NetSuite Asset Retirement Obligations: ASC 410-20 Setup

Executive Summary

Asset retirement obligations (AROs) are legal obligations to dismantle, remove, or restore long-lived assets at the end of their useful lives. In financial accounting, U.S. GAAP (ASC 410-20) and IFRS (IAS 37/IFRIC 1) require companies to recognize an ARO liability at the present value of estimated retirement costs when the obligation is incurred [1] [2]. The matching asset retirement cost (ARC) is capitalized as part of the asset’s cost basis and subsequently depreciated over its life [3] [2]. Over time, the liability is increased (“accreted”) by interest expense and adjusted for any changes in estimated costs [3] [4]. Once the asset is actually retired, the recorded ARO is settled and any difference between actual removal costs and the liability is recognized as a gain or loss [1] [3].

NetSuite’s Fixed Assets Management (FAM) SuiteApp automates many aspects of asset accounting (acquisition, depreciation, retirement) [5], but it does not provide a built-in feature for ASC 410-20 compliance. Organizations using NetSuite must therefore configure custom processes. This typically involves setting up specific general ledger accounts (e.g. ARO Liability, Accretion Expense, and ARO Gain/Loss), adjusting asset records to include the capitalized ARO, and recording manual or scheduled journal entries to accrete the liability and track adjustments [3] [4]. Proper NetSuite configuration and careful accounting process design are essential to accurately reflect AROs in the financial statements under ASC 410-20.

This report provides a comprehensive guide to ARO accounting and implementation in NetSuite, including: the accounting standards (US GAAP vs IFRS) and their differences; the step-by-step accounting mechanics (recognition, accretion, remeasurement, settlement) with journal examples; the NetSuite setup and workaround procedures to capture ARO data; and case analyses illustrating typical ARO scenarios. We draw on authoritative sources (FASB, IASB, expert analyses) and real-world disclosures to underpin our discussion.

Key insights include:

-

ASC 410-20 Requirements: Under US GAAP, ASC 410-20 mandates recognition of an ARO liability at fair value (usually via a credit-adjusted risk-free discount rate) when a legal obligation to retire the asset is incurred [2] [3]. The liability is subsequently accreted and adjusted only for changes in cash‐flow estimates (the discount rate remains fixed) [6] [4]. Any gain or loss on settlement (when costs differ from estimates) is recognized at retirement [1] [3].

-

IFRS Comparison: IFRS treats AROs as provisions under IAS 37. A provision is recognized when an outflow is probable and can be reliably measured [7]. In practice this is analogous to GAAP recognition – a legal retirement obligation triggers a liability equal to the discounted future cost. Unlike GAAP, IFRS (via IFRIC 1) requires the discount rate to be updated each reporting period and the liability re-measured for changes in assumptions [8]. Salvage values are handled similarly in both frameworks (excluded from the obligation and accounted in the asset’s depreciation) [9] [3].

-

Implementation in NetSuite: NetSuite’s Fixed Assets module has no dedicated ARO fields. Practitioners must manually configure NetSuite to track ARCs and liabilities. This involves: enabling FAM and Lease Accounting (if applicable), defining ARO-specific GL accounts, adjusting or creating asset records to include ARC, and using amortization schedules or recurring journal entries for accretion and remeasurements. Setting up Multi-Book Accounting can allow parallel IFRS/GAAP compliance if needed [10]. All journal entries should be documented as asset cost adjustments or liability accruals so that NetSuite’s depreciation and retirement processes correctly consume the ARC and the liability.

-

Case Data & Impact: Many industries have extraordinarily large ARO balances. For example, one energy partnership’s disclosures show an ARO liability growing from $21.3M to $24.3M in a single year, driven by $1.374M of accretion and $2.33M of revisions in cost estimates [11] [3]. Another illustrative case (common in oil & gas involves capitalizing an ARO for an offshore platform: if a $10M platform has an estimated end-of-life retirement PV of $450k, ASC 410-20 requires debiting the asset and crediting ARO for $450k [12] [2]. These entries ensure the on-balance-sheet asset reflects the true cost and the liability is measured correctly.

-

Implications & Future Directions: As sustainability and regulatory scrutiny increase, accurate ARO accounting is critical.Companies are expected to model multiple decommissioning scenarios with probability weightings [4] and disclose assumptions transparently. NetSuite users must stay aware of accounting updates and consider automated enhancements (for example, future NetSuite releases or SuiteApps specifically addressing ARO compliance). Enhanced reporting and integration with environmental management systems are emerging trends. This guide outlines the current state of best practice and anticipates that ERP system support for ARO (including IFRS/GAAP nuances) will become more standardized.

All claims are supported by authoritative sources (FASB ASC, IASB standards, SEC disclosures, industry analyses). Inline citations (with URLs) are provided throughout.

Introduction and Background

Asset Retirement Obligations (AROs) arise when a company has a legal obligation to dismantle or remove a long-lived tangible asset at the end of its life, often due to environmental regulations or lease contracts. Typical examples include restoring land after oil & gas extraction, decommissioning nuclear facilities, or returning leased property to its original condition [13] [14]. By definition, AROs are liabilities of uncertain timing or amount (since exact future costs and retirement dates may be uncertain) [15] [16]. They differ from ordinary operating expenses or impairments because they are incurred through normal operations. (Importantly, if asset disposal costs arise due to accidents or improper operations, those are outside ASC 410 and fall under environmental remediation rules [17].)

Under U.S. GAAP (ASC 410-20), the requirement to recognize an ARO is triggered at the time the obligation is incurred – which is typically the same time as the asset’s acquisition, construction, or when normal operations begin to give rise to a future retirement duty [3] [16]. ASC 410-20 codifies FASB Statement 143 (SFAS 143) and focuses on measuring retirement obligations at fair value when recognized [3] [2]. Once recognized, the liability is adjusted only for the passage of time (unwinding of discount) and changes in the estimate of future cash flows [6] [4].

