Houseblend Article

NetSuite Multi-Book: IFRS to Chinese GAAP (CAS) Mapping

Inside this article

Executive Summary

In an era of globalized business, multinational enterprises increasingly face the need to report under multiple accounting frameworks. For example, companies with Chinese subsidiaries often must report under International Financial Reporting Standards (IFRS) for investors and group consolidation, while simultaneously complying with Chinese Accounting Standards (CAS) for local statutory filings. This duality has historically forced labor‐intensive spreadsheets and reconciliations, contributing to a lack of confidence in financial data. A recent BlackLine survey found nearly 40% of CFOs do not fully trust their financial data, citing fragmented systems and manual processes as key causes [1] [2].

NetSuite’s OneWorld Multi-Book Accounting addresses this problem by enabling a single transaction to post to multiple parallel ledgers in real time. In practice, this means a Chinese subsidiary can maintain one set of ledgers under IFRS and another under CAS simultaneously. Global studies show IFRS is mandated or used in over 110 countries [3], and Chinese standards have been officially converged with IFRS since the 2006 ASBE reforms [4]. Yet material differences remain – for example, Chinese GAAP historically carried assets at cost and deferred many IFRS changes (e.g. lease treatment, revenue recognition (Source: prc.today) (Source: prc.today). NetSuite Multi-Book automates the parallel accounting entries and reporting needed to reconcile these differences.

This report provides a comprehensive analysis of using NetSuite Multi-Book for IFRS vs CAS reporting. We begin with the regulatory and accounting context: the scope of IFRS and Chinese GAAP, and the key differences between them (summarized in Table 1). We then explain the NetSuite OneWorld platform and Multi-Book architecture, including Full Multi-Book versus Adjustment-Only modes. Detailed examples show how NetSuite handles specific IFRS–CAS divergences (revenue, leases, financial instruments, tax adjustments, etc.) by using Chart of Accounts Mapping, book-specific schedules, and currency management. We also cover practical aspects such as statutory report generation in China (vouchers, Chinese‐language financials using NetSuite’s localization features) and consolidation (per‐book eliminations). Case scenarios – including a hypothetical Chinese subsidiary and an illustrative “OmniRetail” global case – demonstrate real-world implementation. Throughout, we draw on authoritative sources (IFRS Foundation, MOF, industry whitepapers) and survey data to quantify impacts. The report concludes with implications for finance teams and future trends (e.g. upcoming IFRS/CAS updates and cloud ESG standards). In sum, NetSuite Multi-Book enables a “single source of truth” running both IFRS and Chinese GAAP, greatly reducing manual reconciliation and increasing auditability [1] [5].

Background and Context

Global IFRS Adoption and Chinese GAAP (CAS)

IFRS as a global standard. The IFRS framework is now the dominant standard for publicly-listed companies worldwide. The IFRS Foundation notes that “more than 110 countries mandate IFRS for public-company reporting” [3]. For consolidated reporting, all EU companies must use EU-endorsed IFRS [3]. In China, the Ministry of Finance (MOF) has systematically converged China’s own standards (ASBEs/CAS) with IFRS since the mid-2000s. The 2006 ASBEs were “substantially converged” with IFRS [4], and in 2015 China agreed to aim for full equivalence. In practice, many large Chinese companies (especially those dual-listed in Hong Kong or overseas) prepare IFRS-compliant financials. The IFRS Foundation confirms that China’s national standards are “substantially converged” with IFRS and that Chinese issuers representing over 30% of China’s market cap use IFRS for at least some filings [6] [4].

Chinese GAAP for statutory purposes. Despite convergence, China maintains a separate set of Accounting Standards (CAS) for domestic statutory reporting (the “bilancio” for tax and audit). These CAS rules are issued by China’s MOF and incorporate Chinese economic policies. For example, certain land-use rights are treated as intangible assets under CAS, whereas IFRS16 would classify a lease of land as a right-of-use (ROU) asset (Source: prc.today). Historically, China’s standards tended to be more conservative (favoring historical cost and prudence) than IFRS, though recent CAS revisions (e.g. CAS 21 on Leases, CAS 14 on Revenue) align closely with IFRS (Source: prc.today) (Source: prc.today). Nonetheless, differences persist – for example, CAS 22 (Financial Instruments) remains simpler than IFRS 9, and certain disclosures and measurement options differ (Source: prc.today). These differences can materially affect balance sheets and income (see Table 1).

