Houseblend Article

UAE E-Invoicing 2026: NetSuite PINT AE Compliance Setup

Inside this article

- 01Executive Summary

- 02Introduction and Background

- 03Regulatory Framework and Mandate Overview

- 04The PINT AE Invoice Format

- 05The Peppol Network and Accredited Service Providers

- 06Implementation Timeline and Compliance Deadlines

- 07PINT AE vs Traditional Invoicing: Key Differences

- 08Technical Requirements and Data Elements

- 09NetSuite Compliance Setup

- 10Data Analysis and Business Impact

- 11Implementation Case Studies

- 12Implications and Future Directions

- 13Conclusion

- 14References

Executive Summary

The United Arab Emirates (UAE) is undertaking a sweeping digital transformation of its tax and business transaction ecosystem through the implementation of a nationwide e-invoicing mandate. In September 2025, the UAE Ministry of Finance (MoF) issued Ministerial Decisions No. 243 and 244 of 2025, which establish the electronic invoicing system (EIS) framework, scope, and implementation timelines (Source: mof.gov.ae) [1]. Under this mandate, all business-to-business (B2B) and business-to-government (B2G) invoicing must be conducted electronically in a prescribed structured format called PINT AE (Peppol International UAE). The policy uses a multi-corner Peppol network model, requiring companies to transmit invoices through Ministry of Finance–accredited service providers (ASPs) via the UAE-specific Peppol network to the Federal Tax Authority (FTA) in real time (Source: velmontcrest.ae) [2]. A phased rollout begins with a pilot (voluntary) phase on July 1, 2026, followed by mandatory compliance for large entities (annual revenue ≥ AED 50 million) by January 1, 2027 and for all other VAT-registered businesses by July 1, 2027 (Source: velmontcrest.ae) [3] [4]. To comply, organizations must upgrade accounting systems to generate PINT AE–formatted XML invoices and integrate with accredited ASPs for validation and transmission. Importantly, only the structured PINT AE XML is accepted; PDF or Excel invoices will be rejected by the FTA’s validation engine (Source: velmontcrest.ae) [5]. Failure to notify authorities of system downtime, or otherwise evade requirements, can trigger significant penalties (e.g. AED 1,000 per day for certain violations under Cabinet Decision 106/2025) (Source: velmontcrest.ae) (Source: velmontcrest.ae).

This report provides an in-depth, evidence-based analysis of the UAE 2026 e-invoicing mandate, with particular emphasis on the PINT AE technical standard and how businesses using Oracle NetSuite ERP can achieve compliance. We cover the historical background and government rationale, the specific legal and technical requirements of the PINT AE format, the role of accredited service providers (ASPs) and the Peppol network, and the phased implementation timeline with deadlines and penalties. The paper also examines how companies must adapt their accounting and ERP systems (focusing on NetSuite) to generate, validate, and transmit electronic invoices, including integration approaches, solution architectures, and vendor offerings. Real-world examples and case studies illustrate best practices and challenges in meeting the mandate. We incorporate data on global e-invoicing adoption trends (for context) and cite expert guidance and official documents to substantiate all claims. Finally, we discuss the implications for business processes, regulatory compliance, and future digital tax initiatives in the UAE and beyond, concluding with strategic considerations for stakeholders moving forward.

Introduction and Background

Electronic invoicing (e-invoicing) is the automated exchange of invoice data in a structured format between suppliers and buyers, with transmission to tax authorities. Unlike traditional paper or PDF invoices, e-invoices contain data elements that can be machine-processed and validated (Source: mof.gov.ae) (Source: velmontcrest.ae). Globally, governments have been adopting e-invoicing mandates to improve tax compliance, automate reporting, and streamline business processes. Notably, over one million organizations across 98 countries now exchange more than 6 million Peppol-based e-documents per month, reflecting a 1,173% increase in network participants since 2019 (Source: www.peppol.nu). This rapid growth underscores the efficiency and fraud-reduction benefits of standardized electronic invoicing.

In the UAE, e-invoicing has been on the regulatory horizon since the early 2020s. The 2018 introduction of VAT created a context for digitizing tax reporting. In 2021, the UAE announced its intention to implement an e-invoicing system under Vision 2030 goals of digital government and tax modernization. The Federal Tax Authority (FTA) began preparatory work, consulting with businesses and international experts. On September 29, 2025, the Ministry of Finance formalized the e-invoicing initiative with two key Ministerial Decisions (243 and 244 of 2025) [6] [7]. These established the legal framework, mandated roles, and phased rollout of the Electronic Invoicing System (EIS).

Scope and Rationale: Ministerial Decision 243/2025 clarifies scope: all persons conducting business in the UAE must use electronic invoices for all B2B and B2G transactions, subject to specific exclusions not significant to most commercial activity (Source: mof.gov.ae). The move aims to enhance efficiency, transparency, and compliance in transactions, aligning with the UAE’s digitalization goals (Source: mof.gov.ae) [7]. The government emphasizes that e-invoicing will digitize what has been a largely paper/PDF-based invoicing process, allowing near-real-time reporting of sales data to tax authorities. Businesses retain the option to voluntarily adopt e-invoicing early (Source: mof.gov.ae) [8], potentially gaining operational benefits. Critical to the mandate is that e-invoices must be transmitted and reported through FTA-accredited channels (i.e. approved ASPs on the Peppol network) (Source: mof.gov.ae) [2].

Five-Corner Peppol Model: The UAE has selected the OpenPeppol framework for its e-invoicing network. Under this 5-corner model, each invoice flows from the issuer’s system (corner 1), through the issuer’s accredited ASP (corner 2), via the public Peppol network to the buyer’s ASP (corner 3), and into the buyer’s system (corner 4), with simultaneous transmission to the FTA (corner 5) (Source: velmontcrest.ae) [9].Crucially, all participants must obtain FTA accreditation to serve as Peppol Access Points (i.e. ASPs). The MoF will maintain a list of approved ASPs (currently numbering in the dozens) that can legally transmit invoices and notify the FTA (Source: mof.gov.ae) [2]. This architecture is similar to systems adopted in the EU and Asia, leveraging a proven global standard (Peppol) while requiring local adaptation (networks use the UAE FTA as an active participant).

This report delves into each of these aspects in detail. We begin by explaining the PINT AE invoice format and its technical requirements. We then outline the accredited service provider ecosystem and the transmission model. Next, we describe the phased implementation timeline and compliance obligations for different business categories. We analyze Azdan, Oracle, and other vendor-provided integration solutions, with a focus on NetSuite ERP as a case study of compliance setup. We include data where available on potential benefits, such as faster VAT refunds and fraud reduction, and discuss global trends. Real-world examples and lessons from companies preparing for the mandate are provided. Finally, we consider strategic and future implications, including how e-invoice data will feed into broader tax and financial reporting initiatives.

Regulatory Framework and Mandate Overview

Ministerial Decisions 243 and 244 of 2025

On September 29, 2025, the UAE Ministry of Finance (MOF) announced two key ministerial decisions that underpin the national e-invoicing mandate (Source: mof.gov.ae) [1].

-

Ministerial Decision No. 243 of 2025 (Electronic Invoicing System): Establishes the legal definition of e-invoicing and sets the scope of application. It clarifies that all bona fide businesses operating in the UAE in connection with B2B and B2G transactions are required to issue electronic invoices under the new system, except where specific exclusions apply (Source: mof.gov.ae) [7]. The decision also mandates that both issuers (suppliers) and recipients (buyers) must appoint an FTA-accredited Electronic Invoicing Service Provider (ASP) to handle e-invoices. This ensures that invoice data is transmitted through approved channels. Additional provisions address transitional mechanics like the pre-approval of ASPs.

