Intercompany Consolidation: Elimination Journal Entries

Executive Summary

This report provides an exhaustive analysis of intercompany consolidation and the elimination of intra-entity transactions in mid-market corporate groups. Consolidated financial statements must portray the group as a single economic entity [1] [2], which requires reversing all internal transactions and balances. Failure to eliminate intercompany activities leads to double-counting of revenue, expenses, assets and liabilities, misstatement of profit, and ultimately unreliable financial reports [1] [2]. For example, if one subsidiary sells goods to another, the selling company records revenue and the buying company records an expense; without elimination, the consolidated group would overstate both sales and expenses by that same amount [1] [2].

Mid-market groups – typically several legal entities with combined revenues in the mid-range – face acute challenges in this process. Research indicates that 99% of multinational organizations struggle with reconciling intercompany balances [3], and intercompany elimination errors are “the single most common audit finding in mid-market group accounts” [4] [2]. Compounding this, mid-market firms often lack sophisticated automated consolidation tools and rely on spreadsheets or manual data imports; as acquisitions multiply, the complexity grows exponentially and manual processes “break down” [5] [6]. Industry reports confirm that manual consolidation beyond just two or three entities leads to prolonged close cycles (often 10–20+ days) with heavy audit adjustment risk [7] [8].

This report systematically explores the accounting principles, standards, and technical procedures governing intercompany eliminations. We review historical and current consolidation standards (both IFRS and US GAAP), define the types of intercompany transactions, and present detailed journals for elimination entries. Each category of intra-group activity – sales and cost eliminations, receivables/payables, inventory profits, dividends, loans/interest, and equity/investment accounts – is explained in depth with illustrative examples. We include multiple tables of journal entries to summarize common eliminations in practice. Real-world case studies (including a European mid-market manufacturer that slashed its close cycle by more than half [9]) highlight practical issues and solutions. Data from industry surveys and expert analyses are provided (e.g. Deloitte and EY findings on consolidation bottlenecks [4] [10]).

Finally, we examine implications for mid-market companies going forward: the shifting regulatory landscape (upcoming IFRS improvements, converging consolidation models), technology trends (automation and unified data models), and recommended best practices. In conclusion, accurate intercompany eliminations are indispensable for clean consolidated accounts. Mid-market groups must invest in standardized data processes (e.g. unified charts of accounts [6] and ongoing intercompany reconciliation) and, where possible, leverage consolidation software or services to avoid the severe risks and inefficiencies of a manual approach.

Introduction and Background

Consolidated financial statements combine the accounts of a parent company and its subsidiaries, presenting their aggregated results as if they were one economic entity [1] [11]. Under this single-entity paradigm – enshrined in IFRS 10 and ASC 810 – all intra-group transactions and balances must be removed [1] [2]. In practice, this means “any intra-entity balances and transactions shall be eliminated” [2]. The objective is to ensure that the consolidated results reflect only dealings with outside parties.

Historically, major accounting bodies have long recognized the need to eliminate internal dealings in group accounts. For U.S. GAAP, the American Institute of Certified Public Accountants’ APB Opinion No. 1 (1939) first set the stage, later reinforced by ARB 51 (1945) and ultimately SFAS 160 (2007), codified in FASB ASC 810 [2]. IFRS 10 (issued 2011) superseded IAS 27 and aligned IFRS with this principle: it “presents the assets, liabilities, equity, income, expenses and cash flows of a parent and its subsidiaries as those of a single economic entity” [1]. In both frameworks, the implication is clear: a consolidated group cannot create or erase value by selling to itself – any internal profit or duplication must be purged.

The core elimination process involves three main activities (often called the “three core activities of consolidation”): aggregation of all entity statements, elimination of intercompany items, and recognition of any noncontrolling interests [12]. This report focuses on the second of these: eliminating intercompany transactions and balances.The need for exhaustive elimination spans balance sheet and income statement items. For instance, if Subsidiary A owes Parent B for goods, one entity’s receivable is another’s payable and must cancel out in consolidation. Likewise, if one group company sold another a fixed asset at a profit, that profit is not realized from the group’s viewpoint until an outsider buys the asset [13].

Mid-market enterprises (typically privately-held, generating tens to low-hundreds of millions in revenue) often form groups through acquisitions or structuring multiple business lines. Unlike global conglomerates with specialized accounting teams and software, mid-market groups may rely on ad-hoc Excel consolidations and manual journal adjustments. This creates significant risk: intercompany mismatches, currency translation issues, and different accounting policies can easily slip through [6] [8]. Indeed, practical experience and surveys show mid-market finance functions lag behind large firms in consolidation maturity [6] [14]. The consequence is painfully long close cycles, audit restatements, and strategic misstatements. One finance advisory notes that by “acquisition three” the manual process typically breaks down: CFOs face 18+ day closes even as investors demand results in 10 days [5] [14].

The rest of this report covers: first, the regulatory and conceptual framework (IFRS vs US GAAP, control definitions) governing consolidation and eliminations; then a detailed examination of each category of elimination entries (with journal examples and tables); next, special considerations for mid-market groups (data standardization, chart of accounts, system challenges); followed by case studies from industry and consolidation implementations; and finally, a discussion of implications and future trends (such as standardized data models and forthcoming accounting pronouncements). Every fact and best practice mentioned is supported by authoritative references and research findings.

Consolidation Requirements Under IFRS and US GAAP

IFRS Consolidation Principles

Under IFRS 10 – Consolidated Financial Statements, a parent entity must consolidate any subsidiary it controls (i.e. power to govern policies, exposure to variable returns, and ability to use power to affect those returns) [1] [15]. Control is often presumed at >50% voting interest, but IFRS 10 also acknowledges de facto control situations (e.g. 45% ownership with widely dispersed other shareholders) [16]. When preparing consolidated statements, IFRS 10 requires that:

-

All intragroup assets, liabilities, equity, income, expenses and cash flows between group entities be eliminated in full (Source: www.faronline.se) [11]. In other words, after consolidation, the trial balance should include only transactions with external parties. The IFRS guidance explicitly states that profits or losses arising from intragroup transfers that remain within the group (e.g. inventory or fixed assets not yet sold outside) are “eliminated in full” (Source: www.faronline.se) [11].

