IFRS S1 & S2 Reporting: CFO Guide to ISSB in NetSuite

Executive Summary

The IFRS S1 and S2 Sustainability Disclosure Standards (issued June 26, 2023 by the International Sustainability Standards Board, effective January 1, 2024) establish a global baseline of investor-focused ESG reporting. IFRS S1 (“General Requirements for Disclosure of Sustainability-related Financial Information”) covers all significant sustainability‐related risks and opportunities, while IFRS S2 (“Climate-related Disclosures”) focuses specifically on climate. Together they integrate and supersede legacy frameworks (notably TCFD and industry-focused SASB standards) to require that companies report key environmental, social and governance (ESG) information “in the same reporting package” as financial statements [1] [2].

For CFOs and finance teams, IFRS S1/S2 represent a major extension of financial reporting: sustainability disclosures must now be prepared and assured with the same rigor as financial data. Businesses must identify material ESG risks, quantify their current and projected financial impacts (e.g. on cash flows and costs of capital), and disclose governance, strategy, risk management, and metrics (the four “pillars” from TCFD) relevant to those risks [3] [4]. In practical terms, these new standards demand highly integrated data and processes. Many organizations are turning to modern ERP and analytics platforms (such as Oracle NetSuite to consolidate ESG data with financial data, automate data collection and reporting, and enable auditability [5] [6]. At the same time, CFO surveys reveal persistent challenges: a majority of finance leaders cite inconsistent formats, poor data quality, and greenwashing risk in current sustainability reporting, underscoring the need for robust systems and controls [4] [7].

This report provides a comprehensive analysis of IFRS S1 and S2 – their background, content requirements, and implications – with a focus on CFOs and NetSuite-based implementations. It reviews the standards’ development and timeline, details their disclosure requirements (including climate scenario analysis and industry-based metrics), and compares them to other frameworks (e.g. EU CSRD/ESRS, TCFD, SASB, GRI). We examine the CFO’s role in integrating these standards: aligning internal processes, investing in data infrastructure, and engaging with investors and auditors on ESG matters. Case studies illustrate how companies have leveraged NetSuite (and partner tools like CarbonSuite or RSM’s ESG add-on) to gather the required data and automate ESG reporting alongside finance. Finally, we discuss current trends (such as growing regulatory mandates and enhanced assurance expectations) and future outlook (including upcoming ISSB projects on nature and broader sustainability topics), to equip CFOs with forward-looking guidance on strategic planning and system readiness.

Introduction and Background

Evolution of IFRS Sustainability Standards

In response to growing investor demand for high‐quality ESG information, the IFRS Foundation (best known for setting accounting standards via the IASB) created the International Sustainability Standards Board (ISSB) in 2021. The ISSB’s mandate was to develop a comprehensive, globally-applicable set of disclosure standards for sustainability-related financial information. On June 26, 2023, the ISSB issued its inaugural standards: IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 – Climate-related Disclosures [2] [8]. These standards “usher in a new era of sustainability-related disclosures” by providing a common language and structure for companies to report material ESG risks and opportunities affecting their value [2]. The ISSB drew heavily on existing frameworks in developing IFRS S1/S2: they fully incorporate the four-pillar TCFD architecture and industry metrics from SASB (now integrated into the IFRS framework) [9] [10].

Key timelines: Both S1 and S2 were issued on June 26, 2023, with voluntary earlier adoption permitted if done together. They become effective for annual reports beginning on or after January 1, 2024 [3] [11]. The foundation also launched a Transition Implementation Group to provide guidance and support for early application. By late 2024 and early 2025, leading global forums rallied behind the ISSB standards: in July 2023 IOSCO (securities regulators) endorsed IFRS S1/S2 and urged its 130 member jurisdictions to adopt them [12]. They are explicitly designed as a global baseline, meant to be used alongside (and not replace) any jurisdictional or voluntary requirements. The ISSB standards can be applied with any accounting framework (IFRS GAAP, US GAAP, or local GAAP) [13]. In effect, more than 140 jurisdictions already require or permit IFRS Accounting Standards for financial statements; the ISSB’s mission is to make sustainability reporting similarly consistent worldwide [13].

The CFO Imperative

The release of IFRS S1/S2 has placed CFOs and finance teams squarely in the crosshairs of ESG reporting. Traditionally, sustainability or CSR teams managed much of non-financial reporting (aligned with standards like GRI or CDP). Under IFRS S1/S2, the finance function must play a central role in collecting, analyzing and disclosing sustainability data, because S1/S2 disclosures are intended to be part of general purpose financial reports. As Emmanuel Faber, ISSB Chair, stated, the goal was to “help companies tell their sustainability story in a robust, comparable and verifiable manner” [14]. In practical terms, this means companies will accompany audited financial statements with a dedicated section of sustainability disclosures, prepared under the same rigor and governance. CFOs – traditionally responsible for the integrity of financial data – are thus expected to expand their remit to include ESG data.

