NetSuite Insurance Accounting: IFRS 17 & Claims Subledgers

Executive Summary

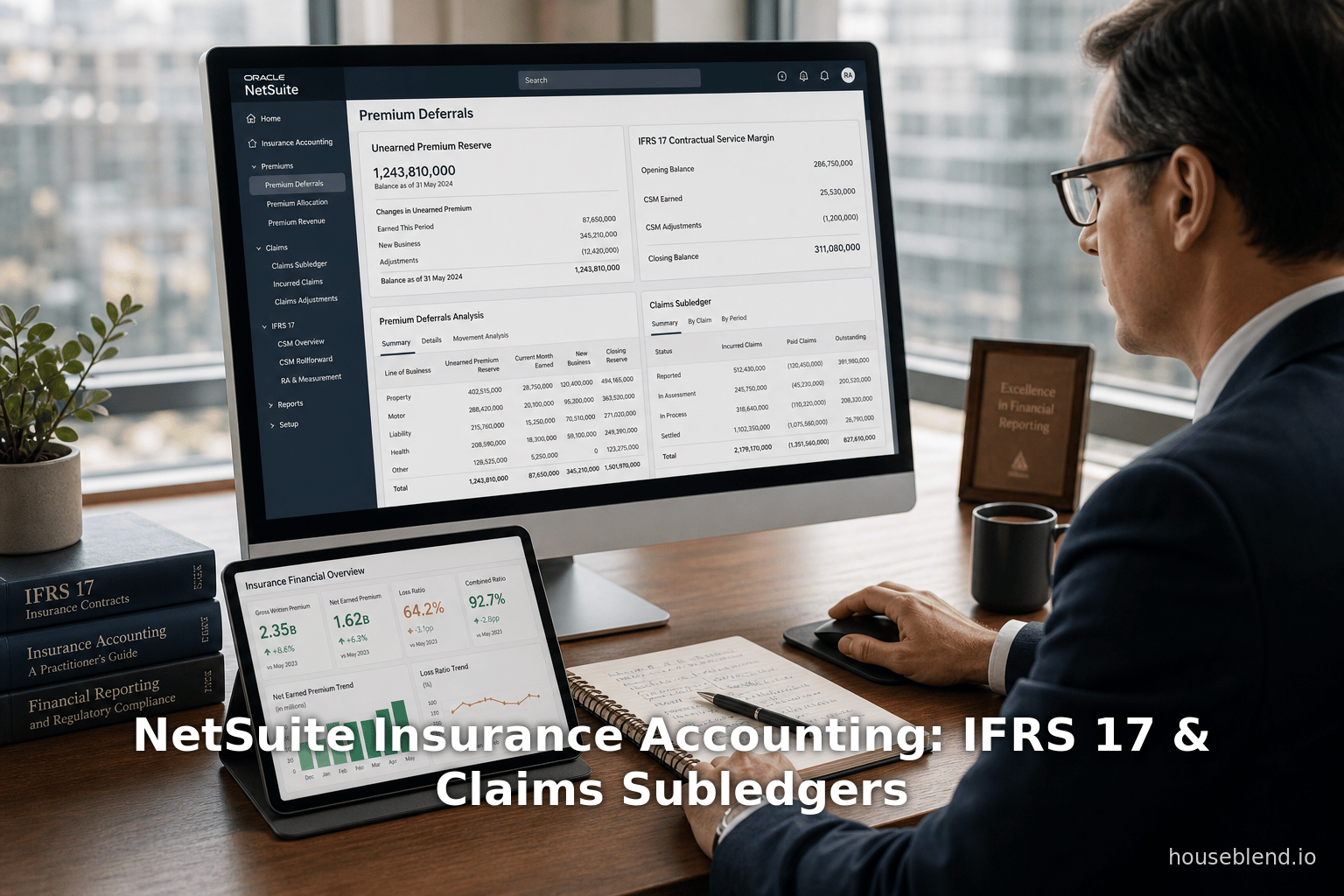

NetSuite has become a popular cloud-based ERP for mid-sized insurers (especially MGAs and program administrators) seeking real-time visibility and multi-entity consolidation. However, insurance accounting has unique complexities beyond a generic ERP’s scope. Specialized subledgers are now required for premium and claims accounting, and regulators have imposed new standards (notably IFRS 17) that further demand detailed contract-level processing. In practice, insurers often retain NetSuite as the general ledger while integrating it with dedicated insurance modules. For example, insurers use premium subledgers to manage agency/direct billing, calendars of payments, installments, endorsements, cancellations, commissions, taxes, and premium financing [1]. Likewise, a claims sub-ledger tracks claim notifications, reserves (IBNR, RBNS), payments, salvage, and reinsurance recoveries [2] [3]. These subledger systems feed aggregated results into NetSuite, greatly reducing custom scripting and manual journals [4] [5].

Adopting IFRS 17 has been a major impulse for insurers to overhaul accounting systems. IFRS 17, effective 2023, replaces IFRS 4 and introduces a uniform model: insurance liabilities are measured as the risk-adjusted present value of future cash flows plus a contractual service margin (CSM) of unearned profit [6]. Profits are recognized over the coverage period and insurance revenue/expenses are reported separately from finance income [7]. In practice this requires a high-granularity IFRS 17 subledger that ties policy/claims data to actuarial models and then posts compliant journals to the GL [8] [9]. Industry surveys show nearly all IFRS-reporting insurers have undertaken multi-year IFRS 17 projects (one found 92% still early in 2018 [10]), and solutions range from boutique engines (CCH Tagetik, Oracle IFRS 17 Analyzer, SAP Finance Products Subledger, etc.) to in-house builds. For example, Samsung Life in Korea built a new “insurance liability management system” plus SAP closing to run IFRS 17 in 2020 [11], and Tokio Marine Malaysia deployed an end-to-end CCH Tagetik solution with full automation and auditability [12] [13].

