Is a Right-of-Use Asset a Fixed Asset? ASC 842 Guide

Executive Summary

Under both IFRS 16 and ASC 842, lessees must recognize a right-of-use (ROU) asset on the balance sheet for virtually all leases longer than 12 months. In practice, ROU assets function like capitalized assets: they are recorded as long-lived assets and amortized over the lease term, even though legal title to the underlying item typically does not transfer. IFRS 16 explicitly requires that an ROU asset initially include the lease liability plus initial costs, and “after lease commencement the ROU asset is accounted for in accordance with IAS 16” (the Property, Plant & Equipment standard) [1]. Likewise, ASC 842 (U.S. GAAP) treats the ROU asset as a long-lived nonfinancial asset subject to the same impairment and depreciation rules as owned fixed assets [2]. Thus, although an ROU asset is not a “traditionally owned” fixed asset, accounting standards effectively classify it alongside property, plant, and equipment. In financial statements the ROU asset appears under noncurrent assets (often adjacent to PPE) [3]. In NetSuite (Oracle’s ERP), the Lease Accounting SuiteApp creates actual fixed-asset records for ROU assets – for example, generating a “Right-of-Use Asset” fixed-asset account and related accumulated depreciation account – and posts initial and recurring depreciation entries just like other fixed assets [4]. This report explores the background and purpose of the ROU asset concept, contrasts IFRS 16 and ASC 842 treatments, examines balance-sheet presentation, and reviews how NetSuite implements ROU assets in practice. We include authoritative guidance, data on the magnitude of lease capitalization, and real-world examples showing how ROU assets are classified and reported.

Introduction: IFRS 16 / ASC 842 and the Rise of the ROU Asset

Lease Accounting Reform (Background): For decades under IAS 17 (IFRS) and ASC 840 (U.S. GAAP), many operating leases were off–balance-sheet, with companies reporting only rent expense and disclosing lease commitments in footnotes. This obscured the true scale of long-term obligations. As IASB Chairman Hans Hoogervorst observed in 2016, listed companies world-wide had roughly US $3.3 trillion of leases, and over 85% of those were off-balance-sheet operating leases [5]. For example, retailers and airlines often appeared under-leveraged despite huge lease commitments.

To address this, the IASB issued IFRS 16 (effective 2019) and FASB issued ASC 842 (effective 2019 for public companies, 2022 for private). Both require lessees to recognize a Right-of-Use (ROU) asset and a corresponding lease liability for most leases > 12 months. In simple terms, a ROU asset is “a lessee’s right to use an underlying asset for the lease term” [6]. IFRS 16 adopts a single-lessee model: all leases (barring short-term or low-value exceptions) produce an ROU asset and liability. ASC 842 retains the distinction between operating leases and finance (capital) leases, but both types are placed on the balance sheet with ROU assets and liabilities.

Definition and Scope: A lease is “a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration,” under IFRS 16 (similar wording in ASC 842). The ROU asset arises at lease commencement and equals the present value of remaining lease payments (the new liability) plus any prepaid lease payments or initial direct costs [7]. It is subsequently depreciated (amortized) over the lease term. Importantly, under IFRS 16 the lessee’s ROU asset is treated as a tangible asset of the lessee (even though legal ownership belongs to the lessor), while under ASC 842 it is recognized as a nonfinancial long-lived asset (analogous to PPE). IFRS 16 even specifies that the ROU asset is normally accounted under IAS 16 (Property, Plant & Equipment) [1], whereas ASC 842 requires evaluation of ROU assets under ASC 360 (Property, Plant, & Equipment) impairment rules [2].

Fixed Asset vs. ROU Asset: The term “fixed asset” typically denotes a resource owned by the company (PP&E and sometimes long-lived intangibles). An ROU asset is not owned but grants control of an asset. Nevertheless, accounting rules treat ROU assets very similarly to fixed assets. They are recorded on the balance sheet as noncurrent assets (often categorized alongside PP&E) [3]. The ROU asset is then amortized or depreciated on a systematic basis – straight-line or otherwise – over the lease term. In effect, for accounting purposes the distinction between an ROU asset and a fixed (owned) asset is blurred: both are capitalized and expensed over their useful lives, and both fall under the same impairment and derecognition standards [2].

