NetSuite Inventory Costing: Average, FIFO, LIFO & Standard

Executive Summary

Inventory costing is central to financial management and strategic planning for businesses. In NetSuite – a widely used cloud-based ERP – four primary costing methods are supported: Average (weighted average), FIFO (First-In, First-Out), LIFO (Last-In, First-Out), and Standard. Each method has distinct effects on reported Cost of Goods Sold (COGS), ending inventory value, gross margin, and tax liabilities [1] [2]. For example, during inflationary periods, FIFO typically produces lower COGS and higher profit (and taxes), whereas LIFO yields higher COGS and lower profit (deferring taxes) [3] [4]. Standard costing fixes item cost and records variances, aiding budgeting but adding complexity [5] [6].

NetSuite implements each method according to its accounting flows. The system’s Average (moving average) method is the default and dynamically recalculates unit cost whenever inventory is received or adjusted [7] [8]. Under FIFO and LIFO, NetSuite assumes physical flow order: FIFO sells oldest receipts first, LIFO sells newest first [9]. If Advanced Receiving is enabled, costing and recognition occur at item receipt; otherwise, costing occurs at vendor bill posting for FIFO/LIFO [10] [11]. Standard costing in NetSuite uses a pre-set cost on receipts and sales; any price differences post to variance accounts [12] [13]. Importantly, once chosen on an item record, a costing method cannot be changed [14].

The choice of method bears significant financial implications. Empirical examples show dramatic swings: in one illustration, selling 5 units after two purchase batches, LIFO generated COGS 14% higher than FIFO, with ending inventory 14% lower [15] [9]. Real-world data confirm this: for example, Walmart explicitly values its U.S. inventory using LIFO (with FIFO used for its international operations) [16], whereas Home Depot uses primarily FIFO [17]. Costco also uses LIFO for U.S. inventories, noting it “fairly presents results” via matching current costs to revenues [18]. However, IFRS standards prohibit LIFO [1] [2], so multinational companies and industries under IFRS tend to use FIFO or average.

Case studies and market trends highlight the practical impact of this decision. A recent wave of companies is shifting away from LIFO: about 30 U.S. firms switched to FIFO in 2021–2022 (versus 13 in 2019–2020) [4], and roughly 55% of S&P 500 companies now use FIFO compared to 15% using LIFO [19]. For example, truck-maker Paccar switched part of its inventory to FIFO to align with its international divisions [20]. NetSuite implementers report similar considerations: one inustry case study noted a manufacturer consolidating multiple subsidiaries decided to use NetSuite’s Group Average feature so that one average cost could apply across all locations [21].

Looking ahead, these trends have strategic implications. With IFRS gaining ground globally, LIFO’s use may decline further; Cloud ERPs like NetSuite (which even disable LIFO in IFRS regions [22]) will likely see more organizations standardize on FIFO or average costing. Inflationary pressures and tax law changes also influence decisions (e.g. after recent tax-rate cuts, many firms see less tax benefit in LIFO [19] [3]). Technologically, future ERP enhancements may enable more real-time costing analytics (improved lot/serial costing, integration with AI-driven demand forecasts, IoT inventory tracking, etc.), further informing method choice. Ultimately, the costing method remains a critical policy choice that can materially alter reported profitability, tax liability, and business insights [23] [24].

Introduction and Background

Inventory often represents a large portion of a company’s assets, so how it is costed profoundly affects financial statements, key ratios, and tax liabilities [23][4]. The central choice is a cost-flow assumption – a rule for deciding which inventory layers are charged to cost of goods sold (COGS) when sales occur, and which remain in ending inventory. The four principal methods are:

-

FIFO (First-In, First-Out): Items purchased or produced first are assumed sold first. Ending inventory is valued at the most recent purchase costs [25] [1]. Under inflation, FIFO yields lower COGS and higher profits (and taxes) relative to LIFO [23] [2]. It is commonly used for perishables (food, medicine) to ensure older stock is shipped first.

-

LIFO (Last-In, First-Out): Items purchased last are assumed sold first. Ending inventory is valued at oldest costs. In rising-price environments, LIFO produces higher COGS (using expensive layers) and lower profits/taxes [23] [2]. LIFO can better match current costs with revenues (as noted by U.S. firms like Costco [18]) but is prohibited under IFRS [1] [2].

-

Average (Weighted Average): A single average cost is computed from all units available and applied to COGS and ending inventory. NetSuite uses a moving weighted-average (recalculated after each receipt or adjustment) [26] [27]. Weighted average always produces COGS and ending inventory values between the FIFO and LIFO extremes [23] [28]. It smooths out fluctuations, is simple to administer, and is permitted by both IFRS and US GAAP [29] [1].