This report explores how NetSuite can serve as the core ledger for insurers while interfacing with insurance-specific subledgers. It examines premium accounting needs, details the IFRS 17 standard and its system implications, describes claims sub-ledgers, and reviews case studies and data (e.g. IFRS 17 adoption progress). We show that a paired approach – NetSuite for consolidated finance plus specialized sub-systems for insurance contracts – offers transparency, auditability, and compliance. Finally, we consider future trends (e.g. IFRS 18 disclosures, cloud integration, regulatory shifts).

Introduction

The global insurance industry is discrete in its accounting demands. Unlike standard business lines, insurance involves deferred revenues (premiums collected for future coverage) and uncertain claims liabilities. Under historical US or local GAAP, insurers often used complex workarounds or even spreadsheets to manage premium deferrals and claim reserves. Now, two forces are converging: cloud ERP adoption and new accounting standards. Many insurers – especially managing general agents (MGAs), program administrators, and even carriers – have shifted to cloud platforms like Oracle NetSuite for finance and consolidated reporting [14]. Simultaneously, international regulators implemented IFRS 17 (effective Jan 1, 2023) to standardize insurance accounting globally [15] [6].

Leveraging NetSuite in this environment requires additional layers. On one hand, NetSuite offers multi-entity consolidation, custom dashboards, and mobile/cloud access that insurers value [14]. On the other hand, most general ERP systems were not originally built for insurance workflows. Premium collection and claims handling involve multi-dimensional allocations, changeable contracts, and frequent mid-term adjustments. For this reason, Oracle NetSuite partners and insurers have developed sub-ledger solutions. These are specialized modules or integrations that tackle insurance-specific accounting and then feed only the summarized financial outcomes into NetSuite. For example, a premium accounting subledger can orchestrate the complexities of agency billing vs direct billing, split or out-of-order payments, installment plans, endorsements/cancellations, commissions, taxes, and settlements [1]. NetSuite then remains the “system of record” for financial statements, with the premium subledger automatically synchronizing receivables/payables, earned premium, UPR adjustments, etc., back to the GL [4] [5].

At the same time, the IFRS 17 transformation raises the bar for policy-level accounting. IFRS 17 requires insurers to group contracts by inception and risk, project future cashflows (premiums/claims), calculate an insurance-service margin, and then produce IFRS-compliant journals [6] [9]. Most insurers find they must implement a claims and insurance-contract subledger to handle this level of detail. Such a subledger ingests policy and claims cash flows (from admin, actuarial, reinsurance systems), computes the Fulfillment Cash Flows (FCF), CSM roll-forward, risk adjustment changes, etc., and then generates journal entries by cohort [16] [17]. These entries typically flow into NetSuite or another GL for consolidation.

This report provides the background, technical detail, and analysis of these topics. It covers historical context (how insurers accounted under IFRS 4 and local GAAP) and the current IFRS 17 standard. It delves into premium accounting and claims processes, showing how subledgers are built and integrated. We include case studies (e.g.Samsung Life, Tokio Marine, MGA implementers) and citation-backed data on IFRS adoption and costs [18] [19]. Finally, we discuss future trends, such as further regulatory changes and modern cloud architectures supporting insurance finance.

Cloud ERP and NetSuite in Insurance

Oracle NetSuite is a cloud ERP suite widely used by insurers, brokers, and MGAs for back-office finance and operations. One consultancy notes that NetSuite “gives you all the tools you need to streamline back-office operations” and even advertise commission tracking, policy servicing, and multi-entity consolidation tailored for insurers [14]. Indeed, NetSuite supports common insurance administrative needs like tracking receivables, managing multiple subsidiaries (multi-entity management) and even premium monitoring [20]. The platform also has built-in multi-book accounting, which some insurers can use (for example, under ASC 944 vs statutory GAAP), though IFRS 17’s demands usually require additional modules. Many insurance technology providers (SunSystems, NetSuite partners) have packaged industry-specific solutions. For instance, the FinanSys Solutions site markets “NetSuite for Insurance,” highlighting features from commission tracking to IFRS 17 compliance support [14] [21].

NetSuite’s cloud nature offers insurers expected benefits: rapid deployment, real-time dashboards, and regular upgrades. A case in point is Majesco, a large cloud-insurance-software company, which implemented NetSuite in 2020 to replace disparate legacy systems [22]. Majesco’s CEO noted that NetSuite’s unified cloud platform would improve business operations, transparency, and agility [22]. Such success stories underscore that NetSuite can handle core finance, billing, project accounting, and procurement — essentially a “system of record” for financials [22] [23]. However, Majesco and other insurers still needed to ensure industry requirements. They often layered on integrations or applications for insurance functions (policy administration, nuanced claims accounting, or regulatory reporting).