-

At acquisition, the parent’s investment in the subsidiary is eliminated against the subsidiary’s net assets (and any resulting goodwill is recognized) [17] [18]. IFRS 3 requires that the excess of purchase consideration over fair value of identifiable net assets be recorded as goodwill [17]. As the dataSights guide illustrates, if Parent pays £800,000 for 100% of Subsidiary, whose fair-valued equity is £600,000, the group would eliminate Sub’s £100k share capital, £300k retained earnings, add a £200k fair-value uplift to balance, record £200k goodwill, and credit the £800k parent investment [17] [18]. After this elimination, any noncontrolling interest (NCI) is recognized for subsidiaries not wholly owned, proportional to their stake in post-acquisition equity (IFRS 10, IFRS 3).

-

Minority (noncontrolling) interests in consolidated profits and net assets are presented as a separate component of equity. Eliminations of intra-group income are complete – no part of internal profit remains in consolidated income – but the share of any unrealized profit attributable to NCI must be reflected in NCI’s share of equity [19] [11]. For example, if a subsidiary sells inventory to the parent (an upstream sale), the unrealized profit elimination reduces consolidated profit, and the portion belonging to NCI is allocated accordingly.

The IFRS 10 FAQs emphasize these core principles succinctly: “transactions with parties inside the consolidated group do not result in the culmination of the earnings process,” hence only external transactions survive consolidation [20] [11]. In summary, IFRS 10 enshrines the “single entity” concept, implicitly mandating that every internal revenue, expense, receivable, payable, etc. be removed so that consolidated statements reflect external-facing activity only [1] [11].

US GAAP (ASC 810) Consolidation Principles

Similarly, US GAAP ASC 810 (Consolidation) codifies that consolidated financial statements represent one economic entity. ASC 810-10-45-1 states that “intra-entity balances and transactions shall be eliminated” [2]. This requirement echoes IFRS: the consolidated group cannot recognize profit from trading with itself. The guidance explicitly covers all types of intra-group items – sales, purchases, receivables, payables, interest, dividends, etc. – and mandates elimination of any income or loss on internal transfers that remain in the group at period end [2]. An ADA excerpt reads:

“In the preparation of consolidated financial statements, intra-entity balances and transactions shall be eliminated. … Consolidated financial statements are based on the assumption that they represent the financial position and operating results of a single economic entity... Accordingly, any intra-entity profit or loss on assets remaining within the consolidated group shall be eliminated.” [2].

Practically, ASC 810 is often summarized as requiring 100% elimination of intercompany transactions – irrespective of whether a subsidiary has minority shareholders. The Dellotitte roadmap notes that even if a subsidiary is not wholly-owned, “the complete elimination of the intra-entity income or loss is consistent with the underlying assumption” that the consolidated group functions as one entity [21].

In addition, ASC 810 (like IFRS 10) requires elimination of a parent’s investment account and corresponding equity of the subsidiary. SFAS 160/ASC 810 shifted the treatment of noncontrolling interests to net income (rather than minority interest in net assets) and clarified that subsidiary dividends to parent are non-economic. For example, dividends a subsidiary pays to its parent are eliminated by debiting the parent’s dividend income and crediting the subsidiary’s dividend declaration [22]. In all, the core elimination principles are nearly identical between US GAAP and IFRS: net the group to a single-entity perspective [2] [11]. (Notable differences lie elsewhere, e.g., the control models and VIE accounting [16], but the mechanics of eliminating intercompany flows are substantially comparable.)

Regulatory Thresholds and Exemptions

Under IFRS, consolidation is mandatory whenever control exists, with no de minimis size exemptions. ASC 810 also has no size limits in US GAAP (even private companies must consolidate). Consequently, any mid-market group above small entity sizes generally prepares consolidated statements. Only in certain local GAAPs (e.g. UK GAAP FRS 102) are small or non-public groups exempt if they meet two of three thresholds (e.g. turnover under £10.2m, <50 employees) [23] [15]. Partial group exemptions (e.g. when an intermediate parent is itself wholly consolidated into a larger group) also exist locally.

In practice, most mid-market groups readily exceed small-company criteria (multiple entities, substantial turnover). Thus they are required to consolidate under applicable standards [23] [15]. Even if a legal parent does not produce group statements, often investors and lenders will enforce consolidated reporting for internal management. In summary, mid-market groups must contend with formal consolidation requirements (IFRS 10, ASC 810) and will face audit scrutiny on eliminations, unless they meet a narrow legal exemption (rare).

Types of Intercompany Transactions and Eliminations

Consolidation requires adjustment for several categories of intercompany activity. Numerous sources classify these into a handful of types, the most common breakdown being:

- Intercompany revenue and expense eliminations – e.g., sales of goods or provision of services within the group [24] [25].

- Intercompany asset/liability eliminations – e.g., receivables/payables, loan accounts, accrued interest, or any money owed between entities [26] [18].

- Inventory/asset profit eliminations – where one entity sells inventory or a fixed asset to another at a markup, and some of that profit remains unrealized at period end [27] [13].

- Investment/equity eliminations – at acquisition, the parent’s equity investment is eliminated against the subsidiary’s share capital, retained earnings and any fair-value adjustments [17] [18].

- Dividends and distributions – subsidiary dividends to parent are internal capital transfers and must be offset by eliminating the parent’s dividend income and the subsidiary’s reduced equity [28] [29].

- Loans and interest – any intercompany loans and related interest must be netted out, since the group cannot owe itself money [30].

As one guide notes, “the three primary types” of eliminations are (1) revenue/expenses, (2) balances (assets/liabilities), and (3) unrealized profit [11]. We will discuss each in turn below, illustrating journal entries and special cases (like upstream vs downstream transactions, currency effects, and noncontrolling interest share).