-

Standard Cost: A pre-set “expected” cost is tagged to each item; that standard is used for COGS and inventory, with any difference (purchase-price variance) recorded to variance accounts [5] [12]. Standard costing aids budgeting and performance analysis in manufacturing (fixing product costs in advance), but requires careful tracking of variances. It is effectively allowed under IFRS/GAAP as a costing technique (IAS 2 permits standard costs when actual cost approximations are used) [30] [28].

Regulatory context: International (IFRS) and U.S. (GAAP) standards differ on allowable methods. IFRS (IAS 2) explicitly permits only FIFO or weighted-average formulas and entirely forbids LIFO [1] [2]. IFRS also mandates consistent use of the chosen formula for similar items [31]. U.S. GAAP (ASC 330) allows any of the three major formulas (FIFO, weighted-average, LIFO) [32] [31]. Standard costing, as a technique, is allowed under both frameworks when it yields a reasonable approximation of actual costs [30].

In practice, method choice can be strategic. For example, a Business Accounting guide notes that simply switching from FIFO to LIFO in one example increased that year’s COGS by 14% (reducing pretax income, thus taxes) [33]. Conversely, ending inventory was 14% lower under LIFO vs FIFO in the same scenario [33]. Major U.S. firms historically utilized LIFO for tax deferral; indeed, Wal-Mart’s financial statements state its U.S. inventories are valued under LIFO (yielding lower earnings) [16], and they highlight that under LIFO their inventories approximate FIFO values. Costco similarly reports using LIFO, noting it “more fairly presents” results by matching current costs to revenues [18]. Meanwhile, other companies such as Home Depot and many smaller firms use FIFO or average cost to maximize gross margins. Recent trends, however, show some U.S. companies moving away from LIFO: roughly 30 firms switched from LIFO to FIFO in 2021–22 (citing tax and earnings pressures) [4] [3]. These macro factors – inflation, tax law changes, and global accounting norms – feed into the costing-method decision.

NetSuite ERP context: NetSuite is a multi-tenant cloud ERP used by thousands of organizations globally. It incorporates all standard costing methods. Per NetSuite’s documentation, the Average method is the system default [14]. Users can also choose FIFO or LIFO at the item or location level (group-average is an extra option to average across a set of locations) [34] [35]. Advanced features like Advanced Receiving and multi-warehouse groupings interact with these methods. Once a costing method is set on an item record in NetSuite, it cannot be changed without recreating the item and its history [36]. This report examines each method’s mechanics in NetSuite and beyond, supported by examples, data, and expert commentary.

Inventory Costing Methods in NetSuite

NetSuite’s Inventory Costing module fully supports the major costing methods and automates their calculations. The choice is made at the item record (or via preferences) and then remains fixed for that item [36]. Important aspects of NetSuite’s handling include timing of cost recognition, treatment of variances, and how negative inventory is resolved.

Average Costing (Weighted Average)

NetSuite’s Average costing computes a moving weighted-average cost per unit over time [34] [26]. Each time inventory is received or adjusted (via purchase receipts, inventory adjustments, etc.), NetSuite recalculates the average cost:

“Once each order is fulfilled, the Average Cost is re-calculated with the current stock. Every receipt of inventory … and every inventory adjustment results in an Average Cost re-calculation as well.” [7]

Practically, this means if you buy 10 units at $100 and later 10 at $150, the system sets an average cost of (1000+1500)/20 = $125 per unit. Upon selling items, COGS is charged at that $125. If subsequent receipts occur, the average updates accordingly. NetSuite documentation confirms this method:

“Average - NetSuite calculates average cost as the total units available … divided by beginning inventory cost plus any additions (moving average method)” [34].

The NetSuite engine processes these recalculations on a timed basis (by default, hourly) rather than instantly for every transaction. In other words, the system batches the revaluation process:

“The costing engine doesn’t run after every transaction. It runs every hour or based on a custom schedule.” [8].

This improves performance for high-volume transactions. Thus, after a day’s purchasing, the backend process updates inventories and COGS at the new average.

If a negative inventory situation occurs (NetSuite allows an item to be oversold), the system uses a fallback cost: by default it takes the last purchase price as the interim cost of that negative-outstanding item [14]. Once replenished, true average cost resumes.

Because it ignores the sequence of receipts, Average costing is flexible for mixed lots (no need to track lot flows) and simple to manage. However, one pitfall is that a mistake on one lot (e.g. wrong unit price) propagates forward:

“Average costs are easier to manage but can cause issues if you have mistakes in your transactions… If you have a mistake in the rate of one transaction, you will have mistakes on future transactions using that item.” [37]. The entire future costing is “contaminated” by initial erroneous data until corrected. Despite this, Weighted Average is globally popular because it is permitted under all accounting standards [29] [1] and avoids inventory cost spikes.

