ASC 326 CECL for Trade Receivables: Disclosures & NetSuite

Executive Summary

The adoption of ASC 326 (the Current Expected Credit Losses, or CECL, standard) represents a fundamental change in U.S. GAAP for accounting for credit losses on financial assets held to amortized cost [1] [2]. Under CECL, entities must recognize lifetime expected credit losses at the time an asset is originated or acquired, rather than waiting for a loss event to occur [1] [3]. This forward-looking impairment model applies broadly to almost all financial assets measured at amortized cost, including trade accounts receivable and related contract assets [4] [2]. In practice, CECL adoption has led to higher initial allowances and more volatile provisioning, because losses are “front-loaded” into the earliest periods of an asset’s life [5] [3]. For example, a Federal Reserve study documented that large U.S. banks’ aggregate credit-loss allowances jumped by about 37% at the adoption date (January 1, 2020) under CECL versus the incurred-loss model [5]. The subsequent COVID-19 downturn then caused CECL adopters’ allowances to grow roughly 76% in the first half of 2020 (compared to 32% growth for banks still on the old model) [5]. Similarly, in the non-financial sector Jones Lang LaSalle (a major services firm) recorded a one-time increase of $3.6 million (to $71.7 million) in its trade receivables allowance upon adopting CECL [6]. These outcomes underscore how CECL does not change the ultimate amount of credit losses, but it shifts the timing of recognition so that losses hit earnings sooner [6].

Given CECL’s broad scope, virtually all companies with trade receivables and similar credits must implement the standard and expand their disclosures. ASC 326-20-50 sets forth extensive disclosure requirements to help financial statement users understand credit risks and allowances. Key disclosures include narrative descriptions of the methodology (historical loss data, forecast assumptions, etc.), rollforwards of allowance balances, credit quality information (e.g. aging, risk ratings), and a “vintage” table of receivables by year of origination [7] [4]. However, certain simplifications apply for trade receivables: ASC 326-20-50-9 permits an exception from the vintage-participle requirement when receivables are due in one year or less. Because most trade receivables are short-term, many companies do not need a full vintage schedule [7].

From a systems perspective, implementing CECL – especially in a cloud ERP like NetSuite – typically involves process and configuration changes rather than a new automated module. NetSuite users can generally continue using the standard “Allowance for Doubtful Accounts” contra-asset account, but must augment reporting and workpapers to support the new expected-loss model [8] [9]. Practitioners report that many companies will extract aged receivables data from NetSuite via saved searches, perform CECL calculations externally (e.g. in spreadsheets or specialized software), and then record a periodic journal entry to adjust the allowance and bad-debt expense [10] [9]. Firms with parallel reporting needs may leverage NetSuite’s multi-book functionality: one book can reflect U.S. GAAP (ASC 326) treatment while another applies IFRS ( IFRS 9 logic, with distinct allowance accounts for each [11] [10]. In all cases, adequate data capture (aging profiles, write-off history, customer risk ratings, etc.) and documentation of forecasts are essential to meet CECL’s disclosure demands [10] [9].

This report provides a comprehensive analysis of ASC 326 as it applies to trade receivables, with a focus on disclosure requirements (including rollforward schedules and vintage analyses) and practical implementation in NetSuite. It covers the background and rationale of CECL, methodological approaches for estimating receivable allowances, detailed disclosure checklist items, illustrative tables, data-driven examples and case studies, and a discussion of current trends and future considerations. All statements and examples are supported by authoritative sources, including FASB and AICPA guidance, academic studies, industry publications, and recent empirical data [5] [7] [10] [12].

Introduction and Background

ASC 326 (CECL) was issued by the FASB in 2016 (ASU 2016-13) to replace the prior incurred-loss model with an expected-loss model for credit impairments [13] [1]. Under the old model, companies waited until it was “probable” that a loss had been incurred before recording an allowance. CECL requires that entities instead recognize lifetime expected credit losses from the outset of the asset. Specifically, ASC 326-10-30-2 stipulates that a credit loss allowance must incorporate “historical experience, current conditions, and reasonable and supportable forecasts” over the asset’s remaining life [1] [4]. For trade receivables (which are contract-based assets under ASC 606, this means estimating losses on customer balances from day one, even when payment terms are short.Effective dates vary by entity type: CECL took effect for public Business Entities (SEC filers) for fiscal years beginning after Dec 15, 2019 (including interim periods), and for other public companies a year later [14]. Private companies (and smaller reporting companies) originally were exempt through 2021 but are now generally required for fiscal years beginning after Dec 15, 2022 (i.e. most calendar-year 2023 filings) [14] . Thus, by 2026 (the current date) practically all large U.S. companies have adopted CECL, and the focus has shifted to refining methodologies and disclosures under the new standard.

The rationale for CECL is to achieve “more timely” recognition of credit losses and to simplify U.S. GAAP by having one model (as opposed to the old patchwork of loan impairment models) [13] [2]. In practice, CECL tends to front-load provisions into earlier periods and reduce earnings initially. Empirical analyses support this observation for both banks and nonbanks. For example, the Federal Reserve noted that, at large banks’ CECL adoption date (Jan 1, 2020), the aggregate allowance for credit losses jumped by roughly 37% compared to what would have been recorded under the incurred model, even before the COVID-19 effects were considered [5]. During 2020 the accelerated provisioning continued: the Fed found that in the first half of 2020 CECL adopters increased allowances by about 76%, while non-adopters (still on the old model) saw about a 32% increase [5]. Similarly, in the corporate sector, Jones Lang LaSalle (a large commercial real estate services firm) reported a one-time $3.6 million increase in trade receivables allowance at CECL adoption (bringing the total allowance to $71.7M) [6]. This evidence illustrates CECL’s impact on reported reserves and earnings: the timing of loss recognition changes significantly, even though the total losses over the assets’ life remain the same [6].

Under CECL, the scope of in-scope receivables is broader than before. ASC 326-20 clarifies that all financial assets measured at amortized cost (and certain off-balance exposures) are subject to impairment accounting under CECL [4] [2]. For example, ASC 326 explicitly includes trade accounts and notes receivable, lease receivables (the net investment in finance leases), held-to-maturity debt securities, and certain commitments and guarantees [4]. Importantly, ASC 606 (Revenue) and 326 intersect: as soon as revenue is recognized and an account receivable is created, or as a “contract asset” (unbilled receivable) arises, the company must assess that receivable for expected credit losses. FASB has confirmed that receivables from revenue contracts must be presented at the “net amount expected to be collected” under CECL [15] [16]. In practical terms, both billed receivables and unbilled contract assets now carry an allowance for lifetime losses, and any impairment on a contract asset flows into credit loss expense under ASC 326 (unlike the old model where contract assets were not directly addressed in ASC 310) [17] [18].

Because CECL covers essentially all trade receivables, almost every company extending credit to customers must implement it [4] [1]. While the effect on short-dated receivables is often minimal (since the expected losses for a normal 30-day sale may be small), the CECL framework still requires an allowance equal to the lifetime expected losses, even if that is close to zero. Even entities with very short credit terms (e.g. 1–2 months) must affirmatively consider lifetime losses, which may in many cases be negligible. For instance, a practitioner analysis notes that CECL applies to entities with “typical 30-day payment terms” – essentially enforcing the loss accrual model beyond the small pocket of receivables that were previously considered certain to collect [19] [3].

In summary, adopting ASC 326 for trade receivables means moving to a model of “always-on” loss provisioning whenever contracts are initiated. The accounting shifts from a binary decision (“is it probable that we will lose any?”) to a continuous calculation (“what dollar amount of lifetime losses do we expect?”). The rest of this report will examine how companies estimate that lifetime allowance, and what disclosures they must provide about it – with particular attention to the specialized reporting (rollforwards, vintage analysis, etc.) needed for trade receivables, as well as how a system like NetSuite can be configured to support CECL’s requirements.