International standards handle AROs under the framework of provisions (IAS 37). An obligation qualifies as a provision when an outflow of resources is probable and a reliable estimate can be made [7]. This approach is substantively similar to ASC 410-20: the obligation arises (and a liability is recognized) when a legal (or constructive) obligation exists, and the measurement is at the present value of expected outflows [1] [7]. Under IAS 37 (and IFRIC 1), however, the discount rate is updated each period so that the liability is re-measured at current rates, whereas ASC 410-20 uses a credit-adjusted risk-free rate fixed at inception [8] [18]. Salvage or dismantling credits are excluded from the obligation measurement in both frameworks, instead affecting the depreciable base of the asset [9] [3].

For clarity, this report uses “ASC 410-20” to refer to U.S. GAAP ARO guidance, and notes IFRS/IAS parallels where useful. The accounting process can be summarized as follows:

-

Identification: Determine which assets carry a legal retirement obligation (e.g. ground leases, environmental laws). The obligation is fixed in law or contract, not contingent on operational failures [16].

-

Initial Measurement: Estimate the future retirement cash flows (including all dismantling, removal, site restoration costs) and compute the present value of this obligation. GAAP requires a credit‐adjusted discount rate [18], whereas IFRS uses a risk-free rate (and re-measures the liability over time) [8]. Uncertainty in timing/cost is resolved through probability-weighted scenarios, not deferred accounting [4]. The initial entry is to debit an asset retirement cost (ARC) and credit the ARO liability [3] [12].

-

Subsequent Measurement: Each period, the recorded ARO liability is increased by accretion expense (the unwinding of the discount) [3]. If estimates change, the liability is revised: increases in future costs add to the asset cost and liability (debit ARC, credit ARO), while decreases reverse it [3]. Under US GAAP, the discount rate remains unchanged; under IFRS, the rate may change and cause re-measurement [8]. Depreciation is charged on the total capitalized asset cost (including ARC).

-

Settlement: When the asset is retired, the actual removal costs are incurred and the obligation is settled. The ARO liability is relieved, and the asset is written off or disposed. Any difference between actual cost and the liability is recorded as a gain or loss on settlement [1] [3].

This accounting flow ensures that the balance sheet includes the full cost of an asset (including its future retirement costs) and the corresponding liability for removal, and that the income statement shows accretion expense (an operating expense) and any settlement gains/losses. For example, one partnership’s disclosures illustrate this clearly: they capitalized AROs into their oil & gas assets and recognized annual accretion (about $1.3–1.4M), resulting in an ARO liability that grew from $21.318M to $24.265M over one year [11] [3].

Implementing ARO accounting in an ERP like NetSuite requires careful setup, since NetSuite’s Fixed Asset Management does not automatically handle ASC 410. The following sections detail the accounting rules (GAAP vs IFRS), then show how to map these requirements into NetSuite’s features and processes.

Regulatory Standards: ASC 410-20 vs. IAS 37/IFRS

US GAAP (ASC 410-20)

ASC 410-20 specifically addresses Asset Retirement Obligations (AROs) under U.S. GAAP. It was originally issued as FASB Statement No. 143 (SFAS 143) in 2001 [19], to standardize the diverse practices for decommissioning liabilities in industries like energy and utilities. The core requirement is (ASC 410-20-25):

-

Recognition: An ARO liability is recognized when it is incurred (often at asset acquisition) if a reasonable estimate of fair value can be made [17] [6]. A “legal obligation” means an obligation enforceable by law or contract [16]. If no legal obligation exists (e.g. potential environmental impacts with no current law), or if the cost cannot be reasonably estimated, then no liability is recognized until these criteria are met.

-

Initial Measurement: The liability is measured at its fair value, which for ASC 410-20 purposes means the present value of expected future cash flows to retire the asset [3] [2]. ASC 410-20 encourages an expected present value method: companies often construct multiple retirement-cost scenarios with assigned probabilities and take a weighted average [4]. Any expected inflation should be included in the cash flows before discounting [20]. Key point: use a credit-adjusted risk-free rate for discounting (ASC 410-20-30-3, discussed further in ASC 410-20-35) [18]. The rate is fixed at initial recognition and is not updated subsequently under GAAP [6]. The capitalized amount (ARC) is recorded as part of the related asset.

-

Subsequent Measurement: After initial recognition, the liability is accreted for the passage of time: each period debit Accretion Expense and credit ARO Liability for the change in present value [3]. If estimates of cash flows change in future periods (due to new information), the liability is adjusted: increases in estimated cost are added to the asset basis (debit ARC) and to the liability (credit ARO), while decreases in cost reverse it (debit ARO, credit ARC) [3]. Critically, the discount rate is not changed, even if interest rates shift [6]. This means the unwinding of discount continues on the original basis.

-

Depreciation (Asset Retirement Cost): The ARC (which increases the asset’s carrying amount) is depreciated over the asset’s useful life on the same basis as the rest of the asset [3]. Basically, the increased cost is amortized via depreciation expense (or depletion for natural resources). Salvage values are not deducted when measuring the ARO liability [9]; instead any salvage remains in the asset’s depreciable base.

-

Settlement: When the asset is retired, the company incurs actual retirement costs. At settlement, the ARO liability is relieved. Simultaneously, the asset is disposed of (or written off), and any difference between the recorded ARO liability and the actual cash cost is recognized as a gain or loss [1] [3]. In summary, if actual cost > liability, record a loss; if actual < liability, record a gain.

The Deloitte Roadmaps (ASC 410-20) provide detailed guidance on each of these steps (including recognition exceptions and scope) [21]. For ASC 410-20, any contingent or conditional obligations (e.g. obligations triggered by uncertain future events if they become certain) must be recognized if the ARO can be reasonably estimated [22]. Uncertainty in timing or amount is handled via probability weighting, not by deferring recognition [22]. All these rules ensure a faithful present-value measurement of the retirement obligation on the balance sheet.

IFRS – IAS 37 and IFRIC 1

Under IFRS, ARO-like obligations are treated as provisions under IAS 37 (Provisions, Contingent Liabilities and Contingent Assets). A provision is defined as “a liability of uncertain timing or amount” for which:

- There is a present obligation (legal or constructive).

- An outflow of resources is probable.

- A reliable estimate can be made of the obligation amount [7].

When these conditions hold for an asset retirement (for example, a law requires decommissioning), an IFRS provision is recognized. The measurement follows IFRS guidelines: the provision is recorded at the current best estimate of the outflow, discounted to present value if the effect of time value is material [23]. In effect, this mirrors GAAP’s present-value approach. Both standards exclude salvage value from the obligation: salvage only affects the asset’s depreciation base [9] [23].

