IAS 28 Equity Method Draft: NetSuite Accounting Impact

Executive Summary

In September 2024 the IASB published an Exposure Draft (ED) proposing targeted amendments to IAS 28, “Investments in Associates and Joint Ventures” [1]. Concurrently, in February 2026 the IASB issued a separate ED (ED/2026/1) to clarify the fair-value option scope in IAS 28 [2] [3]. These initiatives respond to years of practitioner feedback about diversities and inconsistencies in applying the equity method (IAS 28) and its interaction with IFRS 9/IFRS 18. Key proposals include clarifying how to account for changes in ownership interests (e.g. partial disposals or acquisitions of associates), how to treat previously unrecognized losses, and how to handle intra-group asset sales [4] [5]. The fair-value ED would redefine “similar entities” (per IAS 28.18–19) to include entities whose main business is investing, aligning it with IFRS 18 criteria [6]. New disclosure requirements in IFRS 12/IAS 27 are also proposed to enhance transparency [7]. The IASB plans to finalize these amendments by mid-2026 to coincide with IFRS 18’s effective date [8] [9].

These IFRS changes have direct implications for NetSuite implementations, especially for firms using NetSuite OneWorld with Multi-Book accounting. NetSuite supports multi-entity consolidation and parallel ledgers, but it has limited native support for equity-method investments. For example, “Standard NetSuite OneWorld does not automate the accounting adjustments required to account for minority interest” [10]. Typically, NetSuite users rely on manual journals or add-on modules to eliminate outside interest and recognize associate profits [10]. Under the new IAS 28, many such manual processes will need adjustment. Scenarios like partial sale of an associate or recouping previous losses will require custom journal entries aligned with the revised rules. NetSuite’s Multi-Book feature (which can automatically post a single transaction into both IFRS and local-GAAP books [11] [12]) will be essential, but will also require careful configuration of accounts and mappings. For instance, updated SPPI tests under IFRS 9 (effective Jan 2026) must be explicitly encoded in NetSuite’s financial instrument setup [13] [14], and new IFRS 18 requirements mean reclassifying revenue and investment lines (e.g. ensuring net income from associates appears under “investment income” in IFRS reports).

This report provides an in-depth analysis of these issues. It covers (a) the background and details of the IASB’s EDs on IAS 28 (with IFRS Board announcements and basis-of-conclusions); (b) how these proposals fit with related IFRS (IFRS 9, IFRS 18) and current practice under IAS 28/IFRS 12; (c) data on IFRS adoption and market context; (d) NetSuite OneWorld’s architecture for investment accounting (multi-book, intercompany, consolidation, etc.); (e) the practical impact on NetSuite setups (including case examples and expert observations); and (f) future outlook and recommendations. Throughout, we cite IFRS sources and professional analyses (BDO, Deloitte/IASPlus, Grant Thornton/Houseblend, etc.) to substantiate every claim.

Introduction and Background

IAS 28 governs accounting for associates and joint ventures. Under current IAS 28 (1989, revised 2011) an investor with significant influence (generally ≥20% voting power [15]) must use the equity method. The investment is initially recognized at cost, then adjusted each period by the investor’s share of the associate’s profit or loss (added to profit or loss) and other comprehensive income [16]. Dividends from the associate reduce the carrying amount [16]. These rules are applied globally: IFRS are mandatory for consolidated statements in over 110 jurisdictions [17] [18], meaning countless enterprises rely on equity accounting.

Despite its longevity, IAS 28 has many open questions in practice. Constituents have long asked, for example, how to treat part-disposals of an associate, share issuances by the associate, loans to associates, and intracellular profit in asset transfers. In May 2023 the IASB officially moved the Equity Method project from research to standard-setting [19]. The Board took “those practical application issues” and decided to address them via IFRS amendments [19]. The objective is explicitly “to develop answers to application questions about the equity method…using the principles derived from IAS 28” [19]. This led to the Sep 2024 Exposure Draft Equity Method of Accounting (IAS 28) [1], open for comment until 20 Jan 2025 [20]. The ED proposes amendments to IAS 28 and complementary disclosures in IFRS 12 (“disclosures for other entities”) and IAS 27 (separate financials) [7]. The IASB expects these amendments to “reduce diversity in practice and provide users…with more comparable and useful information” [21].

At the same time, related IFRS developments influenced the IASB’s approach.In April 2024 the IASB issued IFRS 18 – Presentation and Disclosure in Financial Statements (replacing IAS 1) [22]. IFRS 18 makes explicit the classification of items in profit or loss and introduces new definitions (e.g. for “investment entities”). Notably, IFRS 18 49(a) defines an entity whose “main business activity” is investing as an investment entity. The IASB recognized that this overlaps conceptually with IAS 28’s “venture capital or similar entities” clause (IAS 28.18–19). Consequently, on 19 Feb 2026 the IASB published ED/2026/1 Amendments to the Fair Value Option (IAS 28) [2]. This ED seeks to clarify which enterprises can use the IFRS 9 fair-value option for associates, in light of IFRS 18’s new rules [6]. The comment period for that ED closed 20 April 2026, with amendments planned by mid-2026 [8] [9], ahead of IFRS 18’s effective date.