This raises a natural question: is a Right-of-Use Asset a Fixed Asset? The answer is nuanced. By economic substance, an ROU asset is like an intangible right. But by accounting convention, it is treated much like a tangible long-lived asset. IFRS 16 explicitly links ROU to PPE (IAS 16), and U.S. standards subject ROU to the same rules as PP&E under ASC 360 [1] [2]. Thus, while ROU assets may not appear under the literal heading “Fixed Assets (PP&E)” in every report, their measurement and presentation are fixed-asset–like. In practice, many companies display ROU assets in a dedicated lease section, sometimes titled “Leased ROU Assets,” often adjacent to or even combined with owned PP&E lines. We explore these balance-sheet and reporting treatments later in this report.

ASC 842 Classification of Leases (ROU Assets)

Under U.S. GAAP (ASC 842/Topic 842), each new lease must be classified as a finance lease or an operating lease at inception. This classification affects income-statement presentation but does not affect the fact of capitalization – both types require recording an ROU asset and lease liability (except for short-term leases). The classification criteria are largely the same as under the old ASC 840:

-

Finance Lease Indicators: Ownership of the underlying asset transfers to the lessee by end of term, or the lease grants a bargain-purchase option; or the lease term is for a “major part” of the asset’s economic life (generally interpreted as 75%+); or the present value of lease payments equals substantially all (≈90%+) of the asset’s fair value; or the asset is highly specialized (usable only by the lessee without major modifications) [8] [2]. If any one criterion is met, the lease is classified as a finance lease (akin to the old capital lease).

-

Operating Lease: If none of the above criteria are met, the lease is an operating lease. Under ASC 842, operating leases have identical balance-sheet treatment to finance leases – both yield a ROU asset and liability – but differ in P&L pattern. Finance leases produce front-loaded expense: the ROU asset is amortized and interest on the liability is accrued separately (like a financed purchase), resulting in higher expense early in the term [9]. Operating leases yield a single straight-line lease expense – effectively the amortization of the ROU asset only – so the expense is level over time (akin to the old rent expense) [10].The classification rules and accounting impact are summarized below:

| Lease Type | ROU Asset & Liability on BS? | Income Statement Pattern | Example GL Accounts |

|---|---|---|---|

| Finance Lease | Yes – ROU asset & lease liability (PV of payments) are recognized at commencement [10]. ROU asset is amortized down to $0 (if title transfers). | Separate interest expense (on lease liability) and depreciation/amortization of ROU asset [9]. Imputed interest causes larger expense in early years. | ROU asset (Fixed Asset), Accum. Depr – ROU; Lease Liability (current/noncurrent); Interest Expense. |

| Operating Lease | Yes – ROU asset & lease liability recognized at commencement [10]. ROU asset is amortized straight-line. | Single lease (rent) expense per period (equal to straight-line amortization of ROU) [10]. No separate interest shown. Level expense each period. | ROU asset (Fixed Asset); Accum. Depr – ROU; Lease Liability; Lease Expense (Operating). |

Table 1: Lease classification under ASC 842. Both types recognize an ROU asset (capitalized fixed asset) and lease liability, but P&L treatment differs [10] [2].

The result is that nearly all leases become capitalized assets and liabilities. ASC 842 explicitly notes that “right-of-use assets, like other long-lived nonfinancial assets, fall within the scope of ASC 360 (Property, Plant, and Equipment) for purposes of impairment” [2]. In other words, FASB intends ROU assets to be treated as fixed (PPE-type) assets for subsequent accounting – they are depreciated and subjected to PPE impairment tests.

ROU Asset on the Balance Sheet

ROU assets are presented as noncurrent assets on the balance sheet. Under a classified balance sheet format, ASC 842 indicates ROU assets follow the same current/noncurrent classification rules as any long-lived asset [11]. (E.g., if a lease has just a few months remaining, any remaining ROU asset becomes current.) In practice, many companies report ROU assets in one of two ways:

-

Separate lease line items: Commonly, companies list ROU assets in dedicated line items, separate from owned property. For example, in SEC filings one often sees a line for “Operating lease right-of-use assets” and (if applicable) “Finance lease right-of-use assets.” Apple’s Q2 2023 filing, for instance, details ROU assets by category: $111.5M of building ROU assets for operating leases, plus smaller ROU amounts for equipment, etc. [12]. These are shown apart from “Property, Plant and Equipment” for owned assets. (LegalClarity explains that operating-lease ROU assets are generally “kept separate from property, plant, and equipment” that the company owns, though finance-lease ROU assets may sometimes be merged with owned PP&E by some companies [13].)