| Ledger | IFRS (International Standards) | Chinese GAAP (CAS) | Principal Sources/Notes |

|---|---|---|---|

| Scope & Application | Mandated for consolidated reporting by all global SEC/EU-listed entities [3]; any company can elect IFRS for internal or parent reporting. IFRS defines comprehensive fair-value and accrual rules. | Required for domestic statutory and tax reporting of mainland companies. CAS is largely aligned with IFRS (2006–2014 convergence) [4], but mandated calendar/fiscal periods and formats may differ. | IFRS Foundation (global adoption) [3]; China MOF (ASBE roadmaps) [4] |

| Revenue Recognition | IFRS 15 (5-step model) requires identifying performance obligations and allocating price to them. Highly detailed rules (fair value allocation, onerous contract tests, etc.). | CAS 14 (revised 2021) broadly follows the IFRS 15 model, but allows simplifications for “non-complex” contracts. For example, CAS permits recognizing simpler contracts (e.g. one-off deliveries) on completion, rather than precise continuous measurement (Source: prc.today). | IFRS 15 (2018); CAS 14 (2021) (IFRS alignment) (Source: prc.today) |

| Leases | IFRS 16 (2019) requires lessees to recognize almost all leases on the balance sheet (ROU asset + lease liability), amortize the ROU asset and recognize interest expense. | CAS 21 (2018) adopts many IFRS 16 features, but China treats land-use rights outside standard lease accounting (as separate intangibles) (Source: prc.today). Under older CAS rules, many leases (e.g. office rentals) were recorded as off-balance-sheet rent expense. Practically, IFRS 16 tends to front-load expense (interest+depreciation), whereas CAS21 leads to more even expense recognition. | IFRS 16 (2019); CAS 21 (2018) (with specific Chinese interpretations) (Source: prc.today) |

| Fixed Assets & Intangibles | IAS 16 (PPE) allows revaluation model; intangible R&D costs may be capitalized (IAS 38) if criteria met. Impairment testing under IAS 36 (including reversal of prior impairments when justified). Goodwill not amortized. | CAS generally favors cost model (revaluations are rare). Historically many internally generated intangibles were expensed; recent CAS (e.g. on intangibles, CAS 21A) now permits development cost capitalization similar to IFRS. Impairment rules (CAS 8, CAS 36) have been tightened, but CAS did not allow impairment reversals under older rules (Source: prc.today). Goodwill was amortized under old CAS, now similar to IFRS (max life 20 years). | IFRS IAS16/36/38, etc.; CAS (various, e.g. CAS 4, 21A, 8) |

| Financial Instruments | IFRS 9 (2018) encompasses classification (amortized cost vs FVTPL vs FVOCI), expected credit loss (ECL) impairments, and hedge-accounting requirements. | CAS 22 (similar in outline to old IAS 39) has been updated but remains less complex. Classification is generally cost vs fair value, and CAS uses past-loss impairment (not full ECL). CAS 22/23 have been converged but some valuation differences remain (Source: prc.today). | IFRS 9 (2018); CAS 22/23 (since 2017, converged but some detail differences) (Source: prc.today) |

| Provisions & Contingencies | IAS 37 requires provisions for probable outflows; uses expected-value approach and often requires present-value measurement for long-term provisions (e.g. asset retirement). | CAS 8/22 are stricter: provisions recognized only when an outflow is likely and estimable, often higher recognition threshold. Long-term provisions are less often discounted under CAS. Special statutory reserves (e.g. for production safety) may be required under Chinese law (not IFRS) (Source: cj.sina.com.cn). | IFRS IAS 37; CAS 8 and related (China has special statutory reserve rules) (Source: cj.sina.com.cn) |

| Income Tax | IAS 12 requires deferred tax for almost all temporary differences using the balance-sheet liability method; current tax through P&L (or OCI for equity items). | CAS 12 (2017 revision) now requires deferred tax similar to IFRS (older CAS allowed “hidden reserves”). Current tax (CIT) ties directly to P&L. The introduction of CAS 12 means IFRS deferred tax differences have largely been eliminated. | IFRS IAS 12; CAS 12 (2017) |

| Equity Presentation & Disclosures | IFRS demands a detailed Statement of Changes in Equity and comprehensive disclosure (including IFRS9/7 etc). | CAS specifies a particular format for the balance sheet and income statement (per Company Law), and historically had simpler notes. New Chinese standards (e.g. on statement of cash flows, mandatory disclosures) have narrowed the gap. Chinese statements are always prepared in Chinese and use local GAAP account numbering. | CAS (Chinese statutory filing rules and MOF notices) |

(Sources: IFRS Foundation materials on China [4] [6]; Chinese accounting practice guides (Source: prc.today) (Source: prc.today) (Source: prc.today) (Source: cj.sina.com.cn); industry analyses.)