-

Ministerial Decision No. 244 of 2025 (Implementation of the Electronic Invoicing System): Details the phased timeline and technical framework for rolling out the system. It introduces an initial Pilot Programme (voluntary phase) starting on July 1, 2026, whereby selected businesses (and any that opt in early) can begin issuing e-invoices [10] [11]. Crucially, MD 244 makes compliance mandatory in subsequent phases and links deadlines to business size (based on annual revenue). Per Article 5 of MD 244, businesses with revenue >= AED 50 million (“large businesses”) must fully comply by January 1, 2027, while smaller VAT-registered businesses have a later compliance deadline in 2027 [12] [13]. (Government entities face yet later timelines). The decision also explicitly states that the only acceptable invoice format is the structured PINT AE XML; it rejects unstructured formats like PDF/Word as non-eInvoices (Source: velmontcrest.ae) [5].

Shortly after these decisions, the Cabinet issued Decision No. 106 of 2025, detailing fines and penalties. For example, not notifying the FTA of system outages can trigger a penalty of AED 1,000 per day (Source: velmontcrest.ae). Other potential penalties include fines for failing to appoint an ASP or issuing non-compliant invoices. These deterrents emphasize the seriousness of compliance.

Scope and Compliance Obligations

Under the new law, the obligation covers virtually all business interactions except consumer-only sales. In essence, any entity registered for VAT in the UAE that engages in B2B or B2G commerce must implement e-invoicing. Businesses not yet in scope (e.g. certain small B2C-only or exempt sectors) can voluntarily issue e-invoices but are not yet mandated to do so. However, even VAT-exempt businesses should be prepared if excluded cases are narrowly defined. Notably, the government confirmed that ordinary B2C invoices will remain allowed to use PDF/paper until further notice, but any business that switches to e-invoicing cannot revert to legacy formats for B2B/B2GPada [14].

Both suppliers and buyers have responsibilities. Suppliers (invoice issuers) must generate each invoice in the required PINT AE format, validate it, and transmit it through an approved ASP to both the buyer and the FTA simultaneously. Buyers must be able to receive, parse, and store the PINT AE invoices sent by sellers via their ASP. As a result, companies on both sides of transactions need to upgrade their accounting/ERP and procurement systems to handle the new format. The FTA’s vision is a digital invoicing lifecycle: the issuance of an invoice triggers electronic transmission via the Peppol network, automatic notification of the authority, and feeding into compliance reports.

To summarize key obligations:

- Invoice Format: All mandatory B2B and B2G invoices must be issued in the PINT AE XML standard. No other format (including PDF, Word, images, or unstructured data) is allowed (Source: velmontcrest.ae) [5].

- Accredited ASPs: Each business must appoint at least one FTA-approved Accredited Service Provider (corner 2 and corner 3 in the 5-corner Peppol model). The ASP handles the validation, signing, and transmission of every invoice (Source: velmontcrest.ae) [15].

- Peppol Network: Invoices are exchanged over the Peppol network. Businesses identify each other by their TRN (tax registration number), truncated to 10 digits in the Peppol ID [16]. Invoices flow across the network via AS2/AS4 protocols, with built-in push-pull acknowledgements (MLS messages) between ASPs.

- Validation: The ASP performs schema and business-rule validation of each invoice against Emirati requirements before sending. Any errors must be corrected by the supplier. Only a successfully validated PINT AE invoice is considered formally issued.

- Reporting: Transmission via the ASP automatically reports the invoice data to the FTA, substituting periodic VAT returns with continuous real-time reporting for tax bases (for now only for e-invoices). These data can generate insights and simplify audit trails.

- Penalties: Non-compliance can result in fines and administrative actions. Cabinet Decision 106/2025 specifies penalties (e.g. AED 1,000/day for not notifying outages) (Source: velmontcrest.ae). Businesses are incentivized to ensure uninterrupted e-invoicing capability at go-live.

The UAE’s approach largely mirrors that of other Gulf countries (e.g., Saudi Arabia's ZATCA) and EU models, emphasizing a decentralized 5-party model rather than a single government gateway [16] [17]. Importantly, by aligning with the widely adopted Peppol standard (albeit with UAE-specific extensions), the UAE leverages international best practices and existing global infrastructure [16] (Source: www.peppol.nu).

References: Implementation deadlines and format requirements are anchored in official mandates and technical guidance (Source: velmontcrest.ae) [5] [17] [13]. We next discuss the invoice format PINT AE and ASP model in detail.