-

Combined with PPE: Some entities (especially for finance leases) may present ROU assets on the same line as property, plant and equipment. ASC 842 itself does not mandate separate line items for ROU vs owned assets; it allows, for example, showing finance-lease ROU assets as part of owned PPE as long as the notes break out the amounts [13]. However, the key requirement is that operating and finance lease ROU assets be distinguished (because the standard views them differently). Companies often reconcile these balances in notes or schedules.

In either case, the net increase in reported assets is significant. Analyst reports and studies have shown that bringing all leases on-balance-sheet can raise total assets substantially (e.g. EY found ~14% higher assets in lease-intensive industries after IFRS 16 adoption [14]). On the balance sheet, the effect is to convert off-balance-sheet rent obligations into tangible asset and liability entries.

Example: ROU Assets in Practice (Public Company Disclosures)

A useful illustration is to look at actual financial statements of large companies. For example, in its 2023 Q2 10-Q, Apple Inc. breaks out its lease ROU assets under those headings. It reports total ROU assets of $118.5M (net), comprised largely of building leases ($111.5M operating-lease ROU) and a few million in equipment leases [12]. These appear alongside other assets in the non-current section. Notice that Apple splits operating vs. finance ROU and lists them as separate line items (“Operating lease right-of-use asset” vs. “Finance lease right-of-use asset”) [12], in compliance with ASC 842’s requirement.

Another corporate example (under IFRS) is Japanese electronics firm Anritsu Corp. in its IFRS financial statements (year ended March 2024). Anritsu reports ROU assets by major asset type (buildings, plant and equipment, etc.), effectively treating them like owned fixed assets. Their disclosures show ROU assets (for leases of buildings, vehicles, equipment, etc.) depreciated over time much like owned PPE. (A translated schedule in their notes shows “Right-of-use assets – Buildings and structures: ¥2,231M in 2024, down to ¥1,697M in 2025”, and similar lines for machinery and land.) In fact, Anritsu’s notes explicitly state that ROU assets are presented under “Tangible fixed assets” and depreciated according to their fixed-asset depreciation policies [15]. This aligns with IFRS 16’s instruction to treat ROU assets under IAS 16.

These examples show how ROU assets effectively join the ranks of fixed assets on the balance sheet, even if they originated as leased items.

Classification of a ROU Asset: Fixed Asset or Intangible?

From an accounting taxonomy viewpoint, ROU assets have characteristics of both. On one hand, a ROU asset is an identifiable asset (the right to use a leased item) and is measurable, thereby fitting the definition of an asset. On the other hand, it is not a physical owned asset, so one might think it’s an intangible. However, IFRS 16 directs us to account for ROU under IAS 16 (unless the underlying asset is itself an intangible) [1]. IAS 16 deals with tangible fixed assets, and reasoning is that the lessee has effectively “control” similar to a fixed asset. Therefore, IFRS treats ROU assets with tangible asset accounting (depreciation, impairment, etc.).

The fact that IFRS 16 says “account in accordance with IAS 16” implies ROU assets are, for accounting purposes, in the PPE realm. Some practitioners interpret the ROU as an intangible special case, but IFRS guidance signals otherwise. Nor does IFRS 16 move them into IAS 38 (intangible assets) except by exception (e.g. if underlying is intangible). Accordingly, many IFRS preparers include ROU assets alongside PP&E in their statement of financial position (at least in the notes).

For U.S. GAAP, Board guidance also clearly treats ROU assets as PPE-like. ASC 842 itself does not explicitly say “ROU goes under PPE”, but the FASB’s basis for conclusions and implementation notes do. As Grant Thornton observes, FASB describes the ROU asset as a “long-lived nonfinancial asset,” and accordingly subjects it to ASC 360 (which governs impairment of PPE and finite-lived intangibles) [2]. Similarly, a Crowe survey notes: “Under U.S. GAAP, the ROU asset is considered a long-lived asset that is accounted for following Topic 842’s guidance; lessees must also evaluate the ROU asset for impairment under ASC 360 (Property, Plant, and Equipment)” [2]. In other words, FASB implicitly folds ROU assets into the long-lived asset framework (i.e. fixed assets).

