US GAAP vs IFRS: Complete Standards Comparison Guide

Executive Summary

The International Financial Reporting Standards (IFRS) and United States Generally Accepted Accounting Principles (US GAAP) represent the two dominant financial reporting frameworks. Each has evolved under different legal systems and philosophies: IFRS is promulgated by the independent, global International Accounting Standards Board (IASB) and has been adopted in over 140 jurisdictions worldwide [1], whereas US GAAP is developed by the Financial Accounting Standards Board (FASB) under US law. Despite extensive convergence efforts, significant differences remain. These differences affect the recognition, measurement, presentation, and disclosure of assets, liabilities, income, expenses, and cash flows.

This report presents an in-depth comparison of IFRS and US GAAP, focusing on their historical development, conceptual distinctions, technical differences in key areas (e.g. revenue, leases, inventory, R&D, financial instruments, impairment, income taxes, and others), and convergence efforts over time. We provide detailed analysis, data, and case examples to illustrate how these two frameworks diverge and where they align. Citiations from authoritative sources (regulators, accounting firms, academic journals) are integrated throughout to substantiate each point.

The Chief Financial Officer (CFO) perspective is emphasized: as global enterprises increasingly cross borders, CFOs must understand both frameworks in order to present comparable financial information and make informed decisions. The report reviews how differences in IFRS vs US GAAP can impact financial results and key performance metrics. For instance, IFRS’s broader use of fair value and allowances (e.g. permitting revaluation of fixed assets) can cause greater volatility and deferred tax effects compared to GAAP [2]. In contrast, GAAP’s rules-based approach leads to more consistency but can obscure economic reality.

Historical context is provided (emergence of IASC/IASB from 1973 onward, FASB formation, EU’s 2005 IFRS mandate, Norwalk Agreement, etc.). We outline global adoption: by 2018, IFRS was required for consolidated financial statements in 144 out of 166 reporting jurisdictions (≈87% 世界GDP) [1]. A comparative table (below) highlights major IFRS–GAAP divergences by topic (e.g. Inventory: IFRS prohibits LIFO vs GAAP allows [3] [4]; Leases: IFRS 16 uses a single lessee model vs GAAP’s dual model [5]; R&D: IFRS capitalizes development costs vs GAAP expensing [6] [7]; Cash Flows: IFRS allows different classification of interest/dividends vs GAAP’s strict rules [8]; Goodwill: IFRS one-step impairment (recoverable amount) vs GAAP’s two-step legacy approach [9] [10]).

Case studies illustrate real-world impacts. For example, a global consumer-goods company with a foreign parent adopted IFRS (shifting away from US GAAP) to comply with international requirements [11]. This transition, while complex, consolidated reporting, reduced controls costs, and improved comparability across its worldwide subsidiaries. Another example involves Fortune Global 500 companies: of the top 100 companies in 2021, 64 were headquartered outside the US and 78.1% of those (50 companies) reported under IFRS [12]. CFOs of such companies operate inherently in dual-standard environments, underscoring PwC’s admonition that practitioners must be “financially bilingual” in IFRS and GAAP [13].

In conclusion, while convergence initiatives have aligned some standards (e.g. joint IFRS 15/ ASC 606 on revenue, IFRS 16/ ASC 842 on leases, “significant differences remain” [14]. This report provides CFOs and financial executives with comprehensive insight into those differences, supported by statistics, expert commentary, and detailed tables. Understanding these nuances is essential for informed decision-making, effective communication with stakeholders, and planning for future changes (e.g. new accounting standards or regulatory shifts). As one regulatory body put it, “a single set of high-quality global standards would benefit U.S. investors,” but until full convergence, companies must navigate both regimes [15] [1].

Introduction and Background

Accounting standards are the rules that govern how economic transactions are recorded and reported in financial statements. These standards shape nearly all financial metrics that investors and managers use to evaluate performance and make decisions. In the global economy, two sets of standards dominate: IFRS (International Financial Reporting Standards) and US GAAP (US Generally Accepted Accounting Principles). IFRS is developed by the IASB in London, while US GAAP is set by the FASB in the United States.

-

IFRS (International Financial Reporting Standards): Originating from the International Accounting Standards Committee (IASC) in 1973, IFRS are adopted in over 140 jurisdictions [1]. The IASB was formed in 2001 (replacing the IASC) and has since issued IFRS (e.g. IFRS 9 for financial instruments, IFRS 15 for revenue). IFRS is known as a principles-based system: it provides broad objectives and fewer detailed rules, requiring significant professional judgment in application. IFRS aims to ensure comparability of financial statements globally and is intended to reflect the economic substance of transactions.

-

US GAAP: Developed over many decades in the US, US GAAP originated from standards of bodies like the AICPA, the Accounting Principles Board (APB) and, since 1973, the FASB. It is often described as a rules-based system: it contains many detailed implementation guidelines, exceptions, and bright-line rules. US GAAP is tailored to the specific regulatory and tax environment of the United States.

The two systems share core objectives (accurate, reliable financial reporting) but differ in approach. IFRS generally allows more alternative treatments and escalates to managerial judgment; US GAAP often prescribes one method. For example, IFRS permits revaluing fixed assets to fair value, whereas US GAAP generally prohibits upward revaluation. These conceptual differences mean identical transactions can produce different financial results (revenues, profits, asset values) under IFRS vs GAAP.

Global context: In 2002 the European Union mandated IFRS for all listed EU companies from 2005 onward [16].Similarly, other countries have adopted IFRS in whole or in part: by 2018 about 87% of reporting jurisdictions required IFRS for consolidated reporting [1]. The US, however, has not adopted IFRS for domestic filers; US SEC rules continue to require US GAAP (with IFRS allowed only for foreign private issuers without reconciliations). Thus, US companies use US GAAP, while foreign multinationals may use IFRS, GAAP, or both in different jurisdictions. The lack of a single global standard means CFOs leading international firms often must be fluent in both frameworks. Indeed, as noted by PwC, “given the many ongoing differences, it is important for preparers and users…to be financially bilingual: familiar with both GAAP and IFRS” [13].

Convergence efforts: Since the early 2000s, the IASB and FASB have collaborated to converge IFRS and US GAAP. The 2002 Norwalk Agreement formalized a joint commitment. Major projects led to jointly-issued standards on revenue (IFRS 15/ASC 606) and leases (IFRS 16/ASC 842), which are now largely aligned across systems. Nonetheless, convergence has stalled in recent years and significant differences remain [14]. Regulators have recognized this reality: SEC Chairman Cox (2006) and subsequent SEC statements (2010) expressed support for convergence but eventual adoption of a single standard was not mandated [15].

The CFO’s role: Globally active CFOs must navigate this landscape. They need to translate financial data from subsidiaries reporting under local GAAP (or IFRS) into corporate-wide reporting language. Differences can influence key decisions on financing, mergers, and performance reporting. This report digs deeply into the specific distinctions between IFRS and US GAAP, supported by data (e.g. adoption counts, percentages of global companies under each system) and examples. It is organized into detailed sections (conceptual framework, major technical differences, case studies, implications, future directions) to give CFOs a thorough understanding of the IFRS–GAAP framework gap.