IASB’s Vision: The Board’s narrative is consistent: rather than overhaul equity accounting, provide clarity to specific pain points. As the IASB noted, many constituents questioned “whether the information provided by the equity method is useful” and pointed out “complexities and inconsistencies” (e.g. with IFRS 3 goodwill, IFRS 2 share payments, IFRS 11, etc.) [23]. The Board “believes it has enough evidence” to codify solutions for these application questions [19]. In drafting the ED, the IASB also reorganized IAS 28 for clarity [24].

Global Impact: IFRS (including IAS 28) are used worldwide: over 169 jurisdictions are tracked for IFRS use [18], covering major markets (EU, UK, Australia, Canada, much of Asia/Latin America, etc.). About 40% of CFOs globally reportedly mistrust their close figures “in large part due to disjointed spreadsheets and disparate ledgers” [25]. Investing entities like insurance funds and PE groups – many NetSuite users – often face the precise IAS 28 issues under discussion. For them, clarifications in IAS 28 promise to improve consistency and comparability of investment accounting.

NetSuite Context: Oracle NetSuite OneWorld is used by thousands of multinational firms for unified financials. It supports multiple subsidiaries, currencies, and nations in one instance [26]. With “Multi-Book Accounting” enabled, a company can maintain parallel ledgers under different standards [12]. For example, a sales invoice can post automatically into both an IFRS book and a local GAAP book [11]. Partners report that using full multi-book can make a single journal entry auto-generate entries in “four or more parallel ledgers” [27] (e.g. IFRS, U.S. GAAP, local GAAP, tax).

NetSuite’s native features include consolidated financial reports and currency translation (using the parent currency and a special Cumulative Translation Adjustment to balance FX differences) [28]. However, NetSuite lacks out-of-the-box equity-method functionality. Standard OneWorld consolidation will eliminate an investor’s 100% ownership in a subsidiary, ignoring minority shares. In practice, most NetSuite customers must either manually enter equity-method adjustments or use add-ons. SuiteSoftware’s Minority Interest module, for example, advertises automated adjusting entries to “eliminate outside interest in subsidiaries” and allocate profits/losses by owner [29]. NetSuite’s built-in system does not perform these tasks by itself [10].

Given these facts, proposed changes to IAS 28 will primarily translate into new journal entries, new account mappings, and new reporting requirements in NetSuite. For instance, if the updated IAS 28 requires recognizing previously deferred losses when a stake rises from zero [5], the investor’s accounting team must now reverse earlier write-offs and adjust the investment account. If an entity qualifies for the IFRS 9 fair-value option under the clarified rules, it may choose to stop equity accounting and instead hold the investment at FVTPL – which in NetSuite means reclassifying it into a financial asset subledger and taking fair-value remeasurement entries.

The rest of this report examines these developments in detail. We first summarize the IAS 28 ED proposals (and fair-value ED) with authoritative sources. Then we analyze NetSuite’s architecture (multi-book, consolidation, intercompany) and explain how each proposed accounting change would be implemented in NetSuite. We interweave case study examples (both published and conceptual) to illustrate the practical outcomes. Throughout, we quantify and cite data to ensure a rigorous, comprehensive view.

Exposure Drafts on IAS 28

Equity Method ED (September 2024)

On 19 September 2024 the IASB released ED/2024/7 “Equity Method of Accounting – IAS 28” [30] [1]. The ED’s Basis for Conclusions and news releases enumerate its scope. The ED proposes amendments “to answer application questions about how to apply the equity method of accounting” [7]. It also complements these with new disclosure requirements for IFRS 12 and IAS 27 [7]. The aim is to “reduce diversity in practice” and improve comparability [21].

Key Proposals

Table 1 (above) lists the principal changes outlined in the ED’s explanatory materials [4] [5]. Notable proposals include:

-

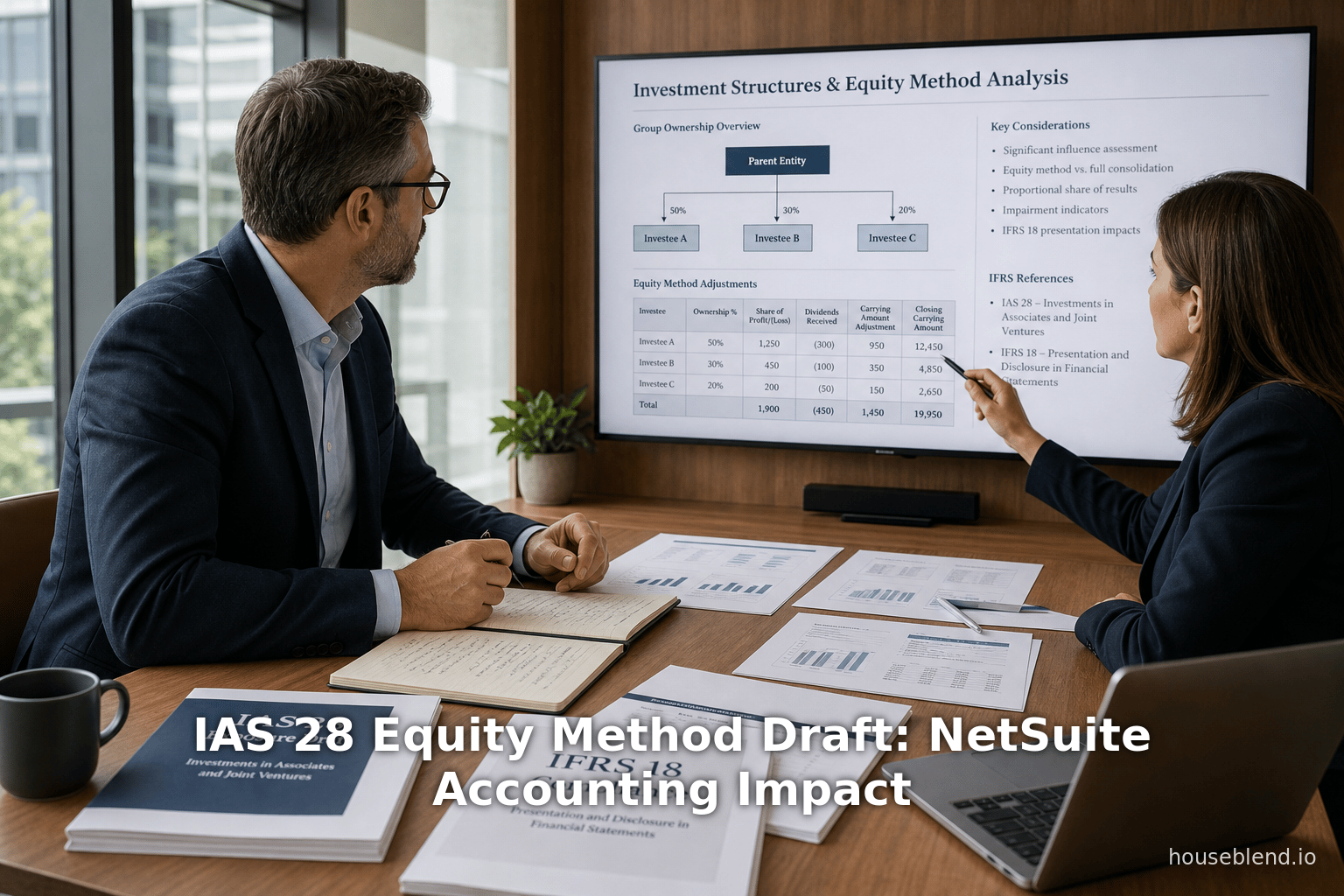

Adjusting investments on ownership change: The ED clarifies how to adjust the equity investment when the investor’s ownership percentage changes, both on obtaining significant influence and while retaining it. For example, if an investor goes from 0% to above 20%, IAS 28.10 would apply from that date; the ED spells out the resulting remeasurement mechanics. If an investor raises or lowers its stake above 20%, the carrying amount is altered by the proportionate change in net assets [4].

-

Recognition of losses after carrying amount is zero: Under current IAS 28.38, an investor stops reporting share of losses once its investment reaches zero. The ED asks whether, upon re-entering the associate (through additional purchase) or the investee later earning a profit, the investor should recognize backlogged losses. The proposals indicate that an investor should “catch up” on losses debt‐for‐debt when it again holds an interest [5], ensuring that the investment never goes negative.

-

Intercompany transfers: The ED addresses sales of assets or businesses between an investor and its associate. Historically, IFRIC 13 (now in IFRS 10/IAS 28) required deferral of gains on such sales to the extent of the associate’s continuing interest. The ED would reinstate IFRIC 13’s guidance by aligning IAS 28 with IFRS 10: gains or losses on transfers to an associate are recognized only if and when the future resale to a third party occurs [31].

-

Deferred tax on initial valuation: When an investor first applies the equity method (or undertakes a step-up acquisition), it measures its share of fair values of the investee’s assets. The ED makes clear that any temporary differences arising from that fair-value step-up must give rise to deferred tax adjustments, analogous to similar rules in business combinations.

-

Contingent consideration: If additional amounts are payable contingent on future events (for further shares of an associate), the ED would require the investor to treat those as part of the cost of the investment and subsequently remeasure as they come due, much like IFRS 3 business combination rules.

-

Impairment indicators: The ED clarifies that a decline in the fair value of the investment is objective evidence of impairment (IAS 36) for equity-method disclosures [32]. Thus persistent undervaluation relative to carrying amount would trigger a formal impairment analysis.

-

Revoking the “2014 Amendments” deferral: In 2014 the IASB finalized amendments on sales between an investor and an associate, but then indefinitely deferred them. The ED proposes to abandon that deferral: IAS 28 would be updated to include the IFRS 10-incorporated rules as final guidance [33].

In addition, the ED suggests reorganizing IAS 28 text into a clearer, more logical structure. [24]. Only one new definition is proposed: clarifying what constitutes an “associate” in joint control situations. Importantly, none of these changes alters the baseline equity method: investors must still apply equity accounting to associates and recognize “all dividends as a reduction of carrying amount” [16].