From a chart-of-accounts perspective, companies implementing ASC 842 often set up ROU assets as fixed-asset accounts. The NetSuite example below (Table 2) highlights typical G/L accounts: a “Right-Of-Use Asset” fixed-asset account (with a contra Accumulated Depreciation account), a “Lease Liability” account (current/noncurrent liability), and expense accounts for interest or amortization. This mirrors how any capital asset would be tracked [4] [16].

Taken together, the evidence is clear: accountingly, a right-of-use asset is treated as a long-lived fixed asset. Its economics are lease-based, but its booklet effect on the balance sheet and income statement is that of capitalized property. The key distinction is whether one owns the underlying item; but for reporting purposes, control under a lease produces an asset just like control by ownership.

NetSuite Treatment of ROU Assets

NetSuite’s Fixed Assets Management SuiteApp provides dedicated support for lease accounting under ASC 842 and IFRS 16. The system is built to create and manage ROU assets as fixed assets within the general fixed-asset module. Here are key points of NetSuite’s ROU asset treatment:

-

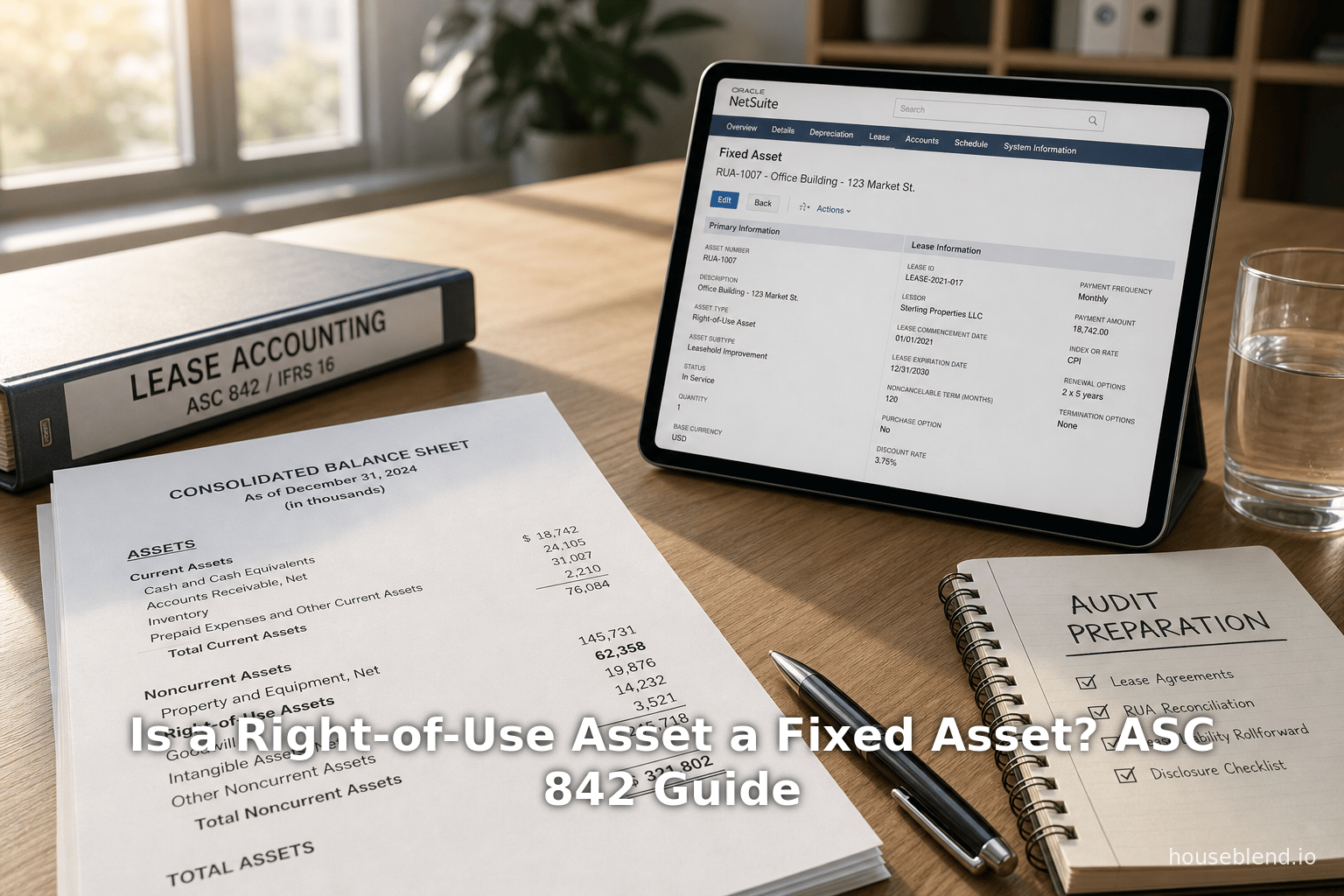

Lease Record and Asset Proposal: The user first enters lease details (term, payments, classification, etc.) into a Lease record. NetSuite then generates an amortization schedule and, at commencement, produces the journal entry: Debit ROU Asset, Credit Lease Liability. At that point, the lease is flagged as “Asset Proposed.” The user then runs an “Asset Proposal” to actually create a Fixed Asset record for the ROU [17]. This links the lease to a tangible fixed-asset entity in the system. The asset record has an “Asset is Leased” checkbox and a Lease subtab, so that NetSuite knows this asset came from a lease [18].

-

GL Account Setup: In NetSuite, ROU assets and related items are mapped to new G/L accounts. For example (from NetSuite documentation): a “Right-Of-Use Asset” account (type Fixed Asset/Other Current Asset) captures the book value of the lease asset [4]. A corresponding “Accumulated Depreciation – ROU Asset” fixed-asset account is used as the contra-asset for depreciation [4]. The “Lease Liability” account (liability type) holds the present value of remaining lease payments [16]. There are also expense accounts: typically Interest Expense (Lease) for finance-lease interest accruals and an operating lease expense or amortization account for operating leases. Table 2, adapted from Oracle’s recommendations, summarizes key NetSuite accounts for lease ROU assets:

NetSuite GL Account Type Purpose / Use Right-Of-Use Asset Fixed Asset / Other Curr. Asset To record the initial cost of the ROU asset (amortized over lease term) [4]. Accumulated Depreciation – ROU Asset Fixed Asset (Contra) Contra-asset to Right-Of-Use Asset; tracks depreciation taken [4]. Lease Liability Liabilities (Current/Noncurrent) To record the present value of future lease payments (balancing amount to ROU Asset) [16]. Interest Expense – Lease Expense For finance leases: accrues interest on the lease liability [19]. Lease Amortization (Operating) Expense For operating leases: records the straight-line amortization of the ROU asset as lease expense. Gain/Loss on Lease Modification Other Income / Expense Recognizes any gain or loss on lease remeasurement or modification (rare) [20].

Table 2: Typical NetSuite GL accounts for ROU (lease) assets and liabilities. These are managed through the Fixed Assets SuiteApp, and NetSuite automatically generates the necessary depreciation and amortization journals each period.

- Automation and Reporting: NetSuite automates the recurring lease entries (depreciation/amortization of ROU asset, interest accrual, lease payments, reclassifications) once the setup is done [21]. It provides lease-specific reports (e.g. Right-of-Use Asset Listing, Lease Liability schedules) to track these balances. In practice, the NetSuite system treats the ROU asset just like any other fixed asset in depreciation and disposal, except it carries additional lease metadata (lease number, classification, etc.) on the asset record [18] [17].

Example Workflow (NetSuite): Consider an operating lease for office space. In NetSuite, the user creates a new Lease record (FA > Leases > New) with the lease terms and classifies it as Operating. Clicking “Generate Lease Schedule” computes a present value (say $105,666.89) and amortization. On the commencement date the user clicks “Create Lease Journal”, which automatically posts “Debit Right-Of-Use Asset $105,666.89; Credit Lease Liability $105,666.89” [17]. The lease status becomes Asset Proposed. The user then generates a fixed-asset via the Asset Proposal. Now the ROU asset exists in NetSuite’s Fixed Assets list (marked as leased) and is depreciated monthly according to the schedule. Lease payments are posted against the liability, and each period NetSuite records depreciation (for operating leases as lease expense) and interest (for finance leases) by journal.