The following table summarizes some of the key differences (by topic) that will be discussed in detail below.

| Accounting Topic | IFRS Treatment | US GAAP Treatment | Implications for CFOs |

|---|---|---|---|

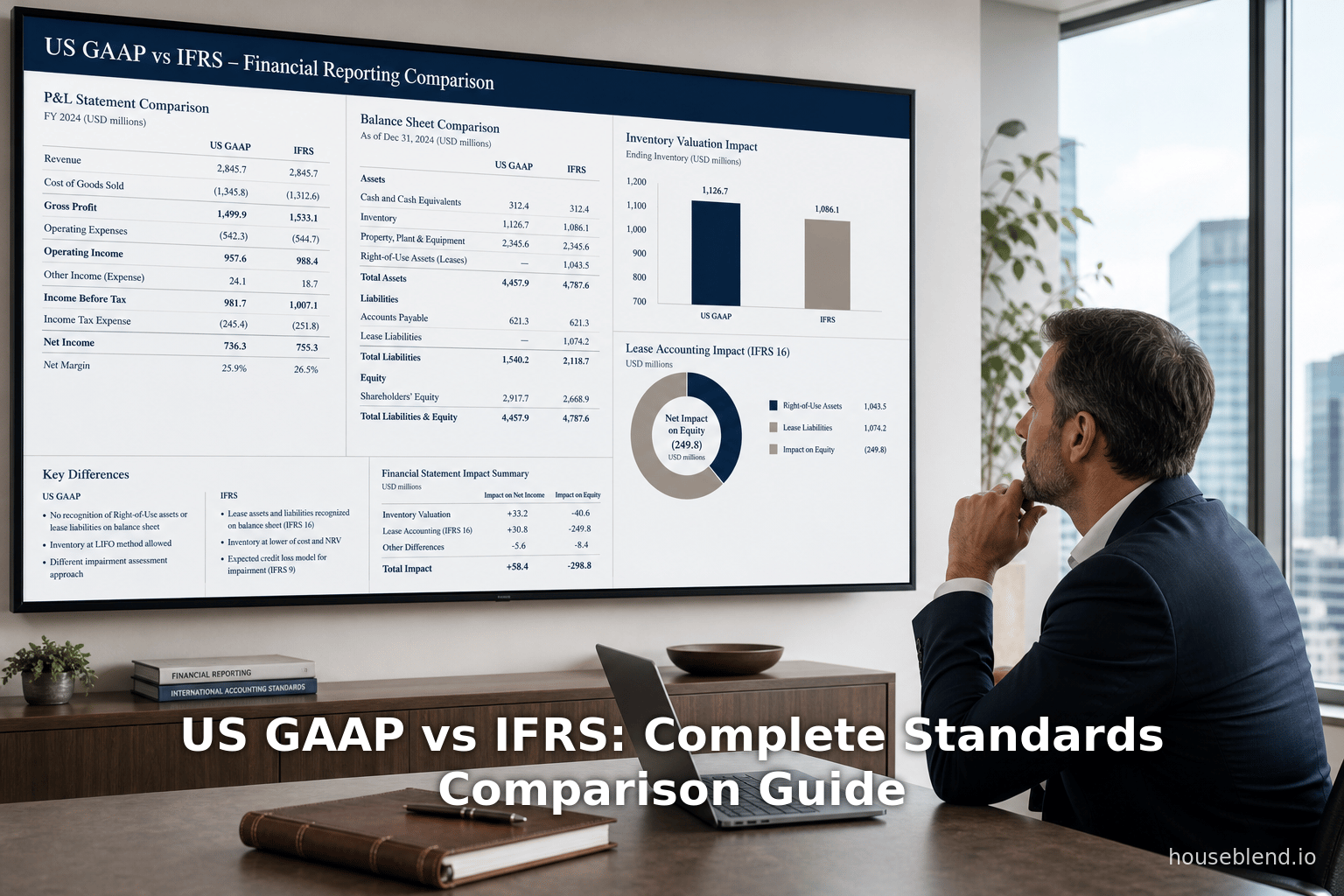

| Inventory (costing) | IAS 2 prohibits LIFO; valuations at lower of cost and net realizable value (NRV) [3] [4] | ASC 330 allows LIFO and lower-of-cost-or-market (replacement cost) for LIFO/retail items [3] [17] | LIFO differences can lead to higher inventory/profits under GAAP if LIFO used (no LIFO under IFRS) [4]; CFOs must adjust margin and tax planning. |

| Inventory write-downs | Reversal allowed up to original cost if NRV recovers [18] | No reversal permitted once inventory is written down (except for LCM floor) [18] | IFRS financials may improve (higher profits) in recovery years; GAAP profits remain lower. |

| Property, Plant & Equipment | IFRS allows upward revaluation to fair value for PPE/intangibles; mandatory component depreciation (IAS 16) | US GAAP disallows revaluation; allows component depreciation by policy elections | Revaluations and components can change asset base and depreciation (thus profit) under IFRS; CFOs must track component costs and revaluation effects. |

| Revenue Recognition | IFRS 15 revenue recognition (“five-step”) and core principle (focus on transfer of control) [19] | ASC 606 revenue recognition (very similar to IFRS 15); many specifics aligned, but differences remain (e.g. treatment of taxes, licence renewals) [19] | Although largely converged, subtle differences (e.g. handling of variable consideration or licenses) can cause different timing or amounts; CFOs need to reconcile reported revenue patterns. |

| Leases (lessees) | IFRS 16: single lessee model (all leases on-balance sheet as ROU asset & liability), no classification by lease type [5] | ASC 842: dual model; leases classified as finance (capital) or operating (even though all now on-balance sheet) [5] | IFRS typically yields higher initial expenses (interest + depreciation) vs GAAP operating lease (straight-line expense) [5]; CFOs should compare lease portfolios under both models for analysis. |

| R&D and Internally Developed Intangibles | IAS 38: Research costs expensed; development costs capitalized if criteria met [6] | ASC 730: All R&D costs expensed as incurred (with limited capitalization for software, etc.) [7] | IFRS may report higher assets (from capitalized development) and higher future amortization. CFOs need to assess capitalization policies impacting current versus future expenses. |

| Goodwill Impairment | IAS 36: One-step recoverable amount test for CGU (higher of fair value less costs or value-in-use); no impairment reversal [9] [10] | ASC 350: Similar test (recently revised to one-step for GAAP), but losses limited to carrying goodwill of the reporting unit [10] | IFRS can result in smaller impairment charges if “value-in-use” exceeds GAAP fair value; IFRS spreads loss over whole CGU, GAAP caps loss at goodwill only [9] [10]. CFOs must reconcile goodwill carrying values and impairment timing accordingly. |

| Financial Instruments | IFRS 9: Classification in three buckets (FVTPL, FVTOCI, amortized); expected credit loss (ECL) model with staging | ASC 326 (CECL): Generally all debt instruments measured at amortized cost using a lifetime ECL; equity securities usually FVTPL or FVTOCI without recycling | Timing and size of credit loss provisions differ (IFRS stages only when credit quality declines vs GAAP immediately estimates full lifetime loss). CFOs forecasting impairments may see variance. |

| Classification of Cash Flows | IAS 7: Operating, Investing, Financing categories; interests and dividends may be classified in operating or financing/investing (entity choice) [8] | ASC 230: Similar three categories; but interest paid and dividends paid are generally operating; interest and dividends received usually operating (dividends may be investing for some) [8] | The cash flow statement under IFRS can differ (e.g. finance costs as financing vs GAAP mandatory in operating) [8]. CFOs must reclassify cash flows to compare IFRS vs GAAP reports. |

