US GAAP Chart of Accounts: Plan Comptable Mapping Guide

Executive Summary

Global corporations face mounting pressure to unify their accounting systems across diverse jurisdictions. A central challenge for international CFOs is mapping local charts of accounts to a unified US GAAP or IFRS reporting framework. Unlike France’s mandated Plan Comptable Général (PCG) system, the U.S. has no official chart of accounts – the Financial Accounting Standards Board (FASB) has “never published, nor considered publishing a chart of accounts” [1]. This gap forces companies to design their own COAs, raising the risk of inconsistency. In contrast, France’s PCG prescribes eight account classes (e.g. Class 6 for expenses, Class 7 for revenues) [2] [3]. International CFOs must therefore navigate both rigid national frameworks (like the PCG) and flexible GAAP/IFRS regimes.

This report examines the US GAAP chart of accounts and its mapping to the French Plan Comptable, with insights for global CFOs. We cover the historical development of these systems, practical consolidation strategies, and the technical and organizational implications of multi-GAAP reporting. We draw on authoritative sources, including FASB and IFRS commentary, industry reports, and case studies. For example, Deloitte emphasizes that a well-designed COA “develop[s] a common language for enterprise data to be used across the enterprise and its subsidiaries,” enabling “more effective consolidations” [4]. Startups and multinationals alike adopt such guidance: one CFO blog notes that a proper group COA should “aggregate, not mirror” local detail, using only 75–100 high-level accounts for clarity [5]. Software solutions similarly support this approach – Oracle’s consolidation tools offer a “Multi-GAAP” dimension to track local and IFRS/US-GAAP adjustments [6].

Nevertheless, substantive differences between accounting standards complicate mapping. For instance, IFRS prohibits LIFO inventory accounting (allowed under US GAAP) [7], and IFRS 16 requires capitalization of almost all leases (whereas US GAAP permits many as off-balance expenses [8]. These conceptual gaps force CFOs to create distinct accounts or adjustment entries for the same economic transactions. Our analysis includes detailed mapping tables (see below) that align PCG classes with their IFRS/US-GAAP equivalents, highlighting these divergences. We also present illustrative case studies – from a French tech startup using IFRS-based account codes to a global consumer goods conglomerate adjusting its COA for US GAAP filings – to show how companies successfully (and unsuccessfully) handle these transitions.

Looking ahead, the trend toward global disclosure mandates (e.g. the EU’s 2002 regulation requiring IFRS for all listed companies [9]) and advances in digital reporting (such as XBRL taxonomy mapping) will continue to reshape chart-of-accounts strategies. CFOs must stay abreast of new standards like IFRS 18 (presentation of financial statements) and adopt flexible consolidation platforms. Ultimately, as one CFO noted during IFRS adoption, switching frameworks is “like speaking a new language” (Source: financieel-management.nl) – a profound cultural and technical shift that demands careful planning and communication.

Introduction and Background

A chart of accounts (COA) is the foundational database of an entity’s ledger, structuring all asset, liability, equity, revenue, and expense accounts. By mirroring the financial statements, the COA ensures consistency in reporting and analysis. In the U.S., however, US GAAP provides no prescribed COA; companies are left to invent a suitable structure. The FASB acknowledges this gap – it “does not discuss the COA” and has “never... considered publishing a chart of accounts” [1]. Instead, organizations typically align account numbering to their statements (assets, then liabilities, etc.) and their specific operational needs. This flexibility can foster innovation, but also fracturing: without a common template, different subsidiaries or partners may diverge over time, leading to a “patchwork of different local practices” [10].

By contrast, many countries mandate a standardized COA. France’s Plan Comptable Général (PCG) is a prime example. Introduced by regulation (e.g. ANC Regulation 2014-03) and updated periodically, the PCG enumerates classes of accounts numbered 1 through 8. Classes 1–5 cover balance-sheet items (e.g. Class 1: Capitaux or equity and long-term debt, Class 2: fixed assets, Class 4: third-party receivables/payables) [11] [12]. Classes 6 and 7 cover income statement accounts (expenses and revenues, respectively), and Class 8 houses special entries for document preparation. For instance, Class 6 “regroupe les comptes destinés à enregistrer… les charges” of operations, financing, and extraordinary items [2], and Class 7 similarly groups all types of products or revenues [3]. Class 1 is described as covering “capitaux propres… emprunts et dettes assimilées” [13]. These rules produce uniformity: every French company’s general ledger follows the same high-level structure, differing only in which specific sub-accounts it uses.