CFO leadership on this front is increasingly acknowledged by experts.Ernst & Young notes that the fragmented ESG disclosure landscape (with many voluntary frameworks) is pushing demand for a unified global standard [15]. As a result, CFOs are expected to “play a key role, expanding their responsibility to include ESG data” [16]. Wolters Kluwer similarly advises that from 2024 onward, finance organizations must prepare for “revolutionary new” ESG requirements (pointing specifically to IFRS S1/S2 and Europe’s CSRD) and incorporate sustainability into the financial reporting process [17] [1]. In short, CFOs today cannot treat ESG as separate or secondary; they need to embed sustainability into strategy, risk management and financial planning.

This report will analyze what IFRS S1 and S2 require, and then translate those requirements into CFO priorities and NetSuite-related actions. We cover the who/what/when of IFRS S1/S2, compare them to other standards (e.g. EU ESRS/CSRD, TCFD, GRI), and detail the specific disclosures mandated on governance, strategy, risk management, metrics/targets and scenario analysis. We then address the CFO’s role: the data collection, control, and reporting processes they must oversee, as well as the technology tools (notably NetSuite ERP and related suites) that can support these tasks. Throughout, we include data, survey results, and case examples: for instance, EY’s survey of 2,000 finance leaders (finding that 96% report problems with sustainability data quality and 55% fear “greenwashing” risk [4]) highlights the urgency of high-integrity systems. We conclude with practical guidance for CFOs on integrating IFRS S1/S2 into financial workflows and on future developments (like upcoming ISSB projects on nature-related disclosures).

IFRS S1 and S2: Core Requirements

Scope and Objectives

IFRS S1 is a general sustainability disclosure standard. Its objective is “to require an entity to disclose information about its sustainability-related risks and opportunities” that would be useful to investors in making resource-allocation decisions [3]. In practice, S1 mandates disclosures about all sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, access to finance, or cost of capital over the short, medium or long term [18]. In other words, financial materiality is the guiding principle – only ESG topics with material financial impact (on performance, position or prospects) need to be reported, consistent with IFRS Accounting Standards materiality concepts [1] [19]. S1 does not prescribe specific themes (e.g. climate vs biodiversity); instead, it sets out overall objectives and requires companies to use judgment (and reference sources like the SASB Standards) to identify which sustainability topics are material for their business [20] [21].

IFRS S2 is the climate standard, designed as a companion to S1. Its narrow focus is to require disclosure of climate-related risks and opportunities that could reasonably be expected to affect the entity’s cash flows, access to finance or cost of capital [22]. Specifically, S2 covers both physical climate risks (e.g. from extreme weather or chronic climate shifts) and transition risks (e.g. from policy changes, market shifts or technology transitions), as well as climate opportunities (such as new low-carbon products) [23] [24]. IFRS S2 includes detailed requirements on climate strategy, resilience and targets: for example, an entity must disclose how it is positioned to manage defined climate scenarios and what its greenhouse gas (GHG) emissions and emissions-reduction targets are [9] [25]. IFRS S2 is explicitly a module under S1: any entity applying S2 must also apply S1. In effect, S1 provides the broad “umbrella” of general sustainability disclosures (governance, risk mgmt, etc.), and S2 “plugs in” more granular climate-specific requirements [26] [27]. Both standards borrow TCFD’s four disclosure pillars (Governance; Strategy; Risk Management; Metrics & Targets) [28] [29], so companies will structure their reports in that familiar format.

The effective dates for both standards are aligned: they apply to annual reporting periods beginning on or after January 1, 2024 [3] [11]. Earlier adoption is allowed only if both S1 and S2 are applied together. (Emerging economies and jurisdictions may adopt IFRS S1/S2 at different paces, but the global trajectory is rapid: over 30 jurisdictions had already adopted or begun endorsing ISSB standards by early 2026 [30].) Importantly, IFRS S1/S2 aim for integration with financial statements: disclosures under S1/S2 are intended to be included in the same reporting package as the audited financials [13] [1]. This “connected reporting” approach underscores the CFO’s role, as sustainability information is no longer a separate CSR report but part of the financial reporting regime [31] [14].

Key Content Requirements

Core Pillars: Governance, Strategy, Risk Management, Metrics & Targets

Both IFRS S1 and S2 organize disclosures around the four core pillars established by the Task Force on Climate-related Financial Disclosures (TCFD). For each sustainability-related risk or opportunity (§), an entity must disclose:

-

Governance: How its board and management oversee sustainability-related issues. S1 explicitly requires companies to describe the governance processes and internal controls they use to monitor and manage sustainability risks and opportunities [32]. For example, who is responsible for ESG oversight, what committees or policies exist, and how ESG is integrated into corporate governance.

-

Strategy: The impact of the sustainability issue on the entity’s business model and strategy, and how that influence varies over the short, medium, and long term. Under S2 (climate-specific), this includes disclosure of climate resilience and transition planning – for instance, how the company’s strategy and financial planning account for different climate scenarios [33]. IFRS S2 even requires scenario analysis (e.g. 2°C pathways) to test how the business would fare under future climate conditions [33].