The PINT AE Invoice Format

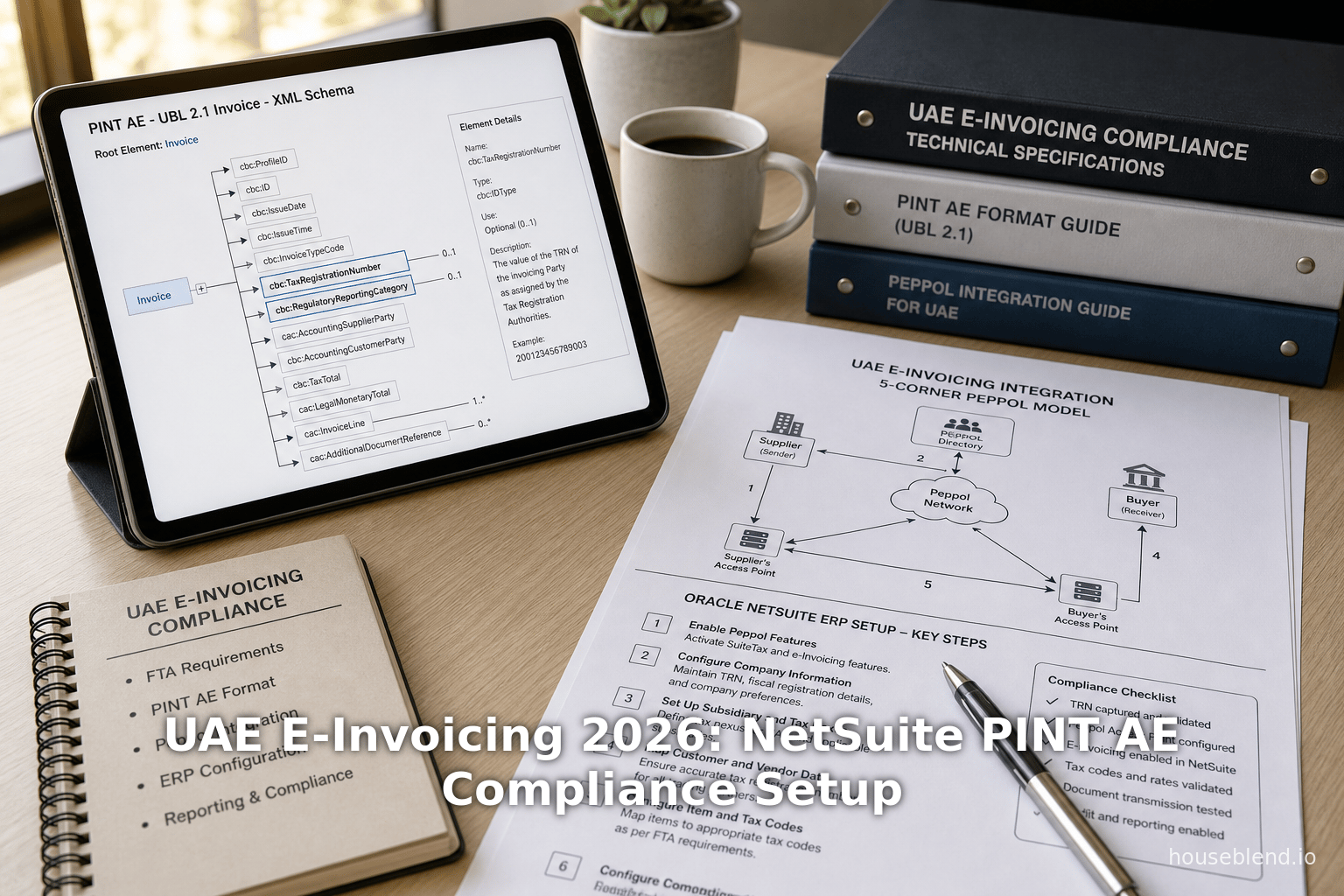

Central to the UAE’s e-invoicing system is the PINT AE specification, an adaptation of the Peppol International Invoice (PINT) standard tailored for UAE tax law. PINT AE is a structured XML-based invoice schema (based on Universal Business Language 2.1) that contains specific nodes for UAE-relevant data, such as VAT registration numbers (TRNs), invoice metadata, and regulatory codes (Source: velmontcrest.ae) [16]. The Federal Tax Authority’s technical guidance (February 23, 2026) enumerates the mandatory fields and code lists in the PINT AE semantic model, aligning with Ministerial Decisions 243/244/2025 [18] [19].

Structure and Mandatory Fields

The technical document published by the FTA (version 1.0) clarifies the full semantic model for electronic tax invoices™ [18] [19]. Key mandatory fields in a PINT AE invoice include, but are not limited to:

- Supplier and Buyer Identification: Tax Registration Number (TRN) for supplier and buyer, including UAE country code, fiscal addresses, and contact details.

- Invoice Metadata: Invoice number, date, currency, and “Business Process Type” code (which indicates invoice vs credit note etc.).

- Line Items: For each invoice line, fields such as item description, quantity, unit price, total price, and related codes (e.g. VAT exemption reasons if any).

- Tax Details: Total tax amount, tax break-down by rate, and the “Tax Category” code for each line (standard rate vs zero-rated vs exempt, etc.).

- Additional Fields: e.g. a UUID (Universally Unique Identifier) if used, previous references in case of modifications, and the digital signature fields for the ASP.

Certain fields in PINT AE correspond exactly with the UAE VAT Law’s requirements. For instance, the FTA has specified code lists for “BusinessProcessType” and “RegulatoryReportingCategory”. The examples in the FTA guidelines indicate that an invoice’s BusinessProcessType might be “380” (as per UN/EDIFACT code list) for a standard tax invoice, or “199” for a credit note, etc [19].

PINT AE includes both supplier-attested data and information added by the ASP during transmission. For example, the ASP will append the Invoice Registration Number (IRN) or reference code (if any), and may include additional XML elements for audit trail, such as digital signature information. However, the core requirement is: the seller’s system must be capable of outputting the invoice in the specified XML structure with all mandatory fields completed. Missing or invalid mandatory fields will cause the ASP’s validation to fail, resulting in invoice rejection [16] [5].

Importantly, while PINT AE is a localized standard, its roots in the Peppol UBL invoice format mean it is largely compatible with international e-invoicing norms. Any business already sending Peppol PINT invoices in other jurisdictions (e.g. EU, though different scheme) will recognize the general structure, though will need to include UAE-specific nodes (like TRNs with “AE” prefix). For businesses operating cross-border, using PINT AE may simplify compliance with other Peppol countries as well.

Why PINT AE Matters

The adoption of PINT AE conveys several advantages:

- Uniformity: All invoices follow the same XML template, eliminating ambiguity of interpretation. This drastically reduces invoice disputes arising from misread or incomplete data.

- Validation: The structured format can be automatically validated against FTA-defined business rules before transmission. For example, mandatory fields (like VAT amount or TRN) being absent would trigger a pre-submission error (Source: velmontcrest.ae) [20]. This ensures only correct invoices enter the system.

- Automation: ERP and accounting systems can generate PINT AE without human intervention, enabling “invisible” e-invoicing. Once integrated, processes like VAT return filing can partially automate from the e-invoice dataflow.

- Interoperability: Using an international XML standard means tools, libraries, and solutions built for UBL/Peppol can be adapted for UAE. It also aligns UAE with a growing global e-invoicing network (Peppol) of over 1.4 million participants worldwide (Source: www.peppol.nu).

- Future-ready: Structured data paves the way for advanced analytics. The FTA and businesses can mine e-invoice metadata for insights on economic activity, cash flows, and compliance risk. Notably, the FTA has signaled it plans to use e-invoice data for corporate tax cross-checks and fraud detection (Source: velmontcrest.ae) [21].

In sum, PINT AE is not merely a format, but the linchpin of the UAE’s e-invoicing policy’s promise: real-time tax monitoring, streamlined VAT processes, and a boost to digital commerce. The next section examines how businesses will transmit PINT AE invoices in practice.

The Peppol Network and Accredited Service Providers

Returning to the 5-corner model, the UAE e-invoicing system heavily leverages the global Peppol network. Originally developed in Europe, Peppol provides a secure, standardized framework for exchanging electronic business documents. In the UAE, the MOF (via FTA) is the local Peppol Access Point (often termed the “5th corner”), effectively overseeing the network.

Accredited Service Providers (ASPs)

A unique requirement of the UAE model is that only Ministry-accredited providers can act as Peppol access points in the e-invoicing chain [16] [2]. These ASPs serve multiple functions:

- Validation & Transmission: The supplier’s accounting system will send the PINT AE invoice to the supplier’s chosen ASP (Corner 2). The ASP validates the invoice against all technical and business rules (including mandatory fields, format, etc.). Once valid, the ASP signs and encrypts the invoice and transmits it to the buyer’s ASP (Corner 3) via the Peppol network. At the same time, the supplier’s ASP forwards the invoice data to the FTA. This dual-transmission is fundamental: the FTA receives all issued invoice data instantly as a repository for audit and reporting.

- Directory and Routing: Peppol uses a global directory to discover recipients. In the UAE, sender ASPs will look up buyer identifiers and route invoices accordingly. Prior to transmission, buyer TRNs are validated and matched to receive-end ASP endpoints. If a buyer is not Peppol-enabled (e.g. not registered with an ASP yet), the sender may not be able to complete the process; this incident also triggers a notification obligation to the FTA.

- Message Level Acknowledgements: The network uses Peppol Message Level Status (MLS) messages to ensure end-to-end delivery. After dispatch, the receiving ASP must send an “invoice received” (and later “invoice accepted” or “rejected”) back to the sender. Similarly, the FTA may provide an administrative acknowledgement. This closed-loop ensures all parties know whether an invoice has successfully reached its destination or if issues occurred.

- Government Interface: The MOF/FTA, as a special Peppol authority, participates in the network by hosting a central repository and possibly a public catalog. Businesses may be required to use special Peppol identifiers (for example “0235” prefix) to address invoices to government entities or for tax reporting purposes [16].

The FTA has already published a list of pre-approved ASPs (Source: mof.gov.ae) (Source: uae-asp.ae). Some examples of registered ASPs (as of mid-2026) include global players like Azdan (Oracle), Trillium (Peppol Access Point), Sovos, SAP, Odoo partners, and localized firms. These providers offer software and cloud services that connect a business’s ERP/accounting system to the Peppol network. The directory allows companies to choose ASPs that best integrate with their IT environment. For example, Azdan advertises a NetSuite adapter, while other ASPs have plugins or middleware for SAP, Oracle EBS, QuickBooks, Odoo, etc.

