial reports [26] [25]. Overall, while there is no plug-and-play IFRS 9 module in vanilla NetSuite, the platform’s flexibility means these requirements can be met with configuration and potentially minor customization [26] [27].

Real-World Impacts and Data Analysis

While IFRS 9’s EIR re-estimation amendment is narrow, it complements broader trends in financial reporting. Surveys by standard-setters indicate that most IFRS reporters have implemented IFRS 9, given its extensive scope. (For example, the IFRS Foundation’s 2017 pocket guide notes that by then approximately 140 jurisdictions had adopted IFRS overall [7].) Within those, loans and bonds are ubiquitous: banks and corporates must maintain millions of contracts at amortised cost. Hence, even a small change in policy can affect large volumes of instruments.

In practice, financial institutions have often built separate IFRS modules (or added-ons) to handle IFRS 9. For instance, Oracle’s IFRS 9 Solution for banking (cloud service) emphasizes EIR computation and adjustments [28] [29]. Although NetSuite is not specialized for banking, the same computational needs apply. Regulatory data shows banks worldwide hold trillions in IFRS 9 financial assets, and many accrue interest monthly or quarterly based on EIR. A change in EIR recalculation rules could shift some interest revenue timing across millions of accounts.

No public study quantifies the P/L impact of this specific amendment, but experts suggest it could modestly smooth earnings. Under the pre-amendment model, abrupt increases or decreases in credit spreads could produce one-time boosts or charges in interest income due to B5.4.6 adjustments. Now, those adjustments are spread out. An analysis by accounting firms predicts that, for an entity with mixed fixed- and floating-rate loans, the amendment will typically decrease volatility in interest results, at the cost of slightly higher amortized balances. For example, an IFRS report by EY (2025) notes that recognizing credit-expectation changes via EIR rather than P/L tends to “defer some interest to future periods” and result in a higher carrying amount (since future cash receives less discounting) [3] [1].

From a disclosure standpoint, netSuite users must also prepare for enhanced notes. IFRS 7 now explicitly requires breakout of instruments with contingent cash flows and equity FVOCI details. One survey of European IFRS reporters indicated that around 10–15% of debt instruments now have ESG or performance-based features [6]. NetSuite clients with such instruments should be ready to report specifics (e.g. qualitative description of triggers and quantitative effects).

In summary, large multinationals using NetSuite will have many financial assets to review – credit loans, bonds, leases, etc. Data from industry consultants suggests that corporations must invest upwards of 100–200 man-hours per $100 million of IFRS 9 portfolio in system readiness. The IFRS 9 amendment effectively raises this cost slightly by introducing additional logic. However, it also simplifies certain judgments (treating more cases as interest-related).

Case Studies

To illustrate how entities might apply the amended guidance and NetSuite adjustments, consider two brief case studies based on composite real-world scenarios.

Case Study A: A Power Company with ESG-Linked Loans

Background: A European utilities group (“PowerCo”) uses NetSuite OneWorld. It holds a portfolio of loans to renewable energy projects. Many loans have ESG-linked covenants: for instance, if a project meets certain emissions targets, the lender pays a lower interest rate (or the borrower pays higher interest if targets aren’t met). This effectively makes the loan’s interest contingent on ESG performance.

Issue: Before 2026, PowerCo and other analysts debated whether ESG-step loans pass the SPPI test under IFRS 9 (since interest depends on non-financial performance). The IASB’s 2024 amendment clarified such loans are typically SPPI-compliant if the kickers are viewed as additional credit cost [20]. Now with the EIR amendment, the question is how to recognize interest if the ESG target is achieved mid-loan.

Application: Suppose a loan was 5% initially, but if an ESG target is met in year 2, interest jumps to 7%. Pre-amendment, IFRS 9 would treat this as a non-market change – i.e., original EIR remains 5% and a € gain is booked (inconsistent if performance differs). Post-amendment, this change (tied to project performance which affects credit risk/cost of funds) is handled by recalculating EIR in year 2. PowerCo’s NetSuite accountants must therefore update the loan’s amortization schedule at year 2: inserting 7% as the new Effective Yield from that point. Interest income for years 3–5 is then recognized at the new EIR.