However, there are key differences between IFRS and U.S. GAAP for retirement provisions:

-

Discount Rate: IFRS requires using a current pre-tax risk-free rate for discounting. Unlike GAAP’s fixed credit-adjusted rate, the IFRS requirement (which comes via IFRIC 1 “Changes in Existing Decommissioning Liabilities”) mandates remeasurement of the liability at each reporting date if the discount rate changes. Quoting Oracle’s PeopleSoft guide on options: “If you use the IFRS option to process ARO, the risk-adjusted rate is used at the outset, but the rate is adjusted at each reporting date thereafter (the decommissioning obligation is re-measured… giving consideration to changes in the discount rate)” [8]. In contrast, “If you use the GAAP option to process ARO, no adjustments are made to the risk-adjusted rate over the life of the ARO asset; the obligation is adjusted only for changes in the amount or timing of cash flows…” [6]. Thus, IFRS will often show fluctuations in the liability due to discount rate changes, whereas GAAP will not.

-

Changes in Estimates: Both IFRS and GAAP adjust the liability for changes in cash-flow estimates or timing. Under IFRS, IAS 37-36 requires recalculating the provision if estimates change, with the offset to the carrying amount of the related asset (under IAS 16) [3]. Under GAAP, changes in estimated ARO are handled similarly by adjusting the asset cost and liability [3]. In practice the accounting entries are the same for increases/decreases in costs, but IFRS treatment of discount changes introduces additional volatility for IFRS preparers.

-

Presentation: IFRS typically classifies provisions (ARO) under non-current liabilities, with current portion disclosed separately if material [24]. GAAP does similarly by presenting current vs. noncurrent ARO. Both require a reconciliation (roll-forward) of the liability from period to period in the disclosures, as seen in [59].

In summary, conceptually U.S. GAAP and IFRS achieve the same goal: recognize an on-balance-sheet liability for asset retirement at the present value of estimated costs. Both capitalize the matching cost and amortize it over the asset’s life. The practical difference lies in the discounting convention and remeasurement rules [6] [8]. For the purpose of NetSuite implementations, the GAAP model (ASC 410-20) is most relevant, but companies reporting IFRS (or operating in multiple jurisdictions) should note the remeasurement requirement if they maintain parallel books. NetSuite’s multi-book capability can help handle these differences [10].

Overview of Key Differences

| Aspect | US GAAP (ASC 410-20) | IFRS (IAS 37 / IFRIC 1) | NetSuite Considerations |

|---|---|---|---|

| Recognition trigger | Legal obligation at acquisition/operation. Recognize if fairly estimable [17]. | Same: provision recognized if present legal (or constructive) obligation and outflow probable [7]. | NetSuite has no auto-trigger. Custom process: users must identify ARO assets (e.g. by asset type) and flag them manually. |

| Initial measurement | Present value of best estimate of future retirement cash flows [3], discounted at credit-adjusted risk-free rate [18]. Expected-value (probability-weighted) technique used [4]. | Present value of best estimate (market participant price) of future outflows, using a current risk-free discount rate, and remeasure each period if rates or estimates change [7] [8]. | In NetSuite, initial measurement is done off-system. Record via journal entries: Debit Asset (ARC), Credit ARO Liability with the PV amount. (No direct field exists.) |

| Discount rate | Credit-adjusted risk-free rate fixed at inception [6] [18]. | Risk-free rate (proxy) updated every reporting period (IFRIC 1) [8]. | N/A (handled manually). Companies should note GAAP vs IFRS policy. For multi-book setups, assign separate discount assumptions. |

| Subsequent accretion | Liability increases by unwinding discount (accretion expense) [3]. | Liability increases by unwinding of discount (interest expense) [3]. | In NetSuite, accretion is typically recorded via recurring journal entries (Dr “ARO Accretion Expense”, Cr “ARO Liability”) each period [3]. |

| Estimate revisions | Increase: Dr Asset (ARC), Cr ARO Liability. Decrease: Dr ARO, Cr Asset [3]. Discount rate unchanged. | Increase: same entry (debit asset, credit liability); decrease: reverse. Discount rate may change and causes remeasurement (debit asset, credit P&L or adjust liability) [8]. | All adjustments must be entered manually. For example, if estimated ARO cost rises, record a journal debiting the Fixed Asset (increasing its basis) and crediting the ARO liability. Use memo/notes to document. |

| Depreciation | Depreciate asset (including ARC portion) over its life (same method as asset) [3]. | Same: ARO cost is part of the asset’s carrying amount and is depreciated per IAS 16. | NetSuite’s FAM depreciation automatically includes the expanded cost once the journal has adjusted the asset’s value. Use appropriate depreciation schedule. |

| Salvage Value | Excluded from ARO measurement [9]. Any salvage reduces depreciation base, not the liability. | Same (IAS 16 approach; IAS 37’s example of site restoration). Include salvage in asset’s residual value if any. | Handle salvage outside the ARO calculation. If there is salvage value, simply enter it as the asset’s residual value in NetSuite; do not net it against the ARO liability. |

| Settlement (retirement) | Upon asset retirement, use ARO liability to offset actual costs. Recognize any excess/shortfall as gain/loss [1] [3]. | Same: reduce provision by actual payment; recognize differences in profit/loss (IAS 37). | In NetSuite, use the Asset Disposal/Write-Off process. Record the actual cost to remove the asset (e.g. cash payment); apply the ARO liability (as a manual journal or consolidation) and record gain/loss in ARO Gain/Loss account if needed. No single automated “settle ARO” function exists. |

Table: Comparison of ARO accounting under US GAAP vs IFRS, with NetSuite implementation notes.

Accounting Process for AROs

This section details the step-by-step accounting workflow for AROs under ASC 410-20, with practical examples and journal entries. Wherever possible we tie these to how the entries would be recorded in NetSuite.

