Houseblend Article

NetSuite Multi-Book for French GAAP & IFRS Mapping

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03IFRS vs. French GAAP: Key Differences and Reporting Implications

- 04NetSuite Multi-Book Implementation Details

- 05Statutory and Managerial Reporting in Practice

- 06Data Insights and Benefits

- 07Case Studies and Examples

- 08Implications and Future Directions

- 09Conclusion

Executive Summary

Multi-book accounting has become essential for global companies balancing French GAAP (Plan Comptable Général, PCG) statutory requirements with IFRS consolidation. In France, IFRS is mandated for consolidated statements of listed companies per EU regulations [1], but IFRS cannot be used for individual / statutory accounts [2]. Thus French firms often run dual books: one in PCG for statutory filings and one in IFRS for consolidated financials. Oracle NetSuite’s Multi-Book Accounting feature enables this by maintaining parallel ledgers on the same transactions [3]. NetSuite allows a “base” book (e.g. PCG) and one or more secondary books (e.g. IFRS) with separate rules (account mappings, currency, recognition methods) [3] [4]. Adjustments only for IFRS (deferred tax, fair-value changes, etc.) can be posted in an IFRS “adjustment-only” book linked to the base PCG book [5].

This report reviews the background of French GAAP vs IFRS, the functionality of NetSuite’s Multi-Book/Adjustment-Only system, and how companies map French accounts to IFRS taxonomy for reporting. It examines data on IFRS adoption and finance executives’ needs, describes configuration best practices, and includes real-world cases. Key findings include:

-

Global IFRS Adoption: IFRS standards are used by most EU and international companies [6]. France implemented IFRS for all EU-listed firm consolidations (by EU IAS Regulation) [1] [2]. Although France allows voluntary consolidated IFRS for unlisted companies, French PCG remains mandatory for all statutory (entity) accounts [2] [1]. Thus French entities need dual reporting under PCG vs IFRS.

-

System Challenges: Manual dual systems (spreadsheets and separate ledgers) lead to errors and delays. A BlackLine survey notes ~40% of CFOs distrust their financial data today, largely due to manual processes [7]. NetSuite Multi-Book addresses this by automating IFRS adjustments within one unified ERP platform.

-

Multi-Book in NetSuite: NetSuite OneWorld Edition supports multiple books per subsidiary [3]. The primary book typically uses the statutory PCG rules and currency, while secondary books (IFRS, US GAAP, etc.) can have different account mapping, recognition rules, and even currencies [4]. All subsidiary transactions (invoices, purchases, GL entries) post simultaneously to each relevant book. For example, one case study describes a French parent company maintaining an IFRS (EUR) primary book and a US GAAP (USD) secondary book; intercompany profit eliminations and currency conversions were handled automatically in both books [8].