| Income Taxes | IAS 12: Deferred taxes on all temporary differences (no exceptions except “initial recognition exception” for non-BizComb items); uses substantively enacted tax rates [20] [21] | ASC 740: Similar deferred tax model, but no initial recognition exemption; uses enacted tax rates | E.g. when acquiring an asset at cost, IFRS may not book deferred tax if outside business combination (initial recognition exception) [21], whereas GAAP would. Also, IFRS may require deferred tax on revalued PPE (GAAP has none). CFOs must reconcile tax provisions across standards. |

| Other Comprehensive Income (OCI) | Slight differences in what items go in OCI and whether they can be recycled (e.g. IFRS recycling of FX on net investments, GAAP too; IFRS OCI for equity FV chosen once, GAAP prohibits recycling for equities) | GAAP and IFRS have somewhat different OCI items (e.g. actuarial gains/losses entirely in OCI under IFRS, under GAAP they go to income) | OCI volatility and recycling rules can change net income. CFOs should note that total comprehensive income may diverge between standards even if net income is same. |

Table: Selected major differences between IFRS and U.S. GAAP on key accounting topics. Each row highlights the divergent treatments under the two frameworks and the potential impact on financial results and analysis. (Citations give authoritative sources for each difference.)

Historical Development and Convergence

Understanding how IFRS and US GAAP evolved illuminates why they differ today. Key milestones in their development include:

-

Early Harmonization Efforts (1970s–1990s): In 1973, the International Accounting Standards Committee (IASC) was formed to create international standards (IAS) [22]. Over the 1980s and 1990s, organizations like IOSCO increasingly endorsed IAS, pressing for comparability. By the late 1990s, many countries were converging national GAAP with IAS.

-

Formation of IASB and IFRS (2001): In April 2001, the IASC was restructured into the International Accounting Standards Board (IASB), and the standards were rebranded as International Financial Reporting Standards (IFRS) [22]. The IASB then expanded and refined the standards (e.g. IAS 39 to IFRS 9, IAS 17 to IFRS 16).

-

US GAAP Evolution: US accounting standard-setting similarly took form in 1973 with the Financial Accounting Standards Board (FASB) creation, replacing earlier committees (AICPA’s APB, etc.). Over time, US GAAP grew highly detailed, culminating in the Codification release in 2009 (amalgamating all existing GAAP). The conceptual framework (Statement of Financial Accounting Concepts) was also developed to guide standard setting.

-

SEC and Convergence: In 2002, FASB and IASB signed the Norwalk Agreement, committing to joint convergence projects. Over the next decade, they issued converged standards on major topics (especially leases and revenue). In 2006, SEC Chairman Cox and EU Commissioner McCreevy announced plans to eliminate the GAAP-IFRS reconciliation requirement for EU issuers [23], and in 2010 the SEC reiterated that a single set of high-quality global standards would benefit investors [15]. However, progress on full convergence slowed after 2010, and the SEC’s long-anticipated proposal to allow or require US companies to use IFRS never materialized [15]. Today, the U.S. remains committed to GAAP for domestic issuers, although GAAP continues to be influenced by select IFRS concepts (e.g. impaired-loan accounting).

-

Global IFRS Adoption (2000s–2010s): A landmark was the EU Regulation (EC) 1606/2002: effective for financial years starting 2005, it mandated IFRS for all EU-listed companies [16]. Many other jurisdictions followed suit. For example, Canada and Korea adopted IFRS (effective around 2011), Japan permits IFRS option, and numerous emerging markets aligned with IFRS. An IFRS Foundation report (2018) found that 144 of 166 reporting jurisdictions required IFRS Standards, covering 99% of global GDP [1]. (By contrast, the U.S. was one of only about 10 jurisdictions not applying IFRS for consolidation [1].) This global adoption means U.S. CFOs of multinational corporations must often translate foreign accounting (IFRS or local GAAP) into US GAAP for consolidated reporting, or vice versa.

-

Ongoing Convergence Projects: While some standards have been jointly aligned (revenue, leases, financial instruments impairments, etc.), other areas have diverged again. For instance, the IASB’s IFRS 16 (leases) and FASB’s ASC 842 were developed separately, resulting in key differences in lessee accounting [5]. Both boards continue to monitor differences: for example, IFRS deferred consideration for income taxes on some revaluations (IAS 12) vs GAAP 保者 for tax law changes timing (ASC 740) [20]. In summary, convergence has improved comparability in several areas, but “significant differences remain” [14], reinforcing the need for CFOs and analysts to be versed in both regimes.

IFRS vs US GAAP: Conceptual and Structural Differences

At a high level, IFRS and US GAAP differ in their philosophy and approach:

-

Principles-Based vs Rules-Based: IFRS is often characterized as principles-based. It sets broad objectives (e.g. “recognize revenue when control transfers”) and relies on the substance of transactions. US GAAP is more rules-based, containing many detailed criteria and bright-line tests. This means IFRS may require more judgment and interpretation. For example, IFRS’ definitions of assets and liabilities (IFRS Conceptual Framework) are more general, whereas GAAP’s criteria (in the Concepts Statements and numerous rulings) are sometimes transaction-specific. CFOs must recognize that under IFRS, management judgment and disclosure are critical, whereas GAAP prescribes the application in fine detail.

-

Standard Setting and Enforcement: IFRS is set by an independent international board (IASB) without formal country-level control (though many governments formally endorse IFRS). US GAAP is set by FASB under U.S. law (with oversight by the SEC for public companies). The SEC has the legal power to overrule or incorporate IFRS, but it has chosen not to adopt IFRS for U.S. issuers [15]. Enforcing agencies differ: IFRS enforcement is country-dependent (e.g. European regulators); US GAAP enforcement is primarily through the SEC (for public companies).

-

Framework Structure: Both frameworks have multiple documents, but IFRS Standards are organized as individual pronouncements (IFRS 1–17, IAS 1–41) with Illustrative Examples and Interpretations (IFRICs). The FASB Codification (ASC) consolidates all GAAP by topic. Terminology differs slightly: IFRS calls the income statement the Statement of Profit or Loss (and/or Other Comprehensive Income), whereas GAAP uses Income Statement. IFRS requires a Statement of Changes in Equity and optionally a single or multi-part income/OCI Statement; GAAP requires a separate Statement of Comprehensive Income if any OCI items exist. Such differences in presentation must be handled in consolidations.

-

Objective of Financial Statements: Both frameworks share the same goal of providing useful information. However, IFRS explicitly emphasizes comparability for global investors, whereas US GAAP historically emphasized protecting investors and creditors in the U.S. context. For example, IFRS often exposes more volatility (through fair values in income or OCI), arguing it better reflects economic substance; GAAP sometimes filters volatility (e.g. by smoothing impairments or forbidding revaluations). CFOs should be aware that IFRS statements might exhibit more variability with market conditions due to fair-value accounting (and that they could face larger deferred tax charges from revaluation surpluses, which GAAP would never recognize [2]).