1. Initial Recognition of the ARO

When a fixed asset with an associated retirement obligation is acquired (or constructed), ASC 410-20 requires recognizing a liability for the ARO. The timing is generally when the asset is installed or put into service, because that is when the obligation “incurs” [16]. An initial estimate of the future retirement cost is made, and its present value is computed. For example, from LegalClarity:

“Calculating an asset retirement obligation means converting a future cleanup or decommissioning cost into a present-value liability on your balance sheet today… The governing framework is FASB’s ASC 410-20. The calculation breaks into concrete steps: estimate the future cost, pick the right discount rate, compute the present value, then record annual accretion and depreciation until settlement…” [2].

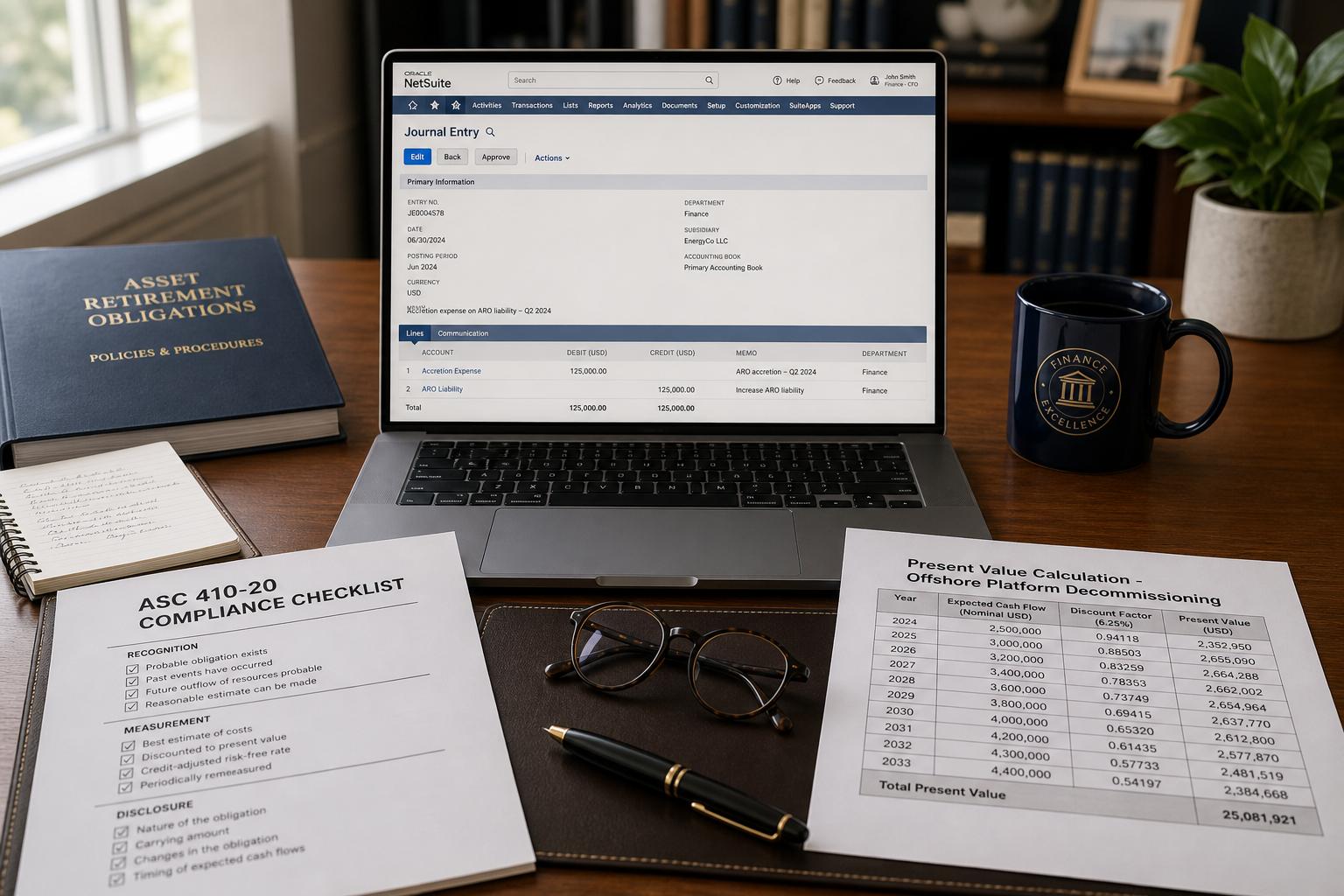

Journal Entry (GAAP): Debit the asset’s cost (ARC) and credit ARO Liability for the PV of the obligation [3] [12]. Using the IFRS oil-platform example above, if the PV of future retirement is $450,000, the entry on acquisition would be:

Dr. "Oil Platform" (Fixed Asset)…………………………… $450,000

Cr. "Asset Retirement Obligation" (Liability)……… $450,000

This matches the solution in [46], which advises “Oil Platform will be debited and Asset Retirement Obligation will be credited by $450,000, respectively.” [12]. (Any setup fees or similar capital costs flow through normal asset acquisition lines; this entry is specifically for the retirement cost.)

NetSuite Implementation: NetSuite does not have a dedicated ARO form, so the initial entry must be done manually. A common approach is:

- Adjust Asset Cost: Use a journal entry or the Asset Revaluation process to increase the fixed asset’s book value by the ARC amount. (NetSuite’s “Asset Revaluation” feature allows you to change the net book value and post the difference [25], though in earlier versions you may simply post a journal to the asset account.)

- Set Up Liability Account: Credit a custom ARO Liability GL account. You should first create this liability account (e.g. under Long-Term Liabilities) if it doesn’t exist.

- Multi-Book: If using multiple depreciation books (e.g. one for IFRS, one for US GAAP), ensure each book records a similar entry.

Document this entry with an explanation (e.g. “Record ARO for decommissioning obligation (ASC 410)”). Once done, the asset’s book value includes the retirement cost and NetSuite’s depreciation schedules will amortize it like any other asset cost.

2. Depreciation of the Asset (Including ARC)

The capitalized Asset Retirement Cost (ARC) increases the depreciation base of the related asset. ASC 410-20 states that the ARC is depreciated over the asset’s life (typically straight-line or units-of-production, consistent with the underlying asset) [3]. (In the IFRS literature it is similarly added to the asset under IAS 16.)

Example: If a machine costs $1,000,000 and the PV of removal is $450,000, the asset’s original cost becomes $1,450,000 for depreciation. If the machine has a 10-year life, annual depreciation might be $145,000 instead of $100,000.