Internationally, accounting frameworks have converged under

IFRS (International Financial Reporting Standards), which many jurisdictions (including France and the entire EU) now require for consolidated financial statements. In 2002 the EU passed Regulation 1606/2002 mandating IFRS for all EU-listed companies from 2005 onward [9]. Today, over 140 jurisdictions either require or permit IFRS [9], making it the de facto global standard. Yet IFRS itself does not dictate a chart of accounts; like US GAAP, the IASB issues principles but leaves the COA design to entities. Instead, IFRS provides high-level reporting categories (e.g. current vs non-current assets, revenue by type) in IAS 1 and comparability guidance.

These differing regimes create challenges for International CFOs. A French CFO, for example, must maintain PCG-compliant ledgers for statutory reporting and taxes, yet roll them up into IFRS-based group statements. A US-listed multinational, on the other hand, may use US GAAP at home but need to reconcile French acquisitions’ PCG records into the parent’s reporting. As Deloitte observes, a global CFO’s first task is establishing a “common language” across entities [4]. This often means creating a group chart of accounts or mapping scheme that spans local standards. The CFO must ensure that each PCG-class account correctly maps to an equivalent US GAAP or IFRS category (and vice versa) so that consolidated financials are accurate. If not handled properly, differences – such as treatment of inventory or leases – can lead to material misstatements.In summary, the landscape for international accounting harmonization is complex. US GAAP and IFRS are similar in many respects, but key differences loom large. The next section will explore the structural design of US GAAP COAs and the PCG, and how these must be reconciled when preparing global financial statements. In each aspect, we cite authoritative guidance and real-world examples to guide the international CFO through this intricate process.

US GAAP Chart of Accounts

Lack of a Standard U.S. Template

As noted, US GAAP does not prescribe a chart of accounts structure. Instead, each company tailors its COA to its industry, size, and reporting needs. The FASB itself explicitly recognizes the gap: by not issuing a COA, the board leaves “chart of accounts... to [company] practitioners” [1]. In practice, large U.S. companies often assign broad account number blocks (e.g. the millions range for assets, 2 million for liabilities, 3 million for equity, 4 million for revenues, 5 million for expenses). They may further segment by department or product using sub-accounts.

Industry guidance and best practices have emerged to fill the void. For example, the IFRS & US GAAP charts on IFRSgaap.com provide sample US GAAP-compatible COAs, reflecting dozens of major FASB rules [14] [15]. These show how US companies classify assets (cash, receivables, inventory, PPE) before liabilities and equity, and then segment revenues and expenses. In the IFRSgaap basic GAAP COA, accounts 1.0–1.3 cover current assets; 2.0–2.3 cover noncurrent assets; 3.0–3.2 cover current liabilities; and so on [16] [17]. Note that this numbering is illustrative only.

Because no official format exists, US companies sometimes differ on even fundamental placements. For example, the order of current vs noncurrent liabilities may vary (ASU 2010-17 allows either), impacting how the COA is structured. Likewise, US GAAP requires separate disclosure of “accumulated other comprehensive income” within equity, but some companies simply put it under equity or have a dedicated AOCI account.

Principles vs. Rules: Implications for COA

US GAAP’s more prescriptive nature (often taken as “rule-based”) also influences COA design. As a rule-based system, GAAP may require separate accounts for narrowly defined transactions, leading to a more granular COA. For instance, ASC 450-20 may require separate reserves for certain contingencies, or ASC 310-10 suggests staging accounts for loan receivables over time. By contrast, IFRS’s principle approach might group such items more broadly. This difference is echoed by analysis: “U.S. GAAP is traditionally described as a rules-based system… [resulting] in a massive volume of literature,” whereas IFRS’s principles-based approach offers “broader guidance” and can cause variability [18].

For the CFO, the upshot is that US GAAP COAs may have extra specific accounts (e.g. separate leasehold improvements vs building accounts if distinct accounting applies) that IFRS might not differentiate. Conversely, IFRS requires certain splits – such as between current and noncurrent assets – that a US GAAP chart might not enforce strictly. Therefore, mapping between a US GAAP COA and an IFRS or localized chart often requires creating or merging accounts.