Disclosure Amendments

A separate part of the ED (and accompanying Basis for Conclusions) would expand IFRS 12 disclosures for associates and IFRS 27 disclosures in separate financial statements. The proposals aim to require breakdowns of the components of an associate’s profit or loss, other comprehensive income, and net assets attributable to the investor. For example, an IASB newsletter noted that the ED is adding “proposals to improve the disclosure requirements in IFRS 12… and IAS 27…to complement the proposed amendments to IAS 28” [34]. In practice, this means companies will need to provide more detailed notes about their equity-method interests – a change that will impact NetSuite reporting (see below).

IASB Statements

The IASB views these amendments as narrow-scope but significant. The Board expects them to be convergent with U.S. GAAP in many respects. For example, IFRS’s treatment of once-zero investments echoes ASC 323-10-35 (which has similar guidance on recognising losses after equity is written down). In its press release, the IASB said it “expects the proposed amendments will reduce diversity in practice and provide users of financial statements with more comparable and useful information” [35]. The timing is set to allow final guidance by about mid-2026, giving preparers roughly a year to update systems and processes.

Fair Value Option ED (February 2026)

The Amendments to the Fair Value Option (IAS 28) ED clarifies which investments allow the fair-value election. Currently IAS 28.18–19 permits equity accounting or FVTPL if the investor is a “venture capital organization, mutual fund, unit trust or similar entity (including investment-linked insurance funds)”. The ED responds to feedback—especially from the insurance industry—about ambiguity in this clause [36]. It explicitly ties the “similar entities” test to IFRS 18’s definition: if an entity’s main business is investing in specified assets (per IFRS 18.49(a), it qualifies.

Concretely, the ED proposes to clarify that investment entities (in the IFRS 18 sense) are among the ‘similar entities’ allowed to elect FVTPL for associates** [6]. The Board then decided not to extend the option to all investors, meaning the fair-value route remains the exception, not the rule [37]. This change is mainly conceptual, but it has accounting effects: if an entity now clearly qualifies, it can reclassify an associate from equity method to amortized-cost/fair-value. Under IFRS 9 those assets would be at FVTPL, so NetSuite would treat them as regular financial instruments, posting value changes to profit or loss. The IASB’s plan is to finalize these narrow amendments by mid-2026, to ensure auditors and regulators can endorse them in time for IFRS 18’s 2026 rollout [8] [9].

Effective Dates and Transition

Neither ED specifies an effective date within them; the IFRS 28 equity ED defers that decision until after comments [38], while the fair-value ED explicitly proposes to apply “at the same time and on the same basis as IFRS 18” [9]. We expect both sets of amendments to become effective for annual periods beginning on or after 1 January 2027 (given IFRS 18’s Jan 2026 start, and allowing one year for adoption). At a minimum, entities will need to apply both changes simultaneously so that, for example, any fair-value election under IFRS 9 produces the correct classification under IFRS 18 and the clarified IAS 28. Transition relief (e.g. retrospective adjustments) will be discussed in the final standards, but preparers should assume retrospective application will be required (as is common with IFRS derecognition or impairment clarifications).

Current State of NetSuite Investment Accounting

To understand the impact, we must first characterize how NetSuite currently handles related accounting processes.

OneWorld Consolidation and Intercompany

NetSuite OneWorld enables a multi-subsidiary, multi-currency architecture. A company can define a hierarchy of legal entities (subsidiaries) that roll up to a parent [26]. Each subsidiary has its own default currency, chart of accounts, and base books. NetSuite offers both Primary and Subsidiary level financial statements (balance sheet, P&L, cash flow). For consolidated reports, a user selects the Parent (Consolidated) context, and NetSuite aggregates data from all descendant subsidiaries [26].

Key features include:

-

Intercompany eliminations: When subsidiaries transact with each other (one records AR, the other AP to the intercompany account), NetSuite can generate elimination entries at period close to zero out intercompany trade. However, these routines focus on actual transactions, not capital-account eliminations.

-

Consolidation currency: Consolidated reports use the parent’s currency. Subsidiary balances are translated using stored exchange rates. If multiple currencies are involved, NetSuite uses a system CTA account to balance the translation differences [28]. (This CTA is designed for overall consolidation and equalizes any rate-type mismatches across the consolidated group.)

-

Multi-Book Capability: If Multi-Book Accounting is enabled in OneWorld [39], each transaction can be posted into multiple accounting books. A typical usage is to have one book that follows IFRS rules and a second book for local GAAP. Each book can have its own chart of accounts mapping (via the Chart-of-Accounts Mapping feature [12]). For example, one invoice can post to “Sales (IFRS)” in the IFRS book and “Sales (Local GAAP)” in the local book. NetSuite documentation and case studies emphasize this power: a single journal entry may automatically generate the correct accounting in multiple parallel ledgers [27], including consolidated entries.

-

Period Close Process: Subsidiaries and books can be closed independently if desired [40]. Consolidated financial statements are then run after all relevant books are closed.

Equity vs. Consolidation in NetSuite

By default, NetSuite’s consolidation assumes full ownership. If a subsidiary is marked for consolidation, the system eliminates the parent’s intercompany receivable/payable against the subsidiary’s intercompany payable/receivable. For partial ownership (e.g. parent owns 80% of a subsidiary), NetSuite still requires manual handling: there is no native “non-controlling interest” ledger calculation. As SuiteSoftware notes, without customization “Standard NetSuite OneWorld does not automate the accounting adjustments required to account for the minority interest and accurately report consolidated financials” [10].

