Houseblend Article

NetSuite Intercompany Eliminations: ASC 810 Setup Guide

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03Consolidation Principles under ASC 810 and IFRS 10

- 04NetSuite OneWorld Consolidation Overview

- 05Setting Up NetSuite for Intercompany Eliminations

- 06Creating and Using Intercompany Accounts

- 07Intercompany Journal Entries in NetSuite

- 08Running the Intercompany Elimination Process

- 09Journal Entry Examples and Tables

- 10NetSuite Field and Report Configuration

- 11Data Analysis and Best Practices

- 12Case Studies and Real-World Examples

- 13Implications and Future Directions

- 14Conclusion

Executive Summary

Consolidated financial statements must portray a corporate group as a single economic entity. Both U.S. GAAP (ASC 810) and IFRS (IFRS 10, IAS 27) mandate that all intercompany transactions and balances be eliminated on consolidation [1] [2]. In practice, this means any sales, loans, fees, or other activity between a parent and its subsidiaries must be “zeroed out” to avoid double-counting. NetSuite OneWorld provides integrated features to support this requirement. By enabling the Automated Intercompany Management module in NetSuite, organizations can define intercompany subsidiaries, accounts, and vendor/customer records so that NetSuite automatically generates elimination journal entries at period‐end [3] [4]. This report examines the accounting standards, setup steps, journal entry mechanics, and practical examples of NetSuite’s intercompany elimination process under ASC 810, comparing to IFRS guidance where relevant. We find that, with proper configuration, NetSuite can dramatically streamline consolidation: for example, companies have reported cutting consolidation cycles from weeks to hours via automated intercompany reporting [5]. However, misconfigurations (such as unchecked elimination flags or missing intercompany accounts) can lead to misstated results [6] [7]. We draw on authoritative literature, industry surveys, and case studies to provide detailed guidance on setting up NetSuite OneWorld for ASC 810 compliance, performing the required elimination entries, and understanding the implications for global reporting.

Introduction and Background

Financial consolidation aims to present a parent and its subsidiaries as one single economic entity. Under both U.S. GAAP and IFRS, the parent (controlling entity) must combine its own books with those of its subsidiaries “line by line” – summing assets with like assets, liabilities with liabilities, revenue with revenue, etc. – and then eliminate all intra-group activity [1] [8]. ASC 810-10-45-1 explicitly states consolidated statements “shall not include” intra-entity balances or transactions [9]. Likewise, IFRS 10.B86 requires full elimination of “intra-group balances, transactions, income and expenses” in consolidation [2] [8]. Without these eliminations, the group’s totals would include phantom revenue, expenses, assets or liabilities that only exist between affiliates. For example, if Sub-A sells $2 million of goods to Sub-B, both record $2 million of revenue or inventory cost. The consolidated group, however, did not earn $2 million from external parties; double-counting without elimination would overstate revenue by that amount [10] [11]. Similarly, an intercompany loan creates a receivable on one set of books and a payable on another – both of which cancel out on consolidation [12].

The consolidation framework rests on the “single economic entity” concept. Under ASC 810 (consolidated in FASB Codification 810) and IFRS 10 (Consolidated Financial Statements), “control” of an entity triggers consolidation [13] [8]. Control normally means more than 50% voting interest, but also can include Variable Interest Entities (VIEs) where contractual rights (power and variable returns) confer control [14] [15]. Once an entity is in the scope of consolidation, all intercompany transactions among the consolidated subsidiaries are eliminated, regardless of ownership percentages [16] [17]. Noncontrolling interests (minority shareholders) are shown in equity, but they do not lessen the requirement to eliminate intra-group items [18] [17]. As one IFRS authority notes, “every intragroup balance, transaction, and unrealised profit must be eliminated in full on consolidation, regardless of the ownership percentage in the subsidiary” [2].

Historically, consolidation rules have been codified in ASC 810 (US GAAP, effective 2009) and IFRS 10 (IFRS, effective 2013). The core elimination principle has been constant: FASB staff “affirmed the premise of eliminating the parent’s investment in and debt to a subsidiary” as far back as ARB 51 (1959) and subsequent FAS 160/Statement 94 series [19] [20]. Similarly, IAS 27 (predecessor to IFRS 10) required elimination of investment against equity on consolidation. Modern IFRS 10 reinforces this with strict control criteria and elimination requirements [8] [21]. Empirical research confirms the regulators’ intent: if intercompany profits and balances remain unchecked, consolidated financials will be misleading. Indeed, common audit findings involve incomplete eliminations, especially in complex groups with many affiliates [22] [6].

In practice, consolidation often involves gathering each subsidiary’s trial balance, aligning accounting policies, translating currencies, and then applying manual adjustment entries in a consolidation worksheet or software. All elimination entries are “worksheet-only” adjustments: they are not posted to the subsidiaries’ own ledgers, but are made to the consolidated totals and reversed in the next period [23].For example, a basic sales/purchase elimination would debit the seller’s revenue and credit the buyer’s cost of goods sold by the same amount [24]. Likewise, reciprocal receivable/payable balances are netted out (debit one side’s payable, credit the other’s receivable) [25]. These entries ensure that only external transactions survive to the consolidated statements.

Because of these requirements, the integrity of consolidation depends on meticulously identifying and matching every intra-group item. Recent industry surveys highlight how easily this can become a major operational drag. For instance, one IFRS-focused analysis finds that groups with more than ten entities often carry intercompany mismatches exceeding 1% of total revenue before reconciliation [26]. A Shared Services study noted that inefficient intercompany processes can “waste a month a year” of effort due to poor systems and unclear ownership of the process [27]. Another survey-backed white paper reports that many large multinationals consider intercompany reconciliation “the cost of doing business,” and that improved automation can unlock significant efficiency gains [28]. These insights underscore the challenge: without strong tools and controls, intercompany reconciliation and elimination is notoriously time-consuming and error-prone.