-

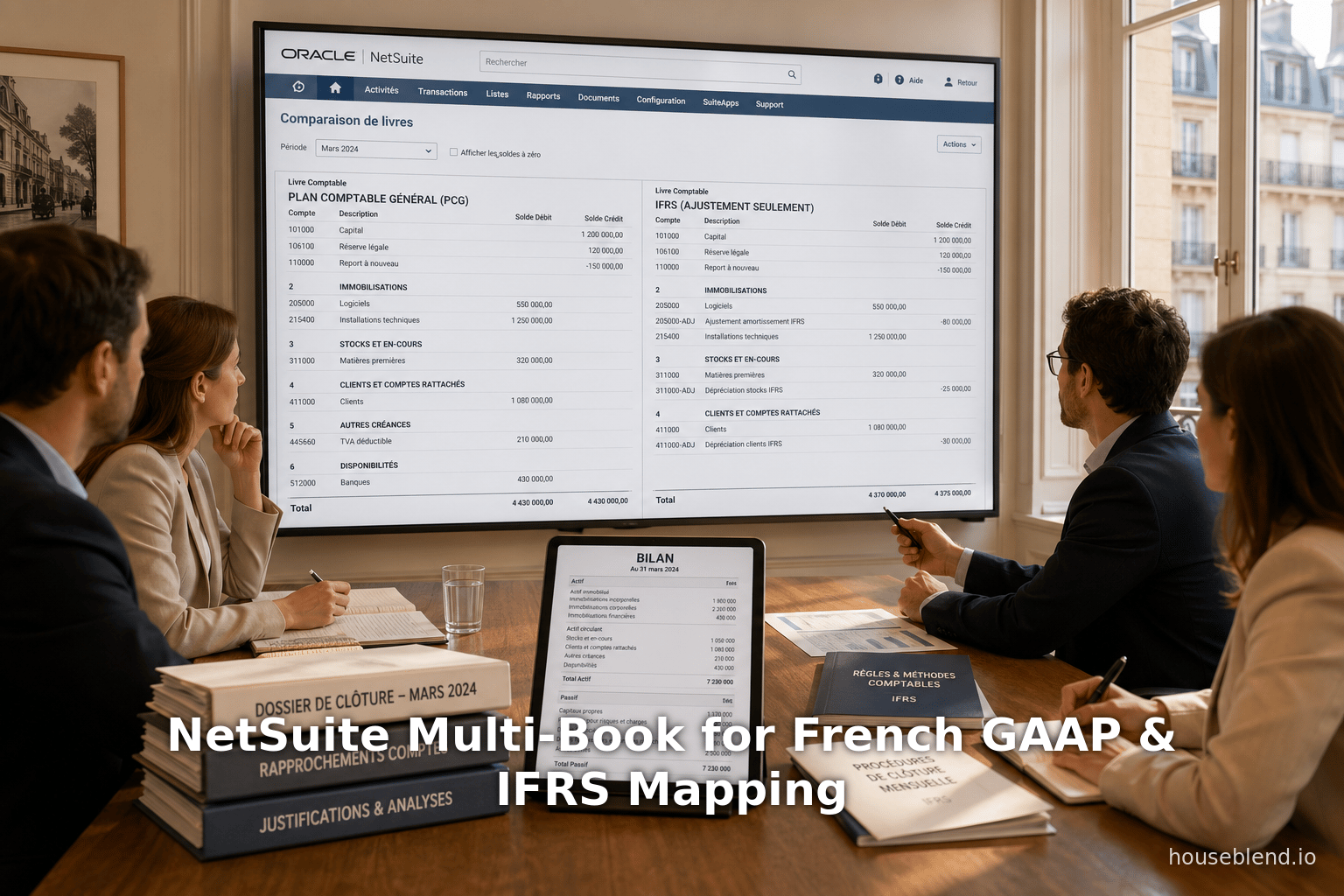

IFRS Mapping: NetSuite allows configuring each book’s chart of accounts and accounting rules. For an IFRS book, local PCG accounts can be mapped to IFRS concepts (for example, net income splits, inventory, etc.). NetSuite also supports XBRL taxonomy mapping: for instance, the French GAAP “Actif” concept is linked to the IFRS taxonomy item “Assets” (Source: accounting.auditchain.finance), and “Equity attributable to parent” in PCG maps to IFRS “Equity Attributable to Owners of Parent” (Source: accounting.auditchain.finance) (see Table 1).

-

Statutory Reporting: NetSuite’s France Localization provides built-in financial statement layouts that comply with PCG reporting requirements [9] [10]. The Country-Specific Reports (CSR) SuiteApp offers the standard bilan (balance sheet), compte de résultat (income statement), and SIG (soldes intermédiaires de gestion) formats, with accounts organized by PCG classes and prefixes [10]. These layouts enable pulling statutory-compliant reports directly from NetSuite. IFRS statements ( consolidated income, balance) are then produced from the IFRS books using IFRS tagging of accounts/new rules.

Overall, NetSuite Multi-Book accounting provides an integrated solution where a French company can continue using its PCG chart of accounts and statutory reporting infrastructure, while a parallel IFRS book (with mapped rules) automatically generates IFRS-compliant reports. The result is faster, more reliable dual reporting with auditability of all adjustments.