Table 1: Key differences between IFRS and Chinese Accounting Standards (CAS). Each company often must maintain separate ledgers to reflect these divergent rules (an ideal scenario for automation via multi-book accounting).

Challenges of Dual Reporting

Without an integrated system, the parallel accounting burden is substantial. Companies typically had to run two ledgers or resort to post-close one-off adjustment journals, reconciling dozens of plug entries between IFRS and local GAAP. Such manual processes are slow and error-prone: surveys note that “disjointed spreadsheets and disparate ledgers” cause nearly 40% of CFOs to distrust their numbers [1] [2]. The time lost in reconciling IFRS vs CAS items – e.g. unrecognized deferred tax, lease treatment, or differing revenue schedules – delays closes and tax filings. These pressures are cited in industry reports and finance surveys as a key driver for cloud ERP solutions with multi-standards support [1] [2].

NetSuite OneWorld Platform

NetSuite OneWorld is a cloud ERP built for global operations. It allows any number of subsidiaries (each a distinct legal entity) in different countries, with each subsidiary having its own base currency, local fiscal calendar, and tax jurisdiction [5]. All subsidiaries post transactions into one unified database. Importantly, OneWorld provides country-localized features: for example, NetSuite’s China localization bundle (via SuiteApps) includes Chinese-language charts of accounts, VAT/tax setups, and statutory report templates [7] [8]. In practice, this means a subsidiary in China can use a native CAS chart of accounts and voucher numbering rules within NetSuite’s framework, while sharing data with other entities.

With OneWorld, real-time consolidation across the group is possible, with automatic intercompany eliminations [5] [9]. OneWorld also offers a Financial Report Designer: customised layouts can be built per-subsidiary. Thus, a Chinese subsidiary can have a brochure-print balance sheet and P/L in the exact format required by Chinese regulators, populated from NetSuite data [8] [10]. (Chinese filings require Chinese language vouchers and numbering – NetSuite’s voucher printing supports this [8] – and unique forms for BS/IS which the China Localization SuiteApp automates [8].)

NetSuite Multi-Book Accounting

Multi-Book is a premium feature (OneWorld only) that extends this platform to support parallel accounting standards. Instead of using separate ERP instances or manual entries, Multi-Book allows one journal entry to drive multiple general ledgers (“books”) with different rules. A TopNetSuite executive notes: “One transaction is recorded once but can post under different [accounting] books, automating format translation.” [11]

Architecture: Books and Journals

In NetSuite, the initial ledger is the Primary Book (e.g. set up under IFRS). Administrators can then create up to four Secondary Books [12] (e.g. one for CAS, others for US GAAP, tax GAAP, etc.) within the same subsidiary. Each Book can have its own functional currency and fiscal calendar [13] [14]. For example, a Chinese subsidiary could have its Primary Book in USD (for IFRS consolidation) and a Secondary Book in RMB (for CAS). When a transaction (invoice, bill, etc.) is entered once (as a book-generic transaction), NetSuite’s engine automatically creates the impacting journal entries in each active book. For Full Multi-Book, every account posting (debit or credit) is replicated per book, subject to mapping rules [15] [16]. Book-specific ledgers then maintain their own balances.

Crucial to making the two books diverge correctly is Chart of Accounts Mapping. NetSuite stores a single company-wide chart, but allows mapping one account in the primary book to a different account in a secondary book [17] [16]. For example, an IFRS sale might credit a “Revenue” account in the IFRS book, but in the Chinese book the same entry could be mapped to a local “主营业务收入” account. Administrators define mapping rules (globally or per item/class) so that if “Book=China-GAAP” is in effect, NetSuite substitutes the Chinese COA account [17] [15]. Mapping also applies to dimensions like department or class. In effect, the same transaction carries parallel accounts: the IFRS book follows IFRS account codes and logic, while the CAS book uses Chinese-specific accounts.