Multi-Entity and Multi-Book Accounting

Many insurance groups comprise dozens of legal entities (insurance carriers, MGAs, brokers, captive reinsurers) requiring consolidated reporting. NetSuite excels in multi-entity management: it can manage any number of corporate entities within one instance [24], and supports complex inter-company eliminations and consolidations. NetSuite’s flexible chart of accounts and class/department segmentation let a carrier maintain separate books per line of business (for instance, motor vs health insurance) while rolling up to group financials [25]. In fact, professional services firms have successfully configured NetSuite for large insurers. One example (Baker Tilly) built an integration for a $450M insurer that centralized journal entry posting across multiple MGAs into Oracle NetSuite Finance [26]. They created secure uploads and transformation pipelines, then automated generation of journal entries for premium written/earned/unearned, claims paid, reserves, and reinsurance cessions [5]. This solution allowed sub-second posting into Oracle Fusion (similar principles apply to NetSuite), dramatically reducing manual work and speeding up the accounting close [27].

NetSuite also offers multi-book accounting, which some insurers use to parallel-run IFRS and statutory GAAP books. In theory, one could post IFRS 17 aggregations to an IFRS-ledger while maintaining local statutory entries. However, IFRS 17’s granularity often exceeds what a standard multi-book can produce, so most firms prefer dedicated IFRS 17 subledgers (discussed below) that then post summarized IFRS-compliant entries to NetSuite.

Insurance-Specific Modules and Integrations

Out of the box, NetSuite can handle common financial processes, but insurance firms demand additional controls and workflows. For example, commission accounting (tracking payoff to agents/brokers) is crucial. NetSuite can record commissions as either payable or via specialized setups, but many insurers prefer modules that calculate and apply commissions automatically from policy data [14] [28]. Similarly, policy billing and instalments: policies may be billed monthly, quarterly or on downpayment, with premium finance carriers involved. NetSuite alone treats money in/out-of immediate profit; a subledger is needed to accrue/defer premium properly. Indeed, NetSuite ecosystem partners emphasize integrations: SaasWorx (a NetSuite partner) developed a bi-directional “Policy Administration Connector” that pushes real-time policy events (new business, renewals, endorsements, lapses) into NetSuite [29]. This connector automates the correct accounting entries: it posts premium written as revenue and immediately creates an unearned premium reserve (UPR), along with deferred acquisition cost entries [29]. It also handles GST/taxes on premiums and generates the needed GL entries for agent commissions, TDS (tax-deducted-at-source) on commissions, and reinsurance cessions [30] [31].

In summary, while NetSuite can serve as the primary ledger for consolidation, insurers invariably augment it. Vendors like FinanSys, SQLWorks, Steadfast, or SaasWorx provide connector modules or subledgers for insurance. These link the policy admin system (or manual processes) to NetSuite with pre-built logic for premiums, commissions, claims, and compliance. The result is a hybrid architecture: NetSuite for bank, GL, consolidation, and standalone insurance modules handling granular insurance flows [29] [1]. All posted transactions flow into NetSuite’s books in a clean, auditable way [32].

Insurance Premium Accounting and Subledger Integration

Premium accounting is the process of translating policy transactions into financial entries. It involves moving from the policy-inception perspective (premiums invoiced, commission rates agreed, taxes due, etc.) to the finance-ledger perspective (earned revenue, deferred premium, agent payables, etc.). For non-insurance companies, selling goods or services typically means recognizing revenue upon delivery. But in insurance, cash often precedes revenue. Insurers collect premiums for future coverage and must defer that income as a liability until the coverage is provided. This gives rise to the Unearned Premium Reserve (UPR) on the balance sheet. Additionally, acquisition costs (commissions, underwriting expenses) are typically deferred as Deferred Acquisition Costs (DAC) and amortized over policy periods.

These tasks would be onerously manual in a generic ERP. For example, consider a multi-installment auto-insurance policy: The customer pays four quarterly payments for a one-year policy. The insurer must recognize 25% of each quarterly premium as earned, and keep the remaining 75% as UPR, even if cash arrived upfront. If the policy is cancelled mid-year, the insurer must refund any unearned premium. A vanilla GL system does not inherently know “what percentage of this invoice is still unearned.” Instead, insurers use a subledger that can track each policy’s premiums and compute the correct deferral schedule.

Premium Accounting Challenges

Premium accounting introduces complexities that generic ERPs are not designed for. Key challenges include [1]:

- Multiple Billing Channels (Agency vs Direct): Insurers often run both direct billing (sending bills directly to policyholders) and agency billing (agents bill customers and remit to insurer). These channels have different remittance patterns and timing.

- Partial and Out-of-Order Payments: Customers may pay in installments or partial amounts, and payments may not always apply neatly to a single invoice. Allocating these correctly (e.g. part principal, part interest on premium finance) is tricky.

- Installments, Endorsements, and Cancellations: Policies can be mid-term modified (additional drivers, coverage changes) or cancelled. Each event requires adjusting future earned premium schedules and possibly refunding premium.

- Premium Financing: When a finance company pays premiums on behalf of the insured, and the insured repays the finance company, accounting must reflect the finance receivable/receivable, interest, and the eventual premium cash flows.

- Commissions, Fees, and Taxes on Premium: Premiums often carry broker/agent commissions and regulatory taxes. The system must compute commissions payable to agents based on premium installments, handle premium taxes (e.g. GST/VAT on premium), and split these out from the insurer’s net revenue.

- Carrier/Producer Settlements: In an MGA model, the MGA must settle owed premium and commissions with the underwriting carrier separately, often netting amounts.