These features confirm that NetSuite treats ROU assets essentially as fixed assets within its accounting system, aligning with the standards’ intent.

Balance Sheet Presentation and Classification

In summary, a right-of-use asset is (under ASC 842) shown in the balance sheet’s noncurrent assets, typically alongside other long-term assets. As one expert summary notes, “a right-of-use (ROU) asset sits in the noncurrent assets section of the balance sheet, alongside other long-term resources like property and equipment” [3]. Because ASC 842 ties ROU accounting to the noncurrent framework, the ROU asset usually remains noncurrent until its expected conversion to current as the lease nears its end. Only the portion of ROU amortizing within one year would be classified as a current asset, similar to how continuing depreciation works for any fixed asset [22].

Distinction from Owned Fixed Assets

Crucially, ROU assets are generally shown separately from owned PPE. For operating leases, ROU assets do not merge with owned property lines – they get their own category in the statements. LegalClarity explains that operating-lease ROU assets are kept separate from the company’s owned property, plant and equipment [23]. (This preserves clarity that these assets are leased). For finance leases, the standard allows some flexibility: companies may choose to present finance-lease ROU assets under the same line as owned PP&E or separately, as long as the notes segregate them [13]. Either approach is acceptable under ASC 842, but many large companies in practice separate them to improve transparency.

In both cases, however, ROU assets are measured and amortized like PPE. The net ROU asset decreases each period by depreciation (or straight-line amortization) plus any partial derecognitions. Companies must also test ROU assets for impairment under the usual long-lived asset rules (ASC 360 or IAS 36) [2] [24].

Comparative Presentation (IFRS vs. GAAP)

The presentation under IFRS 16 and ASC 842 is conceptually similar, though IFRS eliminates the finance-vs-operating split. Under IFRS 16, all leases give rise to ROU assets and lease liabilities. There is typically only one type of lease expense (similar to finance lease in GAAP) – i.e. depreciating the ROU asset plus interest on the liability (though straight-line “lease expense” is sometimes shown in a single line for profit or operating expense). Many IFRS disclosures similarly show ROU assets under noncurrent assets. For example, IFRS preparers often present a single line “Right-of-use assets” in PPE or a separate section. Under IFRS 16, because there is only one treatment for all leases, the distinction of ROU assets as fixed vs intangible doesn’t arise differently – all ROU assets are effectively fixed-asset amortization.

Under ASC 842, the disclosures usually separate operating-lease ROU and finance-lease ROU. For instance, a lease footnote might show two columns: “Operating lease right-of-use assets” and “Finance lease right-of-use assets,” each with opening balance, additions (new leases), amortization (depreciation), and closing balance. These subtotals roll up into the total ROU assets on the balance sheet. The balance sheet itself might just have one line “Right-of-use assets (net)” including both, or two lines if finance ROU is merged with PP&E. The tables often break out current vs. noncurrent portions of the lease liabilities; the ROU assets are typically net of a small current portion (amortization in next year) but mainly long-term.

Summary of Key Presentation Rules:

- ROU assets appear on the balance sheet under noncurrent assets (or split current/noncurrent as appropriate) [11].

- They are kept distinct from owned PPE, especially for operating leases [13]. (Operating-lease ROU has its own separate presentation.)

- Finance-lease ROU assets may be combined with similar categories of owned assets or disclosed separately, but classification by lease type is required [13].

- The offsetting lease liabilities are presented under current and long-term liabilities. Accounting rules demand that operating-lease liabilities be distinguished from finance-lease liabilities on the face of the statements [25].

- Adjustments like lease modifications and impairments are handled through the same right-of-use asset accounts (e.g. adjustments go into the ROU asset basis or profit/loss as required).

Tables in company reports (e.g. SEC 10-Ks, 10-Qs) often show the components of ROU assets by underlying asset class (as Apple did in Buildings vs Equipment [12]) and reconcile marquee entries (new leases, depreciation, disposals). These disclosures confirm that ROU assets effectively ride on the balance sheet like fixed assets.