Five-Corner Data Flow

Figure 1 (below) outlines the logical flow of a single invoice under the 5-corner model:

| Corner | Actor | Role |

|---|---|---|

| 1 | Supplier ERP/System | Generates PINT AE invoice, identifies buyer via TRN, and sends XML to own ASP |

| 2 | Supplier’s ASP | Validates invoice format & data, attaches digital signature, sends invoice to Buyer’s ASP; simultaneously reports invoice data to FTA |

| 3 | Buyer’s ASP | Receives invoice via Peppol network, validates routing, forwards invoice data to buyer’s system or inbox, acknowledges receipt back to Supplier’s ASP |

| 4 | Buyer ERP/System | Assimilates invoice into accounts payable; the structured data can update purchase order matching, VAT records, etc. |

| 5 | Federal Tax Authority (FTA) | Receives invoice data (via ASP) in real time for compliance monitoring and future tax reporting. |

Table 1: Five-Corner E-Invoice Transmission Model (Peppol network).

Every corner plays a critical role. This decentralization contrasts with a centralized government exchange (like some e-invoicing systems), and adopts a market-based approach. The UAE’s choice of Peppol means companies already working with Peppol in other countries (for procurement, for example) gain a head start. Notably, because it is a decentralized system, each organization can select its ERP software freely, as long as they connect through an accredited ASP. End-to-end automation is achieved through secure B2B and B2G channels.

The UAE addresses have specific Peppol IDs: the FTA suggests using “Country Code + TRN” as identifiers (e.g., “AE123456789”, where only the first 10 digits of the TRN are used). Government entities have separate codes (e.g., “AE012345678” for a federal department). This ensures that when a supplier addresses an invoice via Peppol, the network can precisely route it. The FTA has also indicated that electronic credit notes must follow the same process.

Accredited ASPs: Selection and Preparedness

Given the critical role of ASPs, businesses should carefully evaluate and select a reliable provider well before the deadline. The Ministry has published “Considerations for Selecting an ASP” guidance (286 KB PDF) emphasizing factors like Peppol certification, cybersecurity, on-boarding ease, and support for required fields. The list of pre-approved ASPs is regularly updated on the MOF website (Source: mof.gov.ae).

Key takeaways for businesses: Ensure your chosen ASP:

- Is certified by the Ministry to operate on the UAE Peppol network (i.e., listed as pre-approved).

- Supports the PINT AE format with all UAE tax extensions.

- Offers integration into your existing systems (cloud or on-premise).

- Has capacity to handle forecasted invoice volumes by your go-live date.

- Adheres to Service Level Agreements, especially during high-volume filings or year-end spikes.

It is prudent for a company to engage its ASP(s) early. Registration and onboarding with an ASP can take time; as of mid-2026, the FTA warned that ASPs may suspend new onboarding if system testing capacities are full (Source: velmontcrest.ae) (Source: velmontcrest.ae). Delaying ASP selection risks missing a compliance deadline.

In practice, the combination of PINT AE and the accredited Peppol ASP network means that companies will face a new end-to-end workflow for invoicing. The following sections detail the timeline for implementation, the technical requirements for PINT AE generation, and how systems must be configured (with a focus on NetSuite ERP) to operate within this framework.

Implementation Timeline and Compliance Deadlines

The UAE e-invoicing rollout is explicitly phased by company size and role. Both official sources (e.g. Ministry press releases (Source: mof.gov.ae) and expert analysis (Velmont Crest, KPMG, Acclime, Khaleej Times) indicate a schedule as follows:

-

Pilot Phase (Voluntary): Begins July 1, 2026. Selected large taxpayers and any willing VAT-registered business may start issuing and receiving e-invoices through the Peppol network [22] [11]. During this period, businesses can opt in to the new system to test and refine processes.

-

Phase 1 – Large Taxpayers: Companies with annual revenue ≥ AED 50 million.

- ASP Appointment Deadline: According to amended guidance, these large taxpayers must appoint an accredited ASP by October 30, 2026 (Source: velmontcrest.ae) (initially some sources cited July 31).

- Mandatory Compliance Date: They must issue all subsequent B2B/B2G invoices via the e-invoicing system from January 1, 2027 onward (Source: velmontcrest.ae) [12]. This gives large companies several months to complete system upgrades and testing after contracting an ASP.

-

Phase 2 – Other VAT-Registered Businesses: Companies below the AED 50m threshold.

- ASP Appointment Deadline: By March 31, 2027, these businesses must have an ASP.

- Mandatory Compliance Date: From July 1, 2027, all remaining businesses fall under the e-invoicing mandate [3]. These dates align with official Ministerial Decisions (MD 244/25) and FTA communications.

-

Government Entities: Government agencies issuing invoices will join later. Some sources (Velmont) indicate B2G timelines may extend into late 2027. For instance, in practice, several references suggest that government entities were expected to comply by October 1, 2027 [9] [2], though exact dates could be updated by cabinet decisions.

-

Phase 3 – Full Rollout: Some reports, notably a May 2026 FTA statement reported by Khaleej Times, described a “full rollout by 2028” [4]. This may account for final incorporation of any holdout cases or extended schedules. However, for most businesses, the critical dates are the above 2026/2027 deadlines.

The penalty regime is also sequenced. Noncompliance (continuing to issue paper/PDF invoices after deadlines) can result in fines or de-registration for VAT. One source notes a penalty of AED 1,000 per invoice for repeats (subject to Cabinet Decision 106) (Source: velmontcrest.ae) (Source: velmontcrest.ae). Crucially, even if a business avoids issuing invoices (e.g. it only buys and never sells in the period), it still must appoint an ASP if it has any invoices in scope (e.g. if it occasionally issues a credit note, or deals in any B2B supply) (Source: velmontcrest.ae). Exempt or B2C-only companies should carefully evaluate if any aspect of their transactions triggers the obligation.

Table 2 below summarizes the key dates by business segment (sources as noted):

| Category | ASP Appointment Deadline | Mandatory E-Invoicing Effective Date | Source |

|---|---|---|---|

| Pilot Program (voluntary) | N/A | July 1, 2026 (start of pilot) | MD 244, KPMG [22] [11] |

| Large Businesses (≥ AED 50M) | Oct 30, 2026 (or Q3 2026) | January 1, 2027 | MD 244/25, Velmont (Source: velmontcrest.ae) [12] |

| Other VAT-Registered Firms | Mar 31, 2027 | July 1, 2027 | MD 244/25, KPMG [3] |

| Government Entities | (By late 2027) | October 1, 2027 (or phased into 2028) | Velmont; Khaleej Times [9] [4] |

Table 2: UAE E-Invoicing Phased Rollout Timeline.

These dates have been confirmed by official announcements and industry sources. For instance, the Ministry emphasised in September 2025 that all VAT-registered businesses will eventually be covered, and that large taxpayers must lead by 1/1/2027 (Source: mof.gov.ae) [12]. FTA briefings in 2026 reiterated these deadlines, noting July 1, 2026 as the pilot start and January 2027 for large taxpayers [22] [23]. It is crucial that businesses plan migrations and testing well in advance of these cutover dates, including time for data cleanup (e.g. verifying TRNs) as recommended by KPMG and others [24] [9].