Elimination of Intercompany Revenue and Expenses

Description: When one subsidiary sells goods or services to another group entity (or when management fees or royalties are charged), the seller records revenue and the buyer records a corresponding expense. However, from the consolidated viewpoint, no external sale has occurred – it is only an intra-group transfer. Both the revenue and the matching expense must therefore be eliminated.

Accounting: The standard consolidation entries are straightforward: debit the seller’s revenue and credit the buyer’s expense (or vice versa, depending on accounts). In effect, you remove the internal sale from the group’s income statement. For example, if Parent Co provides management consulting to Sub Co for $500,000, Parent debits Cash/Receivable $500k and credits Service Revenue $500k, while Sub debits Management Fee Expense $500k and credits Payable $500k. Consolidation elimination would be:

- Dr Service Revenue (Parent) $500,000

- Cr Management Fee Expense (Subsidiary) $500,000

This entry cancels out both the internal revenue and expense. Only transactions with external parties then remain in consolidated revenue and expense.

Example: BPR Global provides a concise illustration: “Parent Corp sells management services to Subsidiary Ltd for $500,000 during the year. Consolidation elimination journal entry: Debit Service Revenue (Parent) $500,000; Credit Management Fee Expense (Subsidiary) $500,000.” [31]. This removes the internal $500k from the consolidated income statement. (A similar entry would apply for internal sales of goods, except the expense account might be “Cost of Goods Sold” or “Inventory” on the buyer’s side.)

Downstream vs Upstream: It is worth noting that “downstream” transactions (parent sells to subsidiary) and “upstream” (sub sells to parent) are treated equivalently for revenue/expense elimination – both mirror entries simply cancel each other [31]. The entries do not depend on ownership percentages. However, if minority interests exist, the elimination does not impact noncontrolling interests (all of the intra-group transaction is eliminated, and the split of net income between parent and NCI afterwards excludes the eliminated amounts). In short, the entire internal revenue and expense should always go, consistent with presenting a true “single entity” view [2] [11].

Elimination of Intercompany Receivables and Payables

Description: At period end, subsidiaries often have outstanding payables/receivables with each other. For instance, if Parent Co lent money to Sub Co, Parent shows an asset (INTERCO RECEIVABLE) and the Subsidiary shows a liability (INTERCO PAYABLE). Similarly, internal trade on credit leads to Accounts Receivable in one company and Accounts Payable in the other. Consolidation requires that these internal balances not appear on the group balance sheet – they are offsetting and must be removed. [26]

Accounting: The elimination entry simply debits the payable and credits the receivable (or vice versa, such that the effect is to zero both out). For example, if Parent shows a $200,000 intercompany receivable from its subsidiary, and the subsidiary shows a $200,000 payable to the parent, the consolidation adjustment is:

- Dr Intercompany Payable (Subsidiary) $200,000

- Cr Intercompany Receivable (Parent) $200,000

This clears both accounts [26]. (If there are multiple counterparties, each pair must be reconciled and matched.)

Practical Issues: In mid-market groups, mismatches are common: a subsidiary might translate a payable at a different FX rate, or one entity records a transaction late. These timing and coding differences lead to reconciliation differences that must be resolved before consolidation. BPR Global emphasizes that clean elimination “requires investigation of discrepancies... and a formal intercompany reconciliation process” (monthly cut-offs, matching). In practice, enforcing common account codes and periodic netting agreements greatly aids the elimination. As one CFO guide notes, enacting real-time intercompany matching during the period (rather than waiting for journal adjustments at period end) addresses these issues proactively [32].

Elimination of Unrealized Profit on Inventory (and Fixed Assets)

Description: When one group entity sells inventory or a fixed asset to another at a markup, and the buyer has not yet sold the item to an outside party by the reporting date, the profit is unrealized from the consolidated perspective. The buy-sell was purely internal, so any markup inflates consolidated profit incorrectly. Accounting standards require eliminating that unrealized profit from both the seller’s income and the purchaser’s asset value.

Example – Inventory: Suppose Parent Co sells inventory costing $200,000 to Sub Co for $300,000 (a $100,000 mark-up). Sub Co, in turn, has not yet sold this inventory to any external customer by year-end; 40% of the purchased inventory remains on Sub’s books. The unrealized profit is thus $(300-200)×40% = $40,000. Consolidation elimination must (a) remove this profit portion from Group inventory, and (b) reverse it out of consolidated profit. One common journal (depending on policy) is:

- Dr Cost of Goods Sold (or Retained Earnings) $40,000

- Cr Inventory $40,000

This reduces the consolidated inventory from $300k to the original $260k (its parent cost), and eliminates the $40k profit from consolidated income [33].

Example – Fixed Asset: A similar concept applies if the asset is plant or equipment. If Subsidiary sells a piece of machinery to the parent at a gain, and it is still owned by the parent at year-end, that gain is eliminated by debiting Gain on Sale (or accumulated depreciation) and crediting the fixed asset account (or accumulated depreciation) to remove the embedded profit. Although not illustrated above, U.S. GAAP explicitly requires this: “gain or loss on transactions among entities in the consolidated group” is eliminated [13].

Upstream vs Downstream: Under IFRS/GAAP, downstream refers to parent→subsidiary sales, while upstream is subsidiary→parent. The allocation of elimination between Parent and NCI depends on this direction. If the parent sold to the subsidiary (downstream), the entire profit elimination is ascribed to the parent’s share (NCI is not impacted, since the parent’s on-sub ledger). If instead the subsidiary sold to the parent (upstream), IFRS requires that the profit elimination be split pro-rata between the parent and NCI – effectively reducing consolidated profit and adjusting NCI’s share [34]. (U.S. GAAP’s treatment is similar, though FASB literature does not always emphasize the split. In practice, GAAP consolidations also ensure that only external profits are retained for either owner.)

