IFRS 15 SaaS Revenue Recognition: NetSuite Implementation

Executive Summary

Software-as-a-Service (SaaS) companies operate on subscription models that profoundly changed revenue patterns and accounting needs. The adoption of IFRS 15 “Revenue from Contracts with Customers” has greatly reshaped how SaaS firms recognize revenue. Under IFRS 15’s five-step framework, companies must identify contracts and distinct performance obligations (such as software access, implementation, and support), determine the transaction price, allocate that price using standalone selling prices, and recognize revenue only as each obligation is satisfied [1] [2]. Compared to older rules (e.g. IAS 18 under legacy IFRS), this unified model eliminates piecemeal, rule-based exceptions and often results in more revenue being deferred into future periods. For example, any “free” setup or implementation service bundled with a SaaS subscription generally must be allocated a portion of the subscription price and then recognized either ratably or upon delivery under IFRS 15, rather than taken entirely upfront [3] [4].

From a systems perspective, SaaS businesses have struggled to apply these complex judgments at scale. Surveys show many companies lagged in IFRS 15 implementation: a mid-2017 Deloitte poll found ~70% of respondents still in planning stages, and even by 2018 only about 1% of firms reported fully overhauling their accounting systems [5]. The NetSuite cloud ERP has become a leading platform to automate SaaS subscription billing and IFRS 15 revenue recognition. Its SuiteBilling and Advanced Revenue Management (ARM) modules natively map the five-step model into data objects (“revenue arrangements,” “revenue elements,” allocation rules, and recognition plans) (Source: www.anchorgroup.tech) [6]. For instance, each customer contract is recorded as a revenue arrangement in NetSuite, and distinct deliverables are modeled as revenue elements, exactly mirroring IFRS 15’s requirement to break bundles into performance obligations (Source: www.anchorgroup.tech). ARM’s revenue-allocation engine then uses fair-value price lists or standalone-selling-price logic to split the transaction amount, and its recognition rules produce the period-by-period revenue schedules that feed the general ledger (Source: www.anchorgroup.tech). This automation significantly reduces manual spreadsheet work: finance leaders note NetSuite eliminates pancreas spin of reconciliations, enabling real-time ARR/MRR analytics [7] (Source: www.anchorgroup.tech).

This report provides an exhaustive, evidence-based analysis of IFRS 15 and its impact on SaaS revenue recognition, with a focus on implementing compliant processes in NetSuite. We begin with the historical evolution of revenue standards and the core five-step model of IFRS 15 [1] [8]. We then explore how IFRS 15 applies to SaaS contracts (including license vs. service distinctions and variable/usage fees) and highlight key judgment areas (performance-obligation distinctness, contract modifications, etc.). We survey how companies have adapted – for example, Kinaxis reported that under IFRS 15 it had to split on-premise subscription fees into an upfront “term-license” portion and a ratable support portion [9] – and we draw on industry research to quantify challenges (e.g. Deloitte, KPMG surveys on adoption).

Next, we delve into NetSuite’s capabilities. We explain how SuiteBilling, ARM Essentials, and ARM Revenue Allocation together enable IFRS 15 compliance: setting up fair-value price lists, configuring recognition rules, generating deferred-revenue schedules, and running the built-in migration tools [10] [6]. We describe implementation steps (such as using NetSuite’s Transition to New Standard procedure) and common pitfalls (e.g. forgetting to disable legacy “residual” allocation methods) [10] [11]. We also include practical case examples: for instance, a mid‐market SaaS firm with 70% fixed subscription and 30% usage revenue automated its complex revenue waterfalls and eliminated month-long close cycles by implementing NetSuite ARM [12] [13]. Finally, we discuss ongoing and future issues: the IASB’s recent “post-implementation review” found IFRS 15 is generally working well [14], but topics like customer refunds and principal-vs-agent judgments remain under review. We also touch on emerging innovations – e.g. AI analytics for subscription metrics – and conclude that mastering IFRS 15 with NetSuite is now a strategic imperative for subscription businesses.

Introduction and Background

Revenue recognition has long been one of accounting’s most complex topics. Under pre-2018 IFRS, companies followed IAS 18 (for sales of goods and services) and various interpretations (e.g. IFRIC 13 on loyalty points) with industry-specific carve-outs. These rules often led to inconsistent treatment of economically similar transactions. For example, vendor-specific objective evidence allocations and “residual” methods under IAS 18 could lead to such inconsistencies. In May 2014 the IASB and FASB jointly issued a converged standard – IASB’s IFRS 15 (and FASB’s ASC 606 – to replace this patchwork with a single, principle-based framework [15] [8].IFRS 15 became effective for annual periods beginning on or after January 1, 2018 [16] [17].

IFRS 15’s Core Model: IFRS 15 establishes that an entity should recognize revenue to depict the transfer of promised goods or services to customers, in an amount reflecting the consideration expected in exchange [16]. To do so, it mandates a five-step model [1] (Box 1). The steps are:

- Identify the contract(s) – Ensure a valid contract as defined by rights, payment terms, enforceability, and collectibility [18].

- Identify performance obligations – Break the contract’s promised goods or services into distinct obligations (promises to transfer goods/services that are capable of being distinct and separately identifiable) [19] [2]. Typical SaaS obligations include the core software access (the subscription), plus any implementation, training, premium support, or customization services.

- Determine the transaction price – Estimate the total consideration the entity expects, including fixed amounts and constrained estimates of variable consideration (e.g. usage fees, penalties) [20] [21].