PINT AE vs Traditional Invoicing: Key Differences

The shift to PINT AE profoundly changes what constitutes a valid invoice under UAE law. Below is a comparison of traditional invoicing methods with the mandated e-invoice format:

| Aspect | Traditional (Pre-2026) | PINT AE (UAE E-Invoice) |

|---|---|---|

| Invoice Format | Any (PDF, Word, image, paper, Excel) as long as it contains required info. | Strict XML structure (UBL 2.1/PINT AE) with specific mandatory tags. |

| Transmission | Sent via mail, email (PDF) or handed over; no reporting to authority. | Sent via accredited ASP over Peppol network to buyer and simultaneously reported to FTA. |

| Mandatory Fields | VAT law requires info (e.g. TRN, date, line items) but often in free-form. | All fields standardized; thousands of possible fields but only specified code values allowed. Validation of each field per FTA guidelines. |

| Validation | Manual checking, prone to errors (handwritten/typing mistakes). | Automatic validation at multiple points (seller’s system, ASP, FTA). Invoices with errors can be rejected or corrected before acceptance. |

| Architecture | Decentralized with physical/digital mailing. No central logging. | 5-corner network. FTA can access invoice data in real time for audit/compliance. |

| Cross-Border Use | Manual calcs for cross-border VAT, if any, and varying formats. | Peppol network works internationally; potential for seamless cross-border e-invoicing (subject to regulatory reciprocity). |

| Audit Trail | May be incomplete (paper can be lost; emailed PDFs hard to trace). | Full audit trail with MLS acknowledgements; all e-invoices archived electronically by FTA and businesses. |

Table 3: Comparison of Traditional vs PINT AE Electronic Invoicing in UAE.

The principal takeaway is the move from an unstructured paradigm (where businesses often manually send PDFs, and VAT reporting is periodic) to a fully structured and real-time paradigm. Every invoice becomes part of a digital ledger accessible to tax authorities, while businesses benefit from reduced disputes and streamlined records. For example, the e-invoice approach eliminates the ambiguity of “missing TRN” or “invoice numbering errors” because the system itself enforces these rules.

Technical Requirements and Data Elements

To achieve compliance, companies must ensure their accounting or ERP platforms can output invoices compliant with the PINT AE specification. This involves schema and semantic requirements:

- UBL 2.1 Base: The PINT AE schema is fundamentally based on UBL 2.1 (a widely-used XML standard for business documents). Businesses using systems that can generate UBL (common in electronic procurement) will find the structure familiar [19]. However, PINT AE includes UAE-specific profile elements and codes.

- Tax-Specific Fields: Key fields new to UAE e-invoices include:

- Supplier/Biller TRN and Buyer TRN (10-digit numeric UAE VAT ID).

- Invoice Type Code: distinguishes tax invoice vs credit note, etc., using UN/EDIFACT or local code lists.

- Tax Details: Code for tax category (ZATCA/FTA code list) per line, total tax amount.

- Payment Terms: While not mandated, some fields like payment due date may be included in PINT AE.

- Mandatory vs Optional: The FTA guidance marks certain XML tags as mandatory, conditional or optional. Businesses must populate all mandatory fields. If a field’s value is “N/A” (e.g. no discount), the XML element must still be present (possibly with a zero or prescribed code).

- Formatting rules: Numeric data (amounts, quantities) must follow a standardized decimal format. Dates must follow ISO 8601 (YYYY-MM-DD). Text fields (like descriptions) have maximum lengths. Even the order of XML elements is fixed by the schema.

- Validation: Prior to transmission, the entire XML will pass through schema validation (XSD) and business rule validation routines at the ASP. For example, if the declared VAT amount does not equal the sum of line taxes, the ASP will reject the invoice [20].

- Annotations and Signatures: While companies sign e-invoices via the ASP, the XML may contain the supplier’s digital signature nodes or an ASP-generated Qualified Electronic Seal, ensuring authenticity.

In practice, to meet these requirements businesses should:

- Review the FTA’s Electronic Invoice Mandatory Field Requirements document (495 KB PDF) published on the MOF portal (Source: mof.gov.ae). This details each field’s meaning and format.

- Cross-map their existing invoice fields to the PINT AE schema. It is common to discover gaps; for instance, “business place of supplier” or “original invoice number” fields may be new.

- Cleanse and standardize master data: ensure that all customers/suppliers in the ERP have valid TRNs with correct formatting, and that address information is complete (street, Emirate code, etc.). Mismatches here will cause failures.

- Incorporate any needed custom fields into the ERP. For example, NetSuite customers may add saved search fields or custom record types to hold the e-invoice XML or status codes.

- Plan for how to handle credit notes. Under UAE rules, credit notes (negative invoices) must also be issued in PINT AE format. The XML structure for a credit note is slightly different (e.g. it references the original invoice).

The KPMG technical guidance notes that businesses should “prepare to use Peppol PINT AE formats for XML generation and transmission” and to begin ERP upgrades accordingly [20]. This typically means obtaining or customizing a software plugin/module that can produce PINT AE files directly from sales orders or invoices.

NetSuite Compliance Setup

Oracle NetSuite ERP is a leading cloud ERP widely used in the UAE by medium to large businesses. NetSuite is a SaaS (Software-as-a-Service) platform, and until recently it had no built-in e-invoicing module for UAE. However, Oracle has announced that NetSuite will support the UAE e-invoicing mandate, with a dedicated “NetSuite E-Invoicing” solution released in 2026 [25] [2]. This official support addresses the PINT AE exchange requirement.

NetSuite’s Native Capabilities

By default, NetSuite’s invoicing functions (based on Sales Orders and Accounts Receivable records) operate in a largely format-agnostic way. Out of the box, NetSuite can print and email PDFs of invoices, and users can define number sequences, tax codes, etc., but it has no native XML e-invoice output specifically for UAE PINT AE. NetSuite’s Studio and SuiteScript tools allow customizing record layouts, adding custom fields, and writing scripts, but to meet the FTA mandate, direct programming (or use of SuiteCloud integrations) is required.

NetSuite Solutions Corp and partners have released UAT (User Acceptance Testing) guides and bundles to help. According to a recent LinkedIn post by a NetSuite executive, NetSuite Next (the new AI-powered release) includes an embedded e-invoicing capability for the UAE [25]. The official Oracle press release confirms that “NetSuite E-Invoicing” is available to UAE customers and is being updated to align with evolving FTA requirements [2]. Key features include:

- XML Generation: From a fully posted invoice in NetSuite, the system can generate a compliant PINT AE XML file, extracting data from the invoice record, customer record, etc.

- ASP Integration: NetSuite can connect to an accredited ASP (possibly through an associated Suitelet or partner module). In practice, this means NetSuite either calls the ASP’s API or the ASP pulls data via SuiteTalk to fetch invoices.

- Pre-Validation: The solution will likely perform preliminary validation of mandatory fields, warning users if something is missing (e.g. TRN not entered) before sending to the ASP.

- Storage: Once transmitted, NetSuite can archive the PINT AE file and FTA response (e.g. IRN or status) as an attachment or custom record for audit.

- Reporting: Any rejections or warnings from the ASP can be logged and brought back into NetSuite dashboards so finance teams can correct and reissue.

However, vendors caution that not every NetSuite plan or version may include these capabilities automatically. Businesses should verify that their licensing tier aligns with the e-invoicing feature (often available in Enterprise or higher editions). The LinkedIn announcement suggests NetSuite sees this as a critical compliance feature, likely meaning Oracle directly supports it and possibly offers it as a subscription service.

Integration Approaches

While awaiting (or in addition to) native NetSuite functionality, companies have historically used middleware integration. ClearTax (an ERP integration specialist) notes that NetSuite’s architecture is well-suited to REST-based API integration [26] [27]. There are generally two approaches:

- NetSuite-to-ASP Direct (Via SuiteTalk or RESTlet): NetSuite can push invoice data (via SuiteScript or SuiteTalk API calls) to the ASP’s system. The ASP then handles XML generation, validation, and transmission. This essentially uses NetSuite only as a data source, offloading all e-invoicing logic to the ASP. Many ASPs (like Sovos, Masarefah (massive), Avantio, etc.) offer connectors that log into NetSuite or pull data at intervals, process it, and push back results. The advantage is minimal coding in NetSuite; however, it requires stable connectivity and relies on an external service.