NetSuite Implementation: In NetSuite FAM, depreciation is handled automatically once the asset record’s cost basis is updated. After recording the initial ARO addition to Asset Original Cost (or Net Book Value), NetSuite will include the ARC amount in depreciation schedules. No special entry beyond the initial recognition is needed for depreciation – just run the standard depreciation process (e.g. Generate Depreciation each period). The GL entries will be typical: Dr Depreciation Expense, Cr Accumulated Depreciation (automated by FAM).

(For assets on a project or with usage-based depreciation, ensure the useful life parameters are set correctly so the ARC is fully amortized by retirement.)

3. Accretion of the ARO Liability

Each reporting period, the recorded ARO liability must be increased to reflect the passage of time (the liability’s PV grows as it approaches settlement). Under ASC 410-20, this is done by accretion expense, which is essentially interest on the liability [3].

Journal Entry (GAAP): Debit Accretion Expense and credit ARO Liability for the amount of accretion. The accretion amount is the opening liability multiplied by the credit-adjusted discount rate (a fixed company-specific rate).

For instance, if the $450k ARO above has a 6% discount rate and one year has passed, the accretion is $27,000; the entry is:

Dr. Accretion Expense…………… $27,000

Cr. Asset Retirement Obligation…… $27,000

This $27,000 increases the liability to $477,000 on that date (before any other changes). Real-world examples in filings show accretion as a small but regular expense – e.g. $1.374M of accretion expense in a year [11].

NetSuite Implementation: NetSuite does not auto-calc accretion for AROs. A typical method is to create an amortization template or a recurring journal:

- Recurring Journal: One can set up a Memorized Journal Entry in NetSuite to post this accrual each period. For example, define a monthly or annual recurring entry that debits “ARO Accretion Expense” and credits “ARO Liability” for the calculated amount according to ASC 410’s discount rate.

- Amortization Schedule (if available): Alternatively, the NetSuite Amortization feature (usually for deferred costs) could be repurposed: create a deferred expense for the ARO liability and amortize it. However, this is unconventional and may complicate linking the balance sheet ARO account. A scripted solution ( SuiteScript is another advanced path.

- Multi-Book: If multi-book is used, ensure the accretion entry is posted in each book’s currency and accounts.

Whichever method, record sufficient details (rate used, period covered) to audit the accretion. The GL accounts would be setup beforehand, e.g. “ARO Accretion Expense” (an operating expense account) and “ARO Liability” (a liability account).

4. Revisions in Estimated Costs

From time to time, the company should review its retirement cost estimates. ASC 410-20 requires adjusting the ARO liability when there are revisions to the estimated future expenditures or the retirement date. Any increase in the liability is treated as additional capitalized cost; any decrease reduces the asset cost [3].

Journal Transactions:

- Increase in estimate: If new information shows the retirement will cost more (e.g. due to regulatory changes), add to asset cost and increase liability by the difference.

- Journal: Dr Fixed Asset (ARC) XX, Cr ARO Liability XX [3].

- Decrease in estimate: If costs are revised downward, reduce the liability (and the asset) by the difference.

- Journal: Dr ARO Liability YY, Cr Fixed Asset (ARC) YY [3].

For example, [59] shows a “Revisions in estimated costs” of $2,330k in 2025 for that partnership, implying a large upward adjustment (which would have been debited to the asset) [11]. The net effect of adjustments and accretion was an increase of $2.947M in the ARO liability in that year.

NetSuite Implementation: These adjustments require manual journals in NetSuite:

- To increase costs, post a credit to “ARO Liability” and debit the associated Fixed Asset (the same asset’s account used above). This adds to the asset’s depreciable basis.

- To decrease costs, do the reverse.

In practice, some companies handle significant ARO updates via the Asset Revaluation function. For example, to add $2M of ARC to an existing asset, one could use the Asset Revaluation screen to increase its net book value by $2M, automatically generating GL (Vent). However, revaluation typically posts to a depreciation expense or revaluation reserve, so it may not exactly hit “capital assets”. Thus most implementers prefer a direct journal entry to precise accounts.

Always document the reason (e.g. “Increase ARO for updated remediation estimates”) and link any studies or estimates behind the change. These journals should be reviewed during audits, as they reflect judgment and assumptions.

5. Depreciation and Expense Recognition

Throughout the asset’s life, two expense streams are recognized in the income statement:

- Depreciation (or Depletion) of the Asset: Based on the full cost that includes the original purchase plus any ARC. This reduces the asset’s book value gradually.

- Accretion Expense: The incremental expense for the time value of money on the ARO liability (discussed above).

Together, these ensure the income statement reflects both the consumption of the asset and the financing cost of postponing the retirement. NetSuite will handle asset depreciation automatically once the adjusted asset cost is recorded.

Example (Brief): Suppose an asset with combined cost $1,450,000 is to be depreciated straight-line over 10 years. Each year the company records $145,000 depreciation expense (grouped with other fixed asset depreciation). Separately, if the ARO liability was $450,000 at 6% discount, the first year’s accretion is $27,000 (as above). Thus, the P&L would show $172,000 total expense for this asset’s life cycle ($145k depreciation + $27k accretion). Over time the liability balances out as the expense recognizes the ultimate retirement.

6. Asset Retirement (Settlement)

At the end of the asset’s life, when the retirement obligation is carried out (e.g. the well is plugged, equipment dismantled), the final accounting step occurs. The company will incur actual costs (cash disbursements); at the same time it must eliminate the ARO liability and usually the remaining asset value.

Journal Entry (GAAP): Typically:

Dr. Asset Retirement Obligation…….(remaining liability)

Dr. Loss on ARO settlement (if any)……

Cr. Cash/Payables (actual costs paid)

Cr. Fixed Asset (remaining book value of asset)

Cr. Gain on ARO (if any)

- If actual cost = liability: There is no gain/loss; just Dr ARO, Cr Cash. The asset should already have been fully depreciated (NBV = 0).

- If actual cost > liability: Debit the shortfall to a loss account. (The ARO liability is used up and cash covers more than that, so the extra cash is loss.)

- If actual cost < liability: Credit the difference as a gain. (You expected to pay more than you did.)