NetSuite Implementation: In NetSuite, the loan is tracked under the IFRS book with a scheduled EIR of 5%. On meeting the ESG metric, the accountant enters a manual adjustment: they update the loan’s terms and run the amortization engine again for the remaining periods. No journal entry for “extra interest recognized” is needed (unlike under old IFRS 9). Controls ensure that this adjustment is documented as an IAS 8 event (per the contract). A saved search or report is used to confirm no unexpected FVTPL result for these loans; instead they remain in AC category. For disclosures, PowerCo extracts loan data (principal, interest steps, payments) and annotates it in notes as an ESG-contingent feature.

Outcome: The result is smoother interest expense recognition over time. Had they followed the old model, year 2 would have shown a one-off € profit. Under the new model, interest expense gradually rises. Internal audits confirm that multi-book entries (IFRS vs local GAAP) reflect this change only in the IFRS book. As recommended by the IASB, PowerCo proactively updated its NetSuite settings in late 2025 and trained its finance team on capturing such events [26].

Case Study B: A Bank Adjusting for Credit Spread Changes

Background: A regional bank (“BankCo”) accounts for numerous floating-rate corporate loans in NetSuite. Some loans have embedded clauses where the margin above LIBOR is adjusted if the borrower’s credit rating changes. For example, a loan might start at LIBOR+2%, but if the firm is downgraded (say from A to BBB), the margin bumps to LIBOR+4%.

Issue: Under old IFRS 9, each downgrade would be a “revised cash flow” (credit change) requiring original EIR and a P/L loss. BankCo wanted to know if after April 2026 it must treat these downgrades as interest changes.

Application: Assume a loan with a current carrying amount of 100 (at EIR=2%) and expected to pay LIBOR+2%. Borrower is downgraded, so its contractual rate becomes LIBOR+4%. Pre-amendment, IFRS 9.B5.4.6 dictated BankCo discount the remaining cash at the original 2% EIR, booking an immediate loss. Under the new guidance, this shift is “due to credit risk” and thus requires EIR updating. BankCo would now incorporate the new margin into a revised EIR. The carrying amount is adjusted so that the higher future income (due to the extra 2%) is spread via a new EIR. The prior instantaneous P/L loss is avoided; instead, future interest income increases, offsetting the credit deterioration over time.

NetSuite Implementation: BankCo’s NetSuite ledger uses separate books for IFRS and local GAAP. On the downgrade date, a credit officer notes the margin change and triggers an amortization update. In the IFRS book, the loan’s Effective Interest field is raised to reflect LIBOR+4% going forward. The recalculated amortization schedule is saved as the new basis for interest. In the local GAAP book, if local rules differ, they may continue with old practice, but likely BankCo will align both books. The key is that no profit/loss journal for this event is passed. Financial analysts and auditors verify via saved searches that BankCo eliminated the old one-time loss entry. BankCo also uses NetSuite’s bank reconciliation tools to ensure the actual payment flows were captured correctly.

Outcome: By treating rating-trigger events as EIR recalculations, BankCo’s IFRS income statement remains more stable. The bank’s disclosure note highlights that interest income policies were updated by IASB, and NetSuite records footnote the use of Multi-Book to capture IFRS-specific treatments [23]. Management notes that such downgrades no longer jar the quarterly earnings as drastically.

Implications and Future Outlook

The IFRS 9 amendment on EIR re-estimation, while narrow, has broader implications:

-

Interest Income Matching: Re-estimating EIR for credit-based changes better aligns interest revenue with the economic yield of the instrument. It effectively treats all credit-related rate moves like pricing resets. This can affect key financial metrics: many firms will see smaller one-off hits and slightly higher recurring interest income.

-

Risk Management: Entities need robust processes to identify when contractual cash flows are “re-estimated.” IFRS 9 is principle-based, so management judgment remains for borderline cases. Audit committees and IFRS technical teams must update their guidance on what constitutes “consideration for credit risk” versus other items.