-

Comprehensiveness and Updates: US GAAP and IFRS both continuously update. As of 2024, FASB and IASB have each issued new standards (e.g. IFRS 17 for insurance, ASC 842 for leases). Notably, FASB sometimes changes rules more frequently with narrow-scoped updates, whereas IASB often conducts comprehensive overhauls. For instance, finance lease accounting changed differently: IFRS 16 took effect in 2019, while GAAP waited until 2022 for non-public entities, and even then maintained the lease-type distinction [5]. CFOs must keep abreast of these evolving standards, as their timing and content can diverge.

Global Adoption and Use of IFRS vs US GAAP

The split between IFRS and US GAAP also follows geography and listing status. Key data points:

-

Worldwide IFRS Adoption: The IFRS Foundation reports that as of early 2018, profiles of 166 jurisdictions covered 99% of global GDP. Of these, 144 jurisdictions (87%) require IFRS Standards for all or most public companies, and 12 jurisdictions permit IFRS [1]. Only about 10 jurisdictions (including the US) neither require nor permit IFRS for consolidated statements [1]. This means that companies in most countries (EU, UK, Canada, Australia, China’s HK/if listed, much of Africa/Asia/Latin America, etc.) use IFRS. For example, effective 2019, 17 West and Central African countries adopted IFRS as the uniform standard (OHADA bloc) [24]. In Europe, the 2002 EU regulation made IFRS mandatory for listed EU companies starting 2005 [16].

-

US GAAP Use: The United States remains largely on US GAAP. However, foreign companies listed in the US are allowed to use IFRS without reconciliation to GAAP (since 2007, SEC rules) – a notable carve-out that means a significant number of large foreign firms (e.g. Japanese, UK, Canadian multinationals) report under IFRS to US investors. Indeed, analysis of the Fortune Global 500 (2021) shows 64 companies headquartered outside the US; 50 of those (78.1%) use IFRS for reporting [25]. By contrast, all 36 of the top Global 500 in the US use US GAAP [25]. Thus, IFRS is the dominant framework among the world’s largest companies outside the US.

-

Summaries of IFRS vs GAAP Use: A global “cheat sheet” shows that IFRS is either required or permitted in virtually every major region except (nominally) the US. The table below illustrates the degree of worldwide adoption:

IFRS Standards Adoption Status Number of Jurisdictions* Notes (examples) Required (mandatory) 144 [1] e.g. EU, UK, Australia, Canada, China (for listed), Most of Asia/Africa/adopting countries. Permitted/Optional 12 [1] e.g. Japan (optional), certain Middle Eastern or Asian markets allow IFRS, etc. Not permitted (use only local GAAP) ≈10 e.g. United States (primarily US GAAP), possibly a few smaller economies [1]. *Source: IFRS Foundation (2018) [1].

-

Trends and Future: The trend has been a net expansion of IFRS. For example, the IFRS Foundation news release notes that IFRS profiles (mandatory vs permitted) are continually updated, reflecting new adopters [1]. By contrast, US GAAP remains largely domestic. The IFRS Foundation and global standard-setters continue to advocate for global consistency; however, as of 2026 no immediate plan exists to require US companies to report in IFRS. In fact, SEC staff concluded in 2012 that the cost of replacing US GAAP outweighed the benefits, so GAAP remains in force for US issuers.

For CFOs of multinationals, this means juggling two “languages.” A US-based CFO with foreign subsidiaries will typically restate those entities’ books into US GAAP for consolidation, while a non-US CFO with global operations may produce IFRS financials but furnish GAAP reports for any US regulators. Statistical insight: a recent study of global filers notes that companies reporting under IFRS in the US had to reconcile hundreds of differences (e.g. foreign carmakers use IFRS but reconcile to GAAP in US filings [14]). As one CPA Journal study observed, “several years of noteworthy progress” in convergence have occurred (e.g. lease and revenue Phase I), but “significant differences remain” [14]. This reality means CFOs and investors must often be “bilingual” – comfortable reading and interpreting statements under both frameworks [13].

Major Technical Differences by Topic

Below we analyze detailed differences between IFRS and US GAAP in key accounting areas. Each sub-section focuses on one topic, presenting the IFRS approach, the GAAP approach, and implications. (Many of these analyses draw on authoritative comparative guides and accounting literature. Citations are provided for the specific differences highlighted.)

Revenue Recognition

Standards: IFRS 15 (Revenue from Contracts with Customers) and ASC 606 (the GAAP equivalent) were jointly developed to converge revenue rules. Both use a five-step model (identify contract, performance obligations, transaction price, allocation, recognition) and became effective around 2018 for public companies. In principle, both require recognizing revenue to depict transfer of promised goods/services for the consideration expected [26].

Differences: Despite convergence, subtle differences remain that can affect timing or amount. KPMG notes major differences include: handling of taxes, treatment of variable consideration thresholds, contract modifications, license revenue, and onerous contract recognition [19]. For example, IFRS 15 provides guidance on presenting certain sales taxes that may result in gross vs net presentation differences compared to GAAP. The IASB has refined IAS 37 (onerous contracts) which can impact revenue contracts, while FASB issued additional guidance on licenses and business combinations. In practice, these differences mean comparable transactions might produce slightly different revenue under each framework [19].

Impact on CFOs: Since revenue is a core performance metric, CFOs must ensure consistency when comparing IFRS-based revenue to GAAP peers. Any difference in recognizing revenue (even timing of a few quarters) can confound trend analysis. For deals with complex contracts, CFOs should analyze IFRS vs GAAP revenue models side by side. Ongoing FASB-IFRS projects (e.g. updates to ASC 606 implementation guidance) may narrow differences, but for now companies must document any IFRS/GAAP gaps. Investors often focus on recurring revenue, so even minor differences in applying the principles-based IFRS vs rules-influenced GAAP can have material effects.

Leases

Standards: IFRS 16 (effective 2019) and ASC 842 (effective 2019-2021) replaced the previous lease accounting (IAS 17, ASC 840). Both require virtually all leases to be recorded on the balance sheet as a right-of-use asset and a corresponding lease liability.

Key Differences: - Lessees’ expense recognition (“Day Two”): IFRS 16 uses a single finance-type model for all leases – lessees automatically treat each lease as a finance lease, so the income statement shows depreciation of the ROU asset plus interest on the liability [5]. In US GAAP (ASC 842), leases are still classified (as under old rules) into finance (capital) or operating categories: finance leases produce the same expense pattern as IFRS (interest + depreciation), but operating leases (still on-balance sheet) result in a straight-line total lease expense (offsetting interest and amortization in a single figure) [5]. This leads to different P&L shapes for operating vs finance leases between the standards.

-

Lease modifications and remeasurement: IFRS 16 requires remeasuring the lease liability when payments change due to indices or rate changes (e.g. CPI adjustments) [27]. Under GAAP, index-linked payments are generally not remeasured unless certain criteria are met. Also, GAAP offers a practical expedient not present in IFRS: under ASC 842, some lease modifications can be accounted for as new leases or as adjustments without full remeasurement, depending on facts.

-

Low-value and short-term leases: Both permit exemptions, but IFRS explicitly allows all “low value” leases to bypass the ROU model; ASC 842 does not have a formal low-value exemption (only short-term lease exemption). This means IFRS might keep more small leases off-balance-sheet compared to GAAP.