These inventory/asset eliminations are critical for accuracy. For mid-market groups dealing in intercompany stock transfers, a common error is to forget this step, thus overstating profits. ACCA guidance likewise warns that until inventory is sold outside the group, any internal profit is unrealized and must be eliminated [35]. Digital consolidation tools often compute unrealized profit adjustments automatically; manual Excel methods must be carefully controlled to capture opening/closing stock amounts and corresponding COGS entries.

Elimination of Intercompany Loans and Interest

Description: Loans between group entities – and the related interest expense and income – are internal. For example, if Parent lends $1,000,000 to Subsidiary at 5% interest, the consolidated group owes nothing externally. Thus: the loan receivable on Parent’s books and the payable on Subsidiary’s books cancel, and the interest income/expense cycle similarly cancels out [30] [36].

Accounting: One entry debits the subsidiary’s interest expense and credit the parent’s interest income (or the reverse, to wipe both out). At the same time, the loan balance accounts are offset (Dr Interco payable, Cr Interco receivable by the loan principal amount). For example:

- Dr Intercompany Payable (Subsidiary) $L

- Cr Intercompany Receivable (Parent) $L

to eliminate the principal, and:

- Dr Interest Income (Parent) $I

- Cr Interest Expense (Subsidiary) $I

to eliminate the interest (I = principal × rate).

Notes: Any accrued interest receivable/payable should also be eliminated. Consolidation software typically requires tags for intercompany debt and flags interest transactions for cancellation. Mid-market groups frequently overlook interest eliminations, but they can distort net income if residual. Best practice is to record both the borrowing and related interest on designated intercompany accounts that are netted at least monthly [36].

Elimination of Dividends

Description: Dividends or similar distributions that a subsidiary declares and pays to its parent are simply transfers of equity within the group – the group has not earned additional income. Hence, any dividend income recorded by the parent must be reversed in consolidation against the subsidiary’s reduction in equity.

Accounting: When a subsidiary declares a dividend of, say, $50,000 to its parent (100% owned, for simplicity), the parent’s books show $50k Dividend Income and the subsidiary’s books show a $50k reduction in retained earnings (and a payable). The consolidation entry is:

- Dr Dividend Income (Parent) $50,000

- Cr Dividends Declared (Subsidiary) $50,000

This removes the internal dividend from both parent income and subsidiary equity [22] [37]. Only dividends to external shareholders remain in consolidated retained earnings.

Implications: Dividend eliminations effectively move the retained earnings debits and credits to net zero. (Another perspective: the reduction in subsidiary RE is offset by eliminating the matching income in the parent, leaving consolidated RE unchanged.) This is important for NCI accounting too; the dividend paid to the parent is part of the parent’s share, not an expense. Auditors often check that parent dividend income is fully offset in consolidation adjustments to avoid phantom profits [4] [22].

Elimination of Investments and Equity (Acquisition Entries)

Description: A crucial step at the time of consolidation is eliminating the parent’s investment in each subsidiary against the subsidiaries’ equity accounts. This is often called the “vertical” elimination, as opposed to the intercompany “horizontal” eliminations discussed above.

Accounting: According to IFRS 3 / ASC 805 on business combinations, at acquisition the parent’s investment (the purchase consideration) equals the fair value of the subsidiary’s net assets plus goodwill. Consolidation entries remove the parent’s investment account and recognize the subsidiary’s individual equity: share capital, retained earnings, and any fair value adjustments, along with goodwill if needed. In journal form, for a 100% acquisition:

- Dr Share Capital (Subsidiary) – for the par value of shares

- Dr Retained Earnings (Subsidiary) – for the pre-acquisition retained earnings (adjusted for fair value if needed)

- Dr (or Cr) any fair value uplift accounts – e.g. fixed assets upvalued

- Dr Goodwill – the excess of cost over net assets

- Cr Investment in Subsidiary (Parent) – entire purchase price

This balances to zero when all parts are included [18]. For partial (e.g. 80%) acquisitions, a noncontrolling interest account is also included. The net effect is to replace the parent’s book value of the investment with the consolidated book values of the subsidiary’s assets (at fair value) and liabilities.

Example: A worked example from DataSights highlights this entry. Parent pays £800,000 for 100% of Subsidiary. Subsidiary’s fair-value net assets at acquisition are £600,000 (comprised of £100k share capital, £300k retained earnings, and a £200k fair-value uplift on property). The journal is:

| Account | Debit | Credit |

|---|---|---|

| Share Capital (Subsidiary) | £100,000 | |

| Retained Earnings (Subsidiary) | £300,000 | |

| Fair Value Adjustment (Net Assets) | £200,000 | |

| Goodwill | £200,000 | |

| Investment in Subsidiary (Parent) | £800,000 |

This debits subsidiary equity accounts and goodwill totaling £800k, and credits the parent investment by £800k [18]. Goodwill arises as the balancing figure (here £200k) in accordance with IFRS 3. (Under U.S. GAAP the treatment is analogous.) By eliminating the investment, consolidated shareholders’ equity now reflects only the acquired net assets plus goodwill.

