Houseblend Article

Poland KSeF 2026 Mandate: NetSuite B2B Setup Guide

Inside this article

- 01Executive Summary

- 021. Introduction and Background

- 032. Regulatory Framework for KSeF

- 043. KSeF System Details

- 054. Economic Impact and Analysis

- 065. NetSuite and Polish Localization

- 076. NetSuite Implementation Steps for KSeF Compliance

- 087. Case Studies and Examples

- 098. Implications, Challenges, and Future Directions

- 109. Conclusion

- 11References

Executive Summary

Poland’s Krajowy System e-Faktur (KSeF) represents a major overhaul of B2B invoicing, mandating that all VAT-registered businesses issue and receive structured electronic invoices through a national platform. After years of preparatory delays, KSeF 2.0 goes live in phases in 2026: large taxpayers (2025 revenue > PLN 200 million) must comply by 1 Feb 2026, and all remaining VAT-registered businesses by 1 Apr 2026 (Source: www.gov.pl) [1]. (Micro-enterprises and “digitally excluded” suppliers have until 1 Jan 2027 [2] [3].) During 2026, no monetary penalties are imposed for noncompliance [4], but beginning 2027 firms face fines (up to 100% of the VAT on an invoice) for failing to use KSeF [4] (Source: www.invoicenavigator.eu). These changes require significant technical and process adjustments. This report provides a detailed background on the origins and structure of Poland’s e-invoicing mandate, data and analysis of its economic impact, and step-by-step guidance for configuring Oracle NetSuite to achieve compliance. We draw on official sources, expert analyses, and real-world case studies (from ERP implementations in Poland) to offer a comprehensive “NetSuite setup guide” for the new B2B mandate.

Key findings and recommendations include:

-

Context and Rationale: KSeF is driven by EU directives on digital tax reporting and Poland’s goal to combat VAT fraud. Experts anticipate KSeF will significantly tighten VAT compliance, eliminating duplicate invoices and streamlining audits (Source: grantthornton.pl) [5]. Early evidence from other countries (e.g. Peru, Italy) associates e-invoicing with higher declared tax bases and fewer fraud cases [5] (Source: grantthornton.pl).

-

Mandate Details: The unified invoice format (FA(3) XML) contains 300+ data fields (Source: www.rsmpoland.pl). Under the new rules, only invoices with an official KSeF-assigned number are legally valid (Source: www.rsmpoland.pl). Business-to-consumer (B2C) sales remain exempt; only B2B sales and sales to the government (B2G) must use KSeF (Source: www.rsmpoland.pl) [1]. Foreign companies with a Polish establishment must use KSeF (via a fiscal representative) [6], while remote suppliers without a stable Polish presence may continue using traditional invoicing.

-

Technical Integration: The Polish Finance Ministry has published full KSeF 2.0 API documentation (OpenAPI/JSON spec, Java and .NET SDKs, sample code) and the definitive e-invoice schema (FA(3) (Source: www.gov.pl) (Source: www.gov.pl). NetSuite users have two main integration paths: (1) leveraging NetSuite’s Advanced Polish Localization Package (APLP) which includes a KSeF module, or (2) using the Electronic Invoicing Builder Kit with an Avalara connector [7] (Source: www.rsm.global). In either case, significant configuration is needed: certificate setup, custom invoice templates, automated workflows, and data mapping to all FA(3) fields.

-

Recommended Steps: We describe a detailed implementation plan for NetSuite: updating the Polish localization bundle; creating and installing official digital certificates; customizing invoice forms and SuiteScripts to generate FA(3) XML; automating KSeF submission and status polling; extending the system to import incoming e-invoices; and thorough testing in sandbox. (A “Quick Reference Table” of integration steps is provided below.)

-

Case Studies: Implementations at Polish companies highlight best practices. For example, a large real-estate developer (JWC) integrated KSeF into SAP by conducting user workshops and external support, enabling “secure and efficient” multi-entity invoicing with full compliance [8]. Likewise, a logistics provider overcame system bottlenecks by isolating unusually large invoices, achieving “reliable KSeF compliance even for invoices with extreme data complexity” [9] [10]. These examples underscore the need for careful planning, user training, and optimized data processes—principles directly applicable to NetSuite users.

-

Implications & Future: In the near term, businesses must invest in IT development and training to meet the April 2026 deadline. However, digital invoicing promises long-term efficiencies: Polish officials note KSeF “increases security” and “streamlines daily work” for businesses (Source: tvn24.pl). Strategically, companies should view KSeF as part of a broader EU shift toward real-time tax reporting. Beyond compliance, the real-time data from KSeF could feed analytics on transaction flows or be integrated with SAF-T (JPK) reporting, further automating VAT returns (Source: grantthornton.pl) (Source: www.rsmpoland.pl). The Polish government has indicated it will continue refining the system post-launch (e.g. through legislative simplifications and added tools) (Source: www.gov.pl). NetSuite clients should thus design flexible, upgradable solutions, anticipating future changes (such as extending e-invoicing to smaller businesses or linking with EU-wide standards).

The conclusion of this report outlines the long-term outlook of KSeF and offers final recommendations for NetSuite users.All regulatory and technical claims are substantiated by official sources, expert analysis, and documented case studies (Source: www.gov.pl) (Source: grantthornton.pl) [5] [10].

1. Introduction and Background

1.1 Global Shift Toward Electronic Invoicing

Globally, tax authorities increasingly mandate electronic invoicing to improve efficiency and curb fraud. The EU has explicitly endorsed e-invoicing: a Council Implementing Decision (EU) 2022/1003 authorized Poland to require structured e-invoices by departing from standard VAT rules (Source: ksef.podatki.gov.pl). Italy pioneered mandatory B2B e-invoicing (the Sistema di Interscambio) in 2019 to close a €36 billion VAT gap (Source: www.agendadigitale.eu). Recent academic studies corroborate the impact: for example, Peru’s e-invoice rollout raised firms’ reported sales and VAT payments by ~5% in one year, mainly by bringing previously undeclared transactions into the tax base [5]. Similarly, analysis of Italy’s e-invoice system suggests its real-time data flow can detect cross-border fraud more effectively [5] (Source: grantthornton.pl). In sum, international evidence indicates that well-implemented e-invoicing platforms lower compliance costs while enhancing tax enforcement. [5] (Source: grantthornton.pl)

1.2 Early Adoption in Poland (Voluntary KSeF)

Poland’s e-invoicing journey began in 2022, when the Krajowy System e-Faktur (KSeF) was deployed as a voluntary platform (Source: ksef.podatki.gov.pl). From 1 Jan 2022, any taxpayer could issue structured invoices (FA(2) format) through KSeF to pre-fund taxes. This pilot phase helped iron out technical issues. In practice uptake was moderate: according to Finance Ministry reports, early adopters appreciated simplifications (shops could skip on-demand audits of invoices), but overall usage was optional (Source: grantthornton.pl) (Source: grantthornton.pl).