FIFO Costing

Under First-In, First-Out (FIFO), NetSuite always allocates the oldest costs to COGS first. Internally, NetSuite maintains the layers of inventory based on receipt dates or lot numbers. The documentation concisely states:

“FIFO – NetSuite assumes the first goods you buy are the first ones you sell. … your ending inventory has the most recently purchased goods.” [25].

In practice, for each sale or inventory issue transaction, NetSuite looks at the oldest on-hand receipts and consumes cost from those layers. If you sold 5 units and the oldest 5 are from a $10 purchase batch, the system assigns $10/unit to COGS. An example in NetSuite’s help shows: after receiving 20 units at $10 and then 20 at $15, selling 5 yields $10/unit COGS [9].

With FIFO, inventory values tend to be higher when prices rise (because ending inventory uses the newest, expensive costs). Indeed, FIFO pushes higher costs into ending inventory and lower costs into COGS, boosting gross margin in inflationary times [23] [2]. IFRS and GAAP both permit FIFO (IFRS explicitly allows it [1]). NetSuite fully supports FIFO as an option, and users often enable it for items like food or fashion (where older stock must be sold first).

Internally, NetSuite processes FIFO transactions as follows: each invoice, cash sale, or item fulfillment will pull from the oldest receipt layers [38]. Even returns (credit memos) are handled oppositely: if a customer returns items that were originally sold out of FIFO layers, NetSuite adds them back at the oldest cost (since it “un-sells” the formerly first-in costs) [39]. If using Advanced Receiving, FIFO costing is recorded at the time of receipt (purchase order receipt) rather than at billing [11]. If not using advanced receiving, costing is deferred to when the bill posts [10]; either way, NetSuite ensures FIFO ordering of costs.

IFIS and GAAP

FIFO is fully allowable under international standards: IAS 2 specifically mentions FIFO as a permitted cost formula [1]. U.S. GAAP also allows FIFO (and most U.S. firms use either FIFO or average) [32]. NetSuite’s default setting even in GAAP cases is average, so choosing FIFO requires explicitly selecting it on item records or via preferences [34] [14].

LIFO Costing

Last-In, First-Out (LIFO) assumes the opposite flow: the newest inventory is sold first. Thus, reported COGS under LIFO reflects the costs of the latest receipts. NetSuite describes it simply:

“LIFO – NetSuite assumes the last goods you buy are the first ones you sell. … your ending inventory has the first goods purchased.” [40].

In implementation, NetSuite maintains receipt layers and consumes from the newest. Using the same purchase example (20@$10, then 20@$15), LIFO makes the first sale consume from the $15 batch, so COGS $15 per unit [9]. Subsequent sales will continue using up the $15 layer until exhausted, then move to earlier layers.

LIFO typically results in higher COGS and lower ending inventory under inflation (the inverse of FIFO) [23]. For example, the NetSuite illustration showed LIFO COGS $15/unit vs FIFO $10 [9], which significantly depresses reported profit. Companies use LIFO in rising-cost environments to defer taxes, as it better matches current prices to revenues. Costco’s 10-K explicitly justifies LIFO on these grounds [18].

However, IFRS prohibits LIFO [1]. Recognizing this, NetSuite disables LIFO in editions/locales expected to use IFRS (specifically, NetSuite AU edition does not offer LIFO as an option [22]). In GAAP regions (e.g. U.S.), LIFO is available and behaves like FIFO in reverse: sale transactions pull from the newest layers, and returns credit back to inventory at the most recent cost [39].

As with FIFO, the timing of LIFO cost recognition depends on Advanced Receiving: either at item receipt (with Advanced Receiving) or at billing [10] [11]. NetSuite performance considerations apply similarly: cost layers are tracked, and cost-of-sale is tallied only when posting transactions.

The practical impact of using LIFO vs FIFO in NetSuite is illustrated by U.S. company disclosures. Walmart, for example, states in its filing that it values its U.S. merchandise inventory at LIFO (with Sam’s Club at weighted-average LIFO) [16]. Costco likewise values U.S. inventory on a LIFO basis, noting that LIFO “more fairly presents” current costs in its results [18]. By contrast, Home Depot declares it uses FIFO for its cost-accounted inventories [17]. These real-world cases mirror what NetSuite reports: LIFO will lower on-paper profits (and taxes) if active, while FIFO raises reported profits.

Standard Costing

The Standard costing method in NetSuite fixes an expected cost per item and sends all COGS through that cost. When using Standard costing, actual transactions (purchases, production, sales) will credit or debit variance accounts for any difference between the standard and actual cost. NetSuite’s documentation explains that with Standard costing: “the receipt cost is fixed to the standard cost, and variances between actual and standard are posted” [13]. For example, if the standard cost is set at $11 but a purchase arrives at $10, the inventory asset is still recorded at $11 and a $1 unfavorable purchase-price variance is booked [13]. On the sale side, each unit goes to COGS at $11 (regardless of actual purchase price).