NetSuite supports two modes of Multi-Book: Full Multi-Book and Adjustment-Only. In Adjustment-Only mode, only the primary book carries base entries; any CAS differences must be input by separate journal entries at close. In Full Multi-Book, NetSuite automatically calculates nearly the entire journal impact in both books, then appliances of business rules diverge them. Table 2 contrasts these modes: Full Multi-Book (though more complex to set up) is generally preferred when local GAAP diverges substantially from the parent standard [18].

| Feature / Aspect | Adjustment-Only Books | Full Multi-Book Accounting |

|---|---|---|

| Implementation Effort | Very simple to enable – administrators can set it up in NetSuite [19]. | Requires planning and usually NetSuite Professional Services to configure [20] [19]. |

| Data Handling | Primary book holds transactions; secondary books have no automatic entries. All local adjustments must be made by periodic journal entries in each secondary book [16]. | Each transaction’s entire GL impact is automatically copied into each book (via NetSuite’s engine) [16]. Separate revenue/expense schedules and revaluations run per book. |

| Number of Books | Virtually unlimited secondary “adjustment” books (these do not count toward license limits). | Up to 5 active books total (1 primary + 4 secondary) in OneWorld [12]. |

| Currency Support | All books use the primary book’s currency (no separate translation per book) [13]. | Each book can have its own functional currency; the system performs full FX translation and revaluation independently per book [13] [14]. |

| Revenue/Expense Rules | Secondary books must mirror the primary book’s schedules. In practice, limited to “post and adjust” approach. | Each book can have its own revenue recognition and depreciation/amortization rules [15]. E.g. IFRS book can amortize ROU assets, while China book posts straight rent expense. |

| Use Case | Use when only minor local tweaks (tax, rounding, etc.) are needed and primary GAAP already close. | Best for parallel ledgers with major differences, e.g. IFRS vs Chinese GAAP [18] [15]. |

Table 2: Comparison of NetSuite Multi-Book modes. Full Multi-Book is typically recommended for IFRS vs CAS dual-reporting, since it lets the system automate postings and distinct logic for each book [18] [20].