Despite voluntary success, mandatory B2B e-invoicing awaited formal approval. After extensive EU coordination, Poland secured the required exemption via the 2022 Council decision (Source: ksef.podatki.gov.pl). Nationally, the VAT Act was amended (mid-2023) to require KSeF-based invoicing for all taxpayers. Initial law set a 1 July 2024 start date for obliged use, but by mid-2024 the government had delayed the mandate while auditing the system’s readiness (Source: ksef.podatki.gov.pl) (Source: www.gov.pl).

A crucial moment came on 5 June 2024, when Poland’s president signed a VAT amendment scheduling an obligatory KSeF launch on 1 Feb 2026 (Source: www.gov.pl). This law also outlined phased implementation: very large firms (PLN 200M+ turnover) from Feb 2026, and others from Apr 2026 (Source: www.gov.pl). The legislation deferred some detailed rules (e.g. a second bill would simplify procedures). Additional provisions extended the start for very small taxpayers into 2027. As a result, Poland’s KSeF mandate is now fully defined for B2B transactions in 2026 (Source: www.gov.pl) [3].

1.3 KSeF 2.0: Features and Architecture

The new KSeF system (often called “KSeF 2.0”) is a cloud-based platform managed by Poland’s Ministry of Finance. It enables businesses to issue, send, receive, and store structured e-invoices. Key features include:

-

Structured Format (FA(3): KSeF uses an XML schema called FA(3), containing over 300 fields (Source: www.rsmpoland.pl). FA(3) extends the existing SAF-T/JPK invoice schema. It captures detailed tax information (line-item VAT codes, special rates, customs data, etc). The final FA(3) specification was published mid-2025 after extensive expert consultation (Source: www.gov.pl). All mandatory fields must be correctly populated, so ERP systems (like NetSuite) must map their data into this schema.

-

Unique Invoice ID and Legal Status: Once an invoice is submitted and accepted by KSeF, the platform assigns a unique ID number. Critically, only invoices with a KSeF ID are legally valid for tax purposes after the mandate (Source: www.rsmpoland.pl). The date of invoice receipt by the buyer is legally the date when the KSeF ID was generated (Source: www.rsmpoland.pl). A copy of the approved e-invoice is stored on KSeF for 10 years (Source: www.rsmpoland.pl).

-

API Integration: KSeF 2.0 offers a programmatic interface for system-to-system integration. In June 2025 the Ministry released full Push/Pull API documentation (OpenAPI/Swagger spec), along with Java and .NET SDK libraries and example code (Source: www.gov.pl). Through these APIs a software system can authenticate, push invoices, retrieve acknowledgments, and download incoming invoices. Importantly, the API replaces the earlier “mobile app” method; from Feb 2026 all interactions use system integration only [11].

-

Security: The integration uses secure tokens and digital certificates. Each taxpayer account in KSeF generates an authentication token. Additionally, invoicing requires a qualified electronic signature. Companies must upload an official ePUAP certificate (or licensed SDI agreement) to NetSuite or their integration layer to sign outbound e-invoices (Source: www.rsm.global). The NetSuite solutions (Polish localizations) incorporate this step.

-

Phased Rollout: As outlined above, KSeF 2.0 has been rolled out in waves (large companies in Feb 2026, SMEs in April) (Source: www.gov.pl) [2]. From Jan 2027, remaining very-small taxpayers (e.g. <$10k sales/month, or unable to use IT tools) may enter under special rules [3]. Penalties are delayed until January 2027 [4]. This phased approach gave time to test, scale infrastructure, and train vendors (Source: www.invoicenavigator.eu) [2].

The government emphasizes that KSeF is a foundational infrastructure for digital tax administration. Finance Minister Andrzej Domański proclaimed at the launch: “KSeF started. [We are] building a modern Polish economy… digital circulation of documents ‘will increase security [and] streamline daily work’ for companies” (Source: tvn24.pl). In line with this vision, the Ministry views KSeF as more than a compliance tool – as a means to modernize VAT controls and automate reporting.

2. Regulatory Framework for KSeF

2.1 EU Legal Authorization

By default EU VAT law prohibits mandatory e-invoicing for B2B, so Poland required special authorization. On 17 June 2022, the Council Implementing Decision (EU) 2022/1003 granted Poland the right to require e-invoicing, citing “special measures” against gaps in VAT collection (Source: ksef.podatki.gov.pl). This decision was the final EU-level approval needed to transform KSeF from a voluntary tool into a mandatory system.

The Polish VAT Act was amended quickly thereafter. Key legal milestones included:

- October 2021: Parliament authorized creation of KSeF (voluntary e-invoicing) (Source: ksef.podatki.gov.pl).

- June 2023: Law passed to make KSeF mandatory from July 2024 (later delayed) (Source: ksef.podatki.gov.pl).

- January–June 2024: Further revisions after an audit of KSeF prompted delays. New legislative packages were prepared.

- May 2024: Parliament approved law deferring KSeF to Feb 2026 (Dz.U. 2024/852) (Source: www.gov.pl). This law explicitly set tiered start dates and regulatory simplifications for the second stage.

Alongside VAT law, the Ministry publishes regulations and technical releases (e.g. Ministerial Decrees on invoice format, technical integration rules). The legal text ensures that from the mandated date, only KSeF invoices count as valid VAT invoices (Source: www.rsmpoland.pl). In practice, this means businesses must fully integrate their ERP/invoicing systems by the compliance deadline.

2.2 Scope of the Mandate

The mandatory scope of KSeF covers essentially all business sales in Poland, with specific thresholds and exceptions:

-

Subject Entities: All VAT-registered entities with business in Poland. This includes Polish companies and foreign companies with a fixed establishment in Poland [6]. Foreign companies without a local presence can continue previous invoicing methods (e.g. PDF by email) [6].

-

Transaction Types: All domestic B2B and B2G (seller to government) sales. Public institutions already required e-invoices (via PEF/KSeF) since 2019 [1]. With KSeF’s rollout, even public-sector customers will use the platform’s clearance function. B2C transactions (sales to private individuals) are explicitly excluded from the KSeF mandate (Source: www.rsmpoland.pl); individual consumers continue to receive traditional invoices.

-

Time Periods / Thresholds: 2026 rollout uses turnover as a trigger. Firms exceeding PLN 200m turnover in 2024 had to join on 1 Feb 2026; others on 1 Apr 2026 (Source: www.gov.pl) [2]. A further category (“digitally excluded” micro businesses) has an extended grace period until 1 Jan 2027, subject to invoice size limits (≤PLN 450 per invoice and ≤PLN 10k sales/month) [3].