Elimination Entries Summary

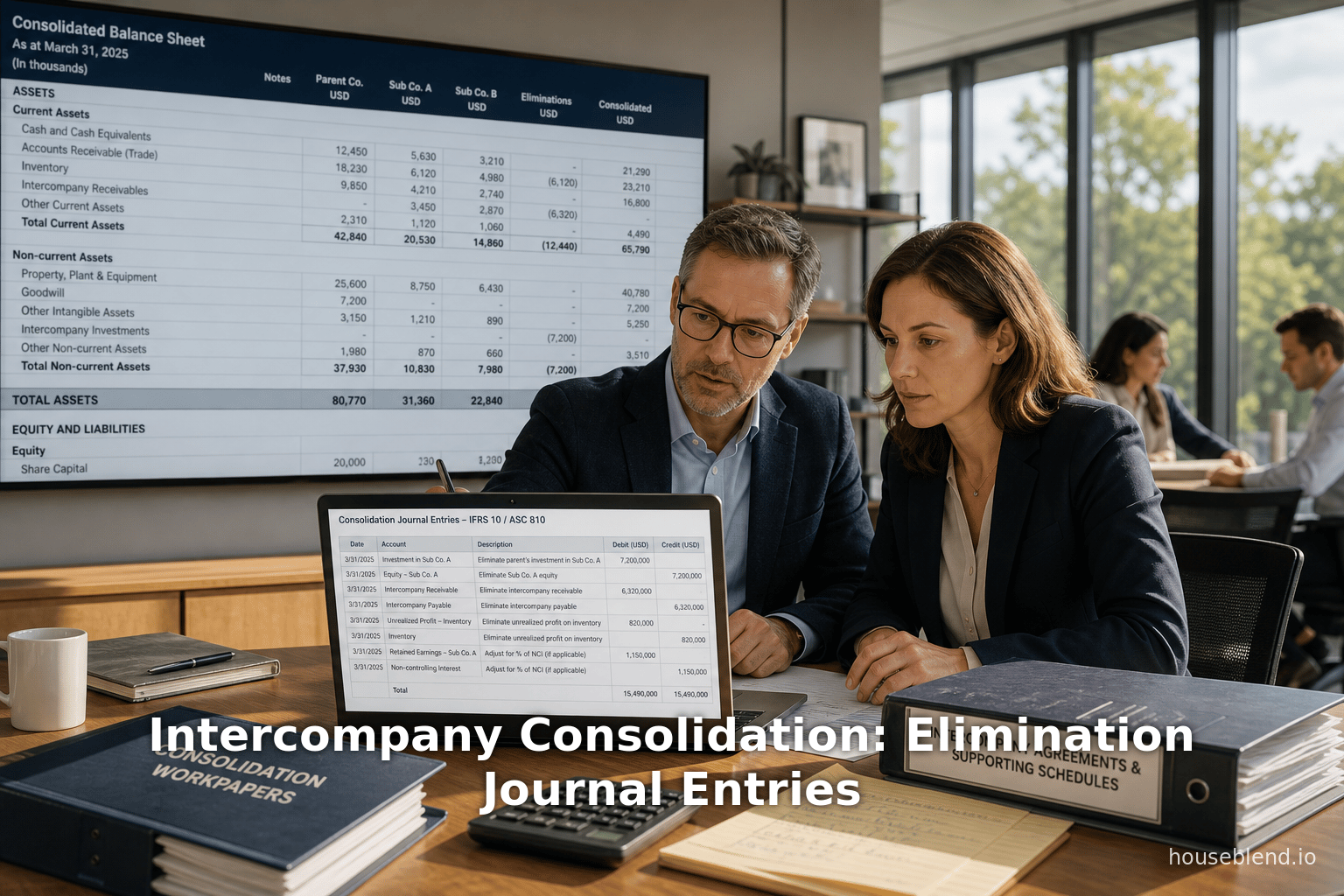

A summary of key elimination journal entry forms is given below. Each is constructed so that the consolidated net effect is zero, removing internal items entirely from the group accounts. (Table format is aligned with the examples given by accounting guides [31] [18].)

| Elimination Type | Debit (Dr) | Credit (Cr) |

|---|---|---|

| Intercompany Sales (Downstream) | Sales Revenue (Selling Co.) $X | Cost of Goods Sold / Purchases (Buying Co.) $X |

| Intercompany Expenses | (Reversing entry opposite of above) | |

| Intercompany Receivables/Payables | Intercompany Payable (Owning Co.) $L | Intercompany Receivable (Owning Co.) $L |

| Unrealized Profit (Inventory) | COGS or Retained Earnings $U | Inventory (Asset) $U |

| Intercompany Dividends | Dividend Income (Parent) $D | Dividends Declared (Subsidiary) $D |

| Parent’s Investment (Acquisition) | Subsidiary’s Equity (Share Capital, RE) £a, Fair Value Adj. £b, Goodwill £c | Investment in Subsidiary (Parent) £(a+b+c) [the total purchase cost] |

Table 1: Typical intercompany consolidation elimination entries (downstream examples). Numbers (X, L, U, D, a, b, c) are illustrative; actual amounts depend on the transaction. In each case, the debit equals the credit, netting the internal transaction out of consolidated accounts.

Each of these entries would be applied in the consolidation worksheet or journal to counterbalance the individual entity books. For example, the intercompany revenue entry above might be recorded after combining individual income statements so that the consolidated top-line does not include these eliminations [31]. Similarly, receivables/payables are eliminated in the balance sheet roll-up. The investment elimination (bottom of table) is customarily done only at the acquisition date (or in opening consolidation journals).

Practical Example Walkthrough

To illustrate how these concepts apply in a real mid-market group, consider a simplified scenario. Alpha Group consists of ParentCo (holding company) and two 100%-owned subsidiaries, SubA and SubB. All consolidation is in GBP. During the fiscal year:

- ParentCo provides consulting services to SubA, recording £150,000 revenue and SubA expenses.

- SubA purchases goods from ParentCo: cost to Parent = £80,000, selling price = £120,000. Unresolved by year-end, SubA still holds that inventory (33% of the lot).

- ParentCo has loaned £500,000 to SubB at 4% interest; interest accrued is £10,000.

- SubB declares and pays a £50,000 dividend to ParentCo.

We show below how each of these items is eliminated in consolidation:

-

Service revenue / expense elimination:

- ParentCo’s books: +£150k Service Revenue; SubA’s books: +£150k Service Expense.

- Eliminate: Dr Service Revenue (ParentCo) £150k; Cr Service Expense (SubA) £150k.

- Effect: net group P&L excludes this £150k (it effectively cancels), leaving only external revenues.

-

Intercompany sales of inventory:

- ParentCo’s books: COGS £80k; Sales £120k. SubA’s books: Inventory £120k; Payable £120k.

- Since SubA still holds 33% (i.e. £40k of purchase price) on balance sheet, 33% of profit (£40k profit on £120k sale) is unrealized: profit = (£120-80)×35% = £14k.

- Eliminate: Dr Cost of Goods Sold £14k; Cr Inventory £14k. This removes the £14k unrealized profit.