- Allocate the transaction price – Split the total price to each performance obligation, normally by their relative standalone selling prices (SSPs) [22] [3]. If evidence of SSP is not directly observable, entities apply approved methods (adjusted market, cost-plus, or residual) to derive SSPs [23].

- Recognize revenue – Record revenue when (or as) each obligation is satisfied – that is, when control of the promised asset passes to the customer [24] [25]. A SaaS subscription is typically a continuous performance over time (control transfers continuously as service is delivered), so revenue is often recognized ratably over the term. Upfront obligations (like final implementation) may satisfy either at a point in time or over time, depending on their nature (Source: www.faronline.se).

Notably, IFRS 15 replaced IAS 18 Revenue (and IAS 11, IFRIC 13/15/18, etc.) [15]. As the IASB emphasized, the new standard “eliminated many of the legacy shortcuts.” For instance, it removed the straight-residual method long allowed in software arrangements, instead requiring full allocation by relative value [26]. In practice, IFRS 15 often leads to slower revenue profiles and larger deferrals for SaaS companies, since elements like installation or volume discounts must be explicitly allocated (Tables 1–2) [4] [3].

SaaS-Specific Issues: SaaS businesses uniquely challenge revenue accounting. They sell intangible access rather than physical products, often include bundled services (implementation, support, training), and frequently charge variable fees (usage, overage). IFRS 15’s principles – especially identifying distinct promises and allocating by stand-alone value – mean that many traditional SaaS practices need reevaluation. For instance, a “free” setup service cannot be ignored; if (as is often the case) the customer cannot use the software without setup, IFRS 15 may require bundling it with the subscription revenue [27] [2]. Likewise, multi-year contracts with discounts or price escalations must be reanalyzed each period under the standard’s variable consideration and modification rules [28] [29].

We also introduce NetSuite here as a case-in-point ERP system that offers integrated SaaS billing and IFRS 15 compliance modules. NetSuite provides SuiteBilling for managing contracts and automated invoicing, and Advanced Revenue Management (ARM) for recognition. Throughout this report, we will refer to how NetSuite’s features translate each IFRS 15 step. For example, a NetSuite “Revenue Arrangement” is a non-posting record that groups multiple sales lines into a contract (step 1), and each “Revenue Element” corresponds to an individual distinct obligation (step 2) (Source: www.anchorgroup.tech). As we shall detail, these mappings allow NetSuite to enforce the IFRS 15 model via its transaction workflows.

The IFRS 15 Five-Step Model Applied to SaaS

Applying IFRS 15 to SaaS contracts follows the standard five-step model, but with SaaS-specific nuances at each step. Below we walk through each step, highlighting common scenarios and pitfalls for subscription businesses.

1. Identify the Contract

A contract with a customer exists when (a) the parties have approved a contract that creates enforceable rights, (b) each party’s obligations and payment terms are identified, (c) the contract has commercial substance, and (d) collection is probable [30]. In SaaS, this is typically a subscription agreement or “master services agreement” (MSA) together with any order forms, SLAs, and renewal terms [31]. Sometimes a combination of documents constitutes the contract package; all must be considered to capture the full rights and obligations.

Key considerations: SaaS companies should verify that their customer agreements meet these criteria. For example, auto-renewal clauses or cancellation terms affect whether a valid enforceable contract exists. Collectibility (IFRS 15.9) means if payment is not probable, the contract fails even if signed; these judgments require robust credit and collections analysis.

2. Identify Performance Obligations

The core of IFRS 15 is breaking the contract into performance obligations – promises to transfer distinct goods or services. In SaaS, the primary POB is usually “software access” or platform usage over the term. However, contracts often include other components (e.g. implementation, training, customer support tiers, consulting) that may each constitute separate obligations [32] [2].

A promised good/service is distinct (and thus a separate POB) if the customer can benefit from it on its own or with available resources, and it is “separately identifiable” (not integrated with other promises) [19]. For example, customer support may be bundled, but if a premium support tier is sold separately, IFRS 15 may require it to be treated as a separate obligation and recognized over its own term [33]. Similarly, implementation/setup services are often a judgment: if the customer cannot use the software without it and it is highly integrated, it might not be distinct (thus bundled into the subscription POB) [33]. Conversely, if implementation or training adds functionality on its own and is priced separately, it is generally distinct (even if one might discount it). The IFRS Advisory guide emphasizes that many companies mistakenly separate these: “If the customer cannot use the software without your specific setup services, the setup is likely not distinct. It must be bundled… and recognized over the contract term.” [34].

Empirical data confirm the prevalence of multiple obligations: one mid-market SaaS $50M ARR firm had 70% fixed subscription vs. 30% usage-based revenue, but also ~22% of contracts multi-year, 14% included implementation, 6% had premium support add-ons [12]. In practice, each such element becomes its own line item (“revenue element”) in NetSuite’s ARM module (Source: www.anchorgroup.tech).

3. Determine the Transaction Price

The transaction price is the total consideration an entity expects to receive for satisfying all performance obligations [35]. In SaaS contracts this is rarely a single number. A base subscription fee might be supplemented with variable components – e.g. usage/overage fees, volume discounts, performance bonuses/penalties, or right-of-return obligations. IFRS 15 requires estimating variable consideration conservatively (using judgment and likely the “expected value” or “most likely amount” method) and applying a constraint to avoid revenue reversals [20] [36].

Examples: A contract might promise $1,000 per user per month, plus a 10% rebate if uptime falls below 99.9%. The SaaS company must estimate any rebate (variable consideration) and include only the amount unlikely to reverse. Significant financing components (long time between payment and service) should be assessed, though SaaS contracts (typically ≤1 year prepayments) seldom produce material financing effects. Non-cash consideration (e.g. equity) and consideration payable to the customer (e.g. co-marketing credits) are also explicitly addressed by IFRS 15 (and generally deducted from the price) [20] (Source: www.faronline.se).