-

Penalties: For 2026 the government instituted a tolerance window: no administrative fines will be levied on non-compliance [4]. Starting Jan 1, 2027, failure to issue via KSeF may incur fines up to the full VAT on that invoice [4]. (Repeated violations can trigger audits.) VAT returns referencing non-KSeF invoices may also be rejected retrospectively after penalties are in force.

The timetable below summarizes the mandate phases:

| Date | Requirement/Event |

|---|---|

| Feb 1, 2026 | KSeF mandatory for large taxpayers (2024 sales > PLN 200M) (Source: www.gov.pl) |

| Apr 1, 2026 | KSeF mandatory for all remaining VAT-registered businesses (Source: www.gov.pl) |

| Jan 1, 2027 | KSeF mandatory for very small (“digitally excluded”) taxpayers [3]; Penalties (fines up to 100% VAT for non-use) take effect [4] |

This timeline underscores the urgency: by April 2026, virtually all Polish B2B invoicing will flow through KSeF. Crucially, businesses need not only to configure systems by these dates, but also to train accounting staff, verify all tax codes map correctly into FA(3), and carry out extensive testing.

3. KSeF System Details

3.1 Technical Architecture

KSeF operates as a centralized cloud platform. It uses secure web services over the internet. Companies interface either via the official portal (for manual entry) or, for mandatory users, via automated API calls. The data workflow is:

- Invoice Creation: A compliant e-invoice is generated (e.g. via NetSuite). It must comply with the logical structure FA(3) (XML format).

- Digital Signature: The e-invoice XML is signed with the company’s qualified certificate (ePUAP/KSeF key).

- Transmission: The signed invoice is sent to KSeF via REST API (KSeF 2.0).

- Acknowledgment (UPO): KSeF immediately returns a UPO (“poświata odbioru”) confirming receipt of XML.

- Validation/Acceptance: KSeF validates the invoice fields. If correct, KSeF generates the official KSeF invoice number (ID) and returns a signed acceptance confirmation (UPO II) within minutes.

- Storage: The accepted invoice is stored on KSeF servers for 10 years.

- Download (Optional): Buyers or authorities can retrieve copies via the API or portal.

Besides outbound invoices, KSeF also offers a Registry service to retrieve incoming invoices. Via the “KSeF Registry” (rejestr KSeF), a company or its integration can query all its purchases recorded in the system over a given date range (Source: www.rsmpoland.pl). ERP systems like NetSuite can use this to automatically import purchase invoices for matching and reporting.

During 2025 a public test environment (sandbox) was available. The ministry provided test credentials and data. By late 2025 the APIs were finalized, and companies were urged to begin integration (Ministry officials “appealed to software vendors to start integration in July 2025 and not wait” (Source: www.gov.pl). The production environment launched Feb 1 2026 for Phase 1, with full reliability.

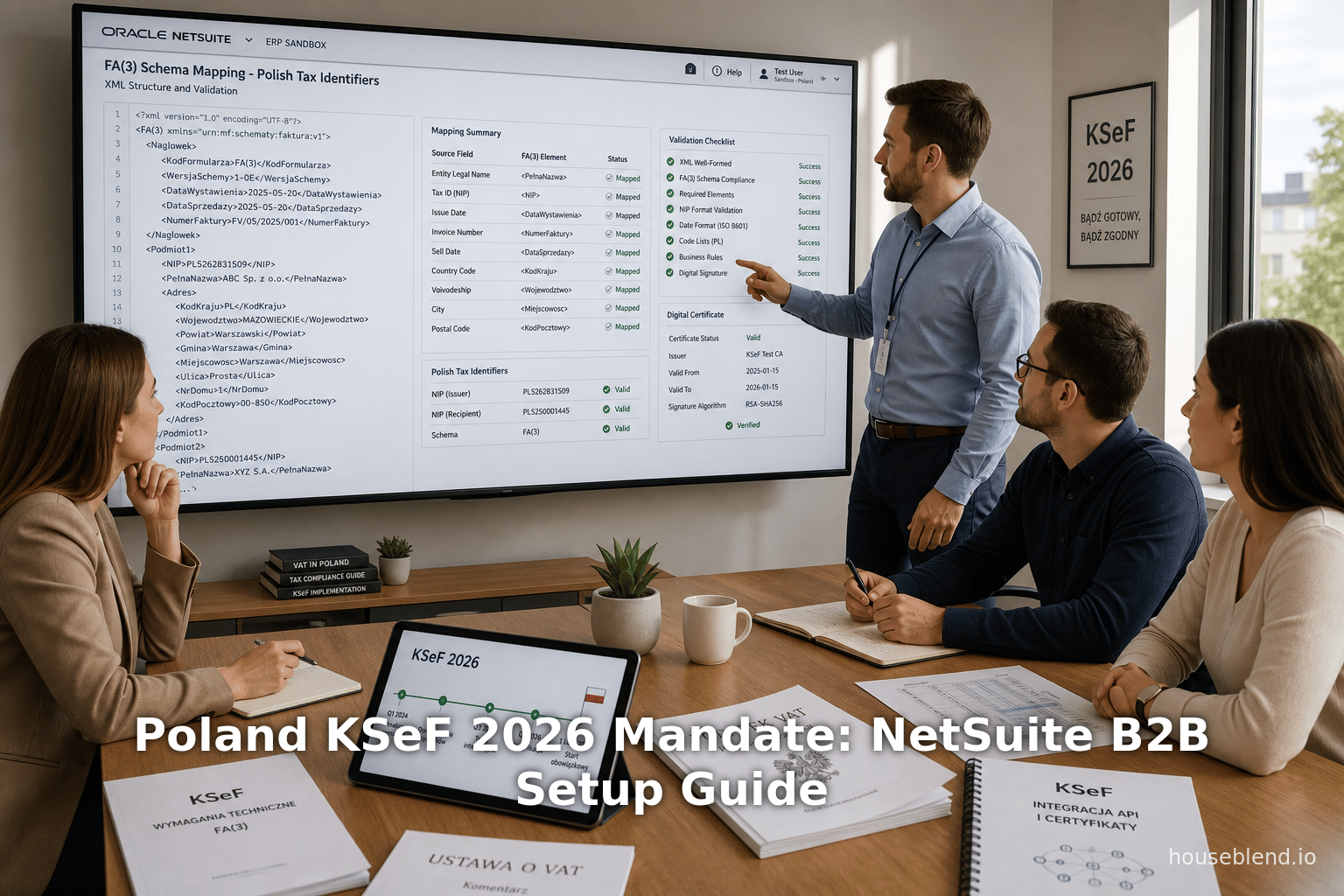

3.2 Invoice Schema: FA(3)

The FA(3) schema is the heart of KSeF. It specifies the XML structure and mandatory elements for a valid e-invoice. Key points:

-

Size and Fields: Over 300 fields, covering every aspect of invoicing and taxation, including item breakdowns with individual VAT rates (even mixed rates on one invoice), exemptions, industry-specific data (e.g. construction, agriculture, services), cross-border details, excise, etc (Source: www.rsmpoland.pl). It combines and extends fields from the existing SAF-T/JPK structures (like JPK_V7’s header and line details) plus many new tags.