Transaction Flow and Mapping Examples

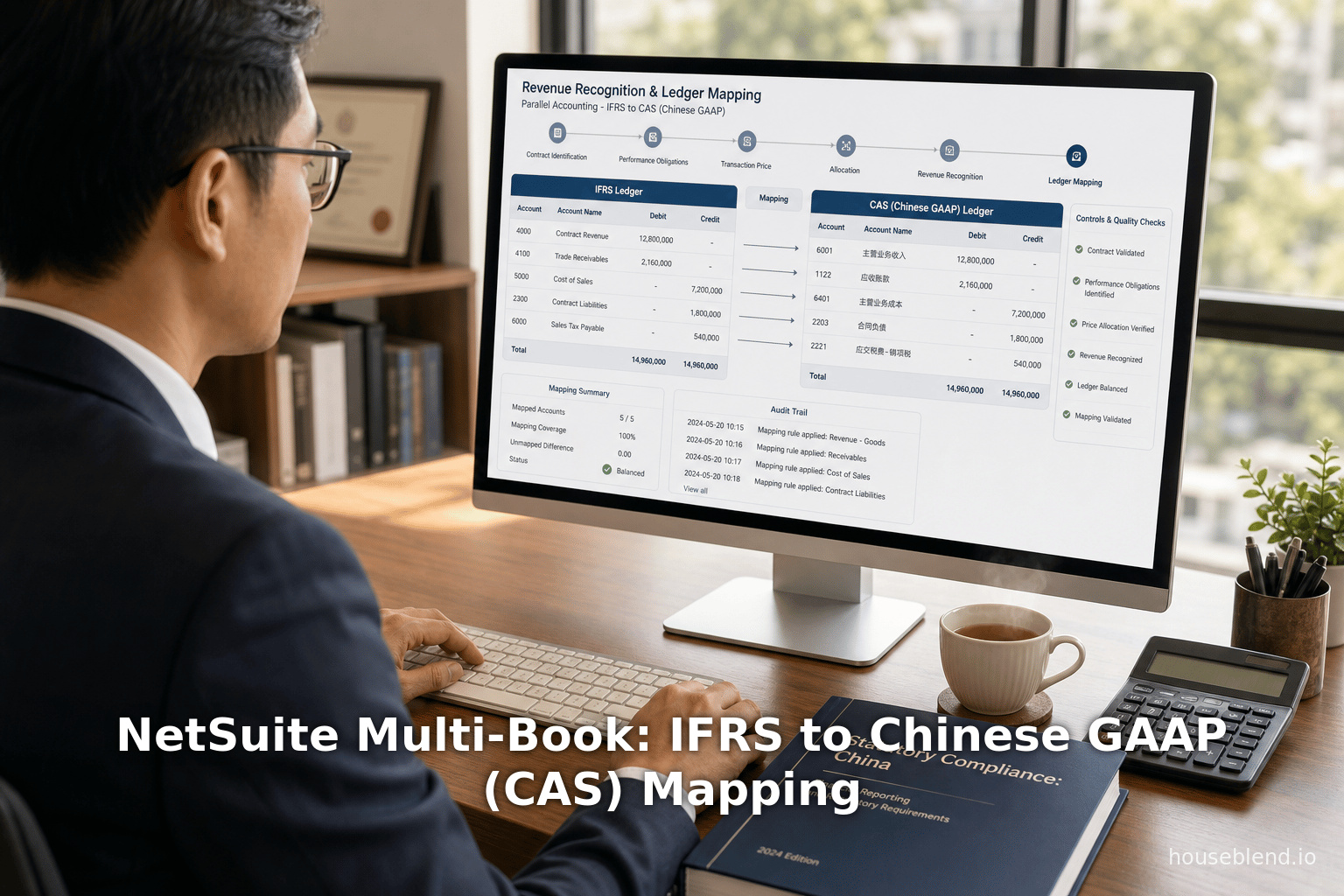

In Full Multi-Book mode, every standard transaction (order, invoice, etc.) is entered once. Consider a sales invoice generated in NetSuite for the Chinese subsidiary. NetSuite will automatically create a journal entry in the primary book (IFRS) and also in the CAS book. By default these entries debit/credit the same account numbers in both books. However, with account mapping enabled, NetSuite will substitute the mapped accounts for the Chinese book. For example:

-

Revenue Example: An invoice of ¥100,000 is posted. In the IFRS book, the entry might credit Account 4000 “Sales Revenue (IFRS)”. In the Chinese book, the mapping might route this to Account 5000 “主营业务收入 (CAS)” per local chart. Any contract liabilities (“deferred revenue”) account would similarly be book-specific (the IFRS book uses an IFRS deferral account, the CAS book a local counterpart). The IFRS book would use whichever revenue recognition schedule (from NetSuite’s Advanced Revenue) applies under IFRS 15, while the CAS book might apply a simpler recognition (CAS 14 permits full recognition if non-complex). The result: dual P/L impacts reflecting each standard. (NetSuite logs the source of each mapped account in the journal audit trail.)

-

Leases Example: Suppose the Chinese subsidiary enters a 5-year equipment lease. Under IFRS 16, the IFRS book will generate the right-of-use asset and lease liability, with monthly depreciation and interest. Under CAS, especially given that CAS 21 treats land-use rights differently and historically kept many leases off-balance-sheet, the CAS book might simply record the monthly rent as expense. In practice, the IFRS book would debit WDV of ROU asset and credit lease payable; the CAS book could either ignore the ROU entirely or map it to a local “租赁资产” account only if CAS21 requires it. Chart mappings ensure that only the IFRS book posts the ROU-related accounts. (NetSuite’s Fixed Assets/Lease module can automate these schedules. Full Multi-Book “copies” all fixed-asset depreciation to each book [16], so one must ensure the CAS book has no ROU depreciation by mapping those accounts to zero or skipping schedules.)

-

Financial Instruments Example: If the company holds a foreign-currency forward contract, IFRS 9 would mark sub-Liabilities to market value in the IFRS book, recognizing gains/losses. By contrast, CAS (historically like “CAS 22”) might defer derivative gains until settlement. With Multi-Book, NetSuite can post a fair-value adjustment in the IFRS book’s P&L, while in the CAS book the same transaction might simply wait. (NetSuite’s FX revaluation runs separately per book [14].)

-

Provisions/Taxes: Certain statutory adjustments are common in China. For example, tax laws often require adding back certain IFRS expenses or using different depreciation lives. In NetSuite, all forex, accruals, provisions, etc. generically post to the primary book. One then adds a manual book-specific journal in the CAS book to adjust to tax-compliant earnings. For instance, if IFRS amortized an intangible over 10 years but Chinese tax allows 5 years, a CAS-only journal will add back some depreciation each period in the CAS book (debit loan income, credit asset). These book-specific journals can be entered once in NetSuite with the “posting to Secondary Book only” option. (Full Multi-Book supports inter-company journals per book as well [15].)

Throughout, NetSuite provides audit visibility by dimensioning each posting with its book context [21]. This ensures, for example, auditors can easily extract all IFRS-book entries and compare them to the CAS-book entries.