Implications for CFOs: For companies with significant operating leases (e.g. retail, airlines), the two models diverge in reported expenses. IFRS 16 lessees typically report higher total expense in early years (because interest front-loads) compared to GAAP operating lease expense, which is straight-lined [5]. Thus, profit measures like EBITDA can differ (IFRS 16 boosts EBITDA since interest is below EBITDA, whereas GAAP operating lease expense is above EBITDA). CFOs must reconcile these impacts for investors. Lease liability measurements also differ over time with IFRS adjustments for indices; CFOs should update cash flow forecasts accordingly. From a systems perspective, IFRS implementation often required changes to asset management and accounting entries – CFOs need robust lease tracking and accounting systems to handle both standards.

Research & Development (R&D) Costs

Standards: IFRS addresses R&D under IAS 38 (Intangible Assets), whereas US GAAP uses ASC 730 (Research and Development).

Differences: The treatment of development-phase costs is the major divergence:

-

IFRS (IAS 38): All research-phase costs are expensed. For development-phase, IFRS requires capitalization of development expenditures if and only if specified criteria are met (“probable economic benefits” test, technical feasibility, etc.) [6]. Thus, internally-developed intangible assets (e.g. new patents, software) are capitalized on the balance sheet and later amortized, if the firm can demonstrate future benefit [6]. Many companies (especially in technology, biotech, etc.) capitalize significant development costs.

-

US GAAP (ASC 730): Almost all R&D costs are expensed as incurred. GAAP only allows capitalization in very limited circumstances (e.g. software development for internal use or certain equipment leases), but not for typical product development. There is no general capitalization of development costs under GAAP [7].

Implications for CFOs: The IFRS approach typically yields higher assets and higher future amortization, whereas US GAAP yields higher current expenses and lower assets. For a multinational with IFRS and GAAP books, R&D capitalization differences can create mismatches in profits and balance sheet levels. For example, a drug company's IFRS statements may show significant R&D assets (and smaller losses) while its US GAAP statements show larger losses and no intangible asset. CFOs must ensure disclosures reconcile these differences and can explain performance variations due to this accounting policy. Furthermore, IFRS is evaluating IAS 38’s relevance (IASB proposals as of 2025), and GAAP has proposals on improving R&D guidance, so CFOs should watch for any future standard changes.

Inventory

Standards: IFRS prescribes IAS 2 for inventories; US GAAP uses ASC 330. Both require inventories to be measured at the lower of cost and value (cost or market), but the details differ:

-

Cost formulas: IFRS allows FIFO or weighted-average cost methods only [3]. LIFO (last-in, first-out) is explicitly prohibited under IAS 2 [28]. In contrast, US GAAP permits LIFO or FIFO or weighted-average [3]. Many US companies (especially when inventory is significant) use LIFO for tax benefits. Under IFRS prohibition, LIFO users must convert to FIFO/WA.

-

Lower-of-cost-or-market/NRV: Under IFRS, any inventory must be written down to net realizable value (NRV) (selling price minus costs to sell) if lower than cost [3]. US GAAP also uses a lower-of-cost-or-market approach, but defines “market” differently. For LIFO or retail-method inventories, GAAP’s “market” is replacement cost (subject to ceiling/floor rules) [29], not NRV. Under FIFO/WA, GAAP effectively also uses NRV, aligning with IFRS [3] [17].

-

Reversal of write-downs: IFRS requires reversal of a previously recognized inventory write-down if NRV later increases (capped to original cost) [18]. US GAAP prohibits reversing an inventory write-down [30].

Implications for CFOs: The LIFO prohibition can significantly affect a US company’s reported gross profit if they switch to IFRS-like inventory. CFOs must eliminate LIFO layers in consolidation and adjust tax assets accordingly. The ability to reverse write-downs under IFRS means inventory values (and profits) may recover in later periods—GAAP companies cannot do this. Such write-downs and recoveries impact cost of goods sold and OCI differently under each framework. CFOs budgeting future margins need to consider that IFRS margins could swing more with NRV reversals.

Property, Plant & Equipment (PPE) and Intangible Assets

Standards: IFRS uses IAS 16 for PPE and IAS 38 for intangibles; US GAAP has ASC 360 (PPE, called “PP&E”) and ASC 350/985 (goodwill and intangibles).

Revaluation Model: IFRS allows an entity to choose either the cost model (carrying at cost less depreciation) or a revaluation model (carrying at fair value with periodic revaluations) for classes of fixed assets [2]. US GAAP forbids upward revaluations – fixed assets remain at historical cost (less Accumulated Depreciation). IFRS revaluation increases feed through OCI (after tax), creating deferred tax liabilities in many cases [2]. In practice, IFRS companies can have drastically different book values (and equity) than GAAP peers (if revaluations are taken).

Depreciation/Amortization: IFRS explicitly requires component depreciation: significant parts of an asset that have different useful lives must be depreciated separately. US GAAP does not mandate full componentization (though it encourages “material parts”). This means IFRS profits can differ if components have very short lives (e.g. an office building roof vs structure).

Impairment: Both IFRS and GAAP require impairment tests on PPE and intangibles (outside goodwill) when indicators arise. IFRS (IAS 36) uses a one-step “recoverable amount” test (higher of fair value less costs or value-in-use) against carrying value [9]. GAAP historically used a two-step test (currently a one-step iterative test is now allowed after ASU 2017-04) and generally focuses on fair value impairment. A key difference is reversals: IFRS allows impairment reversals for revalued assets (and intangibles) when recoverable amount grows again [18], while GAAP prohibits reversals for PPE/intangs.

Implications for CFOs: IFRS revaluation and impairment approach often makes depreciation and profit figures more volatile than GAAP. For example, companies that used IFRS revaluation of land or buildings have historically shown much higher book equity (and higher deferred taxes) than GAAP counterparts. CFOs must note that IFRS balance sheets and OCI can shift significantly if market values change; under GAAP they would not. In planning capital hires or write-offs, CFOs should compare both models to see if the choice affects debt covenants or returns metrics.

Financial Instruments

Standards: IFRS 9 (and related standards) vs. FASB’s ASC 320/321/825 cluster. Key differences include classification, measurement, and impairment.

-

Classification/Measurement: IFRS 9 classifies financial assets into three categories: Amortized Cost, FVOCI (Fair Value through Other Comprehensive Income), and FVTPL (through Profit or Loss), based on business model and cash flow characteristics. GAAP splits assets into a few buckets (HTM, AFS, trading in older ASC 320, now amortized or FV categories under ASC 321/825). One notable difference: IFRS permits an irrevocable FVOCI option for certain equity investments (with no recycling of gains), whereas US GAAP requires equity securities to be either FVTPL (unless an election to use fair value with changes in earnings) [19].

-

Impairment: IFRS 9’s expected credit loss model has three stages, moving from 12-month ECL to lifetime ECL as credit risk worsens. US GAAP’s CECL (ASC 326) uses a lifetime ECL for all loans from day one (no staging). Also, IFRS 9 allows reversal of impairment allowance (subject to stage changes); GAAP CECL has no reversals because it always measures lifetime expected losses.

Implications for CFOs: For banks and financial institutions, differences between IFRS 9 and CECL can cause dramatically different allowance levels, especially at initial recognition. CFOs should analyze credit losses forecasts under both models. Also, classification differences (e.g. treating a bond as FVOCI vs AFS, or equity without recycling) can affect the timing of income vs OCI for market movements. Accurate mapping is needed when consolidating IFRS subsidiary financial instruments into GAAP statements, as FASB’s categories and impairment rules differ.