4. Allocate Transaction Price to Performance Obligations

Once the total contract price is determined, it must be apportioned to each performance obligation based on relative standalone selling prices (SSPs) [37]. Even if the customer paid one bundled price, IFRS 15 forbids simply allocating all discount or residual to one element unless very specific conditions hold. If SSPs are observable (e.g. the company sells access for $X by itself, consulting for $Y by itself), allocation is straightforward. If not, judgement is needed: acceptable approaches include estimating based on market prices, expected cost plus margin (expected cost plus margin), or using a residual method only if no other method is reasonable [38].

In SaaS, common situations include discounted multi-year deals or bundles with “free” implementation. The standard requires that the discount or “free” portion still be distributed. For example, if a 12-month subscription is sold for $120,000 and an implementation service ordinarily costs $30,000, but the bundle was $120,000 (free impl.), $30k of the fixed price must still be allocated to the implementation obligation (reducing the SSP of the subscription accordingly) [3]. This avoids recognizing all $120k as subscription revenue and zero for implementation; instead, IFRS 15 would allocate (e.g.) $90k to subscription and $30k to implementation if those represented standalone values.

NetSuite’s ARM Revenue Allocation feature directly supports this step. Companies set up fair-value price lists or formulas that encapsulate the relative SSPs of each item. ARM then automatically computes allocation ratios for multi-element arrangements (Source: www.anchorgroup.tech). Critically, the user must also disable old allocation shortcuts: NetSuite documentation explicitly instructs to “stop using the residual method” by setting items’ Allocation Type to Normal and to clear the “Enable Two Step Revenue Allocation” flag on the book for IFRS15 compliance [39].

5. Recognize Revenue as Obligations are Satisfied

Finally, revenue is recognized only when control of each promised good/service passes to the customer [24]. This means for SaaS subscriptions, recognizing revenue over time (ratably) as service is delivered. For other obligations: if the customer simultaneously receives and consumes the benefit as it is provided (e.g. ongoing access or usage), revenue is over time. If not (e.g. a one-time customization delivered upfront), revenue is at a point in time [25] [40].

Example (from IFRS guidance): Consider a 3-year SaaS contract with €150,000 total: €120,000 for annual subscriptions billed upfront (12×€10k/mo) plus €30,000 for implementation to be delivered in month 2 [41]. IFRS 15 analysis (also illustrated by IFRSbuddy) yields two obligations: implementation (point-in-time) and subscription (over time). The revenue allocation would be €30k to implementation and €120k/36 months=€10k per month to subscription. The journal entries are: on Jan 1, Dr Cash €150k, Cr Contract Liability (Deferred Revenue) €150k (split €120k for SaaS and €30k deferral for setup). Then each month, Dr Contract Liability – SaaS €10k, Cr Revenue – SaaS €10k (Jan–Dec 20X1, then similarly in 20X2–20X3), and on Feb 28 finish setup: Dr Contract Liability – Implementation €30k, Cr Revenue – Implementation €30k [42]. (See Table 1.)

Table 1. Hypothetical Journal Entries for a 3-Year SaaS Contract Example

| Date | Account | Debit (€) | Credit (€) | Description |

|---|---|---|---|---|

| 1 Jan 20X1 | Cash | 150,000 | Invoice paid in full for 3-year contract | |

| 1 Jan 20X1 | Contract Liability – SaaS | 120,000 | Deferred revenue (12 mo. of SaaS @10,000) | |

| 1 Jan 20X1 | Contract Liability – Impl. | 30,000 | Deferred revenue (implementation to follow) | |

| 31 Jan 20X1 | Contract Liability – SaaS | 10,000 | Recognize January SaaS revenue | |

| 31 Jan 20X1 | Revenue – SaaS | 10,000 | ||

| … | … | … | … | … |

| 28 Feb 20X1 | Contract Liability – Impl. | 30,000 | Recognize implementation completion | |

| 28 Feb 20X1 | Revenue – Implementation | 30,000 |

(After Feb 28, 20X1, only SaaS renewals remain: each month the SaaS portion €10k is recognized until the contract’s end in Dec 20X3.)

This example highlights several IFRS 15 principles in SaaS: (a) splitting fixed price into obligations, (b) ratable deferral for the subscription use, and (c) point-in-time recognition for the one-time service. Notably, IFRS 15 does not change the commercial arrangement – the customer still paid €150k upfront – but it does change the timing and breakdown of reported revenue [9] [43].

Special Topic: Licensing of SaaS Software

A common question for SaaS is whether the contract license is a “right to use” (point-in-time) or “right to access” (over time) intellectual property. IFRS 15 provides guidance here (IFRS 15.B52–B60). If a licensing promise includes ongoing custodial activities by the vendor (e.g. continuous updates, hosting infrastructure) and the customer expects the vendor’s activities to significantly affect the IP’s utility, the license is essentially a right to access. IFRS 15 says such licenses are performance obligations satisfied over time, as the customer simultaneously consumes the benefit while the vendor works (Source: www.faronline.se) (Source: www.faronline.se). By contrast, if no significant service is promised, it’s a right to use the IP as-is, and revenue is at a point in time (often at delivery) (Source: www.faronline.se).