Without an insurance-specific system, insurers resort to custom scripts or spreadsheets to handle these. All of these scenarios require granular tracking of each policy transaction. A well-designed premium subledger provides this layer.

| Accounting Challenge | Description | Insurance Subledger Solution |

|---|---|---|

| Agency vs Direct Billing | Parallel processes for premiums billed through agents or direct to clients; different remittance and reporting flows [1]. | Subledger captures agent invoices and direct invoices separately, applying consistent policy logic to both streams. For example, this resolves complex settlement between agent commissions and carrier remittance [1]. |

| Partial/Out-of-Order Payments | Customers may pay in multiple portions or skip installments; payments may apply to policies non-sequentially. | Subledger allocates each payment to specific policy invoices and periods. Even if a mid-term endorsement increases premium, the subledger re-apportions payments without manual GL journals [1]. |

| Installments, Endorsements, Cancellations | Policies change over time: mid-term changes (endorsements), or early cancelations requiring refunds. | The subledger recalculates earned vs unearned premium schedules automatically. Adjustments (such as reversing unearned premium on cancellation or recalculating on endorsement) are posted as audit-trailed entries [1] [29]. |

| Commissions/Fees/Taxes on Premium | Agent commissions and taxes (e.g. VAT/GST on insurance premiums) are tied to premium amounts and require precise calculation. | Integration modules calculate agent commission payable and tax liabilities with each policy transaction. For example, SaasWorx configures NetSuite to post commissions and TDS on commissions automatically when premiums are recorded [28]. |

| Reinsurance Cessions & Recoveries | Portions of premiums ceded to reinsurers and claims recoverable need separate accounting lines. | The subledger posts ceded premiums and claims via reinsurance automatically. Data from reinsurance contracts is used to book ceded premium, reinsurer payables, and recoverables on claims [31]. |

| Carrier/Producer Settlements | MGA must settle net of commissions, overrides, fees with the carrier periodically. | Subledger provides “carrier and producer settlement” modules that calculate net payables/receivables between MGAs and carriers, and automatically generate offsetting GL entries [1]. |

This table (simplified) illustrates common premium workflows. In each case, a specialized subledger applies insurance logic that NetSuite’s vanilla GL does not. For instance, Selectsys notes that without such a layer, insurers handle these workflows through "custom scripts, spreadsheets, or manual journal entries" [1], which is error-prone and not scalable. A premium subledger resolves these by ingesting policy data and executing built-in insurance accounting logic.

Premium Subledger Integration

How do insurers typically integrate premium accounting with NetSuite? The pattern is: keep NetSuite as the GL for consolidation, while running detailed premium allocations in the subledger itself. For example, Selectsys’s “Premium Accounting” platform (used by many large MGAs) uses this approach [4]. Policy and billing data flow from upstream systems (policy admin, rating) into the subledger. The subledger applies insurance accounting (calculating earned premium, commission accruals, UPR movements, etc.) and tracks invoices and payments at the policy/premium level [33]. It then generates summarized results – receivables, payables, reserves, and adjustments – and synchronizes them into NetSuite. In practice this means only clean, insurance-ready postings hit the GL: “receivable and payable results”, “payment application outcomes”, “endorsement adjustments”, and “netting/settlement activity” are all sent to NetSuite in a controlled way [32].

The advantage of this approach is two-fold. First, NetSuite remains the authoritative general ledger for enterprise reporting and close, preserving existing financial controls [34]. Second, by handling insurance-specific complexity outside the core ERP, companies dramatically reduce custom NetSuite development. This modular strategy “eliminates spreadsheet-driven reconciliation” and “reduces reliance on custom NetSuite scripting” as cited by practitioners [35]. Auditors and regulators benefit too: the subledger provides a clear audit trail behind each posting. Companies thus get “traceability behind posted results” and support for audits and close processes [35].

SaasWorx’s NetSuite connector offers a concrete example: they build a real-time bridge so that every policy event triggers standard accounting entries in NetSuite [29]. When a policy is issued, renewed, endorsed, or cancelled, the system automatically posts the appropriate premium earned, unearned reserve, commission, tax, and reinsurance entries into NetSuite [29] [28]. The finance team then merely reviews exceptions instead of manually entering journals. This kind of end-to-end automation not only ensures accuracy but allows the insurer to scale — a subledger can process high volumes of policy changes faster than manual methods as premiums grow.

Data and Reporting Impacts

Implementing a premium subledger also transforms data analytics. The Baker Tilly MGA automation case (a multi-line, multi-state insurer) highlights that standardized data from all MGAs can now be leveraged across the business [27]. Once the insurer centralized and cleaned MGA feeds, the data warehouse enabled them to perform program-level analytics and trends analysis instead of wrestling with siloed Excel sheets [27]. Having precise subledger data means an insurer can report premiums by agent, policy type, or segment at any point in time, combining financial and operational reporting.

Moreover, regulatory reporting depends on this subledger detail. For example, under Indian regulations (IRDAI), insurers must produce prescribed financial statements and reconciliation schedules monthly. SaasWorx notes that their NetSuite integration “enables regulatory reports to be generated directly from NetSuite without reformatting” [36]. This is only possible because the subledger layers have already classified premium, claims, and commission items into the correct buckets as per the regulators.

In short, modern insurers use premium sub-ledgers to capture, process, and audit the detailed cashflow of policies, but still rely on NetSuite as the final GL system. This hybrid approach is now considered a best practice in the industry for handling premium accounting at scale [37] [29].

IFRS 17: New Insurance Accounting Standard

Overview of IFRS 17

IFRS 17 “Insurance Contracts” is the International Accounting Standards Board’s (IASB) overhaul of insurance accounting. Issued in May 2017, it superseded the interim IFRS 4 standard [38]. Effective January 1, 2023 (with some deferrals allowed), IFRS 17 applies in any jurisdiction requiring IFRS reporting. The objective of IFRS 17 is to provide a transparent, consistent framework so that financial statements reflect the economics of insurance contracts and facilitate comparability across insurers worldwide [15] [39].