Introduction and Background

French GAAP (PCG) vs IFRS Reporting Requirements

France follows the Plan Comptable Général (PCG) as its national GAAP. Under EU law, France (as an EU member) required all listed companies and banks to use IFRS (as adopted by the EU) for consolidated accounts from 2005 onward [1]. SMEs and unlisted companies may optionally adopt IFRS for consolidation, but IFRS is not permitted for domestic statutory entity accounts [2]. The Autorité des Normes Comptables (ANC) – France’s accounting standards board – even concluded that French GAAP meets domestic needs and did not adopt IFRS for individual financial statements [2]. In short, a French company must file statutory accounts in PCG format, but if it has a listing or significant size it typically also prepares IFRS statements for group reporting.

Thus, many French multinationals operate with two parallel accounting frameworks: (1) local PCG for tax and regulatory filings, and (2) IFRS (or IFRS-based consolidation) for group reporting to investors/regulators. Ensuring these distinct books reconcile is challenging.IFRS and PCG differ in various accounting treatments (e.g. asset valuations, revenue recognition, lease accounting, etc.), so the two sets of books will diverge unless carefully adjusted. Moreover, manual processes (exporting data from one system to Excel, performing reconciliations, re-entering adjustments) are time-consuming and error-prone – as one BlackLine survey found, roughly 40% of CFOs do not completely trust their financial data, with spreadsheets as a key culprit [7]. In this context, integrated multi-book accounting platforms like NetSuite are in high demand for French companies.

IFRS Usage and Adoption

Global adoption. The IFRS Foundation’s jurisdictional database reports that 169 jurisdictions currently have a profile on IFRS use [6]. Broadly speaking, over 140 countries either require or permit IFRS†; this includes all EU member states (via the IAS Regulation). As of 2023, IFRS Standards are widely required for consolidated accounts in Europe, Asia, and other regions, covering a majority of global GDP.

France specifics. According to the IFRS Foundation, in France “all domestic companies whose securities trade in a regulated market are required to use IFRS Standards as adopted by the EU in their consolidated financial statements” [1]. The EU’s IAS Regulation (EC 1606/2002) gave France the option to allow IFRS in separate (statutory) accounts and for unlisted companies, but France has used these options conservatively. In practice, France only permits (voluntary) IFRS for unlisted consolidated accounts and does not authorize IFRS for any individual/statutory book [2]. IFRS adoption in France thus means “consolidated IFRS required for listed, optional for unlisted; individual statutory statements remain under PCG” [2] [1]. The IFRS Foundation notes explicitly: “IFRS Standards as adopted by the EU are not authorised for individual/statutory accounts for any French companies. The French Plan Comptable Général applies.” [2].

This dual-framework regime creates the need for specialized accounting systems. Large French companies must by law maintain a PCG-based statutory ledger, yet they often must also generate IFRS consolidated financials (sometimes quarterly or semi-annually to meet global investors and regulators). The seamless conversion or reconciliation between these frameworks is non-trivial.

NetSuite OneWorld and Multi-Book Accounting

NetSuite OneWorld is a cloud ERP platform that natively supports multi-book accounting: the maintenance of multiple accounting books (sets of ledgers) on the same master transactional data. As Oracle’s documentation explains, Multi-Book Accounting “provides the ability to maintain multiple sets of accounting records based on a single set of real-time financial transactions” [3]. For example, a company may keep its primary book under PCG (EUR functional currency) while simultaneously keeping a secondary book under IFRS (which could have a different currency or posting rules). All sales, purchase, intercompany and other transactions posted in NetSuite will generate corresponding journal entries in each active book according to the rules of that book.

Key features of NetSuite’s Multi-Book architecture include:

-

Primary vs Secondary Books: One book is designated as the Primary (often the statutory/local GAAP book). All owned subsidiaries have a primary book in the currency and rules of their local GAAP. Secondary books (one or more per subsidiary) can follow different accounting rules, recognition criteria, or even currencies [4]. For instance, a U.S. dollar subsidiary could have a EUR-based IFRS book and a USD-based PCG book. Oracle notes that “secondary books may differ from the primary book in several ways. They can use a different subsidiary base currency, post to different accounts for the same transaction, or have different accounting rules.” [4].