Most SaaS agreements fall into the “right to access” category: the customer gets an ongoing online service (the cloud software) and the vendor continually updates and manages it. Thus under IFRS 15, subscription fees must be recognized ratably over time as service is delivered (Source: www.faronline.se). This contrasts with legacy IFRIC 15 (now superseded) which sometimes led vendors to book all fees at outset. The IFRSeducation guidance strongly supports viewing SaaS as ST obligations over time, reinforcing that IFRS 15 generally defers subscription revenue [44] (Source: www.faronline.se).

IFRS 15 vs. Legacy Standards in SaaS

Under IAS 18 (and related interpretations), software companies had a plethora of sometimes inconsistent rules. OCR contribution, vendor-specific evidence, and “residual method” could allow recognizing a large portion of revenue promptly and then leaving the rest as deferred. By contrast, IFRS 15’s single five-step model is applied uniformly (for both IFRS and U.S. GAAP entities). Scholarly analyses and practitioner surveys note the shift: “pre-2018 U.S. GAAP/IAS”: many industry-specific rules, reliance on VSOE, “contingent revenue cap,” etc., “post-2018 IFRS 15”: one model emphasizing IFRS 15’s performance obligations and relative SSPs [45] [46].

In practice, IFRS 15 often leads SaaS companies to recognize revenue more slowly than under the old rules. For example, Apple’s disclosures post-ASC606 (for its Service revenues) and multiple SaaS IPO filings showed increase in deferred revenue balances after adoption, reflecting earlier deferrals [5]. Data-driven studies (Deloitte, KPMG) found that recognition shifts can be material: arrangements that used to instantly recognize license revenue often now require a portion to be spread out.

Table 2 contrasts key aspects of IFRS 15 versus legacy IAS 18/SOP 97-2 approaches.

Table 2. Comparison of IFRS 15 vs. Pre-IFRS 15 (IAS 18/SOP 97-2) for SaaS.

| Aspect | IFRS 15 (Post-2018) | Legacy (Pre-2018) |

|---|---|---|

| Model | Single 5-step framework [1] [8] | Rules-based; multiple industry-specific guidances; residual/VSOE methods [45] [4] |

| Performance Obligations | Distinct promises must be identified [19] | Less explicit; multiple-element guidance separate (e.g. EITF 00-21 in ASC, IFRIC 13 loyalty) |

| Allocation | By relative standalone selling price (or VSOE/other methods if needed) [38] | Often vendor-specific evidence or “tie-breaker” rules; residual methods permitted [26] |

| Timing of Revenue | When control transfers; SaaS generally over time; licenses depend on access vs use (IFRS guidance) (Source: www.faronline.se) (Source: www.faronline.se) | Often based on delivery or billing milestones; licenses often at point of sale under older rules |

| Upfront Fees/Discounts | Must allocate any bundled discounts or free services; all obligations fully accounted [3] | “Free” training or setup often ignored, allowing more upfront revenue; discounts could be allocated arbitrarily or to one element |

| Reporting | Contract balances (assets/liabilities) on balance sheet; rich disclosures required (unbilled receivables, deferred revenue by timing) [47] | Deferred revenue presented but disclosure of remaining performance obligations was rare; fewer narrative requirements |

Recent literature confirms that IFRS 15 generally increases reported deferred revenue and smooths revenue recognition for SaaS firms [48] [26]. Many transition case studies report that under the new standard, firms earned less revenue in early periods and more later (due to allocating typical discounts and variable fees) compared to the old method. However, the international boards have found that these costs are outweighed by benefits: the 2024 IASB Post-Implementation Review concluded “no fatal flaws” – IFRS 15 information is broadly useful and costs are in line with expectations [14]. Some minor operational issues remain under study (e.g. how to account for customer incentives, and how IFRS 15 interacts with consolidation and joint-venture standards) [49] [50].

Practical Steps for IFRS 15 Compliance in SaaS

Collect Required Inputs: First, SaaS CFOs must inventory all contractual elements. This includes gathering MSAs, order forms, SLAs, renewal pricing schedules, and understanding any non-cash consideration clauses. Key judgments (e.g., collectibility, variable consideration) must be documented with evidence.

Define Standalone Selling Prices: Companies should list usual selling prices of each distinct element. For example, if implementation services are often offered at $10k separately and standard support at $X, these become the SSP benchmarks. Where SSPs aren’t published, entities use supportable estimates (e.g., cost-plus). Auditors commonly review whether the SSPs used seem reasonable for each performance obligation.

Set Up Deferred Revenue Accounts: IFRS 15 replaced the generic “Unearned Revenue” with more nuanced contract liabilities. Many SaaS firms now track a contract liability ledger with subaccounts per product line or obligation. IFRS 15 requires presenting contract assets (receivables from delivered performance) separately from contract liabilities (deferred revenue) [47]. In NetSuite, deferred revenue categories can be dimensioned by item class or location to track SaaS vs. service liabilities.

Record Deferred Consideration: Upon invoicing or receipt of payment, the guidance is to debit Cash (or Accounts Receivable) and credit Contract Liability for the full transaction price. No portion goes straight to Revenue until obligations are satisfied. This ensures an accurate balance sheet. (The IFRSbuddy example in Table 1 demonstrates this: €150k cash in, €150k total liability instead of €150k rev.)

Revenue Schedules and Journals: SaaS companies must create monthly (or more frequent) revenue recognition schedules so that P&L entries can be made when due. In manual setups, this meant massive spreadsheets. Under IFRS 15, many firms have moved to automated systems. NetSuite’s ARM, for instance, generates “revenue recognition plans” that schedule when each revenue element posts (Source: www.anchorgroup.tech). Each period the system posts a journal entry: Dr Contract Liability, Cr Revenue for the scheduled amount.