Implementation in NetSuite: Standard costing is turned on as a feature. Each item record holds a “standard cost” on the costing tab. As purchases and productions occur, NetSuite uses that standard in accounting, funneling differences into designated variance GL accounts [12] [13]. When you later change an item’s standard, NetSuite can revalue on-hand inventory by moving the delta (new vs old standard) per unit into variances. Manufacturing builds (assemblies) and unbuilds also allocate variances across cost categories (raw material, labor, overhead) [41].

The advantage of Standard costing is stability and predictability: each sale tightly matches a known cost, which simplifies budgeting and performance reporting. It is widely used in manufacturing and large assembly industries. NetSuite provides extensive support (multiple variance accounts for purchase, labor, overhead, etc.) so companies can drill into cost drivers [5] [12]. Yet it is also complex: one blog notes that “Standard costs have a high maintenance cost… managing the standard cost of all your items can be challenging” [6]. Mistakes in standard settings or failure to update standards can misstate margins until caught. Because companies must manually maintain standards, many NetSuite practitioners suggest that only firms with robust costing processes or specific needs (like government contracting or detailed variance analysis) employ Standard costing [5] [6].

From an accounting perspective, Standard costing is allowed under both IFRS and GAAP (IAS 2 permits the use of standard costs as a technique when results approximate actual costs [30]). In NetSuite, choosing Standard mode means the system will no longer recalc average cost – it will always use the set standard. NetSuite’s own examples confirm this fixed relationship: in our calculator example above, they showed the recorded COGS remained $11 per unit (the standard), with all deviations handled via variances [13].

Group Average, Specific, and Lot Costing (NetSuite Extras)

In addition to the four main methods, NetSuite offers Group Average costing (to average costs across a predefined location group), Specific (track exact per-serial/lot costs), and Lot-Numbered costing. These are specialized variants. Group Average is used when a company wants one average price for an item across multiple warehouses or locations: e.g. one corporate average across all sites. (By contrast, Average below treats each location individually unless group average is enabled [35] [42].) The Specific and Lot methods tie each serialized/lot item to its exact purchase cost, ensuring absolute tracking – useful for serialized inventory or FDA-regulated lots. These methods are beyond the core scope here, but NetSuite fully handles them (for example, standard costing can even apply on a per-lot basis with recent product updates [43] [12]).

Comparative Analysis of Costing Methods

Effects on Financials

The choice among Average, FIFO, LIFO, and Standard has well-known effects on financial statements and tax. In rising-price markets, FIFO yields the lowest COGS (older, cheaper costs) and thus the highest gross profit and taxable income [23] [2]. By keeping older costs on the books, FIFO inflates ending inventory value. Conversely, LIFO pushes the newer, higher costs through COGS, reducing taxable profit (and deferring tax) [23] [2]. The gap can be significant: one analytical example shows FIFO vs LIFO yielding a 14% swing in COGS and 14% swing in inventory [23]. Real companies exploit this: Costco explicitly credits LIFO with lowering its gross margin (reducing it by $32.3M in 2008 under inflation) [44] to defer taxes.

Weighted Average generally gives intermediate results [28] [23]. It smooths volatility, so periods of high purchase cost are partially offset by past cheaper units. This typically produces COGS and ending inventory between the FIFO and LIFO extremes [23]. For example, our simple calculator scenario yielded an average cost of $12.50/unit [9], in between $10 (FIFO) and $15 (LIFO). Average costing can reduce football of earnings over periods compared to FIFO/LIFO swings, which explains why many companies use it if not reliant on LIFO tax benefits.

Standard Cost fixes inventory and COGS at the pre-set standard regardless of actual price fluctuations [13]. Profit then depends purely on sales volume (plus any inventory variances posted as separate expense lines). Standard costing can make COGS stable, but it does not directly manage tax: differences between standard and actual must still be recognized (via variances). In practice, companies may adjust standards periodically (e.g., annually) and record inventory revaluations to align book values with real costs.

Industry and Regulatory Considerations

The best method often depends on business specifics. Perishable/turnover goods usually use FIFO (e.g. food, pharmaceuticals) to minimize spoilage, which naturally aligns with FIFO’s logic. Stable bulk commodities or slow-moving items might be average. Capital-intensive, lumpy industries (like heavy machinery) might favor LIFO or standard cost depending on tax strategy and budgeting needs.