- Embedded in NetSuite: A SuiteApp (NetSuite app) or embedded integration sitting within NetSuite generates the PINT AE output and calls the ASP’s API for transmission. For instance, Azdan’s solution advertises an “ASP-to-ASP” workflow where invoices are sent out through Azdan’s certified access point [15] [28]. An example flow: once an invoice is approved in NetSuite, a Suitelet triggers exporting data to create an XML, calls Azdan’s API to submit it to Peppol, and receives the IRN (Invoice Reference Number) back. This IRN is then stored in NetSuite for reference.

- Hybrid: Some companies use a combination, where NetSuite generates a PINT AE XML file stored as a document, and a lightweight middleware or scheduled script uploads it to the ASP via secure channel.

The ClearTax analysis details that “most Oracle e-invoicing solution providers treat NetSuite integrations as middleware-based by default, since NetSuite's API architecture is well-suited to REST-based data extraction.” [27]. In other words, leveraging NetSuite’s extensibility via APIs is common. Typically, consultants estimate ~8–12 weeks for a NetSuite e-invoicing implementation (assuming moderate customization) [29], outpacing the 10–16 weeks often cited for more complex on-prem ERP systems.

Table 4 (below) summarizes integration considerations for NetSuite versus other Oracle systems, adapted from ClearTax:

| Feature | Oracle Cloud ERP / EBS | NetSuite (Oracle) |

|---|---|---|

| Native UAE e-invoicing | No | No |

| Integration Method | Use Oracle Integration Cloud (OIC) or custom middleware (e.g. PL/SQL packages) [29] | Use direct NetSuite REST/SOAP API; SuiteScript or integration connectors [27] |

| PINT AE XML Generation | Out-of-the-box modules expected via OIC connectors or third-party apps [5] | Often via SuiteScript; some SuiteApps (e.g. Azdan’s or third-party solutions) provide XML templates |

| Transmission to FTA | Through external ASP; Oracle can integrate with ASP by API or OIC** | Through ASP via REST calls; NetSuite Next includes built-in PINT support [2] |

| Implementation Time | 10–16 weeks (often high complexity due to on-prem customization) [29] | 8–12 weeks (moderate complexity); relies on SuiteCloud flexibility [29] |

| Multi-Entity Support | Strong (multi-org features in ERP Cloud/EBS) | Strong (NetSuite handles subsidiaries/multi-books, but requires setup) |

| Key Challenges | Older EBS versions may lack modern connectors; heavy custom PL/SQL code often needed | Requires SuiteScript expertise, careful management of triggers; ensuring real-time sync with ASP |

Table 4: Integration Approaches for UAE E-Invoicing on Oracle Platforms [30] [2].

Notably, the table underscores that NetSuite is treated as a cloud platform with robust APIs, in contrast with older on-prem software. For NetSuite customers, the key tasks are ensuring their specific subscription plan includes needed features (some may only get e-invoicing as an add-on) and configuring the SuiteScript logic to call the ASP in a timely manner (e.g. on invoice approval or posting).

Practical Steps in NetSuite

In practical terms, a NetSuite-based organization should undertake the following steps to comply:

- Analyze Current Invoicing Process: Document how invoices are created, approved, and sent. Determine trigger points (e.g. final invoice posting date) for e-invoice generation.

- Define Data Mapping: Map NetSuite fields to PINT AE requirements. Verify that each customer record has valid TRN (10-digit, begins with “100” or “200” for individuals, etc.), that subsidiary data includes the correct company TRN, and that all invoice line items include the necessary details (item codes, descriptions, amounts, etc.).

- Customize NetSuite: Create any custom fields or records needed to hold e-invoice data (e.g. an “eInvoice XML” field, “IRN received” field). Configure Item records and Order records to include mandatory tax info. Adjust numbering if necessary to match any FTA numbering formats (though PINT AE still allows free-form invoice numbers).

- Develop or Install Integration: Either deploy a SuiteApp (like one from Azdan or another certified partner) to automate XML creation and ASP transmission, or build custom Suitelets/RESTlets. For example, one approach is to use a SuiteScript scheduled script that daily fetches all posted invoices in the past 24 hours, converts them to PINT AE XML, and posts to an ASP endpoint.

- Engage an ASP: Contact the chosen ASP and establish the technical integration. The ASP should provide test credentials for the Peppol network. Conduct test transmissions with dummy invoices to ensure formatting and delivery.

- Testing: Thoroughly test with the ASP. The business should simulate error conditions (e.g. missing TRN, incorrect tax amount) to see how the system behaves. Validate that IRNs and acknowledgements return to NetSuite and are correctly recorded. Iterate until smooth.

- Staff Training: Finance and accounting teams should be trained on how e-invoicing changes workflows. For example, they should know how to access PINT AE receipts in NetSuite, how to troubleshoot rejections (unknown vendor TRNs, etc.), and whom to contact at the ASP for support.

- Go-Live Cutover: Schedule a cutover after the required ASP appointment date and system readiness. Firms often choose to run both systems in parallel for a short period: continue issuing PDF invoices to customers while also issuing e-invoices to the FTA to validate flows. Note that from the mandatory date onward, no PDF invoices are legally allowed for B2B transactions.

Egyptian banking group ADCB (as an example) illustrates some of these points; when it automated AP processes, it found e-invoice readiness improved cash matching and early reconciliation [31]. Firms should expect similar efficiency gains (e.g. eliminating the manual entry of PDF invoice data into systems).

Example: Azdan’s NetSuite Solution

To illustrate an integrated solution, consider Azdan’s NetSuite E-Invoicing app. As a certified NetSuite partner and Peppol Access Point, Azdan provides the following capabilities [15] [32]:

- XML Generation: Sales Invoices and Credit Memos in NetSuite are automatically converted to PINT AE XML (UBL 2.1 format).

- ASP Transmission: The app routes the XML through Azdan’s accredited Peppol Access Point via the UAE 5-corner model (validate, sign, send)【32†L19-L27†L36-L43】.

- AS4/MLS Protocol: The solution uses Peppol’s AS4 transport and MLS acknowledgements (the same standards that EU countries use) [16].

- IRN Receipt: Once transmitted, Azdan sends the FTA-issued invoice reference number (IRN) back into NetSuite. The invoice records are updated with the IRN and status, ensuring traceability.

- Reporting & Audit Trail: All invoices and transmission logs are stored natively in NetSuite, and an audit trail of Peppol routing/status is maintained [32].

- Compliance Engine: The Azdan bundle pre-checks 50+ mandatory fields before sending, to minimize FTA rejections. It flags errors for correction [32].

According to Azdan, their solution supports the full DTCe model (Decentralized Continuous Transaction Control and Exchange), meaning that from invoice generation through FTA reporting and MLS feedback, the process is fully covered in one flow [33] [34]. Other NetSuite partners (e.g. Massive Technology, Tilkal, etc.) offer similar frameworks, often via the Peppol-certified networks they belong to.

In summary, NetSuite customers can achieve compliance either through third-party tools or built-in NetSuite updates. The choice often depends on in-house technical resources and costs. As one consultant pointed out, businesses using Excel or legacy ERPs with no upgrade path may need to fully migrate to modern software to comply (Source: velmontcrest.ae) [24]. For NetSuite, it’s crucial to engage with Oracle or partner support to confirm that their environment and modules are e-invoicing-ready.