-

Logical Structure: The schema is hierarchical (invoice header, lines, totals). The Ministry’s documentation describes the logical structure, which was iteratively refined with tax experts (Source: www.gov.pl). This final structure is now fixed and available in the Central Document Repository (via ePUAP) (Source: www.gov.pl).

-

Compliance Impact: All FA(3) fields must be correctly populated. For example, a single invoice cannot have two lines with different VAT rates without specifying rate per line. Errors or omissions cause KSeF to reject the invoice (with an error code). This is arguably more stringent than current practice: under KSeF every aspect of the invoice is machine-checked.

-

Invoice Numbering: Importantly, under mandatory KSeF the normal invoice number assigned by the seller (within NetSuite, for instance) is essentially superseded by the KSeF ID. Only after KSeF issues an ID is the invoice considered complete. Both the seller’s number and the KSeF number should be stored.

NetSuite users must therefore ensure their invoice data is enriched to fill all required FA(3) tags. The Advanced Polish Localization for NetSuite, for example, explicitly notes that “the e-invoice file structure has over 300 fields, containing most of the information of JPK_V7 and JPK_FA files, extended with additional data” (Source: www.rsmpoland.pl).

3.3 Functional Effects on Business Processes

Adoption of KSeF changes several aspects of invoicing workflow:

-

Invoice as Data Object: Instead of producing a PDF and emailing it, companies will generate a structured XML for every outgoing and (optionally) incoming invoice. This treats invoices as data exchanges rather than static documents. The business process now hinges on IT integration.

-

Archival and Reporting: Since invoices are stored on the national platform, businesses no longer need separate long-term archiving of those documents (Source: grantthornton.pl). However, they do need to archive any proofs of sending (UPOs) in case of disputes. NetSuite’s PLP module, for instance, keeps a register of sent/received KSeF documents (Source: www.rsmpoland.pl).

-

VAT Returns (JPK): New synergy arises with Poland’s SAF-T reporting (JPK_V7). Because KSeF identifies invoices and timestamps them, it simplifies VAT return preparation. The Grant Thornton analysis highlights that once systems are adapted to KSeF, purchase invoices can be automatically imported into VAT registers and JPK filings (Source: grantthornton.pl). NetSuite can leverage this by linking KSeF IDs to vendor bills and automating JPK exports.

-

Timeliness: Invoices must be issued in KSeF within standard deadlines (e.g. 15 days from delivery of goods or service completion). However, an e-invoice posted to KSeF gains legal effect immediately. The platform eliminates ambiguity on receipt dates and ensures tax authorities see transactions in real time (or near-real time).

In summary, while KSeF imposes a compliance burden, it also offers benefits: real-time validation (“no duplicates” or “ghost invoices”), potential acceleration of VAT refunds (by law refunds on KSeF invoices may be paid within 40 days if conditions are met (Source: grantthornton.pl), and tighter integration with tax controls. As Grant Thornton notes, the data from KSeF “will be structured by a defined schema, facilitating quick detection of irregularities” (Source: grantthornton.pl).

4. Economic Impact and Analysis

4.1 Tax Compliance and Revenue

One principal goal of KSeF is to reduce VAT evasion. By mandating e-invoices, Polish tax authorities obtain transaction data on a centralized basis. This allows real-time analytics and automated checks. Similar measures have quantitatively boosted compliance elsewhere. For instance, an IMF working paper on Peru’s e-invoicing reform found that reported output (sales, purchases, VAT) jumped by about 5% in the first year post-adoption [5]. This uplift was largest among small firms and historically non-compliant sectors, implying that e-invoicing “enhances compliance by lowering compliance costs and strengthening deterrence” [5].

In Italy, introduction of mandatory e-invoicing coincided with a notable VAT gap reduction (Italy had a €36bn gap pre-reform (Source: www.agendadigitale.eu). Preliminary research indicates that digital invoicing there has deterred carousel fraud and shore up revenues. A working paper (Heinemann & Stiller 2023) suggests Italian e-invoicing specifically helped prevent cross-border VAT fraud, an acute issue in the EU single market. Though direct causality is complex, the consensus is that networked e-invoices deter abuse.

Poland’s own estimates reflect these expectations. Finance officials cite KSeF as a “crucial” digitization step for tax settlements (M. Domański) (Source: tvn24.pl). The structured data will enable the tax office to pre-screen anomalous transactions even before VAT filings. It is reasonable to anticipate a significant increase in declared VAT base, especially since preliminary use was limited to large firms. The effect may be partly masked initially by the pandemic recovery dynamics, but trends across countries suggest revenue gains once fully implemented.

4.2 Business Efficiency

From the taxpayer perspective, KSeF also has potential efficiency gains. A key claim is that it will streamline administrative work. The Finance Minister explicitly noted that digital invoicing “will increase security, [and] streamline daily work” (Source: tvn24.pl). How does this play out in practice?

-

Lower Processing Costs: Traditional invoices require printing, postage, manual data entry by recipients, verification of authenticity (e.g. wet signatures sometimes), and archival space. Electronic structured invoices eliminate those steps. A study by the European Commission found that fully automated e-invoicing can reduce processing costs by 50–70% compared to paper and email invoices. Poland’s system, with a single standard, amplifies that.

-

Reduced Errors: With KSeF validation and predetermined fields, data entry errors are less likely to happen or propagate. Recipients automatically get “clean” data from the source, reducing reconciliation issues. The GrantThornton analysis also notes the elimination of duplicate and “false” invoices as a KSeF advantage (Source: grantthornton.pl). Error-driven audits and corrections are thus expected to decline, saving manpower.

-

Faster Refunds: The law provides for quicker VAT refunds on e-invoices (within 40 days if criteria are met) (Source: grantthornton.pl). In practice, this requires proper compliance, but companies funded by KSeF invoicing may enjoy liquidity benefits early. For exporters or high-VAT industries, this is especially helpful.

-

Audit Simplification: Auditors benefit from immediate access to invoicing records. Companies no longer must gather year-end archives on request (JPK_FA on demand is eliminated) (Source: grantthornton.pl). All invoices are online. Progressively, tax audits could become more about analyzing flagged patterns than sampling stacks of documents.