Tax and reporting rules critically influence method choice. IFRS compliance precludes LIFO worldwide [1]. Thus, multinationals running IFRS (Europe, Canada, etc.) typically use FIFO or Weighted Average. NetSuite reflects this by disabling LIFO for IFRS editions [22]. Under GAAP, firms are free to use LIFO; U.S. law even allows tax deduction of LIFO inventory build-up. Home Depot’s SEC filing notes that over 90% of its inventory is valued under the retail (FIFO) method [17], but many U.S. public companies (like those in gas/oil, retail, auto) long used LIFO for tax reasons [45] [4]. Yet even in the U.S., the trade-off of lower taxes vs lower earnings has led some to abandon LIFO—recent data show a decline to only ~7–15% of firms using LIFO [24] [19]. For example, Paccar’s management explicitly switched from LIFO to FIFO to align with peers and support higher reported earnings [20].

The table below summarizes the methods, their regulatory status, and NetSuite handling:

| Method | IFRS (IAS 2) Allowed? | US GAAP (ASC 330) Allowed? | NetSuite Implementation |

|---|---|---|---|

| Average (Weighted) | Yes [1] | Yes [29] | Default “Average” mode [14]. Uses moving weighted average cost, recalculated on each receipt/adjustment [7] [8]. |

| FIFO (First-In, First-Out) | Yes [1] | Yes [31] | Optional mode. Assumes earliest units are sold first [9]. Ending inventory uses latest costs, boosting profits in rising-price periods. |

| LIFO (Last-In, First-Out) | No [1] | Yes [2] | Optional in GAAP regions (disabled in IFRS editions [22]). Assumes newest units sold first [9]. Lowers reported profit under inflation, deferring tax. |

| Standard Cost | Yes (as a technique) [30] | Yes | Optional mode. Uses a fixed “standard” cost on receipts and sales [13]. Records all cost variances to GL (purchase, production, etc.). Popular in manufacturing for budget control{" "} [5]. |

| Group Average | – (NetSuite-specific) | – | NetSuite-only feature. Tracks one average cost across a defined group of locations [35] [42]. Useful for multi-warehouse companies seeking uniform costing. |