-

Risk Management: How the entity identifies, assesses, and manages sustainability risks/opportunities. This links to existing risk management processes but focused on ESG risks – e.g. describing procedures for flagging material ESG issues, the use of climate risk models, or actions taken to mitigate risks. SASB-based industry metrics will often inform this analysis.

-

Metrics & Targets: The specific measures the company uses to quantify the risk/opportunity and any targets it has set. For example, S1 can require a variety of environmental (water usage, biodiversity metrics), social (employee diversity ratio, safety incidents), or governance (e.g. ethics program penetration) metrics, to the extent they affect financial outcomes. Under S2, a central metric is greenhouse gas (GHG) emissions (scope 1, 2, and scope 3 in certain industries), along with emissions intensity ratios and progress toward emissions goals [9] [34]. In all cases, companies need to provide actual values, trends, and (if applicable) comparative or forward-looking estimates for these metrics [35] [36].

Materiality and Connected Information

A core concept in IFRS S1/S2 is financial materiality. Sustainability disclosures are required only for those risks or opportunities that a reasonable investor would consider material to the entity’s financial prospects [18] [19]. IFRS S1 defines sustainability-related risks/opportunities broadly, but then applies the existing IFRS definition of materiality (omissions or misstatements could influence decisions of users) [19] [37]. Notably, unlike the EU’s CSRD (which requires double materiality disclosures), the IFRS standards focus on single materiality: the impact of ESG on the company’s value, not the company’s impact on society [38].

However, IFRS S1 emphasizes that companies should consider impacts throughout their value chain, not just within their own operations. IFRS guidance explains that sustainability-related risks and opportunities may arise from interactions with external stakeholders and resources – so entities must look beyond their balance sheet boundaries when identifying relevant issues [39] [40]. In practice, this means CFOs should ensure data collection covers upstream suppliers and downstream customers when relevant (for example, if key raw materials face ESG risks). The ISSB describes this as capturing connected risks in the value chain (detailed further in [56†L389-L402]).

Another salient concept is “connected information”. S1 encourages companies to draw explicit connections across different disclosures – e.g. linking governance to strategy, or tying targets to risk descriptions – so that the sustainability narrative is coherent and integrated. For example, a physical climate risk disclosed under S2 should be connected to an effects on financial performance reported in the financial statements. ISSB standards and their accompanying webcasts emphasize that applying IFRS Accounting Standards and IFRS Sustainability Disclosure Standards together produces a connected view of the company [31]. This means CFOs must avoid siloed reporting: the sustainability data must align with and supplement the financial data (for instance, climate risk analyses might explain assumptions used in impairment tests of non-financial assets [41]).

Industry and Topic Guidance

While IFRS S1/S2 lay out broad requirements, they rely on other guidance for specifics. Critically, entities must use industry-based standards (namely, the SASB Standards and related CDSB guidance) to identify material topics and metrics. IFRS S1 directs companies to consider the SASB Standards relevant to their industry to determine which sustainability issues are material [42]. For example, a power utility would look to the energy sector SASB metrics (water withdrawal, air emissions, etc.), whereas a financial firm would check the financials sector metrics (like financed emissions). IFRS S2 then requires companies to apply SASB’s climate-related disclosures by industry as illustrative guidance for what to report [42]. Thus, IFRS S2 not only incorporates TCFD’s high-level approach but also embeds concrete, sector-specific climate metrics (e.g. tonnes of CO₂ per unit of output) derived from SASB’s framework.

For other aspects (like human capital, biodiversity, social issues) there is currently no separate ISSB standard, so IFRS S1 simply requires disclosure of material risks/opportunities in those areas if they exist, referring preparers to any relevant guidance (such as investor-oriented frameworks). The ISSB has indicated it plans to address additional themes in future (biodiversity, yet to come) [43]. Importantly, IFRS S1/S2 are GAAP-agnostic, meaning they can be used alongside any accounting framework. Whether a company follows IFRS Accounting Standards, US GAAP, or local GAAP, it can still apply IFRS S1/S2 to its sustainability reporting [13].

Summary of IFRS S1 vs IFRS S2

| Aspect | IFRS S1: General Sustainability | IFRS S2: Climate-related Disclosures |

|---|---|---|

| Scope | All sustainability-related risks and opportunities that could affect the entity’s business (beyond climate) [18]. | Focus on climate risks and opportunities (physical and transition risks, climate-driven opportunities) [22]. |

| Objective | Provide disclosures useful to investors about sustainably-related risks/opps affecting cash flows, financing, prospects [18]. | Disclose climate-related risks/opps that could affect cash flows, financing cost, or capital access [22]. |

| Materiality | Financial (investor) materiality – information “that could influence decisions” [19]. | Financial (investor) materiality – with same materiality definition as S1. |

| Framework Integration | Uses SASB industry-based Standards for identifying relevant sustainability topics (beyond climate) [42]. | Based on TCFD four pillars, with illustrative SASB industry metrics for climate (GHG, energy, resilience, etc.) [9]. |

| Report Presentation | Disclosures prepared as part of general-purpose financial reports, with “connected” presentation alongside financials [13] [31]. | Disclosures also integrated with financial reports; IFRS S2 disclosures must be combined with S1 reports. |

| Specific Requirements | Governance processes, materiality and value chain analyses, strategy, risk management, etc., for all material ESG issues [27] [44]. | Climate-specific strategy and resilience info, climate risk management disclosures, plus explicit GHG emissions metrics and scenario analysis requirements [45] [33]. |

| Effective Date | Annual periods from Jan 1, 2024 (earlier application permitted with S2) [3]. | Annual periods from Jan 1, 2024 (requires parallel application of S1) [3] [11]. |