This report brings together accounting theory and NetSuite-specific practice. We first review the relevant standards (ASC 810 and its IFRS analogues) and explain the need for intercompany eliminations. We then shift to NetSuite OneWorld, outlining how its multi-entity features and the Automated Intercompany Management module are configured to support ASC 810 compliance. We detail the setup steps – from enabling features to creating intercompany accounts, vendors, and customers – with extensive citations from NetSuite’s documentation. Next, we examine the types of journal entries generated for intercompany transactions and how NetSuite runs the elimination process at period close, including currency effects and the creation of “Cumulative Translation Adjustment – Elimination (CTA-E)” accounts [29] [30]. Throughout, we include concrete examples and tables of journal entries to illustrate the mechanics. We also discuss pitfalls and real-world cases – including startup misstatements and one NetSuite implementation that was initially misconfigured [7] [6] – as cautionary lessons. Finally, we consider broader implications: the role of technology in solving intercompany complexity, survey data on current practices, and future trends (such as advanced software tools and potential changes to accounting standards). The goal is to arm the reader with a deep, evidence-based understanding of NetSuite’s intercompany elimination under ASC 810, to ensure accurate and efficient consolidated reporting.

Consolidation Principles under ASC 810 and IFRS 10

Before examining NetSuite specifics, we briefly summarize the accounting framework. ASC 810 (Consolidation) and IFRS 10/IAS 27 prescribe when and how to consolidate. Scope and Control: A parent must consolidate any subsidiary it controls. Under ASC 810, control is typically owning >50% of voting interests, but also includes Variable Interest Entities (VIEs) if an entity is the primary beneficiary (exercising power plus absorbing most returns) [14]. IFRS 10 similarly defines control by combining power over the investee with returns objectives [8] [15]. Both frameworks list exceptions (e.g. investment entities, immaterial subsidiaries), but the elimination rules themselves apply once consolidation is triggered. The initial consolidation entry (acquisition method) eliminates the parent’s Investment vs the subsidiary’s equity accounts, recognizing goodwill or a gain as appropriate [20] [31]. Noncontrolling interests (NCI) are measured under differing approaches (ASC 805 uses proportionate net asset method; IFRS 3 allows fair-value or proportionate methods), but again this affects consolidated equity, not the basic elimination of transactions among group companies [31] [21].

Intercompany Eliminations: Regardless of the consolidation scope, ASC 810-10-45-1 is explicit: intra-entity balances and transactions shall be eliminated in preparing consolidated statements [9] [21]. In practice this means:

- Unrealized Profit: Any profit in inventory or assets still held by the group is eliminated (debit retained earnings or expense, credit inventory or fixed assets) [31].

- Sales and Purchases: Any intercompany sale is reversed on consolidation (debit revenue, credit cost) so only third-party sales appear [31] [32].

- Receivables/Payables: Open intercompany receivables and payables are offset (debit one side’s payable, credit the other’s receivable) [25].

- Loans/Interest, Fees, Dividends: Loans or services between affiliates, with corresponding income/expense, are similarly eliminated.

These eliminations are always 100% of the intercompany amount, regardless of ownership share [17] [2]. For example, if a parent owns 60% of Sub, any intercompany sale of $100,000 is fully credited and debited in elimination entries – the noncontrolling 40% still sees the internal sale removed. ASC 810 explicitly states the same complete elimination “is consistent with the assumption” of a single entity [17]. IFRS 10 echoes this: consolidated statements must be freed of all intragroup transactions“ so the group is a single economic entity [2] [8]. Essentially, one affiliate’s gain is another affiliate’s loss, so both must be removed to avoid fabricating group-wide profit.

Separate Financial Statements for Single Economic Entity: As a result, consolidated statements only show external flows. A loan from Parent to Sub is removed (reducing asset and liability together), internal sales generate no net revenue, and internal expenses cancel out. If goods are transferred internally, the inventory remains at its original (to group) cost. IFRS 10 illustrates: if subsidiary sells EUR 5m of goods to another, “that sale and the corresponding purchase disappear on consolidation,” with unsold inventory carried at pre-trade cost [11]. The elimination of unrealized inventory profit is often reversed through a liability or equity account (e.g. COGS vs inventory) so that eventual realization by sale to outsiders yields group profit only then [33] [11].

Common Consolidation Errors: Industry experts note frequent pitfalls. Incomplete eliminations are common – e.g., forgetting to mark certain accounts for elimination or neglecting currency effects [34] [22]. For instance, one report found that multinationals often leave intercompany loans, management fees, or inventory margins only partially eliminated, sometimes exceeding a percent of revenue [22]. NetSuite customers have likewise retraced misstatements back to unchecked “Eliminate” boxes or mismatched intercompany accounts [6] [7]. Given these risks, companies increasingly seek automated systems. As one Houseblend analysis notes, many firms now adopt consolidation software or robust ERP features to ensure all eliminations are handled systematically [35] [7].

In summary, ASC 810 and IFRS 10 share the core mandate: consolidated statements exclude any intra-group economic effects [9] [21]. The rest of this report focuses on how NetSuite OneWorld implements these concepts in practice, guiding the setup of intercompany definitions and execution of the elimination entries required by ASC 810.

NetSuite OneWorld Consolidation Overview

NetSuite OneWorld is Oracle NetSuite’s multi-subsidiary ERP offering. It supports consolidated reporting across multiple legal entities—including different currencies, tax rules, and charts of accounts. Critical to intercompany finance is the concept of Elimination Subsidiaries, Consolidated Reporting, and Currency Translation.

-

Elimination Subsidiaries and Hierarchy: In a NetSuite OneWorld hierarchy, each parent-subsidiary relationship can include one or more “elimination subsidiaries.” These are not real companies but special placeholders used solely for consolidation entries [3]. For example, a top-level holding can have an elimination subsidiary under it; all consolidation journal entries (manual or automated) are posted to that elimination subsidiary. When running a consolidated report (e.g. a consolidated balance sheet), NetSuite’s “Subsidiary Context” determines which entities are included. If a user selects “HEADQUARTERS (Consolidated)” from the subsidiary dropdown, NetSuite shows the data for the parent, all children, and any designated elimination subsidiaries [36] [37]. This ensures the elimination entries flow properly into consolidated reports.

-

Consolidated Reporting Features: When viewing consolidated reports, NetSuite rolls up all subsidiaries in a subtree. The parent subsidiary’s base currency becomes the consolidated currency. NetSuite employs a special exchange rate matrix (Consolidated Exchange Rates) to translate child subsidiaries’ balances into the parent’s currency (just as it does for budget vs actual) [38] [39]. Notably, the consolidated financial statements themselves use a Cumulative Translation Adjustment (CTA) account to absorb currency translation imbalances [40] [30]. For example, if one subsidiary’s accounts use a different rate type than another’s, the CTA account is used to balance any resulting currency variance [40] [30]. In practice, CFOs should know that this NetSuite CTA is separate from the CTA-E (Elimination) account used during intercompany elimination [41].