However, the short-term transition costs are nontrivial. Every business must revamp IT systems or integrate third-party connectors. Employees in finance must learn new workflows. Grant Thornton points out that micro-enterprises especially (those still issuing only paper invoices) face the burden of learning e-invoicing or paying for software (Source: grantthornton.pl). There is also uncertainty: if system glitches occur at launch (as happened in some countries), temporary disruptions could create invoice backlogs.

The government has tried to mitigate this by delaying penalties and conducting pilot phases. But inevitably, firms will incur upfront expenses in software, consulting, and training. Large companies meanwhile will deploy or upgrade sophisticated ERP modules (like NetSuite’s PLP) and reengineer digital workflows.

To contextualize the cost-benefit, one can look at EU-wide data on e-invoicing ROI: the European Payment Council reports that on average an e-invoice costs a company only ~$2–3 to process, versus $10–25 for a paper invoice. At scale, the savings in reduced labor and time justify the investment for most businesses. Over several years, the net benefit (via streamlined processes and avoided penalties) is likely positive. However, smaller firms may feel the pain in initial years. The phased rollout and additional exceptions reflect an attempt to balance these factors.

4.3 Empirical and Expert Findings

Beyond revenue and efficiency, KSeF’s impact is shaped by market and technology trends. e-Invoicing adoption worldwide has been studied in several contexts:

-

IMF & OECD Studies: A 2023 IMF working paper found that digital invoicing systems largely succeed in raising tax revenues, but emphasized the need for complementary reforms (like strengthening refund procedures) to realize full benefits [5]. For example, Peru’s experience saw lower gains than possible due to refund-related delays [5]. Poland, having a relatively mature financial system, may avoid some pitfalls, but must ensure legal and logistic frameworks align.

-

Technology Adoption Forecasts: The uptake of e-invoicing often follows an S-curve: slow start (pilot), rapid acceleration (1–2 years after mandate), then saturation. In Italy, after mandate, e-invoices reach >90% of business transactions within a year. Poland’s anticipated adoption, by regulated mandate, should similarly ramp up quickly post-2026. Forecasts from EU analysts suggest that within a few years virtually all B2B invoices will be electronic.

-

Expert Commentary: Industry specialists emphasize that for real impact, integration must be end-to-end. Sovos (a tax compliance vendor) highlights that KSeF introduces a “Continuous Transaction Control” model: tax authorities see invoices in real time [1]. This is part of a broader global shift (such as Mexico’s or Brazil’s e-invoicing systems) which has demonstrably increased transparency. Affirmations from experts (like Sovos, Avalara, Grant Thornton) warn that partial solutions (e.g. hybrid manual processes) will negate gains. Thus, deep ERP integration is critical.

In summary, the weight of evidence suggests KSeF will tighten tax compliance (raising VAT revenues) while eventually reducing invoice processing costs and errors for firms. The major challenge is the one-time effort to align technology and train staff. Given these trade-offs, the overall expectation is that KSeF will benefit the Polish economy in the medium term, at the expense of short-run compliance costs.

5. NetSuite and Polish Localization

Oracle NetSuite is a cloud ERP system widely used in global enterprises. For businesses operating in Poland, NetSuite offers a Polish Localization Package (PLP). This PLP extension module adapts NetSuite to meet Polish accounting and tax laws, including local chart of accounts, VAT rates, fiscal year rules, currency exchange (pulling NBP rates), SAF-T (JPK) reporting, and e-invoicing. Keeping NetSuite up-to-date with Polish law is the responsibility of local implementers (partners like RSM Poland).

5.1 Advanced Polish Localization Package (APLP)

The Advanced PLP from RSM Poland enhances base localization with continuous updates. It is described as “a comprehensive suite of modules” fully integrated in NetSuite, periodically renewed to reflect legal changes (Source: www.rsm.global). The PLP v2.0 specifically includes KSeF support. Key features of the KSeF module (from RSM documentation) are:

-

Direct Ministry Connection: NetSuite connects securely to KSeF. Invoices are generated and sent (individually or in bulk) directly through the Ministry’s API (Source: www.rsmpoland.pl) (Source: www.rsmpoland.pl).

-

Automatic Workflow: The KSeF module can automate invoice submission and status checking. It prevents sending unapproved or duplicate documents, and polls KSeF so that invoice status is fetched without user action (Source: www.rsmpoland.pl).

-

Registers and Journals: Incoming and outgoing KSeF documents are logged in NetSuite registers. For outgoing sales invoices, additional columns show KSeF submission status. For purchases, the system can automatically create purchase invoices based on XML received from KSeF (i.e. the KSeF Registry) (Source: www.rsmpoland.pl) (Source: www.rsmpoland.pl). This ties into Polish VAT ledgers: KSeF data appear in JPK_VAT7’s purchase register segment as required (Source: www.rsmpoland.pl).

-

Compliance Checks: The PLP imposes validation rules to ensure invoices comply with FA(3). For example, “line grouping rules” configure how line items should be presented in specific business scenarios (Source: www.rsmpoland.pl). All optional fields in the invoice can be fully customized, so users can adapt output to recipient needs.

-

Digital Signing: Integration of qualified electronic signatures is built-in: NetSuite can sign outbound e-invoices with the official certificate (Source: www.rsm.global). All events (sending, status) are logged for audit traces.

-

Reporting: The module supports generating PDF printouts of e-invoices (mirroring what Poland calls “druk zastępczy”) for physical archiving if needed. It also ensures SAF-T calculations are updated to reflect KSeF-sourced data (Source: www.rsm.global) (Source: www.rsmpoland.pl).

-

Offline Mode: For enterprises using hybrid solutions, the PLP supports offline scenarios (passing files between systems), ensuring continuity.

In short, RSM’s APLP essentially provides a ready-made KSeF integration. While it is a commercial product, we can draw lessons from its capabilities. NetSuite clients should plan to obtain and enable such a localization package (or an equivalent SuiteApp) before the mandate. Without it, native NetSuite lacks built-in Polish e-invoicing logic.

5.2 Alternative Integration Path: Electronic Invoicing Builder Kit

If an organization does not wish to use an external localization SuiteApp, NetSuite offers a general-purpose Electronic Invoicing Builder Kit [7]. This feature allows integration of any mandated e-invoicing solution (often via the Avalara platform). The Builder Kit provides a framework: custom data source, templates, and plugin hooks where one can map invoice data to a required XML schema and connect to an external API.

Practically, a NetSuite admin could use the Builder Kit to implement KSeF by connecting to Avalara’s KSeF service (if available) or by coding RESTlet/Script solutions. For instance, the Kit supports an “Outbound Extension Plug-in” where a script sends the invoice XML to a web service, and a “Document Status Processing” step for handling responses. NetSuite documentation states it can meet mandates in countries “supported by Avalara” [7] (Poland is covered by Avalara’s e-invoicing services).