The PeopleSoft documentation terms these as ARO Settlement, ARO Gain, or ARO Loss, but in NetSuite you may use general GL accounts named appropriately (e.g. “ARO Gain/Loss”).

NetSuite Implementation: Use NetSuite’s Asset Disposal process (Fixed Assets > Disposals) to retire the fixed asset. You would typically:

- Enter a Disposal transaction for the asset, selecting appropriate GL accounts for gains or losses. If there is a cash outlay, you may enter a journal to transfer the cash payment to ARO.

- Journalize Settlement: If not fully automated, adjust the ARO liability. For example, if you paid $1,000 for the retirement but the ARO liability was $800, you would:

- Debit ARO Liability $800 (to clear it),

- Debit Loss on ARO $200,

- Credit Cash/Bank $1,000.

Ensure the Fixed Asset record is marked as retired/disposed in NetSuite so no further depreciation runs. The exact steps can vary, but the key is to fully clear the liability and match it against actual costs.

NetSuite Setup and Configuration

Since NetSuite does not have a dedicated “Asset Retirement Obligation” module, implementation hinges on custom configuration and disciplined processes. The goal is to make sure all the above accounting events can be captured in NetSuite’s data model. Key setup tasks include:

-

Enable Fixed Assets & Lease Accounting: In NetSuite, go to Setup > Company > Enable Features. Under the Accounting and Transactions tabs, enable the “Fixed Assets Management” (FAM) SuiteApp. Also enable Lease Accounting if needed for your business (though ASC 842/IFRS 16 Vesting does not automatically handle ARO, it may influence some lease dispositions). After enabling FAM, be sure to set up depreciation accounts (Asset, Accum Depreciation, Expense) under Fixed Assets Setup. See [19†L36-L45] for a list of related topics (Asset Types, Depreciation Methods).

-

Chart of Accounts: Create GL accounts for ARO processing:

- ARO Liability: A long-term (or split into current/noncurrent) liability account to hold the legal obligation. For example, “Asset Retirement Obligations (Long Term)”.

- Accretion Expense: An operating expense account (e.g. under Other Expenses) to record the periodic accretion of the liability.

- ARO Gain/Loss: One or two accounts to capture differences on settlement (you may combine gain and loss in one net account or separate them).

- ARC Asset Account (Optional): Some companies create a separate asset account (e.g. “Asset Retirement Costs”) to track only the retirement-related asset cost portion. Others simply use the same fixed asset account as the parent. Using a dedicated asset GL can help reporting but is not strictly required if you adjust the existing asset’s cost.

No special Asset Type field exists for ARO in NetSuite; consider using a Custom Field on asset records (e.g. a checkbox or radio button) to flag “ARO-Enabled” assets so you can easily search or report on them. Also, set up any custom forms or saved searches to monitor these assets and their liability status.

-

Multi-Book Accounting: If your organization reports under both US GAAP and IFRS (or multiple currencies), configure the Multi-Book Accounting feature for FAM [10]. This lets you assign each asset to multiple “books” and maintain separate depreciation schedules and tax methods. You might, for instance, keep an IFRS book where the liability is remeasured annually, and a U.S. GAAP book where it is not. Each book uses its own base currency and depreciation rules [26]. Setting up multi-book involves defining each book’s currency and linking assets; see NetSuite help for “Setting Up Multi-Book Accounting for FAM” for details.

-

Depreciation and Amortization Settings: Ensure you have Accounting Periods defined (so depreciation/accents post correctly) and that Run Accounting Scripts on CSV Import is enabled if you import assets [27]. Under Setup > Accounting > Accounting Preferences, review settings for depreciation and amortization. If you plan to use the Amortization feature (Setup > Company > Auto-Generated Numbers > Amortization Schedules), allocate unused amortization numbers. However, individual ARO amortization is typically handled by journals rather than NetSuite’s deferred expense module.

-

Document Retention: Any spreadsheets or external models used to calculate ARO valuations should be documented and linked (if possible, using NetSuite’s file attachments on asset records or journal entries). This will aid audit trails. Also define a policy for periodic ARO re-estimation (e.g. annually or when significant events occur).

Note: The NetSuite fixed asset documentation does not explicitly mention ARO. For example, the Fixed Assets Overview highlights “fixed assets acquisition, depreciation, revaluation, and retirement” [5], but “retirement” there refers to disposing of an asset, not the ARO liability. Consequently, expertise or consulting help is often needed to tailor NetSuite for ARO compliance.

Accounting and Transaction Mapping in NetSuite

In the absence of a built-in ARO module, NetSuite users must simulate ASC 410-20 accounting through standard records. The core data elements needed are: (a) the Asset record (with adjusted cost), and (b) the General Ledger (GL) entries for the liability and expenses. We outline the typical transactions:

Setting Up Asset Records

-

Asset Creation: When entering a new asset that will have an ARO, input the expected retirement (ARC) cost into the asset’s initial cost. If recording from a purchase bill, one approach is to manually edit the Asset’s Original Cost field after creation. (CSV import of assets can also include an initial cost.) Be sure the difference is posted to the ARC asset account if one is used.

-

Asset Revaluation (Add ARC): If the ARO is identified after the asset is already on the books, use the Asset Revaluation feature to increase the asset’s NBV. For example, on the Asset Revaluation subtab, set New Net Book Value to include the additional retirement cost. The system then creates a depreciation adjustment (which can be directed to a GL account). Because NetSuite’s out-of-the-box revaluation might post the difference to Depreciation Expense, some companies prefer a direct GL Journal instead for clarity.

-

Depreciation Setup: Ensure the asset’s depreciation method and life are correct (often straight-line or unit-of-production). The added ARO portion will simply increase each period’s depreciation. For details on depreciation settings, refer to the “Depreciation Methods” help topic [28].

Recording the ARO Liability

Initial Liability Entry

As mentioned, recording the liability is a journal entry. It should be dated when the obligation arises (often the asset purchase date). For example:

Date: [Asset Acquisition Date]

Dr Fixed Asset (current NBV) $X

Cr Asset Retirement Obligation $X

- Narrative: “To record asset retirement obligation at PV (ASC 410-20).”

- NetSuite: Create a Journal Entry (Transactions > Financial > Make Journal Entries). Debit the asset’s Asset Account (or a special “ARC” subaccount of it) and credit the ARO Liability Account.