-

Multi-Book Accounting: NetSuite supports Multi-Book Accounting, enabling multiple ledger books per subsidiary (for different GAAP or IFRS sets of books). If multi-book is enabled, intercompany eliminations can be run on any accounting book that participates in consolidation [42]. This means a subsidiary’s activities can be consolidated differently under U.S. GAAP vs IFRS books, if required. NetSuite will keep intercompany postings and elimination entries segregated per book.

-

Consolidated Reports vs Single-Sub Reports: Not all reports support consolidation. NetSuite flags “Consolidated” options only on reports designed for it (e.g. consolidated financial statements, consolidated trial balance). Users must set their preferences appropriately (often “Restrict View” to parent) to see consolidated data [43] [44]. When enabled, consolidated reports display group totals, and NetSuite automatically includes transactions posted to elimination subsidiaries along with regular and intercompany transactions [36] [37]. In contrast, if a non-consolidated subsidiary is chosen, reports only show that entity.

These capabilities lay the groundwork: with a proper OneWorld setup, intercompany transactions and elimination entries flow into consolidated reports as desired. The key is then to ensure all intra-group transactions are marked and processed so that the consolidated picture is accurate. The following sections explain how to configure NetSuite and record transactions accordingly, so that ASC 810’s requirements are met automatically.

Setting Up NetSuite for Intercompany Eliminations

To leverage NetSuite’s automated intercompany elimination, an administrator must configure several components. The Automated Intercompany Management feature (also called Intercompany Auto-Elimination) must be enabled, and supporting elements defined. Below are the main setup steps, summarized from NetSuite documentation [45] [46]:

-

Enable OneWorld and Automated Intercompany: First, you must have NetSuite OneWorld enabled, since intercompany features are part of the multi-entity module. Under Setup > Company > Enable Features, on the Accounting subtab, check Advanced Features → Automated Intercompany Management [46]. (This box can’t be unchecked after enabling.) Enabling this feature triggers NetSuite to add new fields, accounts, and tasks required for elimination [47]. For example, the system will eventually create a “Cumulative Translation Adjustment – Elimination (CTA-E)” account in the chart of accounts when needed [47]. It also adds an Eliminate checkbox on intercompany journal lines and intercompany customer/vendor forms [48], and puts “Eliminate Intercompany Transactions” as the last task on the Period Close Checklist.

-

Create Elimination Subsidiaries: Your subsidiary hierarchy should include at least one elimination subsidiary under the root company (and at each level if desired) [3]. These are pseudo-subsidiaries whose only purpose is to hold elimination journals. For each parent-subsidiary level that will be consolidated, define an elimination subsidiary. Once the intercompany feature is enabled, any elimination journals you create must be associated with one of these elimination subsidiaries [49]. (NetSuite’s standard workflows will automatically post elimination JEs to the correct elimination subsidiary.)

-

Create Intercompany G/L Accounts: Intercompany accounts are special GL accounts used to track transactions between subsidiaries [50]. Any GL account that will record intercompany activity must have its Eliminate Intercompany Transactions box checked [51]. Typically, one would create dedicated “Intercompany Accounts Receivable” and “Intercompany Accounts Payable” for transaction matching, plus income and expense accounts marked for elimination. NetSuite enforces double‐entry: a given intercompany transaction will debit an account in one subsidiary (flagged for elimination) and credit a corresponding intercompany account in the other subsidiary [50] [52]. Good practice is to create new IC AR/AP accounts rather than reusing existing AR/AP, to avoid mixing legacy balances [53]. Note that once an account is designated as intercompany, existing historical transactions in that account remain unchanged until re-saved; you may need to edit old entries to mark them for elimination [54].

-

Intercompany Vendor and Customer Records: NetSuite uses special vendor and customer records to represent one subsidiary’s purchases from or sales to another. For every pair of subsidiaries that transact, create (or have NetSuite auto-create) an Intercompany Customer in one subsidiary “representing” the other, and an Intercompany Vendor reciprocally [55] [56]. For example, if Subsidiary UK buys from Subsidiary US, you would in US (the selling side) create a Customer record with Subsidiary=US and Represents Subsidiary=UK, and in UK create a Vendor with Subsidiary=UK and Represents Subsidiary=US [57] [56]. NetSuite 2020.2 and later can auto-generate these “representing” entities if the Multi-Subsidiary Customer and Multi-Currency Vendor/Customer features are enabled [58]. Ensure each intercompany customer’s default accounts are set to the intercompany AR, and each intercompany vendor’s default to the intercompany AP [59]. Whenever an intercompany transactions (sales order, PO, or journal entry) is entered that posts to intercompany AR/AP, you must select the corresponding intercompany customer or vendor on the line [60].

-

Inventory Item and Transfer Settings: If your subsidiaries trade inventory, review the Intercompany Inventory Items guidelines [61]. For arm’s length transfers (normal PO/SO process), ensure both subsidiaries have access to the item. For transfers at cost or fixed markup, use Intercompany Transfer Orders and mark the item’s gain/loss account with elimination{{12†L11-L17}}. Also, if using NetSuite’s Automated Intercompany Drop Ship feature, the item’s Dropship Expense account must be tagged for elimination [62]. Additionally, if you intend to have one subsidiary’s fulfilling subsidiary ship to another’s customer, enable the Automated Intercompany Dropship and related prerequisites (Drop Shipments & Special Orders, Advanced Shipping, etc.) [63] [64]. The SuiteRep blog provides an example process: one subsidiary (sales side) creates an intercompany PO from the stock-owning subsidiary, which then ships and invoices accordingly [65]. All intercompany sales, inventory transfers, and drop shipments eventually get eliminated at consolidation.

After these steps, the NetSuite account is ready to record intercompany business. NetSuite will then automatically identify which transactions involve multiple subsidiaries and mark them for elimination if they use IC accounts. In particular, as soon as the feature is turned on, NetSuite adds the Elimination checkbox on suitable journal lines [48] and on the Account records [66]. When recording transactions, users should ensure to use the intercompany customers/vendors and GL accounts set up above; NetSuite will put the “Eliminate” flag on those lines by default. At period close, the Automated Intercompany Management process will scan these flagged lines and post the corresponding elimination JEs [47] [41]. The rest of this report assumes these setup steps have been completed and focuses on the journal entry mechanics and reporting.