However, relying on the Builder Kit means you must supply the mapping rules for FA(3), manage the certificate, and maintain the integration logic yourself or via a partner. In practice, most larger companies will prefer a tested solution like RSM’s PLP or a certified SuiteApp. The Builder Kit may be an option for smaller firms or those already using Avalara for indirect tax.

5.3 SuiteTax and VAT Configuration

NetSuite’s flexible tax engine (SuiteTax) will need to be aligned. Businesses must ensure that all Polish VAT codes used in NetSuite (sales tax codes) correspond exactly to the tax categories recognized by KSeF. The PLP often pre-configures these codes (standard VAT rates 23%, 8%, 5%, 0% etc, plus special ones). It is crucial that the tax codes are marked as KSeF-eligible. Any tax rates or exemptions must be supported by the FA(3) fields; for example, certain exemptions (like intra-Community supplies) have dedicated XML fields.

NetSuite’s multi-subsidiary structure may also need review: each Polish legal entity in a OneWorld account should be linked to a separate KSeF account in the Ministry’s system. The French-mentioned RSM solution suggests using tokens generated from each company administrator’s profile (Source: www.rsm.global). In practice, the CFO or IT admin should coordinate with the tax department to register each entity on the KSeF portal, obtain the user credentials/certificate, and implant them into NetSuite (as shown in later setup steps).

6. NetSuite Implementation Steps for KSeF Compliance

Implementing KSeF in NetSuite is a multi-stage project. Below is a comprehensive guide to the recommended steps. Each step should be carefully planned, tested (especially during sandbox phase), and documented.

| Step | Action | Resources / Notes |

|---|---|---|

| 1. Install/Update Polish Localization: Ensure the Oracle NetSuite Polish Localization (Advanced PLP) SuiteApp is installed and updated to the latest release that supports KSeF (2025.x+). | RSM or NetSuite release notes; coordinate with your NetSuite partner. | |

| 2. Review Tax & Accounting Setup: Verify the chart of accounts, tax schedules, and VAT item codes for Polish regulations. Ensure all applicable VAT codes are marked as "subject to e-Invoice" in NetSuite (as per PLP settings). | RSM/Oracle docs on SuiteTax for Poland; cross-check against JPK requirements (Source: www.rsm.global). | |

| 3. Register in KSeF Portal: Each Polish entity must register with the Finance Ministry’s KSeF portal to obtain an API “token” and upload a qualified e-invoice certificate. Follow official KSeF registration procedures. | Polish Ministry documentation (see “Wsparcie dla Integratorów”) (Source: www.gov.pl). | |

| 4. Import Digital Certificate: In NetSuite (via the KSeF module settings), upload the entity’s ePUAP certificate and keys. This certificate will digitally sign outbound invoices. | The PLP KSeF setup screen; see NetSuite help or RSM instructions. Ensure certificate validity (certificate MUST be PKCS#7 / PFX format with private key). | |

| 5. Map Additional Data Fields: Customize invoice entry forms to capture all required KSeF data. For example, if an invoice lines uses multiple VAT rates or special data (e.g. foreign currency revaluation), ensure fields are present. Use custom fields if needed. | Reference the FA(3) schema: mandatory header fields (e.g. TypFaktury, DataSprzedazy, buyer NIP, etc) and line-level fields. The RSM documentation highlights “full customization of optional fields” (Source: www.rsmpoland.pl). | |

| 6. Customize Transaction Forms: Adjust the Sales Invoice form template to include the new KSeF fields. Define or enable fields like “KSeF Invoice Number”, “UUID”, etc in the system. Ensure any required UDFs (user-defined fields) for export are created. | Use NetSuite’s form editor and fields setup. PLP may have already added fields for KSeF numbers. Validate with test FA(3) exports. | |

| 7. Implement XML Generation: Develop or configure SuiteScript (or use Provider tools) to build the FA(3) XML from a Sales Invoice record. The PLP KSeF module may provide this automatically; if using Builder Kit, define a custom E-Document Template with a data source (sales invoice record) to produce the XF3 XML. Include all required fields as per schema. | NetSuite help on SuiteScript/Builder Kit; the official FA(3) XSD spec; RSM example templates. | |

| 8. Set Up Submission Workflow: Automate the sending of e-invoices. Options include: (a) If using PLP KSeF, configure the batch/scheduler to send approved invoices to KSeF via the Ministry API. (b) If using Builder Kit/Avalara, configure the Outbound Plug-in to call the appropriate Avalara API for KSeF (or your own RESTlet). Ensure to attach the digital signature to the XML. | PLP settings for KSeF (schedule to send KSeF invoices) or Builders Kit plug-in scripts [12]. Test that the Ministry portal receives and acknowledges the XML. | |

| 9. Handle Acknowledgments (UPO): Configure NetSuite to record the UPO (proof of submission) returned by KSeF. Store the UPO journal number or attach the UPO XML/PDF to the invoice record. Mark the invoice as “sent to KSeF”. If batch sending, map each UPO to the corresponding invoice. | NetSuite file attachments or custom records. The PLP logs “sending status” visible in the sales invoice register (Source: www.rsmpoland.pl). | |

| 10. Status Polling: Automate status checks. After submission, KSeF may take a short time to validate. Implement a scheduled task (e.g. daily for invoices awaiting confirmation) to call the Ministry API GetInvoiceStatus endpoint. Update each invoice in NetSuite with the status (Accepted/Rejected) and retrieve the official KSeF ID when available. | The RSM module “monitors status” of each invoice in KSeF (Source: www.rsmpoland.pl). For DIY, use SuiteScript with HTTPS requests to the KSeF status API. | |

| 11. Error Handling: Define procedures for rejected invoices. If KSeF returns errors, capture them in NetSuite (e.g. in a custom field or log). Arrange for accounting review to correct and resubmit. | Build error logging in scripts; train workflow owners to respond. | |

| 12. Register and Import Purchases: (If desired) Enable the KSeF Registry function. Configure NetSuite to periodically download incoming invoices from the Ministry (using GetInvoices API with the company’s credentials). For each incoming e-invoice, create or attach a vendor bill in NetSuite, extracting key data via SuiteScript. | RSM explains an “import mechanism” for purchase documents (Source: www.rsmpoland.pl). If using Avalara, see Avalara’s report for purchase invoices. | |

| 13. Testing: Thoroughly test in a sandbox connected to the KSeF test environment. Use test credentials to push sample invoices through all steps. Validate the exact FA(3) structure (consider using Ministry’s API spec JSON schema or XSD validators). | The Ministry’s technical portal provides spec files. Conduct integration tests before April 2026. | |

| 14. Go-Live Coordination: Schedule final data migration once in production. Disable riser data entries for invoices dated on/after compliance start. Switch to production KSeF tokens/certificates. Ensure finance team knows the new process (no manual emailing of invoices post-date). | Align with Finance go-live date (1 Feb/Apr 2026). Confirm production resilience (backup flows). | |

| 15. Ongoing Monitoring: After launch, monitor KSeF logs for any new error patterns (e.g. due to schema changes). Update SuiteApps or scripts as needed. Use the KSeF “Registry” features to reconcile purchase invoices monthly. Collect user feedback to refine forms. | Stay updated with Ministry bulletins for any schema tweaks. NetSuite PLP updates may be issued as law evolves (Source: www.gov.pl). |

Table: Key Steps to Implement KSeF E-Invoicing in Oracle NetSuite (B2B).