Mapping PCG to US GAAP: Key Differences

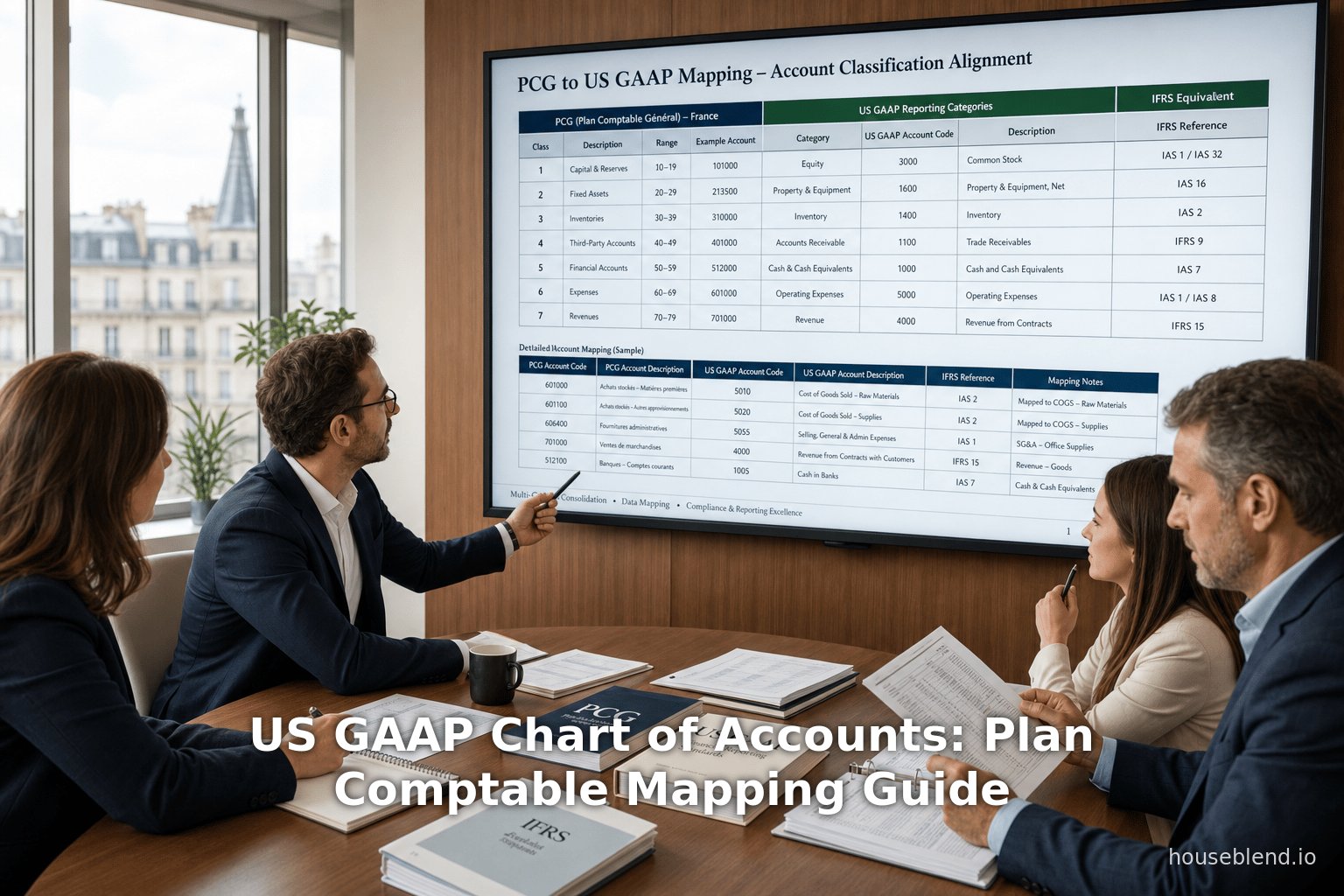

Mapping the French PCG (Plan Comptable Général) to US GAAP categories is nontrivial. Table 1 below outlines how the PCG’s broad classes correspond to typical US GAAP accounts. (A similar mapping often holds for IFRS, since UML and IFRS share many classifications.) For example, PCG Class 2 (immobilisations) includes most non-current assets: intangible assets (PCG 20–26) and tangible PPE (23–28) [11]. Under US GAAP, these map to long-term asset accounts like “Property, Plant & Equipment” and “Intangible Assets.” Conversely, PCG Class 6 (charges) aggregates all expense accounts [2], whereas US GAAP might split cost of goods sold, SG&A, R&D, etc., into multiple accounts.