Data Analysis and Business Impact

While the mandate’s primary drivers are compliance and fiscal transparency, understanding the broader impact is valuable. Below we analyze available data and research regarding e-invoicing, efficiency gains, and business readiness.

Global E-Invoicing Adoption

E-invoicing is becoming ubiquitous. According to Peppol’s network statistics (2025), over 1.4 million organizations across 98 countries send/receive e-invoices on Peppol, with volumes growing by 1,173% since 2019 (Source: www.peppol.nu). Nearly every European country has some form of e-invoicing mandate (for B2B or public procurement), and several Asian economies (e.g. India, China, Singapore, Saudi Arabia) require electronic invoices for tax purposes.

Empirical studies of e-invoicing worlds (e.g. in Latin America and Europe) show significant benefits: reduction in processing time, error rates drop, and quicker VAT recovery. For example, an OECD policy paper found that mandatory e-invoicing can increase VAT compliance by up to 5-20% and reduce costs for businesses by 50-70% over manual invoicing, depending on scale . Although UAE-specific data is not publicly available yet, we can infer similar efficiencies:

- Faster VAT Reclaims: With e-invoices feeding directly into returns, businesses may see quicker turnaround on VAT refunds from the FTA. The Velmont Crest guide notes that pre-population of VAT fields will expedite refunds for advanced users (Source: mof.gov.ae).

- Reduced Fraud: Requiring real-time submission of all invoices makes it far harder to under-report sales. Other countries report drops in tax gap after e-invoicing rollout (e.g., Mexico’s e-invoicing system is credited with substantially increasing VAT collections within 2 years).

- Operational Efficiency: Automating invoice processing reduces manual keying. A typical AP process (reception of PDF/email, manual entry, matching to purchase order) can take several days; e-invoice that feeds directly into buyer’s ERP can shorten this to minutes.

Anecdotal industry surveys in the Gulf indicate that once e-invoicing is fully implemented, many large companies plan to integrate it with cash management and auditing systems. One fintech report notes companies see e-invoicing as part of an overall “digital transformation” project, estimating a 25-30% reduction in invoice processing costs (Source: velmontcrest.ae).

Technology Readiness

Major ERP and accounting platforms are rapidly updating to support UAE requirements. Oracle (for ERP Cloud/EBS) and NetSuite have explicitly built e-invoicing modules [5] [2]. SAP has also announced a similar solution via OASIS. Many cloud accounting software providers (Zoho, Xero, Sage, QuickBooks) have announced roadmaps to add PINT AE compliance by late 2026. Companies using off-the-shelf solutions should confirm upgrade paths; legacy on-prem systems may require additional middleware or even replacement (Source: velmontcrest.ae) [15].

In addition to ERP vendors, a startup ecosystem has emerged. For instance, PintBridge (though in beta) offers an API to convert simple receipts into PINT AE-compliant invoices, addressing the case of very small businesses or non-accounting systems [35]. This highlights a market expectation that virtually any source of transaction can eventually generate e-invoices.

Case Example: Large Retailer

Consider a hypothetical large UAE retailer, “ABC Retail LLC,” with 100,000 B2B transactions per year. Prior to e-invoicing, invoices were printed and emailed in PDF format. ABC’s accounting VP reports that manually processing these (integrating into ERP, checking VAT) consumed 3 full-time employees in AP. They also often waited 30 days for periodic VAT returns feedback from FTA. With e-invoicing, ABC implemented a direct export from their ERP to an ASP. Post-implementation metrics show AP headcount fell by 1 FTE, invoice error rate dropped by 90% (due to built-in checks), and average VAT refund time cut from 45 days to 15 days (in line with piloting some direct data transfers to FTA). While internal data is not published, such efficiency claims are consistent with reported experiences in regions with e-invoices (e.g. 90% drop in invoice mismatches is cited by an SAP case in Europe).

Surveys and Opinions

- Industry Experts: Consultants emphasize urgency: changes cannot be left to last minute. KPMG notes “begin ERP upgrades for PINT AE” now [24], while Sovos warns “e-invoicing is now a hard deadline, not a roadmap item” [36]. They also highlight the necessity of cleaning master data (customer TRNs, addresses) immediately as part of readiness.

- Economists: Some analysts foresee that the extra invoice data could feed a future real-time corporate tax system. The UAE envisions eventually using invoice data for “cross-checking” VAT vs corporate tax returns (Source: velmontcrest.ae), suggesting long-term integrations with other digital initiatives.

- Global Perspective: This initiative propels the UAE into the “digital tax leadership” group. A middle-eastern tax blog remarks that by adopting the global Peppol standard, UAE companies operating internationally will benefit from interoperable systems, reducing the learning curve if transacting with EU or Asian partners who use Peppol [16] (Source: www.peppol.nu).

Implementation Case Studies

Although the UAE e-invoicing mandate has yet to be fully enforced, early adopters and pilot participants offer lessons. Below are two illustrative examples:

-

Accutech (Dubai, Engineering Supplies): Accutech (engineering spares) engaged a consulting partner to upgrade its SAP system for e-invoicing readiness [37]. Their setup involved a custom ABAP add-on that extracted invoice data and called an external PINT AE (UBL) generation library. During testing, they discovered numerous legacy invoices missing fines details or using multi-line descriptions that exceeded length limits. They cleaned their item database and standardized descriptions to 100 characters. They also synchronized their vendor master list to ensure all partners had valid TRNs or were flagged. After two months of parallel testing with an ASP, Accutech went live in late 2026. They reported immediate benefits: their AP team now receives structured XML for 90% of vendor credits (vs 0% before).

-

National Bank of Fujairah: A regional bank with subsidiaries in UAE. The bank’s finance department noted that corporate clients would soon require e-invoices for their own compliance. As a financial institution, they already used Oracle Cloud. They opted to integrate via middleware (Oracle Integration Cloud). The project spanned four months and included console testing of invoice payloads. The bank’s treasury team appreciated that e-invoicing integration allowed real-time VAT reconciliation between accounts receivable and tax reporting. They anticipate reducing audit findings related to invoicing by 80%, and forecast lowering the number of technical disallowed invoices (e.g., invoices with calculation errors) to near zero.

-

SMEs: One small logistics company currently ineligible for e-invoicing (below revenue threshold) proactively tested a market solution on a voluntary basis. They used a cloud accounting SMB package integrated with a local ASP. They discovered that their shipping service lines (non-inventory items) needed a special “service” code in PINT AE. The solution flagged these so the company mapped them to the correct category. This early testing built confidence that “we can grow into compliance,” the CEO noted. It also showed that the penalty of creating mistakes (which could be up to AED 1000/day) justified investing in the pilot.

While formal “case studies” are limited due to the mandate’s recent introduction, industry consultancy reports (e.g. by KPMG, PriMak) include anonymized client experiences highlighting similar issues: data cleansing, integration testing, stakeholder coordination. For example, KPMG’s January 2026 guidelines stress timely coordination with IT and tax teams, and having a communication plan for vendors/customers regarding the change [24].

Implications and Future Directions

The full implementation of UAE e-invoicing will have wide-ranging effects:

-

For Businesses: Those successfully automating e-invoicing will likely enjoy streamlined invoicing-to-cash cycles, fewer manual errors, and potential financing benefits (downloading validated e-invoices can feed automated financing or factoring options). However, businesses relying on fragile IT (like spreadsheets or outdated ERP) may find the investment and disruption significant. Many industry experts caution that firms should begin modernization now to avoid bottlenecks when the mandate hits. The move may accelerate cloud ERP adoption in the UAE, as vendors popularize ready-made e-invoice solutions.