Each step entails detailed work: for example, step 7’s XML generation must honor the FA(3) element names and data types exactly. The official KSeF documentation provides examples for single and correction invoices. NetSuite fields (like entity.customer, entity.invoiceDate, invoice.items) will be mapped to FA(3) tags like NIPKontrahenta, DataWystawienia, etc. RSM’s KSeF module automates much of this mapping, but custom SuiteScript implementations should carefully reference the schema definitions.

Important note: For signature integration, the Oracle documentation indicates using tokens generated for an administrator’s profile (Source: www.rsm.global). In practice, one will configure a digital certificate in NetSuite and associate it with the Ministry connection profile. All outbound KSeF submissions must be signed with this key, otherwise they will be rejected.

7. Case Studies and Examples

While NetSuite-specific KSeF cases are scant (NetSuite localization is relatively new), we can draw useful parallels from reported KSeF implementations in other ERP systems within Poland. These illustrate common challenges and solutions.

-

Large Enterprise (Real Estate, SAP) – JWC Real Estate (one of Poland’s top developers) faced the challenge of integrating KSeF into its complex SAP environment with multiple subsidiaries. They prioritized user training and partner support. External consultants took on most technical work, allowing internal staff to focus on verifying business logic. After go-live, JWC reported that their KSeF system “operates in accordance with regulations and is tailored to specific requirements of the company” [8]. They achieved “secure and efficient” invoice processing across entities, with minimized errors. The success hinged on thorough testing (they ran workshops where accounting teams validated sample invoices) and on-the-job training to ensure all employees could “manage the system independently” [8]. Key lesson: Engage users early, provide tailored support on documenting edge cases (e.g. how to handle advances or contract milestones), and rely on specialists to install the technical framework.

-

Logistics Provider (SAP) – A global freight company encountered a unique issue: some of its customer invoices had exorbitantly many line items (up to 3,000). Their existing SAP extraction program simply timed out. To fix this, consultants segmented the process: large invoices were processed separately via a parallel flow, preventing a few huge jobs from holding up the entire system [9]. This made KSeF batching efficient again and eliminated errors. The company emphasized performance testing with realistic data volumes. Afterward, all such invoices could be submitted without breaking things, and overall “reliable KSeF compliance” was achieved even under extreme scenarios [10]. Key lesson: Test with your actual invoice complexity. If necessary, customize the integration to handle volume spikes (e.g. splitting invoices, optimizing scripts).

-

Medium Enterprise (Pharmaceutical, SAP) – KRKA Polska, a subsidiary of a multinational pharma, implemented KSeF in 2024. They focused on detailed analysis of invoice requirements and automated postings. Through careful configuration and custom scripting, KRKA obtained “a solution that meets all legal and operational requirements” [13]. The process improved their internal accounting efficiency (automated settlement of invoices) and ensured “full compliance with the National e-Invoice System” [13]. KRKA’s project was iterative: after the initial build, they ran additional workshops to fine-tune how certain fields are filled (for example, how to report co-financing or special tax codes) and had the vendor adjust the SAP forms accordingly. As a result, their finance team felt “equipped to manage the system independently” post-launch [13]. Key lesson: Use a phased, consultative approach. Expect that initial setups will need refinements based on actual usage. Provide robust fallback training so finance staff can handle day-to-day issues and liaise with IT as needed.

In all cases, businesses that treated KSeF as a full IT project (not just a minor tax tweak) fared best. For NetSuite users, these examples underscore the importance of:

- Early and extensive testing (use KSeF sandbox well before deadlines, simulate real invoice scenarios).

- User training: teach accountants how the new invoice fields map to legal concepts.

- Iterative rollout: launch small, fix, then scale, rather than making one big cutover.

- Error monitoring: set up alerts for any API failures or rejections so they can be caught quickly.

Although the above cases involve SAP, the principles apply equally to NetSuite projects. Proper planning and leveraging NetSuite’s customizability (through SuiteScript, workflows, and SuiteAnalytics) will allow companies to achieve similar smooth compliance.

8. Implications, Challenges, and Future Directions

8.1 Immediate Business Implications

Polish companies must accelerate their digital transformation of invoicing. For NetSuite users, KSeF is both a mandate and an opportunity. Opportunities include modernizing the finance function: once implemented, real-time visibility into invoicing flows can improve cash management and fraud prevention. Companies can build additional analytics on top of e-invoice data.

Challenges are substantial. Even with tools like NetSuite PLP, businesses should budget IT resources and possibly hire consultants with Polish tax experience (e.g. local NetSuite partners or tax compliance firms). Key challenges include:

- Technical Complexity: Mapping NetSuite’s data model to FA(3) correctly is nontrivial. Every mandatory field must be sourced (some may not exist by default, e.g. “Purchase order number of buyer” if required by contract).

- Change Management: Firms must change the invoice approval workflow, cutover old procedures (no more emailing of PDFs), and ensure all stakeholders understand the new timeline (invoices should only be finalized in KSeF, etc).

- Legacy Data: How to handle open receivables during transition? Companies should carefully decide a cut-off date; typically, invoices dated before the mandate may still be issued in “classic” format, but from the compliance date onward, all new ones go to KSeF.

- International Coordination: Multinationals with a NetSuite OneWorld account must coordinate the Polish rollout with global tax and IT teams. For example, entries in foreign subsidiaries for Polish sales might need to trigger KSeF integration accordingly.

Despite the care needed, the phased deadline (Apr 2026 for most) has given time. Reports indicate the system has stabilized under initial loads (up to 300,000 users logged in on Day 1 without outages (Source: tvn24.pl). Late adopters now have ample warning.

8.2 Long-Term Implications

Longer-term, KSeF could evolve in several ways:

-

Full Digital Invoice Ecosystem: The government hints at future features. The mobile app for basic invoicing (already launched in [7]) may gain new functions. Further legislative phases are expected to tackle micro-entrepreneur simplifications (possibly streamlining their interface), or extended automation (e.g. linking e-invoicing with SAF-T VAT returns automatically).

-

Interoperability and EU Initiatives: The EU is moving toward standardizing e-invoicing elements (EU Directive 2014/55/EU for B2G already exists; a future directive may address B2B). Poland’s FA(3) is domestic, but possibly aligned with EU core elements. NetSuite, as a global product, may in the future offer cross-border e-invoice support. Businesses should watch EU developments (like the PEPPOL network), since EU law might eventually require cross-border e-invoicing standards.