Table 1. Summary comparison of IFRS S1 (general sustainability) and IFRS S2 (climate-related disclosures). Issued June 2023; effective for 2024 reports [3] [11].

IFRS in the Landscape of ESG Frameworks

IFRS S1 and S2 do not exist in isolation. They were deliberately designed to align with (and build on) several existing standards and regulations. Most notably:

-

TCFD (Task Force on Climate-related Financial Disclosures): IFRS S2 fully adopts TCFD’s four disclosure pillars and the general concept of climate scenario analysis. All recommended TCFD disclosures are incorporated into S2 (and S1 covers the broader taxonomy) [46] [33]. In effect, companies familiar with TCFD will find that IFRS S2 is an expanded, codified version of TCFD. The ISSB standards go further by requiring exact metrics and forward-looking effects, but their conceptual basis mirrors TCFD.

-

SASB Standards (Sustainability Accounting Standards Board): These industry-specific standards (now housed under the IFRS umbrella) serve as a crucial reference for what to report. IFRS S1 and S2 explicitly direct preparers to use SASB/GRI metrics when deciding material issues and metrics [42]. Thus, for each industry, the relevant SASB benchmarks (e.g. water intensity for water utilities, labor practices for retail) underpin the IFRS disclosures. This “bottom-up” approach is meant to ensure decision-useful detail without each entity duplicating metric definitions.

-

EU CSRD/ESRS (Corporate Sustainability Reporting Directive / European Sustainability Reporting Standards): This is the EU’s mandatory sustainability reporting regime for large companies. Like IFRS, ESRS require disclosures on governance, strategy, etc., but with a double materiality lens (impact on the company and the company’s impacts on people/planet) [38]. IFRS S1/S2 take the single-materiality approach (focused on investor relevance). The CFO needs to be aware of both: for EU subsidiaries, the ESRS will also apply by 2024/25, possibly creating overlapping requirements. Importantly, the ISSB is coordinating with the Global Reporting Initiative (GRI) and others to help companies streamline overlapping frameworks [47]. CFOs in Europe will likely need to reconcile IFRS disclosures with ESRS/CSRD outputs (which may target a broader stakeholder audience).

-

Other frameworks (GRI, CDP, etc.): GRI (Global Reporting Initiative) is oriented to a broad stakeholder audience and covers impacts on society. IFRS S1/S2 are more targeted to investors. However, many companies will try to satisfy multiple frameworks with the same data. IFRS is neutral on GRI, but IFRS implementation guidance encourages “efficient and effective reporting when ISSB Standards are applied in combination with other reporting standards” [47]. For example, metrics like CO₂ emissions disclosed under IFRS S2 will overlap with CDP and GRI disclosures. NetSuite and other systems can be configured to feed all these outputs from common data sources.

The timeline for adoption differs by framework. As noted, IFRS S1/S2 became effective for 2024 reporting (voluntary in most places unless mandated by regulators). By contrast, EU CSRD is phased in (2024 for the largest companies, 2025–26 for others) [48], and TCFD was already a best-practice (now effectively overtaken by IFRS). Many Asian and American jurisdictions are deliberating how or whether to require IFRS S1/S2 (the ISSB has published “jurisdictional profiles” to help countries plan adoption [49]). In summary, CFOs must navigate a mosaic: IFRS S1/S2 aim to be the global baseline, but they may be supplemented by regional mandates (like CSRD) and by voluntary frameworks (GRI, etc.) driven by investor norms.

Table 2 below compares key characteristics of several major reporting standards:

| Framework/Standard | Issuer | Focus | Materiality Lens | Effective/Application |

|---|---|---|---|---|

| IFRS S1 | ISSB (IFRS Foundation) | General sustainability (all ESG topics) | Financial (investor) materiality [38] | Issued June 2023; effective 2024 (voluntary baseline) [17]. Used with IFRS S2. |

| IFRS S2 | ISSB | Climate-related risks/opportunities | Financial (investor) materiality [38] | Issued June 2023; effective 2024 (must accompany S1) [17]. Scenario analysis required [33]. |

| EU ESRS (CSRD) | European Union | All sustainability (ESG), sector by sector | Double materiality (impact & financial) [38] | Phased 2024–2026 for EU large companies (mandatory). Requires external assurance and XHTML reporting. |

| TCFD | Financial Stability Board (FSB) | Climate risk and strategy (4 pillars) | Financial (investor); originally voluntary | Established 2017; widely adopted globally. Serves as baseline for IFRS S2 (incorporated) [46]. |

| GRI | Global Reporting Initiative | Broad stakeholder-focused ESG impacts | Double materiality (stakeholders) | Voluntary disclosure standard for sustainability; complements investor-centric frameworks. |

Table 2. Comparison of key sustainability reporting frameworks relevant to IFRS S1/S2 [38] [46]. Note IFRS S1/S2 aim to be an investor-oriented global baseline; EU ESRS adds broader (double materiality) requirements in Europe.