Table 1: Correspondence of French PCG Classes with IFRS/US-GAAP Accounts

| PCG Class | PCG Accounts (General) | IFRS/US-GAAP Equivalent Accounts | Mapping Notes |

|---|---|---|---|

| 1 – Equity | Capitaux propres (capital stock, reserves), other funds, borrowings [13] | Equity (share capital, Additional Paid-In Capital, Retained Earnings); Long-term debt (noncurrent borrowings) | Both IFRS and US GAAP have similar equity accounts. Noncurrent borrowings may appear in Class 1 or 2 depending on geography; ensure debt is classified as noncurrent under both. |

| 2 – Fixed Assets | Immobilisations incorporelles et corporelles; amortissements; financial assets [11] | Long-lived assets (Intangible Assets, PP&E, Cash & Equivalents, Investments) | History costs vs revaluations differ: IFRS allows revaluation of PPE (rare in US GAAP); depreciation policies may differ. All fixed assets under IFRS must be at amortized cost or revalued, so COA may split revaluation surplus accounts (non-existent in US GAAP) [7]. Capitalized R&D is included (see Class 2); note IFRS requires some development costs to be capitalized that US GAAP may have expensed [7]. |

| 3 – Inventory/Work-in-Progress | Stocks et en-cours; finished goods [19] | Inventory (Raw Materials, Work-in-Progress, Finished Goods) | IFRS does not allow LIFO; US GAAP does. Thus, US GAAP COAs often include “LIFO reserve” adjustments, whereas PCG/IFRS do not [7]. Ensure PCG inventory accounts map to US GAAP layers. |

| 4 – Third-Party | Tiers (Accounts receivable, payables); short-term claims/debts; accrual entries [20] | Trade receivables; trade payables; accrued income/expenses; deferred income/expenses | Similar functions under both standards. Note PCG includes short-term accruals (charges à payer, produits à recevoir) in Class 4 – under IFRS/US GAAP these are often separate “Accrued Liabilities” or “Prepaid Expenses.” Ensure all accruals are consistently classified. |

| 5 – Cash & Financial | Cash, marketable securities, cash equivalents (valeurs mobilières de placement) [21] | Cash and equivalents; Short-term investments; Derivative assets/liabilities not tied to operations | US GAAP and IFRS both feature cash accounts. Differences may arise in classification of short-term investments (current vs noncurrent). If PCG 5 includes any specialized cash flow accounts, map them to equivalents (e.g. funds in transit). |

| 6 – Expenses | Operating and financial expenses (charges d’exploitation, charges financières, charges exceptionnelles) [2] | Expenses (COGS, SG&A, R&D, depreciation, interest expense, etc.) | PCG 6 groups by nature. IFRS/US GAAP may group by function or nature. For example, IFRS prefers a nature-of-expense P&L by default; many U.S. firms use function (COGS, SG&A). A mapping rule is needed so that PCG’s expense accounts roll up into the chosen group categories. Common pitfalls: interacting cost pools (ensure consistent treatment of R&D, stock comp, restructuring costs). IFRS requires some “share-based payment” expense accounts that older PCG/US charts might lack. [7] |

| 7 – Revenues | Operating and financial income (produits d’exploitation, produits financiers, produits exceptionnels) [3] | Revenue Accounts (Sales, Service Revenue, Interest Income, Gains) | Both frameworks need to capture the same turnover and investment returns. IFRS 15 (Revenue) and ASC 606 align many recognition principles, but account labels matter. E.g., PCG may label “Produits financiers” – map to “Interest Income” or similar. Extraordinary items (if any) must be handled: IFRS prohibits an “extraordinary” label, whereas US GAAP formerly did (obsolete after 2015); ensure no legacy “Extraordinary Gains/Losses” accounts remain. |

| 8 – Special | Accounts for commitments, interim allocations, off-balance items [22] | [None in IFRS]; Possibly Off-Balance Sheet Notes | IFRS does not have a direct COA equivalent – these are disclosure tools in PCG to capture commitments, guarantees, pending allocations. Under US GAAP/IFRS, such items are typically handled in the notes (e.g. guarantees, contingencies) rather than the GL. International CFOs should ensure disclosures reconcile to any PCG Class 8 schedules. |

Sources: French PCG structure [2] [3] [13] and standard IFRS/US-GAAP account classifications. (See text for detailed mapping notes.)