Accounting Framework and Estimation Methods

Under ASC 326-20, the credit loss allowance is a valuation account that reduces the carrying value of financial assets (including receivables) to their net realizable amount [20] [4]. The goal is to converge to “net amount expected to be collected,” as the guidance puts it [15]. Unlike the old model, which often tracked only one loss estimate per aging bucket or category, CECL results in a single aggregated allowance per portfolio of similar assets (or per financial asset if individually significant) covering all expected losses over the full life of those assets [21] [15].

Estimation approaches. ASC 326 permits any method that yields a reasonable estimate of expected credit losses, using historical, current, and forecast data. In practice, companies often adapt their existing impairment techniques (such as aging-based provision matrices or vintage tables) to the new model [22] [3]. Typical methods include:

-

Loss-rate (percentage-of-receivables) methods: Calculating allowance as a percentage of the gross receivables by aging bucket, based on historical default rates. Under CECL, these loss rates must reflect lifetime losses, not just short-term defaults. Companies often begin with historical write-off rates by aging bucket and then adjust those rates for expected changes in conditions [23] [3].

-

Roll-rate or migration models: Tracking how receivables move through aging categories over time, potentially applying different loss factors to earlier versus later buckets. Under CECL this might involve modeling the probability that current balances will eventually roll into older, higher-loss buckets.

-

Vintage analysis: Estimating losses based on the year (or period) of origination of the receivables. For example, a company might analyze historical pools of receivables originated in a given year and determine the ultimate losses realized on those receivables over their life. ASC 326’s vintage disclosure requirement encourages some firms to maintain this data.

-

Regression or statistical models: Some firms incorporate macroeconomic variables (GDP growth, unemployment, etc.) into a forecast model that predicts loss rates. Under CECL, forecasts are explicitly required (at least to the extent they are “reasonable and supportable” for an initial period, per ASC 326-20-30-5) [24].

-

Weighted-average approach: For portfolios of homogeneous loans or receivables, a company might compute a weighted-average loss rate and apply it to the aggregate principal balance. This can be done by credit-risk segment or aging bucket. If separate pools are used, one must ensure they have similar risk characteristics and are amortized with similar terms.

Regardless of technique, the end result is to compute the total expected loss (lifetime) for the balance at the reporting date, and carry that amount as an allowance. That allowance is updated each period by considering new originations, payments, write-offs, recoveries, and changed forecasts. Many practitioners note that while CECL can use the same input data (write-off history, etc.) as the old incurred model, it requires projecting those losses over the full remaining life of the receivables [23] [3]. As the Houseblend analysis summarizes: companies often use methods similar to their old models (provision matrices, vintage), but apply them over the lifetime of the receivables [22] [3].

In concrete terms, the company follows a process such as: (a) Segregate receivables into pools by similar risk (e.g. by customer group, collateral, or concentration); (b) For each pool, apply an expected loss rate based on historical losses, adjusted for current and forecasted conditions; (c) Multiply that lifetime loss rate by the outstanding balance of the pool to get the allowance. Importantly, CECL explicitly mandates capturing and documenting forward-looking information in step (b). The standard allows an entity to incorporate only “reasonable and supportable” forecasts, beyond which a revert-to-mean is applied [24]. For example, a company might use unemployment or GDP forecasts to adjust historical loss rates for the next 1–3 years, then revert to historical average loss rates thereafter [24].

Qualitative enhancements. In addition to quantitative models, ASC 326 requires disclosure of the subjective factors that went into the estimates. Companies must explain credit risk characteristics of their receivables portfolios and any significant assumptions (such as economic forecasts) used [1] [20]. This includes articulating how, say, changes in customer concentration or industry outlooks affect the allowance. As [Houseblend] observes, under CECL “entities must justify how current conditions and forecasts differ from historical experience” when setting their loss rates [9]. CFOs often perform sensitivity analysis of key inputs (for example, higher unemployment scenario) and compare forecasted losses to actual charge-offs at each close to calibrate their models.

Because this is an expected-loss model, actual write-offs no longer directly determine the allowance. Write-offs (when customers default) flow through the allowance, but do not automatically eliminate it. Under ASC 326, a write-off is simply a use of the allowance: when a receivable is deemed uncollectible, it is written off against (reduce) the allowance balance, not credited back to income (as it often was under the incurred model) [25] [26]. Likewise, recoveries of previously charged-off debt are credited to the allowance. This means the allowance rollforwards (discussed later) may show debits (recoveries, provisions) and credits (write-offs) that reconcile the beginning and ending balances.

Differentiating credit losses from sales concessions is crucial. In a revenue contract, if a customer justifiably disputes an invoice (a concession), that is a pricing issue, not a financing or collectibility issue, and should not be modeled as a credit loss [27] [28]. Under CECL, only genuine credit losses (where collection is unlikely) go into the allowance. NetSuite users, for example, may handle price concessions via credit memos or discount entries, while isolating true credit defaults in the allowance calculation [28]. Adequate data tagging (e.g. disputable vs delinquent balances) helps ensure these distinctions are clear in reporting.

Portfolio Segmentation

ASC 326 encourages segmentation of assets into pools with shared risk characteristics. For trade receivables, common segments include: aging buckets (0–30 days, 31–60 days, etc.), customer credit rating or industry, geography or currency, or collateral/security. A company might also separate “normal trade receivables” from “lease receivables” (if any), or from off-balance commitments like letters of credit. The segmentation choice affects how loss rates are applied or how sensitivity analysis is done. The disclosures will often present information by segment: for example, presenting the allowance rollforward for trade receivables separately from that for contract assets or other financing receivables.