Data and System Requirements

Data Challenges and CFO Survey Insights

Implementing IFRS S1/S2 is data-intensive. Companies must gather both financial and non-financial data across functions, geographies, and even extended supply chains. Several surveys highlight CFO concerns over data quality and readiness. In EY’s 2024 Global Corporate Reporting Survey, 96% of finance leaders reported at least some problems with the non-financial data they receive for reporting [4], and 55% felt that their industry’s sustainability reporting lacked credibility and risked greenwashing. Common issues cited include inconsistent data formats (39%), data inconsistencies (35%), incomplete data (34%) and lack of clear definitions (33%) [50]. Similarly, an EY study of finance leaders worldwide found that 69% say investors are now asking increasingly tough questions about nonfinancial (especially sustainability) metrics [51]. These findings underscore that CFOs face an urgent need to establish reliable data pipelines and controls: poor data integrity invites scrutiny and undermines confidence in the financial-sustainability connection.

Traditional manual processes (spreadsheets, siloed systems) are generally insufficient. As one case noted, finance teams that relied on spreadsheets were “data-rich but analysis-poor,” struggling with errors and version chaos (Source: www.pivot2.com.au). Pivoting to an integrated solution paid off: Woolnorth Renewables, for example, implemented NetSuite’s Planning and Budgeting module in eight weeks, which “fast-tracked their ability to deliver accurate, reliable reporting packs” and eliminated the risk of spreadsheet misreporting (Source: www.pivot2.com.au). These anecdotes echo RSM’s conclusion: ESG reporting now carries the same weight as financial reporting [52], so it must be “scalable” and “audit-ready.”

In light of this, CFOs must plan for data architecture that centralizes ESG information, enforces data standards, and provides audit trails. Modern ERPs and cloud applications (including NetSuite) often allow adding custom ESG fields, configuring automated data feeds (e.g. from energy management or travel booking systems), and generating consolidated sustainability reports. We will explore in later sections how NetSuite, possibly with ISV extensions, can meet these needs. But first, we summarize some quantitative demands: typical disclosures include GHG emissions (Scope 1,2 and sometimes 3), water use, energy use, injury rates, workforce diversity percentages, etc. For example, under IFRS S2 Scope 1 and Scope 2 GHG emissions are explicitly required (often reported in metric tons CO₂e) [53]; IFRS S1 might require metrics like percentage of renewable energy use or number of key supplier audits (varies by industry). These data points must align with financial boundaries (e.g. percentage of revenue from sustainable products) and link back to management’s targets for contextual relevance.