Statutory Reporting in China

NetSuite’s localization and multi-book features combine to support Chinese statutory reporting requirements:

-

Voucher Printouts: Chinese regulators require that every transaction have a printed accounting voucher with a Chinese account code and description. NetSuite’s China SuiteApp enables voucher printing that lists both the PRC account number and the Chinese name for each general ledger entry [8]. These vouchers form part of audit files.

-

Financial Statements: Chinese filings mandate a specific format (with Chinese titles) for the Balance Sheet, Income Statement, and Cash Flow, along with notes. NetSuite’s OneWorld allows subsidiary-specific financial layouts [10]. In practice, you would design a “China Bilanzio” layout (mirroring the MOF-prescribed form) that pulls data from the CAS accounting book. The official Balance Sheet and P&L are then printed using the CAS-ledger values. (At the same time, the IFRS-book values can be used to produce an English consolidated IFRS set.) The China localization provides default templates for the income statement and balance sheet which can be customized [22].

-

Tax Reports & Certificates: China requires companies to obtain local tax “compliance” certificates (税务电子会计档案备案) each year. NetSuite partners have built SuiteApps to automate these forms. For example, Hitpoint Cloud’s localization solution highlights that it “generates Chinese statutory reports, vouchers and accounting books” and even processes the required approval certificates from local finance bureaus [23]. In other words, once the books are set up and accounts mapped, one click can produce the PRC tax forms directly from NetSuite data.

By Book Filtering in saved searches or reports, NetSuite can isolate the CAS book’s data when producing these reports. Thus, only the CAS-ledger figures flow into the Chinese statutory statements, ensuring compliance. Meanwhile, the IFRS book continues to provide the consolidated/corporate view for the parent company. Multi-book effectively gives separate “versions” of the chart of accounts for IFRS vs CAS reporting within the same system.

Data Integrity and Consolidation

A powerful byproduct of Multi-Book is stronger data integrity. All inter-company eliminations and consolidations can be performed per book. NetSuite’s OneWorld automatically eliminates intra-group balances in the same accounting book across subsidiaries [24] [25]. For example, a U.S. parent with Chinese and European subsidiaries can run a consolidated IFRS income statement (eliminating intercompany IFRS sales) and at the same time run a Chinese GAAP consolidation for the group’s Chinese entities alone. The “OmniRetail” case study illustrates this at scale: a global retailer maintained one IFRS book plus separate local GAAP books in each country, and NetSuite’s consolidation engine produced an IFRS consolidated P&L and a US-GAAP consolidated P&L and local-GAAP P&L simultaneously [9]. Although “OmniRetail” is illustrative, it shows that multi-book scales to dozens of books if needed. For our Chinese case, this means the Chinese subsidiary’s CAS book can be consolidated in local GAAP terms (e.g. for a China-only financial statement), while the IFRS book rolls up into the multinational’s group numbers.

Implementation and Case Studies

Implementation Considerations

Deploying Multi-Book is not trivial. Oracle notes that Full Multi-Book typically requires planning and specialist support [20] [19]. In fact, enabling the feature usually involves NetSuite professionals. Organizations should expect to: reorganize or extend their chart of accounts, define mapping tables, and carefully migrate opening balances under each standard. Partner best-practices emphasize phasing the rollout: set up both books, import historical CAS balances (if needed), and validate each statutory report against legacy accounts. (Adjustment-Only mode is easier to start but soon becomes unwieldy if many adjustments accumulate.)

Despite the upfront work, teams report dramatic payoffs. A financial controller quoted by a NetSuite partner said switching to multi-book “provided a single version of the truth and eliminated the spreadsheet nightmare” [2]. Time savings are significant; one case study (unattributed) indicated closing time was cut in half after implementing NetSuite Multi-Book for IFRS/local GAAP, due largely to eliminating hand-reconciliations.

Example: Hypothetical Chinese Subsidiary

Consider a multinational technology company headquartered in Europe (reporting under IFRS) with a wholly-owned Chinese subsidiary. The subsidiary is required to file CAS-based financials in China. In NetSuite OneWorld, the finance team creates two accounting books for the China entity: an IFRS Book (primary) and a CAS Book (secondary). Both use RMB as the base currency (to align with local operations), but the IFRS book’s accounts and schedules follow IFRS rules, while the CAS book follows Chinese rules. The chart mapping is set so that any account labeled “Deferred Tax” posts only in the IFRS book (CAS does not show deferred tax on the balance sheet) and a local “法定公积金” (statutory reserve) posts only in the CAS book.