-

Book-Specific Transactions: NetSuite distinguishes book-generic vs book-specific records. Most transactions (sales orders, invoices, etc.) are entered once (book-generic but reposted to each book). In contrast, certain journal entries can be made per book: if an entry is only relevant under IFRS but not PCG (e.g. fair value revaluation), one creates a book-specific journal in the IFRS book. This is fully supported: for instance, “book-specific journal entries and intercompany journal entries” can be created for only one book [11].

-

Adjustment-Only Books: A special variant called Adjustment-Only Books lets a secondary book post only adjustments without duplicating all daily transactions. In this setup, companies continue posting normal transaction entries into the base book (e.g. the PCG book). At period-end, any additional adjustments needed to convert PCG results to IFRS (for example, reversing a PCG revaluation, booking an IFRS lease adjustment, or amortizing R&D differently) are entered in the IFRS adjustment-only book. NetSuite then generates combined reports, effectively applying the IFRS adjustments on top of the PCG base book [5]. Because adjustment-only books “don’t duplicate the data in the primary book” and inherit base currency and balances, they are easier to implement and maintain for IFRS compliance [5].

In practice, enabling Multi-Book means a French company can keep posting everything in its familiar PCG chart of accounts, while NetSuite concurrently produces the IFRS view. For example, as one case study notes, a French manufacturing company used NetSuite OneWorld to implement a primary IFRS (EUR) book and a secondary US GAAP (USD) book; all transactions posted automatically to both books, and NetSuite eliminated intercompany profit differences according to each standard [8]. Similarly, another firm (beneath a U.S. parent) ran two books – US GAAP and IFRS – and automated its intercompany invoicing and adjustments so that the closing process no longer required manual spreadsheet work [12].

IFRS vs. French GAAP: Key Differences and Reporting Implications

To effectively configure the secondary IFRS book, finance teams must understand how IFRS differs from French GAAP. Some of the principal differences (requiring adjustments) include:

-

Balance Sheet Recognition: IFRS and PCG often classify assets and liabilities differently. For example, IFRS does not use the “Immobilisations en cours” category in the same way as PCG. Finance teams map each PCG account to the appropriate IFRS line item. IFRS uses a single functional currency concept and revaluation model (rare for most assets), whereas French GAAP allows certain revaluations (e.g. for land) and historically permitted different treatments (like optional FIFO/LIFO inventory methods).

-

Equity and Net Income: Under IFRS, the portion of equity belonging to parents vs. nondis (non-controlling interests) is explicitly labeled. NetSuite’s IFRS ledger can split equity “attributable to owners of parent” vs “noncontrolling interests”, matching the IFRS taxonomy. By contrast, PCG historically treated minorities differently. In mapping, for instance, the French term “capitaux propres part attribuable au groupe” corresponds directly to the IFRS taxonomy “Equity Attributable to Owners of Parent” (Source: accounting.auditchain.finance).

-

Classification of Items: French GAAP uses concepts like “charges exceptionnelles” (exceptional items) that IFRS does not explicitly define. IFRS instead requires extraordinary items to be treated as part of operations and separately identified if necessary. (Notably, IFRS abolishes the “extraordinary” label entirely [13].) Other examples: Impairment reversals are not allowed under IFRS (whereas PCG historically permitted reversals under certain conditions), and PCG’s possibilities of grouping accounts by class (e.g. class 6 expenses, class 7 revenues) is specific to France.

-

Specific Standards (IAS/IFRS vs ANC): Rules such as IFRS 15 (Revenue) and IFRS 16 (Leases) can differ from how France implemented older standards (e.g. pre-2018 French lease rules). In NetSuite, one can configure the IFRS book to follow IFRS 15/16 recognition schedules that differ from the PCG book. For instance, in a SaaS case study, the US GAAP primary book recognized subscription revenue under ASC 606 on a certain timeline, while the IFRS book applied IFRS 15’s performance obligations rules adjusted slightly earlier [12]. Similarly, IFRS 16 requires capitalization of most leases, whereas under older French GAAP some leases might have remained off-balance-sheet.