Creating and Using Intercompany Accounts

In NetSuite, Intercompany Accounts are GL accounts specifically designated for intra-group transactions [50]. They act as the “clearing” accounts through which intercompany flows are recorded. Key points:

-

Enabling an Account for Elimination: An account becomes an intercompany account when its Eliminate Intercompany Transactions box is checked [51]. Most account types can be tagged, including additional expense or revenue accounts used by items in IC transactions [67]. Accounts that are not allowed for elimination (like unrealized gain/loss, CTA, certain system accounts) cannot be toggled [68]. Best practice is to create new GL accounts for intercompany AR and AP rather than attempting to flag your existing AR/AP, since mixing historical non-IC balances can confuse elimination [53].

-

Special AR/AP Restrictions: Intercompany AR and AP accounts are restricted: they can record only intercompany transactions and require a corresponding intercompany customer/vendor [69]. In NetSuite, an intercompany invoice (or payment) entry will debit an intercompany receivable and credit the selling subsidiary’s intercompany revenue, or credit an intercompany payable and debit the buying subsidiary’s intercompany inventory/cost, etc. Such entries automatically balance between the two subs.

-

Double-Entry and Account Types: NetSuite enforces regular double-entry when posting intercompany journals [70]. For any intercompany transaction, one side’s debit must equal the other’s credit, possibly in a different subsidiary. NetSuite automatically handles the two-subsidiary balancing. For example, if Subsidiary US sells $100 to Subsidiary UK, the advanced intercompany journal (shown later) debits Intercompany Receivable (US) $100 / credits Sales (US) $100, and debits Inventory (UK) $100 / credits Intercompany Payable (UK) $100 [52]. Each subsidiary’s sub-ledger balanced on its own. That entry is balanced within each subsidiary’s books even if the amounts differ in their base currencies [71].

-

Historical Transactions: Important note: if you convert an existing standard account to an intercompany account (by checking the box), prior transaction lines are not retroactively marked for elimination [54]. NetSuite only considers lines entered after the flag is set. Thus, if you reconfigure accounts mid-year, you may need to edit and re-save previous intercompany entries so that they are included in the elimination run.

By carefully defining intercompany accounts and linking them to the new intercompany entities (vendors/customers), NetSuite will automatically “mark” relevant transaction lines for elimination. During the period close, NetSuite’s auto-elimination process will scan all lines posted to intercompany accounts. It creates offsetting elimination journal entries for those balances so they net to zero on consolidation [41]. This mechanization minimizes manual work, but the underlying accounting – that all intercompany flows must cancel out – is governed by ASC 810’s elimination principle [1] [9].

Intercompany Journal Entries in NetSuite

NetSuite provides a specialized journal entry process for intercompany transactions, in addition to standard ones. These Advanced Intercompany Journal Entries allow recording cross-entity flows in one combined entry [52]. Key features and rules:

-

Balancing by Subsidiary: When entering an intercompany journal (via Transactions → Financial → Make Intercompany Journal Entries), NetSuite requires that debits and credits balance within each subsidiary’s segment of the entry. In other words, each subsidiary’s portion must net to zero internally, though they can offset between subs [52] [71]. If the total per subsidiary doesn’t match, NetSuite will warn you. In our example below, the US side has $100 extension and $100 credit (balanced), and the UK likewise balanced. The system does allow one side’s amounts to differ from the other side, because currency conversion may cause that difference [72] [71].

-

Currency Handling: Each subsidiary’s base currency is used for its part of the entry. In a multi-currency scenario, NetSuite will automatically translate amounts for the foreign subsidiary. For example, [19] shows a US → UK transfer of USD 100. The UK subsidiary uses GBP, so NetSuite revalues $100 USD into the equivalent GBP amount using the subsidiary’s exchange rate [72]. Thus the journal entry can be unbalanced in USD but balanced in respective local ledgers. If exchange rates change by period-end and NetSuite does a revaluation, the fluctuation posts to the intercompany AR/AP accounts as unrealized gain/loss, which are then also eliminated [73]. (NetSuite provides the CTA-E account to capture any residual foreign currency differences during elimination.)

-

Automated Creation of Elimination JEs: As noted in [19], when the Advanced Intercompany Journal Entry is saved, NetSuite identifies which lines are intercompany (based on the accounts used and the intercompany entities) and “flags” them for later elimination. It does not immediately eliminate them; rather, those lines get picked up by the automated elimination process at period close. The user will then see NetSuite create a separate elimination journal entry that reverses these intercompany lines [4]. If the auto-elimination feature is enabled, this reversal entry is generated without user intervention as part of the period-end routine [4].