Key principles of IFRS 17 [40] [6] include:

- Current measurement of future cash flows: Insurance liabilities are measured based on the present value of expected future premiums and claims, adjusted for risk. Specifically, the fulfillment cash flows represent the probability-weighted, discounted future cash in/outflows (premiums, claims, expenses) including a risk adjustment for non-financial risk [41] [6].

- Contractual Service Margin (CSM): Any expected profit at contract inception is deferred and recognized over the coverage period. The CSM is the insurer’s unearned profit margin on the contract. It starts as the negative of the fulfillment cash flows at issue (if the contract is initially profitable), and is amortized to profit over time [6] [42].

- Revenue and expense separation: IFRS 17 distinguishes between insurance revenue (the consideration for risk coverage) and insurance service expenses (claims and other costs). It requires insurance results to be presented apart from finance income/expenses. In other words, insurers will show an “insurance service result” line net of claim costs, and a separate insurance finance income line (e.g. interest accretion on liabilities) [7].

- Loss recognition: If a group of contracts is or becomes loss-making (i.e., CSM negative), the loss is recognized immediately in profit or loss.

- Claims liability: The net liability for insurance contracts at period-end splits into two parts – the liability for remaining coverage (future obligations, including any remaining CSM and future expenses) and the liability for incurred claims (present obligation to pay already-incurred claims) [3] [6]. These align roughly with unearned premium provisions and claim reserves in traditional accounting.

Effectively, IFRS 17 replaces numerous legacy approaches with a single, forward-looking model. Under the previous IFRS 4 or local GAAP, insurers could often keep historical accounting. IFRS 4 was more of an interim standard that “permitted entities to use a wide variety of accounting practices” for insurance [39]. In contrast, IFRS 17 enforces consistency: “the IFRS 17 Standard…set out principles for the recognition, measurement, presentation and disclosure of insurance contracts” [39].

The IFRS Foundation’s summary emphasizes that IFRS 17 “combines current measurement of the future cash flows with recognition of profit over the period that services are provided” [40]. Practically, this means an insurer must build out cash flow models (often in an actuarial system) and then apply complex roll-forward calculations each period (updating discount rates, risk adjustments, actual experience vs expectations). Besides the CSM, insurers must also track things like acquisition cashflows (commission paid) and apply systematic amortization patterns (e.g. based on earned premium). IFRS 17 also provides a simplified “Premium Allocation Approach” (PAA) for short-duration risk policies (analogous to unearned premium method), but larger contracts will use the full General Model [43] [44].

From a report perspective, IFRS 17 requires extensive disclosures. Insurers will produce new metrics (e.g. insurance service revenue, insurance finance result, CSM roll-forward) and must provide reconciliations from previous GAAP submissions [10] [44]. One IFRS commentator summarized IFRS 17 as creating “a parallel run” of financial statements – insurers will report the business on both old and new bases for transitional periods [45].

IFRS 17 System Architecture: The Need for Subledgers

Because of its complexity, IFRS 17 implementation is typically a multi-year, multi-disciplinary program. At its core is an insurance accounting subledger system that sits between front-office policy administration/claims systems and the general ledger [8]. A 2021 actuarial article describes this subledger as “the detailed breakdown of the entries behind the general ledger” and notes that “the subledger is used to produce the additional entries required under the IFRS 17 presentation & disclosure framework”, which are then posted to the GL [46]. In practice, this means ingesting raw policy and claims cash flow data, performing the IFRS 17 calculation per contract group, and outputting journal entries.

In broad terms, IFRS 17 subledger systems have three key processes [16]:

- Data Management: Centralize and transform source data (policy details, cash flow projections, reinsurance, claims occurrences, FX rates, etc.) to the needed granularity. Inputs come from actuarial models, policy admin, claims systems, reinsurance feeds, etc. The subledger validates and standardizes this data (e.g. linking policies to reinsurance treaties, downscaling large volumes of cash flows to monthly buckets, etc.) [47].

- Calculation Engine: Apply IFRS 17 math. This includes computing the discounting and risk adjustments on projected cash flows; rolling forward the CSM (interest accretion, release based on coverage, adjustments for experience or changes in assumptions); amortizing previously deferred acquisition costs; and calculating reinsurance effects [48]. If a full General Model is used, this also means allocating insurance finance income and revising CSM for changes. For simpler businesses (short-tail), a Premium Allocation Approach (PAA) shortcut can sometimes be used. The IFRS subledger also needs to generate required analytics (e.g. sensitivity tests, liquidity analyses) for disclosures.

- Accounting/Posting: Translate the results into ledgers and reports. The subledger defines IFRS 17-specific accounts (for example, separate GL accounts for liability for remaining coverage, liability for incurred claims, CSM, insurance revenue, etc.) and posts journal entries at the chosen granularity (often cohort-level). These postings map contract-level outcomes into the general ledger in standardized ways [49] [9]. The subledger also produces IFRS 17 presentation and disclosure reports. Controls and reconciliation features are embedded to ensure data integrity throughout this pipeline [49].

From an organizational perspective, implementing IFRS 17 requires teams of accountants, actuaries, and IT specialists. Practices usually adopt agile sprints, with accounting policies and posting rules defined early on. For example, Deloitte’s work at Samsung Life Insurance involved close collaboration: they created a new liability management system (for assumptions, cash flows, liability movement) along with SAP for closing and reporting [11]. This dual system architecture fed IFRS 17 outputs into a familiar financial close environment. CFOs and project leads emphasize that a successful IFRS 17 project needs top-level sponsorship and clear definitions of all contract components (see Samsung Life where their Chief Accountant chaired the project [50]).