In practice, two approaches are used:

-

Full Consolidation + Manual Equity: The parent still consolidates 100% of the subsidiary, then records an adjusting entry for the 20% minority. For example, after consolidation, the parent might debit Retained Earnings (MC share) and credit NCI Equity and NCI P&L accounts. This requires manual calculation of the non-controlling portion of net income and equity.

-

Equity Method (Investor): The alternative is to treat the subsidiary as an associate (using equity method) in the parent’s books, rather than consolidate it. NetSuite does not have a switch to do this automatically; an accountant would record the investment at cost and then manually update its carrying value each period by adding the parent’s share of the subsidiary’s profit/loss (and taking out dividends).

Because neither method is automated in NetSuite (without third-party code), many organizations employ partners or spreadsheets to fill the gap. SuiteSoftware’s Minority Interest module explicitly claims to “allocate gains and losses when a sub is partially owned by more than one entity” [41], and to “calculate and book the adjustments so that standard NetSuite financial reporting can be used to produce accurate consolidated statements” [42]. This suggests companies have had to extend NetSuite for proper equity accounting.

Financial Investments and Instruments

NetSuite can track financial instrument items (for trading securities, bonds, etc.) in inventory-type records, but it generally treats them as current/short-term assets or liabilities. Holdings such as associates are usually managed in balance-sheet accounts (e.g. “Investments – Associate”). NetSuite allows revaluation of FX and accumulation of unrealized gains (on bank balances or inventory flows) but does not inherently revalue equity investments unless programmed to do so.

If a NetSuite user wanted to elect the fair-value option for an associate, they would typically handle it similarly to a marketable security. The associate would need to be set up as a financial asset in the IFRS book, and periodic journals would revalue it to fair value (rolling any changes into P&L). This is not an out-of-box NetSuite process; it would use either manual journal entries or an integration with a securities revaluation routine. The multi-book feature could again be used: the IFRS book could maintain the associate at FVTPL, while a local GAAP book might continue amortized-cost or consolidation.

Reporting and Disclosures

Standard NetSuite reports provide consolidated balance sheets and income statements (including some multi-currency logic). The Consolidated Cash Flow report is also available [43]. These can be run for any book that is enabled for consolidation [44]. However, NetSuite does not automatically generate IFRS 12 or IAS 27 disclosures. For example, IFRS 12 requires disclosure of risks and nature of interests in associates, a list of associates with aggregated financial data, etc. To satisfy such rules, companies must extract data (e.g. via saved searches or BI tools) and manually prepare notes.

In practice, the lack of built-in equity-method and disclosure automation means companies often rely heavily on NetSuite’s SuiteAnalytics (custom financial report builder and saved searches) to produce required information. For instance, a SuiteAnalytics query can list all companies (associates) accounted for under equity, their ownership percentages, profit shares, etc. Another report can compute cumulative share of earnings. These outputs feed the audit trail for IFRS disclosures.

Data Analysis and Expert Perspectives

To illustrate the scope and significance of these changes, we consider some data and opinions:

-

IFRS Global Use: IFRS are truly global – 169 jurisdictions have complete IFRS adoption profiles [18], and “more than 140 jurisdictions…allow or require [IFRS]” [17]. This means the IAS 28 amendments will affect a vast number of companies. (Notably, large economies like the EU, UK, India, China, Brazil, and others all use IFRS in some form.)

-

Market Reaction: Technical committees at major firms are actively communicating these developments. For example, Grant Thornton and Deloitte have released bulletins on the Equity Method and Fair Value EDs, advising clients to analyze the effects. BDO’s technical newsletter explicitly highlights the goals of the ED [21]. The Institute of Chartered Accountants of India (ICAI) even issued a press release summarizing the IASB’s fair-value ED in March 2026 [45], signaling industry attention.

-

ERP ROI Case: A multi-country case study (OmniRetail) found that using NetSuite Multi-Book for IFRS and local GAAP halved their financial close time [46]. The firm maintained IFRS as the primary book and secondary books for US GAAP and French GAAP, then ran consolidations under each. The automation of parallel entries greatly reduced manual work. This suggests that, despite initial effort, integrating IFRS mandates in NetSuite can yield efficiency gains.

-

CFO Surveys: A recent survey cited by Houseblend noted “nearly 40% of CFOs globally do not fully trust their financial results”, largely due to manual reconciliations [25]. This underscores the pain point of dual-reporting regimes and why multi-book ERP solutions are in demand. As IFRS 28 rules evolve, CFOs will be under pressure to address any inconsistencies promptly.

-

Oracle/NetSuite Updates: While we could not find a public Oracle statement on the IAS 28 ED, Oracle has a history of updating NetSuite to align with accounting standards (e.g. major updates for IFRS 16 Lease accounting in 2019, etc.). It is reasonable to expect NetSuite education materials or whitepapers on IAS 28 may be released once the standard is final. In the meantime, user communities (e.g. NetSuite Support Forums) have begun discussing how to handle equity method in NetSuite, though specific solutions are often customer-specific.