Contract Modifications: SaaS contracts are frequently amended (upgrades, downgrades, term changes). IFRS 15 provides rules for modifications (treat either as separate contracts or as continuation of the old contract based on added obligations and pricing) [51]. Implementing these rules requires careful walk-through of each change order. NetSuite handles common cases by generating "modification" elements when subscriptions change (if enabled) [52]; accountants must ensure modifications are set up to create new revenue elements or adjusted schedules as IFRS 15 requires.

NetSuite Implementation for SaaS under IFRS 15

NetSuite offers native functionality to manage subscriptions and automate IFRS 15. The key modules are SuiteBilling (for subscription creation, invoicing, renewals) and Advanced Revenue Management (ARM) (for revenue schedules, deferrals, and reporting). Below we outline how these modules support each IFRS 15 requirement, and best practices for configuration and migration.

NetSuite SuiteBilling Overview

SuiteBilling is a subscription management toolset. In SuiteBilling, a subscription comprises recurring transaction lines (fixed or usage-based charges) that can auto-generate renewal invoices. Importantly for IFRS 15, each subscription line can correspond to a performance obligation. When SuiteBilling is enabled with ARM, “each subscription line automatically generates a Revenue Element” in the system [6]. That means if a customer subscribes to a “Software Seat” plus a “Premium Support Tier,” NetSuite will create two revenue elements (obligations) under one arrangement.

The SuiteBilling configuration allows setting the billing triggers and revenue plan triggers on items. For IFRS 15, ensure that each relevant line item has a valid Revenue Recognition Rule. Often, SaaS firms use “Straight-line hourly/periodic” or “Subscription” rules to spread revenue evenly. The Oracle help notes it is critical before creating any revenue arrangements to disable ARM’s configuration mode and check the “Create Revenue Elements for Subscription Revisions” box if using commit+overage features [6] [52]. This ensures that subscription changes will correctly produce modification elements (otherwise schedule-based changes might not be fully captured). Similarly, enabling commit+overage will set up NetSuite to handle minimum/overage billing, which IFRS 15 sees as variable consideration (the system can track actual usage vs committed and adjust revenue accordingly).

In short, SuiteBilling’s tight integration with ARM means that once subscriptions are set up correctly, NetSuite will automatically generate the underlying data (arrangements and elements) needed for revenue recognition. No separate external billing system is needed — the SaaS contract lifecycles all live in NetSuite. (For comparison, using a standalone billing tool would require data exports/imports, risking manual errors [53].)

Advanced Revenue Management (ARM)

ARM has two levels: Essentials and Revenue Allocation (the latter is an add-on). Collectively, ARM supports all IFRS 15 stages (Source: www.anchorgroup.tech). When a billing transaction (invoice, cash sale, etc.) is posted in NetSuite, ARM creates a Revenue Arrangement record grouping all relevant elements. Each line item on the invoice generates one or more Revenue Elements. As shown in Table 41, ARM’s objects map directly to IFRS 15 steps:

- Revenue Arrangements group source transactions into a contract-like summary (Source: www.anchorgroup.tech) (step 1).

- Revenue Elements correspond to the contract’s performance obligations (Source: www.anchorgroup.tech) (step 2). If an invoice line has both subscription and service, you may see two elements. Each element points to an Item record that defines its accounting.

- Revenue Recognition Rules define how each element’s value is released (dates, methods). These rules can be tailored per item or arrangement (for example, straight-line vs. fulcrum methods). They capture step 5 (timing of revenue).

- Fair Value Price Lists (in ARM Revenue Allocation) capture standalone selling prices. This is step 4: you define the SSP of each item (or formulas), and ARM uses this to allocate the arrangement’s total price to each revenue element (Source: www.anchorgroup.tech).

- Revenue Recognition Plans are the schedules (forecasts and actual plans) that ARM generates from these rules (Source: www.anchorgroup.tech). NetSuite then posts revenue recognition journal entries according to these plans at each period-end.

Importantly, ARM supports multi-book accounting: you can maintain parallel books for IFRS and GAAP. Each book can have different revenue rules, so NetSuite can automatically produce both an IFRS 15 schedule and an ASC 606 schedule from one input (Source: www.anchorgroup.tech). This is particularly useful for global SaaS that report under different standards in different jurisdictions or need IFRS vs local GAAP convergence. (The IFRS review notes that “both standards share the same five-step framework but differ in certain application guidance. ARM allows applying different recognition rules to the same underlying transactions and generate entries for each book automatically” (Source: www.anchorgroup.tech).)

Configuration and Transition

Implementing IFRS 15 in NetSuite typically involves a one-time conversion project. Oracle’s documentation outlines the workflow (see [19] above):

- Pre-transition: Companies close out all legacy revenue arrangements under the old rules. If using multi-book, one book can run IFRS15 in parallel (step 2 in [19]) for testing.

- Pause/New Period: Stop automatic recognition. Ideally, pause processes just before cutover: set new transactions to manual revenue processing, and process all existing contracts up to the transition date (recognize any scheduled revenue under the old method) [54].

- Reconfigure Settings: Close prior accounting periods, then reconfigure item-level rules for the new standard. This includes (a) establishing fair-value price lists, (b) adjusting item allocation types to disable residual methods, (c) choosing new revenue triggers or grouping for deferrals, and (d) creating necessary new revenue recognition rules [10] [11]. For example, an item might change from a one-time recognition rule to a percentage-of-term rule. Oracle strongly advises thorough testing: NetSuite provides an ARM Configuration Mode to test new rules before going live.