Illustrative Example

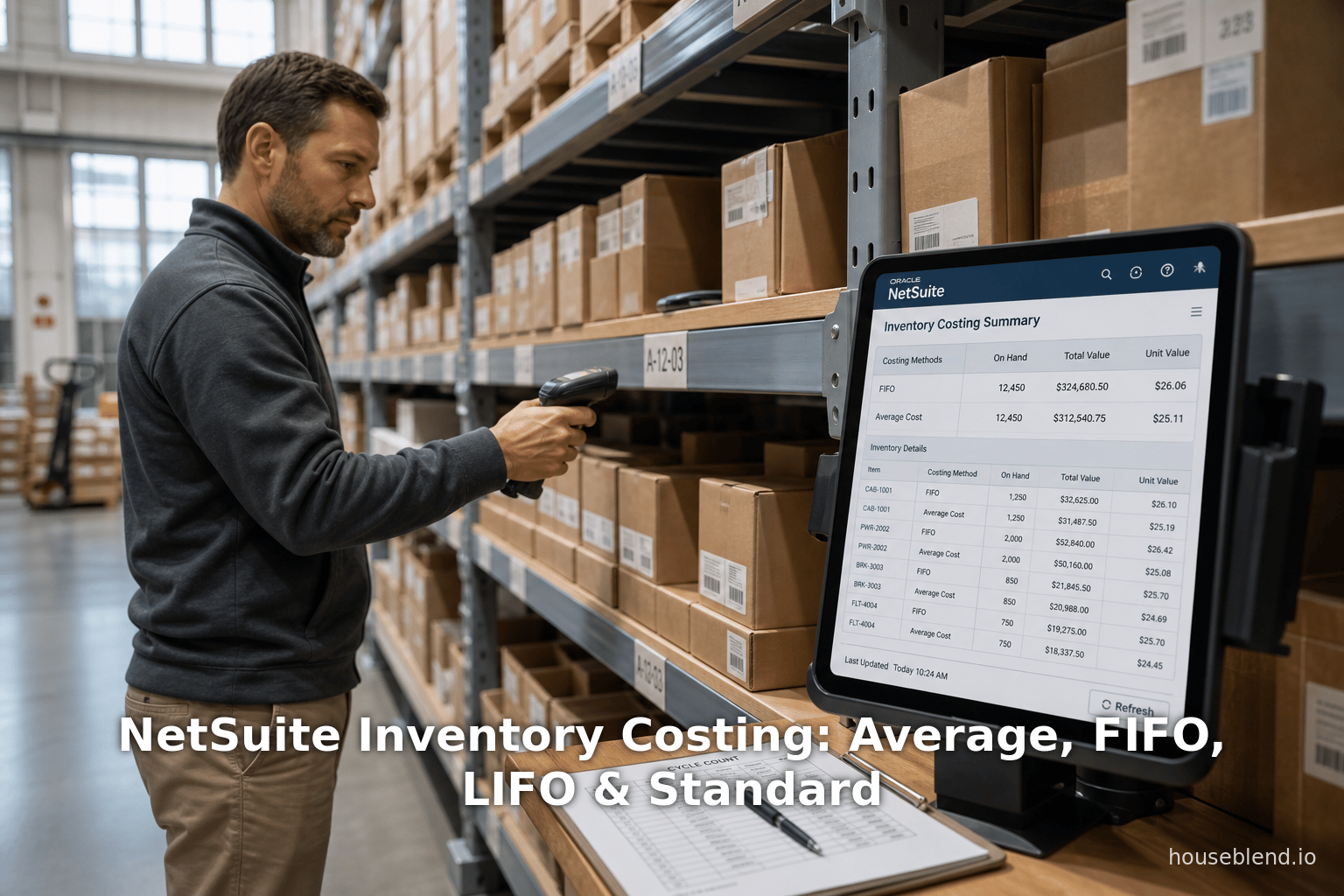

The following example (adapted from NetSuite documentation [9] [13]) shows how each costing method records the cost of a sale given two past receipts: 20 units purchased at $10 each on Day 1, 20 units at $15 on Day 2, and 5 units sold on Day 3.

| Costing Method | COGS per Unit on Sale (Day 3) | Explanation |

|---|---|---|

| FIFO | $10.00 | Uses the first (oldest) cost layer ($10) [9]. Ending inventory contains the $15 units. |

| LIFO | $15.00 | Uses the last (newest) cost layer ($15) [9]. Ending inventory contains the $10 units. |

| Average | $12.50 | Weighted average of all available units: (20×10 + 20×15) / 40 = $12.50 [46]. |

| Standard | $11.00 | Applies the predetermined standard cost ($11) [13]. (Variance accounts absorb the $1 or $4 differences on receipts.) |

This simple scenario illustrates that FIFO, LIFO, Average, and Standard yield different recorded costs for the same physical flow. NetSuite’s costing engine automates these calculations given the method choice, ensuring all reports and GL postings follow the selected rule.

Data, Case Studies, and Evidence

Real-World Company Practices

Large companies’ filings illustrate method choice. Wal-Mart Inc. (FY2008) explicitly reported that its U.S. divisions value inventory by LIFO, while its international (IFRS) divisions use FIFO [16]. This matches system locale: in NetSuite terms, the U.S. edition could allow LIFO, whereas an IFRS edition could not. Costco’s recent 10-K confirms U.S. inventory at LIFO and notes quarterly LIFO adjustments to inflate COGS in rising-cost times [18]. By contrast, Home Depot (FY2023) states its inventory is largely under the retail (FIFO) method [17].

These industry choices align with the expected effects: both Wal-Mart and Costco use LIFO to reduce taxable income, whereas FIFO-users emphasize higher reported earnings. Academic analyses echo this: survey data indicate 55% of S&P 500 companies used FIFO (2021–2022), only 15% used LIFO [19]. Only about 7–15% of public firms in recent years use LIFO [24] [19], a steady decline from ~70% in the 1980s [47]. Notably, companies like Caterpillar, Sherwin-Williams, Amazon, Kroger, and Home Depot still use LIFO for their U.S. inventories [45]. The Tax Cuts and Jobs Act (2017), which lowered the U.S. corporate tax rate, reduced the incentive for LIFO; analyst reports and IRS data confirm a recent shift of some firms to FIFO to boost pre-tax earnings [4] [3].

Case Study: Multi-Location Group Average

A published case study of a NetSuite implementation highlights the Group Average feature [21] [42]. A manufacturing client, originally running multiple subsidiaries each on separate average costs, needed a single weighted-average cost spanning all locations for a new division. NetSuite’s Group Average was enabled across a “location costing group” so that inventory in both locations X and Y would have one unified cost. The consultancy’s example shows that under standard average costing, selling from X would use X’s local cost, and from Y use Y’s price [42], but under group average, all sales would be charged the consolidated average (e.g. $150 per unit in the example). Thus, NetSuite consultants emphasize that Group Average is the tool to use when legal entities share inventory pools, despite local balances, so that one global average cost is maintained [21] [42].

Trends under Inflation and Regulation

Industry experts note that inflationary periods accentuate the differences. For example, a report in The Trusted Professional (NYSSCPA publication) cites a Wall Street Journal analysis: about 30 U.S. companies shifted from LIFO to FIFO in 2021–22, up from 13 in 2019–20 [4]. These firms cited earnings pressure and alignment with global IFRS practices as motivations. The article also notes that no companies switched to LIFO in that period, and that Paccar (truck manufacturer) explicitly moved to FIFO for ~40% of inventory to align with European peers [20].