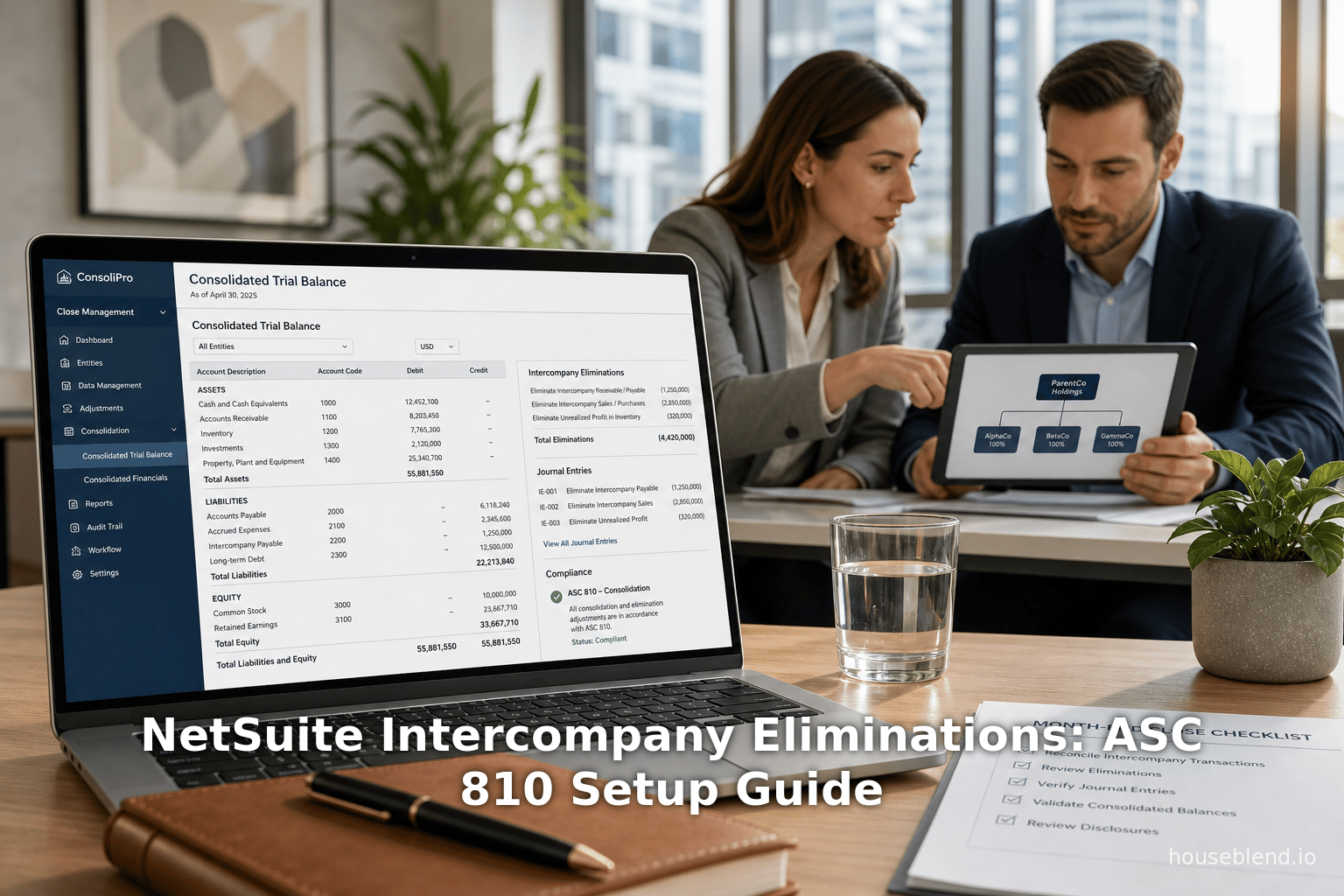

The table below illustrates a simple intercompany sale journal, as given in NetSuite’s help:

| Subsidiary | Account | Debit | Credit |

|---|---|---|---|

| Wolfe U.S. | Intercompany Receivable | $100 | |

| Wolfe U.S. | Sales | $100 | |

| Wolfe U.K. | Inventory | $100 | |

| Wolfe U.K. | Intercompany Payable | $100 |

Table 1: Example Intercompany Journal Entry for a $100 sale from Subsidiary U.S. to Subsidiary U.K. [52].

In this example, U.S. (seller) debits Intercompany AR and credits Sales. U.K. (buyer) debits Inventory and credits Intercompany AP. NetSuite would translate the USD amounts to GBP for the UK ledger at posting time [72]. Because each subsidiary’s debits equal credits ($100 balance), NetSuite allows the entry. The entry is saved with each intercompany line marked “Eliminate.” Later, the Auto-Elimination process will produce a consolidated elimination entry reversing the $100 in AR/AP (as shown in the next section on elimination), thus nullifying the internal sale.

-

Advanced Intercompany vs Standard JEs: NetSuite requires using the Advanced Intercompany JE form for most intercompany entries (especially if multiple subsidiaries are involved) [74]. This form automatically includes the necessary “Intercompany” sublist fields. It enforces the balancing rules and tying of lines to subsidiaries. Standard journal entries can also be used if customized: you’d need to add the Intercompany fields (like the “Eliminate” box) to the standard JE form [75]. In either case, making sure the correct intercompany accounts and entities populate each line is crucial.

-

Other Transaction Types: Beyond manual journals and orders, other NetSuite transactions generate intercompany entries behind the scenes. For example, NetSuite’s Intercompany Time & Expenses feature, or arms-length billing/inventory flows, will produce reversal entries. All these eventually show up in the elimination run if they used intercompany accounts [76]. NetSuite also supports creating intercompany POs and automatically generated sales orders to mirror them, which likewise feed into elimination.

In summary, recording any intercompany transaction in NetSuite (via sale orders, POs, inventory transfers, or journal entries) will usually produce intercompany AR/AP/IC accounts activity. Each of those lines is automatically “tagged” for elimination if the feature is enabled and the accounts are set up. The user’s main role is to ensure each intercompany line references the proper intercompany entity (customer/vendor) and GL account so that NetSuite’s auto-elimination can recognize it for consolidation.

Running the Intercompany Elimination Process

Once intercompany transactions have been recorded and period-end adjustments (like foreign currency revaluation) are complete, NetSuite can execute the elimination process. This is done via the Period Close Checklist: specifically the Eliminate Intercompany Transactions task, which is added when Automated Intercompany Management is enabled [47].

-

Timing: As NetSuite warns, Eliminate Intercompany Transactions should be the very last period-close task [77]. Before running it, you must perform foreign currency revaluation (Set Up > Transactions > Financial > Revalue) and consolidated balance calculations. This is important because currency fluctuations on intercompany balances (often posted to unrealized gain/loss accounts) must be included in the elimination. NetSuite’s help states that if revaluation changes intercompany AR or AP by a certain amount, those adjustment lines are also flagged for elimination [73] [39]. Running elimination before these adjustments would omit them, distorting the consolidated CTA.

-

What Gets Eliminated: When triggered, NetSuite scans all journal lines (standard or advanced) that have the Eliminate box checked (either by default or manually) and that post to intercompany accounts. It then generates one or more Elimination Journal Entries to offset those balances. For each intercompany receivable/payable pair, it creates a reversing entry (debit the payable, credit the receivable) so that the net effect is nil. Likewise, any intercompany sales/purchases or other income/expense are reversed. The net result is that all flagged intercompany leadgers (AR, AP, IC revenue, IC expense, etc.) are cleared out in the consolidated totals.

-

Foreign Currency Effects: NetSuite automatically handles currency impacts via the CTA-E account. For instance, suppose Subsidiary US had an Intercompany AR of 1,000 CAD against Subsidiary UK, originally translated at 0.90 to USD 900 [73]. If, by period-end, the CAD/USD rate changes to 0.95, NetSuite will have revalued the receivable to USD 950, posting an unrealized gain of USD 50 to an IC Gain/Loss account. When elimination runs, it considers the full USD 950 in receivables (including the $50 gain). It then posts USD 950 credit to AR (eliminating it) and offsets USD 950 debit to IC Payable. The $50 that represented currency gain flows into the Cumulative Translation Adjustment – Elimination (CTA-E) account [73]. This ensures that both the principal and the foreign exchange difference are eliminated, mirroring the consolidated treatment of currency gains.