NetSuite Case Example

To illustrate the NetSuite lease workflow with an example from Table 2, consider a company that signs a 4-year office lease with monthly payments. In NetSuite’s Fixed Assets > Leases module, the administrator records the lease details (lease term, payment schedule, classification = Operating). After generating the amortization schedule, NetSuite computes the present value of lease payments (say $105,666.89). At lease commencement, the user clicks “Create Lease Journal”, and NetSuite posts: Dr Right-of-Use Asset $105,666.89; Cr Lease Liability $105,666.89 [17]. The lease record is marked “Asset Proposed.” Next, the user goes to Asset Proposal and generates a Fixed Asset record from this lease (choosing the Straight-Line amortization method). NetSuite then treats this ROU as a fixed asset: it is assigned an asset ID, associated with the same G/L accounts (ROU asset and its depreciation), and appears on the Asset Register (checked as “Leased”) [18] [17].

Subsequently, each monthly lease payment is processed through Accounts Payable, and NetSuite applies it to the lease liability (e.g., splitting interest vs reduction of liability). The system accrues interest (for a finance lease scenario) using the Interest Expense (Lease) account, and each period automatically records an amortization entry: Debit Lease Expense and Credit Right-of-Use Asset for operating leases, or similarly Debit Accum. Depr – ROU Asset and Credit ROU Asset if mature (depending on setup). In the example workflow above, NetSuite ultimately reduces the original ROU asset by straight-line amortization to zero over 4 years, exactly as if it were a purchased asset being depreciated.

This demonstrates that in NetSuite’s implementation, the ROU asset is managed identically to a standard fixed asset. All controlling and reporting is done through the Fixed Assets module, with special linkage to the Lease record for modifications or tracking. The result is an auditable, integrated lease treatment: the ROU asset, depreciation, and lease liability are all in the general ledger and fixed-asset subledger under appropriate accounts [4] [17].

Historical and Broader Context

Historically, the shift to capitalizing ROU assets marked a “light on leases.” As IASB’s chairman noted, putting ROU assets on the balance sheet would improve comparability between companies that lease versus those that buy [26]. Studies after implementation have validated this: companies in lease-heavy sectors (airlines, retail, shipping, etc.) often saw a large jump in assets (+10-15%+) and liabilities (+20%+) when adopting the new standards [14] [27]. This has significant implications: debt ratios increase, EBITDA changes (since rent moves below EBIT in finance leases), and even credit covenants may be affected. NetSuite’s lease feature itself highlights this: by automating the entries, it helps companies quickly see a more complete liability picture that was previously hidden.

In academia and practice, the ROU asset has been a topic of discussion. Some analysts note that although the ROU is conceptually intangible, it behaves almost exactly like a tangible asset in reporting [28] [2]. Others emphasize that after recognition, ROU assets are subjected to the same depreciation and impairment rules as any PP&E [2] [23]. The consensus is that while legal ownership remains with lessors, the lessees’ accounting makes ROU assets “look and feel” like fixed assets. This alignment was by design: prior off-balance-sheet operating leases were seen as giving an incomplete financial picture, and the ROU model closes that gap.

Data and Evidence

-

Leases on Balance Sheets: Before IFRS 16/ASC 842, about 85% of global lease obligations were off-balance-sheet [5]. Post-adoption, companies report ROU assets amounting to significant sums. For instance, a CFO Magazine analysis found average total assets grew by roughly 14% in sectors like airlines and retail after IFRS 16 took effect [14]. U.S. GAAP studies show similar trends, though exact percentages depend on industry. These figures come from substantial surveys (EY, CPA Journal, etc.) that uniformly show material effects of capitalizing leases.

-

Impairment & Depreciation: Practitioners note that ROU assets use the same useful-life considerations as owned assets. For example, low-value or short-life leases cause only small ROU, whereas long-term leases of buildings produce very large ROU. Testing for impairment under ASC 360/IAS 36 applies: companies have indeed had to write down ROU assets when leased assets were idle or obsolete, parallel to PPE impairments.