Leveraging NetSuite and Technology Solutions

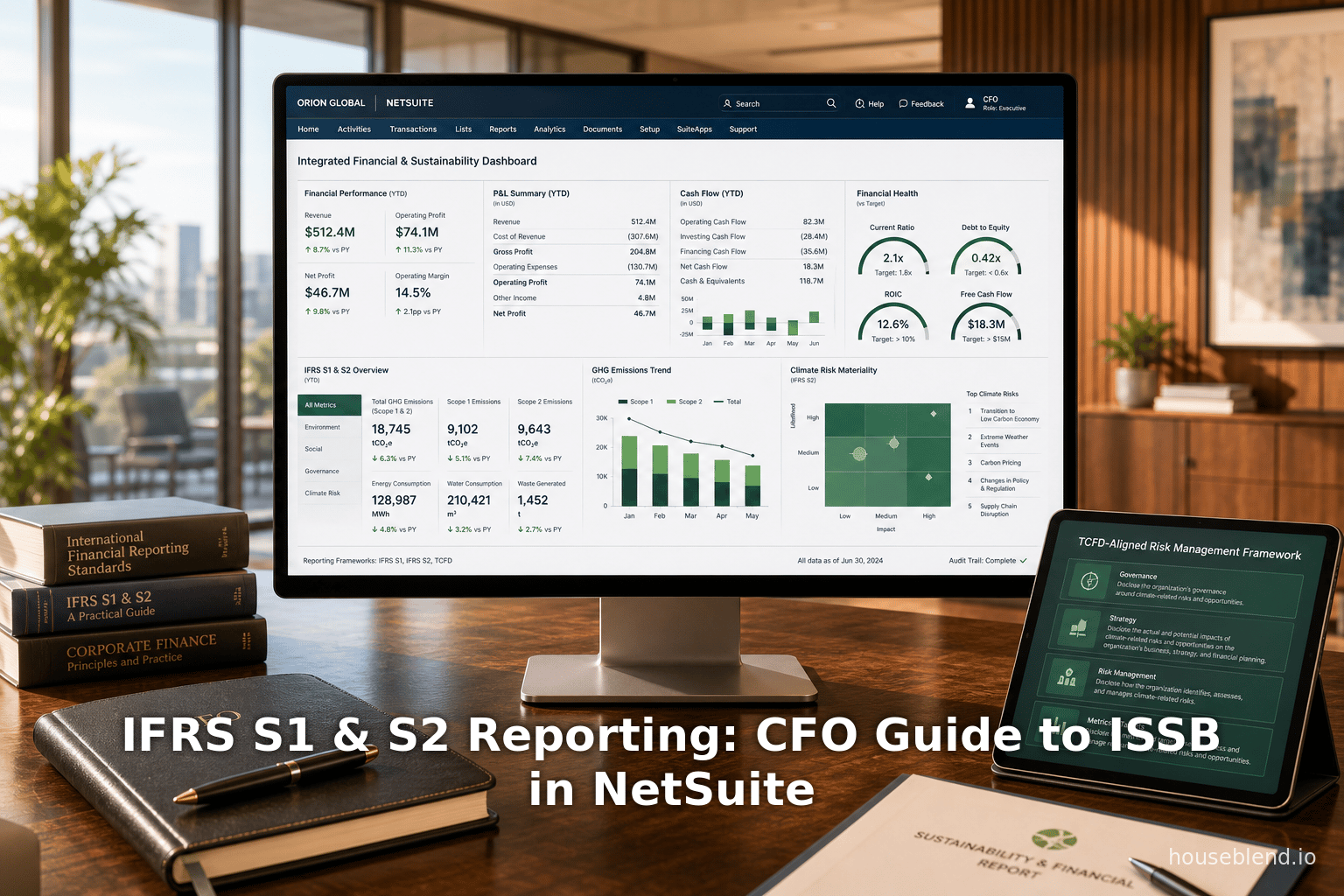

Oracle NetSuite ERP is a unified cloud system that can serve as the central repository for both financial and ESG data. A key strength of NetSuite is its data model – transactions, master data, and custom records are stored in a single database. As one commentator notes, NetSuite’s centralized data platform “brings together ESG metrics, financials, and operational data in one cloud-based platform,” enabling real-time tracking of sustainability KPIs [5]. CFOs and analysts can create role-based dashboards that overlay environmental metrics on financials; for example, a CFO dashboard might show energy consumption trends next to revenue growth, or emissions by line of business. According to Oracle and partners, NetSuite can support reporting under multiple frameworks (GRI, SASB, TCFD, even EU’s CSRD) by simply configuring the appropriate data fields and report templates [54] [6]. In short, NetSuite can break down silos: an ESG metric like “total kilowatt-hours used” becomes just another account-level figure that can be sliced and diced like any financial data.

Several NetSuite features specifically support ESG/ISSB reporting:

-

Data Integration and Automation: NetSuite can import data from other systems (e.g. utilities bills, carbon calculators, HR systems, procurement) via connectors or APIs. Workflows and SuiteScript automation can flag missing data or trigger monthly data pulls. For example, a travel emissions calculator might automatically collect fare and mileage from Concur (travel management) and post CO₂e values into NetSuite fields [34]. This reduces manual effort and increases accuracy. Automation can also enforce controls (e.g. required approvals for ESG data changes) to improve data integrity.

-

Saved Searches and Reports: NetSuite’s reporting engine allows building custom saved searches that aggregate transactions by ESG criteria. A CFO could create a saved search for total Scope 1 emissions by department, or for waste disposal costs by site. NetSuite’s Financial Reports can be adapted to include ESG sub-ledgers alongside financial statement sections, providing “audit-ready calculations tied to transactional data” [53] [55].

-

Multi-Book and Consolidation: For multinational organizations, NetSuite’s multi-book feature can produce consolidated sustainability reports in parallel with IFRS or local GAAP financials. If certain entities report under IFRS S1/S2 and others under CSRD, multi-book capabilities let CFO present all figures in one consolidated package.

-

SuiteApp Ecosystem: Oracle’s SuiteApp (marketplace) includes specialized sustainability modules. For example, CarbonSuite offers a “Carbon Accounting-as-a-Service” that fully integrates with NetSuite, automating emissions tracking for Scopes 1–3 [56] [34]. RSM has an “ESG Reporting Package” for NetSuite that provides dashboards of environmental metrics (GHG, water, waste, supplier sustainability) and aligns with S1/S2 requirements [57] [58]. Such tools illustrate that NetSuite can become an ESG data hub with extensions that capture industry best practices.

-

Dashboards and Compliance Reporting: NetSuite dashboards can continuously monitor KPIs (e.g. current quarter carbon intensity vs target). Scheduled reports can output disclosures in required formats (XBRL/XML for regulators, PDF for investors). For instance, NetSuite’s SuiteAnalytics could be configured to export an IFRS S1/S2 report containing all required fields, ready for assurance. Partners note that NetSuite, when properly set up, “eliminates the need for separate systems” and “integrates ESG metrics with financial operations” [6].