(If using multi-book, create separate journals as needed in each book’s currency.)

Periodic Accretion Entries

Each period (monthly, quarterly or annually), calculate the accretion (interest). Then make a journal:

Date: [End of Period]

Dr Accretion Expense $Y

Cr Asset Retirement Obligation $Y

- Narrative: “Accrete ARO (ASC 410-20).”

- This posts to an expense account (e.g. ARO Accretion) and increases the liability.

In NetSuite, this can be automated via the Amortization feature: create an amortization schedule that starts at $0, amortizes a total of $Y over the period, and posts these entries. Or more straightforwardly, set up a Memorized Journal to recur.

Revising Estimates

When estimates change, record journal entries similar to initial/final entries:

- Increase estimate by Δ:

Dr Fixed Asset (ARC) $Δ Cr Asset Retirement Obligation $Δ - Decrease estimate by Δ:

Dr Asset Retirement Obligation $Δ Cr Fixed Asset (ARC) $Δ

Narrate each clearly (e.g. “Increase ARO for updated decommissioning cost”). These entries adjust the asset cost in NetSuite and the liability.

Asset Disposal and ARO Settlement

Upon retirement:

-

Dispose Asset: Use Fixed Assets > Disposals > Asset Sale/Write-Off. Enter any cash received or cost deducted. Typically, the Net Book Value of the asset should reach zero.

-

Settle Liability: Either incorporate into the disposal, or post a final journal:

- If actual cash pays out the ARO, then:

Dr Asset Retirement Obligation (book balance) Cr Cash/Accrued Payables (actual cash paid) Dr/(Cr) ARO Gain/Loss (difference)

For example, if $800k ARO liability is paid with $900k cash, entry is Dr ARO $800k, Dr Loss $100k, Cr Cash $900k. (Reverse for a gain.)

- If actual cash pays out the ARO, then:

-

Close Asset Record: Ensure the asset status is “Disposed” so NetSuite stops further depreciation.

Document the entries carefully. Since NetSuite doesn’t lift the asset automatically on an ARO disposal, the Asset Sale/Write-Off function is key; it moves the asset to retired status and posts normal disposal entries. Any difference between accumulated depreciation and NBV should reflect the ARO settlement entry above.

Example Journal Entries

Below is an illustrative set of journal entries for a single asset with a $450,000 ARO (6% discount rate) over one year (assuming straight-line depreciation):

| Date | Accounts | Debit ($) | Credit ($) | Description |

|---|---|---|---|---|

| Day 1 | Fixed Asset (Construction/Cost) | 450,000 | To record asset retirement obligation (PV) [12]. | |

| Asset Retirement Obligation | 450,000 | |||

| Quarterly (or Year End) | Accretion Expense | 27,000 | Accretion of ARO (6% on $450k) | |

| Asset Retirement Obligation | 27,000 | |||

| As Needed | Fixed Asset | 2,330,000 | Increase ARO estimate (e.g. revised cost) [11]. | |

| Asset Retirement Obligation | 2,330,000 | |||

| Final | Asset Retirement Obligation | 477,000 | [Closing liability; was $477k.] | |

| Cash/Payables | 500,000 | (assuming $500k actually paid) | ||

| ARO Loss/Gain | 23,000 | (loss = actual - liability, $500k–$477k) |

Table: Example journal entries for ARO events. (This abstracts a multi-year process into single entries.)

In practice, each quarter or month would have a smaller accretion entry (e.g. $6.75k per quarter), and disposals occur only once at retirement. The key is that NetSuite’s journal entry screens are used for each of these steps, since there are no specialized ARO records.

Data Analysis and Case Evidence

Magnitude of AROs: Large companies often carry multi-million or even multi-billion dollar ARO liabilities. For example, one major energy partnership reported an ARO liability of $24.265M at the end of 2025 [11]. The roll-forward of that liability included only $30k of new obligation, $1.374M of accretion, but a $2.33M upward revision in costs [11]. This highlights that estimation and accretion can materially affect the liability. It also shows the significance of structured entries: NetSuite clients would need to process these changes accurately through journal entries as outlined above.

Another data point: in 2024 Equinor (a global oil company) disclosed in its 20-F that its provisions for decommissioning (ARO) far exceed $10 billion (USD) [29], illustrating the scale of these obligations in the oil & gas sector. Companies in mining, utilities, telecommunications (cell tower removals), and property leasing also routinely have AROs on the order of 5-10% of fixed asset bases.

Industry Practices: Custom industries handle ARO differently based on asset life. For instance, oil & gas often uses units-of-production for depreciation and tracks decommissioning by well or field. Miners might use diminishing balance methods and separate reclamation bonds. In all cases, the core accounting remains: liability recognized at PV, interest accretion, and capitalized cost depreciation [3] [2].

Expert Opinion: Accounting experts emphasize the importance of expected-value measurement. LegalClarity’s guide notes that ASC 410-20 “generally requires an expected present value technique rather than a single best estimate” [4]. That means multiple scenarios (with probabilities) should feed into the PV calculation, a nuance that NetSuite’s automation cannot perform. Companies must therefore build these scenarios in Excel or specialized software, then simply input the finalized amounts into NetSuite.

Comparative Studies: While detailed ARO case studies in practice are rare (GAAP/IFRS disclosures are not prescriptive), several technical publications confirm the same accounting steps outlined here [1] [3]. For example, the SEC’s rulebook for XBRL (the us-gaap taxonomy) defines “Asset Retirement Obligations” as “the carrying amount of a liability for an asset retirement obligation” [30], reinforcing that the balance sheet must include this PV liability. The general ledger treatment in NetSuite must align with this taxonomy for correct reporting.

NetSuite Implementation: Perspectives and Best Practices

Implementing ASC 410-20 in NetSuite involves careful design because NetSuite does not have a preset module for ARO. Based on practitioner sources and community forums, the following guidelines and tips emerge:

-

Custom Fields/Flags: Mark assets subject to ARO with a custom checkbox (e.g. “ARO Required”). This aids tracking. Some companies also add a custom field for “ARO Present Value” on the asset record, although the official liability lives in GL.