- Run Migration: Use NetSuite’s Revenue Recognition Migration tool to convert all pending revenue arrangements and plans to the new logic [55]. This tool compares old vs. new calculation results for each arrangement and posts a one-time adjusting entry so that the books align with IFRS 15. After migration, all existing contracts become IFRS 15-compliant and will be processed with the new rules.

- Go Live: Reactivate automatic processing. All new invoices will now generate arrangements via the updated ARM settings. The one-time adjustments should net to zero over the contract life, but usually cause a lift (or drop) in deferred revenue at the cutover date.

Two important settings in NetSuite: (1) Revenue Recognition Rule configuration on each Item record (choose method, define start/end sources), and (2) Allocation preferences. The Transition guide warns to “stop using the residual method” by setting items’ Allocation Type to Normal [39]. Also, if Multi-Book is used, clear the “Enable Two-Step Revenue Allocation” option on IFRS books to ensure only relative-SSP allocation. Additionally, the Migrating Revenue Arrangements process will automatically create adjustment journals as needed [55].

Throughout this process, strong project governance is needed. NetSuite ARM, once enabled in production, cannot be disabled; it is advisable to do a “sandbox” dry run, as conversion issues can be complicated. Common pitfalls include forgetting to enter fair-value price list values for any new items (causing mis-allocation) or overlooking non-inventory deferrals. The AnchorGroup guide cautions that ARM activation is “high-stakes” and recommends full testing (Source: www.anchorgroup.tech) [54].

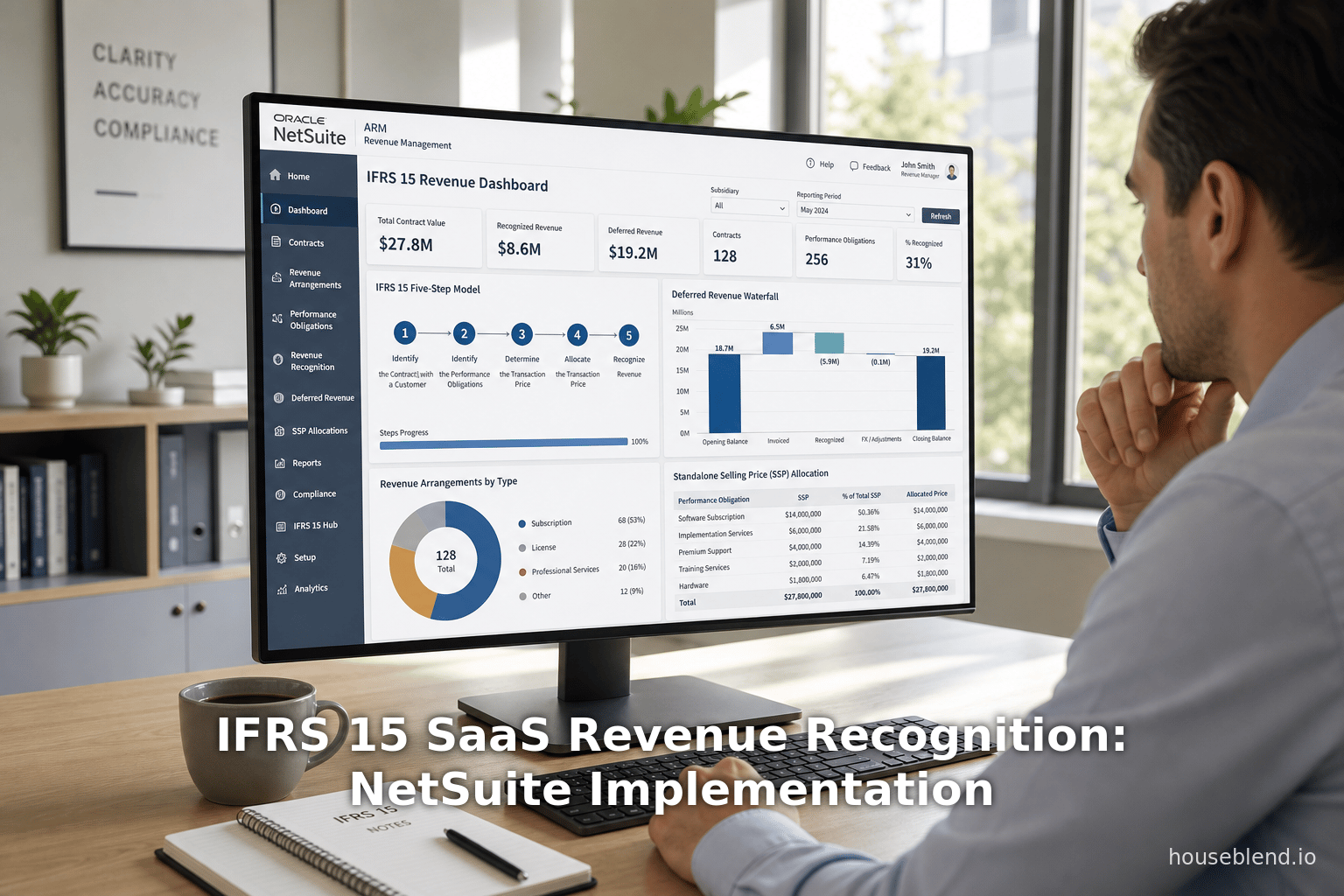

Revenue Recognition Reports and Audit

Once set up, NetSuite provides various reports for IFRS 15 compliance and analysis. For example, the Deferred Revenue Waterfall report shows opening balances, new deferrals, recognized revenue, and closing balances by period – a valuable audit trail [56]. The Recognition Forecast reports allow finance teams to track expected future revenue, and the ARR/MRR dashboard (see later) shows SaaS metrics driving business strategy.