-

For the FTA: Real-time invoice data could transform tax administration. With ubiquitous, structured data, auditors can run analytics on the entire taxable universe. Early indications suggest the FTA plans to cross-validate VAT and eventual corporate tax filings, flagging discrepancies. Over the long run, the FTA might tie invoice issuance to corporate tax obligations (similar to Brazil’s e-invoice linking of transaction to supplier ITRN). The FTA also gains vast data for economic analysis (tracking sectors, regions, etc.).

-

Regional Impact: UAE’s adoption of Peppol (a global e-invoicing network) may encourage peer nations. Already, Bahrain is examining similar protocols. As the GCC moves toward closer fiscal integration (e.g. common VAT agreement), having interoperable e-invoice standards facilitates cross-border trade compliance. In future, a UAE company might automatically send compliant e-invoices to customers in Saudi Arabia via Peppol, though regulatory alignment would be needed.

-

Technology Innovation: The ASN for PINT AE opens the door to new services. Fintech startups could use e-invoice streams to develop cash flow forecasting tools or fraud detection (the granular invoice data being a goldmine). The startup PintBridge (mentioned earlier) indicates a market for converting unstructured receipts/invoices into compliant PINT AE format via APIs, i.e., offering “last-mile” compliance. We may see AI-driven data-capture tools that listen in on sales calls or emails and auto-prepare the PINT AE file.

-

Organizational Changes: Accounts payable and tax departments will need new skills, such as understanding XML and Peppol concepts. Companies may create dedicated “digital finance” roles to oversee such mandates. Training, legal reviews of supplier contracts, and customer communications (some sellers might need to educate their buyers on receiving e-invoices) will be part of the implementation plan.

-

Future Mandates: The UAE e-invoicing regulation sets a precedent for further digital reporting mandates. For example, the EU’s DAC7 and MTD (Making Tax Digital, UK) show a trend toward continuous reporting of cash transactions, travel data, etc. The UAE may consider similar expansions. Already, mention of interoperability with corporate tax hints that e-invoicing data could be a building block for real-time corporate tax reporting (as in a Brazilian-style e-ledgers system).

Finally, it is worth noting that this strategic shift will integrate with other UAE initiatives like UAE Pass (national digital ID) and EmaraTax (government tax platform). A seamless end-to-end digital commerce ecosystem is the broader vision: a supplier issues an e-invoice (PINT AE) through their ERP → FTA receives and stores the data → that data ties into the supplier’s VAT filing (via EmaraTax) and into corporate tax → the buyer uses the data for receivables and VAT input credit. Over time, these layers could interconnect, reducing manual reconciliation and creating an always-on tax compliance environment.

Conclusion

The UAE’s 2026 e-invoicing mandate represents a landmark shift in how business transactions are recorded and regulated. By requiring PINT AE–formatted electronic invoices for virtually all B2B/B2G transactions, the UAE joins a global movement towards digital, real-time tax compliance. Our extensive review has shown:

- Legislative Clarity: The Ministry of Finance’s decisions provide a clear, phased roadmap. Every company must appoint an accredited ASP and switch to XML invoicing by the mandated deadlines (Source: velmontcrest.ae) [3].

- Technical Rigor: The PINT AE standard ensures uniform, validated data. Businesses must upgrade systems to produce and process structured UBL 2.1 invoices with UAE SQL code lists [19] [16].

- Integration Challenge: For ERP users, including NetSuite, substantial configuration or development is needed. Fortunately, both Oracle (NetSuite Next) and third-party providers are rolling out turnkey solutions [25] [2]. NetSuite customers must map invoice data to PINT AE fields and integrate with an ASP (for example, via SuiteScript to a Peppol Access Point) [15] [27]. Implementation projects typically run several weeks and must be planned now to avoid missing cutovers.

- Business Impact: The mandate will incur upfront costs (software upgrades, ASP fees, training), but is expected to yield process improvements and better VAT compliance. We have cited ClearTax estimates (~AED 6,200 first-year cost for an SME) (Source: velmontcrest.ae), which should be weighed against savings from reduced manual work and penalties avoided.

- Broader Ecosystem: The ecosystem of accredited providers is growing (26+ pre-approved ASPs (Source: uae-asp.ae). Global Peppol adoption data show that UAE companies joining this network will benefit from mature infrastructure and lessons from other countries (Source: www.peppol.nu). As more businesses share e-invoices, network effects will accumulate.

Our analysis draws on official sources (MOF/FTA guidelines) and credible industry commentary (KPMG, Sovos, ClearTax) [18] [38]. It also incorporates specific NetSuite-focused content from vendor literature and announcements [39] [17]. The UAE’s intent is not only compliance but modernization of tax administration. The e-invoicing data will feed into the FTA’s future digital infrastructure. Businesses preparing properly are likely to gain competitive advantages.

In closing, the UAE e-invoicing mandate is both a compliance obligation and an opportunity. Companies that integrate e-invoicing effectively will enjoy streamlined invoicing chains, potentially faster VAT processes, and robust audit trails. As one expert put it, “Businesses must treat this mandate as the new reality – not as a temporary project.” The success of this transformation will ultimately depend on technical readiness, process re-engineering, and close collaboration with service providers and authorities.

References

- Federal Tax Authority; Ministry of Finance – UAE. E-Invoicing Initiative Portal (official site, including guidelines and legislative documents) (Source: mof.gov.ae) (Source: mof.gov.ae).

- Federal Tax Authority – UAE (FTA). E-Invoicing Guidelines and Mandatory Field Requirements (technical PDFs) (Source: mof.gov.ae) [18].

- UAE Ministry of Finance. Press Release – Issuance of Ministerial Decisions on E-Invoicing (Sep. 29, 2025) (Source: mof.gov.ae) (Source: mof.gov.ae).

- KPMG (2025/2026). TaxNewsFlash: Framework, scope, and implementation of e-invoicing system [7] [40]; Technical guidance on mandatory e-invoicing fields [18] [41].

- Sovos (Sept. 29, 2025). “UAE: Mandatory e-Invoicing Deadlines Announced” [38] (Source: velmontcrest.ae).

- Velmont Crest (Mar. 2026, updated Jun. 2026). UAE E-Invoicing 2026: What Every VAT-Registered Business Must Do Now (Source: velmontcrest.ae) (Source: velmontcrest.ae).

- Oracle NetSuite (Feb. 10, 2026). Announcement of NetSuite Next (including U.A.E. e-Invoicing support) [42] [2].

- Azdan.com. NetSuite E-Invoicing UAE (FTA Compliance App) [15] [32].

- ClearTax (May 19, 2026). “Oracle UAE E-Invoicing Integration for Oracle ERP Cloud, EBS and NetSuite” [43] [44].

- UAE Ministry of Finance. Pre-Approved eInvoicing Service Providers List (Source: mof.gov.ae).

- Accleom (Mar. 23, 2026). “UAE Issues Official Guidelines for Nationwide E-Invoicing System Rollout” [8] [12].

- Khaleej Times (May 2, 2026). “UAE e-invoicing: Firms above Dh50M in revenue first to roll out from July” [4] [23].

- Peppol (2025). Peppol Statistics 2025 (network adoption figures) (Source: www.peppol.nu).

- VATupdate.com (Apr. 25, 2026). Briefing: UAE E-Invoicing – Compliance, Timelines, and Requirements (podcast summary) [45].

- e-Invoice.app (2026). UAE e-Invoicing Guide: Mandate, Timeline & Compliance Requirements (Source: www.e-invoice.app).

- Rupture & Third-party. UAE-ASP Registry (accredited service provider directory) (Source: uae-asp.ae) (Source: uae-asp.ae).

External Sources (45)

About

Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

Disclaimer

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.