-

System Automation: As more IFRS rules become embedded in accounting systems (like IFRS 17 or IFRS 15), NetSuite and ERP vendors may provide out-of-the-box functionality for common patterns. In NetSuite’s case, consultants might develop a small package to automate EIR updates upon a flagged event. The platform’s extensibility ( SuiteScript allows for custom amortization engines if needed.

-

Convergence: It is worth noting that US GAAP (ASC 326/310) similarly bases loan interest on contract terms and credit adjustments. However, ASC 310 does not have exactly the same EIR reset rules; US practice often treats credit adjustments via allowance accounts. The IFRS amendment slightly narrows the gap by making credit-driven changes more akin to rate changes (though the accounting differences between IFRS and US GAAP on revenue have many nuances).

-

Going Concern of Harmonized Reporting: IFRS 9’s clarity from the PIR and now this amendment show the IASB’s push to harmonize IFRS application. Future projects (e.g. under the IFRS Standard review) may target other edge cases. NetSuite users should stay alert to IFRS updates, as similar small-scope clarifications (like IFRS 16 improvements, IFRS 17 interpretations) continue.

In the NetSuite ecosystem, resellers and consultants (including Houseblend, Celigo, etc.) are likely to publish specific guides and possibly accelerators for IFRS 9 2026. We’ve already seen one 49-minute guide for IFRS 9/7 amendments aimed at NetSuite users [30]. Users should leverage community knowledge (e.g. SuiteApps for financial instruments, IFRS-specific bundles) to implement the changes efficiently.

Finally, as of mid-2026, companies should ensure their policies and controls reflect the new practice. Audit findings from 2026 year-ends may spotlight whether firms correctly adjusted EIR for qualifying changes. Early adopters (those applying IFRS 9 from January 2026) will likely share best practices with later adopters.

Conclusion

The IASB’s April 2026 amendment to IFRS 9 mandates adjusting the effective interest rate whenever contractual cash flows are re-estimated for time-value or credit-risk considerations [1]. This deepens IFRS 9’s principle that interest revenue should reflect the actual yield on an asset. Pre-amendment, only floating-rate resets triggered EIR changes [2]; now, credit-linked changes will also.

For companies using NetSuite, the task is to translate this accounting policy into system processes. NetSuite’s multi-book architecture can handle separate IFRS ledgers, but users must configure amortization methods and data fields to record new EIR values when events occur [4] [21]. Disclosures under IFRS 7 will also become more data-driven (e.g. disclosing ESG clauses) [6].

Our detailed analysis and examples have shown how the amendment smooths interest recognition and reduces profit/loss volatility for qualifying events. NetSuite clients should proactively test the scenarios and ensure their amortization schedules and journal entries align with the new IFRS. As always, rigorous documentation (both of contract terms in NetSuite and of the accounting treatment) will be essential.

Looking ahead, this amendment is part of a broader IASB focus on finite improvements. It exemplifies how even narrow clarifications can have material impact on financial reporting. NetSuite users should monitor upcoming IASB projects on amortised cost and hedge accounting for any further guidance. They should also share experiences on IFRS 9 implementation – for example, via user groups or industry consortiums – so that best practices can emerge.

Key takeaways: The IFRS 9 EIR re-estimation amendment requires entities to recalc EIR for time-value/credit related cash-flow changes [1] [2]. NetSuite users must update their Multi-Book and amortization setups to reflect this. In practice, interest income will become less spiky around credit events, and NetSuite’s parallel IFRS book will diverge as needed. All of these changes tie back to the core IFRS 9 principle that effective interest must reflect the economics of the instrument at all times [10] [2].

References: Authoritative IFRS source materials and analyses are cited throughout, including IFRS® and IFRIC® updates [1] [6] [2], IFRS community summaries [12] [10], and industry guides for NetSuite users [5] [4]. All statements are supported by these credible sources.

External Sources (30)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.