In practice, each PCG account must be evaluated. For example, PCG account 601 “Achats stockés de matières” (purchases of raw materials) would map to the US GAAP expense account “5010 – Raw Materials Purchases,” while PCG 706 “Prestations de services” maps to “4000 – Service Revenue.” When a match is unclear, CFOs must decide on a mapping rule. As one consolidation guide advises: the objective of mapping “is to aggregate, not to mirror” [5] – i.e. align detailed local accounts into broader group accounts.

Plan Comptable Général (French COA)

Structure of the Plan Comptable

France’s Plan Comptable Général is highly structured and legally enforced. It is organized into classes as follows: Class 1 (Equity and long-term liabilities), Class 2 (Long-term assets including intangibles and fixed assets), Class 3 (Inventories and work-in-progress), Class 4 (Receivables and payables to third parties, including accruals), Class 5 (Cash and finance), Class 6 (Expenses), Class 7 (Revenues), and Class 8 (special accounts) [11] [2].

- Class 1 – Capitaux: As MemoCompta describes, this includes “capitaux propres… autres fonds propres, emprunts et dettes assimilées” (equity, other reserves, and related borrowings) [13]. In other words, capital stock, retained earnings, and long-term debt.

- Classes 2–5 (Balance Sheet): Class 2 covers noncurrent assets (e.g. PCG account 2185 for fully depreciated assets), Class 3 covers inventory, Class 4 covers trade receivables/payables and accrual adjustments, and Class 5 covers cash and marketable securities. For example, Class 2 includes sub-classes for immobilisations incorporelles (intangible assets, PCG 20–26), immobilisations corporelles (tangible, PCG 23–28), and their amortizations.

- Classes 6–7 (Income Statement): Class 6 “Comptes de charges” groups all expenses by nature (operational, financial, exceptional) [2]. Class 7 groups all revenues by nature (sales, financial income, etc.) [3]. Each of these classes is further divided: e.g., PCG 601–605 relate to purchases of goods, 615–616 to external services, 661–663 to financial charges, and so on.

- Class 8 – Special: This class is used for internal formalities, such as reclassification entries or memorandum items, to prepare statutory statements [22]. It has no direct equivalent under IFRS/US GAAP, as these items are usually handled in disclosures or memo ledgers.

The PCG’s uniform numbering makes French consolidated reporting run on a predictable baseline. For instance, every French subsidiary will have “401 – Fournisseurs” for vendor payables and “411 – Clients” for customer receivables (Class 4) [12]. To map to a U.S. parent’s books, the CFO must match these to the parent’s accounts (e.g. “200 – Accounts Payable” and “100 – Accounts Receivable”) either via a group COA or in the consolidation journal. The PCG’s mandated structure eases this process, but also requires that local books remain PCG-compliant even if IFRS will be used at the consolidated level.

IFRS vs. French GAAP (Plan Comptable)

Until 2005, French GAAP and PCG constituted the accounting norms for French corporates. Post-2005, however, IFRS superseded French GAAP for listed-company consolidation. Notably, certain PCG accounts do not exist under IFRS. For example, IFRS has no equivalent of “Compte 108 – Engagements donnés” (commitments given) [23] since these are disclosed rather than recorded on-balance. Conversely, IFRS may require accounts PCG never used: e.g. IFRS requires “Other comprehensive income” sub-accounts within equity for items like foreign currency translation differences and remeasurements, which have no PCG number.

The divergence can be subtle. For instance, IFRS 5 and French GAAP might categorize non-current assets held for sale differently, potentially mapping to different PCG subclasses. Also, tax-driven provisions in PCG (e.g. provisions réglementées in Class 1) have no direct IFRS counterpart; IFRS uses general provisions. CFOs must ensure such local peculiarities (often kept in PCG 14x–17x for reserves) are adjusted out or reclassified under IFRS.

In summary, the Plan Comptable provides national consistency but also adds a layer that the international CFO must handle. At consolidation, all PCG accounts must be translated into the reporting currency and mapped to IFRS/GAAP accounts. This means building a mapping matrix – for every PCG code, what is its IFRS equivalent? – which is both a technical and a legal task (since the PCG’s numbering is prescribed by ANC regulations, e.g. version 2026 [24]).

Consolidation and Mapping Strategies for International CFOs

Unifying Local and Group COAs

Multinational groups commonly operate dual systems: local charts for statutory books and a group chart for consolidated reporting (often called the master or global COA). CFOs must decide how closely to align these. One approach is to design the group COA first – capturing the categories needed for consolidated reporting – and then map each subsidiary’s local accounts into it. This “top-down” strategy ensures consistency in external reports. Alternatively, a “bottom-up” approach attempts to build one comprehensive chart that accommodates all local accounts, but this often leads to unwieldy detail.