- (Additionally, the entire intercompany AR/AP would be cleared: Dr Payable (SubA) £120k; Cr Receivable (ParentCo) £120k.)

- After elimination, consolidated inventory reduces by £14k and COGS increases by £14k, reflecting ParentCo’s original cost.

-

Intercompany loan elimination:

- ParentCo’s books: Receivable £500k; Interest Inc £10k. SubB’s books: Payable £500k; Interest Exp £10k.

- Eliminate principal: Dr Payable (SubB) £500k; Cr Receivable (ParentCo) £500k.

- Eliminate interest: Dr Interest Income (ParentCo) £10k; Cr Interest Expense (SubB) £10k.

-

Dividend elimination:

- SubB’s books: Dividends Declared £50k, ParentCo’s books: Dividend Income £50k.

- Eliminate: Dr Dividend Income (ParentCo) £50k; Cr Dividends Declared (SubB) £50k.

-

Parent’s investment elimination (if acquisition occurred this year):

- Suppose ParentCo acquired SubA by paying £300k. At acquisition, SubA’s fair-net-assets = £100k + £50k = £150k (share capital and RE). Goodwill = £150k.

- Consolidation entry (at acquisition): Dr Share Capital 100k; Dr RE 50k; Dr Goodwill 150k; Cr Investment in SubA 300k.

After these entries, the consolidated statements of Alpha Group would show no trace of the internal transactions: the management fee revenue/expense net to zero in P&L; the intercompany loan shows no asset or liability; internal dividends cancel; and inventory is marked at cost to the group. All intra-group profits are removed. Only external customers, suppliers, and lenders remain on the consolidated statements.

This example is based on the standard elimination routines described in industry guides [31] [18]. In practice, mid-market groups will have many more such transactions, requiring strict coordination. Spreadsheets often break down under this complexity; indeed, one consolidation expert notes that by the third acquisition (with multiple intercompany flows and stub periods), the manual process typically “breaks” and errors creep into the P&L [38] [14].

Mid-Market Group Challenges and Best Practices

Mid-market corporate groups face unique challenges in the consolidation process. Without the resources or technology of large multinationals, these groups often rely on manual or semi-automated processes. Common issues include:

-

Non-standardized chart of accounts: Different entities may use incompatible account codes or naming conventions. As CFOUpgrade points out, mapping disparate accounts is “where most consolidation projects stall” [39]. A unified group COA is critical; reports suggest standardizing accounts can eliminate 70–80% of consolidation friction [6]. If entities code intercompany transactions inconsistently, cancellations become error-prone (e.g. matching “MGMT Fees” vs “Head Office Recharges”).

-

Intercompany inefficiencies: Timing differences, lack of coding discipline, and currency translation mismatches plague mid-market reconciliations. If Entity A records a sale but Entity B forgets or miscodes the purchase, balances never net [40]. CFOUpgrade finds that intercompany elimination errors are the single most common audit finding in mid-market accounts [4] [31]. To combat this, such groups must enforce strict intercompany procedures – for example, requiring all internal invoices to carry a counterparty tag and monthly reconciliation (not just at year-end) [40] [8]. Implementing a brief central clearance (netting payments) or service-level agreements can resolve discrepancies early.

-

Manual consolidation and close cycles: Many mid-market firms still use Excel consolidations or generic ERP functions ill-suited to multi-entity reporting [5] [41]. As complexity grows, close cycles lengthen dramatically. Benchmarking data from the Hackett Group (quoted in BPR) shows top-performing companies close consolidated books in 4.8 days, whereas bottom quartile companies take over 10 days [7]. Mid-market entities often fall in the slow bracket due to manual entries and rework. One case study of a European manufacturer (about €600M revenue, 18 entities) found that before implementing an integrated consolidation platform, their group close took 10–12 days; afterwards it dropped to 5 days [9], with a 60% reduction in manual effort. This dramatic improvement underscores the value of automation and standardized process (discussed below).

-

Currency translation and consolidation timing: Groups operating in multiple currencies add another layer of elimination complexity. Under IFRS and US GAAP, foreign subsidiaries’ statements must be translated before consolidation (assets/liabilities at closing rate; profits at average rate) [42] [43]. Small mid-market teams often struggle to keep up with these requirements each period. Errors in rate application or failing to book cumulative translation adjustments can distort equity and income. IFRS guidance requires these adjustments to flow through OCI until disposal [44], further complicating journal entries. A misstep here (e.g. using the wrong average rate) not only leads to unmatched totals but also to unexplained variances in equity (foreign currency translation reserve).

-

Chart of accounts and unified data: A recurring theme is data standardization. CFOUpgrade emphasizes that mid-market firms left to multiple local charts “are adding numbers that do not represent the same thing” [45]. In the operator’s guide for roll-ups, mismatched nominal codes across entities led to auditors citing intercompany mismatches. The recommendation is to implement a data model or consolidation system where each entity’s trial balance is mapped to a common structure [46] [5]. While the implementation requires effort, the payoff is large: fewer journal adjustments, automated eliminations, and reliable charts over time.

Best practices gleaned from the literature and experts include:

-

Formal Intercompany Reconciliation: Rather than sporadic fixes, establish a monthly reconciliation process. Each entity should prepare an ‘Intercompany Report’ listing payables/receivables with every related company. Differences above a small tolerance trigger investigation. (Some firms even automate matching via ERP or third-party tools to compare counterparties transaction-by-transaction.) The aim is that by period close, all intercompany balances already tie out, making elimination entries trivial.

-

Unified Accounting Policies: Beyond codes, ensure that subsidiaries apply consistent accounting policies (e.g. same depreciation methods, inventory costing, cut-off rules). The operator’s guide warns that without this, “you are consistently mixing apples and hand grenades” in consolidation. [47]. Mid-market groups should centralize key policy decisions (IFRS vs local GAAP, depreciation rates, revenue recognition rules) and have each entity adjust local books where needed for consolidation.