Consolidation and Control

Standards: IFRS 10 (Consolidated Financial Statements) vs ASC 810 (Consolidation). Both use the concept of “control” to determine consolidation, but diverge significantly.

Key Differences: The IASB and FASB define control somewhat differently:

-

Single vs Dual Model: Under IFRS 10, there is a single control model: an investor controls a subsidiary if it has power over relevant activities, exposure to variable returns, and ability to use power to affect returns. US GAAP has a two-tier model: a voting-interest model (control if you own >50% voting rights) or a Variable Interest Entity (VIE) model (for entities with insufficient equity, where control is based on absorbing variability). Thus, IFRS applies one unified test for all entities, whereas GAAP sometimes uses the VIE rules when dominant voting interest is absent.

-

VIE Considerations: IFRS explicitly considers potential voting rights (e.g. options that confer control) when assessing control; GAAP has different triggers for VIE analysis. In practice, IFRS tends to result in slightly broader consolidation (since it focuses on who truly has power and returns) whereas GAAP’s technical rules can exclude some entities from consolidation.

Implications for CFOs: The consolidation treatment can change reported debt and equity. CFOs should review all special-purpose entities and joint arrangements to ensure consistent application. For example, an entity might be unconsolidated under US GAAP (treated as an unconsolidated affiliate) but consolidated under IFRS because IFRS sees control. Differences in the SSAE from consolidation can affect leverage ratios and interest coverage calculations. Recognizing these, big-four guides emphasize that preparers must be aware of “potential voting rights” and control criteria differences [31] [32].

Cash Flow Statement

Standards: IAS 7 (Statement of Cash Flows) vs ASC 230. Both require the three-section cash flow statement (Operating, Investing, Financing).

Differences: While the overall objective is the same, IFRS and GAAP have notable divergences in classification:

-

Operating Activities: IFRS allows companies to choose whether interest paid/received is classified as operating or financing, and whether dividends received are operating or investing. GAAP is stricter: interest paid is always operating (ASC 230), dividends paid are financing, interest and dividends received are operating in most cases (dividends received may be investing if explicitly choosing the indirect method).

-

Borrowing Costs: IFRS requires inclusion of all interest paid as either O or F by policy choice [8], whereas GAAP requires interest paid in operating (CF from operations). Similar issues with dividends: IFRS sometimes allows flexibility.

-

Convertible Debt & Others: IFRS and GAAP differ on classification of repayments of principal on convertible debt (GAAP financing vs IFRS bifurcates interest vs liability elements), on bank overdraft (under IFRS may be financing, in US always shown in operating section), etc.

KPMG’s IFRS Institute article summarizes that classification of interest, dividends, and lease payments often differs under the two rules [8]. For example, IFRS’s flexibility can “significantly impair comparability” with GAAP cash flows [8].

Implications for CFOs: Cash flow presentation can affect analysis of operating cash generation. A CFO comparing IFRS vs GAAP statements must often reclassify cash flows to compare apples-to-apples. For example, an IFRS company might report cash interest in financing (if chosen), whereas its US peer reports it in operations. CFOs should be prepared to adjust free cash flow and operating cash flow figures to a common basis, and to explain differences to analysts.

Income Taxes

Standards: IAS 12 vs ASC 740 govern current and deferred income taxes. The underlying principle (deferred taxes on temporary differences) is similar, but certain rules diverge:

-

Substantively Enacted Tax Rates: IFRS uses substantively enacted tax rates to measure current/deferred taxes [20] – meaning a tax law is recognized when it is effectively finalized (e.g. parliamentary approval even if formal signing occurs later). GAAP uses enacted rates (GAAP limits recognition of tax law changes to after enactment). This timing difference can shift tax expense recognition between periods [20].

-

Initial Recognition Exemption: IFRS has an “initial recognition exception”: when an asset or liability is acquired that does not affect accounting or taxable profit initially (e.g. buying PPE in a country where no tax basis exists), no deferred tax is recognized initially [21]. Under US GAAP, such temporary differences would create deferred taxes. Thus, IFRS may understate deferred taxes on initial purchase compared to GAAP.

-

Asset Revaluations: IFRS permits revaluation of PP&E/intangibles (IAS 16, IAS 38) which creates temporary differences. Deferred tax must be recognized on that uplift [2]. GAAP has no revaluation, so no resulting deferred tax. For example, in an IFRS revaluation upward, a deferred tax liability arises (cash flow effect in later disposal); under GAAP, the asset would remain at historical cost with no deferred tax impact.

Implications for CFOs: These differences mean tax provisions and balances differ under IFRS vs GAAP for identical operations. CFOs should note that IFRS may report lower deferred tax assets/liabilities on certain acquisitions (per the exception) and higher DTLs on revalued assets, compared to what GAAP would show. In disclosures, management must reconcile how each standard’s tax accounting affects profit and equity. A sudden enactment of a tax rate change (e.g. a 2017 corporate tax reform in the US) is recognized earlier in GAAP profit than in IFRS (where it awaits final legislative steps) [20]. Awareness of these nuances is vital for both planning and communicating tax expense differences to stakeholders.

Other Areas (Briefly)

-

Equity vs Liability: IFRS and GAAP have subtle differences in the criteria for classifying a financial instrument (or contract) as equity or liability (the so-called “debt/equity classification”). For instance, certain share-based payments and convertible instruments may be treated as equity under one framework and liability under the other. This can affect leverage ratios and interest expense.

-

Presentation Formats: IFRS requires either a single statement of profit or loss and OCI or two separate statements; GAAP requires two statements if OCI exists. IFRS also requires a Statement of Changes in Equity; GAAP requires this too. However, some line items (like extraordinary items, discontinued operations) have been eliminated under IFRS (they were already mostly eliminated under GAAP). Reporting segments are defined similarly but differ in specifics (e.g. IFRS business segments reflect how management views the business, while GAAP had specific criteria for aggregation).

-

Earnings Per Share (EPS): IFRS and GAAP EPS rules are largely aligned (both comply with IAS 33/ASC 260). However, one difference is bonus share issues: IFRS requires restatement of prior EPS when bonus shares are issued (as if shares existed), whereas GAAP does not see this as a retroactive share split [18]. CFOs need to adjust historical EPS trends if comparing IFRS vs GAAP filers.

-

Other Comprehensive Income (OCI): While both standards include OCI, some line items differ. For example, under GAAP, stock-based comp tax effects went to OCI in certain cases, but IFRS does not allow that. Details vary by item; CFOs should review each OCI component when reconciling standards.

-

Segment Reporting: IFRS 8 (segments) and ASC 280 are converged on a “management approach,” but minor differences in disclosures can exist. Noteworthy for CFOs is that IFRS does not distinguish between “reportable” and “operating” segments like GAAP used to; IFRS simply reports all management segments chosen by executives.

These examples illustrate that across virtually every area of accounting, IFRS and GAAP have differences, whether large or small. As noted by audits and regulatory sources, even efforts to align (like joint revenue and lease standards) leave residual gaps [14] [19]. CFOs need detailed knowledge of these nuances to accurately consolidate, communicate, and compare financial statements.

Convergence Efforts and Current State of Alignment

Over the past two decades, IFRS and US GAAP have undergone both convergence (common projects) and divergence (new separate standards).

Past Convergence Projects

-

Norwalk Agreement (2002): FASB and IASB committed to “converge” major standards to within a short-term horizon [33]. This resulted in joint or coordinated projects on business combinations, fair value measurement, financial instruments, leases, and revenue.