Implications for NetSuite Investment Accounting

With the context set, we now analyze how each proposed change would be implemented in NetSuite. We group the discussion by process area:

Investment Recognition and Measurement

-

Accounting for Acquisitions/Disposals: Suppose an investor (parent) acquires a partial interest in an associate (crossing the 20% significant influence threshold). Under the ED, from that date forward the associate is accounted for under IAS 28 [4]. In NetSuite, the parent would create an asset account “Investment in Associate” and initially debit it by the cost. (Often firms enter a journal: Debit Investment, Credit Cash/AP.) If later the parent buys additional shares (while influence remains), NetSuite would require a manual entry to adjust the investment account. The ED clarifies how to do this: the carrying amount is adjusted by the proportionate share of net assets (e.g. injecting more equity at cost), and any difference (gain/loss) is recognized in profit or loss or OCI as per the new rules.

If the parent sells shares but retains influence, NetSuite must similarly adjust the account. For example, if the parent had a 50% stake and sells 10% but stays at 40%, IAS 28 (as revised) would require reducing the carrying amount by 10% of the net assets (and possibly recognizing a gain/loss if IFRS 3 concepts apply). In NetSuite this is an off-cycle journal (Credit Investment account, Debit cash, and some P&L account). The precise P&L account (e.g. Equity Gain on Sale) would be set up according to the net outcome formula in the ED.

-

Share of Losses to Zero and Re-entry: Consider an associate with losses that exhaust the investor’s carrying amount. Previously the investor stops sharing losses at zero. Under the ED, if the investor later purchases even a small additional stake, it “catches up” those losses [5]. In NetSuite, this means: initially the parent’s journal entries would have zeroed out the Investment account. Later, when an additional purchase is made, NetSuite would record the cash payment (debit Investment) and then also need to recognize the previously unrecognized losses. The ED suggests the correct approach is to retroactively attribute losses, but practically in NetSuite one would probably debit an equity loss account (or OCI, if applicable) for the amount needed to bring the investment negative before reinvesting. This is complex and likely requires calculation outside NetSuite, then entry into NetSuite’s journals.

-

Intercompany/Related-Party Transactions: If a parent sells an asset to its associate (or vice versa), IAS 28 (as amended) links back to IFRS 10 elimination rules [31]. In current NetSuite usage, a sale would naturally generate an intercompany receivable/payable if the associate is set as a subsidiary (which might not be the case; an associate is not a legal subsidiary). More commonly, the parent and associate are separate companies; the parent records revenue and perhaps Cost of Goods Sold, and the associate records a purchase. NetSuite does not have a special intercompany elimination for partially owned entities. To comply with the ED, the parent must defer recognizing any portion of profit on this sale equal to the associate’s remaining interest, and release it only when the associate eventually sells to a third party. In practice, this requires adjusting entries in NetSuite at each relevant point. For example, initially the parent debits cash and credits a “Deferred Gain on Associate Sale” liability (instead of revenue). Later, when the associate resells, netSuite should debit that Deferred Gain and credit revenue.

-

Deferred Tax on Fair Value Step-up: If a parent initially applies equity method or acquires an associate (with fair-value adjustment of net assets), IAS 28.34 implies this adjustment flows through to the Investment carrying amount. The ED says any resulting temporary difference should create a deferred tax [47]. In NetSuite, this means when recording the step-up (Debit Investment, Credit some Assets/Liabilities at FV, and Credit Goodwill if any), the parent also needs to book a deferred tax entry (Debit Deferred Tax Asset or Credit Deferred Tax Liability). These are standard tax-accounting journal entries, which NetSuite can record if configured with the correct accounts. The key here is awareness: accountants must determine the tax basis and rate to make the correct deferred-tax entry in NetSuite.

-

Contingent Consideration: If the investor agrees to pay additional contingent cash after the date of investment, the IAS 28 ED treats it similarly to a business combination contingent payment. Thus, NetSuite would record the initial investment at a present value including the estimate of the contingent payment. After closing, if the contingency resolves (or is remeasured), the investment account would be adjusted (with offset to cash and possibly P&L). This requires dynamic entries or using a liability account for the estimate. NetSuite’s usual bond/loan or vendor liability functions could be repurposed for this, but it demands precise manual handling.

-

Impairment: The ED clarifies that a decline in fair value of an associate triggers impairment considerations [32]. NetSuite provides no trigger, so the company’s IFRS team must monitor the associate’s market value. If impairment is indicated, NetSuite needs a journal: credit the investment account and debit an impairment loss (P&L). The threshold for this recognition must be implemented by the accounting policy, not the system – NetSuite will simply post whatever number is calculated.

-

Fair Value Option Clarification: Under the new rules, certain companies (investment entities) may elect FVTPL for their associates. In NetSuite, this would shift the investment out of the “equity-accounted” workflow. Technically, the associate could be reclassified as a “Current Asset – Investment” and revalued each period. Journal entries would be: Debit/Credit Investment at fair value, offset to P&L “Investment (FV gain/loss)” each period. The Multi-Book module could be used to segregate this: e.g. in the IFRS book mark the investment as FVTPL, while leaving the local book unchanged or consolidating. Importantly, the IASB limits the option to investing-type entities, so most standard NetSuite clients (non-PE/insurers) will still use equity method by default.