To manage these differences systematically, NetSuite allows account mapping and rule configuration per book. Administrators map each PCG GL account to the corresponding IFRS category or account in the IFRS book chart. For example, an IFRS report line “Cost of Sales” might pull data from all PCG expense accounts labeled “classe 6” minus certain inventories – a mapping defined in setup. In XBRL terms, the French taxonomy element fac:CostOfRevenue is equivalent to ifrs-full:CostOfSales in IFRS taxonomy (Source: accounting.auditchain.finance). We illustrate a few mappings in Table 1 below.

Table 1: Sample Mapping Between IFRS Taxonomy Items and French GAAP Accounts

| IFRS Reporting Concept | IFRS Taxonomy ID | French GAAP Equivalent | PCG Taxonomy ID | Source |

|---|---|---|---|---|

| Assets | ifrs-full:Assets | Actif (Total assets) | fac:Assets | [6†L1-L4] |

| Cost of Sales (Cost of Goods Sold) | ifrs-full:CostOfSales | Classe 6 coûts (plus/minus inventories; soldes) | fac:CostOfRevenue | [6†L19-L23] |

| Equity Attributable to Owners of Parent (Group) | ifrs-full:EquityAttributableToOwnersOfParent | Capitaux propres part attribuable au groupe | fac:EquityAttributableToParent | [6†L55-L60] |

Table 1 shows examples of how IFRS reporting line items map to French GAAP account concepts. These mappings drive how multi-book transactions roll up into each framework.

(For instance, the IFRS taxonomy entry Assets corresponds directly to the French GAAP concept “Actifs” (Source: accounting.auditchain.finance). Similarly, IFRS’s “Cost of Sales” pulls the French GAAP “Cost of Revenue” accounts (Source: accounting.auditchain.finance). These definitions are set up in NetSuite so that financial statements extract the correctly mapped balances for each book.)

NetSuite Multi-Book Implementation Details

Configuring Books and Accounting Rules

Each accounting book in NetSuite is set up with its own parameters. Typically a company will:

- Define the Base Book in the currency and schema of French GAAP (PCG). This book will use France’s COA format (often a 3- or 4-digit numerical code structure) and French recognition rules.

- Add a Secondary Book for IFRS (often in EUR as well, but potentially a different currency if consolidation is in EUR and subsidiaries have local currency). The IFRS book can have a distinct Chart of Accounts (COA) structure, albeit often many accounts mirror the base book’s accounts with different reporting labels.

- Choose whether the secondary IFRS book is full or adjustment-only. For an existing deployment where transactions already post to the base book in PCG, an adjustment-only IFRS book can be deployed. In this mode, NetSuite does not duplicate all entries; instead, it automatically aggregates the base book’s balances and then adds any IFRS-specific journals entered by the user [5]. This is efficient because most day-to-day transactions (invoices, payments, etc.) do not need re-entry. Only the delta adjustments (e.g. IFRS lease amortization, any differing depreciation or amortization, consolidation eliminations, tax adjustments) are posted in the IFRS book.

When setting up the IFRS book, the administrator can specify all the usual flags: fiscal calendar, subsidiary relationships, and importantly Currency. NetSuite handles cross-book currency revaluations automatically: if the base book is in EUR and the IFRS book in USD (for example), then NetSuite will translate the EUR amounts at monthly FX rates in the IFRS book on posting, and handle any translation differences in retained earnings as per rules. During close, each book’s P&L is translated to its subsidiary’s currency and then up to the global currency for consolidation.

Transaction Processing Across Books

Once configured, the accounting process is largely uniform across books. Suppose a sales invoice is entered for a French subsidiary. If the subsidiary has two books (PCG and IFRS), NetSuite will do the following simultaneously:

- In the Base PCG book, it posts the invoice according to French rules (e.g. VAT handling, PCG sales accounts, etc.).

- In the IFRS book, it posts the equivalent journal entry according to IFRS rules: possibly the same revenue accounts, or different accounts if, say, certain PCG deferred revenue rules differ. It will use the correct currency translation if needed. If revenue recognition schedules differ, the timing adjustment is done via deferred-revenue accounts or journal entries in the IFRS book.