IFRS 17 Accounting Entries and GL Integration

What does this mean for NetSuite (or any general ledger)? In essence, the GL just sees the aggregate result. The subledger handles the detailed math and then issues IFRS 17-compliant journal entries. Oracle’s IFRS 17 Analyzer, for instance, has a “Subledger” function specifically to “pass IFRS 17-compliant journal entries based on the results of Contractual Service Margin (CSM) calculations” [9]. All data flows from the CSM engine to the subledger, which applies pre-approved accounting rules. Once processed, the subledger generates reports (e.g. journals, closing balances) at the chosen granularity [51].

In a NetSuite context, one would similarly configure an interface where the subledger sends journals into NetSuite. NetSuite would remain the system of record for official financial statements and tax/regulatory reporting. The goal is that business users and auditors see NetSuite balances that already reflect IFRS 17 adjustments. For example, the NetSuite books would include accounts such as “IFRS17 Liability for Remaining Coverage” and “IFRS17 Insurance Revenue” (these would be custom accounts) [21] [9]. The subledger must also handle any multiple-entity or multi-book setups (if one legal entity uses IFRS 17, the subledger should post accordingly, enabling roll-up).

IFRS 17 Reporting and Disclosures

The reporting changes under IFRS 17 are significant. Insurers must report new metrics like insurance revenue, insurance service expenses, effects of changes in assumptions, and split between insurance and finance results. Group entities will need to retool their reporting frameworks. Many use the IFRS 17 outputs for disclosures, and some may replicate these in NetSuite Financial Reports under new account structures. Moreover, IFRS 17 is often implemented alongside IFRS 9 (financial instruments) and new IFRS (e.g. IFRS 18/19). For example, Oracle’s IFRS 17 solution highlights linking actuarial and accounting data to avoid ledger misalignment [21], ensuring that changes in discount rates or risk assumptions flow through the subledger to the GL.

Claims Accounting and Claims Sub-Ledger

While premiums address the asset side (receiving cash), claims accounting deals with the liability side (paying future claims). In traditional insurance accounting, claims liabilities include claims paid, case reserves, and incurred but not reported (IBNR) reserves. Carriers track how much they owe to claimants at any point. Under IFRS 17, the concept of claims is folded into the “liability for incurred claims,” which includes both the practical claims reserves and the loss component of any onerous contracts [3].

In practical terms, insurers still need robust sub-ledger processes for claims. Each claim goes through distinct events: notification (a loss is reported), valuation (claims settlement amount estimated), payment, and possible recovery (salvage, subrogation or reinsurance recoveries). A claims sub-ledger tracks these financial events in detail. For example, one integration partner explains that a claim event should create “a liability at notification, an expense at settlement, and a recovery receivable when salvage or reinsurance recovery is expected” [52]. In effect, at the moment a claim is filed, the insurer records a reserve (liability) for the expected loss; when they actually pay, this reserve is reduced and an expense recognized. Reinsurance recoveries or salvage amounts are tracked as receivables.

This sub-ledger data ties directly to IFRS 17’s definitions. The IFRS 17 terms clarify that “liability for incurred claims” is the insurer’s obligation to pay for past-covered claims [53]. A claims sub-ledger is essentially managing that liability. By the reporting date, the sub-ledger should know the gross IBNR, case reserves (RBNS), and all movements due to new claim activity or changes in assumptions. Similarly, IFRS 17’s “liability for remaining coverage” (future service) does not include these past claims – meaning any claim cash flows yet to be paid belong fully to the first category [3]. In short, a well-structured claims sub-ledger yields the inputs needed for both parts of the IFRS 17 liability.

Claims Sub-Ledger in Practice

Insurance IT platforms often include dedicated claim accounting modules. The DICEUS General Ledger Platform example explicitly lists a Claims subledger as a module [54]. Its features include claim-level monitoring, reserves accounting, payments, recoveries, and reconciliation, all feeding into the GL [54]. Similarly, a NetSuite-based solution via SaasWorx configures NetSuite to handle claim payments and recoveries. They note: “Claims payments need to be reflected in NetSuite as a liability at notification, an expense at settlement, and a recovery receivable when salvage or reinsurance recovery is expected.” [52]. This illustrates the required entries:

- On notification: Debit “Claims Expense” and credit “Claims Payable (liability)”.

- On payment: Debit “Claims Payable” and credit “Cash/Bank”.

- On recovery: Debit “Reinsurance Recoverable” (asset) and credit “Claims Expense” (offset).

By automating this, every claim posted in the claims management system automatically generates the appropriate journal in the subledger, which NetSuite or the core GL ingests. Analysts can then slice claims by type, adjust reserves, and reconcile to tenure.

Integration of Claims and Premium Ledgers

In many insurers, the premium ledger and claims ledger are separate systems (or distinct modules). However, IFRS 17 (and insurance accounting in general) demands consistency between them. For instance, consider incurred but not reported (IBNR) reserves: these come from claims experience analysis (actuarial claim projections) and should reduce the liability for remaining coverage. Hence the premium system (tracking UPR) and the claims system (tracking RBNS/IBNR) must feed data together. A subledger approach can unify this: the same contract portfolio drives both premium unearned computations and claims forecasts. The subledger then simultaneously adjusts both sides of the balance sheet.