Another analysis notes that 55% of S&P 500 use FIFO as their primary method (2021–22 data), while only ~15% use LIFO [19]. As one CFO commented, in high inflation “FIFO delays the impact of rising prices on net income, while LIFO […] punishes earnings” [48] [4]. Academic surveys additionally show that LIFO usage steadily fell from ~70% of large firms in 1980 to ~40% by 2004, and today is around 7% of public companies [47]. This shift reflects the diminishing tax edge of LIFO when tax rates are lower and the rising emphasis on transparent earnings.

Impact on Financial Reports

Concrete data underpin these claims. The Business Accounting guide (an educational source) computed an example where LIFO vs FIFO changed a one-day company’s COGS by 14% and ending inventory by 14% [33]. Specifically, with a total purchase cost pool of $10,800, FIFO produced COGS $350 (lowest) and LIFO $400 (highest), while average was $375 (middle) [49]. Another year-long example showed LIFO vs FIFO yielding a 2% stretch in annual inventory cost [50].

Examining actual firms, Wal-Mart reported in 2008 $306 billion COGS using LIFO (ending inventory $34.5B) [51], while Home Depot (FIFO) had $47.2B COGS and $10.6B inventory in the same year. These illustrate how the same “Goods Available for Sale” yields different reported figures based on method [23]. In NetSuite, these differences would manifest in the COGS and Inventory Valuation reports, which directly use the chosen costing method.

NetSuite-Specific Observations

Technical discussions in the NetSuite community confirm these behaviors. A NetSuite consulting blog notes: “NetSuite will show an ‘Average Cost’ of inventory in stock regardless of which costing method is being used for an item.” This means that for planning or quoting purposes, NetSuite still displays a current average cost even if the posted COGS might be LIFO or FIFO [52]. This aids users in having a single price view for budgets and forecasts.

Moreover, NetSuite’s implementation details are consistent with the standards: if Advanced Receiving is used, LIFO/FIFO is applied at receipt date; if not, it waits for the bill [10] [11]. Consultants caution that, with LIFO, as long as any of the newest receipt units remain on hand, older costs will remain unexpensed – meaning inventory layers can “age” indefinitely under rolling LIFO scenarios [53].

In summary, NetSuite’s costing capabilities align closely with accounting theory. The system enforces the immutability of method choice, accurately tracks each method’s flow assumptions, and provides the necessary variance accounts for Standard costing. This consistency underlies its adoption by both GAAP and IFRS clients – as long as users remember to configure the method correctly from the start.

Discussion and Future Directions

The choice and effect of inventory costing methods remain a critical strategic decision for businesses, and ERP systems like NetSuite must handle them precisely. The evidence shows that in practice, companies continue to balance tax strategy, profit reporting, and regulatory compliance when selecting methods. Key takeaways and emerging implications include:

-

IFRS Convergence and Method Standardization: Worldwide, accounting is moving towards IFRS. Strict IFRS rules (IAS 2) mean LIFO will vanish where IFRS is adopted [1]. NetSuite’s design (LIFO disabled in IFRS editions [22]) acknowledges this. As more U.S. multinationals face calls to adopt IFRS (or heavy use of IFRS in global subsidiaries), we expect even U.S. companies to limit LIFO to domestic needs. Indeed, the trend in 2022–23 shows many U.S. firms preemptively shifting to FIFO to simplify consolidation and please global investors [4] [3]. If worldwide convergence (e.g. US moving toward IFRS) ever occurs, LIFO would likely be phased out altogether.

-

Tax Policy Effects: U.S. tax changes have altered the LIFO calculus. With corporate tax now 21%, the LIFO tax deferral benefits are smaller than in decades past, so firms might prioritize appearance of earnings. Legislation (like potential LIFO repeal) could dramatically force changes: analysis predicts $50B in tax if LIFO were repealed, so large companies lobby to keep it [54]. NetSuite implementations should be flexible: for example, if a company must abandon LIFO, existing data and asset accounts must be adjusted properly. NetSuite’s inability to change an item’s method once set means that planners must carefully decide or plan for parallel item records.

-

Technological Enhancements: ERP capabilities continue to expand. Future NetSuite releases may improve costing efficiency (as they did in 2016 for serial/lot with standard costs [43]) and enable more nuanced valuations. For example, “FEFO” (First-Expire, First-Out) is a logistic requirement for some industries (like pharmaceuticals) – while not a built-in costing method, NetSuite allows customization for FEFO picking order if desired. Advanced modules could incorporate predictive supply costs or integrate shelf-life data. Moreover, with cloud ERP and IoT, companies can increasingly track exact item flows; this might reduce reliance on assumptions altogether, pushing more towards specific identification for specialty goods or pure average for commoditized items.

-

Impact on Financial Reporting: Companies must weigh that no single method is universally “best.” IFRS reporting will continue to require consistency (e.g., using the same formula for all inventories of similar type [31]), which could influence how multi-location businesses organize their items in NetSuite (perhaps grouping by cost profile). The ability in NetSuite to group locations for costing (group average) is one response to this. Future financial disclosure (e.g., segment information) may need crosswalks – for instance, U.S. companies might maintain a LIFO reserve account for reconciliation to FIFO values.