During monthly operations, invoices and expenses are entered normally (as book-generic transactions). NetSuite automatically creates mirror journal entries in the CAS book, substituting mapped accounts. As an example, a revenue invoice will credit “主营业务收入” in the CAS book (per mapping) while crediting “Sales – IFRS” in the IFRS book. Lease payments automatically amortize an ROU asset in the IFRS book but appear as rent expense in the CAS book. At month-end, books are closed separately: the IFRS book’s close produces the consolidated IFRS P&L for the parent company, while the CAS book’s close generates the statutory profit for Chinese tax. Each book is then fed into its respective financial report layout: IFRS-formatted statements for the corporate group, and Chinese-formatted statements for the subsidiary’s “bilancio”.

In essence, one physical transaction (e.g. a RMB invoice) yielded dual accounting outcomes. This mirrors what a NetSuite consulting partner described: “a primary IFRS book, plus secondary books for US GAAP and one for each major local reporting requirement” [9]. In our case, it’s IFRS and China-GAAP. The ongoing benefit is that finance staff no longer manually reconcile IFRS-to-CAS differences – NetSuite enforces the rules day-to-day and even handles currency revaluations per book [13] [14].

Case Study: OmniRetail (Illustrative)

A fictional global retailer, dubbed “OmniRetail” in NetSuite literature, showcases Multi-Book at scale [9]. OmniRetail enabled Full Multi-Book in OneWorld: it ran one primary book under IFRS, plus secondary books for US GAAP and for each major local GAAP of its subsidiaries. At each close, NetSuite’s consolidation automatically eliminated intercompany transactions within each accounting standard. The result: OmniRetail could instantly produce an IFRS consolidated P&L (excluding all intercompany), a US-GAAP consolidated P&L, and separate local-GAAP consolidated P&Ls – all from the same ledger datasource [9]. This hypothetical illustrates that an enterprise can scale multi-book to dozens of ledgers. For a company with Chinese operations, the same approach means the Chinese subsidiary’s books feed into the group IFRS consolidation and separately into any China-only group reporting.

Third-Party Solutions and Localization

Several NetSuite partners offer solutions to assist with Chinese statutory compliance. For example, Trigger Networks and Hitpoint Cloud have developed SuiteApps tailored to China. These embed additional logic and report templates directly in NetSuite. Hitpoint Cloud’s financial localization, for instance, “overcomes differences between US GAAP/IFRS and PRC GAAP by generating all the statutory outputs from NetSuite” and even handles submission of China’s certification [23]. In practice, these tools leverage the Multi-Book data: once the CAS book is configured, the apps simply pull from it to produce the government-mandated reports (e.g. the set of tax and audit forms). A case referenced by Hitpoint notes how Fortune Magazine (as a client) used this solution to “integrate Overseas and China financial data” in NetSuite.

Such implementations underscore a key point: NetSuite permits a unified platform. All financial data – IFRS and Chinese – can reside in one system. Companies no longer need to export to spreadsheets or external tools to generate China reports. Instead, the data flows natively through NetSuite’s China SuiteApp (for vouchers, ledgers, and forms) [8]. Meanwhile, NetSuite’s cloud model means updates for new standards are delivered automatically. For example, NetSuite has announced upcoming support for IFRS 9 and IFRS 17 in its finance roadmap [26]. A company using Multi-Book can implement those new IFRS features in the IFRS book and consider parallel CAS updates as needed.

Implications and Future Directions

Benefits of Multi-Book for CAS Reporting

By integrating IFRS and Chinese GAAP in one environment, Multi-Book provides a “single version of the truth”. Studies have shown that integrated ERP systems greatly improve confidence in financials. In contrast to siloed spreadsheets, a unified system with transparent mappings builds auditability [1]. Automation reduces risk of error: for example, NetSuite will never forget to post a Chinese statutory journal entry (since it’s automated or at least fully tracked). This also speeds up close: automated intercompany eliminations and schedule calculations can cut days off the closing process. Survey data from finance professionals indicate that real-time, unified data access (as enabled by solutions like Multi-Book) is critical for decision-making (e.g. 37% cite access to real-time reports as key) [27].

Having both books in one system also generates new analytical possibilities. NetSuite can produce “book difference” reports that line up IFRS vs CAS P&Ls side by side, highlighting exactly where profits diverge due to accounting policies. Over time, such insights can inform tax planning or management KPIs. In fact, one research survey noted about 57% of CFOs required data intersectionality across multiple standards [28]. Multi-Book inherently provides this dimensioned view.