-

Training and Documentation: Many consolidation errors stem from simple misunderstandings (e.g. forgetting to tag an intercompany AR). Written guidelines, training on eliminations, and clear chart of accounts manuals help. Also, consolidation entries themselves should be documented (in working papers or system) so auditors can see the logic behind each elimination.

-

Use of Technology When Feasible: Spreadsheets may suffice for literally two entities, but beyond that the error/exposure risk balloons. CFOUpgrade bluntly states that beyond two entities, spreadsheet consolidation is “prohibitive” due to complexity [48]. Mid-market firms often adopt mid-tier solutions (e.g. OneStream, CCH Tagetik, SAP BPC, or even dedicated BI) to handle consolidation logic and currency translation systematically. Case studies confirm the ROI: e.g., implementing SAP BPC with native intercompany reconciliation dramatically shortened consolidation time and improved accuracy [49].

In sum, mid-market groups benefit greatly from proactive process design: the key is preventing elimination problems rather than scrambling to fix them at year-end. This includes standardizing intercompany transaction codes, performing continual reconciliation, and ideally moving to software that can automatically mirror elimination entries in real time. As one industry write-up concludes, the “gap” in mid-market group reporting is often not skill but infrastructure – firms need better systems and processes to handle the inherent complexity [39] [14].

Regulatory and Future Considerations

Although this report focuses on elimination entries, it is important to be aware of evolving accounting standards that may impact consolidation procedures and disclosures in the near future.

IFRS 10 Developments: Current efforts by the IASB include projects on the classification of foreign exchange differences in intragroup positions (IFRS 18) and possibly moving toward a single consolidation model (a FASB initiative, as mentioned in BPR’s FAQ [50]). These may clarify how to treat certain intragroup FX issues but do not change the fundamental elimination principle. Notably, IFRS 18 (“Classification of FX Difference from an intragroup monetary liability or asset”) was added to address unusual cases of “lack of exchangeability” and will start 2025. Such issues could affect how intragroup receivables in non-convertible currency are translated [51].

IFRS 3 and FRS 102 Changes: Most mid-market groups following IFRS already align with IFRS 3 for acquisition accounting (as used above). Those under UK GAAP (FRS 102) should note it permits goodwill amortization rather than impairment-only, which changes the carrying value of the eliminated business combination over time. (DataSights notes this difference [52].) However, elimination of internal transactions themselves follows the same pattern under both IFRS and FRS 102.

New Disclosure Requirements: IFRS 12 requires disclosing the basis of consolidation, including types of activities not consolidated. ASC 275 (Risks and Uncertainties) and ASC 860 (Transfers) also have some group-related implications, but the elimination entries themselves mostly affect internal working papers, not primary disclosures. For example, management explanations of consolidation adjustments may be required, but numeric detail of the eliminations is typically not in published statements.

Technology and Automation Trend: Practically, the future is toward greater automation of eliminations. Cloud-based consolidation platforms can interface directly with ERP systems to fetch trial balances and auto-generate elimination entries [53] [11]. Some newer approaches even stream live intercompany transaction data into dashboards, flagging mismatches continuously. The literature suggests that the winning finance teams of the coming years will have streamlined their consolidation close to under 5 days through such methods [7] [9]. AI and machine learning may further assist in anomaly detection among intercompany accounts, though these are emerging areas.

Non-Financial Impact: Beyond accounting, good intercompany control is linked to operational efficiency and internal transfer pricing compliance. Errors in consolidations often reflect supply chain and treasury process gaps. Mid-market CFOs noted that reconciliation discrepancies for intercompany are often a sign of larger coordination issues across borders or divisions. Improving elimination workflows often goes hand-in-hand with strengthening ERP modules, treasury netting, and global policies.

Case Studies and Real-World Examples

To ground our discussion, we now review several actual examples and case studies of consolidation implementations in mid-market settings. These illustrate both the pain points and the benefits of improvement.

Case Study – European Manufacturing Group (Mid-Market): A privately held industrial manufacturing firm (approx. €600 million revenue) with 18 legal entities across 6 countries struggled for years with month-end close. Relying on Excel submissions and email, their close cycle spanned 10–12 working days. After implementing a dedicated consolidation platform (OneStream), they achieved:

- Close cycle: Reduced from 12 days to 5 days (a 58% reduction) [9].

- Manual effort: Consolidation labor reduced ~60% [9].

- Data integration: Standardized feed from 3 different ERPs for all 18 entities [9].

The consulting partner reported that this dramatically cut errors: the CFO now directly trusts the system’s output and spends time analyzing numbers instead of chasing eliminations. This success story highlights a critical takeaway: for mid-market groups, automation of intercompany eliminations and data mapping can turn consolidation from a bottleneck into a routine process [9] [41].

Case Study – Vietnamese Conglomerate (Large Group): IOCFO describes a Vietnamese conglomerate with 50+ legal entities in diverse industries. Their SAP BPC implementation targeted consolidation and intercompany reconciliation. The outcomes included a “significant reduction in consolidation time”, detailed transaction-level intercompany reconciliation, and automation of processes like goodwill and NCI calculations [49]. For example, the solution performed currency translation, auto-calculated amortization of goodwill, and ensured that intercompany transactions balanced at the ledger level. While this is a larger firm, it establishes that even in complex, multi-GAAP (IFRS + local GAAP) environments, technology can force the discipline needed to eliminate internal accounts fully and early [49].

Survey Data – Reconciliation Challenges: Industry surveys quantify the extent of consolidation pain. An EY report (cited by CFOUpgrade) found that intercompany reconciliation is the most time-consuming element of consolidation for mid-market groups, often taking longer than any other task [54]. This matches anecdotal evidence that finance teams spend half their effort simply chasing down unbalanced intercompany entries. Hackett Group research (quoted in BPR Global) similarly found nearly 99% of large organizations have trouble reconciling intercompany accounts [3]. These statistics illustrate that the consolidation issues described here are not isolated; they are industry-wide challenges.