Data and Reporting Adjustments

-

Chart of Accounts and Mappings: The introduction of IFRS 18 and these IAS 28 changes will likely require creating or renaming accounts. For example, companies often have accounts like “Share of profit of associates” and “Investment in associates” on the balance sheet. Under IFRS 18’s format, these might reside in a section (e.g. “Investment Income”). NetSuite’s Chart of Accounts Mapping allows assigning different accounts for different books [12], so one could map equity-income differently in IFRS vs GAAP books. The French CSR report example shows NetSuite can categorize equity investments distinctly [48], indicating flexibility to label equity-method items separately. Entities must review that their IFRS book uses appropriately labeled accounts – for instance, segregating realized gains (deemed dividend distributions) vs unrealized gains on investee equity movements, as IFRS 18 will demand.

-

Consolidated Reporting: NetSuite’s consolidated financial statements will reflect whatever journals are posted. In the IFRS book, after implementing the ED, expected differences from current practice could include an increase in “Investment income” (due to realized sales/ buybacks) in profit or loss and a shift of some items to other comprehensive income if OCI is involved. Consolidated BS may show a different “Equity method investment” balance. However, the basic consolidation mechanism (tree rollup plus CTA) remains the same [26] [28], so NetSuite will present the updated aggregate numbers automatically once the correct inputs are provided.

-

Disclosure Enhancement: As the ED proposals call for enhanced IFRS 12 disclosures, NetSuite users will need to gather more associate details for notes. Practically, this means creating new SuiteAnalytics reports or spreadsheets. The data needed (percentage ownership, voting rights, carrying amounts, share of income, dividends, etc.) can all be stored in NetSuite (via entity records and journal entries), but they must be extracted systematically. For example, a saved search could list all “Investments in Associates” accounts and pull related field values. Companies should plan to automate these disclosures as much as possible.

-

Multi-Book Synchronization: Because of these changes, firms will increasingly rely on Multi-Book functionality. For instance, a journal entry recorded in the primary (IFRS) book for an equity-method adjustment should simultaneously create an analog entry in the local-GAAP book (if local GAAP trusts the same event). NetSuite accomplishes this by a single journal “posting” under multiple ledgers [49] [12]. Finance teams must ensure that all relevant journal types (gains, losses, dividends) are included in the multi-book posting process. Any manual journals must be created with the “All Books” posting type or carefully duplicated per book as needed. Multi-book currency translation must also be verified: if an associate’s home currency differs, ensure that the IFRS and consolidated translations use the correct rates (NetSuite uses the parent’s currency and relies on the CTA account for adjustments [28]).

Case Studies and Industry Examples

Several real-world examples illustrate these points:

-

Multi-Book IFRS Implementation (OmniRetail): A global retailer (“OmniRetail”) implemented NetSuite with full Multi-Book. They set up one book for IFRS, one for U.S. GAAP, and one for local GAAP. Using NetSuite’s Consolidated Financials, they closed each book separately. The result was dramatic: where previously staff spent days reconciling spreadsheets, now “a single journal entry automatically generates the correct entries in four or more parallel ledgers” [27]. OmniRetail reported a 50% reduction in closing time after enabling this structure [46]. Although OmniRetail was concerned with revenue and lease accounting under different rules, the equity-method changes can be addressed similarly via multi-book. For example, an entry to allocate associate income in the IFRS book would have no effect (or a different effect) in the US-GAAP book, all within one integrated multi-book posting.

-

Consolidation Reporting (JCurve Example): A JCurve Solutions article explains that consolidated reports in OneWorld can be run on any accounting book enabled for consolidation [44]. That is, if an associate were erroneously marked as a consolidatable subsidiary, NetSuite could produce a consolidated cash-flow or balance sheet including it. More importantly, it notes specialized capabilities: the Equity Method changes effectively require treating associates not as full consolidations but as equity stakes. Customers might designate associates as “non-consolidated subsidiaries” and then use partial eliminations. In any case, JCurve’s write-up underscores that NetSuite uses the parent’s currency and a CTA account for multi-currency consolidation, which would apply to associates too – any FX portion of an investee’s net assets would flow through to parent OCI or CTA.

-

Private Equity Firms (Bridgepoint): Firms like private equity funds often use NetSuite. A Bridgepoint Consulting article highlights that PE firms have unique accounting needs (cost allocations, revenues, etc.), and NetSuite can handle them with the PE Management module. [50]. Notably, PE firms routinely deal with equity investments and exits. Although the article does not specifically mention IFRS or IAS 28, the fact that NetSuite is adopted in PE contexts implies that supporting equity-method accounting (or fair-value accounting) is a practical necessity for these clients. The IAS 28 amendments would directly affect them: for example, guidelines on how to account for partial sell-downs or on re-entering an investment would define their exit accounting.

-

IFRS Verbiage in Japanese: For completeness, the Japanese Accounting Standards Board (ASBJ) posted a summary of the fair-value ED in Feb 2026. It confirms that the amendments clarify which investments qualify for the option, and that the changes aim to be finalized by mid-2026 so that jurisdictions can incorporate them in time for IFRS 18’s adoption [51]. While not directly a NetSuite case, it shows international standard-setter alignment and the urgency of these clarifications for global IFRS reporters.