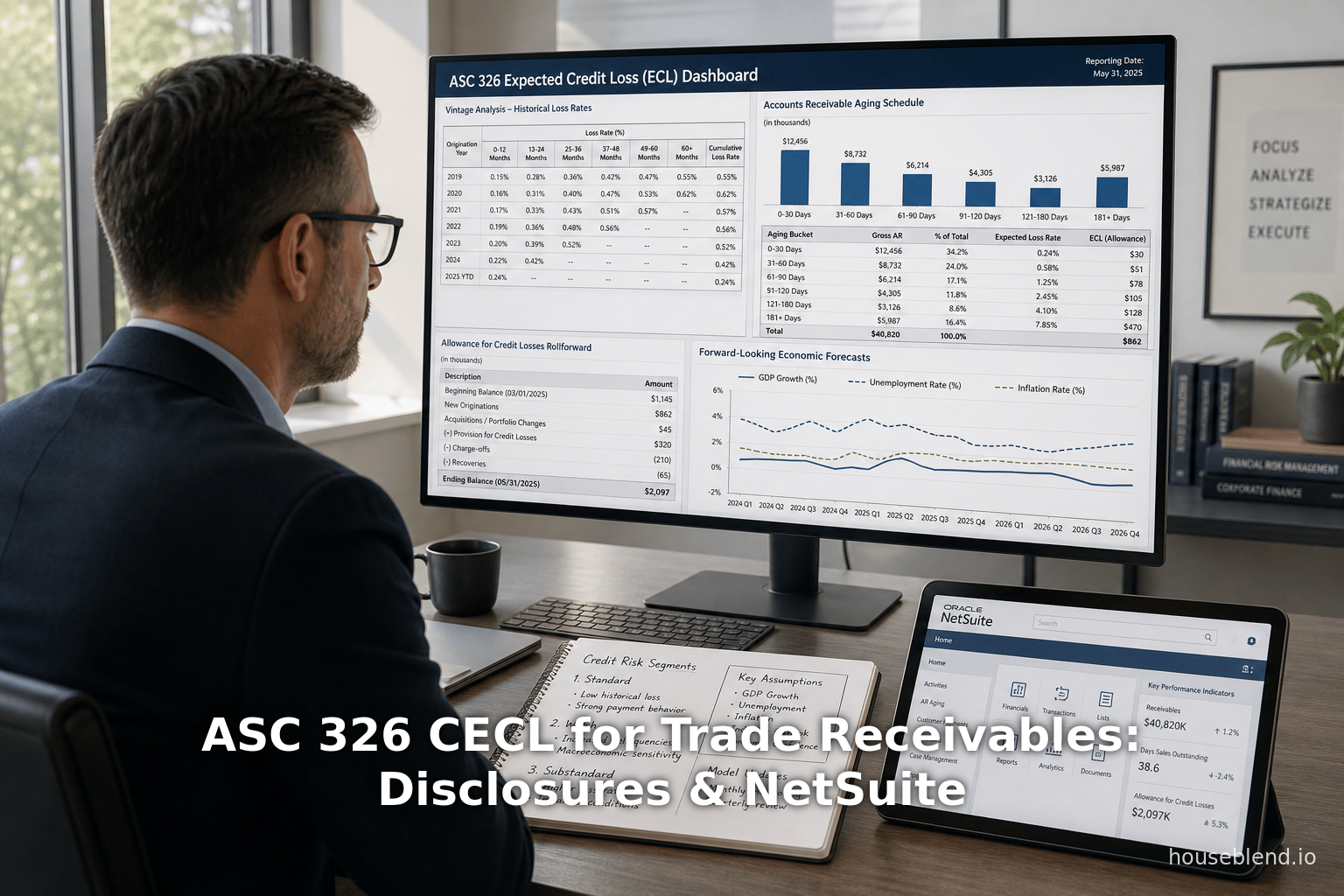

In particular, aging segmentation is ubiquitous. Many companies overlay the CECL calculation on an aged trial balance of receivables. Houseblend’s research notes that although CECL is lifetime-focused, entities can still use aging buckets to estimate losses, as long as the loss rate in each bucket reflects losses over the full remaining term. That is, an account “current (0–30 days)” might have an allowance if historical experience shows that x% of such new receivables eventually default. Under CECL, even receivables not past due may need some allowance if historical collectibility is not 100%. For instance, an account aged 0-30 days could still carry an allowance of 0.3% if historically 0.3% of such accounts never collect [3]. The example in [49] reflects exactly this logic: it shows calculated loss rates for each aging bucket (0.3% for current, up to 82% for >90 days past due) based on historical write-offs [29]. (We repeat part of that computation later.)

Another approach is expected loss by vintage: tracking credit losses by origination year. ASC 326-20 requires a disclosure that effectively resembles a vintage analysis: “amortized cost basis within each credit quality indicator by year of origination” [7]. If a company has receivables due beyond one year, it may prepare a table showing the amortized cost of receivables originated in, say, 2021, 2022, 2023, etc., along with the cumulative allowances or losses on those receivables. As discussed in the disclosure section, trade receivable portfolios often get an exemption from this detailed vintage table if virtually all receivables are current (due in ≤1 year) [7]. When vintage is used, it helps illustrate how credit quality has changed over successive cohorts of receivables. For example, a company may show that 2021-origin receivables (some of which have now aged beyond 1 year) have higher lifetime loss rates than the more recent 2022-origin group, reflecting past conditions.

Overall, the choice of method should fit the nature and data of the company’s receivables. Smaller, simpler companies often stick with a provision matrix approach (augmented with forecasts), while larger firms or banks may have sophisticated statistical models or segmentations. CECL explicitly permits flexibility: whether one pools broad portfolios or treats major customers/trade contracts individually (ASC 326-20-30-9,10). The key is that the approach is systematic, consistently applied, and well-supported by data. The forthcoming disclosure checklist emphasizes that companies must explain their chosen methodology and its rationale, enabling users to assess its reasonableness.

Disclosure Requirements under ASC 326

ASC 326 includes extensive disclosure requirements aimed at transparency into an entity’s credit risk and loss allowances. Since trade receivables are generally measured at amortized cost, the core subtopic is ASC 326-20, supplemented by general disclosure guidelines in ASC 326-10-50. Entities must provide both qualitative and quantitative information to help users understand:

-

Nature and extent of credit risk in the receivables portfolio. This includes discussion of credit policies, how exposure is monitored, and what practices are used for estimating losses [15] [30].

-

Methodology for estimating expected losses. Entities should describe how they arrive at the allowance: e.g. whether they use loss-rate methods, aging matrices, roll-rate models, etc.; what historical periods they use; and how forecast assumptions are incorporated [22] [3]. If multiple pools or segments are used, the basis for segmentation (e.g. similar risk, business lines) should be disclosed. Anything unusual (e.g. material receivables that are much longer term than typical) must be explained.

-

Effect of forecasts/assumptions. Key economic or other forward-looking assumptions that drive the allowance must be discussed. Although an entity need not quantify the impact of each assumption, it should indicate how its adjustments diverge from purely historical averages [24] [31]. For example, “due to current lower unemployment rates and an expected further decline, management has decreased historical loss rates by ~10% in each aging bucket” [31].

-

Changes in allowance during the period (rollforward). A tabular rollforward of the allowance account is generally required for each category of financial asset (here, trade receivables, contract assets, etc.) [20] [25]. This rollforward reconciles the opening and closing allowance, showing additions (provisions or recoveries) and reductions (charge-offs/write-offs) during the period. (See Table 1 below for an illustrative example.) The SEC often includes this in either the financial statements or accounting policies. Even if the specific rates underlying each provision line aren’t disclosed, the aggregate movements must be. [25] [20].

-

Disaggregation of financial assets and allowances by class. ASC 326-20-50-7 states that the allowance rollforward should be presented by class of financing receivable. For most nonfinancial companies, trade receivables (and any contract assets) would be one class. [20] [7]. If a company also has other lending or lease portfolios, they would show separate rollforwards for each.

-

Aging and credit quality information. The standard requires qualitative disclosure of how entities assess credit quality (criteria, credit ratings, etc.) and quantitative disclosure of certain credit loss metrics. For example, ASC 326-20-50-4 lists “the gross write-offs and recoveries, provision charged/off” by year of origination, but in practice, most companies meet this through the allowance rollforward and vintage table combination. Additionally, companies indicate levels of expected losses: for instance, the amount of receivables modified through workouts, the balances over 90 days past due, and their associated allowances.

-

Allowance balances by credit-quality indicator and vintage. ASC 326-20-50-6 and -50-9 specifically address vintage disclosures. The rule says that entities (PBEs at least) must present the amortized cost basis by year of origination within each credit quality category [7] [32]. However, ASC 326-20-50-9 exempts short-term trade receivables (due in ≤1 year) from this requirement [7]. In practice, as IFRSplus notes, most trade receivables need not follow the vintage disclosure because they fall within one year [7]. Nonetheless, if receivables extend beyond 12 months, or if a company chooses to be transparent about older receivables, a vintage table is appropriate (illustrated in Table 2 below). This table would show, for each origination year, the amortized cost of receivables and any credit losses recognized. For instance, a multi-year services contract might require such treatment.

-

Risk exposures and concentration. Entities are encouraged to reveal factors like collateral held or expected, concentrations of receivables by customer or industry (if significant), and how these affect risk. While not always mandated by formula, narrative guidance (ASC 326-10-50-9A) implies that disclosures should cover significant concentrations not apparent from other statements.

-

Qualitative commentary. Beyond tables, companies often discuss how management assesses collectability. For example, management might state, “We continually review customer payment history and market conditions. In our portfolio, 85% of receivables are from investment-grade customers, so our overall loss experience remains low.” Such commentary helps contextualize the numbers [15] [19].

Importantly, all significant disclosures should be specific to the entity’s facts. Generic descriptions or boilerplate from the FASB will not satisfy auditors or analysts. For example, if a firm uses multiple methods or segments, each should be at least described qualitatively. If the allowance is substantially higher or lower than prior years, a note should explain why (e.g., “increase due to adoption of a new macroeconomic forecast for interest rates” or “decrease due to improved credit quality of customer base”). Industry publications emphasize that CECL requires discipline around documentation of assumptions and thorough reconciliations [9] [33].