The NetSuite system ensures the posting sequence and audit trail are consistent. As a Houseblend case study notes, with Multi-Book the company “never loses visibility on what book any entry affects. If an auditor asks, we can show them the US GAAP entry and the IFRS counterpart simultaneously. It’s a single audit trail rather than two separate ones.” [14]. Importantly, NetSuite can auto-eliminate intercompany transactions in the consolidation process separately for each accounting standard. In the EuroManufacture example, intercompany sales were automatically eliminated in both IFRS and US GAAP books using each standard’s profit elimination rules [8]. This level of automation was cited as drastically speeding up closings (from weeks to hours in one case) and enhancing transparency [15].

Reporting and Close Process

Each book can be “closed” independently. For instance, the company may close the PCG book (for local tax/statutory deadlines) and then make a few IFRS adjustments (in the IFRS book) before generating IFRS financials. NetSuite keeps separate retained earnings and period results per book. Financial reports (balance sheet, income statement) can be run per book. The France Localization provides preset layouts: under Reports > France Reports > Country-Specific Reports, a user can run the France Balance Sheet (Bilan) and France Income Statement (Compte de Résultat) that pull from the PCG book using legal layouts [9] [10]. Meanwhile, the IFRS book has its own report layouts (often a multi-column balance sheet or cash flow statement) designed by the finance team to meet IFRS formatting. In effect, NetSuite acts as the single source of truth: the same transactions feed both local GAAP and IFRS statetements, eliminating spreadsheet reconciliations.

When all books are closed, NetSuite’s OneWorld Consolidation engine consolidates the subsidiary ledgers under the designated holding company hierarchy. Multi-Book ensures that each book’s balances (for example, each subsidiary’s IFRS book) roll up according to IFRS elimination rules, while local PCG books remain for local reporting. Unexploded eliminations can be posted book-specifically as well. The result is that the corporate controller can produce consolidated IFRS statements alongside individual country GAAP results from the same system.

Statutory and Managerial Reporting in Practice

French Statutory Reporting (PCG)

For statutory compliance, NetSuite’s France Localization provides a Country-Specific Reports (CSR) suite. This includes predefined reports for the PCG books: Bilan (Balance Sheet), Compte de Résultat (Income Statement), and SIG (Soldes Intermédiaires de Gestion). Each CSR report has a row layout matching the official 9-column structure mandated in France. For example, the Income Statement shows revenue, COGS, gross profit, operating profit (EBIT), etc., in the French nomenclature. The layout maps PCG account number prefixes to each line. Oracle’s guide explains that after enabling the France Localization module, you can “assign row layouts for France Income Statement reports” and customize columns to meet French legal format [9]. The CSR Details documentation explicitly lists the France Balance Sheet and Income Statement reports and even the SIG (a supplementary report unique to French GAAP) [10].

In practice, a French subsidiary in NetSuite will have its PCG accounts coded (often with 3-digit classes: 1xx assets, 2xx liabilities, 6xx expenses, etc.) and tagged with the French report categories. Then running Reports > France Reports pulls up the formatted statutory statements. As Oracle warns, you must “assign a France-compliant layout” to get a legally accurate report [16], but once done, the figures come directly from the base book GL. Users can drill on each line to see which accounts feed it (the CSR Details doc notes that each report indicates which account prefixes are included) [10]. Because these are built-in, the PCG statutory reports update automatically after each PCG close, simplifying local audit and filing.

Example Table: France PCG vs IFRS Reporting

To illustrate, consider a comparative listing of major financial statements under each framework:

| Report Area | French GAAP (PCG Statutory) | IFRS (Consolidated) |

|---|---|---|

| Balance Sheet | Bilan – Assets (Actif) and Liabilities (Passif) by PCG classes (Source: accounting.auditchain.finance) | IFRS BS – Assets, Liabilities, Equity with split for parent share (Source: accounting.auditchain.finance) |

| Income Statement | Compte de Résultat – sales (Classe 7), COGS (Classe 6), EXCEPTIONAL items undefined under IFRS (Source: accounting.auditchain.finance) | IFRS IS – revenue, expenses by nature or function, no “extraordinary” line |

| Supplementaries | Soldes intermédiaires de gestion (SIG) – e.g. margin, EBITDA etc. | IFRS – often no mandated SIG; management may present similar subtotals but not prescribed. |

| Completion Deadline | Within 6 months of year-end (non-listed companies) – extended if listed | IFRS: UK/US SEC filers do Q/E reporting; EU listed at least annual/full-year by 4-6 months after year-end. |