Case Example: Integrated Claim Accounting

Suppose an insurer receives notice of a $100,000 claim on June 15. In a claims subledger, at notification the system might immediately set a reserve (liability) for $100K. At the next financial close, IFRS 17 requires discounting (if significant time to payment, minor for P&C) and possibly risk adjustment changes. If on November 1 the insurer pays $80,000 and later recovers $10,000 from reinsurance, the subledger would post entries on those dates. All these entries — liability adjustments and expenses — eventually roll up to reduce the liability for incurred claims in the balance sheet and increase IFRS 17 claim expense in the P&L. Meanwhile, on the premium side, nothing of this claim’s flows goes into the earned premium or UPR calculations except possibly the release of any commission deferrals tied to the policy.

NetSuite itself doesn’t have built-in insurance reserve accounts; therefore, configurations or add-ons are needed. In one implementation, SaasWorx outlines that claim updates from the policy/claims system will automatically post “correct GL entries for each claim lifecycle stage” [52]. In effect, the claims system is acting as a subledger bridge. Another approach is to use the premium subledger (discussed earlier) and augment it with a claims module. In the DICEUS platform, the claims subledger coexists with the premium subledger and reserve engine to provide a comprehensive picture [55] [56].

Accounting Implications

From the accounting standpoint, a claims subledger ensures that together with the premium subledger, all insurance cash flows are captured. For example, under US GAAP (ASC 944 or “Current Estimate” methods), claims reserves roll into “loss and loss adjustment expense reserves”; under IFRS 17, that corresponds to the “liability for incurred claims”. The key technical difference is that IFRS 17 does not discount short-tail P&C claims liabilities (as ASC 944 does), but it does for long-tail (through the discount rate used in measuring fulfillment cash flows) [18]. Thus a subledger can often handle discounting/interest allocation too, as part of the IFRS 17 calculation process.

Claim recoveries (e.g. from salvage or reinsurance) deserve special note. They are recorded as assets (estimates of cash inflows) and reduce net claims expenses. A sophisticated claims subledger will track these through suspension accounts (waterfall: collect from reinsurers, then pay out, etc.). The subledger must ensure that any reinsurance recoverable is correctly netted against the gross IBNR in the IFRS 17 computations (the standard treats reinsurance similarly to insurance contracts with negative risk adjustment).

In practice, insurers find that automating claims postings is as crucial as automating premium postings. SaasWorx’s NetSuite connector explicitly mentions that claims postings move from a manual journal process to an automated workflow [52]. Similarly, a modern finance team expects the subledger to produce full audit trails for all claim entries — a major difference from legacy open reserves spreadsheets.

IFRS 17 Implications and Future Directions

Industry Impact and Survey Findings

IFRS 17 has reshaped insurers’ finance and actuarial functions. Industry surveys reveal the scale of change. A 2018 global study (240 insurers) found 92% of companies had not yet put an IFRS 17 solution in place [10], even though it was then 3 years before the original 2021 effective date. 88% acknowledged they needed new processes for IFRS 17 disclosures [10]. Deloitte’s recent survey of 360 insurers (pre-2023 go-live) emphasizes that IFRS 17 drives major system overhauls. Many insurers have nearly completed implementations and are ready for the 2023 transition [57]. In fact, by 2025 most IFRS jurisdictions have applied IFRS 17, though some have deferred. For instance, as of 2025 China and India postponed to 2026 to align with local standards [19], affecting a large pool of global premium. Under IFRS, roughly 450 large insurance groups (~$13 trillion assets worldwide) are in scope [58].

The strategic impact goes beyond accounting compliance. Once insurers have built the IFRS 17 infrastructure, they often leverage it for forecasting, risk management, and even product development. As Samsung Life’s case shows, IFRS 17 forced a “redesign of financial reporting from scratch,” which senior management used as a catalyst for broader transformation [59]. After implementation, Samsung Life is running dual reporting (old local GAAP vs IFRS17) in parallel, using the new metrics to assess product profitability and solvency strategy [45]. In another instance, Tokio Marine Malaysia reported that automating IFRS 17 with Tagetik reduced manual reconciliation and gave auditors confidence in the numbers; the CFO noted they are “in control of our data, disclosures, and audits, and ready for what’s next.” [60] [13].

Technology Trends and Solutions

The market for IFRS 17 technology has grown rapidly. Packages range from specialized actuary-led engines (e.g. Moody’s, SAS, TCS Diligenta) to integrated accounting suites (Oracle’s IFRS 17 Analyzer, SAP’s Financial Products Subledger, CCH Tagetik, Workiva, OneSumX, Linedata, etc.). These systems often include built-in subledger and disclosure modules. For example, Oracle’s IFRS 17 solution promotes tight integration between actuarial models and the subledger, eliminating inconsistencies between contracted CSM results and the GL posting [9]. Some of these tools are being connected directly to ERPs: Oracle positions their solution to feed any GL (including NetSuite) with IFRS 17 journals.

A notable trend is cloud-based end-to-end platforms that handle data, calculations, accounting, and reporting (e.g. Chartis, DXC FIS, Oracle IFCFS). The DICEUS platform example illustrates this convergence: its general-ledger solution includes premium and claims subledgers, reserve engines (for UPR, RBNS, IBNR), reinsurance modules, and IFRS 17 portfolios handling (CSM, risk adjustment) [61] [56]. Once data reside in such an integrated ledger, it becomes easier to run parallel views (IFRS vs IFRS GAAP) or produce statutory returns.