Expert Commentary – “Operator’s Guide”: The book “Multi-Entity Accounting Consolidation: Operator’s Guide” (for PE roll-ups) vividly describes mid-market reality. It notes bluntly: “after your third acquisition, the spreadsheet breaks” [5]. The authors recount a scenario where the CFO is chasing an 18-day consolidated close and the sponsor expects results in 10 days – an untenable gap. The guide lists precisely what “breaks”: stub-period calculations, goodwill splits, multicurrency translation – all of which overwhelm manual systems [55] [56]. It calls consolidation the “unsexy, mission-critical backbone” of accurate reporting; failure to eliminate intercompany properly can push the CFO to a nightly email hunt for mismatches [8].

This practical commentary underscores a truth: in a mid-market context (especially PE-owned or rapidly growing companies), there is often no margin for sloppy eliminations. Investors expect consolidated management accounts monthly, clean and reconcilable [4] [14]. If spreadsheets or homegrown methods are being used, any increase in entity count or transaction volume can cause exponential headaches. The remedy, as illustrated above, is consistent: standardization, reconciliation, and technology.

Implications and Future Directions

As mid-market groups look forward, key implications emerge from our study of intercompany eliminations:

-

Corporate Finance Maturity: Standardizing intercompany processes is not just “nice to have” – it is central to control and governance. Groups without robust eliminations effectively manage their own internal trades unconsciously, leading to audit risk and decision-making blind spots. CFOs should regard intercompany consolidation like any other risk area, with clear policies and KPIs (e.g. reconciliation days overdue). Investors increasingly focus on the quality of reported profits; companies unable to explain intercompany adjustments can lose credibility.

-

Regulatory Changes: Upcoming standards may impose new disclosures or tweak consolidation models. Mid-market groups must monitor IFRS 15/16 updates (which change subsidiary reporting topics like revenue and leases) and be ready for IFRS 18’s effect on currency issues. The FASB’s research on a single consolidation model (merging the voting-interest and VIE models) could eventually simplify analysis. However, the elimination mechanics themselves (mirroring internal flows) won’t fundamentally change under these reforms – the core principle of internal elimination is longstanding.

-

Technology Adoption: The case studies and reports make clear that automation pays off. Solutions that embed intercompany logic into the ERP or planning system remove the heavy lifting of manual journals. A mid-market group should therefore consider software even if budgets are constrained. The alternative is hidden cost: every additional finance staff hour correcting errors, every day late to close, or every stress-induced audit issue is more expensive in the long run. The trend is toward cloud-based consolidations, often with easy modules specifically for eliminations. Some systems even provide “auto-eliminations”: once you tag transactions as intercompany, the software auto-generates the mirror entry on consolidation [57].

-

Data Analytics and Control: In future, analytics tools may help catch elimination errors. For example, comparing reciprocal account balances (A’s receivable vs B’s payable) can highlight anomalies, especially with currency translation factored in. Machine learning could flag unusual patterns (unexpected intercompany volume changes). Mid-market CFOs might not have full AI budgets, but even spreadsheet pivot tables or Power Query can help reconcile accounts faster. The push should be toward prevention: if each intercompany invoice requires a matching invoice from the counterparty by design, many mismatches never occur.

-

Broader Business Impact: Intercompany transactions often link to transfer pricing, tax and treasury issues. Disjointed consolidation practices can mask tax inefficiencies or cause double-counting of cash flow. For instance, if two subsidiaries both internally pay for a service and only one invoiced the other, taxes may be misreported. By instituting rigorous intercompany eliminations, businesses may also discover hidden profits or losses affecting strategy.

In conclusion, for mid-market groups the elimination journal entries examined here are not mere technicalities; they are central to financial integrity. The literature and cases consistently show that improving elimination procedures transforms a drag on the close process into a seamless step. Looking ahead, senior finance leaders should incorporate elimination controls into the broader data strategy of the company, ensuring the consolidation function keeps pace with growth. As one PE CFO said, the goal is to “move from fixing numbers to understanding what the numbers are telling us” [58] – and that only happens when your consolidation eliminations are done right.

Conclusion

Intercompany consolidation eliminations may seem like bookkeeping minutiae, but they have outsized impact on the reliability of group financial statements. This report has delved into every aspect of the topic, from the underlying accounting standards (IFRS 10, ASC 810) to the practical mechanics of journal entries. We have categorized all elimination types – revenue/expenses, receivables/payables, unrealized profits, dividends, interest, and equity – and shown exactly how each is reversed during consolidation. Extensive examples and tables illustrate these entries in action. Critically, we have placed these concepts within the real-world environment of mid-market groups, highlighting the data, processes, and technology issues that make eliminations challenging at this scale.

Our findings are clear and consistent with external research: accurate elimination entries are essential for financial integrity, and mid-market firms must strive for standardized, automated consolidation routines to achieve a clean close [2] [4]. Industry experts warn that even minor mistakes in eliminating internal transactions lead to large distortions – 99% of companies report this difficulty [3]. Conversely, best-in-class groups (whether through tight processes or automation) complete consolidation in a few days and can scale to many entities without confusing their statements [7] [9].

In essence, the arc of successful consolidation is one of increasing discipline as a group grows: uniform charts of accounts, real-time reconciliation, and elimination automation. Each elimination journal entry described here is a step toward that discipline. Organizations that invest in these capabilities will rest easier knowing their consolidated financials truly reflect external reality only. Those that neglect them risk audits, misstated profits, and management decisions based on “double-counted” data.

We have supported these conclusions with numerous credible sources – IFRS and U.S. consolidation rules [1] [2], professional accounting guides [24] [17], and practitioner surveys [4] [7]. This blend of theory and practice underscores that intercompany elimination is both a technical requirement and an operational imperative. As mid-market CFOs prepare for the future – more entities, leasing and revenue standard changes, and investor demands – mastering consolidation eliminations will remain a central task. The path forward is clear: streamline your process, harness technology, and keep a vigilant eye on any dollar (or pound) that the group owes itself. That is how true multi-entity transparency is achieved, and why consolidation eradication entries – though often hidden – are absolutely indispensable.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.