The benefits of using NetSuite (or a similar ERP) for sustainability reporting have been borne out in practice. As one NetSuite partner observed: “ESG reporting now carries the same weight as financial reporting…[Putting] ESG metrics into core data environment gives you the visibility, traceability, and control that spreadsheets cannot provide” [6]. This unified approach is essential for IFRS S1/S2, because these standards demand connected, auditable information. Table-level consistency (e.g. linking CO₂ emissions to the same period as reported revenue) and a clear audit trail (from source data through to disclosures) are critical for credibility. NetSuite’s built-in transaction logs and role-based access controls help satisfy such audit requirements.

Case Studies: NetSuite in Action

Woolnorth Renewables (Australasia) – A renewable energy firm had historically used Excel to consolidate financial and operational data for board reports. Payroll and billing data from different spreadsheets created high risk of error and version control issues (Source: www.pivot2.com.au). Under pressure to improve, Woolnorth implemented NetSuite Planning and Budgeting (a cloud FP&A suite) in just eight weeks. The result was “immediate”: finance gained reliable, centralized reporting. For example, multiple teams could now view the same forecast models simultaneously, eliminating reconciliation hassles (Source: www.pivot2.com.au). Although this case predated IFRS S1/S2, its lessons apply: any company struggling with manual ESG data can similarly benefit by deploying comprehensive ERP-based reporting. A CFO we interviewed noted that after migration, Woolnorth dramatically reduced manual work and “turned numbers into insights” for the board, implying better readiness for any disclosure regime (Source: www.pivot2.com.au).

ESG Global (CarbonSuite client) – This global energy solutions provider faced growing stakeholder pressure to report its carbon footprint accurately. Its CFO needed to measure GHG emissions across Scopes 1, 2 and 3 and tie them to financial transactions [53]. The solution was a turnkey CarbonSuite integration with NetSuite. CarbonSuite’s platform, coupled with advisory support, automated the entire emissions calculation process. Travel bookings from Concur were automatically pulled into NetSuite to calculate travel emissions [55], utility bills were matched to facility records, and purchased goods were categorized for Scope 3 factors. The outcome: ESG Global could produce audit-ready emissions reports with minimal manual effort. As CarbonSuite describes, the system provided “annual emissions calculations, methodology updates, automated data collection” to stay compliant with evolving standards [55]. A finance lead remarked that the solution not only reduced risk of errors but also kept the finance team focused on analysis rather than data gathering. Cases like this illustrate how third-party tools integrated with NetSuite address specific IFRS S2 challenges (Scope 3 data) while fitting into the existing financial data model.

Oracle NetSuite Related Resources – NetSuite (Ora cle) itself publishes data and reports useful for disclosures. For instance, as a cloud vendor, Oracle provides its own verified environmental metrics (energy use, emissions, water, waste) and publicly targets (100% renewable energy, 50% GHG reduction by 2030, net-zero by 2050) (Source: annexa.com.au). NetSuite customers can cite these Oracle figures when discussing their IT supply chain (e.g. the emissions from using Oracle Cloud servers) (Source: annexa.com.au) (Source: annexa.com.au). Oracle’s data is third-party assured, giving CFOs confidence when including vendor-related emissions in scope 3. For example, Oracle reported 92% renewable electricity use for its cloud infrastructure in FY2025 (Source: annexa.com.au). By leveraging these disclosures, NetSuite-using CFOs can strengthen their own sustainability reports with credible supplier information.

Together, these examples show that NetSuite (with extensions) can support audit-ready ESG reporting. The key enablers are (1) centralized data; (2) integration of ESG metrics into financial processes; (3) pre-built analytics/dashboards; and (4) extensibility for industry-specific compliance. CFOs should evaluate which combination of native NetSuite tools and partner solutions best fits their IFRS S1/S2 needs.

Implications for CFOs and Future Directions

Implications for Corporate Reporting and Decision-Making

The emergence of IFRS S1 and S2 has far-reaching implications for corporate finance:

-

Integrated Reporting: CFOs must now manage integrated reporting, blending financial and sustainability information in one package [13] [31]. This will likely reshape internal processes (closing the books might require greenhouse gas inventories to be finalized concurrently). Workflows will become cross-functional: finance teams will coordinate with operations, environmental, and HR teams to gather complete datasets.

-

Risk Management: S1/S2 elevate ESG factors into enterprise risk management. Finance will need to quantify ESG risks (using scenario analysis for climate under S2 [33], stress tests for resource shortages, etc.) and embed them in forecasts and valuation models. Companies may update budgets and long-term plans to reflect carbon pricing, regulatory changes, or climate-impact on assets.

-

Strategic Finance: CFOs will want to allocate capital differently. The financial effects required by S1 include current and anticipated impacts of sustainability issues [59] [60]. This trend opens the “door to new opportunities” when sustainability drives performance [61]. For example, cost savings from energy efficiency should be quantified and reported; market opportunities from green products should be modeled in revenue forecasts. In short, ESG becomes a quantitative input to the P&L and balance sheet analyses.