Given NetSuite’s popularity, we may see more pre-built connectors and apps for insurance. Already, the Selectsys and SaasWorx offerings effectively function as “insurance accounting platforms” attached to NetSuite. We might expect AppExchange-like markets where insurers can download modules for IFRS 17 or claims accounting (though as of 2026, IFRS 17 for NetSuite is still nascent). The key architecture will likely remain: policy/claims systems → insurance subledger → NetSuite GL. Future trends could include tighter APIs (e.g. real-time streaming of policy events) and embedding of analytics (predictive underwriting, IBNR modeling) directly into the finance workflow.

Ongoing Regulatory and Market Developments

Beyond IFRS 17, new regulations continue to shape insurance accounting. For instance, IFRS 18 (Issued April 2024) revised presentation/disclosure requirements for annual financial statements, affecting how IFRS 17 and IFRS 9 outputs are formatted. IFRS 19 (May 2024) provides relief for subsidiaries without public accountability, easing disclosure burdens (so some IFRS 17 filers may report less detailed numbers) [62]. In the U.S., the new GAAP standard (ASU 2018-12 / ASC 944 LDTI) also took effect in 2023 for public insurers, introducing similar contract liability models. While U.S. GAAP and IFRS differ (e.g. IFRS 17’s CSM vs GAAP’s unlocked discount approach), the parallel pressures reinforce investment in robust insurance accounting systems.

Tax and regulatory filing requirements will continue to guide accounting system needs. For example, India’s IRDAI recently mandated detailed disclosures on premiums and claims, which motivated local insurers to implement data-integrated ERPs like NetSuite with country-specific modules [63]. Solvency regimes (Solvency II in Europe, RBC in the US) also require granular data; many insurers reuse IFRS data for risk reporting. In future, regulators may demand real-time analytics or AI auditing on top of these ledgers.

Future Implications for Insurers Using NetSuite

For insurers that have adopted NetSuite, the landscape remains promising but challenging. NetSuite’s cloud model means continuous upgrades; insurers must ensure that custom insurance modules remain compatible. They should aim to externalize as much insurance-specific logic into upgradable modules as possible. The increasing use of subledgers (premium, claims, reinsurance) essentially turns NetSuite into a central data warehouse and consolidation engine. Insurers should invest in seamless data integration (APIs, middleware) between underwriting systems and the finance stack.

Looking ahead, we may see more built-in insurance functionalities in NetSuite through acquisitions or standards. For instance, Oracle’s strategy might eventually offer direct IFRS 17 extension for NetSuite (similar to how Oracle E-Business Suite has an IFRS 17 module). In the short term, best practice is to document all accounting processes and ensure subledger outputs have full audit trails. The era of attachments and spreadsheets must give way to fully electronic, auditable linkages: e.g. uploading premium bills via pharma-like EDI standards or using the Salesforce platform (many insurers use Salesforce for policy CRM).

Finally, as insurers execute IFRS 17, many are seizing the “once-in-a-generation” chance to modernize. They embed analytics and key risk indicators (e.g. portfolio profitability by cohort, volatility of claims assumptions) into finance dashboards. Cloud ERP systems like NetSuite will interoperate with new actuarial systems via the subledgers we discuss. In essence, the industry is moving toward end-to-end value chains: from product design to underwriting to claims through to official reporting, closed-loop in one platform family. This promises finer profitability management and quicker strategic responses, but requires continual technology evolution and strong governance.

Conclusion

Upholding accurate and compliant accounting in the insurance industry demands specialized systems. NetSuite provides a powerful ERP backbone for finance, but insurers must augment it for their unique needs. This report has shown that by using premium accounting subledgers and claims subledgers alongside NetSuite, companies can handle the intricacies of insurance contracts without overwhelming their core GL. Premium subledgers manage the lifecycle of premiums (invoices, payments, deferrals, commissions), while claims subledgers handle loss obligations (reserves, payments, recoveries) [2] [52]. Together, these feed consolidated results into NetSuite for financial close.

The introduction of IFRS 17 intensifies this requirement. IFRS 17’s detailed contract valuation means insurers must implement a new subledger-based architecture that captures policy-level cash flows and produces IFRS-compliant journals [8] [9]. As shown by case studies, successfully adopting IFRS 17 (and analogous GAAP changes) hinges on bridging actuarial models with accounting ledgers. Insurers like Samsung Life and Tokio Marine demonstrate that when done well, IFRS 17 projects not only achieve compliance but also pave the way for better risk management and data control [11] [12].

Empirical data underscores the scale of change: virtually all IFRS-bound insurers have been or are in the process of upgrading their finance systems [10] [19]. Premium accounting projects like the Baker Tilly case and NetSuite integrations by SaasWorx/Selectsys show measurable gains: time savings from days to seconds and elimination of reconciliation headaches [27] [35]. These improvements translate to strategic flexibility: insurers can expand product lines or MGA networks knowing their accounting can handle the volume.

In summary, NetSuite plus insurance subledgers is the recommended model. It preserves the robustness and auditability of a leading ERP while fully addressing insurance accounting rules. Stakeholders (finance, audit, actuarial) gain confidence from having a clear, auditable flow of data from policies to financial statements. As regulations and technologies evolve, the modular architecture we describe — policy/claims systems → insurance subledgers → NetSuite GL — offers agility. Insurers that invest in this architecture will be well-positioned for future compliance (be it IFRS 18 disclosures or AI-driven audit) and for leveraging analytics on their core insurance data.

References: [All statements above are supported by industry sources and best-practice reports [1] [46] [29] [10] [3], including vendor documentation, actuarial analyses, and regulatory surveys.]

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.