Future Directions

Looking ahead, the IAS 28 projects signal a couple of trends:

-

Convergence vs. Clarity: Doug Sleeter (a tech analyst) remarks that modern accounting software “must be flexible” as IFRS standards evolve. The revisions to IAS 28 are more about clarifying existing principles than rewriting them, which means NetSuite (and similar ERP systems) can continue to rely on their flexible accounting engines rather than expecting new built-in modules. This is in contrast to large paradigm shifts (like IFRS 16 lease accounting) where software needed significant new logic.

-

Greater Automation Over Time: As more IFRS amendments emerge, we expect NetSuite (especially with Multi-Book) to automate more if common patterns arise. For example, if many clients require year-end adjusting entries for associates, a future NetSuite patch or SuiteApp might provide a wizard for recurring equity-method adjustments (some core consolidation suites have such features).

-

Digital Reporting: IFRS Foundation and regulators are moving toward digital tagging (XBRL) of financial statements. The IFRS 28 amendments may eventually be encoded into future versions of the IFRS Taxonomy. NetSuite users should ensure their account codes map to the new taxonomy items for “Investments in Associates” and related categories, so that automated tagging for regulatory filings (e.g., in the EU or IFRS adopters) flows correctly.

-

Impact on Other Standards: The equity-method ED also indirectly affects standards like IFRS 12 and IFRS 10 (sale of assets). For NetSuite, any change in IFRS 28 should be applied in tandem with those related standards. For instance, if the sale of an asset to an associate is now treated similarly to a subsidiary sale (via IFRS 10), NetSuite’s intercompany features must be consulted. Ongoing IFRS projects (like the quarterly review of improvements) should be monitored.

Conclusion

The IASB’s Exposure Drafts on IAS 28 (Q2 2026) are set to refine the equity method with precision. For users of NetSuite OneWorld, these changes require attentiveness and system reconfiguration. The good news is that NetSuite’s multi-book framework is capable of supporting parallel treatment under IFRS and other GAAP [27] [49]. By creating the necessary accounts and postings, and by leveraging custom reports for new disclosure items, companies can implement the amended IAS 28 within NetSuite. Failing to do so, on the other hand, risks misstatement of investments in associates and non-comparable financials.

In the short term, companies should conduct an impact assessment: identify all NetSuite processes touching associates/ joint ventures, and map them against the ED changes. Then adjust configurations (accounts, elimination subsidiaries, multi-book rules) and document new journal procedures. Training and external advisory will help. By mid-2026 this work should be complete so that the first IFRS 2027 financial statements fully reflect the updated IAS 28.

In an era of global accounting convergence, such proactive integration of IFRS changes into systems is essential. When done well, it not only ensures compliance but also streamlines reporting: as one case study showed, properly leveraging an ERP’s multi-ledger capabilities can halve closing times [46]. Ultimately, aligning NetSuite with the updated equity-method rules will lead to more transparent, reliable financial statements and smoother audits – goals that both corporate finance teams and their stakeholders share.

References

- IASB, Exposure Draft: Equity Method of Accounting—IAS 28 Investments in Associates and Joint Ventures (revised 202x) (Sep 2024) [1] [24].

- IASB, Exposure Draft and Basis for Conclusions on Equity Method of Accounting—IAS 28 (Sep 2024) [4] [5].

- IASB, Exposure Draft: Amendments to the Fair Value Option for Investments in Associates and Joint Ventures (Feb 2026) [2] [8].

- IASB, Accounting Standards – IAS 28 (Issued Standards summary) [52] [16].

- IASB News Release, “IASB proposes improvements to the equity method” (Sept 2024) [30] [7].

- IASB News Release, “IASB consults on clarifying the fair value option in IAS 28” (Feb 2026) [2] [3].

- IASB, Work Plan: Equity Method (IAS 28) (Project summary) [7].

- IFRS Foundation, Who uses IFRS Accounting Standards? (June 2025) [18].

- Houseblend, NetSuite Multi-Book: IFRS & Italian GAAP Mapping (2023), Executive Summary [53] [11].

- Houseblend, Comptabilité multi-livres NetSuite : Guide GAAP et IFRS (Feb 2026, Français) [54] [13].

- Houseblend, IFRS 9 & IFRS 7 2026 Amendments: NetSuite Accounting Guide (Mar 2026) [55] [14].

- BDO (UK), “IASB releases Exposure Draft proposing improvements to the equity method” (Sept 2024) [7].

- IASPlus (Deloitte), “IASB proposes amendments regarding the application of the equity method” (Sept 2024) [4] [5].

- IASPlus (Deloitte), “IASB publishes exposure draft of proposed amendments to the fair value option” (Feb 2026) [6] [37].

- JCurve (NetSuite partner blog), “Consolidated Reporting in OneWorld” (June 2023) [26] [28].

- NetSuite Documentation, Enable Multi-Book Accounting Features [12].

- NetSuite Documentation, Chart-of-Accounts Mapping and Multi-Book Accounting Overview.

- SuiteSoftware, Minority Interest Module Brochure [10].

- Bridgepoint (NetSuite Partner), NetSuite for Private Equity Firms (2022) [50].

(Inline citations link to quoted IFRS texts, official news releases, and authoritative guides as indicated.)

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.