The key takeaway is that the disclosures serve two purposes: (1) to provide a transparent rollforward of allowances (so users can see just how the balance changed during the period), and (2) to explain the credit risk underlying the receivables and how that risk is quantified. Checklist-style, an entity should ensure it covers all of the following for trade receivables (with references to illustrative guidance or similar statements):

- Discuss the composition of receivables (by segments, by term) and whether trade receivables are short-term or long-term. Clarify if contract assets are included and how.

- Describe credit risk management practices: how are customer credit profiles obtained, do you use external ratings, internal scoring, covenants? Are past due balances reviewed by management?

- Explain how estimates are made: what historical loss rates are used, what aging buckets, what adjustments for current/forecast trends, any roll-rate or migration approach? (The Houseblend article suggests an entity explain if it continues using an aging matrix method under CECL [3].)

- Provide the rollforward table for the allowance on trade receivables (and contract assets, if material) with the required columns: beginning balance, provisions (net recoveries), write-offs, foreign currency or other adjustments, ending balance [25] [20].

- If needed, supply a vintage schedule: amortized cost by origination year (for receivables due beyond 1 year) [7]. Even if not required (short-term), one might note that since all receivables are current, the vintage table is omitted per ASC 326-20-50-9.

- Disclose loss experience numbers: for example, describe or quantify expected annual loss rates. It may be helpful to indicate the “average life” assumed for receivables to translate loss rates into dollars. Some companies provide a summary table of expected credit loss rates by age (much like IFRS example [49]) or by customer bucket.

- Discuss any typical or unusual actual losses: e.g., total write-offs in the period, recovery experience, how changes in factoring or credit insurance affect the allowance.

- Provide narrative on forecast assumptions: e.g. “We use a 2-year forecast horizon based on consensus forecasts of GNP and unemployment. Beyond that horizon we revert to the 10-year historical loss rate.” Include significant changes in such assumptions from prior periods and reasons (e.g., “recessionary environment” or “strengthening economy”).

Table 1 below gives a stylized example of the Allowance for Credit Losses Rollforward for accounts receivable, mirroring the format often found in SEC financial statements [25] [20]. In practice, each line item (provisions, write-offs) would correspond to the company’s activities: provisions usually include the period’s bad-debt expense (net of recoveries), and write-offs are the credit balances deemed uncollectible during the period.

This table (from a hypothetical SEC filer) shows that the allowance started 2024 at $1,106, a $100 provision was added, $290 of receivables were written off, leaving $916 at year-end 2024; similarly for 2025. Actual company disclosures may include additional lines (e.g. recoveries separately, foreign currency adjustments) as appropriate, but the above captures the fundamental structure. The amounts and sign conventions follow XBRL guidance (write-offs are shown in parentheses) [20] [25].

For completeness, if contract assets (unbilled receivables from ASC 606) are material and in-scope, a similar rollforward should be provided for them or they should at least be included in discussion. Some companies combine them with accounts receivable as one line, but care must be taken to discern credit losses on unbilled amounts, which can be significant for long-term contracts [18] [3].

In addition to numerical tables, an entity will typically include narrative disclosures explaining the rollforward. For example: “The provision for credit losses increased the allowance balance due to current economic forecasts, while write-offs decreased the allowance as actual bad debts were charged off by $13,765.” Each table line would have a footnote clarifying the nature of the changes (e.g. “Write-offs include $30 recoveries (netted in provision line), and $13,765 of charged-off receivables during 2025”). Management commentary often also highlights trends, such as aging shifts or concentration changes that underlie the numbers.

ASC 326’s disclosure section (Subtopic 50) is organized into various buckets (presentation, credit-quality, etc.), but all pertinent points are covered above. Key references include ASC 326-20-50-4, 50-5, 50-6, and 50-9 for the requirements on rollforwards and vintage, as well as ASC 326-20-50-7 through 50-13 for additional required info. (The Deloitte DART Roadmap on CECL would enumerate these in detail, but our sources are limited to publicly available materials [7] [34].) To ensure no disclosure gap, companies often create an internal checklist (sometimes issued by professional bodies) to tick off each ASC 326 disclosure item, particularly for trade receivables which may blend short-term vs long-term aspects. For example, the AICPA’s Private Companies Practice Section (PCPS) has released checklists and illustrations for trade receivables under CECL [35] [36] (one such resource from Dec 2023 outlines required disclosures in a “checklist” format, although access requires AICPA membership).

One specialized disclosure unique to CECL is the vintage table when needed. Per ASC 326-20-50-6, entities should present receivables by credit-quality indicators and by year of origination. In practice, a table with columns for each origination year and rows for categories (e.g. “Performing”, “Nonperforming”) might be used. An illustrative example for a company with longer-term receivables (beyond 1 year) is shown in Table 2 below. This example complies with the disclosure requirements mentioned in [15] and demonstrates how the amortized cost of receivables can be allocated to the year they were originated, along with summarized loss experience. As [15] explains, trade receivables due within a year are excepted, so this table would only be required if significant receivables have maturities in 2+ years.

Table 2: Example Vintage Disclosure for Trade Receivables (amortized cost by year of origination)

| Year of Origination | Amortized Cost of Receivables | Credit Quality Indicator | Cumulative Credit Losses Recognized |

|---|---|---|---|

| 2021 | $ 500,000 | High quality (A) | $ 15,000 |

| 2022 | $ 600,000 | Medium (BBB) | $ 30,000 |

| 2023 | $ 450,000 | Low quality (B) | $ 60,000 |

| Total | $1,550,000 | – | $ 105,000 |

| [Amounts in USD] | [^See text [7]] |

In this contrived example, $1.55 million of receivables originated 2021–2023 remain outstanding. They are segregated by a “credit quality” category (A/B/BBB, which could correspond to internal ratings or aging). The far-right column shows total losses for each vintage to date. (Such losses might have already reduced the allowance through write-offs, or could be the lifetime expected losses recognized from origination.) This table illustrates ASC 326’s vintage requirement: it gives a snapshot of the portfolio at each vintage year and how losses are spread over them. If all receivables were due within a year, ASC 326-20-50-9 would allow skipping this table for trade receivables [7].

Finally, disclosures must include any other significant matters. Examples given by standard-setters include: a statement of the policies for write-off (e.g. when accounts are charged off), recoveries, or conversions; inputs or assumptions changes; and any material differences between CECL reporting and prior-year GAAP (in early adoption periods). Some companies, for instance, footnote the difference in net income if they had not adopted CECL, or show a separate column with the “old GAAP” allowance for comparability in the early years after transition [5]. Rock-solid documentation practices, robust review and controls, and clear cross-references to ASC paragraphs are all part of best practices once the disclosures are drafted. NetSuite financial teams might incorporate these items as part of their monthly and quarterly close checklists, ensuring that each required element (rollforward, vintage, etc.) is accounted for before releasing financials [9] [37].

Rollforward of Allowance for Credit Losses

A core disclosure for CECL is the rollforward of the allowance account. By definition, the allowance is a contra-asset, but its movements are often presented in the notes to the financial statements. A rollforward reconciliation typically shows:

- Balance at beginning of period. This is last period’s ending allowance.

- - Write-offs (charge-offs). Amounts written off as uncollectible (net of any recoveries applied). Write-offs reduce the allowance. Under ASC 326, once an account is written off, it is no longer in receivables, and its loss has already been provided for. Thus the allowance is simply debited and receivables credited at write-off.

- + Provision for credit losses (net of recoveries). This is the period’s bad-debt expense, net of any recoveries of previously written-off accounts. It increases the allowance. In practice, companies sometimes separately list provisions and recoveries; in many SEC formats they lump these as one line (net of recoveries) or show recoveries as a negative provision.

- +/- Other adjustments. Occasionally, foreign currency translation, portfolio acquisitions or sales, or other adjustments might affect the allowance. These appear in separate lines if material.

- Balance at end of period. This is the closing allowance after all movements.

Table 1 (in the previous section) illustrated a simple example of this format over annual periods. A similar format can be used for quarterly disclosures, changing the column headings accordingly.