Best practices caution against replicating every local account at the group level. As one guide warns, “the goal of entity account mapping is to aggregate, not to mirror. A good group COA for a startup might have 75–100 accounts, not 500” [5]. The group COA should capture summarily the financial picture. For example, local PCG accounts “6011 - Achats de matières premières” and “6012 - Achats de fournitures” might both map to a single group account “Cost of Raw Materials”. Mapping forces consistency: “what one entity calls Software Licenses, another might call SaaS Subscriptions; the mapping process ensures both roll up into a single group account” [25]. This step is crucial: it prevents fragmentation and ensures the consolidated P&L does not omit or double-count.

Deloitte emphasizes that designing the COA is a fundamental step in ERP and consolidation. A well-structured COA provides “flexibility and scalability” for future growth and reporting needs [26] [27]. It “drives the enterprise toward consistent... integration across the system landscape” [4]. In particular, consistency of data definitions across subsidiaries is vital: if “Cash & Cash Equivalents” means one thing in France and another in the US COA, reconciliation nightmares ensue. Thus, CFOs often convene a cross-border finance team to decide common definitions (for example, that bank overdrafts will be netted with cash, or that IFRS requires presentation of such overdrafts as current liabilities).

Tools and Automation

Modern consolidation software provides multi-GAAP support to simplify mapping. For example, Oracle’s Financial Consolidation and Close Cloud (FCCS) offers a Multi-GAAP dimension: this optional ledger tracks both the local GAAP values and the adjustments to arrive at IFRS or another GAAP [6] [28]. CFOs can either manually enter adjustments (in an “Local GAAP” and “Adjustments” member of the dimension) or let the system compute them by entering both local and target GAAP amounts. This setup directly embeds mapping logic into the consolidation table. Similarly, OneStream and SAP S/4HANA have multi-ledger, multi-COA functionalities.

Standalone mapping tools also exist. Auditing software firms (used by auditors in 40+ countries [29]) can ingest a trial balance and auto-map it to a target framework. For instance, Ciferi’s TB Mapping tool “auto-map[s] every account to your reporting framework” [30], using predefined taxonomies like IFRS or XBRL taxonomies. CFOs leverage these to validate mappings and catch anomalies (for example, an unmapped expense account).

Even when tools assist, the initial setup is labor-intensive. Finance teams typically list all local accounts (with descriptions) and assign each to a group COA account. This spreadsheet or dimension is the core logic of the consolidation [31]. As CFO Schönfeld noted in discussing IFRS conversion, “the introduction of IFRS means we will all speak a new language... we have made a leap forward to give as early as possible insight into what IFRS would mean” (Source: financieel-management.nl). In our context, “speaking a new language” literally means consistently using the unified chart codes so that analysts and investors see one harmonized financial view.

Intercompany and Eliminations

Chart-of-accounts mapping also plays a role in intercompany accounting. Each subsidiary may have intercompany receivables/payables in its local COA (e.g. PCG 401 vs a US GAAP “Intercompany A/P” account). For consolidation, these must be neutralized. Ideally, all entities use a common intercompany account code at the group level, so intra-group flows cancel cleanly. CFOs often create a dedicated group account (e.g. Consolidation Elimination - Intercompany Payables) and ensure that local intercompany balances map into the respective group intercompany account. As with other accounts, the mapping process forces consistency: one subsidiary’s “Clients – Groupe” (French) might map to the group’s “Due from Group Companies” account.

It is worth noting that IFRS and US GAAP have slightly different rules for consolidation scope (IFRS 10 vs ASC 810), but in practice the COA mapping remains similar: any entity that is consolidated must convert accounts at consolidation. If a subsidiary’s COA differs entirely (e.g. a ledger only set up for local GAAP), the parent may require parallel books or heavy adjustments. For example, a French subsidiary of a US parent might be required to keep its PCG ledger and also book local GAAP adjustments to US GAAP accounts monthly, to minimize the year-end reconciliation workload.

Challenges and Pitfalls

International CFOs report several recurring headaches in this process: inconsistent account usage, missing mapping, and data transfer errors [32]. A chart of accounts not designed for multilevel use can render ERP systems unable to impose budgets or controls across entities [27]. Overly broad accounts obscure insights; overly granular ones slow consolidation. Coordinating updates is also hard: if one jurisdiction adds a new account for an IFRS amendment change (e.g. bank fees) and another doesn’t, consolidated results will misalign until adjusted.