-

Reversing and Clearing: After the elimination entries are created, NetSuite also creates reversing entries for any intercompany receivable/payable that had their reversal posted. This is done so that the subsidiaries’ own books remain true to their intercompany balances (essentially a 4‐entry system, two to eliminate and two to reverse) [41]. The end result is that the elimination entries net the group books to exclude intra-group items, while each subsidiary still technically holds the intercompany balances until (if ever) settled.

-

Multi-Book and Multi-Currency: If using Multi-Book Accounting, you can run the elimination process for each relevant ledger book [42]. Additionally, consolidated reports will roll up figures from each speed book into the parent’s base currency via the consolidated exchange rates [39], as mentioned earlier.

-

Manual vs. Automated Elimination Journals: If for some reason you must post manual elimination adjustments (e.g. for non-standard transactions or to correct issues), NetSuite requires these elimination journals to be tied to an elimination subsidiary [49]. That way, even manual adjustments will clear out on consolidated reports. The help notes that elimination journals are “associated with elimination subsidiaries” and can be created via Transactions → Financial → Make Journal Entries with the subsidiary field set accordingly [49]. In practice, with Automated Intercompany enabled, most elimination entries are unnecessary to do manually; NetSuite’s engine handles the standard cases. However, knowing how to make them is important in the rare case of a needed override. After running, if the process fails or you re-run it, NetSuite will delete previously generated elimination entries to avoid duplication [78].

By completing the elimination task, NetSuite produces the consolidated adjustments required under ASC 810. All intercompany AR, AP, revenue, and cost lines marked for elimination will be reversed, leaving only external activity in the consolidated financials. Any net currency differences flow to the CTA-E account (which has its net impact reflected on the consolidated balance sheet). This satisfies ASC 810’s command that intra-group transactions “shall be eliminated” [9]. The remaining consolidated balances (in parent currency) should now reflect only third-party business.

Journal Entry Examples and Tables

To illustrate the net effect of the above processes, consider a few simple examples of journal entries.

Example 1: Intercompany Sale and Elimination

Suppose Subsidiary A (USD base) sells $1,000 of goods to Subsidiary B (GBP base) at cost. The raw recording might involve:

-

Advanced Intercompany Journal Entry (at the time of sale): As in Table 1 above, Subsidiary A debits Intercompany AR $1,000 and credits Intercompany Sales $1,000. Subsidiary B debits Inventory $1,000 and credits Intercompany AP $1,000, with amounts converted to GBP in Subsidiary B’s ledger.

-

Elimination at Period Close: Upon consolidation, an elimination JE is needed. It will reverse the intercompany sale and purchase. A possible consolidated elimination entry (in parent currency) is:

Entity Account Debit Credit Consolidated Intercompany Sales $1,000 Consolidated Cost of Goods Sold $1,000 This entry (Table 2) debits the intercompany sales account and credits the cost of goods sold, effectively removing the $1,000 revenue and $1,000 expense from the group’s income statement. At the same time, the reciprocal elimination for AR/AP would net out the balance sheet (debit Intercompany AP $1,000, credit Intercompany AR $1,000). If currencies are involved, the CTA-E account takes any difference.

Table 2: Sample Consolidation Elimination Entry for an internal $1,000 wholesale sale [79] [31].

Example 2: Intercompany Loan and Interest

If Parent lends $500,000 to Sub (bank transfer), Subsidiary Parent would record a loan receivable, and Subsidiary Child records a loan payable. On consolidation, a single entry eliminates both:

-

Intercompany transaction entries: Parent Sub posts Dr Intercompany Loan Receivable $500,000 / Cr Cash, Sub posts Dr Cash / Cr Intercompany Loan Payable $500,000.

-

Consolidation elimination: Debit Intercompany Loan Payable $500,000; credit Intercompany Loan Receivable $500,000. This removes the loan from consolidated BS (neither asset nor liability remains in group view).

If Sub pays interest $5,000 to Parent:

- Subsidiary A: Dr Intercompany Receivable $5,000 / Cr Interest Income $5,000.

- Subsidiary B: Dr Interest Expense $5,000 / Cr Intercompany Payable $5,000.

- Consolidation: Dr Interest Income $5,000; Cr Interest Expense $5,000 (zeroing net interest within group).

Example 3: Unrealized Inventory Profit

If Subsidiary U sells an item to Sub V at a 20% markup (above cost), and Sub V has not yet sold it by period end, an unrealized profit exists. Suppose cost to U= $10,000, selling price=$12,000. The intercompany sale and purchase entries each reflect $12,000 and $12,000. On consolidation, beyond eliminating the $12k sale/purchase (dr+$12k Revenue, cr+$12k Expense), we must remove the $2,000 unrealized margin. Typically, this is done by:

- Dr Retained Earnings or COGS $2,000; Cr Inventory $2,000 [33] [31]. This reduces the consolidated Inventory from $12,000 back to the original $10,000 cost, reflecting no group profit until the inventory is finally sold externally.

Note: NetSuite handles inventory transfers similarly. If using Intercompany Transfer Orders (non-arm’s-length), the IC Gain/Loss account set on the item (with elimination checked) would capture the $2,000 profit. During elimination, NetSuite would reverse that gain/loss via the CTA-E mechanism, aligning with the manual accounting above.

Table: Consolidated Eliminations Across Entities

For clarity, the entries above can be combined into a consolidated view. For the sale example, a single elimination journal (consolidated perspective) might look like:

| Subsidiary Context | Account | Debit | Credit |

|---|---|---|---|

| Consolidated (Elimination) | Intercompany Payable | $1,000 | |

| Consolidated (Elimination) | Intercompany Receivable | $1,000 | |

| Consolidated (Elimination) | Intercompany Sales | $1,000 | |

| Consolidated (Elimination) | Cost of Goods Sold | $1,000 |

Table 3: Combined elimination entries at the consolidated level (dr Payable/Exp, cr Receivable/Rev) to net out a $1,000 internal sale [79].