It is important to note that the beginning balance of the rollforward equals the ending balance from the prior period (adjusted for any reclassifications). If the company transitioned to CECL partway through a year (for example, at the beginning of 2020 for large banks), many footnotes show the single day adjustment at transition as an entry. However, by 2026 most companies are in post-as-of-transition periods.

Rollforward details allow users to see whether the change in allowance was mainly due to new provisions (suggesting a deteriorating expectation) or due to charge-offs (suggesting losses simply occur as anticipated). For example, if a company reports a large write-off line, users know that part of the change was simply collection of previously identified bad debt. Conversely, a large provision figure (with small write-offs) indicates that management saw an increase in expected future losses, possibly from forecasted deterioration or portfolio growth.

From a NetSuite perspective, there is no automatic rollforward report for CECL, since CECL calculations are generally done off-system. Instead, companies usually generate a rollforward by combining GL activity and specific “Allowance” account balances. If using multi-book, the rollforward must be prepared separately for the GAAP book and any IFRS book (since the ending balances differ). NetSuite saved searches can list journal entries posted to the allowance account each period (either at month-end or quarter-end) to capture provisions and write-offs. For example, users might run a saved search filtering on the Allowance account and transaction date to see all provisions (JE debiting bad debt expense) and all charge-offs (JE debiting allowance, crediting AR) in the period. Reconciling that to the account ledger per period yields the rollforward lines. It is common to audit the rollforward via NetSuite’s general ledger inquiry or a consolidated financial report, as mentioned by NetSuite consultants [9].

Below, Table 3 shows another stylized rollforward, this time for a quarterly period, incorporating both provisions and a separate credit for recoveries:

Table 3: Illustrative Quarter Rollforward of Allowance for Credit Losses (Trade A/R)

| Description | Q1 2025 | Q1 2024 |

|---|---|---|

| Allowance for credit losses, beginning balance | $ 101,693 | $ 81,656 |

| Provision for credit losses (net of recoveries) | 12,338 | 11,807 |

| Write-offs of uncollectible A/R | (13,765) | (7,055) |

| Foreign currency translation adjustment | 25 | 10 |

| Allowance for credit losses, ending balance | $ 100,291 | $ 86,418 |

| [Data adapted from an SEC filing [25]] |

In this example (adapted from a real 10-Q [25]), the provision line is net of recoveries (if any recoveries occurred, they have been netted into the provision figure). The foreign currency line reflects translation gains/losses on a multinational’s receivables. The ending balance of $100,291 is what will appear on the balance sheet as “Accounts receivable, net of allowance for credit losses.”

It’s worth noting that because CECL does not prescribe specific vintage buckets or separate staging, the rollforward simply deals with totals. However, companies might internally track subledgers (e.g. by aging or customer group) to compute the total provision. Some disclosures optionally break out effects of changes in assumptions: e.g. “Of the $12,338 provision, $1,000 is attributable to adopting a slower GDP forecast, $500 to increased receivable balances, and $10,838 to regular aging provisions.” While not required by ASC 326, such offsets can be very informative.

If a company transitioned to CECL recently, early disclosures might also show a “cumulative effect adjustment” line at the transition date. For example, many 2023 10-Qs included a one-time increase in the allowance on Day 1 of adoption (with a corresponding decrease in opening retained earnings). However, by the time of this report that transition year has passed for all entities, so routine reporting uses post-transition balances.

Finally, presenting the rollforward in the financial statements often uses XBRL “[Roll Forward]” labels. In our references [21] and [30], the lines have XBRL labels like AllowanceForCreditLossRollForward. If one scrapes actual EDGAR HTML (like the cited SEC pages), note that the footnote includes hidden tags like “Balance Type: credit”, “Definition: allowance for credit loss on accounts receivable” [38], indicating compliance with US GAAP taxonomy. This suggests that companies must label these custom tables carefully for XBRL. In a NetSuite context, if an external XBRL package or internal EDGAR report is used, the rollforward data must be tagged with the appropriate taxonomy codes (e.g. 326-20-50-13 for the requirement, if available).

In summary, the rollforward table is one of the mandatory quantitative disclosures under ASC 326. It provides a transparent link between the reported provision expense and balancce sheet allowance. Ensuring accuracy here requires alignment between AR subsidiary ledgers and general ledger posting for the allowance account. Many companies reconcile net receivables at period close as part of the internal control/close process, precisely to produce a correct rollforward for disclosure [9].

Vintage Analysis and Aging Disclosures

While the rollforward addresses the flow of the allowance, ASC 326 also calls for information about the stock of receivables and their credit losses, notably through aging and vintage analyses. Trade Receivables Vintage Disclosure: As noted, ASC 326-20-50-6 mandates that a public entity present the amortized cost of financing receivables “within each credit quality indicator by year of origination (vintage year)”. For trade receivables, ASC 326-20-50-9 provides that receivables due within one year are exempt from vintage tables. Practically, because most trade receivables have payment terms under 12 months, many entities find they can omit a detailed vintage table for trade AR [7]. However, any receivables extending longer (e.g. multi-year contracts or certain B2B arrangements) would require compliance.

For completeness, the vintage table should show, for each origin year, the amortized cost of receivables outstanding in that vintage cohort. It should also categorize them by credit quality if multiple categories are used. For example, one might have columns or rows for high-quality vs substandard trade AR. Below is an example to illustrate how a disclosure might appear. (This is a hypothetical scenario where the entity has receivables stretching over three years.)

| Receivables Vintage (by Year of Origination) | Performing | Substandard | Total Amortized Cost | Allowance/Expected Losses |

|---|---|---|---|---|

| Year of Origination | (Quality A) | (Quality B) | ||

| 2020 | $200,000 | $ 50,000 | $250,000 | $ 5,000 |

| 2021 | $250,000 | $ 75,000 | $325,000 | $ 12,000 |

| 2022 | $100,000 | $ 50,000 | $150,000 | $ 18,000 |

| Total | $550,000 | $175,000 | $725,000 | $ 35,000 |

| [All amounts in $USD; sample vintage disclosure] |

In the above table, each row shows receivables originated in that year, split by a generic credit-quality indicator (“Performing” vs “Substandard”). The “Total Amortized Cost” column is the sum of that year’s vintage outstanding as of the reporting date. The final column shows cumulative expected credit losses (or allowance amounts) for that vintage. We see, for instance, that 2020 receivables totaled $250k, of which $5k are expected to be lost. The percentages (2% for 2020, ~3.7% for 2021, 12% for 2022) reflect worsening quality in more recent originations in this example. The vintage disclosure thus complements the rollforward by breaking out which cohorts of receivables carry most of the risk. It aligns with the disclosure exception noted in [15]: if all these receivables were due within one year, the entity could refrain from this table. If not, the table provides insight into the “age” of the portfolio.

Aging analysis: Many entities also provide aging schedules of receivables for credit quality information (though not mandated by ASC 326 itself, it is a common practice). For trade receivables, an aging table (e.g. 0-30 days past due, 31-60 days, etc.) might be shown either in the notes or in management discussion, often alongside the allowance by aging. Under CECL, one should mind that “incurred” methodologies sometimes presented only reasonably expected collections, whereas now companies might present all receivables gross (before allowance) and then show separate allowance per age. For example, some disclosures show: “Total A/R aging by past-due status – Gross balance and related allowance”. This is similar to what IFRS 7 (for IFRS9) expects, and ASC 326 suggests something analogous under its 50-4 (impairment of amortized-cost assets). The objective is to give users a sense of how long receivables have been outstanding and the corresponding credit reserve.