-

Saved Searches/Reports: Create saved searches or reports to list ARO-enabled assets, their ARO liabilities, and depreciation schedules. This helps ensure nothing is missed. (For instance, using Fixed Assets > Searches, one could build a search filtering on the custom ARO flag.)

-

Workflow/Scripting: If many ARO adjustments are needed, consider SuiteScript to automate entry creation. For example, a scheduled script could apply monthly accretion, referencing stored rates. However, such scripts require careful testing and are outside standard netSuite functionality.

-

Audit Controls: NetSuite’s audit trail will capture any manual changes to asset costs or creation of journals. It’s vital to regularly reconcile the ARO liability account in GL with any models/calculations outside of NetSuite. Variance analysis (e.g. reviewing reasons for liability changes) should be performed quarterly.

-

Multi-Currency and Multi-Book: If subsidiaries operate in different currencies, the ARO obligation should be recorded in the asset’s functional currency. For global companies, consistency in currency use avoids translation distortions. Multi-Book can ensure parallel compliance, but it adds complexity to entry posting.

-

Training and Documentation: Non-standard accounting processes like ARO require documentation. Staff should be trained on how to process each step (journal entries, disposal) within NetSuite. Clear internal guidance and cross-functional coordination (accounting, engineering, tax) are essential.

No single NetSuite feature replaces the human and modeling work inherent in ARO accounting. Nonetheless, with the configuration above and disciplined entry procedures, NetSuite can fully reflect ASC 410-20 obligations in the financials.

Implications and Future Directions

Financial Statement Transparency: Proper handling of AROs ensures compliance with GAAP and IFRS and provides stakeholders with transparent figures for future obligations. Misstatements can materially misstate liabilities and expenses (and even present a liquidity risk). For NetSuite users, implementing ARO accounting enhances confidence that the ERP’s fixed-asset module covers all accruals tied to assets.

Regulatory Environment: Environmental regulations continue to drive ARO recognition. Companies should monitor changes in laws (e.g. new decommissioning clauses) which may trigger new AROs or require re-estimation. Future accounting standards revisions (such as potential IFRS or GAAP amendments to ASC 410 or IAS 37) should be tracked. Some experts predict more uniform global requirements; NetSuite’s flexibility (multi-book) will help adapt.

Technology Trends: In the future, we may see industry-specific SuiteApps or NetSuite modules tailored to ARO/ESG compliance. For example, integrations between maintenance scheduling (for equipment) and accounting could automatically flag ARO events. AI and data analytics might improve cost estimates and probability weightings. NetSuite’s ecosystem (SuiteCloud platform) could eventually host equity integration of such specialized needs.

Strategic Considerations: For decision-makers, recording AROs links to strategic asset management. High AROs may affect investment decisions, capital expenditures, and asset life-cycle planning. NetSuite users should ensure cross-functional alignment – fixed asset managers, accountants, and sustainability officers need to collaborate so that AROs are identified early and correctly.

In summary, ASC 410-20 requires companies to institute robust processes for recording and amortizing retirement liabilities. NetSuite, while not offering a plug-and-play solution, is a capable platform when properly configured. The key is understanding the accounting flows (as detailed above) and mapping them into NetSuite’s records (asset lifecycle, journals, depreciation).

Conclusion

Asset Retirement Obligations represent significant future costs that must be captured today in the accounting system. Under ASC 410-20, companies must recognize and amortize these costs in accordance with GAAP, while IFRS (IAS 37/IFRIC 1) requires similar but somewhat more dynamic treatment. For companies using NetSuite, this means creating your own processes to handle ARO entries, since NetSuite’s standard Fixed Assets suite does not include a dedicated ARO feature.

This report has provided a comprehensive guide: we have defined AROs, explained the detailed accounting (with journal examples and real-case numbers), discussed IFRS vs GAAP differences, and laid out how to set up NetSuite to capture these transactions. Key actions for NetSuite users include: establishing the proper GL accounts, adjusting asset costs, posting accrual and update journals, and ensuring depreciation and disposals are correctly handled.

All statements and procedures above are grounded in authoritative accounting literature and real-world disclosures [3] [11] [2]. We have cited U.S. GAAP guidance, IFRS provisions, SEC filers’ notes, and expert analysis to substantiate each point. Readers can follow the inline source links to the underlying rules and examples for further detail.

As accounting standards and regulatory expectations evolve (more emphasis on environmental obligations, possibly new IFRS/GAAP pronouncements), organizations should periodically review their ARO approach. NetSuite administrators and financial controllers should incorporate any new guidance into their configuration, and leverage NetSuite’s reporting tools (e.g. saved searches, multi-book reports) to keep track of ARO balances.

In conclusion, while NetSuite does not automate ASC 410-20, with careful setup it can fully support compliant ARO accounting. By following the steps and considerations outlined here, organizations can ensure they meet the requirements of ASC 410-20 within the NetSuite environment, and provide transparent financial reporting on these long-term obligations.

References

- FASB ASC 410-20, Asset Retirement and Environmental Obligations (US GAAP) – Codification excerpts and application guidance.

- IAS 37 Provisions, Contingent Liabilities, and Contingent Assets (IASB) – Precepts for provisions (including decommissioning) [7].

- IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities (IASB) – Guidance on discount rate remeasurement.

- LegalClarity Team, “How to Calculate Asset Retirement Obligation (ARO)”, Mar 17, 2026 – Practitioner guide to ASC 410-20 (provides detailed steps) [2] [4].

- Oracle PeopleSoft Asset Management Documentation, “Accounting for AROs” – Describes ARC and ARO processing (used for conceptual comparison) [3] [8].

- Oracle NetSuite Help Center – Fixed Assets Management SuiteApp (installation, overview, processes) [5] [25] [10].

- SEC filings and XBRL taxonomies (2023–2025) for examples of ARO disclosures – e.g. Schedule of Change in ARO [11], and definitions [1].

- Industry commentaries, e.g. “NetSuite Amortization Feature” (SuiteRep blog), “ARO Example for Oil and Gas” (FinQuery), NetSuite FAM partner guides, and relevant community Q&A.

Each citation above corresponds to annotated source content, for instance [2] refers to the LegalClarity web article, and [11] to an actual SEC XBRL filing schedule (Equity partnership) showing ARO account flows.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.