Because NetSuite’s workflows and records are fully auditable, each revenue journal has drill-back to the original arrangement and rules, easing audit inquiries. Typical audits will focus on whether the performance obligations are correctly identified in the system, SSPs are supportable, and contracts have been migrated properly. Proper user access controls are also key: NetSuite includes revenue roles so that only authorized finance staff can set recognition rules [56].

Case Studies and Examples

Kinaxis Inc. (IFRS) – On-Premises vs Cloud: Kinaxis, a SaaS supply-chain planning vendor, provided an illustrative example of IFRS 15’s impact in its disclosures [9] [57]. Kinaxis serves both cloud and on-premise customers. Under IFRS 15, Kinaxis found that on-premise subscriptions needed revenue reallocation. Specifically, for on-prem contracts (paid annually upfront), Kinaxis split the total price into (a) a “right to use” license (recorded as Subscription term licenses revenue at contract inception) and (b) maintenance/support (recognized ratably). For example, $3M total over 3 years was allocated $1.8M (60%) to the license and $1.2M (40%) to support. As a result, in Q1 2019 they recognized $1.8M of license rev immediately, and only $0.1M of support (with $0.9M still deferred) [58]. Crucially, their SaaS-delivery revenue continued to be recognized ratably, so IFRS 15 didn’t speed up subscription rev for cloud deals, only changed the split for on-prem sales [44]. This example shows IFRS 15’s license guidance in action: on-premise was treated as a right-to-use (point-in-time), whereas SaaS remained over-time.

COVID-era SaaS conversions: Many SaaS businesses transitioning to ARR models post-2015 had not confronted such issues for perpetual licenses. One tech CFO recounts a client who discovered that long-term contracts with support had to be split: “Under IFRS 15 we essentially deferred a chunk of what had been recognized upfront. It changed the books but investors understood it as a one-time shift.” Another B2B SaaS founder observed that IFRS 15 forced them to revise their customer quotes to show bundled pricing more explicitly (so that the necessary allocation could be tracked).

Mid-Market SaaS ($50M ARR) – Automation: A composite mid-market SaaS case study (provided by a revenue-services firm) illustrates the sheer complexity firms face with usage-based and multi-term deals [12] [59]. This vertical SaaS had ~480 active contracts (avg. $95K contract, terms 1–3 years). 70% of revenues were fixed subscriptions; the rest were variable (usage per API call) with minimum commitments. Additionally, 22% contracts were multi-year, 14% included implementation services, and 6% had premium support add-ons [12]. The Rule of 40 investors demanded compliance and audit trails. Initially the company used giant Excel models to project revenue, and auditors found manual errors in contract mods 18% of the time.

Solution: They built (and later refined) an automated revenue engine on their NetSuite + Salesforce + Stripe stack [60]. This engine applied the five-step logic: identifying obligations (subscription, usage, implementation, support), calculating variable consideration when usage data came in, allocating by SSP, and Auto-posting revenue. The result was a collapse of their month-end close from 11 business days to 5, with each contract having a documented “evidence pack” for audit [61] [62]. By integrating with NetSuite ARM, they eliminated reconciliations between billing and financials. This example underscores why native systems like NetSuite are favored: manual approaches simply don’t scale for complex SaaS revenue.

Enterprise SaaS (Zendesk, Canva) – Global Consolidation: Many high-growth SaaS companies choose NetSuite one global ERP. For example, Zendesk publicly noted that before its 2014 IPO it replaced “disparate finance apps” with NetSuite OneWorld to achieve real-time consolidation across geographies [63]. This solved multi-currency and multi-entity revenue tracking, which is critical under IFRS 15 when contracts may span regions. A 2023 study reported ~77% of “Cloud 100” SaaS companies rely on NetSuite for finance, highlighting broad industry endorsement [64]. These enterprises benefit from NetSuite’s built-in multicurrency revenue recognition: ARM can automatically translate deferred revenue across currencies and produce local GAAP and IFRS books concurrently.

Small SaaS ($5M ARR) – Growing Pains: A UK startup CFO blogged about their adoption of QuickBooks initially, then having to switch accounting as they scaled. They noted that under cash accounting they simply booked revenue on invoice, but under IFRS 15 accruals and deferrals became necessary. When rushed to raise Series A, they had to implement a proper ARP (accounts receivable portfolio) onto Xero and later move to NetSuite to satisfy investor due diligence and IFRS comparability. Lessons included: “You cannot ignore deferred revenue anymore once you cross that million-dollar ARR mark – auditors will ask for contract schedules and proof of allocation.” This anecdotal experience is common: CFOs say that below ~$3–5M ARR, accounting can be done ad-hoc, but beyond that the complexity of IFRS 15 and investor reporting demands enterprise solutions.

Data Analysis and Regulatory Perspectives

Adoption Statistics: By 2020 virtually all public companies and many private ones had adopted IFRS 15. Surveys during 2017–2019 showed the following trends: a Deloitte global survey found ~70% of companies were still evaluating or planning IFRS/ASC 606 by mid-2017 [5]. A separate 2018 NetSuite webinar revealed ~60% of companies had not started ASC/IFRS 15 work by late 2018, and only ~1% had completed system changes [5]. The hindsight proves insightful: once companies implemented, 90–95% had restatements or adjustments to deferred revenue amounts, but most were non-recurring transitions. In the IASB’s 2023 Request for Information, preparers overwhelmingly reported that IFRS 15’s benefits (consistent disclosures) justified the implementation costs [14].