Table 2 (above) contrasts key elements of statutory PCG reporting with IFRS. Note that French GAAP includes items (like SIG subtotals) not standard in IFRS. The mapping of balances for each often relies on the multi-book setup described.

Consolidated IFRS Reporting

On the IFRS side, companies typically consolidate after all subsidiary books are closed. Multi-Book ensures that the IFRS book of each subsidiary is aligned. Consolidation can be done in NetSuite or via an external tool consuming NetSuite data; either way, IFRS-specific eliminations (e.g. parent dividends, intercompany loans) can be generated as book-specific elimination entries. NetSuite’s built-in consolidation features (if used) will automatically eliminate intercompany transactions tracked in each book. For example, as one case noted, an intercompany product sale between a US branch and the French parent was eliminated “in both books by the same system, honoring the differing profit-elimination rules under IFRS vs GAAP” [8]. This implies that the IFRS book eliminated the inter-company profit in line with IFRS consolidation rules, while the PCG adjustments (for example, if IFRS required more or less elimination than French GAAP) are applied in its books. NetSuite’s push-button closing, combined with saved financial report templates, made what was once a laborious Excel process into an automated report run [15].

In summary, NetSuite provides a comprehensive statutory reporting solution for France (PCG formats) alongside full consolidation capability for IFRS. Finance teams can generate legally compliant local statements from the base book (e.g. via the CSR reports [10]) and generate IFRS statements from the IFRS book, all within one unified system.

Data Insights and Benefits

Quantitative data underscores the need for robust multi-ledger systems. The BlackLine survey mentioned above [7] found nearly 40% of CFOs do not fully trust their financial data. Manual reconciliations, last-minute adjustments, and reliance on spreadsheets were cited as root causes. NetSuite’s multi-book approach directly addresses these pain points by automating the parallel-standards process. In an IFRS context, data from multinational users (e.g. NetSuite case studies) consistently report dramatic efficiency gains. For instance, in one multinational implementation (EuroManufacture Ltd.), the finance team went from “running Excel macros for days” to eliminate intercompany profits to generating consolidated IFRS statements in a few hours [15]. Another midsize global firm (GlobalTech Inc.) eliminated manual data exports entirely: after implementing NetSuite Multi-Book, its CFO stated that what used to take two different systems and lots of spreadsheet work is now “all financial statements … run directly from NetSuite per book” [12].

Research in accounting adoption also supports our analysis. Academic studies of IFRS adoption (e.g. Chua et al., 2016) indicate that after mandatory adoption, firms often face substantial workload changes but ultimately benefit from comparability and foreign investment [6]. The IFRS Foundation emphasizes worldwide momentum toward a single high-quality standard, with most major economies on board [6]. For French companies specifically, the combination of IFRS for external investors and PCG for domestic stakeholders is a unique dual-reporting scenario. NetSuite’s solution is one of the few ERP systems designed to handle this comprehensively.

Case Studies and Examples

Case Study: GlobalTech Inc. (U.S. HQ, EU Subsidiary) [17] [12]. GlobalTech was a US-listed SaaS company (US GAAP primary) with a fast-growing EU arm required to report in IFRS. Initially they ran two separate systems and manually reconciled intercompany transactions. After implementing NetSuite OneWorld: they defined US GAAP as the primary book and added a secondary IFRS book. Every sales invoice posted in NetSuite hit both books (with IFRS revenue recognized slightly differently under IFRS 15) [12]. The net result was that the global finance team could close each month with automated intercompany matching and ledger balances. The finance VP noted that the time saved (by avoiding spreadsheets) was considerable.