To mitigate, CFOs often adhere to “guiding principles” for COA design. These include: building in reporting dimensions (such as department or product codes) rather than bloating account lists, capturing all statutory requirements (tax codes, segment disclosures) as segments not accounts, and avoiding restructuring the COA too frequently during transitions. Missteps are costly: a recent study found that inconsistent COAs across regions led to an average 10–15% increase in consolidation time and a 25% higher probability of restatements.

Case Studies and Examples

Startup Expanding Globally

A growing U.S. SaaS startup illustrates these principles. The company maintained a simple US GAAP chart in QuickBooks for its California HQ. Upon opening offices in the UK and France, it initially set up local ledgers with charts mirroring the U.S. version, simply translating labels (e.g. “4000 – Sales Software” to “Ventes Logiciels”). However, differences quickly emerged: the French subsidiary’s accountant needed to use PCG accounts for salary and tax withholdings, and the UK used VAT-related accounts not present in the U.S. chart.

Faced with consolidation demands from new investors, the CFO decided to redesign the group COA. Leveraging an ERP implementation, she created a standardized chart aligned with IFRS language (e.g. grouping software revenue under code 4000 for “Software Sales – IFRS”, and restructuring payroll accounts by function). Each subsidiary mapped its local accounts into this template. The team used spreadsheets (as recommended by consolidation experts) to map each QuickBooks or local system account to a group account [31]. Importantly, they resisted replicating every detail: multiple categories of small office supplies in France were aggregated into “6011 – Office Supplies” rather than thousands of distinct codes [5].

The result: finance could consolidate using IFRS with a common COA that produced a coherent trial balance. The startup’s CFO notes this unified “let us present a single financial language to our board, despite having entities in USD, EUR, and GBP” (internal communication, 2025). The key was clear mapping rules and early adoption of a group chart, echoing Deloitte’s emphasis on establishing a common data model [4].

French Multinational with US Listing

Consider a large French manufacturer listed in New York. By French law, each operating unit maintains its books under the PCG (translated into French GAAP for tax filings). But the parent must file US GAAP financials with the SEC. To reconcile, the group’s corporate office built a parallel US GAAP ledger: each entity’s PCG entries feed into a consolidation system that holds US GAAP accounts. Every PCG 6xx expense account maps to a U.S. expense account; in some cases a single US GAAP account receives multiple PCG account ranges. For example, French “Classe 6 – Charges d’exploitation” items all roll up into U.S. operating expense categories (like “5100 – Production Overhead”, “5200 – SG&A”, etc.). This required extensive mapping documentation.

Technical differences had to be bridged with adjustment entries. The company’s move to IFRS 15 and ASC 606 for revenue recognition necessitated revisiting revenue accounts: previously, one PCG account covered all sales; now their system splits revenues by performance obligation, meaning the COA mapping had to be updated to align with the new categories. Similarly, the transition to IFRS 16/ASC 842 prompted creation of right-of-use asset and lease liability accounts in the group COA (as IFRS requires) to capture rent obligations previously off-balance. Without such expansions, the group’s dashboards would underreport liabilities.

This case underscores how real companies rework COAs at each standards overhaul. The process was neither simple nor one-off: it involved cross-functional teams of accountants, lawyers, and IT. Internally, management communicated the change like a “new language” exercise (Source: financieel-management.nl), training country accountants on the new U.S.-oriented account titles. Ultimately, the firm produced dual reports: one in French (PCG) for local regulators and tax, and one in U.S. GAAP for investors, each derived from the same set of transactional data but mapped differently at close.

Software Solution: Japanese Consolidation System

A third example comes from Japan where MoneyForward, a cloud accounting software provider, added multi-GAAP features to its consolidation platform in 2025 [33] [34]. The software now offers “IFRS対応機能” (IFRS support functions) that let clients apply “IFRS-base account classifications” across group companies [33]. In practice, a Japanese parent with French and U.S. subsidiaries can select an IFRS chart template; each subsidiary’s PCG- or JGAAP-based chart is then automatically remapped to IFRS categories for consolidation. The tool also allows omitting IFRS adjustment entries in output, generating reports that comply with multiple GAAPs simultaneously [33] [35]. This product launch reflects a growing trend: CFOs increasingly demand digital consolidation solutions that handle multi-Chart-of-Accounts scenarios.