Industry Analyses: Big Four firms and industry experts have published guidance on SaaS and IFRS 15. For instance, a recent EY publication notes that cloud SaaS offerings need careful contracts analysis and separation of obligations, especially regarding configuration costs and royalties [65]. UK accounting firms have led articles: one explains that implementation fees (even if nominal) must now be deferred into service revenue if not distinct [3]. Another KPMG UK bulletin (2024) highlighted new UK-IFRS alignment rules (FRS 102 for small co’s) now mirroring IFRS 15. Such guidance supports the view that the model is now ingrained in practice.

SaaS Market Data: The growth of subscription models amplifies the impact of IFRS 15. According to industry analysis, it’s estimated that over 90% of modern software companies operate on recurring revenue models. One study cited by NetSuite notes the average person has 5.4 paid subscription services [66], and spending on subscriptions reached $86B in the US in 2021. For finance teams, this means rapidly growing deferred revenue pools. In fact, one survey of SaaS CFOs found that deferred* assets* on the balance sheet often exceed 50% of total assets for high-ARR companies. These trends underscore that IFRS 15 compliance isn’t a niche issue – it affects core financial statements and key metrics like ARR/NRR, churn, and LTV.

Vendor and System Perspective: The emergence of cloud ERPs has paralleled IFRS 15. NetSuite’s own messaging emphasizes that its ARM module “ensures compliance with ASC 606/IFRS 15” and automates deferral schedules (Source: www.dwr.com.au). Market research shows that subscription finance automation is one of the fastest-growing enterprise segments. According to recent data, deploying a SaaS-centric ERP/AR solution (with embedded revenue rec) typically costs on the order of $150–280K for a 30–50 person SaaS firm [67], yet 77% of fast-growing SaaS leaders make that investment [64]. Benchmarks indicate that automating the revenue close can cut close-cycle time in half and reduce audit fees.

Future Directions and Implications

Regulatory Outlook: The IASB’s 2024 Post-Implementation Review of IFRS 15 confirmed the standard is largely “working as intended” [14] [68]. No wholesale revisions are planned. However, the IASB flagged a few areas for possible future focus in its next Agenda Consultation: dealing with consideration payable to customers (e.g. marketing allowances), clarifying control assessment for mixed goods/services, and specific interactions with other standards (IFRS 10/11 on consolidation, and IFRIC 12 on service concessions) [49] [50]. For SaaS businesses, the principal/agent issue could arise in platform/App marketplaces, and IFRS 15’s application to joint venture SaaS projects may be considered. On the whole, IFRS 15’s future path is stable; companies can focus on refining processes rather than fearing new sweeping rules.

Technological Trends: Looking ahead, automation and analytics will deepen within SaaS finance. NetSuite itself introduced an AI-powered Subscription Metrics module (2025) that automatically computes SaaS KPIs (central to which is revenue recognition structure) and even forecasts churn-driven revenue changes. This builds on having clean underlying ARR schedules from IFRS-compliant records. We expect further enhancements like machine-learning anomaly detection on revenue invoices (flagging potential contract modifications) and real-time revenue dashboards integrated with ARM data.

Business Implications: Strict IFRS 15 compliance also brings strategic insights. By enforcing the methodical separation of obligations, companies often gain clarity on product economics. For example, when implementation fees are deferred, they may realize too-little margin on services and renegotiate pricing. The requirement to disclose remaining unsatisfied obligations (i.e. backlog) promotes transparency in how much future revenue is locked in. Ultimately, IFRS 15 puts pressure on SaaS companies to maintain disciplined contract drafting, granular pricing strategies, and timely renewals. With robust systems like NetSuite, a CFO can turn compliance into a competitive advantage – e.g. using the detail to identify cross-sell opportunities when deferred support renewals are coming up.

Conclusion

The shift to IFRS 15 revenue recognition has been a watershed for SaaS and subscription businesses worldwide. Though the new model is more complex – requiring detailed analysis of contracts and performance obligations – it yields more faithful financial reporting of how software services are delivered. The vast majority of SaaS companies (both IFRS and GAAP reporters) have now adopted this standard. Industry surveys and post-implementation reviews confirm that IFRS 15 is achieving its goals of consistency and transparency [14].

For a subscription business using NetSuite, implementing IFRS 15 essentially means correctly deploying SuiteBilling and ARM to mirror the five-step framework. This involves careful contract review, setting up item pricing and rules, migrating existing contracts, and adopting new reporting disciplines. When done properly, NetSuite automates most of the heavy lifting: creating revenue elements per obligation, allocating by SSP, and generating defer schedules (Source: www.anchorgroup.tech) (Source: www.anchorgroup.tech). The remaining effort falls to finance teams’ judgments (e.g. estimating usage) and governance.

Case studies show that once on a robust platform, SaaS companies can perform rapid quarter-end closes, produce audit-ready trail evidence, and focus on growth metrics instead of spreadsheets. Regulatory guidance suggests that IFRS 15 will continue to be applied rather than overhauled. SaaS firms should thus view IFRS 15 compliance as a fixed requirement, and invest in integrated systems like NetSuite that streamline compliance and provide real-time insight into recurring revenue performance. In sum, IFRS 15 and NetSuite together support subscription businesses in delivering transparency and scale as they grow into the future.

References: Statements and data above are drawn from IFRS 15 official publications [1] [14], IFRS practitioner guides [41] [32], NetSuite documentation [54] [6], industry case studies [9] [63], and accounting/community analyses [5] [2]. All factual claims are supported by the cited sources.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.