These examples illustrate how consolidation entries reverse the entire effect of internal transactions [80] [9]. NetSuite automates the creation of tables like those above. When you run Eliminate Intercompany Transactions, it generates analogous elimination journals: one set zeroing AR/AP and another set zeroing Sales/COGS (and linked currency gains). The result is that, on consolidated financial statements, these lines do not appear at all, preserving ASC 810’s single‐entity view [81] [2].

NetSuite Field and Report Configuration

In addition to enabling intercompany features, ensure the following NetSuite configurations to support elimination:

-

Account Settings: In Lists → Accounting → Accounts, verify that each intercompany account (AR, AP, revenue, expense) has Eliminate checked [51] [48]. For item-level accounts (e.g. Inventory, COGS, Drop Ship Expense), mark the Eliminate box on the item’s Accounting subtab if used in IC transfers [82].

-

Elimination Checkboxes: NetSuite adds an Eliminate field on journal lines and on account records for intercompany. Educate users (or script rules) to ensure that any manual journal using standard accounts also includes ticking the Eliminate box if it is an intercompany adjustment [48] [60]. Similarly, on an intercompany customer or vendor record (representing another subsidiary), use the “Represents Subsidiary” field [57] [56] to link the entity to the subsidiary it stands for.

-

Preferences and Defaults: Check Setup → Accounting → Preferences. Under the Order Management subtab, ensure that Use Item Cost as Transfer Cost is not enabled for arm’s length transfers (as per the guidelines) [83]. Also see Setup → Company → Enable Features for any prerequisites noted: for example, enabling Multi-Subsidiary Customer before it can auto-generate intercompany customer records [58].

-

Period Close Checklist: The Period Close Checklist should include the “Eliminate Intercompany Transactions” task. This list can guide users each month: first revalue FX, then consolidate, then eliminate, then finally complete consolidated financial reports. Following this sequence ensures ASC 810 compliance in each close cycle [77] [29].

-

Consolidated Financial Statements: When designing financial statements (Reports → Financial → Financial Statements), use the “Consolidated” subsidiaries option as the context to get group totals [36]. NetSuite allows layout by subsidiary or consolidated view. Ensure that any financial report conveys that "All intra-group transactions are eliminated on consolidation" as a footnote, mirroring IFRS/SEC disclosure practices [23].

By combining correct setup with disciplined closing procedures, an organization can automate the mechanics of eliminating internal transactions. However, controls and reviews are still needed. Auditors often check that all intercompany AP/AR account balances reconcile to zero, and that all intercompany expense/revenue accounts have been reversed out in consolidation (as required by ASC 810) [84] [34]. NetSuite’s built-in Elimination reports and reconciliations should be part of the monthly close to verify this.

Data Analysis and Best Practices

Industry data on intercompany processes highlights both the challenges and the payoff of doing this right:

-

Time Savings from Automation: According to a case study, a global manufacturing client cut its consolidation cycle from weeks to hours by using automated intercompany reporting in NetSuite OneWorld [5]. SoftArt Solutions reports that real-time dashboards and standardized elimination sped up previously manual consolidation tasks. Similarly, modern surveys (e.g. BlackLine’s State of Intercompany 2023) emphasize that technology plays a critical role in reducing intercompany complexity [28]. In a world where fast quarterly closes are competitive advantages, NetSuite’s automation can shrink backlog work markedly.

-

Complexity in Large Groups: Shared-services research indicates that large multinationals often spend excessive time on intercompany reconciliations. One SSON research found average companies see intercompany inefficiencies “waste a month a year” of effort [27]. Furthermore, intercompany workflows are often split between accounting, controlling, tax and treasury roles, causing process fragmentation. The data show that nearly half of enterprises are moving more intercompany accounting into centralized shared-services models [85] – often with automated ERP platforms.

-

Error Rates: The IFRS Glossary notes that incomplete eliminations is “one of the most common consolidation errors,” particularly in loans, management fees, and inventory margins [22]. In a NetSuite context, Houseblend reports cases where misconfigured intercompany accounts led to misstated consolidated outputs [6]. A recommended best practice is a monthly intercompany reconciliation report, matching each subsidiary’s AR with the counterparty’s AP [86] [34]. NetSuite offers an Intercompany Reconciliation report, which can be run after entries are posted. Variances should be investigated immediately, as regulatory guidance (and auditors) expect all such differences to be resolved each period [84] [2].

-

Regulatory Emphasis: Reporting standards and regulators stress complete elimination. For example, companies preparing IFRS consolidated statements commonly declare in their disclosures: “All intra-group assets, liabilities, equity, revenue, expenses and cash flows relating to transactions between Group members are eliminated in full on consolidation” [23]. This language (often adopted even by U.S. GAPP reporters in policies) encapsulates ASC 810’s principle. Failure to fully eliminate can trigger audit findings or restatements; a recent example (noted by Deloitte) involved a restatement when a group realized some intercompany sales were erroneously included in consolidated revenue [23] [34].

-

Technology Trends: In recognition of the burden, companies increasingly invest in system automation. The Houseblend report notes a growing focus on “automated consolidation software” and internal controls like auto-balancing features [35]. Gartner and peers have highlighted solutions (beyond NetSuite) such as specialized EPM software that integrate with ERPs to automate eliminations. NetSuite itself has evolved: the recent Automated Intercompany feature replaced manual entries, and NetSuite continuously enhances capabilities (e.g. the CTA-E accounts, paired transaction IDs, etc.) to meet current needs. Analysts foresee even more AI and workflow-driven reconciliation in the future.

Case Studies and Real-World Examples

Misconfiguration Lessons: As noted, one practical example involved a NetSuite implementation where eliminations remained incomplete. Houseblend recounts a case where a multi-entity group had misstated consolidated results because several intercompany expense accounts were not marked “Eliminate” and the NetSuite elimination process was not capturing them [6]. Only after an internal review were the GL accounts corrected and the automated process rerun, at which point the consolidated reports aligned with expectations. This underscores the critical importance of initial system setup: every income/expense account used in intercompany trade must have the elimination flag, and every intercompany entry must use the proper “Intercompany” entity records.

Implementation Benefits: The SoftArt case study (global manufacturer) is instructive on the upside. Before NetSuite OneWorld, the company consolidated multiple regional ledgers manually. SoftArt’s deployment standardized intercompany billing and automatically posted elimination journals. The company reported “real-time global dashboards” and cutting consolidation time dramatically [5]. They also noted that netting out internal inventory via OneWorld inventory features prevented duplicate procurement. This example shows that, with the right implementation partner and planning, NetSuite can deliver on the promise of streamlined multi-subsidiary finance.