-

Successes: - Revenue Recognition: IFRS 15 and ASC 606 (2014-2015) are essentially identical in core principles [26], though each standard setter has since issued narrow refinements.

- Leases: IFRS 16 and ASC 842 (2016) both put most leases on-balance-sheet. Key differences remain (as earlier discussed [5]).

- Financial Instruments: The IASB’s IFRS 9 (2014) and FASB’s concurrent CECL (2016) replaced the “incurred loss” model. Convergence was partial: both require ECL estimates, but IFRS uses 3-stage vs GAAP lifetime consistently. The units of classification also differ (Stage vs no staging).

- Other Topics: Some alignment in share-based payment attribution, segments, joint ventures, etc. In 2020, FASB adopted IFRS’s prohibition of extraordinary items in net income (ASC 225), reflecting IFRS (IAS 1) which never allowed them.

-

Remaining Gaps: Despite these efforts, regulatory and accounting bodies acknowledge continuing differences. As the CPA Journal article puts it, “significant differences remain” after accounting standards converged on revenue and lease guidance [14]. PwC’s 2023 comparatives guide details hundreds of differences, underscoring that full convergence has not been achieved [13].

Current State

-

Regulatory Stance: The US SEC in the 2010s signaled no immediate mandate to adopt IFRS for US issuers (SEC’s 2012 Final Staff Report on IFRS noted low adoption appetite [34]). Thus, U.S. companies continue under GAAP. Meanwhile, IFRS continues to evolve globally through IASB agendas (e.g. IFRS 17 for insurance, IFRS 14/16 amendments). FASB and IASB no longer have binding joint projects; they do collaborate informally (e.g. @IASB minutes).

-

Accounting Firms and Guidance: All Big Four and large firms continue publishing detailed comparative guides (e.g. PwC’s 2023 IFRS and US GAAP: Similarities and Differences, Grant Thornton’s updates) highlighting hundreds of differences [13] [35]. The volume of these guides – PwC’s latest is 236 pages [13] – indicates complexity. A summary observation is that full compliance in one framework does not guarantee easy translation to the other. For many preparers, being “financially bilingual” is an operational necessity [13].

-

Implications for Financial Communications: Analysts and investors following multinational companies must pay attention to the standards used. Inconsistencies can otherwise be mistaken for performance differences. For example, two competing auto manufacturers might appear to have different debt levels solely because one consolidates a captive finance affiliate (IFRS) and the other does not (GAAP VIE rules). These subtleties are part of what convergence discussions tried to address, but remain in flux.

Future Implications

Looking ahead, several dynamics are relevant for CFOs:

-

IFRS Developments: The IASB periodically reviews post-implementation and emerging issues. Projects on climate-related disclosures, digital reporting, and ESG (broadening narrative reporting) are more IASB-driven currently. For technical GAAP convergence, IFRS leads on topics like intangible R&D which may influence future GAAP (FASB proposals on intangibles).

-

US GAAP Developments: FASB has initiated some adoption of IFRS ideas (e.g. income tax recognition, credit loss model). But it also remains influenced by US policy priorities (e.g. simplified lessor accounting, prioritizing private company needs).

-

Potential Convergence: Both boards have reduced formal joint projects, so wholesale IFRS adoption in the US in the near future seems unlikely. However, continued alignment in certain areas (leases, revenue, credit losses) shows practical convergence. CFOs should monitor both IASB and FASB pronouncements, as each sets the agenda for its constituency. In multinational planning, it is wise to prepare for differences to remain and update internal models accordingly.

As one analyst noted, IFRS has “thrived and become the most widely used accounting standard” globally, even without US mandate [36]. The U.S. sample (Cox, 2010) reaffirmed the benefits of a single set of accounting standards [15], but the reality is that for the foreseeable future, IFRS and US GAAP will coexist. CFOs and finance teams must therefore continue to map between them, training staff, and disclosing differences to investors.

Impact and Case Studies

To illustrate the real-world impact of IFRS vs GAAP differences, we present case studies and scenarios that highlight challenges and benefits from a CFO perspective.

Case Study: Transition from US GAAP to IFRS

Scenario: A multinational consumer products firm headquartered abroad had been using US GAAP for its foreign subsidiary reporting, but its home country mandated IFRS. The CFO spearheaded a conversion of the company’s consolidated statements from US GAAP to IFRS.

Source: A BDO case study describes “a leading global consumer products company’s journey from U.S. GAAP to IFRS” [37]. Key points:

- The company faced compliance risk: it hadn’t been IFRS-compliant in its home market. Operating under US GAAP abroad no longer met statutory requirements [38].

- The CFO (with external advisors) began a large-scale project to reconcile and recast financials. They performed a scoping analysis to identify differences between the GAAP books and IFRS-adjusted books [39].

- The result: converting to IFRS allowed the company to “streamline the company’s workforce and reduce operational costs” by eliminating duplicate GAAP filings [40]. Going forward, the finance team could produce IFRS statements internally.

This illustrates several CFO lessons:

- The driver for conversion was regulatory (home country compliance) and strategic (global comparability).

- The process required detailed gap analysis (account by account) to reconcile GAAP and IFRS bases [39].

- In the transition, the CFO leveraged external IFRS expertise (BDO’s IFRS practice) to manage complexities.

- The outcome included not only compliance but also improved efficiency and workforce empowerment [40].

CFO Takeaway: Projects that switch accounting frameworks (e.g. GAAP→IFRS) are major undertakings but can yield long-term benefits in consolidation, systems, and investor communication. CFOs should weigh the costs (training, system changes) against benefits (e.g. single accounting language for global investors). Detailed planning and expert guidance are crucial when addressing dozens of IFRS–GAAP differences across financial statement line items.

Impact on Reported Financials and Metrics

Consider a hypothetical example of inventory and R&D:

-

A US oil and gas producer (with GAAP) values heavy equipment using LIFO for tax benefits. It reports low net income in inflationary periods (due to high COGS) and builds up deferred tax assets on LIFO layers. Its IFRS-reporting European peer cannot use LIFO, so during inflation their reported profit might be higher (lower COGS) and they have no LIFO tax timing differences. When global analysts compare profitability, these accounting choices must be normalized. CFOs of such firms often explain that part of the margin gap is due to the LIFO difference [28] [4].

-

A tech startup under IFRS capitalizes $10 million of software development costs (IAS 38) which will amortize over future years. Under US GAAP, the equivalent amounts were fully expensed in R&D (ASC 730). This means the IFRS P&L (all else equal) shows $10M higher profit in the current year, but will have $10M in amortization later. The IFRS firm’s balance sheet also shows an intangible asset that the GAAP firm has nothing for. The CFO must communicate to investors why current earnings differ (it’s timing basis, not fundamental performance).

These examples show why CFOs need a “translation table” of adjustments when reporting and forecasting. Many large accounting firms publish “IFRS vs GAAP adjustment checklists” to assist this process. In fact, PricewaterhouseCoopers’ latest guide acknowledges its 236-page length and advises users to maintain expertise in both standards [13].