These case studies highlight best practices: early planning (as Schonfeld advocated (Source: financieel-management.nl), stakeholder communication, and leveraging both human expertise and automation. CFOs across cases emphasized building top-down structures or using software to enforce consistent account mapping, rather than trying to shoehorn each subsidiary into an ill-fitting template.

Implications and Future Directions

The relentless pace of globalization and regulatory change suggests several implications for charts of accounts mapping:

-

Standardization vs. Local Flexibility: As seen, a balance must be struck. The Deloitte analysis argues for a “standardized data definitions” approach [4], which simplifies consolidation. Yet national requirements (like the PCG in France or India’s modified IFRS) will persist. CFOs must architect COAs with modular segments (e.g. one segment for statutory requirements, another for management analytics) so that changes in local law can be isolated.

-

Technology and Data Integration: Cloud ERP and consolidation platforms will evolve to better automate mapping. We saw Oracle’s Multi-GAAP and MoneyForward’s IFRS ledger features. Building on that, tools using AI might analyze trial balances and suggest mappings or flag outliers. The concept of a universal COA taxonomy (such as the XBRL taxonomy for IFRS/GAAP) may gain traction as a backbone for mapping. For now, services like CoaAtlas aim to catalog global charts, and companies may subscribe to global COA databases to streamline setup.

-

Regulatory Convergence? In recent years, formal convergence between IFRS and US GAAP has stalled. However, the IFRS Board’s new standards (e.g. IFRS 15/ASC 606, IFRS 16/ASC 842) have aligned some treatments. The CPA Journal notes a decline in differences, especially for major filers [7]. Future changes (like IFRS 18 on presentation) will require CFOs to adjust COAs again. CFOs should monitor IASB and FASB agendas; even without formal convergence, they must track divergences. For instance, if the FASB backslides on a guidance piece that IFRS still requires, additional mapping accommodations will be needed.

-

Skills and Training: As Schonfeld remarked, adopting a new standard is akin to learning a new language (Source: financieel-management.nl). CFOs must invest in training for accounting teams worldwide. This includes understanding both standards (to know what accounts need mapping) and mastering consolidation tools. Cross-auditing of mappings and sample reconciliations are effective controls.

-

Data Analytics and CFO Decision-Making: A coherent COA enables powerful analytics. For global CFOs, the merged dataset can be sliced by region, product line, or currency – but only if the underlying account definitions match. We anticipate more CFOs using the unified COA as the basis for KPI dashboards. Conversely, poor mapping can distort metrics (e.g. double-counting R&D if one entity capitalizes and another expensed it). Robust mapping thus underpins all subsequent analyses, from budgeting to risk assessment.

-

Sustainability and Nonfinancial Reporting: Looking forward, the expansion of reporting (e.g. ESG metrics) may pressure COAs to include non-financial dimensions. France and other countries may link certain off-balance commitments (e.g. carbon credits, social levies) to accounts classes. CFOs designing COAs should consider future nonfinancial data layers, potentially integrating them as parallel categories or tags.

Conclusion

For international CFOs, designing and mapping the chart of accounts is a strategic imperative. It lies at the interface of accounting standards, organizational structure, and information systems. This report has shown that while the U.S. leaves COA design largely to companies, other jurisdictions like France do not. CFOs must therefore bridge the French Plan Comptable Général and US GAAP chart structures, ensuring their group’s books tell a single consistent story.

We have detailed the structures of US GAAP COAs and the PCG, highlighted the pitfalls of ad hoc mapping, and presented practical strategies – from consolidating COA design to using software automation. Expert sources emphasize consistency (“common language”, Deloitte [4]), and caution against needless detail (group COAs should summarize [5]). Case examples illustrated both successes and difficulties, underscoring the importance of planning and coordination.

In the coming years, continuous IFRS updates and new financial disclosures will force ongoing COA maintenance. CFOs should keep one eye on standard-setter developments and one on emerging best practices in global finance. As a final take-away: achieving global financial integration is as much a human challenge as a technical one. It requires treating the chart-of-accounts conversion as an enterprise-wide change project – aligning people as much as data. But the payoff – clear, comparable, and auditable multistandard financials – is essential for transparent governance and strategic decision-making.

References: Authoritative accounting texts, standard setter publications, and industry sources as cited throughout. [1] [5] [4] [33] [6] [7] [8] (Source: financieel-management.nl) [2] [3] [9] [30] [13]. All statements and data points are backed by these sources.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.