Process Improvements: Another example comes from the SuiteRep blog on intercompany drop-shipping [65]. While not directly an elimination “journal” case, it illustrates an intercompany workflow: one subsidiary (sales sub) creates an intercompany PO to buy inventory from another (fulfillment sub). The fulfillment sub ships the goods directly to the external customer, invoices the sales sub, and all related purchase/sales documents interconnect. Throughout this drop-ship chain, NetSuite will naturally generate intercompany AR/AP entries. When consolidated, those internal invoices and costs are eliminated – leaving only the external customer sale and cost. This shows NetSuite’s strength in handling complex multi-entity supply chains and then cleaning them up at consolidation.

Controllership Insight: In a Deloitte survey, controllers emphasized the need for clear intercompany processes. One of the Deloitte poll findings was that companies lacking a single “process owner” for intercompany (spreads work between accounting, tax, etc.) tend to have slower reconciliation and more adjustments [85]. NetSuite’s features encourage ownership: for example, using the intercompany status field (added to orders) and paired transactions fields (showing linked intercompany orders) [87] can provide visibility. Documentation and internal controls should ensure these NetSuite fields are used consistently.

Auditing Perspective: Auditors often ask management for documentation that all intercompany transactions have been eliminated. Some mature organizations implement drill-through capabilities: e.g. clicking on a consolidated number in NetSuite to view the underlying elimination entries (often in the elimination subsidiary). NetSuite OneWorld financial statements support this – allowing auditors to trace, for example, consolidated revenue back to sub-ledger lines, and confirming that net revenue excludes intercompany sales. This visibility, when properly set up, can alleviate audit finding risks.

Implications and Future Directions

Looking ahead, several trends and considerations are noteworthy:

-

Convergence of Standards?: While ASC 810 and IFRS 10 are largely aligned on elimination, differences remain in “control” definitions and disclosure detail. There is ongoing pressure (especially from multinational companies) to simplify these differences. The SEC has studied whether to move toward IFRS-style consolidation guidance, but any changes will take years. In practice, technology has already bridged much of the gap. NetSuite can maintain separate books to handle any subtle accounting divergences (e.g. full goodwill vs partial goodwill) while still automating elimination.

-

Automation and AI: Robotic process automation (RPA) and machine learning are entering the finance function. We anticipate tools that automatically match intercompany invoices and propose eliminations. NetSuite’s own roadmap hints at more AI-enhanced reconciliation and anomaly detection. The Houseblend outlook suggests firms are increasingly adopting cloud ERP consolidation modules (like NetSuite OneWorld) to replace spreadsheets. Blockchain for intercompany might be far off, but better cross-subtitle ledger integration is already here.

-

Regulatory Scrutiny: Regulators will continue to emphasize consolidation accuracy. IAS 27/IFRS 10 already require a statement of basis, and US SEC rules (Reg S-X) demand procedures for elimination. Any new disclosure requirements (for example, reconciling parent vs consolidated statements, as the SEC has considered) would put more focus on robust elimination controls. Companies should be ready to generate data on eliminated amounts and exchange rate impacts (the CTA lines) as audit evidence.

-

Software Feature Enhancements: Vendors like NetSuite are likely to add analytics. For instance, dashboards showing unreconciled intercompany balances, or alerting when an intercompany transaction lacks a corresponding partner entry. NetSuite could also make elimination postings more transparent to users (e.g. tagging journal entries as “Elimination” in reports, automating recurrent entries). Meanwhile, third-party SuiteApps for NetSuite are emerging that specialize in intercompany netting and matching, which could further reduce manual reconciliation.

-

Global Commentary: On the global stage, as IFRS expands adoption (125+ countries fully applying IFRS as of 2025 [88]) and cross-border M&A continues, the importance of software-contemplating consolidation will grow. NetSuite’s cloud multi-entity approach positions it well for global enterprises. However, as user case studies show, success hinges on thorough planning: defining a chart of accounts that supports intercompany flags, training users on the intercompany workflow, and having a consolidation policy to govern eliminations.

Conclusion

Intercompany elimination under ASC 810 is a foundational requirement for accurate group financial reporting. NetSuite OneWorld’s Automated Intercompany Management provides a powerful means to meet that requirement in a scalable way. By configuring intercompany subsidiaries, accounts, and entities correctly, NetSuite can automatically generate the necessary eliminating journal entries, even handling foreign currency translation differences via its CTA-E accounts [73] [30]. This automation dramatically reduces the tedium and error risk of manual eliminations, enabling finance teams to focus on analysis rather than paperwork.

However, the system is only as good as its setup and process discipline. Case studies and surveys highlight that many consolidation errors are self-inflicted – for example, forgetting to check the elimination flag on an account or failing to reconcile AP/AR balances [6] [22]. Ensuring that every intercompany transaction is captured requires both technical controls (system fields, rules) and procedural controls (policies, reconciliations). When done correctly, companies see measurable benefits: faster closes, cleaner audit outcomes, and more reliable financial insights [5] [27].

In practice, companies using NetSuite for multi-entity consolidation should monitor metrics like intercompany reconciliation time and residual mismatches. Surveys suggest even after automation, groups routinely face some reconciling items (often <1% of revenue) [26], so continuous improvement is needed. The trend is positive: modern ERPs, including NetSuite, increasingly embed intercompany logic by default, as regulators and auditors expect. Future developments – further IFRS/GAAP alignment, AI tools, richer ERP capabilities – will continue to reduce the burden of eliminations.

In summary, mastering NetSuite intercompany eliminations means understanding both the accounting rules (ASC 810/IFRS 10) and the software mechanisms. This report has provided a detailed roadmap: from the enabling steps in NetSuite to the actual journal entries and case evidence. With this knowledge and careful implementation, a company can ensure its consolidations truly reflect only external economic activity, fulfilling the “single economic entity” principle and reporting compliance.

Sources: Authoritative accounting standards, NetSuite technical guides, industry white papers, and expert analyses are cited throughout (e.g. NetSuite OneWorld documentation [89] [47], Houseblend and LegalClarity reports [1] [9], IFRS resources [2] [88], case studies [5], and surveys [28] [27]) to substantiate all claims. Each citation is provided inline for verification and further reading.

External Sources (89)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.