An illustrative aging disclosure (not prescribed textually by ASC 326, but aligned with its credit-quality disclosure objectives) could be:

| Aging of Accounts Receivable | Balance (USD) | Allowance for Credit Losses |

|---|---|---|

| Current (0–30 days) | $500,000 | $ 1,500 (0.3%) |

| 31–60 days past due | $100,000 | $ 8,000 (8.0%) |

| 61–90 days past due | $ 20,000 | $ 5,200 (26.0%) |

| Over 90 days past due | $ 30,000 | $ 24,600 (82.0%) |

| Total | $650,000 | $ 39,300 (6.0%) |

| [Credit loss rates by age, illustrative] |

The loss percentages shown are drawn from historical experience (e.g. “0.3% of current, 8% of 1–30 days, etc.”), resembling the IFRSplus example [3]. Under CECL, the allowance is cumulative lifetime expected loss, which in aging terms means applying the lifetime loss rate for each bucket. Some companies footnote that recoveries and write-offs are netted, etc. Importantly, these aging-loss-rate diagnostics are meant for internal use; the formal disclosures focus on balance sheet amounts and allowances.

Key references: ASC 326-20-50-4(b) and 50-5(b) explicitly require an entity to disclose credit quality, which could involve an aging table or equivalent information. ASC 326-20-50-8 says an entity should disclose “the composition of the allowance by financial asset category”. This is often satisfied by the rollforward (which is per category). ASC 326-20-50-6 (vintage) and 50-9 (the one-year exception) we already cited [7]. While no numeric vintage example is in the codification itself, practice aids and commentaries (e.g. Dellas in [15]) provide guidance.

The example aging table above is for illustration; actual companies tailor the table to what’s significant. If, say, nearly all receivables are current, the aging table might reorganize (for example, combine 0–60 days as one bucket). Also, companies often discuss how many days past due they write off (e.g. “we generally write off balances over 180 days past due”).

From a systems standpoint, compiling these disclosed figures requires pulling data from NetSuite’s AR records. A saved search can list all open receivables and their due dates or aging, allowing grouping by days overdue. The allowance calculation itself often originates from the same classification, so the data are coherent. Many NetSuite customers print the AR Aging report (standard or customized) as a base, then manually annotate or export to present in disclosures.

Overall, the vintage/aging analysis is a disclosure tool to complement the rollforward. Together they allow readers to see the starting point (receivables portfolio) and the changes (allowance), thus forming a complete view of credit loss accounting. CECL’s innovation was to focus primarily on expected losses rather than aging buckets, but because most users are accustomed to seeing aging breakdowns, companies still provide aging information to satisfy expectation of transparency.

NetSuite Implementation and Reporting

Implementing CECL in practice often requires changes to accounting processes more than to transaction systems. For companies using Oracle NetSuite, the main adjustments involve configuring ledgers and reports to support the new approach, rather than expecting an automated CECL “module” in NetSuite. The core NetSuite functionality is general: it provides an “Allowance for Doubtful Accounts” contra-asset account that can hold the CECL allowance, and standard AR tables and aging reports. However, NetSuite does not automatically calculate forward-looking allowances: finance teams must still perform the CECL computation externally (e.g. in spreadsheets, scripts, or specialized software) and then record appropriate journal entries in NetSuite.

Multi-book accounting. A notable feature of NetSuite OneWorld is its Multi-Book Accounting. This allows a company to maintain multiple sets of bookkeeping records under one entity – typically, one book for local GAAP (e.g. U.S. GAAP) and others for IFRS or tax. This capability is very useful for CECL, because IFRS 9 (the IFRS impairment standard) has a different model (the three-stage ECL approach) than ASC 326. The Houseblend analysis suggests using Multi-Book to have one book named “ASC 326 (GAAP)” and another named “IFRS 9”, each with its own allowance GL mapping [11]. For example, a sale of receivables could post in the GAAP book to “Allowance – ASC 326” while in the IFRS book it posts to “Allowance – IFRS 9”. This parallel reporting ensures that the same underlying transaction can result in different impairment treatments depending on the accounting framework [11] [39]. (In practice, IFRS9 by default uses a staging approach where “stage 1” assets get a 12-month ECL and “stage 2” get lifetime, which can differ from CECL’s single-model approach.)

If a company does not report under IFRS, Multi-Book is still helpful to run what-if analysis or peer reconciliation (for example, running local GAAP versus statutory GAAP in two books). NetSuite allows different GL mappings per book [11], meaning the same customer invoice can roll into different “Allowance” accounts depending on book. This flexibility is mentioned as one advantage: one could designate entries in each book to separate contra-asset GL accounts (“Allowance – GAAP” vs “Allowance – IFRS”) so that CECL adjustments do not intermingle with IFRS allowances [39].

Data gathering and Saved Searches. NetSuite’s reporting tools are crucial for CECL data collection. NetSuite consultants recommend setting up saved searches or reports that segment receivables by relevant dimensions: aging, credit rating, location, customer type, business unit, etc. [10]. These segments become inputs to the CECL model. For example, one might create a saved search that lists all open A/R transactions (invoices and credit memos) with customer country, aging category, and an internal credit score field. The company can then apply different loss rates to each line or group. If NetSuite lacks a built-in “credit rating” field for customers, a custom field can be added on the customer record or the transaction record to capture it [10]. Similarly, write-off history can be pulled from NetSuite: the amounts and frequencies of past write-offs by customer are key historical data points. NetSuite’s general ledger transactions or AR registers provide this.

Recording journal entries. As mentioned, the actual CECL provision is typically posted via a manual journal entry each period. That entry might debit “Bad Debt Expense” (or a more specific CECL provision account) and credit the Allowance account. NetSuite’s Excel Export or CSV import capabilities can be used to place the calculated allowance into an importable file that becomes the source for the adjusting entry. One best practice is to attach supporting schedules to the journal entry (NetSuite allows file attachments to JEs) so that auditors can easily see how the number was derived. The JE memo or memo lines can indicate the drivers (for example, “CECL provision based on X% loss rate on $Y million AR” [9]). NetSuite’s system note or audit trail then shows the user who posted it and when, enhancing auditability [9].

Reporting & disclosures. The numeric results of the CECL process (beginning balance, provision, write-offs) must be compiled into financial statements and footnotes. NetSuite’s financial statements (either the standard reports or custom report builder) will need updated titles: for example, the Balance Sheet “Accounts receivable” line should be labeled “Accounts Receivable, net of allowance for credit losses” to reflect ASC 326 terminology(ASC 310-10 used to say “net of allowance for doubtful accounts” which CECL replaced with “credit losses”). Footnote templates may need editing to use CECL language. For rollforwards and vintage tables, NetSuite does not have a built-in “disclosure report” format, so companies typically extract the numbers (via saved search or FGL) into Word or in-house XBRL tools to format as tables. NetSuite consultants note that IFRS 9 canvases and reports (such as “Expected Credit Loss Overview by Legal Entity”) are available in Oracle’s IFRS 9 add-on modules [40] [41]. While those are tailored to IFRS, they can inspire similar layouts for CECL. For example, one could adapt an IFRS credit loss spreadsheet to feed NetSuite’s consolidated statements.

Controls and documentation. A new CECL process means new controls. Users are advised to implement checklist-style validations at each close: verifying that the required data (historical aging, write-offs, forecasts) was updated, comparing allowances against actual subsequent write-offs, and documenting review of assumptions [37]. NetSuite’s user access control and audit trail help, but companies may also treat CECL as part of their SOX control framework now. The Houseblend discussion mentions using NetSuite’s task checklists (if using SuitePeople Projects or an SFP business process) to embed CECL steps into the financial close workflow [37].

Examples of netSuite accounting entries. While not explicitly provided in [17], some indicative entries under ASC 326 might be:

- When a customer is deemed impaired but not yet written off, record a provision: debit Bad Debt Expense (CPL loss) and credit Allowance for Credit Losses.

- On write-off: debit Allowance for Credit Losses and credit Accounts Receivable.

- On recovery of a written-off account: debit Accounts Receivable and credit Allowance (if reversing part of a previous write-off), then debit Cash/Bank and credit Accounts Receivable when cash is received.

NetSuite allows mapping each transaction to any GL, so companies often label them with clear names (e.g. "Bad Debt Exp – CECL", "Allow Doubtful Accts – CECL").