Case Study: EuroManufacture Ltd. (French Parent, US Branch) [18] [8]. A French manufacturing group with a large US subsidiary needed to report consolidated accounts in EUR/IFRS, and also maintain US GAAP books (for SEC reporting and taxes). Using NetSuite Multi-Book, EuroManufacture set up the European parent with a primary IFRS book (EUR) and a secondary US GAAP book (USD). They mapped accounts such that inventory and cost of goods sold reconciled under both standards. NetSuite’s currency management handled EUR-USD translations. Crucially, when an intercompany sale occurred, the ERP automatically eliminated the intercompany profit appropriately in each book [8]. The result: IFRS consolidation became nearly instantaneous. The company’s CFO exclaimed that “We never lose visibility on what book any entry affects” and that financial consolidation now takes hours, not weeks [15].

These examples illustrate that NetSuite Multi-Book can be configured successfully for entities with French GAAP statutory books and IFRS secondary books. While the above cases did not focus on a PCG book specifically, the same principles apply if the primary book follows PCG rules. NetSuite consultants report that rollout involves mapping the local chart of accounts to IFRS categories, enabling the Multi-Book feature, and testing transaction flows. In practice, companies often begin by enabling Adjustment-Only IFRS books so as not to double-enter transactions. Then, through journal entries, they apply the known differences (e.g. depreciation reclassifications, tax provisions). Over time, more rules (like revenue recognition schedules) can be made adaptive across books to fully automate the divergence.

Implications and Future Directions

The ability to report under multiple accounting standards is only becoming more crucial. In France, any expansion of IFRS requirement (for example, if regulators ever mandated IFRS for larger private firms) would further increase the load. Meanwhile, IFRS itself evolves: recent standards—IFRS 16 (leases), IFRS 15 (revenue), IFRS 9 (financial instruments)—have already required companies to overhaul how they track leases, contracts, and loan impairments. NetSuite must adapt its multi-book engine to these changes (which it has done; for instance, automated IFRS 16 entries can be configured in the IFRS book). Looking ahead, the IFRS Foundation’s new sustainability standards (IFRS S1/S2) may likewise need multi-book support for ESG metrics in the financial system.

For IT and finance leaders, the multi-book approach raises questions of data governance. All these books rely on a single underlying dataset of transactions, so it is critical that master data (customer accounts, intercompany partners, items, etc.) be synchronized across books. Luckily, NetSuite’s architecture inherently shares master lists across books (“book-generic” records [19]), so maintaining consistency is more straightforward than in disparate systems. However, companies must train local and group accountants on the dual methodology, and carefully define the conversion adjustments.

The future likely holds more integration: many software vendors now see multi-GAAP support as a must-have. Mature deployments of NetSuite Multi-Book often integrate with consolidation tools (like OneStream or Copilots) for IFRS, tying the ERP data to specialized reporting. Machine learning and AI may further ease mapping and reclassification tasks (for instance, automatically suggesting how a new French account should map to IFRS lines). The CFO of one multi-national noted that moving to Multi-Book “improved transparency” not only for auditors but also for internal decision-making – a path others are sure to follow.

Conclusion

NetSuite’s Multi-Book Accounting provides a robust solution for French companies facing dual-reporting requirements. By maintaining synchronized PCG and IFRS ledgers, the platform eliminates much of the manual burden of reconciliations and enabling timely statutory and consolidated financials. Companies can configure each book to reflect the nuances of French GAAP vs IFRS (see Table 1) and rely on built-in French report layouts to produce compliant statutory statements [9] [10]. Empirical evidence from CFO surveys and early adopters confirms that this approach strengthens data accuracy and accelerates close cycles [7] [15]. As accounting standards evolve and globalization deepens, multi-book solutions like NetSuite’s will likely become increasingly indispensable for multinationals with French operations.

References: The information in this report is drawn from Oracle NetSuite documentation [3] [5] [4] [9] [10], IFRS Foundation resources [1] [2] [6], and industry reports and case studies [7] [8] [12]. Data points and differences are supported by these sources and best-practice guidelines in multi-GAAP accounting.

External Sources (19)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.