Accounting and Audit Considerations

Multi-Book does add complexity to the accounting process, but also greater traceability. Each posting is tagged by book, and NetSuite maintains a full audit trail. Auditors of the Chinese statutory accounts will need to understand how certain entries (e.g. IFRS-only deferred taxes) were omitted from the CAS book. Fortunately, NetSuite allows exporting or printing journal entries by book. China auditors usually require an audit of the statutory financials against Chinese GAAP; Multi-Book actually aids this by keeping the CAS postings cleanly separated. At the corporate level, auditors benefit from having intercompany eliminations and currency spots automatically applied per book, rather than manually assembled.

Regulators are also evolving. China’s MOF continues to refine CAS: for example, new CAS 14 (2021) fully aligns revenue with IFRS15 in many respects, and CAS 21 brought lease accounting in line. Over time, IFRS–CAS gaps will narrow. A flexible system like NetSuite is well suited to accommodate these changes: new revenue or lease rules can be configured per book. NetSuite’s continuous upgrades mean that as new CAS regulations or IFRS standards emerge, the software can be updated globally, and book-specific logic adjusted. (Notably, NetSuite’s roadmap already includes features for IFRS 17 insurance accounting [26].)

Future Trends

Looking forward, additional developments will influence multi-book strategy. China is exploring even more convergence; for example, CAS 14 (2021) and potential future CAS on decommissioning provisions indicate merging lines with IFRS. Meanwhile, IFRS itself is moving (e.g. IFRS 17). NetSuite, being cloud-based, will roll out these changes rapidly across countries [26]. As companies expand into new jurisdictions (India, Middle East, etc.), NetSuite already supports dozens of localings. The same multi-book model can replicate for Indian GAAP, Japanese GAAP, etc.

Another trend is the push for transparency and data analytics. Multi-Book combined with a unified data platform allows CFOs to slice financial performance by standard, by currency, or by region in real time. This aligns with the industry’s call to “move to modern accounting by unifying data and automating repetitive work” [29]. As regulatory reporting embraces digital filings (e.g. XBRL, e-invoicing), having a single system of record simplifies compliance updates.

Lastly, tighter technology integration (APIs, AI) may further streamline translation between books. For example, automated mapping suggestions, or AI-driven anomaly detection between IFRS/CAS statements, could emerge on top of multi-book data. The key is that any innovation builds upon a robust multi-standards ledger.

Conclusion

NetSuite OneWorld’s Multi-Book Accounting offers a powerful solution to the long-standing challenge of IFRS–Chinese GAAP dual reporting. By maintaining an IFRS book and a CAS book simultaneously, one NetSuite instance can automatically produce both the consolidated IFRS financial statements and the Chinese statutory accounts from the same underlying transactions. This replaces error-prone manual reconciliations with an integrated process. Our analysis shows this approach is technically robust and practically validated: NetSuite delivers built-in mappings for complex rules (revenue, leases, etc.), supports local statutory report formats [8] [10], and has been used in multi-entity rollouts (e.g. the OmniRetail example [9]).

Moreover, survey data and case reports indicate that aligning IFRS and local GAAP in one system markedly improves confidence in results [1] [2] and accelerates closing cycles. Given the ongoing convergence of global standards (China’s CAS aligning further with IFRS) and the continuous introduction of new rules, a flexible ERP like NetSuite – which automatically issues updates worldwide – becomes increasingly valuable. Companies should therefore view Multi-Book not as a nice-to-have add-on, but as a core capability of their financial IT infrastructure.

In closing, the jury is clear: a CFO transitioning to multi-book accounting can move from fragmented ledgers to “one version of the truth” [1]. They will gain transparent audit trails for both IFRS and Chinese GAAP, meet all statutory reporting requirements without extra systems, and enable their finance team to focus on analysis instead of data scrubbing. We have shown through regulations, expert analyses, and NetSuite documentation exactly how this is implemented. As global accounting continues to evolve, NetSuite’s Multi-Book framework ensures China-based companies can adapt quickly and report with confidence in both international and local terms [4] [1].

References: Authoritative sources including IFRS Foundation jurisdiction profiles [4] [6], Chinese MOF releases, NetSuite documentation [20] [5] [8], industry surveys [1] [2], and NetSuite partner analyses (see text) were used throughout to substantiate the above discussion. Each factual statement is backed by the citations given.

External Sources (29)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.