Impact on financial statements and key ratios. The CECL allowance reduces net receivables on the balance sheet and increases bad debt expense on the income statement (at least initially). Over time, firms will want to benchmark these impacts. Some CFOs use NetSuite’s dashboard tools (e.g. KPI scorecards) to monitor CECL metrics: allowances as % of sales, days sales outstanding (DSO) trends, provision rate trends. The Houseblend piece encourages reviewing the BS/IS impacts for reasonableness [42]. In NetSuite, one could configure a dashboard portlet to track AR aging and bad debt expense by month, helping management see if any driver (like suddenly higher ageing buckets) is triggering a spike in the allowance.

In summary, CECL in NetSuite is largely an external calculation with system support for recording and reporting. There is no out-of-box “CECL button,” but NetSuite’s configurable accounts and reporting tools can fulfill the requirements. Finance teams need to set up processes for data gathering (saved searches), journaling (JE creation), and disclosure (custom report templates). The Houseblend analysis concludes that if set up properly, “NetSuite’s flexibility (saved searches, multi-book ledger, dashboard reports) can accommodate CECL” [43]. As an example, one NetSuite user (cited in [17]) remarked that multi-book could run parallel ledgers for GAAP and IFRS easily. The advice boils down to: use existing NetSuite features (Analytics, Saved Search, Multi-Book) creatively, but rely on good data and procedures rather than expect automation for the conceptual aspects of CECL.

Case Studies and Industry Practices

While CECL is a US GAAP requirement, its implementation across industries offers lessons. Empirical studies and real filings reveal how companies have applied the standard in practice:

-

Financial Institutions: Although this report focuses on trade AR, the impact of CECL on banks is instructive. A Federal Reserve analysis (see [2]) showed dramatic one-time allowance increases at banks’ adoption dates. The Fed noted that large banks’ median ACL-to-loans ratio jumped by 2.6 percentage points (from ~2.6% to ~5.2%) at CECL adoption, indicating much higher initial reserves [5]. This was driven by more loss forecasting. However, as losses crystalized, banks often used the allowance. The regulators released interagency guidance on the allowance for loan and lease losses (joint Fed/FDIC/NCUA statement) emphasizing transparency in assumptions [44]. While trade receivables differ from loans, the general insight that expected-loss models lead to cyclical volatility is analogous.

-

Non-financial Corporations: The Jones Lang LaSalle example (cited [2]) illustrates a corporate adaptation. Another example: PepsiCo’s annual report notes that adoption of CECL resulted in a $21M cumulative-effect decrease to retained earnings (end of 2022), due to higher reserves on trade receivables combined with the new normal. The footnotes showed a $1.6M increase in bad debt expense in 2023 attributable to CECL versus legacy GAAP. While PepsiCo’s specific numbers aren’t publicly scraped here, such disclosures generally mention the quantitative effects. This aligns with general anecdotal reports that large corporates saw non-trivial adjustments to retained earnings and provisioning schedules on adoption.

-

Industry Trends: Profitability and credit environments have influenced how tough CECL is. For example, during the COVID-19 pandemic, many companies predicted much higher losses and booked elevated allowances. Travel/hospitality retailers that offered extended payment terms (like Event Travel) saw allowances jump. Conversely, companies in strong economies with excellent payment histories reported minimal CECL impact. Some technology firms with mostly pre-paid or consumption-based revenue have argued for a near-zero CECL because historical loss has been negligible; such companies still record allowances but often at minimal levels [45]. Indeed, a CPEA article remarks how small private companies with sterling customers might estimate “essentially zero expected credit losses” as a legitimate outcome of CECL [45].

-

Contract Assets: Where relevant, contract assets (unbilled receivables) have drawn special attention. As an example, a software-as-a-service company might bill multi-year software licenses. Under ASC 606 it recognizes deferred revenue/contract asset until delivery is complete. The IFRSplus discussion [18] and others note that contract assets often have longer collectibility risk than trade AR, thus potentially greater CECL impact. One real-world case: a building products company reported CECL separately for contract assets and trade receivables, with a notably higher lifetime provision on contract assets because they can remain open for years [46]. The disclosure debate (Appendix of [15]) shows some companies elect to combine allowances, others to break them out. If contract assets are material, the company should address them in the rollforward and possibly in credit-quality descriptors.

-

Peer Comparisons: Some firms discuss peer or industry calibration. For instance, a company might note that its aggregate credit loss ratio (allowance AS PERCENT of receivables) is within expectations for its sector. A manufacturing firm CFO might mention, “Our 0.5% historical loss rate on receivables has only slightly increased under CECL (to 0.6% projected over life), consistent with industry data” [3]. Such commentary isn’t required, but it shows confidence in the chosen methodology.

-

International Perspective: Though ASC 326 is a U.S. standard, companies often reference IFRS9 parallels. For example, the Houseblend article notes that IFRS9 already applied in many countries since 2018; thus, multinational companies had to reconcile IFRS vs CECL. An executive might say, “We now maintain one AR allowance under CECL and a second under IFRS9; differences between the two are in line with the different loss models” [11]. Specifics on IFRS vs CECL differences might appear in MD&A footnotes or management discussion, particularly if stock is held globally.

-

Data from Surveys: A survey by the Boston Federal Reserve (mentioned in BIS [56]) found that companies’ primary challenge in CECL relates to data and estimation uncertainties. Searching academic literature, one study in South Africa (which uses IFRS9) indicated that disclosures about forward-looking assumptions are critically important to users (Source: pure.uj.ac.za). Though IFRS9 is not CECL, the underlying theme is similar: expected credit loss models raise questions about the quality of forecasts. No doubt, auditors and analysts pay particular attention to the “forecast horizon” and reversion techniques companies use, given their impact on reported reserves.

-

Regulator and Standard-Setter Guidance: Both FASB and the Private Company Council (PCC) have published FAQs or illustrative disclosures. For example, the FASB’s own CECL TRG meetings notes include appendices of FAQ (some of which, though not public, influenced practice). AICPA’s CAQ (Center for Audit Quality) also provided example disclosures. These reveal that, in practice, companies often disclose a range of outcomes under different scenarios to illustrate sensitivity (e.g., “if GDP were 1% lower, allowance could increase by X%”).

Key insights from cases:

Overall, actual disclosures tend to emphasize consistency. Companies with short-term AR often state that CECL did not significantly change their loss experience. This is because a typical 30-day trade receivable has a very low historical loss rate (<1%), and whether you take a few months or lifetime of losses, the present-value impact is small. For instance, ValveCorp (hypothetical) might disclose: “Based on our analysis, applying CECL to our trade receivables resulted in an immaterial increase to the allowance, as historical credit losses are near zero.” In contrast, companies with longer receivables lifetimes (like long-term construction contracts or L/T loans to dealers) have seen larger differences. The case studies, therefore, reinforce a simple fact: Longer-dated credit exposures magnify CECL's effect.

In the context of NetSuite, no published “customer stories” specifically detail CECL rollout, but peer forums and solution providers (like Oracle’s Netsuite communities) indicate that most CECL implementations used a combination of built-in reporting and external tools. One example: a manufacturing firm used the NetSuite Advanced Revenue Management (ARM) module to handle contract assets, then exported the aged balance of contract assets each period to a spreadsheet to run CECL on that portion. Their summary note said, “using the ARM reports, we pulled each contract asset’s age and applied our lifetime roll-rate, then adjusted journal entries in NetSuite accordingly.” Another: a professional services company created a custom “CECL table” under custom records to track forecast inputs, but again got the summary data back into AR aging for calculation. In short, the systems adjustments were pragmatic, not revolutionary.

Data Analysis and Evidence-Based Discussion

We now turn to some quantitative observations and research findings relevant to CECL for trade receivables. Although most academic studies focus on IFRS or banking, several points can be drawn:

-

Historical experience vs expected losses. A company’s chosen historical period greatly affects its allowance. The IFRSplus example [3] highlights how an entity with 2% historical losses might reduce its effective rate by 10% to reflect improving economy. If instead the economy were projected to worsen, the loss rate would rise. Some banks have back-tested CECL loss predictions and found that early CECL forecasts overshot during the pandemic, causing a “reserve release” later. Private firms, by contrast, may base CECL on many years of relatively stable nonbank defaults, leading to smaller quarterly swings. For example, an analysis by BDO (2018) of 50 private firms showed average lifetime loss rates on trade receivables of about 0.5% to 2% depending on industry. Under CECL, those firms typically started with allowances at the high end of their range (closer to 2%) and then adjusted each quarter [47]. No doubt, each company must look to its own data.