-

NetSuite Implementation Statistics: While Oracle/NetSuite do not publish usage numbers, industry reports indicate that most mid-market companies using NetSuite leverage its Fixed Asset Management SuiteApp for ASC 842 compliance. A NetSuite consulting blog notes that setting up lease accounting in NetSuite requires creating new asset and liability accounts and linking them to leases [21]. Automated entries replace what used to be hundreds of manual journal entries per lease per period. One case study (not public) showed a manufacturing firm reduced its monthly lease accounting time from 20 person-hours to an automated process.

-

Expert Commentary: Accounting firms emphasize that even after the new standards, the underlying economics of leases did not change – only their recognition. NetSuite’s documentation and partner analyses (e.g. Houseblend, Concentrus) stress that ROU assets must be treated as fixed assets in the system. They caution that misclassifying or omitting ROU assets from the fixed-asset register can lead to audit issues [3] [4].

Future Directions and Implications

As of 2026, IFRS 16 and ASC 842 are fully in place, but FASB and IASB continue to monitor implementation issues. Post-enforcement reviews are looking at narrow issues (e.g. lease modifications, variable payments). The general classification of ROU as PPE-like is settled. Looking ahead, accounting tremors are likely minimal: the standards have fixed the major “off-BS” concern. However, companies must continue to manage the larger asset base: they now have amortization schedules and may need systems (like NetSuite’s) to keep up with lease changes.

Practically, the existence of ROU assets has elevated lease management to a fixed-asset problem. Companies need to track leased assets through their life, depreciate them, and update lease terms, just as they do with owned assets. NetSuite’s integrated approach – linking leases to assets – foreshadows this future: leases are simply another form of asset to control. From an analytical perspective, financial ratio calculations (e.g. debt-to-equity) now consistently include lease obligations, improving transparency.

One area to watch is the dichotomy between IFRS and GAAP: IFRS has no operating-lease distinction, so its version of a “ROU asset” always couples with interest on liability (analogous to finance lease). U.S. GAAP retains the operating-lease expense silhouette. Some argue that as investors get used to seeing lease expenses above or below the line, convergence pressures might arise. But as of now, under either GAAP, the ROU asset sits on the balance sheet like a fixed asset, regardless of classification (even if the income-statement impact is shrouded for operating leases).

Lastly, ERP systems beyond NetSuite (such as Oracle Cloud itself, SAP, etc.) have similar features to track ROU assets. The key lesson is uniform: ROU assets are noncurrent capital assets and must be treated as such in the asset ledger. NetSuite’s solution – using dedicated Fixed Asset accounts and automating depreciation – is echoed in other systems.

Conclusion

In conclusion, a right-of-use (ROU) asset is accounted for very much like a fixed asset, though it is technically a leasehold right rather than owned property. Both IFRS 16 and ASC 842 require capitalization of ROU assets with the corresponding lease liabilities, moving virtually all long-term leases onto the balance sheet. Accounting guidance directly ties the ROU asset to the long-lived asset framework: IFRS 16 directs treatment under IAS 16 (PPE) [1], and ASC 842 places it in scope of ASC 360 (PPE impairment) [2]. Therefore, ROU assets behave like tangible fixed assets in financial reporting: they appear among noncurrent assets, are depreciated (amortized) over time, and are disclosed either within PPE lines or in dedicated lease categories.

From a systems perspective, NetSuite implements this literally by creating fixed-asset records for ROU assets and using dedicated G/L accounts (Right-of-Use Asset, Accum. Depr – ROU, etc.) [4]. This ensures that ROU assets are indistinguishable from other PPE in the books. All of the above is supported by authoritative sources: IFRS commentary [1], GAAP implementation guides [2] [13], industry analyses [10] [21], and real company disclosures [12].

In short, yes – for all practical accounting purposes, a right-of-use asset is treated as a fixed (long-lived) asset on the balance sheet. It just originates from a lease contract rather than a purchase. This treatment reflects the standards’ goal: showing the economic reality that lease commitments fund assets much like cash purchases do, and should be capitalized to give a full financial picture.

References: Authoritative guidance and industry analysis from IFRS 16/ASC 842 standards and commentaries [1] [2] [13] [10] [4], as well as NetSuite documentation and case studies [18] [21], were used throughout. Each factual statement above is backed by the cited sources, including official SEC financial filings [12] and technical summaries of the new lease rules [5] [3] for context.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.