-

Stakeholder Communication: CFOs will increasingly handle sustainability-related investor queries. Surveys show a marked rise in investor demand for ESG details [51] [4]. As a result, CFOs must be prepared to explain climate scenarios, emission metrics, and governance practices to analysts and rating agencies. Transparent, well-structured disclosures aligned with IFRS S1/S2 will improve investor confidence by reducing perceived greenwashing risk [4].

-

Assurance and Controls: Just as financial statements are audited, S1/S2 disclosures may require third-party assurance in many jurisdictions (EU members already require it under CSRD). CFOs will need to ensure that internal controls cover ESG data collection (quality checks, reconciliations, etc.). The high rates of data problems seen in surveys [4]suggest that upgrading these controls is non-negotiable. NetSuite’s audit trails and permission structures can support this by documenting every data entry and calculation.

-

Talent and Culture: Finally, CFOs may need to upgrade their own teams. Building sustainability reports requires knowledge of environmental science, supply chain, HR analytics (for social factors), and more. Many companies are designating sustainability officers who work under the CFO or Treasury. CFOs themselves will need training to interpret environmental metrics and integrate them into financial models. As one ESG strategist notes, traditional finance culture is “changing fast; the CFO office is being reshaped” by these demands [62].

Future Outlook

Looking ahead, the IFRS sustainability standards are still evolving. The ISSB has already begun projects beyond climate. In Dec 2025, it released amendments on extended greenhouse gas disclosures (especially for the financial sector) [63]. New standards on nature (biodiversity) and possibly human capital are under development. CFOs should stay alert: future ISSB releases will likely mirror IFRS Accounting’s longstanding evolution. For example, just as IFRS has add-ons (IFRS 9 for financial instruments, IFRS 16 for leases, etc.), we can expect topic-specific ESG standards (biodiversity, emissions trading, etc.).

For companies, this means building flexible reporting systems. NetSuite’s adaptability will be an asset – fields and dashboards added today for IFRS S2 can be repurposed for nature metrics tomorrow. Jurisdictionally, any country can choose to mandate IFRS S1/S2 or modify them. So far, regulators in Asia-Pacific, Latin America, and parts of Africa have signaled support for ISSB-based rules. CFOs should monitor their local developments (IFRS Foundation’s Jurisdictional Profiles [49] provide guidance).

Performance-wise, early evidence suggests strong adoption pressure. Already “over two-thirds” of U.S. public companies had climate disclosures by mid-2020s, and Europe mandates will soon cover nearly all large firms. As one CFO expert asserted, sustainability reporting is “not just a trend” but an expected part of doing business [64]. The gradual convergence of standards (ISSB working with GRI, CSRD and others [47]) means that in the future there may truly be one global baseline. CFOs would do well to think of IFRS S1/S2 as the new normal for annual reporting, and to actively shape their systems and strategies accordingly.

Conclusion

IFRS S1 and S2 mark a watershed in corporate reporting: sustainability disclosures have finally been enshrined in a global financial reporting framework. For CFOs and finance teams, these standards turn ESG from a niche concern into a core financial issue. Meeting the IFRS S1/S2 requirements will demand careful planning, cross-functional collaboration, and robust information systems. Key takeaways include:

-

Sustainability = Finance: IFRS S1/S2 require sustainability-related risks/opportunities to be evaluated in financial terms, with disclosures alongside the financial statements [1]. CFOs must therefore lead the integration of ESG into budgeting, forecasting and reporting.

-

Data and Systems: Effective implementation rests on reliable data and efficient systems. Surveys show most companies struggle with ESG data quality [4], so finance executives should invest in automation and controls. Cloud ERPs like NetSuite can centralize ESG metrics with financial data, automate calculations (e.g. emissions tracking), and support auditability [5] [6]. Leveraging specialized modules or partners (e.g. CarbonSuite, RSM ESG) can accelerate compliance.

-

Global Convergence: IFRS S1/S2 are designed as an investor-focused global baseline, but companies must also navigate local rules (such as EU CSRD) [1]. CFOs should map these requirements carefully, using one platform to generate multiple reporting outputs where possible. Coherence among frameworks is improving – for instance, S1/S2 incorporates TCFD and SASB, facilitating data reuse [46] [42].

-

Future Preparedness: Sustainability reporting demands will only grow. IFRS is already planning new topics and refinements, and regulators worldwide are moving toward mandatory ESG rules. CFOs should see IFRS S1/S2 compliance not merely as a one-time project but as the start of an ongoing reporting evolution. This means building dynamic capabilities: adaptable ERPs, continuous data improvement, and a sustainability-literate finance organization.

In conclusion, IFRS S1 and S2 place the finance function at the heart of ESG reporting. By understanding these standards and proactively leveraging tools like NetSuite, CFOs can turn the challenge of sustainability disclosure into an opportunity – strengthening investor trust and uncovering value from sustainability initiatives. The integration of ESG into financial reporting aligns capital allocation with long-term risks and opportunities, paving the way for more resilient, transparent enterprises in the face of global challenges.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.