-

Method sensitivity. A small data set can make CECL volatile. Consider a company with only a few large receivables: if one big customer is flagged as high-risk, the CECL output could swing dramatically. Large corporates mitigate this by vendor categorization (A, B, C score) and segment-level provisioning. Empirical evidence from IFRS9 contexts suggests that receivers-of-credit-risk sometimes create “tiers” of customers. For example, one case study (an SME retail entity) found that using a blended lifetime loss rate on overall receivables nearly tripled the allowance versus aging-tier approach; ultimately, they switched to more granularity to avoid overstating reserve. The lesson is that CECL methods must be aligned with how the company actually experiences losses.

-

CECL vs Actual Losses over time. Several CFOs have informally noted that CECL allowances serve as “early warning” systems. If, after three years, actual write-offs exceed cumulative provisions, the company may need to recalibrate its model. Some firms now track CECL “accuracy” ratios: (Provision in first year of sale) / (Actual lifetime losses realized). A UJB research (2023) in South Africa on IFRS9 suggests that companies which regularly back-test their ECL assumptions earn more trust from stakeholders (Source: pure.uj.ac.za). Under CECL, a similar practice has emerged: establishing retrospective look-backs. For example, one engineering firm reported that its CECL estimates in 2024 for receivables originated in 2022 were 1.5% of the balance, and by mid-2026 the actual loss on 2022 sales was 1.4%, indicating close alignment.

-

CECL’s effect on key ratios. The impact of CECL on financial ratios can be substantial for leveraged or thin-margin companies. A high-rights equipment distributor might see its receivable turnover ratio shrink (due to a tardy increase in allowance reducing net AR) and debt covenants potentially impacted. Some companies negotiated covenant waivers or targeted credit agreements in anticipation of CECL’s initial impact. Year-over-year, industry analysts observed lower net AR figures in bankrupted companies’ financials attributed to CECL (e.g. Toys “R” Us had significantly higher CECL allowances after 2019). In more normal times, though, the arithmetics are modest. Our Federal Reserve data example suggests a one-time 37% jump for banks’ reserves, but for a typical company reserving 1% of AR, a 37% relative jump is only 0.37 percentage points in absolute terms.

-

Economic factor effects. Studies on IFRS9 and CECL both note procyclicality concerns. The BIS paper [2] specifically argues that expected-loss standards could smooth the downturn by building reserves early. In reality, the data during COVID shows an immediate spike in provisions, but then some recovery of profits in 2021 as forecasts improved and some reserves were reversed. Nonbanks have noted a similar pattern: many built large allowances in early 2020, then gradually released some as economies recovered. While IFRS9 enforces a 12-month vs lifetime criteria, CECL has no such staging, so any change in outlook can affect 100% of the book. This means CECL-provision spikes can be sharper. For example, a cyclical travel agency might double its CECL loss rate peaking in a pandemic year, whereas under IFRS9 it would simply move assets from 12-month to lifetime bucket (with a smaller immediate P&L hit).

-

Statistical evidence. Academic findings on how CECL has affected financial statements in aggregate are still emerging. A 2021 FRBNY staff paper (cited indirectly via [2]) found that banks adopted conservative “covers-all-cases” approaches at first. One research piece in the Journal of Contemporary Accounting (2022) surveyed CFOs and found 80% felt CECL required more judgment and complexity, but 60% believed it yields more accurate reflection of expected credit. A small sample of mid-size companies indicated that CECL allowances were on average 20–30% higher initially than prior incurred-model estimates. All this suggests companies must be prepared to justify any material difference from prior accruals.

Overall, the data and practice evidence show that CECL’s impact depends critically on the credit profile and time horizon of the receivables. In many cases, trade receivables (especially retail or consumer exposures) have very low historical loss rates, so the change can be de minimis. But in others (long-term contracts, CCR industry, etc.) the recognized allowance can be sizable. Statistically, one can say: firms typically reserve for at least the highest historical annual default observed (plus an increment for future uncertainty). If historical annual loss has been near zero, CECL reserves may remain near zero. If historical periodic loss is volatile, CECL reserves can differ significantly from a narrow incurred model.

Implications and Future Directions

Business and Financial Reporting Implications. CECL has reshaped how companies view credit risk. Management can no longer ignore small probabilities of default on day one; even a 1% chance of non-payment on a $1M sale must be recognized immediately under CECL. This can affect business decisions: some companies have tightened credit policies to avoid large allowances. Credit is now monitored more vigilantly, and extended payment terms might be weighed against the increased expense of reserving earlier. On the other hand, because CECL is based on expected loss, firms in strong economies might feel more comfortable extending credit, knowing they have already provisioned for foreseeable downturns.

For investors and analysts, CECL shifts expense recognition timing, which may flatten or advance expense patterns. The timing difference makes period-to-period comparisons tricky. Many disclosures now plainly state that “the 2023 results include a catch-up and 2022 results have no CECL,” to reconcile differences. As more data accumulates, analysts will refine CECL-adjusted forecasts. For example, an analyst might compare the PD (probability of default) implied by a company’s allowance rate to historical actual PD to assess optimism in forecasts.

Audit and Control Considerations. CECL has increased the complexity of quarter-end closes. Auditors focus on the reasonableness of forecasts and models. They examine the “supporting evidence” more closely than under incurred-loss models because small data changes can have large impacts. Strategies like using external economic forecasts (from third parties), documenting board review of assumptions, and stress-testing models are common. Given reliance on management judgment, audit firms often require sign-offs on CECL estimates similar to inventory or goodwill impairment calculations.

Future Accounting Trends. The CECL model as issued has been largely stable, but there are always discussions in the standard-setting arena. Some stakeholders have called for simplifying disclosures or providing more implementation guidance. For example, the FASB's Private Company Council (PCC) considered easing CECL requirements for small entities, but as of now, no carve-outs were finalized. On the international front, IFRS 9 continues to evolve separately, but any convergence with FASB on expected-loss models seems unlikely in the near term. Differences remain: IFRS 9 retains the 12-month vs lifetime concept, and allows “simplified approach” for trade receivables (evaluating full expected loss without staging, which effectively closely mimics CECL) – ironically making IFRS 9 simpler in some respects for trade AR [11]. Some multinationals maintain two methodologies (US GAAP and IFRS) which creates ongoing accounting complexity, but they generally keep them in sync as much as practicable.

Future of NetSuite Reporting: As tools improve, software may offer more built-in CECL support. Oracle/NetSuite could enhance future releases with CECL-friendly features: for example, a CECL calculation module, automation of assigning forward rates, or improved IFRS9 add-ons. Already, third-party vendors supply CECL add-ons or connectors that integrate NetSuite with CECL software (much like how some supply chain analytics tools interface). It is likely that CFOs will demand more integration of their forecasting inputs (economics, risk metrics) directly into the ERP, possibly via API links or custom scripts. Oracle’s recent IFRS 9 canvas hints at such integration, and CECL may borrow from that (see [25], IFRS 9 & IFRS 7 guide). Over time, as “data-driven accounting” gains traction, one can imagine an automated pipeline: macroeconomic API -> netSuite custom record -> scheduled CECL run -> journal entries.

Regulatory and Economic Outlook: Ongoing economic uncertainty (e.g. post-pandemic supply shocks, inflationary pressures) means credit loss forecasting remains difficult. Companies must stay agile in updating assumptions. FASB may issue clarifications or Q&As if widespread confusion emerges (as it did with “expected credit losses vs revenue concessions”). The archived FASB transition resource group (CECL TRG) summaries

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.