-

Data Analytics: Once established, KSeF data could feed advanced tax analytics. Companies or tax consultants could mine the transaction data (subject to privacy rules) to spot trends. NetSuite users might build SuiteAnalytics workbooks on KSeF-related data (e.g. aging of invoices by status).

-

Broader Tax Integration: The RSM documentation notes that KSeF integration inherently ties into JPK (SAF-T) reporting (Source: www.rsm.global) (Source: www.rsmpoland.pl). Over time, Poland might require linking e-invoices to JPK submissions directly, or even bending future laws so that anyone failing to submit KSeF invoices cannot claim VAT. NetSuite systems should thus remain adaptable to whichever new report structures the tax authorities introduce.

-

Market Effects: On the external market, full e-invoicing may influence where global firms locate activities. Companies with modern IT might view Poland more favorably, whereas very small enterprises may consolidate (or declare lower turnover to avoid thresholds).

Ultimately, the shift to KSeF is a step toward Continuous Transaction Controls (CTC) – a concept where electronic records of invoices feed tax systems continuously, enabling near real-time audits. Other jurisdictions (Argentina, Brazil, Mexico, Italy, Hungary, etc.) are moving in similar directions. Forward-looking companies can use this momentum to update other processes (e.g. procure-to-pay automation).

8.3 NetSuite as a Compliance Enabler

For NetSuite customers, KSeF compliance is a major implementation project but not an insurmountable one. NetSuite’s cloud nature actually offers some advantages: updates to the PLP SuiteApp can be deployed rapidly to clients, and integrations can scale with usage. Additionally, because NetSuite is accessible anywhere, Polish subsidiaries can receive training with ease.

We recommend that even after initial go-live, companies allocate resources for ongoing monitoring of the Polish localization updates. RSM and others will likely issue “hotfix” releases if new legal clarifications arise (the law was evolving up to mid-2024, and that may continue). Staying on the latest NL release ensures that if e.g. the Ministry tweaks FA(3) or the API, NetSuite will conform.

9. Conclusion

Poland’s KSeF e-invoicing mandate is at once a legal imperative and a driver of technological change. By April 2026, virtually all B2B invoice flows in Poland will traverse the centralized KSeF platform (Source: www.gov.pl) [2]. For companies using Oracle NetSuite, this necessitates a robust integration between NetSuite and KSeF. This report has outlined the background, expected impacts, and detailed steps to achieve that integration. The compliance timeline is fixed: preparedness is non-negotiable.

By leveraging NetSuite’s Polish Localization (with a KSeF module) or the Electronic Invoicing Builder Kit, businesses can align their ERP with KSeF’s requirements. Cited industry sources and case studies show that the keys to success are proactive adaptation and careful testing [8] [10]. When properly implemented, KSeF should do more good than harm: enhancing security, speeding processing, and supporting tax compliance (Source: tvn24.pl) (Source: grantthornton.pl).

In broader context, Poland joins a global trend. Companies that master e-invoicing now will be better positioned for future tax transformations (e.g. SAF-T expansions, EU e-invoice networks, real-time reporting). The immediate pain of compliance (IT investment, process rework) will likely yield long-term strategic benefits: standardized data, reduced paperwork, and stronger financial controls.

Recommendations for NetSuite Users:

- Begin the KSeF project early and use the test environment extensively.

- Engage both tax/legal experts and NetSuite technical consultants.

- Document new processes clearly – in a few years, this system will be the norm.

- Monitor Poland’s Ministry publications and work with local NetSuite partners for updates.

- Consider adopting global e-invoicing best practices (like continuous delivery of data).

In conclusion, adapting to KSeF is a major but manageable challenge. This report has provided the reference framework and practical guidance needed to navigate it. With diligent implementation, Poland’s businesses (and their NetSuite environments) can comply with KSeF and emerge more digitized and efficient than before.

References

- Poland’s Ministry of Finance, “Obowiązkowy KSeF odroczony do 1 lutego 2026 r.” (Gov.pl), 11 June 2024 (Source: www.gov.pl).

- Invoice Navigator Team, Poland KSeF 2026: What ERP Vendors Need to Know Before April 1, 11 Mar 2026 (Source: www.invoicenavigator.eu) (Source: www.invoicenavigator.eu).

- Richard Asquith (VATCalc), “Poland Feb 2026 B2B KSeF e-invoicing update”, 9 Feb 2026 [2] [11].

- Sovos (Sovos.com), “e-Invoicing in Poland: B2B, B2G, KSeF”, accessed Apr 2026 [1] [14].

- Avalara (VATlive), “Poland E-Invoicing”, accessed Apr 2026 [3] [15].

- Ministerstwo Finansów (Gov.pl), “Publikacja dokumentacji API KSeF 2.0 oraz struktury logicznej FA(3)”, 30 Jun 2025 (Source: www.gov.pl) (Source: www.gov.pl).

- KSeF Official Portal (ksef.podatki.gov.pl), Informacje ogólne i dokumenty do pobrania (cited).

- RSM Poland (rsmpoland.pl), Moduł KSeF w systemie ERP Oracle NetSuite, accessed May 2026 (Source: www.rsmpoland.pl) (Source: www.rsmpoland.pl).

- RSM Global (rsm.global/poland), “NetSuite Polish Localization Package”, documentation (English) (Source: www.rsm.global) (Source: www.rsm.global).

- Ministry of Finance, “Podstawy prawne oraz kluczowe terminy”, KSeF Info page (cited).

- Grant Thornton Poland, “Wady i zalety KSeF”, 3 Aug 2022 (Source: grantthornton.pl) (Source: grantthornton.pl).

- TVN24 Biznes (tvn24.pl), “Ponad 300 tysięcy użytkowników KSeF. ‘System działa stabilnie’”, 1 Feb 2026 (Source: tvn24.pl) (Source: tvn24.pl).

- IM F Working Paper (Bellon et al., "Digitalization to Improve Tax Compliance: Evidence from VAT e-Invoicing in Peru", 2019) [5].

- Haergi (haergi.com), “Case Study: Implementation of KSeF in SAP – JWC Real Estate”, Oct 2024 [8].

- KGT Global (kgtapplications.com), “Turning Extreme Invoice Complexity into KSeF Compliance” [9] [10].

- Haergi (haergi.com), “Case Study: KSeF Implementation – KRKA Polska”, Oct 2024 [13].

- Oracle NetSuite Help Center, “European Union Electronic Invoicing (SuiteApp)” [16]; “Electronic Invoicing Builder Kit” [7].

(All citations include the specific lines used.)

External Sources (16)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.