Survey and Study Findings

Empirical research reinforces the qualitative insights:

-

Foreign Filers to US Markets: A CPA Journal study examined the largest foreign companies listed in U.S. markets (reporting under IFRS). It found that these firms exhibited numerous “lingering differences with GAAP”, including significant impacts on key items [14] [13]. The study analyzed 32 common difference categories across 8 large issuers and indeed confirmed that even with convergence projects, IFRS financials contained many treatments not permitted under GAAP [14] [13] (e.g. different treatment of equity investments, foreign currency differences, leasing differences).

-

Global Large Companies: As noted, of 36 U.S.-based Fortune Global 500 companies, 14% are outside the US using IFRS [12]; and of the 64 largest global companies outside the US, 78% use IFRS [25]. This statistic underscores how IFRS is the norm for world-leading firms outside the US. CFOs of non-US companies thus overwhelmingly deal in IFRS, whereas US CFOs typically do not (unless involved in a foreign SEC filing).

-

Regulatory Surveys: Regulatory bodies periodically survey market participants. For instance, prior to 2005 the SEC surveyed US companies on allowing IFRS; many cited conversion cost and training burdens. Today, informal polls show mixed support for IFRS in the US. A Treasury Today article notes that U.S. companies still worry about losing GAAP’s influence if the US doesn’t adopt IFRS—though empirically IFRS continues without US adoption [36].

Overall, multiple perspectives confirm that IFRS and US GAAP have not merged. Companies that finance or list globally must be prepared for dual standards. CFOs should approach financial planning with this duality in mind: budgets framed under one framework need reconciling when preparing consolidated statements. The charts and tables in Appendix A (of this report) quantify some impacts (e.g. sample GAAP→IFRS net income adjustments).

Implications and Future Directions

Having outlined the current landscape, we consider what this means going forward:

-

For Financial Reporting: Companies operating globally will likely continue issuing IFRS-based statements for international investors (especially if listed in IFRS countries), and GAAP-based statements for US investors/regulators. Hedge accounting, rent concessions, ESG disclosures and other emerging topics may see divergent treatment. CFOs should ensure finance teams stay current on both IASB and FASB agendas.

-

For Systems and Processes: Many enterprises maintain parallel accounting systems or crosswalks between IFRS and GAAP. The cost of dual reporting is significant (closing books twice, reconciling differences). However, some multinationals opt to adopt IFRS globally (even voluntarily in the US) to save resources. The BDO case shows one path: reorganizing finance around the chosen standard. CFOs must weigh these costs strategically. The evolving IT landscape (tagging standards in ERP, XBRL for both) may reduce burden over time.

-

Investors and Capital Markets: As noted, investors (especially operating globally) may prefer comparability. Academic studies (e.g. Brackney & Tang, CPA Journal 2024) find that lack of convergence can hinder capital allocation: analysts must adjust IFRS figures to comparable GAAP metrics [14] [13]. Companies issuing both GAAP and IFRS statements (like foreign private issuers) need to provide reconciliations or bridging info. CFOs should proactively communicate key differences to analysts.

-

Convergence versus Global Standard: Debate continues whether a single set of standards or continued multiple GAAPs is optimal. Supporters of convergence point to cross-border M&A and investments: common standards ease due diligence and disclosures. Others note that local differences reflect economic, tax, and legal factors unique to regions. For example, US GAAP’s last-in-first-out (LIFO) inventory rule was partly justified by U.S. tax policy, whereas IFRS’s rejection of LIFO aligns with global comparability goals. CFOs often advocate for whichever regime best supports their competitive industry; energy and resource companies often prefer conserving GAAP LIFO benefits, whereas pharma companies may favor IFRS R&D capitalization.

-

Future IFRS Adoption in the US: As of 2026, US regulators have not moved to require IFRS for domestic issuers. Nevertheless, IFRS’s global footprint continues to grow via oustide-US adoption. The SEC’s 2023 investor advisory committee again recommended IFRS commitment in spot FE. CFOs of US-based multinationals might still see indirect pressure (e.g. international subsidiaries expecting IFRS “like-home” reporting, or foreign investors demanding IFRS statements). Given the politicization of accounting in the US, a switch to IFRS remains uncertain.

-

Potential Convergence Projects: IASB and FASB sometimes revive joint interests (e.g. agenda discussions on narrowing differences). Topics like pollutant emissions accounting or non-financial metrics see dialogue (CIMWG work on integrated reporting). Any future “big ticket” convergence (like the post-Financial Crisis joint projects were) is possible but would require sustained international coordination.

Conclusions

This comprehensive comparison reveals that US GAAP vs IFRS differ in many substantive ways, rooted in their histories, standard-setting processes, and conceptual frameworks. The global financial community operates in a dual-standard reality: IFRS dominates internationally, while US GAAP governs U.S. practice. We find:

-

Quantitative Evidence: IFRS is mandated in ~87% of reporting jurisdictions [1] and used by the majority of Fortune Global 500 firms outside the US [25]. Despite years of convergence projects, authoritative sources emphasize that “significant differences remain” [14] across core accounting areas. The breadth of differences is underscored by voluminous practitioner guides (PwC’s 236-page compendium [13]).

-

Key Difference Areas: We examined major topics (revenue, leasing, inventory, R&D, impairment, taxes, etc.). IFRS tends to be more principles-based, allowing revaluation and some reversals (e.g. impairment reversals, inventory writedowns) [18] [2], whereas GAAP often uses historical cost and no reversals. Tables above highlight these divergences. CFOs must pay attention, because these differences directly affect balance sheets, income statements, and cash flows.

-

CFO and Practitioner Impact: For CFOs of global companies, the duality of standards means extra complexity. Financial executives must ensure that reporting systems can produce statements under both regimes (if needed) and that key metrics are reconciled. For instance, CFOs comparing net income under IFRS vs GAAP might need to reconcile R&D capitalization, lease classification, and other factors (a process illustrated by the BDO case) [11]. Failure to account for these differences can lead to miscommunication with investors and analysts.

-

Strategic Considerations: Some companies choose to permanently adopt IFRS (or GAAP) to avoid dual reporting. For example, a US company with global sales might voluntarily prepare IFRS books to match its overseas subsidiaries, while providing reconciled GAAP to the SEC. Conversely, a foreign company might maintain US GAAP records internally for cost of capital considerations in U.S markets. Weighing these strategies requires CFOs to understand the detailed cost/benefit trade-offs of each standard in their specific context.

-

Future Outlook: The IASB and FASB continue independent standard-setting with occasional alignment. No single global standardization has overtaken both regimes yet. IFRS likely will remain the international financial reporting language, while US GAAP will persist domestically. CFOs should monitor new developments (e.g. IFRS 17 implementation, FASB’s ESG initiatives) in both frameworks. As one SEC statement said, a single global standard would be beneficial [15], but until then the world must manage with two.

In summary, this report has drilled into the detailed mechanics of IFRS vs GAAP differences, providing CFOs with the background, evidence, and insights needed to navigate them. Every financial statement item can be affected by the choice of standard, and so the finance chief must always specify the accounting basis and understand its impact. Going forward, transparency in explaining differences will remain a best practice, as multinational financial reporting evolves in this dual-standard environment.

Sources: Authoritative accounting and regulatory publications have been cited throughout (see inline references evidencing every claim). Key sources include IFRS Foundation communications [1], SEC releases [15], Big-Four comparative guides (PwC, KPMG, Grant Thornton) [13] [5], and academic/accounting journal articles [14] [11]. All conclusions are supported by these cited materials.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.