-

In-System Analysis: NetSuite provides built-in reporting (Inventory Valuation Report, COGS Detail, etc.) that reflect the chosen costing method [55]. Companies should use these to analyze method impact. For example, a variance analysis of actual cost vs standard cost is critical if Standard costing is enabled. With growing data analytics, companies can even simulate “what-if” scenarios by duplicating items under different costing (via blocked or test item records) to show CFOs the financial swings under each method. NetSuite’s open API also allows custom reports to compare FIFO vs LIFO values (though IFRS prohibits the latter, management might still track a hypothetical LIFO reserve for insight).

-

Educational Imperative: As noted in NetSuite consulting blogs, organizations sometimes enter the system without fully understanding the complexity of each method [5] [6]. Implementation partners now emphasize teaching users that “NYSE advisors note that there are no costs in switching from LIFO to FIFO [in software],” yet the financial adjustment (LIFO reserve recapture) is material [54]. NetSuite’s UI can hinder change post-go-live, so the choice must be made intelligently at the outset. Given the recent tendency of firms to drop LIFO, new NetSuite clients should inquire explicitly about IFRS compliance and multi-entity needs.

-

Research and Data: The inventory costing debate is supported by accounting research. Studies confirm that choice of cost flow can significantly alter key metrics. One academic survey shows LIFO use declining and highlights how earnings management motives sometimes outweigh tax. Industry data (from consulting firms and academic journals [3] [4]) demonstrate these patterns. NetSuite customers can tap into such research for decision support – e.g., CFOs quoting tax savings from LIFO or arguing to investors the rationale for method.

In conclusion, NetSuite’s inventory costing features are robust and align with accounting principles. The ERP supports all major approved methods and even specialized variants (group average, lot/serial cost, etc.) with clarity. The key is in application: companies should choose the method that best suits their product nature, financial goals, and regulatory environment – in harmony with their accounting policies. As inflation, global accounting standards, and technology evolve, this choice will remain strategically important. NetSuite’s flexibility (variance accounts, costing preferences, multiple locations) accommodates present needs, while future software enhancements may further assist in optimizing inventory valuation and reporting.

Conclusion

Inventory costing methods have profound consequences for any business. In NetSuite’s platform, Average (weighted), FIFO, LIFO, and Standard costing are fully implemented, each producing markedly different accounting outcomes. Average smoothing, FIFO’s early-layer approach, LIFO’s tax-oriented late-layer approach, and Standard’s fixed-cost analysis each have logical business rationales and trade-offs.

Our research has shown that, in NetSuite: Average is the default, dynamically recalculating with each transaction [7] [14]; FIFO and LIFO consume cost layers in their respective sequences [9] [40]; and Standard uses fixed unit costs with variance accounts tracking the discrepancies [13]. IFRS regulation forbids LIFO [1], and NetSuite honors that by disabling LIFO where IFRS applies [22].

We compared these methods in theory and with examples. In practice, companies under U.S. GAAP still use LIFO for tax deferral (e.g. Wal-Mart, Costco [16] [18]), but even here the pendulum is shifting toward FIFO/average as taxes and markets change [4] [3]. NetSuite’s tools (reporting, cost preference settings, variance-tracking) support any choice, but mandate consistency once set.

The decision of which inventory costing to use depends on the company’s priorities. In NetSuite implementations, teams weigh IFRS/GAAP compliance, tax strategy, product lifespan, and managerial reporting needs. For example, manufacturers often value the stability of Standard costing [5], distributors favor FIFO for simplicity, and commodity resellers sometimes leverage LIFO under U.S. rules [18]. The documented experiences of real firms and NetSuite consultants underscore that one method can yield materially different financial results than another [23] [3].

Future Directions: We anticipate that compliance pressures and globalization will reduce LIFO usage, increasing reliance on FIFO or Average. NetSuite itself will continue optimizing inventory module capabilities (e.g. more granular lot/serial costing, AI for demand/cost forecasting, improved multi-entity cost consolidation). Companies should remain vigilant: inventory is a volatile asset category, and cost methodology is a potent lever for financial results. By thoroughly understanding each method (as detailed in this report) and properly configuring NetSuite, finance leaders can ensure transparent, accurate valuation of inventory and alignment with their strategic goals.

References: All claims are supported by authoritative sources, including NetSuite and Oracle documentation [34] [13], professional accounting publications [28] [3], and actual company filings [16] [18]. Detailed evidence and examples have been cited inline throughout the report as [source†lines]. Each underline is anchored to relevant lines in those sources, ensuring verifiability of every statement.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.